The JPMorgan Smaller Companies Investment Trust plc - July 2020

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

The JPMorgan Smaller Companies Investment Trust plc July 2020 Georgina Brittain, Portfolio Manager Katen Patel, Portfolio Manager FOR PROFESSIONAL CLIENTS | NOT FOR RETAIL USE OR DISTRIBUTION

Agenda The case for UK mid & small caps UK market outlook Investment process The JPMorgan Smaller Companies Investment Trust plc 2 | FOR PROFESSIONAL CLIENTS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

The case for UK mid & small caps A compelling long-term asset class 3 | FOR PROFESSIONAL CLIENTS | NOT FOR RETAIL USE OR DISTRIBUTION

Long term performance of UK mid and small caps

Cumulative returns

1,800

1,600

S&P 500

FTSE 250 (ex IT)

1,400 Russell 2000

MSCI Europe (ex UK) Small Cap

1,200 MSCI Europe (ex UK)

MSCI AC Asia Pacific (ex Japan)

1,000 MSCI Emerging Markets

FTSE All-Share

TOPIX

800

600

400

200

0

'95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20

… long term returns amongst the best in the world

Source: J.P. Morgan Asset Management, Bloomberg. All series are rebased to 100 as at 31 December 1994 to 30 June 2020. All indices in GBP and include reinvested dividends.

Indices do not include fees or operating expenses and are not available for actual investment.

Past performance is not a reliable indicator of current and future results.

4 | FOR PROFESSIONAL CLIENTS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

Opportunities for extraordinary growth

Innovators or disruptors

Nimble business models

Rapidly growing new markets

OneSavings Oxford

Future Spirent

Bank Instruments

Image source: Shutterstock

The securities above are shown for illustrative purposes only. Their inclusion should not be interpreted as a recommendation to buy or sell.

5 | FOR PROFESSIONAL CLIENTS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

Mergers & Acquisitions

Sell-side Buy-side

Percentage of index acquired FTSE 100

FTSE 250

Smaller companies Larger companies

12%

Small Cap

FTSE 100 avg.

10% Corporate

Family ownership

ownership

8%

6%

Less efficient or Fewer opportunities

4%

sub-scale for business

businesses improvement

2%

0%

Limited overall Regulatory and

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019 market impact logistical challenges

Source: Liberum, Bloomberg, as at 31 December 2019.

Past performance is not a reliable indicator for current and future results.

6 | FOR PROFESSIONAL CLIENTS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

Opportunities for active managers in under-researched companies

Rolling average analyst coverage by market cap

25

20

FTSE 100 FTSE 250 FTSE Small Cap

15

10

5

0

£m

... Average of 18 analysts covering each FTSE 100 company

Average of 10 analysts covering each FTSE 250 company

Average of 5 analysts covering each FTSE Small Cap company

Source: Liberum, Datastream. As at 7 January 2020.

7 | FOR PROFESSIONAL CLIENTS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

The UK Market Outlook 8 | FOR PROFESSIONAL CLIENTS | NOT FOR RETAIL USE OR DISTRIBUTION

Economic outlook: pandemic woes visible to all, outlook beyond unclear

UK retail sales and consumer confidence UK GDP growth forecasts for 2020 at historic lows

8 10 15%

10%

0 0

Real GDP, YoY %

5%

-8 -10

0%

-16 -20 -5%

UK Retail Sales % YOY

(LHS) NIESR, -7.2%

-24 -30 -10% IMF, -10.2%

GFK Consumer OBR, -12.4%

Confidence (RHS) -15%

-32 -40 1900 1920 1940 1960 1980 2000 2020

2005 2008 2011 2014 2017 2020

Outturn IMF OBR NIESR

UK Purchasing Managers Index Brent crude oil price ($/barrel)

70

100

60

80

50

60

40

Manufacturing PMI 40

30 Services PMI

Construction PMI 20

20

0

10 2015 2016 2017 2018 2019 2020

2005 2008 2011 2014 2017 2020

Sources: top left chart: ONS, GfK, with data from January 2005 to June 2020; bottom left chart: Bloomberg, data from January 2005 to June 2020; top right chart: Panmure Gordon, data as of 14th July 2020; bottom right

chart: Bloomberg, data from January 2015 to July 2020. Opinions, estimates, forecasts, projections and statements of financial market trends are based on market conditions at the date of the publication, constitute our

judgment and are subject to change without notice. There can be no guarantee they will be met.

Past performance is not a reliable indicator of current and future performance.

