KNOWLEDGE REPORT VIETNAM - 2Q 2014 | VIETNAM OVERVIEW - www.colliers.com/vietnam - Colliers International

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

2Q 2014 | VIETNAM OVERVIEW

VIETNAM

KNOWLEDGE REPORT

The Vista, District 2, HCMC

www.colliers.com/vietnam

VIE TNAM PROPERT Y MARKE T AT A GL ANCE TABLE OF CONTENTS VIETNAM ECONOMIC UPDATE • Vietnam’s macroeconomic improving thanks to ............................................... 1 stable FDI inflows HO CHI MINH CITY & HANOI’S ECONOMIC UPDATE HO CHI MINH CITY PROPERTY MARKET Office ............................................... 2 • Market Overview • Market Insight • Forecast Retail ............................................... 3 • Market Overview • Market Insight • Forecast Condominium .............................................. 5 • Market Overview • Market Insight • Forecast Serviced Apartment .............................................. 7 • Market Overview • Market Insight • Forecast HCMC INDUSTRIAL MARKET .............................................. 9 HANOI PROPERTY MARKET ............................................... 10 Office • Market Overview ............................................... 11 • Market Insight • Forecast Retail ............................................... 12 • Market Overview • Market Insight • Forecast Residential .............................................. 13 • Market Overview • Market Insight • Forecast

VIETNAM | 2Q 2014 | ECONOMIC UPDATE

Vietnam’s macroeconomic improving thanks to stable FDI inflows

VIETNAM 2Q14 Y-O-Y 3Q14F In 2Q14, GDP growth rate achieved 5.25%, bringing the six-month

GDP Growth 5.25% 0.3%

rate to 5.18%, according to the General Statistical Office. Vietnam’s

Total Registered FDI (US$ billion) 3.52 -21%

Exports (US$ billion) 37.6 16.2% macroeconomic continues to improve thanks to stable FDI inflows and

Imports (US$ billion) 37.3 9.0% strong manufacturing export though the domestic demand remains

CPI 4.7% -1.8%

Total retail sales (VND billion) 737.6 10.7%

weak given low sentiment from private sector and risky bad debts of

International Visitors (million) 1.9 9.0% commercial banks.

Base Rate 9% 0.0%

Exchange Rate (US$) 21,246 -0.9% The incidents of China’ oil rig dispute put some challenges

VN-Index 562.02 8.4%

to the economy growth yet impacts were limited. Japanese,

Gold Price (VND million/ tael) 36.7 -9.79%

Source: Colliers International

Korean, American and Taiwanese are currently major FDI

stocks in Vietnam. The total registered FDI from China into

Vietnam remains small although it has been risen in recent

FDI OF VIETNAM, 2Q 2014

years.

Moreover, trade activities between two countries well improved

in the first half of 2014 when both export and import turnovers

increased steadily 20.8% and 21.1% alternately compared to the

similar period last year. However, tourism industry has been hurted

because of dramatical fall from Chinese holidaymakers after big

surge of 30% in the first four months of 2014. International visitors

to Vietnam through the border gates with China in June slowed

Source: GSO, Colliers International

down 50% against May.

VIETNAM’ S IMPORT - EXPORT FIGURES, 2Q 2014 Forecast

>> The expected Free Trade Agreements (FTA) between European

Union (EU) and Vietnam by the end of this year will strongly

increase the country’s export turnover because most of applied

taxes to Vietnamese products trade to EU will gradually reduce

to 0%.

> > The FTA signing will also provide many opportunities for

local firms to gain significant flow of quality investment

Source: GSO, Colliers International from Europe nations, acceleration of shared expertise and

transfer of advanced technology.

>> It is noticed that local authorities have implemented strategic progress to minimise economic dependence on China market

as well as meeting the Trans-Pacific Partnership requirements.

> > In the near future, Vietnamese manufactures have to utilise local resources and seek for alternative exporting markets.

> > Meanwhile, there are also other segments required urgent improvement including logistics infrastructure, shortage of

skilled labor, supply chain management capability and facilitate linkages with foreign firms.

P.1 | Colliers International

HO CHI MINH & HA NOI | 2Q 2014 | ECONOMIC UPDATE

Export turnover of HCMC expects strong growth in 2014

HO CHI MINH CITY 2Q14 Y-O-Y 3Q14F >> The impact of tax incentives and other preferential

GDP Growth 8.7% 0.6% policies encourage an enormous capital inflow from

Registered FDI (US$ million) 106 -18.2% foreign investment, contributed around 23.3% to

Exports (US$ billion) 7.85 10.2% the city budget in 2Q14.

Imports (US$ billion) 7.06 -5.1%

CPI 5.02% 2.54% >> HCMC, being an export-oriented economy,

Total retail sales (VND billion) 159.5 6.6% recorded export turnover of approximately

International Visitors (million) 0.8 -1.5% US$14,182 million in the first six months of 2014,

Source: GSO, Colliers International growing approximately 5.7% year-on-year.

