THE NEXT BIG THING IN INDIAN APPAREL - cloudfront.net

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

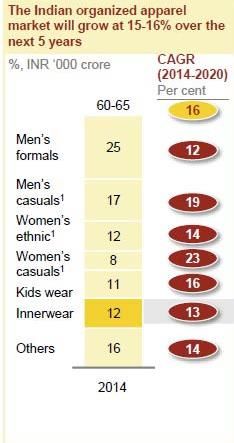

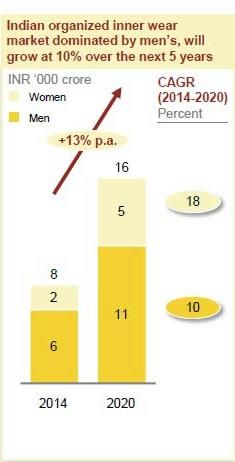

THE NEXT BIG THING IN INDIAN APPAREL Introduction Aditya Birla Fashion and Retail Ltd. (ABFRL) is India’s No.1 Fashion Lifestyle entity and was formed after the consolidation of the branded apparel businesses of Aditya Birla Group comprising Aditya Birla Nuvo Ltd's (ABNL) subsidiaries Madura Fashion & Lifestyle Ltd. and Pantaloons Fashion & Retail Limited (PFRL) in May 2015. ABFRL has been growing at a rate in excess of 20 percent over the last 5 years and hosts India's largest fashion network with over 7,000 points of sale spread across over 375 cities and towns. Madura Fashion & Lifestyle is the custodian of several icons, including the top four fashion brands of India - Louis Philippe, Van Heusen, Allen Solly, and Peter England — each of which clocked MRP sales in the vicinity of INR 1,000 crore. It also includes India's largest fully integrated fashion multi-brand outlet chain Planet Fashion; India's largest premium international brand retailer The Collective and the British fashion icon Hackett London's mono-brand retail in India. A fast-fashion brand for the youth, People is a one-step destination for international and fashion forward styles which is also a brand under ABFRL. Van Heusen in India Van Heusen is India's No. 1 premium lifestyle brand for Men and Women. With a rich heritage of 128 years in the US, the brand entered India in 1990. Over a period of its 25 years of history in India, Van Heusen has emerged as a fashion authority for the ever evolving Indian professionals becoming the go-to source for the latest in fashion trends as well as for expert advice on what to wear, when to wear it and how to wear it. Today, Van Heusen is not only the most preferred work wear brand, but also effortlessly straddles the entire spectrum of occasions like casuals, ceremonial and party wear. The brand embodies the positioning, ‘POWER DRESSING’. Van Heusen customers are the corporate leaders for whom elegance and style are not just fads, but a philosophy. Thus the Van Heusen range is modern, minimalistic and timeless in design and is distinguished by high quality. Van Heusen with its distinctive and fashionable range of products helps corporate leaders create their best impact, as much as for their style as substance. Innerwear – The Next Big thing in Apparel Innerwear happens to be one of the fastest growing apparel category in the country with a current market size of Rs.19,966 Crore and is projected to clock a growth of 13% CAGR for the time period FY14-FY20. 7% of the annual spend on apparels happens to be on innerwear. 63% market share is for women’s innerwear and remaining is for men’s innerwear segment.

In-spite of such huge market, currently, around 65% of the industry happens to be in the un-organized

sector. The premium segment of the market is growing even faster, wherein the market has lot of

potential for growth in coming years. Some popular brands available in the market are Jockey, Rupa, VIP,

Hanes, CK, Lovable etc…

Indian Innerwear

Market

19,966 cr

Women’s

Men’s Innerwear

Innerwear

7,387 cr 12,579 cr

Unorganised Organised Unorganised Organised

~6000 cr ~1,400 cr ~10,500 cr ~2,000 cr

Men’s Innerwear Market

The Men’s Innerwear market is about Rs.7,400 Crore in market size with the organized sector accounting

for more than 75% of the market. The organized market can further be classified into 4 segments based

on positioning and pricing as follows:

1. Super Premium – Brands like Calvin Klein and Tommy Hilfiger are present in the super premium

segment and they have a price point of greater than Rs.500 per inner wear. This segment accounts

for 2% of the market

2. Premium – Between the price range of Rs.200 – Rs.500 per inner wear with brands like Levi’s,

Jockey, UCB, US Polo present in the segment. Accounts for 12% of the market.

3. Mid-premium – Also called the Mass premium segment, this is where Jockey predominantly

operates with Hanes as the other major brand in this segment. Indian brands like Rupa, Amul have

also entered this segment with new brands. This is between the price range of Rs.120 – Rs.200

per inner wear. This segment contributes to 36% of the market.

