The Sochi Olympiad: An Introduction to 2014 - July 2008

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

The Sochi Olympiad: An Introduction to 2014 July 2008

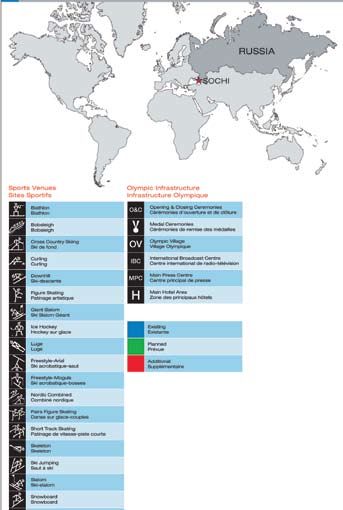

Sochi 2014 – Main Sites

Source: Sochi 2014

Purchase price: £60 (including VAT)

© Copyright material of Forrest Research Limited. Distribution

or storage including databasing by any means including,

without limitation, electronic distribution is not permitted

without the prior authorisation from Forrest Research.

The Sochi Olympiad:

An Introduction to 2014

1. Executive Summary

R Sochi is the first winter Olympiad to be delegations from a variety of markets have

held in a sub-tropical resort, and the already started their respective pitches.

combination of its Black Sea coastline R The main contracts will be awarded at a

and mountain skiing facilities, less than national level by the Olympic Organising

an hour from the coast, offers multi- Committee (contacts are available) but at

season tourist potential. Few global best contracts will be awarded to joint-

centres can compete with the proliferation ventures, but most probably sole Russian

of leisure activities that Sochi could entities.

realistically offer throughout each season

R At a regional level the Krasnodar Krai

– provided sufficient investment capital is

administration will be involved in transport

made available.

infrastructure development to assist the

R The successful implementation of the Olympiad, there are also a range of

Sochi Winter Olympiad 2014 is and will development projects not associated with

remain a principal goal of the current the Olympics, and common to most

Russian administration, which realistically aspiring Russian regions which should be

should now remain in office till 2016. The judged on their own commercial viability

loss of prestige as a result of any failure and with the usual caveats.

is too great to countenance. It will not be

R It is at the City of Sochi level that the bulk

allowed to fail. As a result the large

of Olympiad associated investment and

Russian Corporates have been tasked to

business opportunities for British

cover specific projects to ensure their

companies are realistically available.

completion. Accordingly the scope for non-

Few if any are actually Olympic

Russian corporates in the larger projects

designated, they are largely background

will be limited.

service, logistic and infrastructure

R The central programme of infrastructure opportunities. The key to their success is

development directly associated with the that they provide the economic and

Olympics – the Federal Target Programme physical framework within which both the

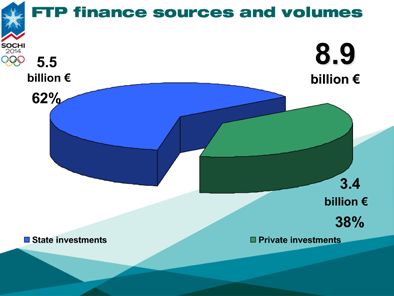

(FTP) for the Development of Sochi as a Olympiad and Sochi Resort will achieve

mountain climate resort 2006-14 – will their success.

generate at least US$ 12 billion of

R Sochi will be one of the most dynamic

investment at the Sochi Olympic Park and

components of the Russian economy at

in the ski resort of Krasnaya Polyana (the

least until 2014 given the massive level of

Red Clearing).

direct and indirect investment, and it is

R Other non-direct investment projects this flow of capital expenditure

associated with the development of Sochi (conservatively estimated at the

as a mountain climate resort are currently equivalent of US$40 billion) that will fuel

equivalent to US$28 billion, and it is here rapid growth in the wider parts of the

that British businesses could start to Sochi economy.

make an impact. Official and business

R Major transport links are being upgraded, infrastructure developments will

not just in Sochi but throughout provide an additional motor, and growth

Krasnodar, that will stimulate growth, but up to and after the Olympiad is

of particular interest is the completion of expected to average a minimum of 6%

the refurbishment of Sochi International in real terms per annum.

Airport – the opening of the Austrian R Despite the potential re-emergence of

Airline serviced route to Vienna in April is current account deficits beyond 2011,

the first of many anticipated. no serious balance of payments

pressures anticipated in the period up

Political stability until the Olympiad.

