THE RACE BETWEEN THE VIRUS AND THE VACCINES - B.C. ECONOMIC REVIEW AND OUTLOOK February 2021 Ken Peacock Chief Economist & Senior Vice President

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

THE RACE BETWEEN THE VIRUS AND THE VACCINES

B.C. ECONOMIC REVIEW AND OUTLOOK

February 2021 Ken Peacock Dr. David Williams

Chief Economist Vice President, Policy

& Senior Vice President

B.C. ECONOMIC

REVIEW AND OUTLOOK

FEBRUARY 2021

THE RACE BETWEEN THE VIRUS AND THE VACCINES

H I GHL I G HTS

•Global GDP is expected to expand by 5.6% in 2021 and 4.6% •The provincial economy will grow by 4.5% in 2021,

in 2022, following a -2.8% contraction in 2020, according marginally outpacing Canada. A slightly stronger growth

to the Bank of Canada. Globally, vaccination programs are performance is expected in 2022.

being rolled out about six months earlier than previously

expected. It is assumed this will allow many advanced •Global trade has recovered; this backdrop is positive for

economies (except perhaps, Canada) and China to achieve B.C.’s merchandise exports which are trending higher and

broad COVID-19 immunity for their populations by the end will help to underpin the recovery.

of 2021. Other emerging economies would achieve this by

•Provincial employment has almost returned to its pre-

mid-2022.

COVID level; the labour market recovery, however, is very

•The U.S. economy is expected to recover faster than most uneven across sectors.

other advanced economies and to return to full capacity by

•Air transportation and other tourism-dependent industries

the end of 2021, roughly two years earlier than Canada.

remain the epicentre of economic displacement. They will

•Canada’s fiscal response in 2020 was easily the largest in be slow to revive and will weigh on the recovery process.

the world. Nevertheless, Canadian GDP growth is expected

•Retail spending has rebounded and is on a healthy upward

to be only 4.0% in 2021 and 4.8% in 2022, after a large

trajectory.

contraction of -5.5% in 2020. The tepid recovery (relative

to other countries) means the economy will operate •Construction will be a leading growth engine in 2021-22 as

with considerable excess capacity, and inflation will not several large capital projects resume full-scale activity and

sustainably return to its 2% target, until sometime in 2023. governments spend more on infrastructure.

COVID-19 PANDEMIC the course of COVID-19 or delays IMPROVED GLOBAL

The COVID-19 pandemic to date has

the economic recovery currently OUTLOOK, ESPECIALLY FOR

caused over 100 million infections

expected in 2021-2022. THE UNITED STATES

and more than 2.2 million fatalities Canada is in the top third of affected Global GDP growth is expected

worldwide. In terms of fatalities per countries. Out of 152 jurisdictions, to reach 5.6% in 2021 and 4.6% in

capita, the worst hit countries are Canada has the 47th highest fatality 2022, following a 2.8% contraction

Belgium, Slovenia, United Kingdom, rate per capita, at 532 deaths per in 2020, according to the Bank of

the Czech Republic, and Italy. The million persons. This is similar to Canada (Table 1). Many countries

U.S. has the 8th highest fatality rate. Greece, Ukraine, Israel, Costa Rica, are in the grip of a second pandemic

A new variant (B.1.1.7), a mutation Eswatini, and Russia. Canada has wave, compounded by the spread

of the SARS-CoV-2 virus, emerged recorded over 800,000 COVID-19 of the new B1.1.7 strain, that is

in December in the U.K. and has infections and 20,300 fatalities, proving considerably worse than the

since been reported in over 30 the majority of which have been first wave in respect of cases and

more countries, including Canada. concentrated in a few provinces fatalities.

It remains to be seen whether the (Figure 1). B.C. accounts for around

Despite the reintroduction of social

arrival of the new variant alters 9% of cases and 7% of deaths

lockdowns, the economic impact

nationally.

