The future of wealth management revisited - Winter 2020 - Deloitte

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

The future of wealth management revisited Winter 2020

Brochure / report title goes here |

Section title goes here

Contents

From disruption to transformation 3

Design principles shaping experience 5

The FA experience reimagined 6

Building a new, scalable architecture for digital 8

Transformation in progress: More emerging ideas and trends 12

A long view of transformation and opportunity 14

Authors’ note

In this article, we present the third point of view (POV) in a series on the future of Wealth Management

(WM) in the US. Our first POV, published in 2015,1 focused on sources of disruption and innovation in WM,

and the second POV in 20172 centered on the digital transformation of WM. This POV provides an update

on past perspectives and predictions and elaborates on new market and competitive trends.

2

The future of wealth management revisited

From disruption to transformation

It is an understatement to say that the much more out of our meeting!” A different A reason for the diminished effect is a

Wealth Management (WM) industry in investor spoke of using a robo-adviser to macroeconomic environment that has

the United States is undergoing profound manage part of his own assets in order to normalized faster than anyone expected

change. The 10 disruptors we discussed “keep a check on my adviser.” coming out of the financial crisis. Therefore,

in 2015—from new consumer preferences the need has receded for adapting advisory

and digital models to demographic, Another disruptor we identified in 2015 frameworks to the kind of new investment

macroeconomic, regulatory, and competitive that has made a strong impact in the environment where correlations between

trends—came together to upend the industry is the trend toward goals-based asset classes do not hold, inflation does

industry like a perfect storm, driving planning. In fact, organizing financial not exist, and volatility has become the

massive levels of disruption and plans centered on goals such as new normal—perhaps until the next

transformation, even if not all have education, real estate, retirement, and financial crisis?

made the same level of impact on the health care have by now become an

industry (see figure 1). industry standard across the banking, We have also seen the wealth management

insurance, and asset management industry making limited progress toward

Some disruptive trends have been more sectors. Some simplified versions of democratizing access to new asset

evident than others. A standout example financial planning are increasingly accessible classes and investment products. We

is consumers’ digital propensity, or their to all retail investors through compelling find weight in two explanations for slower

increasing comfort with using digital digital applications, and the breadth of democratization: reduced performance

channels and applications. This propensity financial and other life goals included in of alternative products and regulatory

has risen faster than anyone expected and these plans continues to expand, with constraints slowing down innovation.

has spread from a small group of digitally investment and protection strategies

inclined investors to the mainstream of becoming better integrated. Considering the overall picture, however,

virtually every investor segment. the depth of disruptive innovation and the

Other disruptors have been slower in speed of fundamental shifts across the

Digital proliferation spans generational their manifestation. The impact of big data WM industry continue to impress us. These

divides. Digital propensity is no longer and advanced analytics has not been as shifts are reshaping WM organizations and

specific to only younger investors, nor is it widespread as we expected. The industry how they are approaching user experience

limited to consumers who cannot afford has been slow in its work on potential and architecting their technology platforms

high-end wealth and private banking use cases and the transition from for the future.

services. Rather, it can be observed in every proofs of concept to operationalized

age group and every wealth tier. In a recent analytical capabilities.

survey of ultra-high-net-worth clients of a

leading private bank in New York City, we In our opinion, this delay is the result of

disproved the widely held assumption that investments in big data and advanced

ultra-high-net-worth clients have limited analytics being crowded out by other

digital needs and expectations because they priorities—such as regulatory compliance,

have direct access to large, multidisciplinary platform modernization, and new client

teams. We heard such an investor in her 60s digital capabilities—along with artificial

wonder about the financial planning and intelligence (AI) tools and technology

investment framework that her financial maturing a bit more slowly than expected.

adviser used: “I wish I had access to that Nevertheless, we continue to believe that AI

framework digitally and could try different will transform our industry by empowering

scenarios on my own before I sit down investors and advisers as well as by driving

with my financial adviser. I would get so new levels of client insights, personalization,

and efficiency in operations.

3

The future of wealth management revisited

Figure 1. 10 disruptors revisited

Disruptors* As observed in 2015* Industry impact expected in 2020

A new generation of investors think

All investors seem to have been rewired by now, and it is about the

differently about advice and bring new

“rewired” adviser as well! Leading wealth managers have invested

attitudes and expectations to the WM

The rewired investor industry; also influencing is how older

heavily in new digital experiences and tools to empower investors

and their advisers. However, we have seen only the beginning of

investors purchase and consume

this transformation.

wealth services.