R This March’s Presidential election R Inflation will continue to be difficult to

provides the basis for political stability dampen but remain constrained at

for the next 8 years, with President present level (in range of 9-12%

Medvedev in all likelihood serving average per annum).

two terms.

R Rouble to continue to experience

R Regional stability seems assured given upward pressure but authorities to

the progressive re-ordering of Kremlin- continue policy of achieving effective

Provincial devolution and the ending of under-valuation of the currency against

asymmetric devolution of power to major trade partners.

semi-autonomous Republics.

R Specific regional growth hot spots and

R Sochi will provide an effective enclave developments to continue to

administrative process to deliver the be a feature of overall pattern of growth

Olympiad, and parochial issues will not – with Sochi and to a lesser extent

be allowed to interfere with the issue. Krasnodar, forecast to be amongst the

R The Russian-Georgian impasse of top performers.

Abkhazia is likely to remain an impasse

To successfully bid, identify projects your

with any solution frozen until post-2014

company can realistically compete for and

despite the provocation over Kosovo’s

successfully implement:

UDI.

R Olympiad projects

Economic stability R Associated projects – a key opportunity

R Despite major liquidity pressure in the area (infrastructure/housing/transport/

Banking System, the Kudrin Put hotels/Olympic services/training &

(making available the massive language)

stabilisation fund resources to support R Sochi resort projects – the longer term

banks if required) will support liquidity. opportunity in a high growth area.

R Growth will continue to be heavily

determined in part by oil prices,

although projected capital

The Sochi Olympiad:

An Introduction to 2014

Table of Contents

1. Executive Summary............................................................................3

2. National Context....................................................................................6

a. Geography. .......................................................................................................... 6

b. History.................................................................................................................. 8

c. Constitutional Settlement............................................................................. 10

d. Political Climate.............................................................................................. 11

e. Economy........................................................................................................... 14

3. Regional Description: Krasnodar Krai.......................... 18

4. City of Sochi............................................................................................. 23

5. Olympic Bid............................................................................................... 26

6. Olympic Facilities – ........................................................................ 30

Summary of Principal Projects

7. Structure of Olympic Management ............................... 32

and Implementation

8. Olympic Associated Principal ............................................. 36

Principal Upgrade

9. Ancillary Opportunities................................................................ 38

10. Sochi Working Party....................................................................... 40

11. Contact Details. ................................................................................... 41

3 National context

a. Geography

Population (2007): 143,377,752

Land area: 17,075,200 sq kms

Capital: Moscow

Main Cities (1 mln plus):

Moscow, Saint Petersburg, Novosibirsk, Nizhny Novgorod, Yekaterinburg, Samara,

Omsk, Kazan, Chelyabinsk, Rostov-on-Don, Ufa, Volgograd, Perm

The City of Sochi, within which the ski resort of Krasnaya Polyana and the central

Winter Olympic complex are located, is the most southerly part of the western

Russian Federation. The City is located within Krasnodar Krai (defined as a Federal

subject within the constitution of the Russian Federation), which itself forms part of

the Southern Federal District – one of the seven federal okrugs (districts) through

which central or federal government activities are administered across the Federation.

The Russian Russia and the Wider Region

Federation is

the world’s

largest

country in

tems of land

mass with

some 11

seperate time

zones. Given

this size, the

climate of

Source: Forrest Research

Russia is

extremely varied ranging from extreme Arctic conditions in the more northern regions

and much of Siberia to generally more temperate conditions in the south. In addtion

to its extensive coastlines, principally with the Arctic, Pacific but also the Black and

Caspian seas, it shares borders with approximately 14 UN member states. Of these,

the most problematic remain those which its shares with Georgia, primarily as a

result of seccessionist conflicts in Abkhazia and South Ossetia, but also regarding

the neigbouring and troubled Russian region territory of Chechnya.

The Sochi Olympiad:

An Introduction to 2014

As a territory that straddles both Europe and Asia, the Russian Federation does not

fit neatly into the common definitions of either Europe or Asia, indeed the designation

Eurasia only serves to highlight the difficulties of categorising the country. The thrust

of diplomatic efforts, since Russia’s emergence as an independent state, has been

to establish an effective regional role and global position. In the immediate aftermath

of the collapse of the Soviet Union, the CIS (Commonwealth of Independent States)

was established as a regional interstate organisation ultimately comprising: Armenia,

Azerbaijan, Belarus, Georgia, Kazakhstan, Kyrgyzstan, Moldova, Russia, Tajikistan,

Ukraine, and Uzbekistan, with Turkmenistan as an associate member. The CIS has,

however, struggled to establish an effective role given the difficulty of reconciling the

region’s difficult historic legacy and the aspirations of many its members to exercise

their recently acquired independence. Furthermore the expansion of both the EU and

NATO eastwards, has offered alternate regional access, as has the opening up of

the common borders with Turkey and China.

