The Sky's The Limit? UK Operational Real Estate - Student Accommodation - Build to Rent - Retirement Living - Savills

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

UK Operational Real Estate

REPORT

Savills Research

The Sky’s The Limit?

Student Accommodation – Build to Rent – Retirement Living

2

UK Operational Real Estate

Savills Summary Six

Here are our six key takeaways from

this report:

1 Residential operational real estate in the UK is still

in its early stages, representing an exciting growth

opportunity for investors and developers.

2 Institutions are already active, but we expect

appetite and activity to grow substantially as

investors appreciate the underlying demographic

drivers and the design & management considerations

particular to the sector.

3 The student accommodation sector is the most

mature and liquid of the operational real estate

markets: currently worth over £50 billion.

4 Build to Rent is still evolving and has enormous

growth potential: at just under £10 billion today,

we predict at full maturity it will be worth

almost £550 billion.

5 The retirement living sector also has huge

capacity to grow. Within it, the care home market

is more established, with institutions and REITs

already actively investing. A market for retirement

Contents housing investment is now emerging. We believe

the retirement living sector could grow from today’s

Summary 3 £120 billion to over £260 billion in value at full maturity.

Market overview

Investment flows into the UK

4

6

6 While there are differences in design and

management requirements for these asset classes,

operators and investors are waking up to the

potential crossover between student housing, Build

What's transacting where? 8 to Rent and retirement living. Opportunities abound

for these parties to leverage their experience and

Student accommodation 10 expand across the sectors.

Build to Rent 14

Retirement living 18 The UK's operational real estate will grow

from £223 billion today to £880 billion at

Conclusions 21

full maturity

3

UK Operational Real Estate

The sky’s the limit?

The sub-sectors of the UK’s operational real estate

are at different stages of maturity

This paper covers residential As a more mature sector, Institutions have invested in UK care

operational real estate. By this we opportunities for growth in PBSA homes for many years, but the scale

mean places owned and operated by will likely be by outperforming the of that activity is growing rapidly. By

professional, large-scale investors competition on brand differentiation, contrast, retirement housing has been

where people live, whether those rather than through innovation. a slower burn, with institutions only

people are full-time students, young Organic growth will largely be limited recently entering the sector. Retirement

professionals, working families, or to growth in the full-time student living (care home and retirement

retirees. population, rather than increasing housing) is, therefore, an emerging sector

Operational real estate offers penetration. where many of the rules are still being

attractive opportunities for investors Capacity for new entrants is limited, written. We expect to see competition

and developers. It’s supported by with firms such as Unite, UPP and GCP intensify as new entrants compete to

strong fundamental demographic and REIT maintaining their hold on the develop new product and build sufficient

economic drivers. Already, investors majority of the market. We estimate brand awareness to attract their target

have made significant inroads into the UK’s PBSA sector is worth just over end-users. We calculate the total value of

many of these property sectors. £50 billion. retirement living today is £120 billion: at

However, many aspects of operational BTR is still evolving. There is plenty full maturity, we predict the sector will

real estate are still emerging, and there of space for new entrants, and the be worth £266 billion in today's values.

are challenges still to face. In this competitive landscape is likely to The scale of investment in these asset

document, we identify many of those look very different in ten years’ time. classes is growing. Whether it’s the

challenges and explain how they might Opportunities for growth in BTR will recapitalisation of the Chapter student

be addressed. be driven by developing new stock and housing portfolio, Goldman Sachs’ £2

Of the UK operational real estate delivering innovative new products and billion investment in retirement housing

markets that we examine in this report, tenure structures. While the BTR stock developer Riverstone, or Greystar’s

purpose-built student accommodation completed to date is worth less than recently launched £2 billion BTR fund,

(PBSA) is the most mature, followed £10 billion, at full maturity, w estimate investors are increasingly confident

by Build to Rent (BTR) and then the BTR sector could grow to £550 pouring large amounts of capital into

retirement living (RL). billion in today's values. operational real estate, often across

multiple asset classes.

WHAT DO WE MEAN BY MATURITY?

Emerging Mature

•Intense competition from many small businesses •Market dominated by a handful of larger businesses

•New entrants and innovations often disrupt the market •New entrants and innovations gain little market share

•Revenues reinvested to fuel growth •Profits distributed to investors

•Innovation is the key driver of value •Brand is the key driver of value

•Cost of capital is high •Cost of capital is low

•Lack of transparency makes valuation difficult •Abundant comparable information makes valuation easier

•Customer needs evolve rapidly as knowledge and experience •Customer needs move slower

of the sector develops

4

UK Operational Real Estate

Figure 1 Summary of UK operational real estate asset classes

Student Accommodation Build to Rent Retirement Living

(PBSA) (BTR) (RL)

Full-time students Households in the Over 75s

Size and Target market private rented sector

potential

1,844,500 5,202,700 5,693,800

Size of target

market (2019)

640,000 30,400 1,193,000

Current stock

640,000 1,740,900 1,731,600

Stock at maturity

£51.2 £9.6 £121.0

Current sector

value (bn, 2019)

£51.2 £543.6 £265.6

Value at maturity

(bn, 2019)

£3.1 £2.6 £1.3

Investment Investment in

market 2018 (bn)

£4.7 £2.3 -

Average

investment

2015-17 (bn)