Where Leaders Meet to Unlock BC’s Full Potential | www.bcbc.com

B.C. ECONOMIC

REVIEW AND OUTLOOK FEBRUARY 2021

appears to be less disruptive than

TA BL E 1 : G LO B A L E CO N O MI C F O R E C AST

during the first wave because of ( A N N UA L % C H A N G E I N R E A L G DP )

extraordinary fiscal and monetary

support already in place and because 2019 2020f 2021f 2022f 2023f

people have adapted to new ways

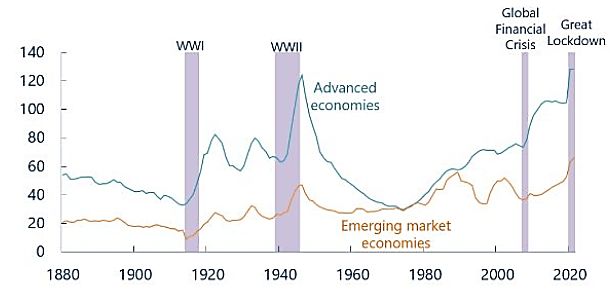

of living and working. Global public World 2.8 -2.9 5.6 4.6 3.9

debt as a percent of GDP is at levels U.S. 2.2 -3.5 5.0 3.9 2.0

last seen in the aftermath of World

War II (Figure 2). Euro area 1.3 -7.1 4.4 4.5 2.7

The good news is that effective Japan 0.3 -5.2 2.8 1.9 1.0

vaccines are being rolled out

China 6.0 1.7 8.4 5.4 5.9

globally about six months earlier

than previously forecast. This has Canada

pulled forward the timing of the

Potential GDP 1.5-2.1 0.1-1.3 0.2-1.6 0.3-1.9 0.2-2.2

economic recovery in the advanced

economies (except perhaps, Canada). Actual GDP 1.9 -5.5 4.0 4.8 2.5

Commodity prices have improved

f - forecast

in anticipation of stronger global

Source: Bank of Canada.

demand (Figure 3). The Bank of

Canada assumes that vaccination

programs will achieve broad unemployment rate is currently 6.7%. CANADIAN OUTLOOK

population immunity in the advanced Additional fiscal support of USD

Canadian GDP growth is expected

economies and China by the end 900 billion will be rolled out during

to be 4.0% in 2021 and 4.8% in 2022,

of 2021, and in other emerging 2021 whilst extraordinary monetary

following a large contraction of 5.5%

economies by mid-2022, enabling policy stimulus remains in place.

in 2020. The Bank of Canada assumes

a gradual resumption of normal The U.S. recovery is expected to be

that vaccinations help achieve herd

activities. Risks to the global growth broad-based across consumption,

immunity by the end of 2021 in line

outlook are evenly balanced. investment, and trade as the rollout

with other advanced countries. This

of vaccines gradually allows rollback

United States GDP growth is timing is looking increasingly shaky,

of virus containment measures.

expected to be 5.0% in 2021 however. Canada's vaccination

and 3.9% in 2022, following a The U.S. output gap – the difference rate appears to lag other advanced

relatively mild (in comparison to between the level of potential and countries by about six months.

Canada, Japan, and the Euro area) actual GDP – is expected to close Therefore, a more realistic assumption

contraction of 3.5% in 2020. The U.S. towards the end of 2021 and inflation may be that Canada will achieve herd

will reach 2% by late 2022. This is immunity by mid-2022, in line with

much earlier than in other countries, the emerging market economies.

including Canada – where the output Canada’s economy will likely operate

Canada increased its

gap will not close for another two below its potential until demand fully

indebtedness by a further 41%

years. In other words, even though recovers sometime in 2023, and in

of GDP during the pandemic the U.S. was the 8th most affected the interim, this will cause persistent

– the largest increase in the country from the coronavirus (as disinflationary pressures. Inflation is

world. Canada thus became noted earlier), its economy will be not expected to sustainably return to

the 6th most indebted operating at full capacity by the end the central bank’s 2% target until

country globally as at 2020- of 2021. U.S. GDP growth will cool to 2023.

around 2.0% in 2023 as the effects of

Q2. This will leave us more The shock to aggregate demand

policy stimuli ebb.