HIGH IMPACT

Most successful robo-advisers shifted early from B2C to B2B2C

models in partnerships with established broker-dealers and large

Science- vs. human- With the rise of robo-advisers, new

advisory firms. These larger firms have been designing hybrid

combinations of science- and human-based

based advice models that leverage advanced analytics and AI to empower

advisory models have emerged.

advisers and improve on the manufacturing and delivery of

financial advice.

Investors value holistic advice on how

Holistic goals- Almost every wealth manager has adopted some version of goals-

to achieve multiple, often conflicting, goals

based advice and has started to automate and digitally deliver

based advice through a range of investment

goals-based planning.

and funding strategies.

Not much progress here in terms of helping customers better

Longevity concerns increasingly are or prepare for retirement or manage through a decumulation phase.

Catching the should be at the heart of client–adviser But longevity remains a key concern of many investors with new

retirement wave conversations, even years ahead tools to nudge customers to save and plan earlier in life. Leading

of retirement. firms have positioned their brands around some notion of

“safe retirement.”

MEDIUM IMPACT

The rising cost of Increasing regulatory burdens and rising Although the DOL Fiduciary rule was not enforced, the industry

risk and increasing costs of risks pose new challenges to WM continues to move toward Best Interest standards. The new SEC

regulation burden firms and their parent companies. Reg BI rule is a case in point.

Most successful robo-advisers have been co-opted by large wealth

New firms and new business models as well managers into partnerships. Insurance companies and retirement

New competitive as renewed commitment by incumbent providers have started to move more decisively into financial

WM firms will drive higher intensity of planning and wealth management. Banks have invested in digital

patterns competition for the same clients and the WM capabilities and are in a better position to fight back against

same assets. large asset managers, although the latter continue to be relentless

in executing against their vision and continue to grow market share.

Big data and advanced analytics are

Despite significant investments in upgrading their data

on the cusp of transforming the WM

infrastructure and enabling big data capabilities, large wealth

Analytics and big data industry, with new ways to engage with

managers have been slow to articulate use cases, build proofs of

clients, manage client relationships, and

concept, and actually develop predictive or algorithmic analytics.

manage risks.

LOW IMPACT

Somewhat to our surprise, product innovation has been fairly

Democratization of Retail investors are demanding

limited in this space in the last several years. There is growing

access to the same asset classes and

asset classes and investment strategies as high-net-worth

consensus that the alpha that matters to mass affluent and mass

strategies market investors is created through matching goals with investment

or institutional investors.

strategies, more than accessing higher return products.

Two demographic trends: (1) Advisers are

It is the nature of demographic trends to work their way slowly but

The aging of advisers aging and leaving the industry faster than

steadily through the industry. We have only seen the beginning

firms are replacing them; (2) Wealth is about

and transfer of wealth of the wave, with some wealth managers feeling the pinch as they

to change hands, upsetting established

struggle to connect with a new generation of investors.

client–adviser relationships.

This is a challenging macro-

The macro- The investing environment has stabilized and recovered faster

environment for investors and their

than retail investors anticipated, with several years of strong equity

environment advisers to find the right return/risk

returns and real estate gains.

combinations.

4

The future of wealth management revisited

Design principles shaping experience

As their digital propensity continues With these principles applied to digital

to rise, retail investors increasingly experiences, it is possible to optimize a

view experience, rather than product balance of human and machine interaction

offerings, as the differentiating factor with investors, dispelling the polarizing

for WM firms. In the past few years, their notion of “humans vs. machine.” Investors

expectations have greatly elevated. Our are now able to intuitively trust machine-

2017 paper described the kind of digital based advice as much as a person. For

experience that investors have come to instance, a “human” experience is one

expect from their advisory firms: (1) sentient, that treats the client as a human being

intelligent, and highly engaging; (2) human, who’s capable of having feelings of anxiety

modern, transparent, and trusted; and (3) whenever the market is volatile, irrespective

highly automated, frictionless, integrated, of whether the firm reassures the client

and collaborative. Many WM firms used through a timely phone call from a person

these characteristics as “design principles” or a tailored digital communication

to guide the development of compelling generated by a next-best-action algorithm.

digital experiences for their clients. In fact, The important point is to acknowledge

they found that the same “north star” and address the investor’s feelings in real

applies to all wealth tiers, from mass market, time. Similarly, investors expect to receive

retail customers to high-net-worth clients, “intelligent” advice rooted in the best

with variations in experience delivery, tools, finance theory, regardless of whether that

and functionalities. advice is delivered by a finance expert or

an automated advice engine that leverages

industry-leading finance algorithms.