Finance Many bank and non-bank Some bank and non- Some non-bank

lenders, cost of finance bank lenders, cost of lenders, cost of finance

low for borrowers with finance slightly higher higher due to untested

track record than PBSA model

Risks and Biggest risks Brexit restricting EU End of no-fault evictions Local authority funding

evolution student numbers reduces flexibility for for residential care is too

investors low, putting providers

In London: restrictions in under financial pressure

Draft New London Plan In London: plans to

impose social rent Potential restrictive

(with a registered legislation on event fees

provider landlord) on

BTR schemes in Draft

New London Plan

Possible Flexible use of space, Greater understanding Emergence of retirement

innovation and supporting residents of how location and housing for rent and the

to create communities amenities influence value 'rent-to-rent' model

and build loyalty

Support for residents Co-location of retirement

to curate events, housing, care homes,

building communities and dementia care in

retirement villages

Source Savills Research using ONS, RCA, EAC

5UK Operational Real Estate UK Operational Real Estate

Investment flows into the UK

Domestic investors have dominated UK operational real estate

over the last three years, but the North Americans aren't far behind

£8.4bn

£1.9bn

£5.4bn £2.6bn

£1.9bn

Source Savills Operational Capital Markets

Figure 2 Investment volumes into the UK by source of capital and sector, 2016-18

UK Value Deals North America Value Deals Europe Value Deals Asia-Pacific Value Deals Middle East & Africa Value Deals

Student £4.1bn 136 Student £3.3bn 31 Student £877m 9 Student £2.2bn 19 Student £1.0bn 31

Build to Rent £3.2bn 72 Build to Rent £1.4bn 18 Build to Rent £501m 10 Build to Rent £35m 1 Build to Rent £931m 9

Retirement living £1.1bn 49 Retirement living £673m 15 Retirement living £498m 5 Retirement living £395m 1 Retirement living - -

6 7UK Operational Real Estate UK Operational Real Estate

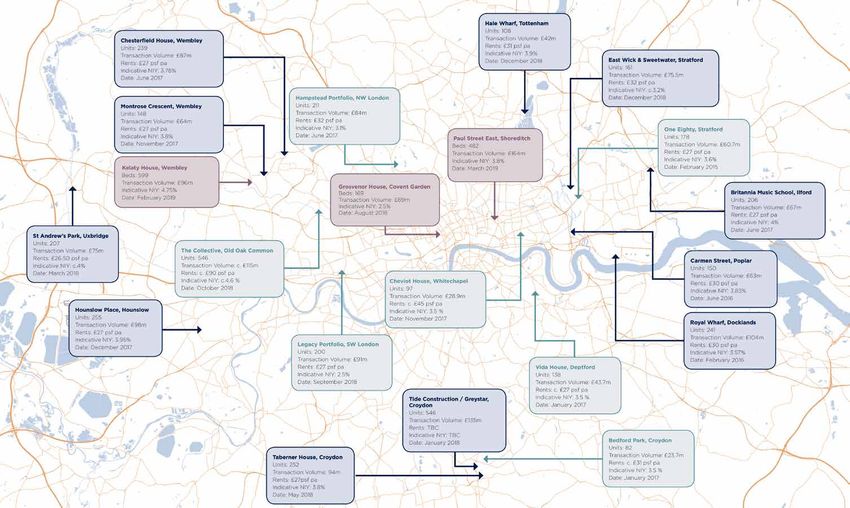

What's transacting where?

Figure 3 London has been a hotbed of transaction activity across BTR and PBSA.

Here we identify some of the more significant recent deals.

Source Savills Operational Capital Markets

Key Operational / Income Producing BTR / Forward Funded PBSA

8 9UK Operational Real Estate

Student accommodation

The most mature of the UK's operational real estate sectors,

investors will face stiff competition to increase their market share

Purpose-built student accommodation The year in review fall in domestic investment since 2016

(PBSA) is the most mature and liquid Investors placed £3.1 billion in UK reflects both a particularly strong year

of the operational property markets PBSA in 2018, 19% less than in 2017 in 2017, when UK investors made up

in the UK. Investors had access to the and 45% less than in 2015. Price per 53% of investment volume, and a shift

sector as far back as 1998, when Unite student bed remains high, at £90,000, in focus to development, with UK

Students listed on the Alternative in line with the average for the PBSA developers building the stock for

Investment Market (AIM), a sub- previous four years. international investors to acquire later.

market of the London Stock Exchange. Just four deals accounted for more

Its transfer to the London Stock than half the PBSA investment market The years ahead

Exchange itself in 2000 marked the last year, down from five deals in 2017 The first quarter of 2019 has been

beginning of PBSA’s evolution into a and 12 in 2014. Institutional investors relatively quiet, with just over £600

mature, mainstream investment class. such as Allianz, Brookfield, and million of investment. That’s 44%

In the following years, a host of Aberdeen Standard dominated the PBSA less than Q1 2018 and 38% less than

new investors entered the market, market in 2018, accounting for 61% of Q1 2017, reflecting the uncertainty

with REITs GCP and Empiric Student the value invested and 56% of the beds. leading up to the UK’s original March

Property offering retail investors North American investors had the 29th deadline for leaving the EU.

access to the PBSA market. 2015 and greatest share of investment into UK More than half the investment in Q1

2016 saw the latest new entrants, student housing for the first time since came from just two deals: iQ agreed

CPPIB and Brookfield. Since then, 2015: 31%. Investment from mainland to forward fund almost 2,000 student

new entrants have played a less Europe and the UK was roughly equal, homes in Leeds and Coventry, and

significant role in aggregating stock at with each accounting for just over 23% Chapter acquired Paul Street East

scale. Now the market is dominated by of the year’s total. Investment from near Old Street, London.

a tight group of large-scale investors, mainland Europe and the Middle East We predict that 35,000 PBSA beds

with only small movements in market last year was higher than the three- will trade in 2019, with a total value

share of late. year average. The disproportionate of £3.5 billion. Based on the pipeline

Figure 4 Direct let net initial yields for student accommodation

Net initial yield Trend

London 4.00% Down

Super prime regional 4.75% Down

Prime regional 5.25% Down

Secondary regional 6.00% Up

Source Savills Operational Capital Markets

10UK Operational Real Estate

Figure 5 Student accommodation investment by source of capital

£6bn

£5bn

£4bn

Value invested (£bn)