vulnerable to future financial from the pandemic has been uneven.

and economic shocks. High-contact services industries saw

Where Leaders Meet to Unlock BC’s Full Potential | www.bcbc.com 2B.C. ECONOMIC

REVIEW AND OUTLOOK FEBRUARY 2021

F IG URE 1: P ROVIN C ES HAV E FA R ED D I F F ER EN TLY

COVID-19 cases and fatalities by province, per capita, as at 25 January 2021

COVID-19 Cases per 1,000 population, COVID-19 Deaths per 1,000 population,

at 25 January 2021 at 25 January 2021

Quebec Quebec

Alberta Manitoba

Manitoba Canada

Canada Ontario

Saskatchewan Alberta

Ontario B.C.

B.C. Sask

Nova Scotia Nova Scotia

New Brunswick NB

Nfld & Lab Nfld & Lab

PEI PEI

0 5 10 15 20 25 30 35 0.0 0.2 0.4 0.6 0.8 1.0 1.2

Source: Government of Canada, COVID-19 Situational Awareness Dashboard.

F IG URE 2: GLOBAL P U BL I C I N D EBT ED N ESS I S AT L E V E L S L AST S E E N A F TE R WO R L D WA R I I

Global public debt, % of GDP

Sources: Historical Public Debt Database; IMF, World Economic Outlook; Maddison Database Project; and IMF staff calculations.

Where Leaders Meet to Unlock BC’s Full Potential | www.bcbc.com 3o

B.C. ECONOMIC

REVIEW AND OUTLOOK FEBRUARY 2021

F IG URE 3: COMMO D I T Y P R I C ES HAV E ST R EN GTH E N E D

Bank of Canada commodity price index, weekly since Jan 2020, Canada

Index, 3 Jan 2020 = 100

180

Total Energy Metals and minerals Forestry Agriculture

160

140

120

100

80

60

40

20

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan

Sources: Bank of Canada.

F IG URE 4 : COVID CAU SED A N EX T R AOR D I N ARY DE C R E AS E I N L A B O U R D E M A N D

Employment hours by industry, change from Feb to Dec 2020, Canada

Professional, scientific and technical services 4%

Public administration 3%

Educational services 3%

Utilities 3%

Finance, insurance, real estate, rental and leasing 1%

Health care and social assistance -1%

Forestry, fishing, mining, quarrying, oil and gas -2%

Manufacturing -3%

Wholesale and retail trade -5%

GOODS INDUSTRIES -5%

ALL INDUSTRIES -5%

SERVICES INDUSTRIES -5%

Agriculture -7%

Construction -8%

Transportation and warehousing -10%

Information, culture and recreation -11%

Business, building and other support services -15%

Other services (ex. public admin.) -18%

Accommodation and food services -32%

-35% -30% -25% -20% -15% -10% -5% 0% 5%

Sources: Statistics Canada.

Where Leaders Meet to Unlock BC’s Full Potential | www.bcbc.com 4o

B.C. ECONOMIC

REVIEW AND OUTLOOK FEBRUARY 2021

F IG URE 5: CANADA'S F I SC A L R ESP ON SE WAS E AS I LY TH E L A R G E ST A M O N G ST TH E G 2 0 CO U N TR I E S

Change in G20 budget deficits during 2020 (% of GDP) vs projected 2020 GDP growth

% of

CAN GBR USA BRA ITA ESP JPN DEU FRA RUS ZAF AUS CHN IDN IND KOR MEX TUR

GDP

0

-5

-10

-15

Discretionary Non-discretionary (including automatic stabilizers) GDP growth in 2020

-20

Note: Discretionary fiscal support is measured as the change in the cyclically adjusted primary balance (CAPB); nondiscretionary fiscal support is the residual.

The allocation between discretionary and non-discretionary measures should be considered indicative because output gap estimates, which are used to derive

the CAPB, are subject to a high degree of uncertainty.