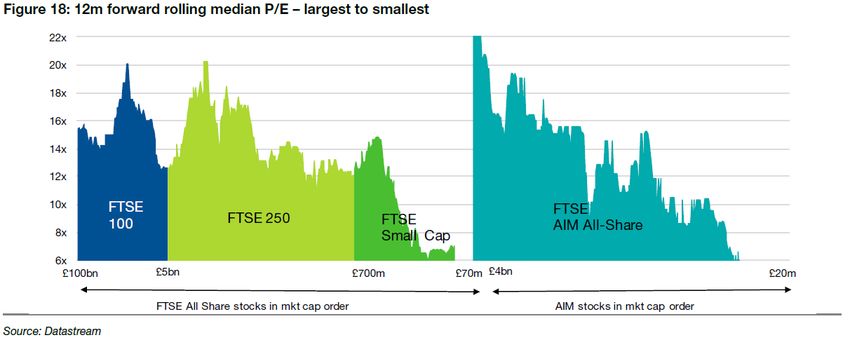

9 | FOR PROFESSIONAL CLIENTS ONLY – NOT FOR RETAIL USE OR DISTRIBUTIONUK market valuation

FTSE 100 FTSE 250 NSCI & AIM

2021 P/E ratio (ex loss-makers) 13.4x 13.3x 11.7x

2021 median earnings growth 12.1% 19.0% 19.6%

2021 dividend yield (ex non-pay) 4.5% 3.5% 3.6%

12m forward rolling median P/E – largest to smallest

Source: Top table is from Peel Hunt as at 13 July 2020; bottom chart is from Liberum as at 10 September 2019, using Datastream. Opinions, estimates, forecasts,

projections and statements of financial market trends are based on market conditions at the date of the publication, constitute our judgment and are subject to change

without notice. There can be no guarantee they will be met.

10 | FOR PROFESSIONAL CLIENTS ONLY – NOT FOR RETAIL USE OR DISTRIBUTIONGlobal earnings expectations and equity valuations GTM – UK | 48

Consensus estimates for global earnings per share growth Global forward price-to-earnings ratios

% change year on year, earnings per share estimates x, multiple

50 75x

40x

45 2020 2021

Current

40 35x

35 Range since 1990

30 Average since 1990

25 30x

20

15 25x

10

Equities

5

20x

0

-5

-10 15x

-15

-20 10x

-25

-30

5x

-35

-40

-45 0x

US Europe UK Japan EM US Europe UK Japan EM

ex-UK ex-UK

Source: (Left) FTSE, IBES, MSCI, Refinitiv Datastream, Standard & Poor’s, TOPIX, J.P. Morgan Asset Management. MSCI indices are used for Europe ex-UK and

EM. UK is FTSE All-Share, US is S&P 500 and Japan is TOPIX. Data used are in local currency, except for EM, which is in US dollars. (Right) IBES, MSCI, Refinitiv

Datastream, Standard & Poor’s, J.P. Morgan Asset Management. MSCI indices are used for all regions/countries (due to data availability), except for the US, which is

represented by the S&P 500. Past performance is not a reliable indicator of current and future results. Guide to the Markets - UK. Data as of 22 June 2020.

Opinions, estimates, forecasts, projections and statements of financial market trends are based on market conditions at the date of the

publication, constitute our judgment and are subject to change without notice. There can be no guarantee they will be met.

11Are UK equities still cheap?

UK market cheap on price to book and near the lows of the 1980s

UK Market Price to Book (x)

UK Market Price To Book Value Max Min Median

4.0

3.5

3.0

2.5

2.0

1.5

1.0

0.5

0.0

1980 1990 2000 2010 2020

Source: Datastream, Morgan Stanley Research. Data from 1 January 1980 to 23 June 2020..

Past performance is not a reliable indicator of current and future results

12 | FOR PROFESSIONAL CLIENTS ONLY – NOT FOR RETAIL USE OR DISTRIBUTIONInvestment Process 13 | FOR PROFESSIONAL CLIENTS | NOT FOR RETAIL USE OR DISTRIBUTION

What do we look for in a company?

For every stock we ask 3 questions:

IS IT A GOOD BUSINESS?

We consider the quality of the company through its profitability, sustainability of earnings and capital allocation discipline

IS IT ATTRACTIVELY VALUED?

We look at a company’s valuation to assess if its future prospects have been incorrectly estimated by the market

IS THE OUTLOOK IMPROVING?

Assessing the operational momentum of the business and how is this being reflected in expectations

THREE COMPLEMENTARY CONSIDERATIONS THAT HELP PREDICT STOCK RETURNS

14 | FOR PROFESSIONAL CLIENTS ONLY – NOT FOR RETAIL USE OR DISTRIBUTIONStock specific considerations: A differentiated approach to fundamental analysis

Focused fundamental research on the drivers of share prices

Stock specific considerations

2,945 820 408 60

Company newsflow Fundamental Company meetings IPOs and Placings

(Comments written) revisions evaluated

Source: J.P. Morgan Asset Management, Data for International Equity Group – European Behavioural Finance Team for calendar year 2019 for UK equities only.