£3bn

£2bn

Other/Not known

Russia

Middle East & Africa

£1bn Asia Pacific

USA

Canada

Europe

- UK

2013 2014 2015 2016 2017 2018

Source Savills Operational Capital Markets

of portfolios either on or approaching Evolution turn their attention to less mature

the market, we would expect to see A little over a third (35%) of full-time PBSA markets across mainland

a flurry of activity in the second half students in the UK live in purpose- Europe, such as Italy, Spain and

of this year. In particular, we expect built student accommodation. Portugal. Attitudes towards full-time

to see activity accelerate once there We see little scope for PBSA to study in these countries are changing,

is further clarity regarding Brexit, increase its penetration of this target with more students choosing to live

whether this arises from securing market. The sector will still be able to away from home during their time at

a withdrawal agreement, a further, expand in line with growing full-time university. This will fuel increased

longer extension to Article 50, or a student numbers, and there will be a demand for PBSA, driving investor

hard Brexit on 31st October 2019. natural churn of development as older appetite in these markets.

schemes become obsolete and are In November 2018, the UK

Finance redeveloped. Government gave the green light

Debt finance for development or Universities operating their own for universities to offer accelerated

stabilised PBSA assets is widely student housing will become more two-year undergraduate courses.

available through a range of lenders, active in the market as their current This will allow students to remain

including clearing banks, other schemes age: for example, Reading at university studying for two 45-

banks and also non-bank debt University has closed some of its week years, rather than the current

providers. This is the case for major older blocks in order to redevelop. standard of 36 weeks for three years.

developments right through to small Other universities could choose to We believe that this change

schemes, due to the relative maturity partner with private PBSA developers will have only a limited impact at

of the market: lenders feel they to help reinvigorate their stock. established universities with a strong

understand the UK PBSA proposition. Operators trying to increase their focus on research. One of the selling

The strength of some student market share will have to do so at the points of Russell Group universities

housing developers’ track records expense of their competitors, or in has always been that they attract

even means that their lending costs new markets. With parts of the UK leading lecturers and professors, who

can be cheaper than for most Build to PBSA market looking fully supplied, are working at the cutting edge of

Rent developments. we expect to see larger investors their fields. ▶

11UK Operational Real Estate

35% Proportion of full-time students

living in PBSA in the UK

Offering accelerated degree courses Risks and mitigation in PBSA than domestic students

would require these professors to There are two categories of risk according to HESA data. Currently,

spend a greater proportion of their facing the student housing sector. EU students pay the same fees as

time teaching, rather than working on The first and most pressing is UK students. Government has yet to

new research, which they are unlikely political, with Brexit a persistent clarify what fees EU students will face

to want to do. theme and immigration, education, after Brexit, but the prospect of levying

At newer, teaching-focused and planning policy all high on the substantially higher international

universities, demand for these agenda. The second, more fundamental student fees on EU students remains

intensified courses is likely to be set of risks are demographic on the table. This would mean EU

greater. This will have a mixed effect considerations stemming from the students could see their fees double

on demand for PBSA. On the one UK’s ageing population. or more. Those students would also

hand, the total number of students The most apparent risk facing lose access to finance from the Student

at these universities will fall unless the UK PBSA market in 2019 is Loan Company, meaning they would

they can dramatically increase Brexit. Specifically, the uncertain have to find a way to pay those higher

recruitment, as some students will future for international students fees up front. A large number of EU

be on campus for two years rather following the UK’s departure from students might well look elsewhere

than three. the EU poses challenges for student for a university education should fees

On the other hand, having a housing investors. increase in this way.

greater number of students on 51-week While EU students make up just However, changes to immigration

leases will increase net operating 7% of full-time undergraduate students policy could mitigate any potential

income for those schemes that are let. in the UK, they’re more likely to live falls in EU student demand.

Figure 6 Acceptance rates for undergraduate students by domicile

Not EU Other EU UK

85%

80%

75%

Acceptance rate

70%

65%

60%

55%

50%

45%

40%

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Source UCAS

12UK Operational Real Estate

The Project, Hoxton

As of March 2019 graduates from on PBSA schemes and requiring

overseas can now remain in the UK developers to have a nominations Flexible space

for six months after graduating from a agreement with a university in place to The Project in Hoxton,

bachelors or masters course, up from secure planning permission. For now, East London, is a good

four months. This is some way off the PBSA consents are still being granted, example of how PBSA

post-study work visa system scrapped in but unless the Mayor is forced to back developers can create flexible

2012, which allowed graduates to remain down, these proposals could make new amenity areas to support their

for 12 months, and countries such as the PBSA development all but impossible residents and make best use of

US and Australia which allow graduates anywhere in Greater London. the space through the day.

to remain for up to 18 months. Last year we reported that the sector Depending on what students

However, it marks a positive shift faces a demographic challenge (Investing want, the space can be

in rhetoric. This change, and the in Private Rent , 2018), with the student configured for quiet study,

potential exclusion of international age population approaching a trough. workshops, yoga classes,

students from immigration caps, could We're now one year closer to a return to film screenings, and DJ nights.

help UK universities recruit more growth. From 2020 onwards, population Expect to see more

students from outside the EU and projections show rising numbers of community creation initiatives

further bolster PBSA demand. people at university age, suggesting in the next generation of UK

Acceptance rates for non-EU students we’ll see increasing demand for student PBSA schemes.

have fallen over the past decade places and for accommodation.

as universities have felt increasing

pressure from immigration policy. Old dog, new tricks

The immigration white paper suggests While PBSA may be the most mature of

Government is taking a less hard-line the operational property asset classes,

approach with regards to overseas there are still lessons it can learn from

students, however. After the UK leaves other, more emerging sectors.