Sources: IMF, WEO database; and IMF staff estimates.

the largest drop in GDP, resulting in a (CERB). The household saving rate, current policy settings we see little

severe decrease in labour demand as which is usually around 5% or less of reason to expect it will be sustainably

measured by employment hours by disposable income, soared to a record higher in the long term. Canada

industry (Figure 4). The distribution 27.5% in 2020Q2 before slipping to was the 9th most indebted country

of the shock has particularly affected (a still high) 14.6% in 2020Q3. In our globally in 2019, with the combined

lower-income and young workers view, it will require a careful balancing debt of corporations, households,

who work in high-contact service act to wean Canadian households off and governments hitting 302% of

industries. The national unemployment fiscal and monetary stimuli as private GDP in 2019. Canada increased its

rate was 8.8% in December 2020, sector demand improves over the next indebtedness by a further 41% of

having peaked at 13.8% in May. three years. GDP during the pandemic – the

largest increase in the world. Canada

Extraordinary policy stimulus has Overall, the near-term risks to the

thus became the 6th most indebted

helped to offset the shock. Canada’s Canadian outlook are weighted to the

country globally as at 2020-Q2. This

fiscal response – both federal and downside as Canada's vaccination

puts us in a vulnerable position once

provincial combined – was easily rates falter and appear set to push

the COVID crisis has passed.

the largest in the world as a share back to mid-2022 the timing for a full

of GDP (Figure 5). Households return to normal activities. Canada’s Canada’s borrowing spree was partly

were more than compensated for long-term prosperity appears more a necessary response to the crisis and

the loss of private sector wages precarious. Labour productivity partly a rational response to ultra-low

through federal programs such as the growth has been chronically low for global interest rates. Arguably, it is

Canada Emergency Response Benefit the past two decades, and based on also a bet that either borrowing costs

Where Leaders Meet to Unlock BC’s Full Potential | www.bcbc.com 5B.C. ECONOMIC

REVIEW AND OUTLOOK FEBRUARY 2021

will stay ultra-low for a long time or

that decades of higher productivity TA BL E 2 : B .C . E CO N O MI C O U TLO O K ( B C B C F O R E C AST)

growth lie ahead. In our view, this ( A N N UA L % C H A N G E U N L E SS OTH E RW I S E I N D I C AT ED)

seems an ambitious and improbable

bet. More likely, the combination 2019 2020 2021f 2022f

of very high indebtedness and

chronically low productivity growth

Real GDP 1.7 -6.0 4.5 4.8

(in stark contrast to the post-war era) Employment 2.6 -6.2 5.2 3.2

indicates that Canada’s economy will

be more susceptible to future financial Unemployment rate (%) 4.7 8.8 6.4 5.2

and economic shocks. Housing Starts (000 units) 45.2 38.0 42.0 45.0

Retail sales 0.7 1.8 4.5 4.0

B.C. OUTLOOK: EXPORTS

B.C. CPI 2.3 0.8 1.8 2.2

AND CONSTRUCTION

SUPPORT GROWTH WHILE f - forecast

CONSUMER FACING Sources: Statistics Canada and BC Stats; BCBC for forecasts.

SERVICES RECOVER LATER

The near-term economic outlook

resume and accelerate as vaccines eased. B.C.’s tailored approach to

for B.C. is broadly similar to that

are administered in North America closing consumer-facing businesses

for Canada. Following the massive

and around the world. According should also help limit the downside.

COVID-induced demand shock in

to B.C.’s COVID-19 Immunization Many consumers and businesses

2020, the provincial economy will

Plan, vaccinations will be completed have adjusted to operating under

rebound and expand by 4.5% this

by the end of September. (As limited and restricted physical

year, just ahead of the Canada-wide

noted above, it is starting to look distancing conditions. The final

pace. In 2022 the B.C. economy

like disruptions in vaccine supply quarter of 2021 will see a more

should pick up a little more steam

will push back the target date.) As fulsome re-opening of consumer-

and grow by 4.8%, in line with Bank

of January 27, more than 124,000 facing businesses and, perhaps, a

of Canada’s expectation for Canada.