5The future of wealth management revisited

The FA experience reimagined

Investors are not the only ones who •• Smart (i.e., intelligent, sentient, and Such a compelling experience for advisers

expect more compelling digital highly engaging): FAs require tools that and their teams can be enabled through a

experiences; financial advisers (FAs), make them “smarter” with next-best- variety of functionalities, applications, and

product specialists, and administrative action algorithms, investment ideas, and tools (see figure 3). WM firms that have

personnel at WM firms are no different. content curated to their clients; their prioritized the creation of compelling digital

In fact, FAs expect the same high-level- tools need to be integrated with client experiences for their employees have often

experience characteristics, which we now apps to allow for continuous dialogue found it well worth the effort. In addition to

categorize within the overarching terms of and exchange of ideas, enabling the co- increasing their workforce productivity, it

efficiency, intelligence, and trustworthiness creation by FAs and their clients of client became easier to hire, retain, and energize

(see figure 2): profiles, plans, and strategies with real- the best talent in the industry.

time visualization of emerging output.

•• Efficient (i.e., highly automated, •• Trustworthy (i.e., human, modern,

frictionless, integrated, and trusted, and transparent): FAs expect

collaborative): FAs want to be more experiences that are customized to their

effective and efficient with an integrated personal needs; they count on their home

set of capabilities and the automation of office and support functions to back them

many of their tasks. Integration enables up and make them look good in front of

them to access their tools through desktop their clients—not to micromanage them;

and mobile devices; empower themselves and they need to be able to run advanced

with guided workflows and research and queries to analyze their book of business,

query tools; and help their entire team to access best practices, and get marketing

work as a unit to better serve their clients. support to grow their business.

6The future of wealth management revisited

Figure 2. The experience advisers and their clients want

What investors want (CX) What advisers want (AX)

•• Everything is easy, intuitive, and •• We make your work easier, faster,

efficient better

•• We never stop learning about you so •• You can do your work on your own time,

that we serve you better on all your devices (e.g., phone, tablet,

•• Every interaction counts desktop)

EFFICIENT •• Our people, algorithms, and tools all •• We guide you though your work before

(i.e., highly automated, work for you you have to search for what you need

frictionless, integrated, and •• You experience our team as moving •• We help you and your team work

collaborative) as one together and move as one

•• We anticipate your needs, and you •• We augment your thoughts and intuitions

hear from us before you think of us and arm you with best ideas/insights

•• You learn at your own pace through •• You can engage and advise your clients

simulations and iterations and prospects on a continuous basis

•• We are always available for you, •• You have the tools to co-create with

anywhere, in real time clients and prospects

SMART •• We understand who you are and how

(i.e., intelligent, sentient, and you feel

highly engaging)

•• We treat you as a human being that is •• We understand your unique needs

both rational and emotional and allow you to customize your

•• We appreciate your trust and reward experience

loyalty •• We always have your back and create

•• We are always acting in your best transparency to help you, not to

interest and compliant with all manage you

TRUSTWORTHY regulations •• We help you grow your business the

(i.e., human, modern, trusted, •• Pricing is transparent and value-based way you want to

and transparent)

7The future of wealth management revisited

Figure 3. The end-to-end experience advisers and their teams expect

A X E2E design principles:

How the experience

should feel for FAs and

their teams What this looks like at leading WM firms

e make your work easier,

1. W •• Common, repetitive tasks are automated

faster, better •• You never have to enter the same information twice

•• You don’t have to go looking for the data and insights you need; they are where you need

them, when you need them

•• New tools and enhancements are so intuitive that you don’t need training

•• The system is as fast and stable as best-in-class consumer apps

EFFICIENT

(i.e., ou can do your work on your •• You have access to your entire personalized workstation through mobile, tablet, and desktop

2. Y

own time, on all your devices with a single experience

highly

automated, (e.g., phone, tablet, desktop) •• You can bring your own device when you want to or leverage firm-provided devices

frictionless,

integrated, 3. We guide you through your •• Your needs are anticipated

and work before you have to •• You never have to switch between applications/tabs to perform common tasks and

collaborative) search for what you need workflows

•• You have one search box that delivers results across all platforms and repositories, with

“fuzzy” search and Boolean logic

•• You have real-time guidance at the point you need it, without having to call or search (e.g.,

tool tips, compliance guidance, constructive error messages)

4. W

e help you and your •• You can share and assign tasks with your team, and track progress in real time

team work together and •• Client information and meeting notes are shareable and actionable

move as one •• If a team member is out, another member has the knowledge and visibility to complete their

tasks

5.We augment your thoughts •• You are given new ideas (trading, balance sheet optimization, etc.) and smart suggestions on

and intuitions and arm you where to apply them

with best ideas/insights •• You are offered suggestions on innovative and targeted actions based on big data and

predictive modeling

•• You can view your client’s sentiment and emotional state and are offered ways to act upon it