15 | FOR PROFESSIONAL CLIENTS ONLY – NOT FOR RETAIL USE OR DISTRIBUTIONInvestment philosophy

We believe that attractively valued, high quality stocks with

positive momentum outperform the market

VALUE QUALITY MOMENTUM

Themes: Themes: Themes:

- Out of favour stocks with - Market leaders - Structurally growing end

catalysts markets

- High return of capital

- Cyclical end market recovery - Bolt-on acquisition strategy

- Disciplined capital allocation

- High cash generation - Disruptive technology

The numbers: The numbers: The numbers:

FCF yield Trust Index ROIC Trust Index Momentum Trust Index

Small Cap 6.5% 3.7% Small Cap 13.5% 9.3% Small Cap -13.2% -17.7%

Source: J.P. Morgan Asset Management, FactSet, as of 30 June 2020. Figures reported are weighted medians. Figures shown are Value = Free Cash Flow Yield, Quality = return on invested

capital, Momentum = 3 month historic earnings per share revisions. Small Cap is the JPMorgan Smaller Companies Investment Trust plc, whose index is Numis Smaller Companies plus AIM ex

IT.

16 | FOR PROFESSIONAL CLIENTS ONLY – NOT FOR RETAIL USE OR DISTRIBUTIONA deep understanding of the portfolio’s positioning

A powerful tool for visualizing exposures

Red flags

Liquidity

analysis

Style exposures

Fundamental

adjustments

Top stock actives

Alpha drivers

ESG rating

17 | FOR PROFESSIONAL CLIENTS ONLY – NOT FOR RETAIL USE OR DISTRIBUTIONThe investment process in action – Dunelm

High quality business Dunelm– Total Return

• UK Market leader in fragmented homewares category GBP Share Price Consensus EPS Estimate GBP

• Improving product range and well-managed supply chain 14 0.80

13 0.75

0.70

Attractively valued 12

0.65

11

• Consistently cash generative and strong balance-sheet 0.60

10 0.55

• Disciplined approach to shareholder returns

9 0.50

0.45

Promising outlook 8

0.40

7 0.35

• Market share gains driving multi-channel revenue growth

6 0.30

• Margin expansion potential Jun 2019 Sep 2019 Dec 2019 Mar 2020 Jun 2020

Source: J.P. Morgan Asset Management, Bloomberg. Share Price 30 June 2019 – 30 June 2020. * The consensus EPS estimate is an arithmetic average of selected broker estimates for earnings per

share of the company for the year shown. The companies/securities above are shown for illustrative purposes only. Their inclusion should not be interpreted as a recommendation to buy or sell..

Past performance is not a reliable indicator of current and future results.

18 | FOR PROFESSIONAL CLIENTS ONLY – NOT FOR RETAIL USE OR DISTRIBUTIONThe investment process in action – Computacenter

High quality business Computacenter – Total Return

• Global IT infrastructure/services provider. High returns on GBP Share Price Consensus EPS Estimate GBP

capital and track record of outperforming market estimates 20 0.96

0.94

18

Attractively valued 0.92

16

• Strong cash-flow generation, high dividend growth and net 0.90

cash balance sheet 14 0.88

0.86

12

Promising outlook 0.84

10

0.82

• Benefitting from a multi-year trend of digital investment by

8 0.80

enterprise and public-sector clients Jun 2019 Sep 2019 Dec 2019 Mar 2020 Jun 2020

Source: J.P. Morgan Asset Management, Bloomberg. Share Price 30 June 2019 – 30 June 2020. * The consensus EPS estimate is an arithmetic average of selected broker estimates for earnings per

share of the company for the year shown. The companies/securities above are shown for illustrative purposes only. Their inclusion should not be interpreted as a recommendation to buy or sell.

Past performance is not a reliable indicator of current and future results.

19 | FOR PROFESSIONAL CLIENTS ONLY – NOT FOR RETAIL USE OR DISTRIBUTIONThe JPMorgan Smaller Companies Investment Trust plc 20 | FOR PROFESSIONAL CLIENTS | NOT FOR RETAIL USE OR DISTRIBUTION

Fund summary

JPM Smaller Companies Investment Trust plc

Annualised performance to 30 June 2020

Georgina Brittain Katen Patel

Portfolio Manager Portfolio Manager

Experience: 25 / 25 Experience: 15 / 7 15% 13.11

Trust Benchmark

9.31

10%

6.98 7.22

Nimble and Portfolio size £223.4m 5%

2.11

focused No. of stocks 88 0.08

0%

-5% -3.54

Discount to NAV 13.4%

Inexpensive

Historic dividend yield 1.6% -10%

-10.74

-15%

Strong long term outperformance 1 year 3 years p.a. 5 years p.a. 10 years p.a.