doses had been administered. This return to travel. Economic growth

These two-years of robust growth, first phase covered long-term care over the course of 2021 will also be

however, come after the steepest homes, health care workers and lifted by the return to full capacity

decline in GDP in a century. We other high-risk populations. Phase in the construction sector. All of this

estimate the B.C. economy 2 begins in February and covers assumes B.C.'s vaccination program

contracted by about 6% in 2020 on seniors aged 80 and over and other goes to plan.

an average annual basis. We estimate high-risk and vulnerable populations

the downturn was larger than for not immunized in Phase 1. In April,

Canada as a whole, owing in part the third phase shifts to the general EXPORTS HELPING THE

to B.C.’s oversized tourism and air population starting with persons RECOVERY

transportation industries, a much aged 75 to 79. Distribution continues B.C.’s diverse export sector is adding

larger film and television industry in 5-year increments down to 60 to the recovery. A projected 5.6%

(which was shuttered for part of years at the end of June, with the expansion in global output in 2021

the year), and the pull-back in our youngest adults (18-24) completing anchors a generally positive outlook

oversized construction activity. the vaccination process by the end of for most of the province’s export

The economy will struggle in the September. industries. Global trade has regained

first quarter of 2021 amid rising In the second and third quarters of its pre-pandemic level and continues

and elevated COVID cases and 2021 we expect economic growth to to rise. The fact that the U.S. suffered

temporary weakness in Canada pick up as restrictions are gradually a comparatively mild COVID-

and the U.S. But growth should induced recession and is growing

Where Leaders Meet to Unlock BC’s Full Potential | www.bcbc.com 6B.C. ECONOMIC

REVIEW AND OUTLOOK FEBRUARY 2021

at a respectable clip is also positive. EMPLOYMENT REVIVES Following massive job losses

B.C.’s forest product exports are in March and April last year,

Following massive job losses in March

buoyant. An 8.4% GDP growth rate

and April last year, provincial job provincial job numbers (but

in China in 2021 – China is B.C.’s

second largest export market – is

numbers had mostly recovered by not hours worked) had mostly

the end of the year. As with Canada, recovered by the end of the

also good news for the province.

the COVID shock dealt unequal blows

year.

Activity in the film and television across the economy.

sector was hit when productions

Employment in tourism-related

were closed for a period in 2020. The hit to hours worked was larger in

sectors, food and accommodation,

Filming has resumed and again is an B.C. than in Canada. Nationally, hours

transportation, entertainment, and

important factor driving B.C.’s overall worked fell 8.7% for the full year.

personal services recovered to some

exports higher. The B.C. food and accommodation

extent in the second half of 2020, but

The weak spot in in B.C.’s export industry took the biggest hit,

the recovery lost momentum in the

base, of course, is international with hours falling by nearly one

latter part the year. Sluggish activity in

tourism. Even with vaccines and quarter. Even though construction

these industries is expected to persist

the expectation that the U.S. and has stayed open throughout the

well into 2021 (and perhaps beyond).

much of Europe will vaccinate their pandemic, hours worked in the

In contrast, the number of people sector fell 16% because of the need

populations much faster than Canada,

working in B.C.’s natural resource to physical distance on sites. The

we believe international travel will be

sector, manufacturing and in impact of scaled-back workforces

slow to recover. The industry suffered

professional and technical services and fewer hours worked was

a devastating blow in 2020. And

is up sharply since February. especially significant at large capital

the future is uncertain. There will be

Employment in the broad public sector projects. Many smaller projects were

pent up demand to resume travelling

has also increased over the past six postponed in 2020.

later this year if feasible, or perhaps

months with education reopening and

by mid-2022 (again, depending on

health care hiring for COVID testing

the actual vaccination rate). But the

and tracing. RETAIL ACTIVITY MOVES

recovery will probably take multiple

HIGHER

years. And it’s unclear when the The provincial unemployment rate

Canada-U.S. border will reopen, and currently sits as at 7.2%, well down Consumers have adjusted to

under what conditions. Meanwhile, from the 13.4% rate last spring. The distancing measures, reduced hours,

the number of international job market will be slower to heal and other impediments and are

visitors coming to the province for younger age cohorts with the out spending again in retail outlets

plummeted a staggering 97% in unemployment rate for persons below around the province. Sales in stores