Krasnodar Krai is located at the western edge of the Caucasus mountain range with

the bulk of the territory on the Kuban-Azov plain, encompassing a total area of 76,000

square kilometres. The total length of the internal border is 1540 kms, of which some

740 kms comprise coastline. Within the Southern Federal Okrug, to the north and

north-east, Krasnodar Krai borders the Rostov region, to the east Stavropol, to the

south and east Georgia (Abkhazia) and the Republic of Karachayevo-Cherkessia, whilst

to the south are the coastlines of the Azov and the Black Seas. Whilst the krai territory

wholly encompasses the separate administrative unit of the Republic of Adygea.

Notwithstanding the recent unilateral declaration of independence by the former

Serbian province of Kosovo, it is neither in Russian or Georgian interest to seek a

immediate or even medium-term change to the current status quo. Indeed, the impact

of Sochi being awarded the XXIInd Winter Olympiad, should serve to mollify existing

disputes, calm diplomatic relations and sustain current de facto territorial settlements.

However, as recent incidents have highlighted, the Russo-Georgia relationship can at

times suffer from acute stress. The security provision for the Olympiad will

nevertheless be understandably tight.

Russia responded to Kosovo’s declaration of independence by strengthening ties

with Abkhazia, although falling short of officially recognizing the breakaway region.

The Abkhaz authorities are apparently attempting to promote a Taiwanese solution,

with Russia adopting international practice similar to that accorded Taiwan, informally

acknowledging and trading with the territory while not officially recognizing it. This

indeed appears to be the case with Russian authorities suggesting that as 2014

construction commences, it will purchase Abkhaz construction materials and hire

workers from Abkhazia. This has caused disquiet within the EU, with the Commission

pushing for a policy of respect of Georgia’s sovereignty and territorial integrity.

The Krasnodar region is situated on the same latitude as northern Italy and Southern

southern France. As a result, the climate of the greater part of Krasnodar region is

moderately continental, whilst at the Black Sea coast it can be termed sub-tropical.

The average temperature during January is from -5C in the mountains to 0C in the

plain, whilst in July it ranges from 13C to 24C respectively. The mean annual

precipitation is in the region of 400 mm in the plain and over 3200 mm in the

mountains. The usual duration of the agricultural season is approximately 260 days,

boosted by the rich cherrozen (black earth) soils prevalent in the plains. The

favourable almost Mediterranean climate, warm seas, natural mineral springs and

medicinal mud have enabled the Kuban, and Sochi in particular, to promote a

positive ecological and environmental image, and accordingly remains one of the

most popular tourist resorts within the Federation.

b. History

Independence: 24th August 1991

National Day: 12th June

The ethnic origins of the Russian peoples lie in the first millinenia and one of the

earliest Russian states, the Moscovy principality, was established in the 12th

century. The complexity of this history is reflected by the fact that whilst the official

language is Russian, over 100 other officially recognised languages are spoken. In

addtion, although Christianity is the principal religion, with the Russian Orthodox

Church predominant amongst ethnic Russians and other Slavs, a range of other

religions are represented. The large pre-1917 Jewish population has been depleted

by war and revolution, although a signifcant proportion remain and not just within the

Birobidzhan autonomous district. The main concentrations of adherents of Islam are

among the Tatar, Bashkir and Chuvash peoles of the Middle Volga, and the peoples

of the northern Causcases, including the Chechen, Ingush, Karbardins and the

peoples of Dagestan. Buddhism is main religion of the Buryats, the Yyvans and

Kalmyks. Furthermore, whilst both the Imperial Russian state and its successor the

Soviet Union are crucial factors in the formation of Russia’s historic legacy, it is

important to note the fact that in its current constitutional formation and geographic

extent that the Russian Federation is a relativley new state.