Performance 1st in peer group over 3 years and over 1 Excess

+12.12 +10.91 +5.00 +3.47

year* return (%)

Source: J.P. Morgan Asset Management. As at 30 June 2020 unless otherwise stated. Experience: Industry/Firm as of 31 March 2020. NAV returns are net of fees, in GBP, with income reinvested.

Prospective dividend yield is indicative and based on mid market prices, and include the declared and net prospective dividends for the current financial year. Benchmark changed from the FTSE

Smaller Companies Index ex IT to the NUMIS Smaller Companies Index plus AIM ex IT on 1st January 2019. *Peer group of 26, Morningstar peer quartile ranking within EAA CE UK Small-Cap Equity

universe. Morningstar™ rankings/universe: © Morningstar. All Rights Reserved.

Past performance is not a reliable indicator for current and future results .

21 | FOR PROFESSIONAL CLIENTS ONLY – NOT FOR RETAIL USE OR DISTRIBUTIONPerformance attribution

Stock: 11.68

JPM Smaller Companies Investment Trust plc Attribution summary

Sector: -0.17

for 12 months ending 30 June 2020 Benchmark

Numis Smaller Companies

plus AIM (ex IT) Index

Stock attribution

Relative Stock Impact Relative Stock Impact

Top 10 contributors Top 10 detractors

weight (%) return (%) (%) weight (%) return (%) (%)

Games Workshop Group 4.07 65.73 2.41 Vistry Group 1.33 -25.28 -0.68

Avon Rubber 2.07 136.87 1.89 OneSavings Bank 2.90 -25.66 -0.64

Team17 Group 2.25 88.62 1.57 Dart Group 1.84 -1.24 -0.63

Judges Scientific 3.01 52.52 1.52 ITM Power Not Held 686.12 -0.52

Future 3.38 31.78 1.41 Centamin -0.63 9.85 -0.50

Dunelm Group 2.86 37.76 1.13 Ferrexpo -0.15 -48.98 -0.48

Spirent Communications 1.80 61.26 0.98 Go-Ahead Group 0.28 -59.69 -0.45

Liontrust Asset Mgmt 1.42 88.25 0.95 GlobalData Not Held 89.69 -0.45

Codemasters Group Holdings 1.66 50.44 0.83 TBC Bank Group 0.82 -43.70 -0.43

Ei Group 0.75 43.34 0.67 Rank Group 0.31 -36.21 -0.35

Source: Factset. Data is gross of fees in GBP. Attribution results are for indicative purposes only. The portfolio is actively managed. Holdings, sector weights, allocations and leverage, as applicable, are

subject to change at the discretion of the Investment Manager without notice. Past performance is not a reliable indicator of current and future results.

22 | FOR PROFESSIONAL CLIENTS ONLY – NOT FOR RETAIL USE OR DISTRIBUTIONPortfolio positions

Numis Smaller Companies plus

JPM Smaller Companies Investment Trust plc Benchmark AIM (excluding Investment

as of 30 June 2020 Companies) Index

Top 10 overweight positions

Stock Portfolio weight (%) Benchmark weight (%) Relative position (%)

Games Workshop Group 4.8 0.0 4.8

Dunelm Group 4.5 0.0 4.5

Future 4.6 0.7 3.9

Team17 Group 3.6 0.4 3.2

Judges Scientific 3.3 0.2 3.1

Computacenter 3.1 0.0 3.1

Softcat 2.5 0.0 2.5

OneSavings Bank 2.2 0.0 2.2

Pets At Home 2.8 0.7 2.2

Avon Rubber 2.7 0.5 2.1

Total 34.1 2.5 31.6

Source: J.P. Morgan Asset Management, Factset. The investment trust is actively managed. Holdings, sector weights, allocations and leverage, as applicable, are subject to change at the discretion of

the Investment Manager without notice.

23 | FOR PROFESSIONAL CLIENTS ONLY – NOT FOR RETAIL USE OR DISTRIBUTIONPortfolio positions

Numis Smaller Companies plus

JPM Smaller Companies Investment Trust plc Benchmark AIM (excluding Investment

as of 31 December 2019 Companies) Index

Top 10 overweight positions

Stock Portfolio weight (%) Benchmark weight (%) Relative position (%)

Games Workshop Group 4.5 0.8 3.7

OneSavings Bank 3.7 0.4 3.3

Future Plc 3.7 0.5 3.2

Judges Scientific 3.2 0.1 3.1

4Imprint Group 3.4 0.4 3.0

Forterra Plc 2.8 0.3 2.5

Dunelm Group 3.5 0.9 2.5

Dart Group 3.5 1.0 2.5

MJ Gleeson 2.6 0.2 2.4

Marshalls 3.1 0.7 2.3

Total 34.0 5.3 28.5

Source: J.P. Morgan Asset Management, Factset. The investment trust is actively managed. Holdings, sector weights, allocations and leverage, as applicable, are subject to change at the discretion of

the Investment Manager without notice.