>> In June, income from exporting was 4.3% lower than experienced figure in May, reflecting temporary market disruptions.

>> However, with recently adjusted the VND/USD exchange rate up by one percent and external demand picking up in the second half of

the year, exports are forecast to bounce back and accelerate in the upcoming months.

Ha Noi saw growth of implementing FDI

HA NOI 2Q14 Y-O-Y 3Q14F >> In the first half of 2014, Hanoi’s GDP increased by

GDP Growth 7.4% -0.3% 7.4% (y-o-y).

Registered FDI (US$ million) 522 13.7% >> The service sector contributed 4.1 percentage

Exports (US$ billion) 2.85 8.0%

points and another 3.2 percentage points was

Imports (US$ billion) 5.1 -21.5%

added by the Construction and Industry.

CPI 6.43% 1.0%

International Visitors (million) 0.59 18.4% > > Generally, the CPI of June saw a y-o-y gain of

Source: GSO, Colliers International approx. 6.43%.

>> Regarding to foreign investment, the accumulating registered FDI of Hanoi in the first two quarters of this year reached US$560

million, a 13.7% y-o-y growth.

>> The implementing FDI was estimated about US$405 million, increasing by 6.5% y-o-y.

>> The predicted total number of international visitors to Hanoi in the first six-month of this year reached approx. 1.1 million, equaling

to 28.2% y-o-y increase. The forecasted number of local visitors rose by only 3.2% (y-o-y).

HCMC - HANOI FDI GROWTH BY MONTH HCMC - HANOI GDP GROWTH RATE, 2Q 2014

Source: GSO, Colliers International Source: GSO, Colliers International

P.2 | Colliers International

HO CHI MINH CITY | 2Q 2014 | PROPERTY MARKET HCMC Property Market Overview View of HCMC CBD

HO CHI MINH CITY | 2Q 2014 | OFFICE MARKET

2Q14 3Q14F* Office market retains upward movement

> > In 2Q14, Grade A buildings saw a lift of occupancy rate, whilst

Average asking rent

asking rent slightly declined by 0.74% q-o-q, yet growing 5% in

comparison to the same period of 2013.

Occupancy rate

> > Vacancy rate of Grade B continued its noticed improvement

dropping to 8.6% from 9.2% in previous quarter.

Supply > > The average asking rent of CBD Grade B towers went up to

US$19.48/ sq m/ month while non-CBD buildings witnessed a

GRADE A OFFICE PERFORMANCE, 2Q 2014 difficult period when both asking rents and occupancy rate fell

moderately in reviewed quarter.

Market Insight

>> Currently, there are few options for tenants who require adequate

office spaces in CBD Grade A and B buildings.

> > This provides opportunities for office developments in CBD

fringe and outer districts including District 3, 2 and 7 with

Source: Colliers International

GRADE B OFFICE PERFORMANCE, 2Q 2014 competitive rental rate and incentives.

> > In particular, District 2 will be a promising office area as

a new CBD of the city connecting directly to District 1 and

surrounding zones.

>> We predict a trend of moving out of downtown early next year with

completion of buildings with high quality specifications covering

Lim 2 Tower, SSG Tower and Viettel Office and Trade Center.

Source: Colliers International

> > As a result of stable demand and steady occupied space,

VIETTEL COMPLEX UNDER CONSTRUCTION sublease activities at top graded office developments has

been more popular in second quarter of this year.

Forecast

>> We foresee a moderate growth from both average asking

rents and occupancy rate during the latter half of 2014 given

improving economic scenes though at low pace compared to

the previous year.

> > During the next quarters, retaining existing tenants will be

top priority of landlords to secure constant income as well

as pricing strategy.

Source: Colliers International

P.3 | Colliers International

HO CHI MINH CITY | 2Q 2014 | OFFICE MARKET

HCMC Office Market Overview

Com-

NLA Service Occupancy NFA asking rent

No Name Address pletion

(sq m) Charges (*) rate (*)