Similarly the settlement of the area that now constitutes the Krasnodar Krai is

comparativley ancient, whilst the current political structure of the Krai is relativley

recent. As a result of the favourable natural conditions and the mild climate,

archaeolgical evidence of settlement dates to the earliest epochs. Pontian Greeks

established city colonies in the Kuban, whilst in succeeding historic periods the

regions was settled by the migrating hordes of Hun, Khazars, Pechenegs, Polovets,

The Sochi Olympiad:

An Introduction to 2014

and Mongol-Tatars. In the medieval period, trading posts of primarily Venetian

merchants, including Marco Polo, established trading colonies, maintaining close

relations with the Adyegan tribes and through them access to the Silk route and

China. The first evidence of Slavic settlement dates to Xth Century, with the

foundation of the Russian town of Tmutarkan, which existed till the Mongol-Tatar

invasion on the Taman peninsula. Subsequently, the Kuban came under the

hegemony of the expanding Ottoman Empire. The second wave of Russian settlers

were related to the dispersal of the surving rebels associated with the revolt of

Kondratia Bulavina and Ignat Nekrasov. However, sustained Russian settlement of

the Kuban dates to two Russian-Turkish wars of XVIII century, particuallry after the

success of (the American) Admiral John Paul Jones in the Azov sea battles. As a

result, in June 1792, Catherine the Great granted the lands of the Taman Peninsula

to the Black Sea (Zaporozh) troops, under Beily, as a military frontier buffer to the

Turks. Prior to the establishment of the Soviet Union, the the region was

administered as the Kuban Region and the Black Sea Province. These administrative

areas were combined into the Kuban-and-Black Sea region in 1920. The northern

Caucasian region was formed in 1924 and in 1937 the Azov-and-Black Sea Region

was divided into Rostov region and Krasnodar region, the later including the

Adygeyan autonomous oblast. In 1991 the Adygeyan Region was re-organised as the

Republic of Adyegya, a seperate administrative entity from the Krasnodar Krai,

although the Republic lies entirely within Krasnodar Krai.

In the comparatively short history of the Russian Federation since its emergence as

an independent state, the second decade of its existence has been charecterised by

robust rates of GDP growth and the increasing predictability and pragmatism of the

government process. Understandably however, both the structure of the economy

and the constitutional settlement are still dynamically evoloving. The creation of an

independent state framework, the establishment of the foundations for a market

economy and most notably the emergence of a pluralist political system, were all

products of the often chaotic period of the first decade. The asymetric devolution of

power to the then 89 constituent Federal Subjects (regions) of the Federation

created a number of anomalies but helped preserve the basic integrity of the

Federation. Under the adiminstration of President Putin a more ordered, coherent

and intelligible system of devolution has been driven through. Moreover it is worth

stating that in succeeding the previous incumbent President Yeltsin, Putin achieved

the first constitutional democratic transfer of power in the Russian people’s long

history. Accordingly, the constitutional process has been further strengthened by the

successful election and subsequent innaugration of Dmitri Medvedev as the

Federation’s third Presdiential incumbent.

c. Constitutional Settlement

Constitution adopted: 12th December 1993

System: Presidential Republic with bicameral legislature

The present Constitution of the Russian Federation came into effect toward the end

of 1993, following approval via a Federation-wide plebiscite. This constitution sets

out the parameters of the Russian state as a republican democratic Federation

founded on the rule of the law. The constitutional framework provides for formal

separation of power between independent legislative, executive and judicial

branches. Furthermore, the constitutional structure favours a multi-party system,

political pluralism and a secular state structure with recognised religious

associations equal before the law.

The initial 1993 constitutional settlement created 89 members (federal subjects) of

the Russian Federation. There has however been a subsequent, if slow, process of

amalgamation, due to demographic and economic factors, between some of the

more remote Federal Subjects. These federal subjects essentially corresponded to

regional administrative districts that emerged during the political autarky of the

1930s and 1940s. Almost all possess distinct geographic features, historic or ethnic

legacies that provide a degree of local legitimacy that ensures they are real factors

in the political process. Their latent strength is also recognised in that whilst Russian

is the declared national language, constituent peoples of the Federation have

guarantees protecting their native languages. During the 1990s, a number of regions

were able to secure a high degree of devolution if not effective autonomy, this was

particularly the case with some of the constituent Republics with strong ethnic

identities. This system of asymmetric federalism was not conducive to effective

administration, exacerbating regional disparities and consolidating local elite control

before effective local democracy could flourish. Under both Putin’s administrations

there was an apparently concerted campaign to regularise the process of devolution

and reclaim some of the decentralised powers back to the Kremlin to ensure that

regional political leaders conformed to the thrust of Federal government strategy.