2020. In downtown Vancouver hotel age 25 likely to stay above 10% for have rebounded. By November

occupancy was just 28% last summer much of 2022. retail spending was up around 10%

(it is lower today). Countries are year-over-year. With the exception

on different re-opening timelines of gas stations and clothing stores,

HOURS WORKED FELL even the hardest hit segments had

and the airline industry has been

SHARPLY recovered. Retail activity is expected

severely disrupted – with Canada

hit harder than most due to punitive In 2020 the total number of hours to remain solid in 2021, supported by

travel restrictions. Business travel – worked in B.C. plunged by 10%. This extraordinary government financial

including for conventions and large exceeded the 6% drop in employment transfers to households and also

meetings – will eventually rebound, because hours worked also captures because curtailed spending in areas

but it is unlikely to get back to its people who retained their jobs but such as entertainment, travel, and

pre-pandemic level for many years, worked fewer hours. The province also dining means consumers will realign

particularly since people have seen saw a significant rotation to part-time some spending to other parts of the

how digital communications saves employment during the shutdown. broad retail sector.

both time and money.

Where Leaders Meet to Unlock BC’s Full Potential | www.bcbc.com 7B.C. ECONOMIC

REVIEW AND OUTLOOK FEBRUARY 2021

F IG URE 6: EX P ORTS TO U.S. HI G HER , BOOST E D BY F O R E STRY E X P O R TS

B.C. merchandise exports, SA, $billons B.C. merchandise exports, SA, $ billions

2.2 1.4

2.1 1.3

2.0

1.2

1.9

1.1

1.8

1.7 1.0

1.6 0.9

US

1.5

Rest of world 0.8 Forestry products

1.4

0.7 Energy products

1.3

1.2 0.6

Jan 17 Jan 18 Jan 19 Jan 20 Jan 17 Jan 18 Jan 19 Jan 20

Source: B.C. Stats. Latest data November 2020, seasonally adjusted, 3-month moving averages.

F IG URE 7: EMP LOYM EN T R ECOV ERY HAS P L ATE AU E D I N H A R DE R - H I T A N D M O D E R ATE LY- H I T I N D U ST RI ES

Employment* in “hard-hit,” “moderately impacted,” “growth industries”, and “public sector” Growth industries:

Indexed February 2020=100 - Agriculture

- Forestry, mining, natural gas

110 - Manufacturing

- Prof., scientific and tech serv.

105

Public sector:

100 - Health care (public)

- Education (public)

- Public administration

95

Moderately impacted:

90 - Transportation & warehousing

- Finance, Insurance & real estate

85 Hard-hit - Construction

- Wholesale and retail

80 Moderately impacted - Private Education

Hard hit:

Growth industries - Accomm. & food services

75 - Information, culture & rec.

public sector

- Business, building & support serv.

70 - Other services

- Private health care

65

2017 2018 2019 2020

Feb.

Latest: December 2020. *aged 15 and over, seasonally adjusted, 3-month moving averages up to 2020.

Source: Statistics Canada, Labour Force Survey. Table 14-10-0294-01.

Where Leaders Meet to Unlock BC’s Full Potential | www.bcbc.com 8B.C. ECONOMIC

REVIEW AND OUTLOOK FEBRUARY 2021

F IG URE 8: TOTA L N U M BER OF HOU R S WOR KE D I N B .C . F E L L 1 0 % I N 2 02 0

Total hours worked by industry, 2019-2020 % change

10

9.5

5

0

-0.1 -3.3

-1.7 -1.8

-5

-6.7

-10 -7.8 -8.5

-10.1 -10.1 -10.6

-15 -13.0 -13.5

BC Canada -16.2

-20 -19.0

-25 -22.8 -23.0 -23.8

-30

-35

Agri- Public Prof., Finance Mfg. Health Edu- Goods- Whole- ALL Services- Trans- Forestry, Other Info. Business, Accom.

culture admin. sci. & ins. & care cation prod- sale INDUS- prod- port. mining, Con- services & building &

& tech. real ucing & retail TRIES ucing & ware- oil struction cultural & other food

serv. estate sector trade sector housing & gas ind. serv. serv.