the EU and seeks free trade agreements With brand awareness and loyalty

with countries such as China and India, increasingly important for student

student visas are likely to be a valuable housing operators in a highly

part of the UK’s wider trade offer. competitive landscape, co-living and

If non-EU student acceptance rates co-working offer interesting parallels

rose in line with rates for EU students, and lessons to be learned. Amenities

the number of international students such as lounges, study/work areas

could increase by more than 7,000 and games rooms are common to all

per year. Given that international these spaces. Yet where co-living and

students are more likely to live in PBSA, co-working go beyond this is in the

this could have a significant effect on curation of these spaces. Through

student accommodation demand. running events, or enabling residents

Planning still presents a risk to to run their own events, these spaces

student housing development, especially can help create a positive sense of

in London. The Mayor of London’s Draft community that builds loyalty and

New London Plan suggests imposing encourages residents to renew their

affordable student housing requirements leases time after time. ■

13UK Operational Real Estate

Build to Rent

The growth potential of UK Build to Rent is huge. The volume of funds being

raised to target the sector is testament to the scale of investor demand

Private renting is not a new concept further third of the market, largely firms attempt to refinance or exit

in the UK, but it's only in the last few due to Grainger buying partner APG’s in the near future: as we saw with

years that large-scale, institutional 75% share of GRIP for £396 million. Lone Star’s marketing of Quintain

investors have made their mark on Last year’s investment volumes last year. Given comparatively poor

the sector. 2013 was the year things would have been somewhat higher had sentiment in some parts of the

changed, whether you consider the Lone Star’s proposed sale of Quintain residential sales market at present, we

watershed moment to be M&G’s gone ahead. Even though the sale predict many will sell to institutions

acquisition of a Berkeley residential didn’t go through, the scale of interest rather than breaking up blocks for

portfolio or Delancey funding the in acquiring one of London’s largest sale to individuals, driving a spike in

Athlete’s Village in Stratford. BTR developments bodes well for the investment activity.

The sector has expanded rapidly market in general. In addition to these investors,

in the years since, with over 30,000 Despite similarities between PBSA housebuilders are paying more

homes complete and a further 110,000 and BTR, relatively few investors are attention to the demand from

in the pipeline that will be built, let, active across both sectors. Goldman institutional investors to forward

and managed by professional investors Sachs, Legal & General, M&G, fund stock. This gives those

as homes for rent. Greystar, and Aberdeen Standard developers an opportunity to reduce

Looking to the student are among the few to have invested their risk exposure and helps generate

accommodation sector as our in both. Goldman Sachs and Legal & returns more quickly, allowing them

benchmark, there’s at least a General are the only two investors to move onto the next site faster.

decade to go before institutional with commitments across all of PBSA,

private rent reaches maturity. BTR and retirement housing. Finance

This means there is still scope for Given the similar challenges in Availability of development

seismic shifts in the sector. There development and management, we finance for BTR development is

is also plenty of opportunity for would expect to see more investors generally similar to that for student

new and innovative entrants to expanding their capabilities to cover accommodation, despite the

disrupt the market, as customer the full spectrum of operational relative youth of the sector. In fact,

awareness and understanding of residential assets. In particular, banks and other debt providers are

this tenure increases. there are opportunities for firms arguably more comfortable with the

to capitalise on brand awareness to demographic drivers for BTR. The

The year in review encourage graduates leaving PBSA to clear story of housing undersupply

Build to Rent investment totalled move into the same investor’s BTR and stretched affordability as the

£2.6 billion in 2018, 11% higher than schemes, and for those in later life premise for BTR investment is easy

in 2017 and the highest level of leaving BTR for retirement housing. to understand, and perhaps provides

investment since 2014. more comfort for a lender than the

Institutions, such as Legal & The years ahead more discretionary international

General and M&G, continued to grow, Five years have now passed since 2014, student demand that helps underpin

increasing their share of investment when private equity firms invested the UK PBSA proposition.

from £382 million in 2015 to £880 over £1 billion into the BTR sector. Nevertheless, the cost of finance

million in 2018, over a third of the With a typical 4-6 year investment for BTR development currently tends

total. Public companies made up a horizon, we would expect to see those to be the same or higher than for

14UK Operational Real Estate

Carmen Street, Poplar

similar PBSA schemes, simply because last two years, as they sell properties.

BTR developers haven’t yet had the There is an opportunity for larger scale, London and

chance to build such a strong track professional investors to aggregate the regions

record in what is still a new sector. portfolios of rental homes. While London remains

We expect to see the cost of finance for There are parallels here with the most popular location

BTR decrease as the sector matures, how institutional and professional for BTR investors, competition,

potentially becoming even cheaper than investment grew to 47% of rental stock planning policy, and higher

finance for PBSA. in the US. In the aftermath of the sub- costs will push more

The PRS debt guarantee scheme is prime mortgage crisis in 2007, large- development to the regions.

a helpful statement of Government’s scale investors were able to acquire Many investors have already

support for the BTR sector, but take-up portfolios of scale from distressed bought into Manchester’s

to date has been slow simply because mortgagees. While there is no crisis of investment and rental growth

not much stock has completed yet. such scale on the horizon in the UK, story, and there are still

Refinancing demand for stabilised there is an opportunity emerging for considerable opportunities

assets will grow substantially over the investors to aggregate portfolios from for expansion at the lower

next five years as the pipeline of BTR individual landlords struggling to end of the market and in other

stock completes and begins to let up. service buy to let mortgages. regional cities across the

In the more mature student UK such as Bristol, Leeds

Evolution accommodation market, 35% of full-time and Glasgow.