This strategy seriously compromised local autonomy, and although it did not

completely erode it, ensured that the process was more ordered, intelligible,

predictable and compatible with the Kremlin aspirations.

Furthermore, the Kremlin attempted to secure greater uniformity with the creation of

an additional administrative level in between the Kremlin and the federal subjects.

Seven Federal Okrugs (districts) were established by President Vladimir Putin in May

2000, and were initially seen as an attempt to effect economies of scale and co-

ordinate infrastructure planning. Whether it is significant depends on ones point of

10The Sochi Olympiad:

An Introduction to 2014

view, but the borders of the okrugs are congruent with those of the military districts

and comparable to the Soviet-era economic planning districts. Each region includes

from between 6 to 17 oblasts and autonomous republics. The okrugs were

established to strengthen the control of the centre over the regional governments

and for security. The governors of the regions are selected by the President. Their

responsibilities include identifying and recommending candidates for oblast governor

positions to the President. The envoys also insure that federal policies are put into

practice in the regions. Significantly however, the crucial relationship remains that

between the Kremlin and the federal subjects, with little discernible intermediation

on the part of the federal okrugs.

The constitution identifies the separate areas of authority of the Federation, as

distinct from that of the joint authority of the Russian Federation and the members of

the Russian Federation. It also establishes the relationship between federal laws,

federal constitutional laws and the laws and other normative acts of the subjects of

the Russian Federation. The powers of the federal executive bodies and the

executive bodies of the members of the Russian Federation are defined.

The head of state of the Russian Federation is the President, elected by universal

direct suffrage every four years. According to prevailing interpretations, the same

individual can only stand for two consecutive terms of office, and, although it has yet

to be tested constitutionally or in practice, after an interregnum a former incumbent

may apparently return for further terms of office. The President appoints the

government and following recent legislative revisions appoint the regional governors.

d. Political Climate

President: Dmitri Medvedev

Prime Minister: Vladimir Putin

Next election (Presidential): March 2012

Electorate: 109,145,517

The restoration of the authority of the Kremlin during the Putin Presidency has been

variously interpreted, by some as a move back to a more autocratic form of

government, by others as the creation a more rational and effective state structure.

That this shift from a centrifugal to a centripetal direction of political power has been

paralleled by a similar apparent shift in the balance of public and private

participation in the economy in favour of state and quasi-state entities, has raised

serious international concerns over the future direction of Russia. Although it is

undeniable that the space available for civil society has contracted over the past

decade, it is questionable that the near anarchy of the 1990s offered real

11democratic opportunities within a law-based framework. Furthermore, the substantial

and real failures, both in political and economic terms, of the liberal market

reformers during the 1990s, coupled with the failure of the Communists to transform

themselves into a market-orientated social democratic party, has ensured that there

is no really credible alternative to the administration. This is particularly the case,

given that the Putin administration was able to continually deliver strong economic

growth, including the broad-based delivery of rising per capita incomes.

As a result, political aspirants have increasingly sought to be associated with the

Kremlin. This tendency has been further facilitated by the tightening of the electoral

process with the move away from single-member constituencies to multi-member

party-list elections, with the electoral threshold increasingly raised. Moreover, with

seats assigned by the largest remainder method to the lists of parties winning a

minimum of 7.0 percent of the national vote, the opportunity for oppositional groups

has been yet further constrained. Accordingly pro-Kremlin parties increased their

control of the Duma in elections in December last year, with, of the political

groupings offering an alternate strategy, only the Communists with sufficient

organisational capacity to gain a foothold in the lower chamber. The Liberal

Democrats are supportive of the Kremlin strategy, and Putin especially, despite

claiming to be an independent, if somewhat quixotic, political formation. The results

of the Duma election provides the Kremlin with a parliamentary majority large enough

to revise the constitution, given the restructuring of the composition of the Federal

council (the upper chamber), making it a much more compliant political entity.