•• The best finance theory, behavioral science, and market research is automatically embedded

into your workflow

SMART

(i.e., ou can engage and advise

6. Y •• You have compelling, visual tools to engage clients and prospects in deep conversations

intelligent, your clients and prospects •• You are offered compelling, best-in-class, two-way communications tools and content to

on a continuous basis engage with clients the way they like to engage

sentient,

•• Data from client activity and interactions feeds directly into relevant workflows

and highly

•• When a client reaches out, you have all the relevant information you need and can address

engaging)

their concerns—all in in one place

7. Y

ou have the tools to •• You have tools that can be shared with clients to facilitate collaboration, remotely or in

co-create with clients person, in real time

and prospects •• You can run simulations and tweak variables with clients in real time to discuss planning and

solution proposals

•• Plans you create with your client are evergreen, living artifacts, which you and your client can

review and modify in your own time

8. W

e understand your unique •• Your tools and data views are tailored to your role and can be controlled by you

needs and allow you to •• You have one modern, consistent look and feel across all your tools

customize your experience •• You can create your own custom views and reports, share those with others, and select

popular views and reports from a shared repository

9. W

e always have your back •• Issues outside of your control that you and your clients encounter are promptly and

TRUSTWORTHY and create transparency proactively addressed

(i.e., human, to help you, not to manage you •• You can trust us to treat your clients as you treat your clients

modern, •• You have visibility into your clients’ and team members’ actions

trusted, and

transparent) e help you grow your

10. W •• You have access to clear best practices and KPIs that help you optimize your practice

business the way you •• You can track your progress toward custom and suggested measurable goals and KPIs of

want to your choosing

•• You have templated and custom analysis and queries on your book of business

•• You are provided the training, marketing, and product support you need

•• You are suggested growth opportunities based on data, tailored to your book of business

8The future of wealth management revisited

Building a new, scalable architecture

for digital

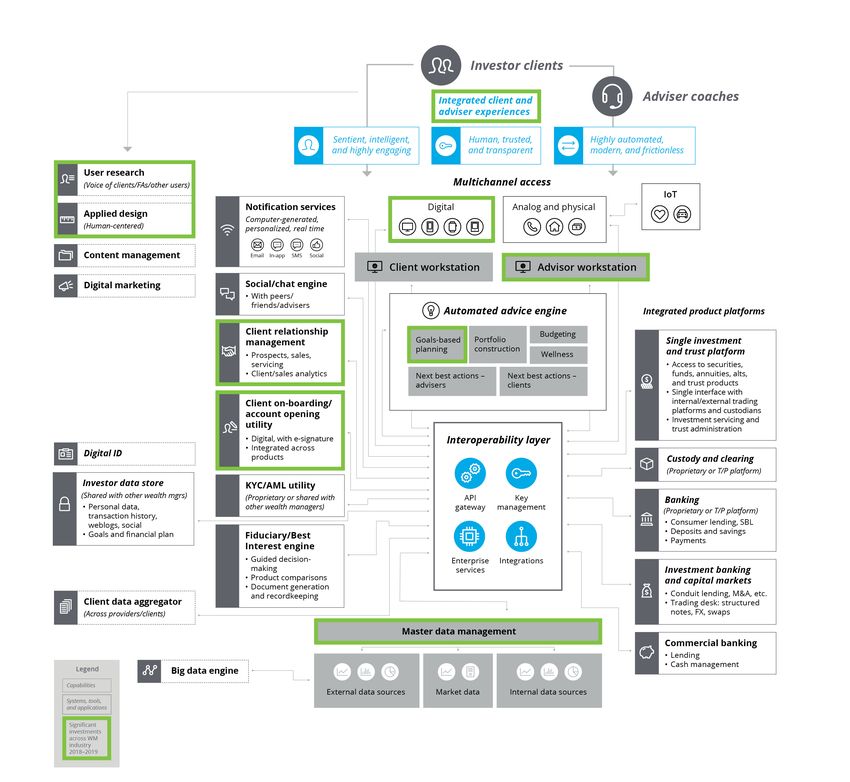

In our 2017 paper, we also outlined a and Asia and have found this functional prioritize capabilities and create a roadmap

functional architecture for a scalable WM architecture to be a reliable guide to the for building and aggregating the right

platform that would enable the digital future (see figure 4 for a slightly updated capability set over time, so as to enable the

adviser of the future. We have reviewed this version; see our 2017 paper for a detailed desired transformation of their wealth

functional architecture with more than 50 description of capabilities).3 In fact, many platform.

wealth managers and a number of WM leading firms adopted a version of this

industry vendors in North America, Europe, functional architecture as a starting point to

Figure 4. A functional architecture for the digital wealth adviser of the future*