24 | FOR PROFESSIONAL CLIENTS ONLY – NOT FOR RETAIL USE OR DISTRIBUTIONPortfolio positions

Numis Smaller Companies

JPMorgan Smaller Companies Investment Trust plc plus AIM (excluding

Benchmark

as of 30 June 2020 Investment Companies)

Index

Active and absolute sector positions

Relative to benchmark (%)

12 11.2

10

8

6.2

6

4 3.3 3.0 2.8

2

0

-2

-1.9 -2.1 -2.3 -2.4

-4 -3.1

Leisure General H'h' Software Media Pharmaceuticals & Oil Support Construction Mining

Goods Retailers Goods & Biotechnology & Services &

& Comp. Gas Materials

Home Serv. Producers

Construct.

Portfolio

Weight (%)

13.6 10.1 5.2 10.8 7.8 2.5 1.9 4.4 2.4 2.0

Source: J.P. Morgan Asset Management, Factset. The investment trust is actively managed. Holdings, sector weights, allocations and leverage, as applicable, are subject to change at the discretion of

the Investment Manager without notice.

25 | FOR PROFESSIONAL CLIENTS ONLY – NOT FOR RETAIL USE OR DISTRIBUTIONCOVID-19: Update

The Smaller Companies investment trust is focused on bottom up stock selection and that has not changed as a result of the

COVID-19 crisis.

Paying particular attention to firms balance sheets and cash flow, but this is not a deviation from how we pick stocks.

Picking the long term winners is our area of expertise, not timing the market.

Assessing relative upside on a multi-year approach to determine new buys and sells for the portfolio

Revenue reserves:

Smaller Companies revenue reserve as at 31st January 2020 was £ 6,004,000 which provides approximate cover of 1.4x

the 2019 dividend rate.

Source: J.P. Morgan Asset Management as of 13 May 2020. Opinions, estimates, forecasts, projections and statements of financial market trends are based on market conditions at the date of the

publication, constitute our judgment and are subject to change without notice. There can be no guarantee they will be met.

26 | FOR PROFESSIONAL CLIENTS ONLY – NOT FOR RETAIL USE OR DISTRIBUTIONCOVID-19 – Portfolio changes

Buys

– Adding to existing high conviction holdings – Media, Construction, Retail, Technology

– New opportunities created by share price volatility – Industrials, Leisure, Technology

Sells

– Position reduction due to relative valuation – Leisure, Construction, Real estate

– Sold due to preferred opportunities elsewhere – Transport, Financials

Gearing

– Reduced to provide firepower for opportunities (placings/share price volatility)

Already starting to be utilized

Highly selective participation in placings to date

Source: J.P. Morgan Asset Management as of 30 June 2020. The portfolio is actively managed. Holdings, sector weights, allocations and leverage, as applicable, are subject to change at the discretion

of the investment manager without notice.

27 | FOR PROFESSIONAL CLIENTS ONLY – NOT FOR RETAIL USE OR DISTRIBUTIONLong term investment performance

Cumulative returns 30 June 2020 (%)

450%

400% JPMorgan Smaller Companies Investment Trust NAV

350% Benchmark

300%

250%

200%

+107%

150%

100% Share price discount to NAV is 13.4%

50%

Oct 2009 Oct 2010 Oct 2011 Oct 2012 Oct 2013 Oct 2014 Oct 2015 Oct 2016 Oct 2017 Oct 2018 Oct 2019

...long term alpha generation by current portfolio managers

Source: Bloomberg, J.P. Morgan Asset Management. Data from 31 October 2009 – 30 June 2020. Benchmark changed from the FTSE Smaller Companies Index ex IT to the NUMIS Smaller

Companies Index plus AIM ex IT on 1 January 2019. NAV returns are net of fees, in GBP, with income reinvested. All indices in sterling and include reinvested dividends. Indices do not include fees or

operating expenses and are not available for actual investment. Returns are cumulative.

Past performance is not a reliable indicator of current and future performance.

28 | FOR PROFESSIONAL CLIENTS ONLY – NOT FOR RETAIL USE OR DISTRIBUTIONSummary

Opportunities for extraordinary growth by small and mid cap companies

Robust, disciplined process. Established and refined over three decades

Strong long term trust performance vs. benchmark and peers

Past performance is not a reliable indicator of current and future performance.