Duma election Results December 2007

Party Votes % Seats %

United Russia 44,714,241 64.30 315 70.0

Communist Party 8,046,886 11.57 57 12.7

Liberal Democrats 5,660,823 8.14 40 8.9

Fair Russia 5,383,639 7.74 38 8.4

Agrarian Party 1,600,234 2.30 - -

Yabloko 1,108,985 1.59 - -

Civic Strength 733,604 1.05 - -

Union of Right Forces 669,444 0.96 - -

Patriots of Russia 615,417 0.89 - -

Party of Social Fairness 154,083 0.22 - -

Democratic Party of Russia 89,780 0.13 - -

Source: Russian Electoral Commission

The consolidation of electoral predominance, although not necessarily political

dominance, was complete with the election of Dmitry Medvedev as President, in

March this year. His succession to Vladimir Putin provides a powerful element of

12The Sochi Olympiad:

An Introduction to 2014

political stability and continuity. The election of Medvedev was so widely anticipated,

that at times it appeared less of an election than a coronation, with serious and .

valid concerns over the level of openness and fairness in the electoral process. .

This despite the real levels of popularity of Putin. The degree to which media access

was essentially restricted to pro-Medvedev commentary and the legalistic efforts to

undermine oppositional candidates participation, indicates some fragility of

confidence on the part of the Kremlin. Indeed, the fact that Putin is retaining

influence as Prime Minister and Chairman of United Russia, whilst contributing in

one sense to policy continuity, also probably reflects a significant degree of factional

conflict within the Kremlin power structure.

This stability and predictability of the political process under the administration of

President Putin has played a significant part in fostering the expansion of capital

inflows. Putin’s high levels of popularity throughout his Presidency, was due in no

small part to the success of the economy and the widening distribution of the

benefits derived from it. The maintenance of consistency in macroeconomic

management under the new administration of President Medvedev will be a critical

factor in sustaining economic growth over the medium-term. Notwithstanding the

apparent evidence of increasingly bitter factional conflict within the Kremlin hierarchy,

concerns over the likely strength and competence of the forthcoming Medvedev

administration have in part dissipated by the fact that Putin will retain a role as

Premier. However, for a country undergoing only its second constitutional change of

the head of state, and continued narrowing of the scope of civil society, the process

will not be without sudden squalls. Moreover, the economy remains one in transition

and will require a sensitive economic management strategy.

Presidential Election Result

Candidate Nominating Organisation Votes %

Dmitry Medvedev United Russia, Agrarian Party, 52,530,712 70.28

Fair Russia, Russian Ecological Party

– “The Greens” and Civilian Power

Gennady Zyuganov Communist Party of the 13,243,550 17.72

Russian Federation

Vladimir Zhirinovsky Liberal Democratic Party of Russia 6,988,510 9.35

Andrei Bogdanov Democratic Party of Russia 968,344 1.30

Invalid ballots 1,015,533 1.35

Total 73,731,116 100.00

Source: Russian Electoral Commission

13e. Economy

2006 2007 2008f 2009f 2010f

Real GDP (YOY%) 7.4 8.1 8.6 8.0 7.6

CPI (annual avg %) 9.7 9.0 12.9 11.3 9.9

Federal Govt Balance (% GDP) 7.4 5.4 5.3 3.5 2.5

Current Account Balance (% GDP) 9.7 6.1 8.0 5.0 3.0

FDI (US$ bln) 32.4 52.5 60.0 70.0 80.0

Forex Reserves (US$ bln eop) 304 476 610 720 700

Exchange Rate (RuR/US$ annual avg) 27.2 25.6 24.0 25.0 26.0

Source: Rosstat, Central Bank of Russia, Ministry of Finance

Economic fundamentals are strong as a result of high world commodity prices in

recent years, which have provided a significant boost to external liquidity. However,

heavy reliance on oil and gas exports may dent future economic performance as the

global economy is slowing and commodity prices may fall.

As in preceding years, the dynamism of the economy’s performance has been

underpinned by high global oil prices, with real GDP recording growth in excess of 8%

last year. Despite sensitivity of the overall economy to oil prices and further erosion

of international competitiveness forecast, growth in 2008 and 2009 can be

anticipated to remain robust and likely to remain at close to 8% in real terms

annually. Indeed over the medium-term, essentially the period encompassing

Medvedev’s first term, the strong foreign exchange position (equivalent to US$ 534

billion as of end May 2008) and the restructured stabilisation funds (as of July

2008, the Oil Reserve Fund stood equivalent to US$ 140 bln and the National

Welfare Fund almost US$ 33 bln), the economy and the fiscal position will be largely

insulated from any global oil price volatility. Whilst oil prices are currently trading

above US$ 135 pb, even at the comparatively low levels of US$35-40 per barrel,

the Reserve and Welfare Funds are structured to continue to accumulate resources.