Source: Statistics Canada, Table 14-10-0036-01.

F IG URE 9: CONSUM ER S R ET U R N TO B.C . STOR E S

B.C. retail sales SA, millions $

8500

Thousands

8000

7500

7000

6500

6000

5500

5000

15 16 17 18 19 20

Source: Statistics Canada, Table 20-10-0008-01. Latest: November 2020. SA = seasonally adjusted.

Where Leaders Meet to Unlock BC’s Full Potential | www.bcbc.com 9B.C. ECONOMIC

REVIEW AND OUTLOOK FEBRUARY 2021

F IG URE 10: MOST SE G M EN TS OF R ETA I L HAV E R E COV E R E D. . .

B.C. retail sales, y/y % change

30

10

-10

-30

-50

-70 May June July August Sept. Oct Nov

-90

Retail trade - Motor Gasoline Clothing Furniture & Food & Building General Electronics &

total vehicle and stations stores home beverage material & merchandise appliance

parts dealers furnishings stores garden stores stores

stores equipment

supplies

Source: Statistics Canada, Table 20-10-0008-01.

F IG URE 11: ...BUT FOOD SERV I C E SA L ES ST I L L W E L L B E LOW P R E - PA N D E M I C L E V E L S

B.C. food service sales, SA, $millions B.C. food service sales by segment, y/y% change

1200 10

1100 0

1000 -10

900 -20

800 -30

700 -40

600 Food services and -50 Full-service

drinking places Limited-service eating places

500 -60

400 -70

300 -80

Jan 17 Jan 18 Jan 19 Jan 20 Jan 17 Jan 18 Jan 19 Jan 20

Source: Statistics Canada, Table: 21-10-0019-01. Latest: November 2020. SA = seasonally adjusted.

Where Leaders Meet to Unlock BC’s Full Potential | www.bcbc.com 10B.C. ECONOMIC

REVIEW AND OUTLOOK FEBRUARY 2021

F IG URE 12: N ON -RESI D EN T I A L P ER M I TS HAV E H E L D U P I N N O N - ME TR O A R E AS

Non-residential building permits, B.C. metro Non-residential building permits, B.C.

areas*, millions $ excluding metro areas*, millions $

550 180

500 160

450

140

400

350 120

300 100

250

80

200

60

150

100 40

Jan 16 Jan 17 Jan 18 Jan 19 Jan 20 Jan 16 Jan 17 Jan 18 Jan 19 Jan 20

*Vancouver, Victoria, Abbotsford and Kelowna.

Source: Statistics Canada . Table: 34-10-0066-01. Latest: December 2020. 6-month moving averages.

F IG URE 13: P ROVIN C I A L HOU SI N G STA R TS R ELATI V E LY STA B L E I N TH E WA K E O F TH E PA N D E M I C

B.C. housing starts, 000s

60

seasonally adjusted annual rates

50

3 month moving average

40

30

20

10

08 09 10 11 12 13 14 15 16 17 18 19 20

Source: Statistics Canada, Table: 34-10-0158-01. Latest: December 2020.

Where Leaders Meet to Unlock BC’s Full Potential | www.bcbc.com 11B.C. ECONOMIC

REVIEW AND OUTLOOK FEBRUARY 2021

Despite a solid growth B.C.’s large residential construction CONCLUDING THOUGHTS

outlook, it will still take time sector will also support growth in

Considering the damage reaped in

2021. The reduction in mortgage

for the provincial economy to 2020, the B.C. economy could post

rates to near-record lows is good for

fully heal. Much depends on affordability (although the benefit

a solid growth performance over

the path of the virus the next two years. However, as for

has largely been offset by rising

Canada, the timing of the economic

prices for single family homes).