29 | FOR PROFESSIONAL CLIENTS ONLY – NOT FOR RETAIL USE OR DISTRIBUTIONAppendix 30 | FOR PROFESSIONAL CLIENTS | NOT FOR RETAIL USE OR DISTRIBUTION

Performance

JPMorgan Smaller Companies Investment Trust plc as of 30 June 2020

Annualised performance, net of fees (%)

One Three Five

Three months YTD

year years years

JPMorgan Smaller Comp. NAV (debt at fair value) 22.00 -20.14 0.08 6.98 7.22

JPMorgan Smaller Comp.share price 21.47 -30.16 2.13 10.23 8.29

NUMIS Smaller Companies Index plus AIM ex IT * 19.17 -19.78 -10.74 -3.54 2.11

Excess return (NAV) +2.37 -0.45 +12.12 +10.91 +5.00

Calendar year performance, net of fees (%)

2015 2016 2017 2018 2019

JPMorgan Smaller Comp. NAV (debt at fair value) 20.37 -0.95 31.62 -13.64 49.21

JPMorgan Smaller Comp. share price 26.03 -6.69 36.41 -9.04 67.53

NUMIS Smaller Companies Index plus AIM ex IT * 12.99 12.54 15.61 -13.80 22.14

Excess return (NAV) +6.53 -11.98 +13.85 +0.19 +22.14

Source: J.P. Morgan Asset Management/Morningstar. Net asset value performance data has been calculated on a NAV to NAV basis, including ongoing charges and any applicable fees, with any income reinvested, in

GBP. NAV is the cum income NAV with debt at fair value, diluted for treasury and/or subscription shares if applicable, with any income reinvested. Share price performance figures are calculated on a mid market basis in

GBP with income reinvested on the ex-dividend date. The performance of the company's portfolio, or NAV performance, is not the same as share price performance and shareholders may not realise returns which are

the same as NAV performance. Indices do not include fees or operating expenses and you cannot invest in them. Geometric excess returns. Periods over one year are annualised. *Benchmark changed from the FTSE

Smaller Companies Index ex IT to the NUMIS Smaller Companies Index plus AIM ex IT on 1st January 2019. Past performance is not a reliable indicator for current or future results.

31 | FOR PROFESSIONAL CLIENTS ONLY – NOT FOR RETAIL USE OR DISTRIBUTIONPremium/Discount to NAV

JPM Smaller Companies Investment Trust plc

0

-5

-10

-15

-20

-25

-30

-35

Dec '16 Mar '17 Jun '17 Sep '17 Dec '17 Mar '18 Jun '18 Sep '18 Dec '18 Mar '19 Jun '19 Sep '19 Dec '19 Mar '20 Jun '20

Source: Bloomberg. Data from 31 December 2016 to 30 June 2020.

Past performance is not a reliable indicator for current and future results.

32 | FOR PROFESSIONAL CLIENTS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION5 years' historic gearing level vs. benchmark

JPM Smaller Companies Investment Trust plc

Gearing Level Index

20% 6,000

Month end gearing level - LHS

Old benchmark level - RHS

16%

New benchmark level - RHS

5,000

12%

8%

4,000

4%

0% 3,000

May 15 Sep 15 Jan 16 May 16 Sep 16 Jan 17 May 17 Sep 17 Jan 18 May 18 Sep 18 Jan 19 May 19 Sep 19 Jan 20 May 20

Source: Bloomberg, J.P. Morgan Asset Management

As at 30 June 2020 (weightings exclude cash/cash equivalents). Investment trusts may utilise gearing which will exaggerate market movements both down and up which could mean sudden and large falls in value. For

further details, please refer to the trust’s annual report and accounts. Gearing is the ability to borrow money to invest that money on behalf of the shareholders.

Past performance is not a reliable indicator for current and future returns.

33 | FOR PROFESSIONAL CLIENTS ONLY – NOT FOR RETAIL USE OR DISTRIBUTIONBenefits of mid & small cap strategy in an actively managed closed ended structure

Benefits Reserves provide the ability to smoothing income return

Pence per share

7

Liquid access to a less

No inflows/ outflows Special dividend

liquid asset class

6 Dividend

Earnings per share

5 Net revenue reserves per share (RHS)

Reserves provide the ability

Active use of gearing to

to smoothing income return

enhance returns 4

for shareholders

3

Independent Board of

Higher disclosure 2

Directors provide oversight

1

Share buybacks at a Opportunity for investors to

0

discount to NAV accretive buy shares at a discount to

to shareholders NAV

…with the opportunity for active managers to add value in under-researched companies

Source: J.P. Morgan Asset Management. All figures based on the current trust total shares, after the 5 for 1 rights issue which lapsed in 2017. Data as at 31 December 2019.