Wealth managers are transitioning to digitally enabled,

scalable platforms to empower clients and advisers

with compelling experiences

9

* Source: The digital advisory model of the future, Deloitte, March 2017.The future of wealth management revisited

In the last 18 months, a number of these Financial Services Cloud solution or Together, these capabilities (client

firms have focused their investments Microsoft Dynamics’ product. The digital solutions, state-of-the-art

on a small number of core capabilities more successful CRM projects we have CRM, modern data management, and

in order to kick-start and accelerate seen were thought of as “experience streamlined on-boarding solutions)

their transformation (see figure 5 in the design” projects rather than “technology have been important levers to

appendix). Four capabilities being prioritized implementation” projects. They kicked accelerate the transformation of

by WM firms stand out to us the most: off with a user-centric discovery phase WM platforms; shorten the time to

to (1) define the desired experience for impact on the bottom line; and create

1. New client digital solutions to various user personas through extensive positive dynamics with clients, FAs, and

engage directly with investors and get ethnographic research and (2) create shareholders, so as to continue further

to know them better, initiate a planning a compelling prototype with multiple transformation over the next several years.

relationship with them, provide them wireframes to describe which screens

value through tailored content and users would see and how they would A number of leading WM vendors have

advice, and help them transact on actually engage with the new system also used our functional architecture

their own terms. When these solutions through key journeys. Then the project to articulate where they fit in the

are positioned as complementary to team could proceed to build, test, and transformation of their client firms and,

the traditional client–adviser service launch the new technology solution in some cases, to position themselves as

model, retail investors benefit through through a series of agile sprints with a broader platform-enablers beyond a narrow

enhanced experiences and greater prototype to guide them and maximize set of capabilities for which they were

value. Advisers benefit as well with user adoption and business impact on initially known. A good example of

higher levels of client engagement and the back end. the latter would be a vendor like

satisfaction and increased leverage Salesforce, which can be seen as a CRM

to engage with more clients. Finally, 4. Modern data management (Customer Relationship Management)

WM firms benefit from stronger, more (MDM) capabilities to create an system or a broader platform with a data

institutional relationships with retail interoperability layer on top of legacy interoperability layer linked to an analytics

investors. As they designed, built, and systems, feed data-hungry client and capability, user interfaces, and a

launched these new tablet and phone adviser solutions, and enable the game- container that encompasses most of an

applications, WM firms have had to changing digital experiences that users adviser workstation.

build and embed human-centered want. We have seen firms leverage MDM

design capability at the heart of product platforms like Informatica, or integration

management and transition their services like MuleSoft, to orchestrate

organization from doing digital to and deliver data where it is needed for

being digital.4 key processes on a real-time or periodic

basis. In this way, firms effectively model,

2. Broker-dealers launch new digital store, enrich, and master “objects,” such

applications to engage their affluent as client information, accounts, and

and high-net-worth clients on a transactions, which are then able to be

discovery, planning, and advice journey, moved to where they need to be, so that

while also building a digital lab factory core applications can use the data to

capability to ensure that they will be support the business.

able to continue the development of

compelling digital experiences for their 5. Streamlined on-boarding solutions

clients and FAs. to address common pain points in (1)

converting prospects to clients and

3. State-of-the-art CRM capabilities opening new accounts, as well as bulk

to upgrade sales practices, improve FA conversions as a result of FA and FA-

digital experience and productivity, group transfers; and (2) supporting

and foster growth. In fact, we have requirements for regulatory compliance

seen CRM system implementations or during these processes. As firms

upgrades spreading across the WM standardize the on-boarding process

industry, with large broker-dealers, across lines of business in banking and

high-net-worth private banks, and retail wealth management, they enable clients

managers selecting Salesforce’s to access cash, lending, and investment

products with similar tools.

10The future of wealth management revisited

Much work remains, however, before machine-generated communications and continued pricing pressure across the

fully scalable, digitally enabled WM tailored content delivered to individual value chain, catalyzed by zero-dollar

platforms become a reality. investors. More generally, we have only seen trading and the proliferation of high-yield

For one, it will take more time and the beginning of exponential technologies— cash and money market products. The

investment to create the data such as robotics, cognitive computing, and results of this pressure include increased

infrastructure required to enable such distributed ledgers—applied to wealth merger discussions and proposals in