As of March 2019, there were just over students live in purpose-built housing. In March 2019, London

30,000 complete BTR homes in the UK, Assuming a similar level of penetration developer Telford Homes

according to Savills/British Property in the private rented sector (and plc entered an agreement

Federation data. There were a further accounting for cross-over between the with Invesco and M&G, giving

37,500 homes under construction and PRS and student accommodation for the those investors first refusal

72,200 in planning, bringing the total younger age bands), we estimate that the on funding any new Telford

pipeline to 140,100 homes. UK Built to Rent sector could comprise developments. While these

We estimate that the 30,000 over 1.7 million households at full deals will result in lower profit

completed BTR homes have a total value maturity, with a total value of almost margins for Telford in the

of approximately £9.6 billion, based £550 billion. short term, this funding model

on average values for standing PRS We expect purpose-designed and allows them to recycle capital

portfolio transactions. This is just under built homes to make up the majority of and deliver sites more quickly,

1% of the total value of privately rented this supply. Portfolios aggregated from while also reducing their

housing in the UK, at £1.5 trillion. The buy to let property sales will comprise a risk exposure.

vast majority of the remaining stock significant minority.

is owned by individual landlords: 1.9 Reaching this potential will

million homes are owned with a buy to require a serious step up from

let mortgage. current delivery levels. With buy to let

Recent changes to tax and regulations looking less attractive, housebuilders

have made buy to let much less will have to consider routes to market

attractive for individual landlords. Our other than sales to buy to let landlords.

analysis of UK Finance figures suggests Block sales to professional investors

that landlords have redeemed over will undoubtedly be one of those

120,000 buy to let mortgages in the alternatives. ▶

15UK Operational Real Estate

Figure 7 Build to Rent investment by type of investor

£3.5bn

£3.0bn

£2.5bn

Value invested (£bn)

£2.0bn

£1.5bn

Other/not known

£1.0bn Private Equity

JV

Registered Provider

£0.5bn

Private Company

Public Company

Institution

-

2013 2014 2015 2016 2017 2018

Source Savills Operational Capital Markets

Risks and mitigation Much depends on the detail of the Key BTR deals

While Brexit dominates the foreign proposed changes, which will not In January 2019 Legal & General

policy agenda, housing sits at the become clear until later this year. forward funded Buchanan Wharf,

top of parliament’s domestic policy We have more clarity on Labour a 324 apartment scheme on the south

priorities. That’s been reflected in plans for rent control. Reassuringly, bank of the River Clyde in Glasgow. This

the policy announcements made these resemble rent stabilisation was the first forward funded BTR deal

since the tail end of 2018. measures, as seen in New York City, in Glasgow and Scotland’s first

Since 2013, Government has for example, rather than rent caps. transaction involving a purpose-

supported households buying new Shadow Housing Minister John designed rental scheme.

build homes through Help to Buy. Healey has clarified that Labour plans Transport for London’s (TfL) recent

That changes from April 2021, when would be to cap rental growth within agreement with Grainger is a prominent

Government plans to restrict the tenancies to CPI plus a small premium. example of a trend that Savills expects

scheme, and in March 2023, when the to see much more of in the coming

scheme is set to end entirely. Without Capital complications years: public/private partnerships. The

this source of Government support, Uncertainty regarding the possibility TfL and Grainger partnership combines

demand for rental homes will rise as of rent controls and the Draft New the two entities’ expertise, capital, and

fewer households are able to access London Plan may be why regional land to unlock delivery of 3,000 BTR

home ownership. schemes now make up a majority of homes across London.

Last year also saw the publication BTR homes under construction. With mounting pressure on

of the Letwin Review, which reported There is a caveat to John Healey’s government departments to release

on housing delivery rates on large comments on Labour’s rent control more land and reduce reliance on

residential sites in England. One of plans to consider. The Shadow central government funding, we expect

the key recommendations of that Housing Minister has said that their to see more deals like this over the

report was to encourage a greater policy would support introducing remainder of this parliament.

diversity of tenures on large residential more assertive rent control measures In addition to urban apartment

developments, including BTR. in areas where rental affordability is schemes, we expect to see an increase

More recently, Government most stretched, such as London. For in activity from investors developing

announced that it would end no- now, the detail behind this policy house-led schemes in suburban

fault evictions. While Build to Rent aspiration remains unclear. Should locations. This type of housing appeals

landlords are unlikely to want to Labour reveal plans to introduce to a different part of the market from

evict residents without good reason, rent caps, however, this could make flats, which comprise most Build to Rent

losing this option makes BTR look London look far less appealing for development to date. PRS REIT has

riskier as a long-term investment. It BTR investors. been notable in investing in houses to

could seriously delay redevelopment The Draft New London Plan, rent so far, but firms such as Grainger,

if a landlord needed to go through a currently still in examination, could Legal & General and M&G all have BTR

lengthy Section 8 court hearing for also make it much more difficult to houses in their pipelines.

every home on a scheme, for example. deliver BTR schemes.

16UK Operational Real Estate

£544 bn Size of the UK BTR

sector at full maturity

The Collective, Old Oak

In particular, some of the Mayor offering, and better and worse

of London's Further Suggested access to public transport. In Resident amenities

Changes to the plan include allowing the case of PBSA, developers The management of The Collective

boroughs to set affordable housing must also consider proximity to bought the firm’s scheme at Old Oak

requirements on BTR schemes universities, as there is often a Common in October 2018 for £115m. It

that include social rent homes, steep downward gradient in the is the only stabilised co-living scheme in

where the homes are managed by rent you can charge as you move the UK, and comprises 546 residential

a registered provider. Since most further away from campus. BTR units with associated amenity space and

BTR investors are not registered schemes must consider these commercial units.

providers, this would make it factors, taking heed of proximity

impossible for single BTR blocks to the prime localities in their

to remain in single management. wider area and setting rent These events can help foster a sense

Where this is a requirement, the expectations accordingly. of community, encouraging residents to

likelihood of securing investment When providing amenities stay in the scheme longer and decreasing

is poor at best, potentially making on schemes, BTR developers voids. Even without events, there are ways

some BTR development in London need to think about what provides to promote communities in schemes: in

much less attractive. actual value to residents as PBSA, shared study and recreation spaces

opposed to headline-grabbing bring people together organically.

