The Dollar as an International Currency: Towards a New Bretton Woods?

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Interdisciplinary Journal of Research in Business ISSN: 2046-7141

Vol. 2, Issue. 5, (pp.01- 06) | 2012

The Dollar as an International Currency: Towards a New Bretton Woods?

Marco Mele

Luspio University

marco.mele@luspio.it

ABSTRACT

For over half a century the U.S. dollar has been the currency par excellence as it was the main vehicle for

business transactions and financial affairs, both private and official level. The undisputed pre-eminence of the

U.S. dollar has been the hallmark of international monetary relations throughout the second half of the

twentieth century. The centrality of the dollar has survived unscathed the numerous imbalances and tensions

that, in the past decades have marked the economic environment, financial and political world, and all the

inevitable consequences occasioned in the monetary environment. The U.S. and European crisis, however, may

have initiated a process of profound transformation of the international monetary system, characterized by the

loss of the dollar as an international currency. The emergence of a credible alternative to the dollar in the role

of an international currency, that these were the first of the sovereign debt crisis in Europe, are the factors

likely to undermine the undisputed leadership of the dollar but also the reasons that make rethink the

impossibility of a new monetary order the name Bretton Woods 2.

1. THE DOLLAR IN THE HISTORY OF THE BRETTON WOODS

The Bretton Woods system was the regulation of international trade between the end of World War II and the

beginning of the seventies of the last century. It owes its name to the locality of the United States (Bretton

Woods, New Hampshire), where, in July 1944, there was a Monetary and Financial Conference, which was

attended by 44 countries, which was intended to govern future relations you type the international economic and

financial, in order to prevent the 'world economy to return to the origins of world War II. These difficulties

depended largely on the lack of cooperation among States, the widespread adoption of protectionist policies and

competitive devaluations of the exchange rate: these were certainly the main factors that led to World War II.

The agreements were ratified in December 1945 in Washington by the majority of participating countries. Such

agreements, abandoned the idea to create an international unit of account, gave the U.S. dollar a central role in

the new system of international exchange rates. The centrality of the dollar was due to the fact that it was the

only currency convertible in gold at a fixed parity ($ 35 per ounce of gold). For foreigners the gold

convertibility of dollars held was granted only to the central banks of the member countries participating in the

Bretton Woods system. In the new system, the exchange rate between the dollar and other currencies, and

therefore all the exchange rates between the participating currencies, were regulated by a system of fixed

exchange rates, consisting of a central rate around which would be allowed little jitter (initially +1% and -1%

compared to the rate) of the exchange rate.

In this contest, the return to convertibility of currencies general, at the end of 1958, and the subsequent entry

into operation of the monetary system created at Bretton Woods, marked the beginning of the rise of the dollar

as the key currency in international transactions officers.

If you choose to define their own currency equal in terms of the U.S. dollar, the member countries of the IMF

agreed, in fact, the role of the U.S. currency unit of account of the Fund.

Assuming, in the transactions on the foreign exchange market spot, oscillations did not exceed 1% margins

above and below parity with the dollar, and enshrining, thus, the obligation for the central banks of Member

States of the IMF, to intervene in the foreign exchange market to buy or sell its currency whenever its listing had

differed from that margin, was given to the dollar the role “anchor for pegging” for the international monetary

system.

Having defined the parity of their currencies in terms of gold, and committing to sell gold to central banks for

dollars at the fixed price of $ 35 per ounce, the United States became the only country that could not intervene

in the foreign exchange market, becoming the role of country n. Therefore, the U.S. gave up to pursue a policy

1Interdisciplinary Journal of Research in Business ISSN: 2046-7141

Vol. 2, Issue. 5, (pp.01- 06) | 2012

of exchange accepting, in fact, a passive role, and allowing, in this way, with other countries to realize their

exchange rate policies in a non-confrontational way. This circumstance contributed to the emergence of the

dollar as the intervention currency, n -1 used to stabilize exchange rates.

Finally, the use of the U.S. dollar for purposes of intervention - such as “intervention currency” - favored its use

for backup purposes - as a reserve currency. This outcome was favored by certain characteristics of the dollar -

its high degree of liquidity (ie, its ability to be converted quickly and at low cost in another currency), the

stability of its value, its sufficient rate of return (ie, the attractive investment opportunities offered by financial

markets USA) - which had contributed to the emergence of the U.S. dollar as the basis of values at the level of

private international transactions.