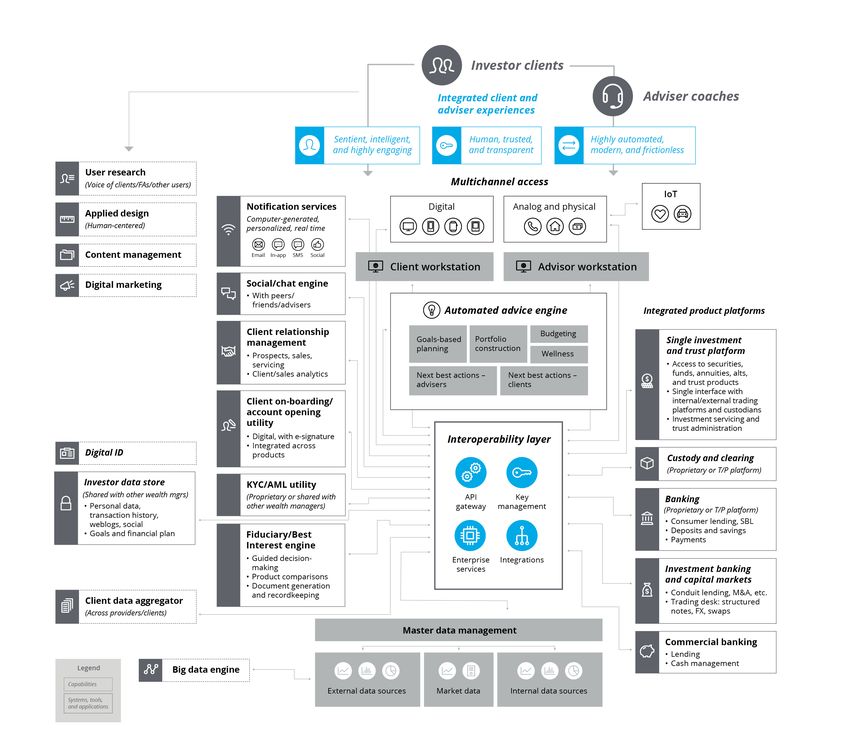

platforms. Furthermore, we have seen management across its capability discount brokerage, custody, and clearing;

only limited progress to date in creating map (see figure 6 in the appendix). acquisitions of banking and trust charters

powerful, automated advice engines by wealth managers; and large WM vendors

with holistic and dynamic planning as Our 2017 paper also called for a new acquiring smaller ones. In our opinion, these

the framework for continuous client economic model and a dramatic increase developments only create more urgency for

engagement; next-best-action algorithms in adviser productivity in response to increased adviser productivity and platform

for investors and their advisers; and real- continued pricing pressure.5 Within efficiency through the digital transformation

time, digital engagement models with the last couple of years we have seen we are discussing in this update.

11The future of wealth management revisited

Transformation in progress:

More emerging ideas and trends

With the adoption of new functional we believe that shared, integrated the pressure to close a deal within a certain

architecture transforming the current experiences between investors and their time frame.

environment, we see even more changes advisers along similar digital standards will

coming in the industry. What follows are also increase the convergence of wealth This concept of treating prospects as

five structural trends that we believe will management and retail banking (see below). quasi-clients is part of a larger idea

shape how WM firms compete. to broaden the definition of a client.

2. The rise of the quasi-client: When For instance, some WM firms have started

1. Integration of client and adviser robo-advisers first appeared on the to think through how to turn their client

experiences: As we mentioned, scene some five to seven years ago, they base into networks of like-minded people

leading WM firms have dedicated stumbled onto a new issue. They were and communities of interest, with clients

significant efforts to the development quick to give prospective clients a login becoming quasi-partners.

of compelling digital experiences for that would allow those prospects to

investors and their advisers, utilizing aggregate information across multiple 3. The convergence of retail banking

a human-centered design approach. providers and receive some guidance on and wealth management through

The more forward-looking firms have portfolio construction, tax optimization, advice: Industry observers have been

gone one step further to acknowledge and other investment topics for free. talking about the convergence of wealth

that adviser and client experiences are The issue was that many post-login management and retail banking (RB)

not independent; rather, they should prospects or quasi-clients never for years. Until recently, convergence

support and reinforce each other, aided converted into full-fledged clients by focused mostly on mass affluent

by seamless integration. transferring assets over and paying an customers. Large asset managers with

asset management fee. Robo-advisers retail businesses built lending and cash

For example, through her workstation, an had de facto created a “prospect zone,” management capabilities to cross-sell

adviser can gain line-of-sight into her client’s but they did not quite know how to to their mostly mass affluent, retail

goal-setting and planning digital application, monetize it, beyond some attempts customer base; conversely, retail banks

which enables her to insert herself into the at mining the data and conducting built up their investment product and

conversation at the right time. For another marketing experiments on these advisory capabilities, in an attempt

example, imagine an elevated in-person quasi-clients. to hang on to the same mass affluent

client meeting where an adviser can switch customers who happen to be their most

his tablet app to “client mode” and co-create Today, a few leading wealth managers are profitable retail customer relationships.