Learning from student novelty. PBSA operators often Finally, it’s vital to consider how a

There are a few things the help their residents with setting scheme interacts with its surroundings.

BTR sector can learn from the up events, providing space Plans for PBSA schemes often meet

more established PBSA market and logistical guidance. We’ve objections that they will “studentify”

to help make the most of schemes. seen a similar approach at The the surrounding area, which means they

Firstly, it’s important to Collective’s co-living space at have to work even harder to get local

consider location at a micro level. Old Oak Common, where staff communities on side. Ensuring that a

Cities are not homogenous: they support residents running yoga scheme engages and interacts with its

have areas of high and low value, classes, business coaching and surroundings, regardless of tenure, will be

stronger and weaker amenity cooking courses. key in securing public support. ■

17UK Operational Real Estate

Retirement living

Care homes and retirement housing each face challenges, but the demand

for these products will only grow as the country's population ages

Retirement housing

Retirement housing has been a Villages and English Care Villages Size matters

feature of the UK housing market in 2017, and has recently made Prior to 2000, 80% of retirement

for decades. The bulk of existing headlines by launching its urban housing supply was on smaller

stock is sheltered housing for social retirement brand Guild Living. ReSI schemes with fewer than 50 homes.

rent, built using grant funding in the REIT has been building its portfolio More recently, the bulk of supply

1970s and 1980s. Much of the balance of retirement housing, purchasing has come from larger developments,

is made up of owner occupied homes, schemes from Aviva and Places for with schemes of over 50 homes

built by specialised housebuilders People. And Goldman Sachs-backed making up 56% of supply in the ten

such as McCarthy & Stone. Riverstone aims to build a London years to 2018.

A more investible market is retirement housing pipeline worth As the sector continues to move

beginning to emerge, however. more than £2 billion over the next towards a care-based model,

Demographic and affluence trends two years. developments will get larger

show there’s huge potential: an ageing More recently, some developers to incorporate efficiencies of

population with vast stores of housing have departed from these traditional scale. Larger schemes can also

wealth is an attractive customer base. models. Auriens and Birchgrove will accommodate a range of tenures

New Zealand, the US and France shortly begin letting retirement more f lexibly, as demonstrated by

serve as examples of the potential homes for private rent, each targeting the Extra Care Charitable Trust

for retirement housing to grow into a very different price points. While on their large, multi-tenure

large scale and appealing asset class. retirement PRS is unusual today, developments.

there are excellent reasons for older The largest retirement village in

The sector so far people to choose this tenure. the UK today is Lark Hill Village in

There are 730,000 retirement housing In the case of Goldman Sachs- the West Midlands, with 340 homes.

units across the UK, according to funded, luxury London scheme In the future, this size of scheme

the Elderly Accommodation Counsel Auriens, customers will avoid a could become the norm.

(EAC). More than half these homes, stamp duty bill equivalent to over a

52%, were built or last renovated over year’s rent by choosing not to buy. Risk and mitigation

30 years ago. In the case of more mid-market Retirement housing currently sits

There are two models for Birchgrove, renting enables residents across two planning use classes.

developing retirement housing for to unlock the equity held in their The C3 use class is the same as for

sale. The first, and simplest, is largely former homes. The nation’s largest regular residential developments,

indistinguishable from the traditional retirement housing developer, and requires a developer to provide

housebuilder sale model, with a price McCarthy & Stone, has also started affordable housing. The C2 use

premium to reflect the added cost of offering homes to rent in its schemes. class requires some kind of care to

providing communal facilities such There is significant untapped be provided on site, but without an

as a residents’ lounge, café or gym. potential in retirement homes for affordable housing contribution.

Alternatively, a developer might charge rent. While many older households Guidance on the amount and

an “event fee” – a charge when the own their homes, a rent-to-rent model type of care needed to qualify as

resident sells their property, usually for could help them move into retirement C2 is inconsistent across the country,

a proportion of the sale value – to fund housing while retaining ownership leading to uncertainty over whether

these shared amenity spaces. of their family home and avoiding a potential retirement living scheme

It’s only in the last few years that stamp duty. will be viable. In London, guidance is

we have started to see institutional We estimate that more than 570,000 clearer, in that C2 developments are

investment into the sector. Legal & households over 75 could afford to rent expected to provide both care and

General assembled Inspired Villages a retirement home using the rental affordable housing, putting them at

from its acquisitions of Renaissance income from their main home. a disadvantage to C3 schemes.

18UK Operational Real Estate

£244 bn Size of UK retirement housing

sector at full maturity

Figure 8 Retirement living schemes by number of units

180,000

160,000

Number of retirement living properties by size of scheme

140,000

120,000

100,000

80,000

60,000

200+

40,000 150-199

100-149

50-99

20,000

25-49

10-24

0-9

0

1969-1978 1979-1988 1989-1998 1999-2008 2009-2018

Source Savills Research using EAC

Clarity on what level of care is residents and developers, enabling that at full maturity the UK’s

required on C2 developments, faster retirement housing delivery. retirement housing sector could

perhaps through an update to be worth £244 billion.