Year

1 Saigon Centre 65 Le Loi 1996 11,650 6.5 95% 40.0

2 Saigon Tower 29 Le Duan 1997 13,950 6.0 99% 37.0

3 Sunwah Tower 115 Nguyen Hue 1997 20,800 6.0 91% 43.0

4 The Metropolitan 235 Dong Khoi 1997 15,200 6.0 94% 41.0

5 Diamond Plaza 34 Le Duan 1999 15,936 8.0 99% 41.0

6 Kumho Asiana Plaza 39 Le Duan 2009 26,000 8.0 93% 49.0

7 Bitexco Financial Tower 45 Ngo Duc Ke 2010 37,710 8.0 88% 34.0

8 President Place 93 Nguyen Du 2012 8,330 6.0 97% 30.0

9 Times Square 22-36 Nguyen Hue 2012 9,000 7.0 60% 50.0

Grade A 158,576 7.0 90.4% 39.8

1 OSIC 8 Nguyen Hue 1993 6,500 6.0 94% 20.0

2 Yoco Building 41 Nguyen Thi Minh Khai 1995 5,000 4.0 100% 16.0

3 Somerset Chancellor Court 21-23 Nguyen Thi Minh Khai 1996 3,200 5.0 100% 21.0

4 Central Plaza 17 Le Duan 1997 6,094 5.0 100% 26.0

5 Saigon Riverside Office 2A-4A Ton Duc Thang 1997 10,000 5.0 98% 20.0

6 Saigon Trade Center 37 Ton Duc Thang 1997 31,416 6.0 96% 23.0

7 Harbour View Tower 35 Nguyen Hue 1997 8,000 5.0 98% 22.0

8 MeLinh Point Tower 02 Ngo Duc Ke 1999 17,600 6.0 99% 24.0

9 Zen Plaza 54-56 Nguyen Trai 2001 11,037 5.0 95% 21.0

10 Bitexco Office Building 19-25 Nguyen Hue 2003 6,000 5.0 92% 25.0

11 The Landmark 5B Ton Duc Thang 2005 8,000 5.0 82% 21.0

12 Opera View 161-167 Dong Khoi 2006 3,100 7.0 90% 26.0

13 Indochina Park Tower 4Bis Nguyen Dinh Chieu 2006 2,145 3.0 77% 10.0

14 Petro Tower 1-5 Le Duan 2007 13,304 5.0 99% 30.0

15 City Light 45 Vo Thi Sau 2007 10,000 5.0 98% 15.0

16 The Landcaster 22Bis Le Thanh Ton 2007 7,000 5.0 100% 24.0

17 Gemadept Tower 5 Le Thanh Ton 2008 14,000 7.0 100% 23.0

18 Fideco Tower 81-85 Ham Nghi 2008 15,000 6.0 100% 20.0

19 Havana Tower 132 Ham Nghi 2008 7,326 6.0 99% 21.0

20 Sailing Tower 51 Nguyen Thi Minh Khai 2008 16,910 6.0 96% 26.0

21 Royal Center 235 Nguyen Van Cu 2008 14,320 5.0 100% 23.0

22 TMS 172 Hai Ba Trung 2009 4,000 4.0 100% 23.0

23 Bao Viet Tower 233 Dong Khoi 2010 10,650 6.0 100% 21.0

24 Green Power Tower 35 Ton Duc Thang 2010 15,600 6.0 96% 22.0

25 Vincom Center 68-70-72 Le Thanh Ton 2010 56,600 5.0 70% 23.0

26 Saigon Royal 91 Pasteur 2010 5,340 4.0 100% 19.0

27 A&B Tower 76 Le Lai 2010 17,120 6.0 98% 29.0

28 Maritime Bank Tower 192 Nguyen Cong Tru 2010 19.596 5.0 89% 23.0

29 Empress Tower 138 Hai Ba Trung 2012 19,538 6.0 93% 26.0

30 Lim Tower 9-11 Ton Duc Thang 2013 29,265 6.0 97% 28.0

31 Sunny MB Tower 259 Tran Hung Dao 2013 13,200 5.5 12% 22.0

Grade B 399,596 6.0 89.5% 23.1

* US$/ sq. m/ month (on net area)

P.4 | Colliers International

HO CHI MINH CITY | 2Q 2014 | RETAIL MARKET

2Q14 3Q14F* Reverse movements between retail malls and

high street shops

Average asking rent

HCMC retail market witnessed a downturn tendency with fall in both

Occupancy rate occupancy rate and rental from retail centers during 1H 2014.

The retail podium experienced slight drop in both figures with notable

Supply vacant spaces within CBD area after prolonged fully-occupied condition.

Regardless weaken adjustment in rents, both department store and

MARKET PERFORMANCE, 2Q 2014 shopping centre segments still recorded 3% and 2% increase in

vacancy rate respectively, mostly contributed by suburban malls.

In contrast, we saw accelaration of expansion activities from international

F&B brands with open of the 2nd McDonald’s restaurant, the 3rd Starbuck

and the 17th Baskin Robbins stores in HCMC.

Market Insight

Source: Colliers International Central shopping centers struggling in retain tenants

MARKET PERFORMANCE BY SECTOR, 2Q 2014 >> We noticed significant empty spaces in both CBD and suburban retail

centres during last quarter disregard moderate decline in rental from

operators.

>> A lengthen pull back period of consumer’s expenses forced retailers,

especially local brands, to review business plan while top brands

took the opportunities to obtain prime locations in order to seize the

market shares.

>> However, either move-out or relocation trend still excess expansion

movement.