Past performance is not a reliable indicator for current and future results.

34 | FOR PROFESSIONAL CLIENTS ONLY – NOT FOR RETAIL USE OR DISTRIBUTIONJ.P. Morgan International Equity Group – Drawing on resources around the world

Malcolm Smith

Head of the International Equity Group

Quantitative Research* Fundamental Research

10 years average industry experience 19 years average industry experience

Nick Horne Mark Ferguson

Head of Global Structured Equity Group Global Head of Equity Research

Christian Pecher David Small

Philippa Clough Asia Head of Research North America Head of Research

Head of Quantitative Research - London 14 Asia Research Analysts 25 North America Research Analysts

7 Quantitative Research Analysts

Maciej Wasilewicz Shumin Huang & Giovanni Carriere

Won Choi Europe Head of Research Emerging Markets Heads of Research

Head of Quantitative Research – New York 13 Europe Research Analysts 29 Emerging Market Research Analysts

7 Quantitative Research Analysts ^^^

10 Product Analysts*

Portfolio Management

19 years average industry experience

56 Portfolio Managers**, supported by a team of 12 Associate Portfolio Managers

Managing Global, International^, Europe & UK Equity Portfolios

Investment Specialists Implementation* Trading & Data Scientists***

19 years average industry experience 19 years average industry experience 21 years average industry experience^^

Frances Gerhold James Ford Kristian West

11 Investment Specialists in Asia, Europe & the US 10 Implementation Specialists 31 Equity Traders

7 Trading Analytics & Strategy

Supported by a team of 14

7 Data Scientists

Data as at 30 June 2020. * Some of the team members have additional PM responsibilities. Quantitative research team for New York includes VP & above **Some of the team members have additional

Implementation, Quantitative Research or Analyst roles. ^ International is Global ex-US. ^^ex-data scientists. *** Trading & Data scientists details are as of March 31, 2020. ^^^ VP & above. Note this

illustrates the resources available and does not necessarily reflect reporting lines

35 | FOR PROFESSIONAL CLIENTS ONLY – NOT FOR RETAIL USE OR DISTRIBUTIONEuropean Small and Mid Cap team

Continental Europe UK Small & Mid Cap

Francesco Conte Guy Anderson Georgina Brittain

Industry: 31 yrs Industry: 18 yrs Industry: 25 yrs

Firm: 21 yrs Firm: 8 yrs Firm: 25 yrs

Ed Greaves Katen Patel Ed Hezlet

Industry: 13 yrs Industry: 15 yrs Industry: 5 yrs

Firm: 9 yrs Firm: 7 yrs Firm: 5 yrs

Jack Featherby Anthony Lynch Manasij Hajra

Industry: 6 yrs Industry:Portfolio implementation

Dedicated team ensures efficient portfolio implementation, in collaboration with our award-winning trading desk

Implementation team Trading team

Guideline management

Corporate actions

Account on/off boarding

Cashflow monitoring

Prime broker interactions

Portfolio reporting

Source: J.P. Morgan Asset Management. Data as at 31 December 2019. 1Markets Choice Awards: a peer-based survey of exchanges, sell-side desks, institutional buy-side investors, hedge funds and

technology providers. 2Financial News Trading & Technology Awards

Past performance is not a reliable indicator of current and future results.

37 | FOR PROFESSIONAL CLIENTS ONLY – NOT FOR RETAIL USE OR DISTRIBUTIONIntegrating ESG into our investment approach

Quantitative ranking Fundamental analysis

Fundamental

analysis to

Third party data sources integrated Bottom-up ESG analysis

understand

into proprietary methodology impact Materiality focus

Data can be incomplete

Improvement / deterioration as

well as absolute score Understand transmission

mechanisms

In-house ‘red flags’ model

– Corporate governance Stewardship

– Forensic accounting Informs scoring

Partnership with specialist ESG team

– Financial distress

What is the impact on shareholder

Challenge value

data

...systematic and explicit consideration of ESG factors throughout the investment process

ESG - Environmental, Social, & Governance.

38 | FOR PROFESSIONAL CLIENTS ONLY – NOT FOR RETAIL USE OR DISTRIBUTIONThe UK Edge Image source: J.P. Morgan Asset Management. 39 | FOR PROFESSIONAL CLIENTS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

Biography

Georgina Brittain, Managing Director, is a portfolio manager for small and mid cap strategies within the J.P. Morgan Asset

Management International Equity Group – Behavioural Finance Team, based in London. Georgina is a fund manager for the JPM

UK Smaller Companies Fund, the JPMorgan Smaller Companies Investment Trust and co-manager for the JPMorgan Mid Cap

Investment Trust. She is also a co-manager for our range of European small cap funds. An employee since 1995, Georgina was

previously an analyst in the UK research department. Georgina obtained an M.A. in Classics from Oxford University, and earned

a Diploma in Law from City University, London. She is a qualified barrister.