However, during the sixties, for a variety of reasons (including the creeping inflation that made it convenient

convertibility of dollars into gold, the shortage of dollars as a reserve currency in the face of the great

development of international trade, the growing inadequacy, compared needs, the American reserves of gold,

resizing U.S. hegemony), the Bretton Woods system began to disintegrate, and the end was sealed in August

1971 by the unilateral declaration of inconvertibility of the dollar into gold U.S. President Nixon, who, followed

by the devaluation of the dollar, opened the way to the establishment in 1973 of the current regime to floating

exchange rates.

The definitive end of the system of exchange rate adjustment, which was centered on the monetary regime

created at Bretton Woods, however, was actually decreed by Kingston Accords, signed on January 8, 1976 - at

the end of the meeting of the Interim Committee of the IMF - and ratified in April of the same year.

These agreements sanctioned, in fact, the possibility that each Member State of the IMF chooses independently

the exchange rate regime that will be adopted. It was, in essence, legalized the use of floating exchange rates.

Agreements Kingston introduced new laws in order to: (1. The Gold. He was enshrined in the demonetization of

the precious metal. In particular, were abolished the official price of gold, its role as a common denominator of

equality and units of Special Drawing Rights, and the obligation of Member States to make payments in gold to

the IMF, in particular for quota increases and the payment of interest, (2. The Special Drawing Rights. Was the

methodology of calculation of SDR introduced in 1974, it was decided that the interest rate on the SDR would

follow the trend of the market, it decreed that the SDR would have served as a common denominator of parity

and means of payment, reference to both increases the stakes in the IMF, which interest expense (3. the shares in

the IMF. Was sanctioned the sixth general review of quotas of participation in the IMF, which recorded an

overall increase of 33.6%, rising from 29 billion to 39 billion SDR (4. operational structures of the IMF. In the

context of a reorganization of the apparatus of the IMF, were provided two departments, with separate

administrative and accounting tasks: the "General Department" and "Department of Special Drawing Rights."

Agreements Kingston are the culmination of the crisis, from the late sixties of the last century, has hit the

international monetary regime created at Bretton Woods. Following the collapse, during the seventies, all of its

foundational pillars - except the one represented by the role of the dollar as an international currency - the gold

exchange standard has given way to a new international monetary order, the dollar standard, in which the dollar

plays the role of key currency, although lacking any engagement with the gold and subjected, like any other

currency, to wide fluctuations in the foreign exchange market.

2. BY THE DECLINE OF THE DOLLAR TO THE NEW BRETTON WOODS

As of the end of the last century, in what is known in the literature as "dollar area" has come delineating an

opposition between the center country - the United States - which consumes more than it produces, recording

current account deficit, and the countries of periphery - the emerging economies of Asia and oil-producing

countries - which produce more than they consume, recording current account surplus. The two regions' "dollar

area" have, therefore, consumption propensities to save and complementary, by virtue of which each has

established a sort of coincidence of interests: the excess of demand on production in the U.S. translates into an

excess of imports over exports, which allows you to fill the excess production demand in the peripheral

countries, fueling a flow of exports, which, in turn, ends meet U.S. demand (R.I. McKinnon, 2005).

This coincidence of interests between the center and the periphery of the dollar is the leading reason for which

some economists believe that the significant deficits registered by the United States can continue to remain for

one or two decades.

2Interdisciplinary Journal of Research in Business ISSN: 2046-7141

Vol. 2, Issue. 5, (pp.01- 06) | 2012

Among the supporters of this line of thought, there are economists Dooley, Folkerts-Landau, and Garber,

creators of the theory of the second so-called Bretton Woods (BW2). They, in a series of articles published in

the early 2000s (M. Dooley, D. Folkerts-Landau, P. Garber, 2003, 2004a, 2004b, 2004c), have argued that the

exchange rate regime currently in force is nothing but the 'implicit iteration of the Bretton Woods system, which

is all the base that has governed international monetary relations between the immediate post-war period and the

early seventies of the last century.