a profile with a client, or to “adviser mode” looking to borrow a page from the robo-

in order to communicate notes and next advisers’ playbook and improve on the idea The battlefield has started to shift from

steps with his support team at the office. of a “prospect zone.” The idea is to allow investments and banking products to

Most importantly, adviser experiences prospects and WM firms to exchange value financial advice. With the automation

will be designed with the principal in a way that is meaningful to the prospects of goals-based financial planning and

objective of enabling the right investor while minimally committing the adviser’s budgeting functionalities, more impactful,

experiences at every interaction. In time or resources. These quasi-clients can holistic financial guidance can now be

fact, client and adviser functionalities will stay in the prospect zone and begin to feel digitally manufactured at low cost and

increasingly be built on the same technology like clients as long as they need. With new consumed through compelling digital

platforms and leverage the same advisory digital tools that guide investors through experiences. It is not just mass affluent

frameworks, thus facilitating the integration discovery and planning, as well as curated investors who are interested, but also every

of adviser and investor experiences. As content and some elements of guidance mass market customer. One of the largest

client and FA digital tools connect and that can make for a meaningful value US retail banks plans to offer some form of

increasingly share common platforms, exchange, advisers can nurture a pipeline financial planning and advice to every one

of future clients at very low cost—without of its customers within a few years.

12The future of wealth management revisited

With this trend, we foresee a major banking operations, giving them access Large outsourcing transactions for

structural shift: Financial wellness and to these corporations’ millions of greater focus and efficiency: In the last

wealth management will move to the individual employees via the wellness several years, we have seen most leading

heart of retail banking. RB customer programs of corporate retirement WM firms—even those with a belief of

relationships will no longer be anchored plans. Part of their value proposition proprietary technology and tools ingrained

in transaction accounts but in some form to corporate plan participants is their in their culture—reach out to external

of digital guidance. The digital experience ability to offer the full force of banking vendors for best-in-class point solutions.

around guidance and advice, thus, will be and wealth management in addressing Now, we are seeing some of the same

at the heart of every relationship between participants’ wellness and financial vendors position themselves for broader

US consumers and their retail banks. needs. Some form of digital planning platform plays that enable several capability

and guidance can be the glue that holds domains across the entire value chain .

4. Closed-loop systems to engage together all these disparate products

retirement customers: A closed-loop and offerings within one integrated We have also heard of large potential

system has its benefits, with customers customer experience. outsourcing deals to technology companies

and merchants on the same payments that focus on most of the middle- and

network operated by a single issuer. We believe we’ll see more institutional back-office functions of a large broker-

Universal banks can benefit by keeping retirement, consumer banking, wealth dealer or a large institutional retirement

corporate retirement plan employees management, and commercial banking lines provider. Because of increasing demand for

within the same family as their wealth of business working together. Because it will value-added activities and the reduction

management and banking customers, take significant investments in technology of operation and technology costs over

or within a closed-loop system. These for large, diversified banks to realize this time, we expect to see more of these

large banks have relationships with tens “closed-loop” vision, it will be very difficult large transactions in the future with more

of thousands of corporations through for smaller banks and wealth management industry utilities created in the process.

their institutional retirement business firms to compete.

and their commercial and investment

13The future of wealth management revisited

A long view of transformation

and opportunity

While this paper was never meant to be In looking at this overall picture of

an exhaustive survey of innovation and transformation in wealth management, The risk to wealth management

change in the WM industry, it is hard to we are reminded once again that human

firms is twofold: Slow down

avoid the conclusion that we have witnessed beings tend to overestimate the pace

only the beginning of a massive wave of of change and underestimate the depth their transformation efforts

transformation that is sweeping through the of transformation. The risk to WM firms because the market is not

industry. The sea change will not happen is twofold: Slow down their transformation moving against them as fast as

instantly; we believe the transformation of efforts because the market is not moving expected, or assume that they

WM will take about 10 years. against them as fast as expected; or assume have done enough to date and

that they have done enough to date and

miss the opportunity to truly

The extent of transformation looks to be miss the opportunity to truly transform their

far-reaching for any WM organization. The infrastructure and business model. Great transform their infrastructure

transformation will be led by the customer peril remains if investments in building the and business model.

and the front office. Transformation of the right, digitally enabled, scalable platform

middle- and back-offices then follows front- happen haphazardly, with rushed action or

office transformation to enable compelling insufficient half-measures. To truly adapt to

experiences by way of the necessary and take advantage of fundamental industry

functional architecture. transformation, WM firms must play

the long game.