4. Economy – The biggest segment of all with 50% market share, most of the Indian brands like Amul,

Rupa, VIP, etc. operate in this segment with price points lower than Rs.120 per inner wear

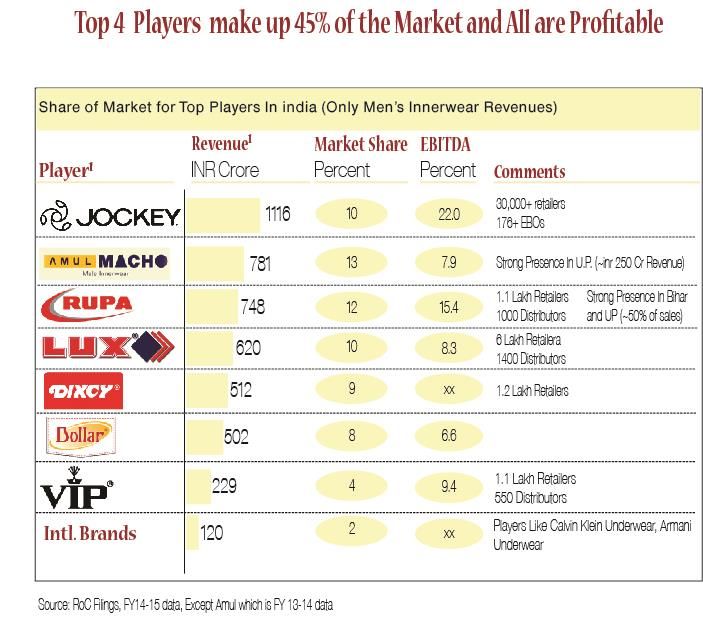

The market share and distribution strength among the different players in India are as below:

JOCKEY India

JOCKEY entered the Indian Innerwear market in the year 1995 through PAGE Industries Ltd. who hold the

licenses for manufacture, distribution and marketing for JOCKEY brand of innerwear in India. In the last

10 years JOCKEY has done a considerable job to become the market leader by upgrading the market from

economy brands to mid-premium and premium brands.

Currently Jockey’s market size for the Men’s and Women’s market are around Rs.1200 and Rs.450 crores

respectively.

JOCKEY’s success comes from a few of the following factors:

1. Distribution Strength – Is present across 1200 cities with around 400 distributors and 30,000+

retail outlets. Also has 176+ Exclusive Branded Outlets (EBOs) titled JOCKEY zones across the

country. All of this has resulted in JOCKEY commanding a 60% market share of IW sales in the

Large Format Stores(LFS). Its widespread distribution network has resulted in Tier 3 Cities

contributing to a staggering 45% of JOCKEY’s annual sales.

2. Brand Positioning – Brand has been positioned in the Premium category through all of its ATL

campaigns however, it has priced in the affordable range. Therefore, it straddles along the

‘Aspirational but affordable’ positioning with Young Indians perceiving the brand as

“International”, “Contemporary” and “Trendy” and sometimes even seen as a status symbol.

3. Marketing & Advertising – JOCKEY has been actively involved in the marketing of its brands

through various ATL and BTL campaigns. It has an annual marketing and ad spend of about 6% of

sales.

4. First Mover advantage – JOCKEY was the first player in the Indian Innerwear segment to

positioning themselves in the mass-premium category and this has been capitalized well through

its far reaching distribution network.ABFRL Enters The Innerwear Market

India’s fashion power-house, ‘Aditya Birla Fashion and Retail Limited’, unfolds a new chapter in the Indian

retail landscape by foraying into the Rs.7000 crore men’s Innerwear & Athleisure market. The company

introduced the all new range of Van Heusen men’s innerwear & athleisure wear in Bangalore, Chennai

and Hyderabad markets with the localised distribution model in October of 2016.

“Aditya Birla Fashion and Retail’s expansion into the two new categories is a strategic progression of the

brand, thereby offering complete fashion solution to the Indian Men. The new segment is based on the

ethos of Fashion, Innovation and Performance as we want to offer stylish, trendy and new-age product to

our consumers. We see big business opportunity in the growing Innerwear and Athleisure segment and

this will significantly contribute to the leadership position of the company.” says Ashish Dikshit, Business

Head of Aditya Birla Fashion & Retail Ltd.

With this new initiative, ABFRL aims to expand in the new segment and has plans to bring a differentiated

product range to Indian customers. The company is also foraying into developing a fast growing category

of Athleisure. Athleisure is an emerging space of multipurpose wear that goes from gym to street to couch.

Crafted on the principles of Fashion, Innovation and Performance, Van Heusen Innerwear & Athleisure

offer sophisticated styling with new and innovative product features for the best in class comfort and fit.

Entry into IW segment - Where should we operate?