The Bretton Woods regime consisted of a country center, the U.S., and a periphery, composed of the countries

of Western Europe and Japan. The peripheral countries, came out destroyed by World War II, carried out a

development strategy based on exchange rates anchored to the dollar, highly undervalued, and control of capital

flows, which resulted in an export-led growth (M. Dooley, D. Folkerts-Landau, P. Garber, 2003). These

countries recorded, consequently, substantial current account surplus, and accumulated increasing amounts of

foreign currency reserves. The United States, for their part, were the main export market for peripheral

countries, supporting the export-led growth as they pursued (SG Hall, G. Hondroyiannis, PAVB Swamy, G.

Tavlas, 2010), and guaranteed them a service financial intermediation, providing liquid assets to short-term and

illiquid assets in exchange for the long term. Basically, the town center of the international monetary system

gave loans to long and short-indebted towards the peripheral countries, working, in fact, as a central bank.

Once the countries of Western Europe and Japan reached a high level of socio-economic development, and

brought to completion the process of reconstruction and consolidation of democratic institutions, abandoned

their status as a "periphery" of the system, putting an end to 'adoption of strategies "controlled growth" and

giving up, then, the factors on which they were centered, ie fixed exchange rates and controls on capital flows,

which gave way, respectively, to floating exchange rates and markets open capital.

Dooley, Folkerts-Landau and Garber (2003) argue, however, that floating exchange rates and free capital

movements have been a mere transition in the more general context of international monetary relations,

characterized by the absence of a suburban real own, "for which a development strategy based on growth

'export-led', was the overarching goal of economic policy."

This transitional phase lasted two decades and ended with the collapse of communism, between 1989 and 1991,

which, in fact, "revived" the exchange rate regime of Bretton Woods, bringing new emerging economies to

replace all 'Western Europe and Japan in the role of the periphery of the system.

The periphery of the new system of Bretton Woods (BW2) consists of those in emerging Asian countries, which

have adopted a development strategy similar to the one pursued in Western Europe and Japan after World War

II: export-led growth policies based de jure or de facto the anchor of national currencies to the dollar. By

controlling foreign exchange, these countries are able to maintain their currencies undervalued, achieving

compensatory advantages that allow them to increase exports, reduce imports - recording, in this way, a current

account surplus - and attract foreign direct investment flows. Like what happened to the European countries and

Japan in the first Bretton Woods, even the emerging Asian countries accumulate massive amounts of dollar

reserves, in consequence of the underestimation of the national currencies. The emerging economies of Asia are

not, however, the only ones to benefit from the second Bretton Woods: also the country center, the U.S. enjoys a

number of benefits. By reason of vulnerability and distortions that characterize their banking systems and

national financial peripheral countries end up investing the substantial foreign exchange reserves accumulated

financial assets in the United States. The resulting inflow of foreign capital in the U.S. makes it easier for the

continuation of current account deficit, helping to keep U.S. interest rates low (M. Dooley, D. Folkerts-Landau,

P. Garber, 2004a), and stimulating, in thus, the use of debt and higher levels of consumption and imports.

3. THE MISCONCEPTION OF THE NEW BRETTON WOODS

It is not so easy to talk about a new Bretton Woods. An economic analysis initially requires the study of the

historical context in which the “Conference” went taking shape: the end of World War II.

The 1944 was the year of the invasion of Normandy where the tide of war had become clear, on the Eastern

Front, the Soviets showed how conflict resolvers. The course details were still to be defined, but no one was so

idealistic as think that after the suffering they had suffered as a result of the Nazis, the Russians would withdraw

from the territories on which they had marched in the direction of Berlin.

At the same time was therefore already to delineate the contours of the future Cold War: the world between

Russia and the United States - or Europe - had two prospects before him: to enter the orbit or experience the

3Interdisciplinary Journal of Research in Business ISSN: 2046-7141

Vol. 2, Issue. 5, (pp.01- 06) | 2012

U.S. occupation. For the Europeans, any hope of rebuilding was linked to the will of the United States. Apart the

danger of an attack by the Soviets, the war had destroyed Europe and the damage further aggravated every inch

that the Soviets and the Americans spread. States continental - and not only the United Kingdom - were indebted

during the war: in a few words were in pieces. This war was very different from the First World War, where

clashes were concentrated along some trenches. This was instead characterized by a blitzkrieg massive

bombing, which left the continent in ruins - almost nothing could be rebuilt. Even avoiding mass starvation was

a challenge and any hope of rebuilding depended on the financing of the United States. The Europeans would

accept any offer. It is in this context that we can find also the basis of the agreements of the Conference: the

Bretton Woods were part of a larger American project which aimed to prolong military alliances over the

surrender of Germany - but without the Soviet Union.