Source: Colliers International

>> Medium-sized sites ranging from 150-200sm. q in city downtown

SC VIVOCITY @ SAIGON SOUTH are current market hot spots.

Forecast

> > We expect increasing competition in retail sector given

a pipeline of new projects coming in next year including

SC Vivocity (District 7), Vietttel Complex (District 10),

Lim Tower 2 (District 3) and SSG Tower (Binh Thanh).

> > Nevertheless, recent acquisitions of Pico Plaza (Tan

Binh) by Lotte and Hi-tech Healthcare Park (Binh Tan)

by Aeon Mall show prospective outlook of local market

Source: Colliers International to foreign investors.

P.5 | Colliers International

HO CHI MINH CITY | 2Q 2014 | RETAIL MARKET

HCMC Retail Market Overview

Name of Project / Comple- NLA Average Rental

No Address Location Occupancy Rate

Building tion Year (sq m) (US$/sq m/month)

1 Hotel Continental Saigon 132-134 Dong Khoi District 1 2000 200 90 100%

2 Caravelle Hotel 19 Lam Son Square District 1 2000 150 95 100%

3 New World Hotel 79 Le Lai District 1 2000 1,000 40 100%

4 Sheraton Saigon 88 Dong Khoi District 1 2002 750 125 67%

5 Opera View Lam Son Square District 1 2006 1,260 100 100%

6 The Manor 1 91 Nguyen Huu Canh Binh Thanh 2006 2,000 20 90%

7 Saigon Pearl 92 Nguyen Huu Canh Binh Thanh 2009 5,000 16 75%

8 Rex Arcade 141 Nguyen Hue District 1 2010 2,000 120 99%

9 The Manor 2 91 Nguyen Huu Canh Binh Thanh 2010 2,500 20 90%

10 Bitexco Financial Tower 45 Ngo Duc Ke District 1 2011 8,000 35 79%

11 The Vista Walk Ha Noi Highway District 2 2012 5,000 20 40%

12 President Place 93 Nguyen Du District 1 2012 800 60 67%

13 Times Square 22-36 Nguyen Hue District 1 2013 9,000 90 72%

14 Saigon Airport Plaza 1 Bach Dang Tan Binh 2013 7,623 17 90%

Retail Podium 50,323 57 78%

1 Diamond Plaza 34 Le Duan District 1 1999 9,000 90 98%

2 Zen Plaza 54-56 Nguyen Trai District 1 2001 6,817 60 97%

3 Parkson Saigon Tourist 35 Le Thanh Ton District 1 2002 17,000 90 97%

4 Parkson Hung Vuong 126 Hung Vuong District 5 2007 24,000 60 70%

5 Kumho Asiana Plaza 35 Le Duan District 1 2009 6,830 40 100%

6 Parkson Flemington Le Dai Hanh District 11 2009 26,000 25 50%

7 Parkson Paragon Nguyen Luong Bang District 7 2011 7,500 35 65%

8 Parkson C.T Plaza Truong Son Tan Binh 2012 12,235 40 90%

9 Parkson Cantavil Premier Ha Noi Highway District 2 2013 17,815 40 82%

Department Store 127,198 52 77%

1 Saigon Center 65 Le Loi District 1 1996 3,500 75 100%

2 City Plaza 230 Nguyen Trai District 1 2000 5,250 16 88%

3 Superbowl Vietnam - TSN Truong Son Tan Binh 2002 5,500 18 55%

4 Tax Center 135 Nguyen Hue District 1 2003 7,000 75 100%

5 An Dong Plaza 18 An Duong Vuong District 5 2004 18,000 40 80%

6 Saigon Square 1 77-89 Nam Ky Khoi Nghia District 1 2006 1,300 167 100%

7 Nowzone Nguyen Van Cu District 1 2008 9,000 35 95%

8 Lotte Mart Saigon South Nguyen Huu Tho District 7 2008 24,000 35 96%

9 Saigon Square 2 7-9 Ton Duc Thang District 1 2009 1,400 90 80%

10 Vincom Center B 72 Le Thanh Ton District 1 2010 45,000 63 73%

11 Maximark 3/2 Extension 3/2 Street District 10 2010 25,000 35 80%

12 Lotte Mart Phu Tho Le Dai Hanh District 11 2010 24,500 30 85%

13 Crescent Mall Nguyen Van Linh District 7 2011 45,000 35 78%

14 Satra Pham Hung Pham Hung District 8 2011 11,528 15 55%

15 CMC Plaza 79B Ly Thuong Kiet Tan Binh 2011 18,000 10 60%

16 Taka Plaza 102 Nam Ky Khoi Nghia District 1 2011 1,000 90 100%

17 Union Square Dong Khoi District 1 2012 38,000 73 65%

Shopping Centre 349,062 40 80%

P.6 | Colliers International

HO CHI MINH CITY | 2Q 2014 | CONDOMINIUM MARKET

Local developers endeavour to gain trust from buyers

> > The Secondary market recorded a minor q-o-q drop in price though

2Q14 3Q14F*

it is still a considerable decline to 2Q12.