14The future of wealth management revisited

Appendix

Figure 5. Where wealth managers have invested in the last 18 months*

Leading wealth managers have concentrated their

investments in a subset of capabilities to accelerate

the transformation

* Source: The digital advisory model of the future, Deloitte, March 2017.

15The future of wealth management revisited

Figure 6. Where new technologies fit in

New technologies will enable the wealth management

platforms of the future

Investor clients

Integrated client and Adviser coaches

adviser experiences

Sentient, intelligent, Human, trusted, Highly automated,

and highly engaging and transparent modern, and frictionless

User research

(Voice of clients/FAs/other users) Multichannel access

IoT

Notification services Digital Analog and physical

Applied design

Computer-generated,

(Human-centered) personalized, real time

Content management Email In-app SMS Social

Client workstation Advisor workstation

Digital marketing Social/chat engine

• With peers/

friends/advisers

Automated advice engine Integrated product platforms

Client relationship Budgeting

management Goals-based Portfolio Single investment

planning construction

Wellness and trust platform

• Prospects, sales,

servicing • Access to securities,

• Client/sales analytics Next best actions – Next best actions funds, annuities, alts,

advisers – clients and trust products

• Single interface with

Client on-boarding/ internal/external trading

account opening platforms and custodians

utility • Investment servicing and

• Digital, with e-signature trust administration

Interoperability layer

• Integrated across

Digital ID products Custody and clearing

(Proprietary or T/P platform)

Investor data store KYC/AML utility

(Shared with other wealth mgrs) (Proprietary or shared with API Key Banking

• Personal data, transaction other wealth managers) gateway management (Proprietary or T/P platform)

history, weblogs, social

• Consumer lending, SBL

• Goals and financial plan

Fiduciary/Best • Deposits and savings

Interest engine • Payments

• Guided decision- Enterprise Integrations

making services Investment banking

• Product comparisons and capital markets

• Document generation • Conduit lending, M&A, etc.

Client data aggregator and recordkeeping • Trading desk: structured

(Across providers/clients) notes, FX, swaps

Master data management

Commercial banking

• Lending

• Cash management

Big data engine

External data sources Market data Internal data sources

Exponential technologies

Advanced Visualization Robotics AI, cognitive Machine Cloud Biometrics Distributed Quantum

analytics computing learning computing ledger computing

16The future of wealth management revisited

Authors

Gauthier Vincent Harry Datwani Janet Hanson

Principal Principal Managing Director

US Lead, Wealth & Retirement Sales Transformation Lead Wealth Technology & Operations Lead

Deloitte Consulting LLP Deloitte Consulting LLP Deloitte Consulting LLP

+1 203 905 2830 +1 213 553 1361 +1 704 227 7849

gvincent@deloitte.com hdatwani@deloitte.com jhanson@deloitte.com

Tom Kirk Gordon Smith Josh Uhl

Senior Manager Senior Manager Senior Manager

Wealth Technology Transformation Digital Wealth Lead Wealth Regulatory

Deloitte Consulting LLP Deloitte Consulting LLP Deloitte & Touche LLP

+1 212 436 2986 +1 619 237 6577 +1 212 436 4326

thkirk@deloitte.com gordonsmith@deloitte.com juhl@deloitte.com

Contributors

Rob Heller Aditya Jagtiani

Manager Senior Consultant

Wealth Management Wealth Management

Deloitte Consulting LLP Deloitte Consulting LLP

+1 212 436 3439 +1 212 436 3251

robheller@deloitte.com adijagtiani@deloitte.com

Endnotes

1. 10 Disruptive Trends in Wealth Management, Deloitte Consulting LLP, 2015.

2. The Digital Wealth Manager of the Future, Deloitte Consulting LLP, 2017.

3. The Digital Wealth Manager of the Future, Deloitte Consulting LLP, 2017, pp. 8-9.

4. See Deloitte: Activating the digital enterprise; https://www2.deloitte.com/us/en/pages/human-capital/articles/the-digital-organization.html.

5. The Digital Wealth Manager of the Future, Deloitte Consulting LLP, 2017, p. 12.

17The future of wealth management revisited 18

The future of wealth management revisited

19This communication contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively, the “Deloitte Network”), is, by means of this communication, rendering professional advice or services. Before making any decisions or taking any action that may affect your finances, or your business, you should consult a qualified professional adviser. No entity in the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies on this communication. Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. In the United States, Deloitte refers to one or more of the US member firms of DTTL, their related entities that operate using the “Deloitte” name in the United States, and their respective affiliates. Certain services may not be available to attest clients under the rules and regulations of public accounting. Please see www.deloitte.com/ about to learn more about our global network of member firms. Copyright © 2020 Deloitte Development LLC. All rights reserved.

You can also read