Katen Patel, Executive Director, is a portfolio manager for small and mid cap strategies within the J.P. Morgan Asset

Management International Equity Group – Behavioural Finance Team. He is the co-manager of the JPM UK Smaller Companies

Fund, the JPM UK Equity Income Fund, the JPMorgan Smaller Companies Investment Trust and the JPMorgan Mid Cap

Investment Trust. An employee since April 2013, he previously worked at HSBC Bank Plc in a European equity sales role. He

obtained a B.Sc. in Management from the London School of Economics. Katen is a CFA charterholder.

… expertise, experience and the backing of a large group

40 | FOR PROFESSIONAL CLIENTS ONLY – NOT FOR RETAIL USE OR DISTRIBUTIONInvestment objective and risk profile

JPMorgan Smaller Companies Investment Trust plc (the Company) as at September 2019

Investment objective

Aims to provide capital growth from UK listed smaller companies. The Company aims to provide capital appreciation for shareholders from a

diversified portfolio of UK listed small companies, emphasising capital rather than income growth. Returns are principally determined by the

performance of the investments made by The Company, although The Company has the ability to use borrowing to gear the portfolio within the

range of 10% net cash to 15% geared in normal market conditions. Gearing may magnify gains or losses experienced by The Company.

Key Risks

External factors may cause an entire asset class to decline in value. Prices and values of all shares or all bonds could decline at the same time,

or fluctuate in response to the performance of individual companies and general market conditions.

This Company may utilise gearing (borrowing) which will exaggerate market movements both up and down.

This Company invests in smaller companies which may increase its risk profile.

The share price may trade at a discount to the Net Asset Value of the Company.

The single market in which the Company primarily invests, in this case the UK, may be subject to particular political and economic risks and, as

a result, the Company may be more volatile than more broadly diversified Company's.

Companies listed on AIM tend to be smaller and early stage companies and may carry greater risks than an investment in a Company with a full

listing on the London Stock Exchange.

Please refer to the Investor Disclosure Document, latest annual report, and Key Information Document (KID) for more information relating to the Company.

41 | FOR PROFESSIONAL CLIENTS ONLY – NOT FOR RETAIL USE OR DISTRIBUTIONImportant information For Professional Clients only – not for Retail use or distribution. This is a marketing communication and as such the views contained herein do not form part of an offer, nor are they to be taken as advice or a recommendation, to buy or sell any investment or interest thereto. Reliance upon information in this material is at the sole discretion of the reader. Any research in this document has been obtained and may have been acted upon by J.P. Morgan Asset Management for its own purpose. The results of such research are being made available as additional information and do not necessarily reflect the views of J.P. Morgan Asset Management. Any forecasts, figures, opinions, statements of financial market trends or investment techniques and strategies expressed are unless otherwise stated, J.P. Morgan Asset Management’s own at the date of this document. They are considered to be reliable at the time of writing, may not necessarily be all inclusive and are not guaranteed as to accuracy. They may be subject to change without reference or notification to you. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested. Changes in exchange rates may have an adverse effect on the value, price or income of the products or underlying overseas investments. Past performance and yield are not reliable indicators of current and future results. There is no guarantee that any forecast made will come to pass. Furthermore, whilst it is the intention to achieve the investment objective of the investment products, there can be no assurance that those objectives will be met. J.P. Morgan Asset Management is the brand name for the asset management business of JPMorgan Chase & Co. and its affiliates worldwide. To the extent permitted by applicable law, we may record telephone calls and monitor electronic communications to comply with our legal and regulatory obligations and internal policies. Personal data will be collected, stored and processed by J.P. Morgan Asset Management in accordance with our EMEA Privacy Policy www.jpmorgan.com/emea-privacy-policy. Investment is subject to documentation. The Investor Disclosure Document, Key Features and Terms and Conditions and Key Information Document can be obtained free of charge from JPMorgan Funds Limited or www.jpmam.co.uk/investmenttrust. This communication is issued by JPMorgan Asset Management (UK) Limited, which is authorised and regulated in the UK by the Financial Conduct Authority. Registered in England No: 01161446. Registered address: 25 Bank Street, Canary Wharf, London E14 5JP. Material ID: 0903c02a82895403 42 | FOR PROFESSIONAL CLIENTS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

You can also read