Primary market

>> During second quarter of 2014, the Primary Condominium market saw

a q-o-q gain of almost 7% in average asking price while it is almost

Secondary market

equivalent to same period of 2012.

Supply >> High-end apartments experienced a slight decrease in price while that

of both Mid-end and Affordable segments notably gained 15% and 9%

Sold rate respectively in reviewed quarter.

The first half of this year noted surge in absorption rate

CHANGE OF UNIT TYPES OVER 2010 PERIOD

of residential sector, mostly from affordable condominiums

located in suburban areas.

As a result of that, there was a strong growth in supply of

residential for sale market from both newly-launched and

re-launched projects.

Followed a large stream of new developments in 1Q, last

quarter witnessed release of next phases and relaunch of

delayed condominiums.

Docklands Saigon (District 7) was relaunched by Pau Jar Group

Source: Colliers International after nearly 2 mute years while Hung Thinh Group introduced 8x

Thai An (formerly named Thai An 6) at Go Vap District given the

success of 8x Dam Sen in Tan Phu District.

SECONDARY MARKET PERFORMANCE BY DISTRICT

The Primary market also welcomed 727 new apartments

from mid-scale residential developments including Topaz

Garden, An Gia Garden (Tan Phu) and SSG Tower (Binh

Thanh).

Market Insight

> > Positive performance during 1H14 showed sign of recover for

residential market, especially from affordable and mid-end

segments.

Source: Colliers International > > That reflects an increase of market confidence after a long

period of wait-and-see attitude.

P.7 | Colliers InternationalHO CHI MINH CITY | 2Q 2014 | CONDOMINIUM MARKET

> > We saw significant efforts from local developers in building reputation and gaining buyer’s trust via good construction

progress from many projects.

> > Instead of totally rely on traditional sources from bank loan and customer’s cashflow, the developers now seek for

alternative financial supports including partners, construction vendors and even brokerage firms.

> > Multiple partners can share development risks whilst construction companies are willing to obtain en bloc of units for

trading as part of their business strategy.

Forecast

Steady take-up of new launchs given gain of market confidence

>> We expect constant absorption rate from new market supply till the end of this year given growth in market confidence.

> > Efficient-sized flats selling at US$700 per sq. m will remain the most sought-after products because of acceptable

expenses and eligible elements for financial support from 30 Trillion Package.

> > Existing developments face competitive pressure leading to strategic changes of (1) rebrand project with new pricing

approach and marketing strategy or (2) transfer project, mostly via loan acquisition.

HCMC Condominium Market Overview

Launched Average asking

No Name of Project Address Location Grade Total units

Year price (*)

1 Xi Riverview Palace 190 Nguyen Van Huong District 2 2008 High-end 270 2,100

2 Cantavil Premier Ha Noi Highway District 2 2010 High-end 200 1,720

3 Canh Vien 3 Nam Vien Area, PMH District 7 2011 High-end 116 1,990

4 C.T Leman Plaza 117 Nguyen Dinh Chieu District 3 2011 High-end 200 4,200

5 Star Hill Commercial Area, PMH District 7 2012 High-end 351 2,000

6 The Vista (Tower 4) Ha Noi Highway District 7 2013 High-end 141 1,470

7 The Prince Residence Nguyen Van Troi Phu Nhuan 2013 High-end 282 2,190

High-end developments

1 Everrich 2 422 Dao Tri District 7 2010 Mid-end 3,125 1,350

2 Thao Dien Pearl 12 Quoc Huong District 2 2010 Mid-end 450 1,670

3 Saigon Airport Plaza 1 Bach Dang Tan Binh 2011 Mid-end 242 1,800

4 Tropic Garden Nguyen Van Huong District 2 2012 Mid-end 388 1,200

5 Happy Valley Nguyen Van Linh, PMH District 7 2012 Mid-end 818 1,670

6 Sunrise City (Central + North) Nguyen Huu Tho District 7 2013 Mid-end 1,500 1,550

Mid-end developments

1 Topaz Garden Trinh DInh Thao Tan Phu 2014 Affordable 212 610

2 Ngoc Khanh Tower Nguyen Bieu District 5 2014 Mid-end 99 1,260

3 8x Thai An Phan Huy Ich Go Va[ 2014 Affordable 200 650

4 The Park Residence Nguyen Huu Tho District 7 2014 Mid-end 716 715

5 Parc Spring Nguyen Duy Trinh District 2 2014 Affordable 265 850

New launches in 2Q 2014

* US$/ sq. m

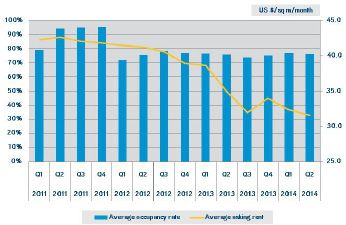

P.8 | Colliers InternationalHO CHI MINH CITY | 2Q 2014 | SERVICED APARTMENT MARKET

Noticed new market supply from refunctioned condominium developments

2Q14 3Q14F* >> Top-tier serviced apartments in HCMC experienced fall in occupancy

rate during last quarter.