This despite greatly increased fiscal expenditure and rising import demand, which is

unlikely to be reined in during the first few years of a new administration. With

massive expectations, real need for infrastructure investment, capital re-equipment

and plant modernisation, demand for foreign direct investment will not diminish.

However much the administration may wish to dictate the terms and conditionality

of inward investment, and while the parameters may become more discernible and

the available sectors more intelligible, fdi will be a key component supporting future

economic development. This is most especially the case in the oil and gas sector,

where there are severe concerns regarding Russia capacity to sustain current output

levels and consequently the apparent acute need for capital investment to boost

productive potential.

14The Sochi Olympiad:

An Introduction to 2014

Fortuitously Russia’s capacity to generate inward capital investment flows continues

unabated. This despite deteriorating conditions in global capital markets and in the

face of the tightening legislative and regulatory environment within Russian itself.

Notably with regard to sensitive, but in many cases largely ill-defined, strategic

national sectors, particularly extractive industries. Nevertheless, according to

preliminary UNCTAD estimates Russia fdi flows increased over 70% to the equivalent

of US$48.9 billion, up from US$ 28.9 billion in 2006. Not only was the Federation

the recipient of just over half of fdi flows into transitional economies, but was the

second largest destination, after China (including Hong Kong), of FDI flows toward

emerging markets, and even exceeded Italy in terms of receipts.

With its accumulated reserves and comparatively prudent husbanding of oil-derived

revenues, the immediate impact of the global tightening of market liquidity on

Russian economic performance is likely to be constrained. Not that Russia is likely

to emerge unscathed. In the third quarter Russian capital outflows increased to the

equivalent of US$ 9 billion, contributing to the sharp drop in Russian asset prices

experienced during that period, with the reserve position easing the equivalent of

US$ 7 billion. In the final quarter of last year, there was however a limited recovery

of capital inflows, which contributed to renewed reserves accumulation.

Official estimates for the period January-September 2007, indicate that net inflows

of foreign private capital amounted to US$131 billion, more than 50% of that

recorded for the whole of 2006. This was primarily comprised of external financings

raised by both corporates and banks. Notably recourse to external borrowing by

Russian corporates surged to the equivalent of US$ 61 billion, two-and-a-half times

as much as during 2006 as a whole. Moreover, the bulk of this financing is attributed

to funding the state-owned oil company, Rosneft’s acquisition of the remaining

Yukos’ assets and the securing by Gazprom of foreign shareholders majority ownership

of a gas field. Corporate bond issuance increased to US$ 16 billion in net terms.

Given the apparent scale of the global credit crunch and its potential longevity, the

banking sector’s recourse to international capital markets during 2008 could prove

problematic, although not insoluble. During 2007 foreign borrowing exceeded that

incurred in 2006, with in the region of US$ 60 billion committed over the year. In a

sector already dominated by state-owned institutions, further extension of state

participation in the banking sector could prove an immediate consequence of the

reshaping of global capital markets during 2008. With borrowing and bond issuance

sharply scaled back in the final quarter of 2007, 2008 could prove to be an interesting

period for corporate and bank refinancing.

15A particular feature of Russian capital flows, is the proportion of returning Russian

funds, reflected by the fact that offshore financial centres provide a significant core

of Russian fdi. Nevertheless adjusting for returning Russian funds, foreign direct

equity investment was equivalent to US$7 billion, which was primarily the result

of IPOs by two state owned financial entities, VTB and Sberbank.

Sochi

Source: Sochi 2014

Adjusting for returning Russian funds, whilst net outflows of resident capital jumped

to US$75 billion during January-September, equal to almost 10% of GDP. Although

equity investment abroad accounted for a third of capital outflows in the first nine

months of 2007, and a further third was attributed to foreign lending by Russian

domiciled institutions, capital flight increased significantly during 2007. Monthly

capital flight flows are now over US$ 4 billion double that sustained in 2006.

According to Bank of International Settlements (BIS) data, Russian residents

significantly reduced bank deposits in Europe. Cumulative liabilities to Russia fell

by US$ 55 billion, the largest yet recorded fall since data became available in 1993.

British, German, French and Belgian resident banks all reported notable shifts in

deposit patterns. Whilst US dollar denominated liabilities fell by over US$ 39 billion,

16The Sochi Olympiad:

An Introduction to 2014

recording their lowest proportion of Russian liabilities, Euro-denominated assets also

eased by the equivalent of US$ 21 billion. Similarly, IMF data indicates that Russian

banks reduced their foreign exchange reserves abroad by as much as US$ 17 billion

in the fourth quarter of 2007 and by US$ 39 billion in the first quarter of 2008.