National Planning Practice Evolution To put this figure into context,

Guidance, would reduce this We estimate that the 730,000 we have calculated the value of

uncertainty and could unlock more retirement housing units across housing owned and occupied by

retirement housing development, the UK are worth just under £100 the over 65s to be over £1.6 trillion.

particularly if it levelled the playing billion. Accounting just for today’s Much of the increase in the value

field for schemes in London. over-75 population, we believe that of the retirement housing sector

Some retirement living the retirement living sector could could be funded through older people

providers have ‘event fees’, charging grow to 1.7 million homes at full choosing to downsize. The challenge

former residents a proportion of maturity. This is an increase of 138% here will be providing a product

the property’s value on resale. Poor over current stock. Accounting for that can tempt these older residents

communication of what these fees population growth, this figure would out of a home they’ve likely lived in

pay for and when they are levied has be even higher. for decades.

harmed the sector’s reputation. We noted in our earlier publication The potential benefits of a

Government has promised to (Spotlight on Retirement Living, 2018) larger retirement living sector are

implement the Law Commission’s that the supply of sheltered homes substantial. Offering homes that allow

recommendations for event fee reform, for social rent is in line with need. older people to age in place, retirement

including restrictions on when they This additional stock will, therefore, villages can help free up much needed

can be charged and standardised comprise a mix of market sale and family housing, reduce the nation’s

information to be included in intermediate homes, either privately social care costs, and address feelings

marketing and sales documents. New rented, shared ownership, or new of isolation and loneliness in the older

Zealand, which has a better-established products such as rent-to-rent. The population. Based on research from

retirement living sector, enacted mix of different housing tenures and Demos and The Aston Research Centre

similar legislation back in 2003. types required affects the values of for Healthy Ageing, government saves

This suggests that greater these homes. between £1,000 and £1,540 per year for

transparency around event fees Accounting for the tenure of each person moving into retirement

could help rebuild trust between this additional stock, we estimate housing with care.

19UK Operational Real Estate

85% Increase in care home investment

in 2018 vs 2017

Care homes

Almost 420,000 people live in elderly Risk and mitigation of the UK’s 470,000 care beds are

care homes in the UK, accounting for Four Seasons has dominated recent in dated buildings with facilities

just under 15% of the population aged elderly care headlines with their that are no longer fit for purpose.

over 85, according to LaingBuisson fall into administration. This The number of care beds is

figures. The ONS projects a 36% comes alongside a 33% increase in decreasing year on year, as unviable,

increase in the 85+ population by 2025, insolvencies for elderly and disabled smaller or older homes close faster

and we expect to see a corresponding care homes between 2017-18 and than the restricted rate of new

increase in care home demand. 2018-19, according to our analysis of development. As stock levels fall

However, despite the demographic Insolvency Service figures. and the number of older people

drivers supporting care home demand, Care homes are funded through increases, we expect a swell

some operators are facing financial a mix of sources. Residents with of demand for new care home

pressure due to a heavy reliance on more than £23,250 in savings (more development over the next few years.

local authority-funded residents. in Wales and Scotland) must pay While there are many reasons

for care themselves, while local a person might move into a care

Investment authorities fund care for those below home, one of the most common

Elderly care home investment was this savings threshold. causes is the onset of dementia. The

£1.3 billion in 2018 across 26 deals. Local authority funding for care Alzheimer’s Society reports that

That’s almost double the investment homes is severely restricted, with the 70% of elderly care home residents in

we saw in 2017, £0.7 billion, despite state paying substantially lower rates 2019 had dementia or severe memory

a similar number of deals (24). Net than an individual funding their own problems, and one in six people

initial yields averaged 6.6% in 2018, care. This puts financial pressure on aged over 80 across the UK suffered

slightly down from 6.9% the previous care homes with a high proportion from the illness. PHE estimated

year. While average yields only of local authority-funded residents. that 645,000 people aged over 65 in

compressed by 22 basis points, last Without reform, we are likely to England had dementia, of whom just

year also saw three transactions with see more care homes close as they two thirds (68%) had a diagnosis.

yields below 4.0%, with Aberdeen struggle to remain profitable on local These conditions require careful

Standard paying a record low 3.75% authority fees. management. While retirement

for Moore Place in Esher. In spite of these funding housing may be suitable for helping

Just two deals made up more than challenges, the UK’s ageing older people live independently

half the value invested last year: population will drive growing without care for longer, even the

Aedifica’s acquisition of the Forest need for elderly care. For the many best-designed retirement village

portfolio from Lone Star, and Chinese care home operators attracting a cannot hope to care for dementia

private equity firm Cindat’s purchase high proportion of private paying patients without specific care

of HCP’s Ice portfolio. This interest residents, it’s possible to deliver facilities and staff on site.

from overseas marks a change from strong and sustainable returns. As the population with conditions

2017, when 74% of investment volume such as dementia grows, the need

in elderly care homes was domestic. Evolution for care homes and dementia care

The long lease lengths and indexed We estimate that, in pure numbers facilities will rise in turn. We would

rents on care home leases make them terms, the amount of care home expect demand for retirement

attractive for investors. Leasing to an places available today is broadly in housing to be strongest on village

operator means investors can expect line with need. schemes offering the option of

a stable, steady rental income stream, That’s not to say there is no residential and dementia care on

similar to more established property potential for growth, however. site, so that residents are able to age

sectors such as offices. As with retirement housing, many in place.■

20UK Operational Real Estate

Conclusions

Operational real estate in the UK offers exciting

growth opportunities for investors and developers

Operational real estate is a broad these operational sectors. retirement housing market on

term, covering a huge range of sectors Worth over £50 billion, we predict the one hand and the more mature,

at different stages of maturity. the rising student-age population liquid care home market on the

and expansion into new markets will other. The challenges they face

On one end of the spectrum, the be the main drivers of growth. The are very different: for care homes,

student accommodation and care sector faces challenges in the form of restricted local authority funding;

home markets are highly liquid. Brexit and the planning system, but for retirement housing, lack of a

Comparable information and debt can boast a long history of strong, proven track record. However, both

finance are both readily available. stable returns in the face of political benefit from strong demographic

Some way further along that spectrum and economic turmoil. support, with the UK’s 75+ population

we have Build to Rent, which projected to grow more than a third

continues to evolve as landmark Build to Rent has come a long way by 2030. Increasing demand for

schemes demonstrate a strong track in the last decade, growing from a retirement living will force us to

record. And at the far end, we have niche topic at investment conferences find solutions to these challenges,

institutions taking their first steps in to one of UK real estate’s most as the sector grows in value from

the retirement housing sector. exciting asset classes. Worth a little £162 billion now to £235 billion at

under £10 billion today, we predict full maturity.