Average asking rent

>> Grade A buildings slightly increase average asking rent given stable

vacancy rate approximately 10%.

Occupancy rate >> Last month, Grade B buildings recorded a drop of 6% in rental.

The first half of 2014 saw a notable new supply being refunctioned from

Supply condominium projects in CBD areas.

The New Pearl condominium project in District 3 is informed to be

GRADE A PERFORMANCE, 2Q 2014 completed by 3Q 2015 with 160 serviced flats after a prolonged

delay in construction.

The Waterfront Luxury Apartment (formerly known as Delta River

Tower) in District 1 with over 180 units is expected to operate by early

of 2016.

Market Insight

>> Continous stagnant condition of luxury residential market and solid

performance of serviced apartment lead to temporary refunctional

Source: Colliers International

decisions.

>> The developers will be able to get cashflow from leasing activities in short to mid-term while the buildings are revertable to

apartment for sales given similar specifications.

Comple- Total Average

No Project Name Address Location ARR(*)

tion Year Room Occupancy

1 The Landmark 5B Ton Duc Thang District 1 1995 66 81% 31

2 Somerset Chancellor Court 21-23 Nguyen Thi Minh Khai District 1 1996 172 93% 34

3 Sedona Suites 65 Le Loi District 1 1996 89 82% 30

4 Nguyen Du Park Villas 111 Nguyen Du District 1 2004 41 94% 30

5 The Landcaster 22 Bis Le Thanh Ton District 1 2007 55 73% 37

6 InterContinental Asiana Saigon 39 Le Duan District 1 2009 260 97% 36

Grade A 701 90% 34

1 Somerset HCM 8A Nguyen Binh Khiem District 1 1998 165 85% 26

2 Saigon Sky Garden 20 Le Thanh Ton District 1 1998 154 83% 26

3 Norfolk Mansion 17-21 Ly Tu Trong District 1 1998 126 90% 33

4 Diamond Plaza 34 Le Duan District 1 1999 42 98% 29

5 Garden View Court 101 Nguyen Du District 1 2000 76 93% 31

6 Nikko Saigon 235 Nguyen Van Cu District 1 2011 54 60% 28

Grade B 738 79% 27

P.9 | Colliers InternationalHO CHI MINH CITY | 2Q 2014 | INDUSTRIAL MARKET

Foreign 3PLs show increasing interests in RBF and warehouse segment

HCMC MASTER PLAN OF INDUSTRIAL ESTATES > > There is no new industrial supply during last quarter.

>> There are 13 industrial parks, 3 export processing zones and Saigon

Hitech Park with a total area of approximately 4,600 hectares operating

in HCMC

> > According to the master plan, by 2020, the city will have 22 industrial

areas with 7,000 hectares of new and expanded land area.

>> Current average vacancy rate of industrial properties in HCMC in reviewed

quarter is 33% and expected to be flat throughout this year given moderate

economic growth forecast.

> > The average asking rent of HCMC industrial parks was almost flat in

the last three months and is predicted to gain slightly 2% next year

due to increasing demand at a constant market supply.

Source: Public Domain, Colliers International

Market Insight

>> The Northern and Western zones are projected as major manufacturing and industrial hubs of the city taking advantage of Ring

Road System and East-West Highway.

> > The Southern zone with Hiep Phuoc IP as a core development will become a logistics and supply chain management center

given the cluster of main seaports in the surrounding areas.

> > Foreign third-party logistics (3PL) service providers show increasing interests in Ready-Built-Factory (RBF) and warehouse

segment. The typical size of these workshops is 1,000-2,000sq. m.

HCMC Industrial Market Overview

Area

No Name of Development Location Warehouse Rental Occupancy Rate

(hecta)

1 Tan Binh Tan Binh + Tan Phu District 128 3-4 100%

2 Linh Trung 1 Thu Duc District 62 3-4 100%

3 Tan Tao Binh Chanh District 380 3 87.7%

4 Tan Thuan District 7 300 4 81%

5 Le Minh Xuan Binh Chanh District 100 3 100%

6 Vinh Loc Binh Chanh District 203 3-4 100%

7 Cu Chi Western North Cu Chi District 208 2-3 100%

8 Hien Phuoc 1 Nha Be District 311 3-4 92%

9 Cat Lai 2 District 2 124 3.5 89%

10 Dong Nam Cu Chi District 287 2-3 27%

* US$/ sq. m

P.10 | Colliers InternationalHANOI | 2Q 2014 | PROPERTY MARKET Hanoi Property Market Overview Keangnam Hanoi Landmark Tower

HANOI | 2Q 2014 | OFFICE MARKET

Office market experienced downward tendency in last quarter

>> The down trend in office market has continued in reviewed

2Q14 3Q14F* quarter with decline in both occupancy rate and asking rent.