Based on the various market studies that were done as part of the exercise in entering this segment,

ABFRL identified considerable opportunity to enter the Premium and Mid Premium segment owing to the

key following factors:

• Premium segment is growing fast and has limited competition

• Anecdotal fatigue with Jockey

• No viable alternative

Consumer Segmentation

The consumers in the Premium and Mid-premium segment can be categorized as follows:

1. Young Aspirers

• Men employed in high paying jobs

• Ambitious and show a keenness to purchase branded innerwear

2. Discerning Urbanites

• Men employed in well-paying jobs

• Evaluate value on a benefit and convenience metric rather than purely on price

• Buy quality stuff and don’t mind paying a premium for it

3. Optimistic Pursuers

• Men from smaller cities who wish to have a lifestyle like metros

• They seek opportunities to experiment with aspirational brands4. Corporate Climbers

• People with limited disposable income

• These people are cautious buyers

Product Range

The brand offers Innerwear range comprising of four collections – Classic, Platinum, Signature and Active.

Each collection has been designed to offer a differentiated range to the various consumer segments

Classic – Classy wardrobe essential offering performance features like “All day fresh” and “Colour fresh”

Platinum – The range offering sophisticated styling and elevated comfort with “Pima cotton”

Signature - Fashion innerwear with “Flexi stretch” feature for body defining fit

Active - True sports innerwear with “Swift Dry” feature.

Athleisure - Crafted with elevated fashion and new age fabric, it also comes with “Smart-Tech” feature

that offers benefits like “Quick Dry”, “Stain Release” and “Anti-stat”, making this a true cross over between

fitness and fashionChannel Mix

Branded innerwear market is predominantly a Multi Branded Outlet (MBOs) led business with Exclusive

Branded Outlet (EBOs) for Innerwear and E-commerce channels occupying only 14% share of business.

MBOs contribute to almost 85% of the sales in the branded IW industry and this makes the distribution

channel look very similar to FMCG industry against that of branded apparel where EBO and LFS are still

the predominant channels for sales. Here, an MBO could be defined as an outlet which sells Multiple

Brands of IW and this could either be a large garment MBO or a neighborhood hosiery store.

Sales Contribution by Channels Sales Contribution by Outlets

2% 1%

13% EBOs 8% 11%

Hosiery Stores

MBOs

Garment Stores

Modern/Regio

85% nal Chains 80% Cosmetic Stores

Others

Purchasing Behavior

Men’s Innerwear tends to be a low involvement category in the minds of most of the Indian consumers.

While the size for the inner wear is pre-determined, because this is an intimate product the brands and

styles are also pre-determined in the minds of the consumer for the most part. Due to this, product and

feature conversations rarely happen between the retailer and the consumer even though there is

considerable scope for both conversation and market upgradation due to the change in consumer

demographics and increase in purchasing power. This exercise becomes all the more difficult in an online

channel.

In the offline channel Men’s Innerwear tends to be predominantly purchased in one of the two following

scenarios:

1. Purchased along with but at the end of outer wear apparel in the same departmental/LFS/hosiery

store

2. Customer visits an IW dedicated MBO and purchases inner wears that are needed for the next 3-

6 months in a single visit

In the online channel, purchase tends to more or less mimic the offline store purchase behavior with some

customers purchasing IW at the end of their shopping and some buying IW dedicatedly for the next 3-6

months. However, here the customer is more aware of the size, brand and style that he purchases

regularly and tends to stick with it as he is more familiar and comfortable with the product.

There is however one more special scenario where the customer purchases Innerwear on an ad hoc basis.

This is driven by a need to travel and the customer usually purchases inner wears one week prior to his

travel.Online Penetration

Currently the sales contribution from the E-com channel is only 1% and this is poised to grow anywhere

between 4% to 7% by 2020. This is primarily due to two factors:

1. The favorable demographic change – with more than two thirds of India’s 120+ billion population to be

in the working age group and one thirds to be within the less than 30 age group

2. Interest penetration along with connectivity speeds is constantly on the rise and this paves the way to

reach a much larger geographical spread than that is ever possible through the brick and mortar retail

route.

These two factors result in younger and more internet savy customers in the coming days, which provides

immense opportunity for VHIW. Branded IW tends to be a business which is pre-dominantly led by the

MBO channel unlike the Branded Apparel space which is dominated by EBO and LFS channels. This

presents a challenge in scaling up – both in terms of time and in terms of resources to be deployed to be

even present in a market.

Online channels like E-com presents us with an opportunity to overcome both these obstacles and reach

out to every single customer in every corner of the country.

Questions:

In the online channel,

1. What are the key success factors to scale up IW selling through E-com channel? What are the

competitive benchmarking on these factors and what are the opportunity for VH to penetrate this

segment fast?

2. Should the inventory planning (product mix, way of packaging) for E-com be different from the

offline channels? If yes, what are the key insights?

3. What is/are the Target Groups for conversion and market upgradation? How to identify the TG

for targeted marketing activities?

4. What should be the marketing plan to create awareness for brand VH, upgrade and/or convert

from the competition brands esp. Jockey?

5. What are the ways to communicate product features like Flexi-stretch and Quick Dry to the

consumers for market upgradation?

For any queries, please write a mail to mflpinnacle@abfrl.adityabirla.comYou can also read