Common to all these sectors is it has capacity to grow to more than

the recognition that investing in £500 billion in value at full maturity, In total, the UK’s residential

where people live is attractive. The accounting for around 1.7 million operational real estate is currently

fundamental demographic and households. The volume of funds worth £223 billion. Growing these

economic changes supporting these being raised and invested in this sectors to full maturity will require

sectors are difficult for investors sector, even in the face of political investors to hold their nerve in the

to ignore. Institutional interest uncertainty, demonstrates the sheer face of political headwinds and

will continue to grow as these asset strength of conviction investors have economic uncertainty. Overcoming

classes mature and can increasingly in BTR. those challenges, however, will

demonstrate their track record. increase the value of these sectors

Retirement living is perhaps the fourfold to £880 billion.

The student accommodation most diverse of all these operational That is an opportunity worth

market is among the most mature of real estate sectors, with the nascent getting excited about.

21UK Operational Real Estate

Figure 9 The bluffer’s guide to operational residential real estate

Term Explanation

Operational residential Property owned and managed by professional investors

real estate where people live. Includes student accommodation, Build

to Rent, and retirement living.

PBSA Purpose-built student accommodation - student halls.

PRS Private rented sector. Can be homes owned by individual

landlords or professionally managed, purpose-built homes

for rent.

Buy to let Small scale investment into privately rented housing,

often financed with a mortgage.

BTR Build to Rent. Homes that are professionally operated

for rent by large-scale investors.

Multifamily Professionally managed blocks of flats to rent:

so called because many families live in the one building.

Single family Professionally managed houses to rent: so called because

usually only a single family lives in each building.

Senior living Homes for older people (typically 75+). Includes retirement

housing and care homes.

Retirement housing Homes purpose-built for older people, often incorporating

common amenity spaces such as lounges, cafes and spas.

Care homes Facilities with higher levels of social and medical care

provision for people with more serious care needs.

C3 A residential planning use class. C3, dwelling houses,

covers standard housing, BTR and retirement housing

without care.

C2 A residential planning use class. C2, residential institutions,

covers care homes and retirement housing providing

elements of personal, social and/or medical care.

Institutional investor Large, long-term investors such as pension funds and

insurance firms. Typically these investors seek long-term,

stable returns.

REIT Real Estate Investment Trust. Provides investors tax-

efficient exposure to property assets.

Risk-free rate The rate of return an investor would receive from an

investment with zero risk. In practice, no such investment

exists, but gilt rates or swap rates act as a good proxy.

22Savills Residential Research

We are a dedicated team with an unrivalled reputation for producing well-informed and accurate analysis, research and

commentary across all sectors of the UK property market.

Lawrence Bowles Lucian Cook Jacqui Daly Nicholas Gibson Richard Valentine-Selsey

0207 299 3024 0207 016 3837 0207 016 3779 0207 409 8865 0203 320 8217

lbowles@savills.com lcook@savills.com jdaly@savills.com nicholas.gibson@savills.com richard.valentineselsey@savills.com

Savills Operational Capital Markets

We provide our clients with valuation, consultancy and transactional advice in respect of residential investment and

development, student accommodation, healthcare and retirement living. We have corporate finance and debt advisory

teams that are embedded across the division. Our track record across the UK and Europe is unparalleled, having advised

on over £10bn of investment in the last 24 months alone.

Peter Allen Andrew Brentnall James Hanmer Craig Woollam Samantha Rowland

Executive Director, Director, Director, Director, Director, Head of

Head of Operational Residential Capital Markets Head of UK Student Head of Healthcare Healthcare Valuation

Capital Markets UK Board Member Investment 0207 409 9966 0207 409 9962

0207 409 5972 0207 409 8155 0207 016 3711 cwoollam@savills.com srowland@savills.com

pallen@savills.com abrentall@savills.com jhanmer@savills.com

Joe Guilfoyle Andrew McMurdo Peter Blake Craig Langley

Director, Head of Director, Director, Head of National Director, Head of

Corporate Finance Head of Debt Advisory Development Consultancy PRS Valuations

0207 016 3767 0203 810 9889 0207 016 3707 0207 409 8093

joe.guilfoyle@savills.com andrew.mcmurdo@savills.com pblake@savills.com clangley@savills.com

Savills plc is a global real estate services provider listed on the London Stock Exchange. We have an international network of more than 600 offices and associates throughout the Americas, UK, Europe,

Asia Pacific, Africa and the Middle East, offering a broad range of specialist advisory, management and transactional services to clients all over the world. This report is for general informative purposes only. It may

not be published, reproduced or quoted in part or in whole, nor may it be used as a basis for any contract, prospectus, agreement or other document without prior consent. Whilst every effort has been made to

ensure its accuracy, Savills accepts no liability whatsoever for any direct or consequential loss arising from its use. The content is strictly copyright and reproduction of the whole or part of it in any form is

prohibited without written permission from Savills Research.

2333 Margaret Street London W1G 0JD +44 (0)20 7499 8644

You can also read