Average asking rent >> In 2Q 2014, Grade A asking rents experienced downward tendency.

>> Rent was recorded on average as US$31.6 per sq. m per month

Occupancy rate as landlord of office buildings are offering incentives to ease up

situation for tenants.

Supply >> The average occupancy of the Grade A offices was about 73%,

a bit lower than the previous quarter.

GRADE A OFFICE PERFORMANCE

EVN Tower (Cua Bac Street, Ba Dinh District) has been launched

in this quarter, adding approx. 45,621 sq m of NLA to the market.

Lotte Centre Hanoi hasn’t been ready to use in this quarter as

schedule. It is planned to open in September 2014.

As the supply still outweighed the demand, the market still

belonged to tenants. Whereas the Western segment became

Source: Colliers International

strongly competitive, landlords of Grade A building in the old

FUTURE SUPPLY BY DISTRICT CBD remain confident to their strategic location.

However, on another hand, it seems to be right time for the owners

of old buildings in the CBD to renovate and upgrade in order to

maintain their conditions.

The reasonable asking rental also attracted tenants from “villa” or

“townhouse” offices moving to standard office buildings.

Completed NLA Average asking

No Name of Project Developer Location

Year (sq m.) price (*)

Source: Hoa Binh Trading & Invest-

1 Colliers International

Viet Tower 1 Thai Ha, Dong Da 2008 20,000 18

ment JSC

2 EVN Tower EVN 11 Cua Bac, Ba Dinh 2012 45,621 45

Lot 32, Duong Dinh

3 Star Tower CFTD - VLA 2012 3,465 17

Nghe, Cau Giay

2 Dai Co Viet, Hai Ba

4 Pacific Building NCX 2013 4,279 17

Trung

115 Tran Hung Dao,

5 VID Tower 30/4 Tourism & Trading JSC 2013 4,136 21

Hoan Kiem

63 Le Van Luong,

6 63 Le Van Luong 319 Group 2013 12,254 18

Trung Hoa, Cau Giay

P.11 | Colliers InternationalHANOI | 2Q 2014 | RETAIL MARKET

Market expect more supply in latter half of 2014

>> The supply was unchanged as there was no new space adding

2Q14 3Q14F*

to the market in this quarter.

Average asking rent >> The average market rent was recorded at approximately US

$48.85/ sq m, a decrease of 1.8% q-o-q or approx. 25.9% y-o-y.

Occupancy rate >> The occupancy rate was about 80.2%, declining by 1.4 percentage

point q-o-q.

Supply

>> Generally, the retail market seems silent as the economic still

MARKET PERFORMANCE, 2Q 2014 grey. However, we still see some lighting points. Baskin Robbins,

the world’s largest chain of ice cream specialty shops, opened its

first shop in the old CBD of Hanoi, after a chain of 20 shops had

already launched in HCMC.

Lotte Center Hanoi is delayed to launch until 3Q 2014. Given their

prime location covering a very large area between the Old and

Source: Colliers International

New CBDs, its huge supply has been forecasted to strongly affect

MARKET SUPPLY, 2Q 2014

the market.

However, the current silent of other large retail spaces at Times

City, Royal City raises a question on the future launching of Lotte

Center Hanoi.

Source: Colliers International

Completed NLA Average asking

No Name of Project Developer Location

Year (sq m.) price (*)

1 EVN Tower EVN 11 Cua Bac, Ba Dinh 2012 4,385 45

2 Tran Hung Dao, Hoan

2 Hong River Tower Thien Duc Services JSC 2012 2,300 35

Kiem

63 Le Van Luong,

3 63 Le Van Luong 319 Group 2013 20,728 45

Trung Hoa, Cau Giay

459C Bach Mai, Truong

4 Mo Market Shopping Mall Vinaconex 2013 24,223 45

Dinh, Hai Ba Trung

5 CTM Building CTM 139 Cau Giay 2014 5,000 45

* US$/ sq m/ month (on net area)

P.12 | Colliers InternationalHANOI | 2Q 2014 | RESIDENTIAL MARKET

End-users are major demand of Hanoi residential market

2Q14 3Q14F* >> The average asking price of the primary market increased

slightly about 1% comparing to 1Q14.

Primary market

>> The secondary market marginally dropped 0.8% in asking

price from previous quarter with the average asking price of

Secondary market US$1,472 per sqm. It has not yet shown the actually recovery of

the market but it leads to increase the demand for apartment.

Supply

>> The 2-bedroom units with efficient area of 65sq. m to 80sq. m

are preferable regarding market liquidity and total price.