At Bretton Woods, the United States put at the center of this new system, agreeing to become the largest trading

partner of the member countries. The United States would allow the Europeans to have access to its markets to

cost practically nothing and would have turned a blind eye on rates until the European continent had not reached

a sufficient level of welfare. The sale of European goods in the United States would help Europe from the

economic point of view and in return the United States would receive the support of political and military

matters: thus was born the NATO - the last bastion against the Soviet invasion.

The Bretton Wood was therefore based on the possibility of maintaining national sovereignty within a web of

relationships, which eventually was guaranteed not only by the political power of America, but also on its

economic power. The American economic power stood with that of other nations of the non-Communist world

and ensured the stability of the international financial system.

With the outbreak of the U.S. subprime mortgage crisis (September 2008), however, many economists and

politicians have begun to outline the need for a new Bretton Woods, as if to justify the errors of finance with the

rules of a system of international exchange rates.

The financial crisis of last September has not been shown, therefore, that the international economic system has

changed, but instead revealed what happens if the "guarantor" of the international financial system is in crisis

because it is a global crisis due to infection. But, in reality, Bretton Woods has remained unchanged: the U.S.

economy is still the largest, and its problems affect the whole world.

It is therefore wrong to talk about a redefinition of the Bretton Woods Agreements based on a reduction in the

role and the dollar as the key currency of the international monetary system. As many authors over the last five

years have risen, through econometric techniques in time series, the euro as an international currency, second

only to the dollar, the current situation of the European sovereign debt crisis does not play in favor of an

antagonist to the dollar.

The use of the dollar as the international reserve currency par excellence is the result of forces from the United

States or their policies, but believed that the international application has been throughout history to the U.S.

currency. The European currency, young for the trait of “hysteresis historical" though it has been a success in

the choice of anchor currency in some countries and currency invoicing in others, but does not have the political

sovereignty and not even a real Central Bank. In fact, as we noted in the recent sovereign debt crisis, the

European Central Bank does not have sufficient authority to regulate the banks of Europe and even the freedom

to act on the primary markets to put an end to the crisis.

To strengthen the above-mentioned hypothesis is necessary to analyze the performance of the euro-dollar

exchange rate. This is necessary because you have to separate what is the crisis of sovereign debt crisis,

however, the euro currency. The crisis has origni based on a lack of confidence about the ability of euro area

countries to honor their debts, but as this crisis has affected the euro and its propensity to international currency,

it is necessary to analyze their exchange rate with the dollar. In recent years, the euro had played a key role as an

international currency in relation to the choices of private and economic in general to use the European currency

for transactions, including financial. The exchange rate, ie the continuous appreciation the single currency was

a sort of lack of euro against the increasing international demand. the inability to print new money from the

ECB did appreciate its value against the dollar, highlighting the strength of the euro as an international currency.

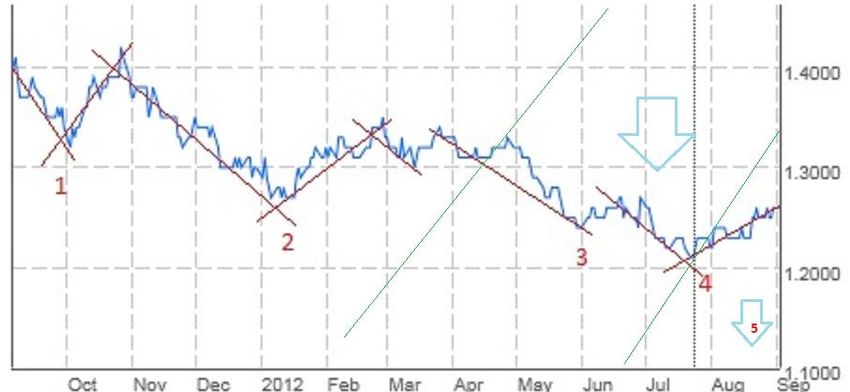

However, as we can see from the chart below, over the past year the euro has gradually depreciating against the

dollar at the same time the sovereign debt crisis. Not only. the analysis of Elliott Wave 5 clearly shows a

decreasing trend rebound minimum for next month. This reflects the continuation of the European crisis and

how it affects the single currency, its role as an international currency and the ability of the dollar to continue to

be the base currency of global exchange rate system.