recovery hinges on the timing for

Although residential home sales

vaccine delivery, which is racing

were initially curtailed because of

HOUSEHOLD SPENDING against the spread of the virus and

COVID, later in the year sales activity

ON SERVICES SLOWER TO the B.1.1.7 variant. B.C. has enjoyed

climbed to record highs. While sales

RECOVER a comparatively strong rebound in

may stabilize in 2021, the level of

employment. The province’s export

Retail spending has posted an activity will remain elevated and

and construction sectors are leading

impressive revival but some parts housing starts should pick up from

the recovery as spending on high-

of household consumption will not 2020. The provincial government

contact services remains restricted.

regain pre-crisis levels until large is expected to continue with its

The drop in interest rates has spurred

gatherings are allowed (e.g., sporting affordable housing programs

activity in the residential real estate

events, concerts, conventions, which will further add to new home

sector, which should translate into

casinos, and some other services are construction over the forecast

more home building in the coming

reopened). In-house dining is still horizon.

years.

operating at around 50% capacity

and recently (November) restaurant Despite a solid growth outlook, it

sales fell again. IMPACT OF FISCAL AND will still take time for the provincial

MONETARY POLICY STIMULI economy to fully heal. Much

In response to the pandemic’s depends on the path of the virus,

CAPITAL INVESTMENT AND the impact of new strains, the pace

economic disruption, the federal

CONSTRUCTION PROVIDE A of vaccinations, and how businesses

government delivered hundreds of

BOOST IN 2021 and consumers respond to what

billions of dollars in financial support

Construction has long been a key to households and businesses while remains a complex and uncertain

B.C. economic engine and that is set the Bank of Canada slashed its economic environment. There are

to continue. In the five years to 2019, policy interest rate and engaged significant risks to our baseline

construction registered the strongest in unprecedented “quantitative forecasts. It is starting to look likely

average growth performance of easing” by directly purchasing that Canada, and therefore B.C.,

any major industry group. In 2019, government-issued debt. Overall, could lag other advanced countries'

construction of large capital projects Ottawa has done the lion’s share vaccination rates by about 6 months.

accounted for more than half of of the fiscal heavy lifting in the That would mean herd immunity

all economic growth. Construction past year. However, provincial and a return to normal activities

will continue to make an outsized governments, including in B.C., also is not possible by the end of 2021

contribution to growth in B.C. Non- stepped forward with significant as curently expected. Rather, this

residential building permits reached measures aimed at shoring up would take place by mid-2022, in line

record highs in 2019 and have stressed health care systems and with the timing for emerging market

generally held up well during the assisting households and firms. economies. For B.C., another key

pandemic. Fiscal stimulus will boost With the bumpy economic recovery unknown is how quickly the battered

non-residential construction over the now underway, we anticipate that tourism sector springs back to life

next two years as governments look governments will continue to invest after a truly disastrous 2020.

to advance various capital projects in infrastructure and move only Looking further ahead, government

to boost the recovery and “green” gradually to unwind the extraordinary policy risks have also emerged as

the economy. spending programs adopted in 2020. factors that could weigh on the

Where Leaders Meet to Unlock BC’s Full Potential | www.bcbc.com 12B.C. ECONOMIC REVIEW AND OUTLOOK FEBRUARY 2021 broader business environment and affect the outlook for investment. The tax burden for business and high-skilled earners in B.C. (and Canada) has increased and is now higher than in most competing jurisdictions. The increasing array of new, complex and costly regulations is making it harder for many firms to justify deploying fresh capital to the province. Canada’s recent decision to sharply boost carbon taxes over the next decade could speed the decline of some natural resource and manufacturing industries that are sensitive to the cost of energy. More generally, both Canada and B.C. have entered an era of activist and expanding government. In this setting, policymakers need to be alert to waning competitiveness and pay attention to the province’s ability to attract private sector capital investment dollars and qualified talent. CO-AUTHORED BY Ken Peacock, Chief Economist & Senior Vice President David Williams, DPhil, Vice President of Policy Where Leaders Meet to Unlock BC’s Full Potential | www.bcbc.com 13

You can also read