Sold rate >> From US$1,000 to US$1,500 per sqm is the asking price of the

most number of units in both primary and secondary market.

PRIMARY MARKET PERFORMANCE, 2Q 2014

>> Ha Dong and Cau Giay areas with affordable projects pricing

at US$857 per sq. m on average are leading in supply number

of apartments.

The survey of Colliers showed that the number of apartments in

the primary market decreased of approximately 6% from previous

quarter.

The price of apartment has slightly increased in compare with

Q1.2014; meanwhile, the transaction volume has notably increased.

Source: Colliers International This escalation trends to continue in next quarter.

In 2Q14, the Vietnamese government has released series of legal documents related to the real estate market including two sig-

nificant documents:

>> Circular No. 76: the apartment buyer has to pay the land use tax instead of the developer. This policy aims to reduce the financial

burden for the investor so the construction progress could be improved. But it also raises the concern in the buyers about the

transparency of the calculation and allocation this land use tax.

>> In a declaration in July 2014, Vietnamese government stated that they would terminate approving new commercial residential

project until 2015. It is predicted that this declaration will reduce the supply of apartment to market therefore the transaction price

will increase more.

Hand-over Average asking

No Name of Project Developer Location Total units

Period price (*)

No. 1 Thang Long High-

1 Thang Long Number One Viglacera 2Q 2014 1,000 1,619

way, South Tu Lam

62 Nguyen Huy Tuong,

2 My Son Tower My Son 2Q 2016 340 1,071

Thanh Xuan

Linh Dam Urban,

3 HH4 Hop Phu 1Q 2016 1,800 857

Hoang Mai

234 Pham Van Dong,

4 Green Starts An Binh 1Q 2016 930 985

North Tu Liem

5 Discovery Complex Kinh Do 302 Cau Giay, Cau Giay 1Q 2016 512 1,500

P.13 | Colliers InternationalKNOWLEDGE REPORT | 2Q 2014 | VIETNAM

About Colliers International 485 offices in

Colliers International is a leader in global real estate services, defined by our spirit of

enterprise.

Through a culture of service excellence and a shared sense of initiative, we integrate the

63 countries on

resources of real estate specialists worldwide to accelerate the success of our partners.

We connect through a shared set of values that shape a collaborative environment throughout

6 continents

our organization that is unsurpassed in the industry.

With more than 100 professionals in 2 offices in Vietnam, the team is market driven and

$2 15,700

billion in professionals

has proven and successful track record with both international and local experience.

annual revenue and staff

From Hanoi to Ho Chi Minh City, we provide a full range of real estate services

• Research 2.5

>>Market research across all sectors billion square feet

>>Market analysis, advisory, and strategy under management

• Valuation & Advisory Services

>>Valuation for land, existing property or development sites COLLIERS INTERNATIONAL

>>Feasibility studies to determine NPV, IRR and highest & best use

HO CHI MINH CITY

• Office Services

Bitexco Office Building, 7th Floor

>>Tenant Representation

19-25 Nguyen Hue Street

>>Landlord Representation District 1, HCM City, Vietnam

• Residential Sales & Leasing Tel: + 84 8 3827 5665

• Retail Services

• Investment Services HANOI

Capital Tower, 10th Floor

• Real Estate Management Services

109 Tran Hung Dao Street,

• Corporate Services Hoan Kiem District, Hanoi, Vietnam

• Industrial Leasing Tel: +84 4 3941 3277

The foundation of our services is the strength and depth of our experience.

QUANG NGUYEN

Please contact, If you would like to recieve our other research reports Research Manager

quang.nguyen@colliers.com

Publication Coverage Frequency Content Availability

+84 938 056 603

Research & Forecast Vietnam Cities Quarterly All market sectors Publicly available LINH PHAM

Report Research Manager

CBD Report HCMC CBD Monthly Office, Retail, Hotel and Publicly available linh.pham@colliers.com

Serviced Apartment +84 912 013 536

Asia Pacific Office Asia Pacific in- Quarterly Office market Publicly available

Report cluding Vietnam YEN NGUYEN

Vietnam Property Vietnam cities Quarterly All market sectors On subscription Research Analyst

Market Report yen.nguyen@colliers.com

Development Vietnam cities At request All market sectors On subscription +84 915 478 778

Recommendation

This document has been prepared by Colliers International for advertising and general information only. Colliers International makes no guarantees, representations

or warranties of any kind, expressed or implied, regarding the information including, but not limited to, warranties of content, accuracy and reliability. Any interested

party should undertake their own inquiries as to the accuracy of the information. Colliers International excludes unequivocally all inferred or implied terms, conditions

and warranties arising out of this document and excludes all liability for loss and damages arising there from. This publication is the copyrighted property of Colliers

International and/or its licensor(s). ©2013. All rights reserved.

www.colliers.com/vietnam Accelerating successYou can also read