4Interdisciplinary Journal of Research in Business ISSN: 2046-7141

Vol. 2, Issue. 5, (pp.01- 06) | 2012

Current exchange rate eur / dollar (1 year)

Source: our elaborations on Powerdesk Fineco data, 2012

4. CONCLUSION

The process of affirmation of the dollar as the key currency of the international monetary system began after

World War II, when the international monetary regime outlined by the Bretton Woods agreements, based on the

concept of symmetry, that of equality of rights and responsibilities between member countries, eventually

evolve into a hegemonic monetary regime, centered, that is, the absolute primacy of the U.S. dollar.

However, the current global financial crisis, now spilled over to the real economy, it seems, in some ways, a

new edition updated of what happened in the mid-sixties of the last century. It is, in fact, the ultimate

consequence of a series of behaviors adopted by the United States, essentially aimed at achieving internal

balance, in utter disregard of the requirements of external equilibrium, as if the current account deficit

accumulated over decades were not of crucial importance. The result was an injection of excess liquidity, which

has promoted the global economic imbalance, favoring the outbreak of the financial crisis.

Even today, therefore, at the beginning of the new millennium, the United States, have abdicated their

responsibility to the country center of the international monetary system, adopting economic policy decisions

which, neglecting the potential effects on foreign economies, they sent them a profound instability. This has led

to the risk of undermining the confidence of the rest of the world in the U.S., as a key currency country, with

significant repercussions for the International Monetary Fund. The magnitude of the crisis is such, that is, to

move the thinking of many economists to the possibility of a process of profound transformation of the

international monetary, in which the dollar standard to give way to a new monetary regime.

The lack of an alternative to the dollar in the international economic system, perhaps even failed with the crisis

of the euro-zone, remove the thought of a new international monetary order. On the contrary, in a world ruled by

speculative finance, a new order should be sought rather in the institutional and financial asstetti, creating a sort

of branch connected to the existing Bretton Woods system.

REFERENCES

1. Alesina, Alberto and Robert J. Barro (2000), “Currency Unions”, NBER Working Paper 7927.

2. Bekaert, G., and Harvey, C.(1995), Time-varying world market integration, J.Finance 50, 403-444

3. Baek, Seung-Gwan and Chi-Young Song (2001), “Is Currency Union a Feasible Option in East Asia?”,

unpublished manuscript.

4. Bayoumi T and B. Eichengreen (1994), ‘One Money or Many? Analyzing the Prospects of Monetary

Unification in Various Parts of the World’, Princeton Studies in International Finance No 76.

5. Bayoumi, T and B. Eichengreen (1997), “Ever Close to Heaven? An Optimum- Currency-Area Index

for European Countries, European Economic Review 41, 761-770.

6. Bayoumi, T. and P. Mauro (1999), “The Suitability of ASEAN for a Regional Currency Arrangement,”

IMF WP/99/162.

5Interdisciplinary Journal of Research in Business ISSN: 2046-7141

Vol. 2, Issue. 5, (pp.01- 06) | 2012

7. Bayoumi, Tamim, Barry Eichengreen and Paolo Mauro (2000), “On Regional Monetary Arrangements

for ASEAN”, Journal of the Japanese and International Economics, 14, 121-148.

8. Blanchard, Olivier J., and Quah, Danny (1989), “The Dynamic Effects of Aggregate Demand and

Supply Disturbances,” American Economic Review, 655-673.

9. Canova, Fabio and Harris Dellas (1993), “Trade Interdependence and the International Business

Cycle,” Journal of International Economics, 34, 23-47.

10. Cheng, Y., and Mak, S. (1992), The international transmission of stock market fluctuation between the

developed markets and the Asian-Pacific markets, Appl, Finan. Econ. 41, 43-47.

11. Clark, Todd, and Eric van Wincoop (1999),“Borders and Business Cycles,” Journal of International

Economics, forthcoming.

12. Dornbusch, R. and Y. Park (1999), “Flexibility or Nominal Anchors?,” in Exchange Rate Policies in

Emerging Asian Countries eds by S. Collignon, J. Pisani-Ferry, and Y. Park, Routledge, London.

13. De Brauwer, Gordon (2000), “Does a Formal Common-Basket Peg in East Asia Make Economic

Sense?” paper presented at the Financial Markets and Policies in East Asia at ANU, Canberra,

Australia.

14. Eichengreen, Barry and Tamim Bayoumi (1999), “Is Asia An Optimum Currency Area? Can It

Become One?: Regional, global and historical perspectives on Asian monetary relations”, in S.

Collignon, J. Pisani-Ferry, and Y. C. Park(eds.) Exchange Rate Policies in Emerging Asian Countries,

347-366.

15. Frankel, Jeffrey and Andrew Rose (1998), “The Endogeneity of the Optimum Currency Area Criteria,”

Economic Journal 108, 1009-1025.

16. Geweke, J. (1977), “The Dynamic Factor Analysis of Economic Time Series Models,” in D.J. Aigner

and A.S. Goldberg, eds., Latent Variables in Socio-economic Models, (Amsterdam: North Holland).

17. Glick, R, and Hutchinson, M.(1990), Financial liberalization in the Pacific Basin: Implication for real

interest rate linkage, J.Japan.Int.Econ. 4, 36-48.

18. Gregory, A.W., A.C. Head and J. Raynauld (1997), “Measuring World Business Cycles,” International

Economic Review, vol. 38, No. 3, pp.677-701.

19. Heston, Alan and Robert Summers (1991), "The Penn World Table (Mark 5): An Expanded Set of

International Comparisons, 1950-1988", Quarterly Journal of Economics, pp.327-368.

20. Imbs, Jean (1999), “Co-Fluctuations,” CEPR Discussion Paper No. 2267.

21. Kalemli-Ozcam, Sebnem, Bent Sorensen and Oved Yosha (2001), “Economic Integration, Industrial

Specialization, and the Asymmetry of Macroeconomic Fluctuations,” Journal of International

Economics, Vol.33, pp.107-137.

22. Kenen, Peter B. (1969), “The Theory Of Optimum Currency Areas: An Eclectic View” in R. Mundell

and A. Swoboda eds, Monetary Problems of the International Economy, The University of Chicago

Press, Chicago, 1969, pp. 41-60.

23. Kwan, C. H. (1998), “The Theory of Optimum Currency Areas and the Possibility of Forming a Yen

Bloc in Asia”, Journal of Asian Economics, Vol. 9, No. 4, 555- 580.

24. [24] Krugman, Paul/ Obstfeld, Maurice (2003), International Economics: Theory and Policy. San

Francisco: Addison Wesley.

25. Lewis, Karen K. (1999), “Trying to Explain Home Bias in Equities and Consumption”, Journal of

Economic Literature, Vol. 37, pp.571-608.

26. McKinnon, Ronald I (1963), “Optimum Currency Areas,” American Economic Review 53, pp. 717-

725.

27. McKinnon, R. (1999) ”The East Asian Dollar Standard, Life after Death?” Working Paper, Stanford

University.

28. Mundell, R. 1961, “A Theory of Optimum Currency Area,” American Economic Review, Vol. 60,

pp.657-665.

29. Rose, Andrew K. (2000), “One Money, One Market: The Effects of Common Currencies on Trade”,

Economic Policy 30.

30. Sargent, T.J. and C. Sims (1977), “Business Cycle Modeling without Pretending to Have Too Much A

Priori Economic Theory,” in New Methods in Business Cycle Research: Procedures from a

Conference (Minneapolis: Federal Reserve Bank of Minneapolis, pp.45-110.

31. Stock, J.H. and N.W. Watson (1991), “A Probability Model of Coincident Economic mIndicators,” in

K.Lahiri and G.H. Moore, eds., Leading Economic Indicators: New Approaches and Forecasting

Records, Cambridge: Cambridge University Press, pp.63-89.

32. Tavlas, J.H. and N.W. Watson (1991), “A Probability Model of Coincident Economic mIndicators,” in

K.Lahiri and G.H. Moore, eds., Leading Economic Indicators: New Approaches and Forecasting

Records, Cambridge: Cambridge University Press, pp.63-89.

6You can also read