Whilst this was in part due to Central Bank of Russia activities, and there was a

compensating increase in Russian securities holdings of US$ 92 billion by the end of

2007, the shift in the asset/liability pattern may be indicative of further liquidity

pressures in the domestic financial sector.

Given the difficult global market conditions, 2008 could mark a new stage in the

structure of fdi for Russia. Whilst Russia itself can mobilise considerable capital

investment resources, the scale of demand, both actual and potential, will ensure

that fdi will continue to play a key role of the expansion of the economy. Indeed with

the anticipated narrowing of surpluses in 2009 and 2010, fdi is set to play a more

significant role. How this will be achieved will obviously depend on the stance the

Russian authorities take. Whilst there have obviously been problems in the so-called

strategic sectors, across the wider economy a more favourable attitude prevails.

This can perhaps best exemplified by the development proposals associated with the

Sochi 2014 Winter Olympics. The Federal government itself has implemented a

US$ 12 billion Federal investment programme to develop the Black Sea resort into

a global winter sports capital. Associated investment into the City’s infrastructure

and resources are likely to be double if not triple the cost of the Federal investment

programme. Both the regional government, Krasnodar Krai, and the Sochi City

authorities have adopted a proactive approach to secure the financing necessary to

the realisation of these projects, with a range of options available, including public

private partnerships, foreign investment is being actively courted. The degree to

which fdi can be attracted to Sochi will be indicative of the likely scale of fdi flows

into Russia generally, and will probably provide a model for future fdi projects.

173. Regional Description: Krasnodar Krai

Population: 5.1 Million (2002)

Area: 76,000 sq km

Governor: Alexander Nikolayevich Tkachev

According to 2002 census results, the Krai’s total population was 5.1 million people,

with an average population density of 67.4 people per square km. The economically

active population amounts to 2 million. Although the 2002 official unemployment rate was

stated as 0.7%, the real rate was actually nearer to 11.0% in terms of the

demographic structure, the equivalent of 58% are of working age, 19% are below the

statutory working age, and 23% are beyond the statutory working age. As of 2002, the

major urban centres of the Krai were Krasnodar (644,800 inhabitants), Sochi (328,800),

Novorossiysk (231,900), Armavir (193,900), Yeisk (84,600) and Kropotkin (81,300).

Krasnodar region is formed of 48 municipal units including 26 townships, 21 settlements

of the urban type and 1717 rural settlements. The administrative centre of the Krai is

Krasnodar City. It celebrated the 210th anniversary of its foundation in 2003 and is the

administrative, financial, industrial, scientific-educational and cultural centre of the Krai.

As a subject of the Russian Federation, and a component of the Southern Federal Okrug,

the parameters of the executive structure of the Krai are stipulated by the national

constitution. The head of executive power is the Governor (or head of administration)

who is elected by universal suffrage for 5 year terms. Alexander Nikolayevich Tkachev

was elected Governor of the Krasnodar Krai on March 14, 2004. Similarly, the legislative

assembly of Krasnodar is elected by universal suffrage for the term of 5 years which

adopts the laws of Krasnodar Krai obligatory for execution in the territory the region.

The Gross Regional Product (GRP) share of Krasnodar in the all-Russian volume of GRP

amounts to 2.2%. During 2004 the volume of GRP of the region was RuR 331.8 bln,

which exceeds the volume of GRP in 2003 by 7.8% in comparative prices. This positive

GRP performance was a result of growth across the main economic sectors. Agriculture

occupies the largest part of GRP structure (17.2%), followed by the industrial complex

of the region is represented by 6,300 organisations including over 500 large- and

medium-sized organisations. The leading industrial branches are food processing,

power generation, fuel production, engineering industry metal-working, and the

construction material industry, in total equivalent to over 60% of industrial production.

The Krai is rich in natural resources, containing more than 60 commercially exploitable

mineral deposits: oil & natural gas fields, marl, iodine-brome mineral water, marble,

limestone, sandstone, iron ores and apatite ores. In terms of hydro-carbons, the Krai is

one the oldest producing regions, with 69 oil fields under exploitation, the principal oil

fields situated in the western and central parts of the foothills (in the districts of Abinsky,

Seversky, Apsheronsky, Slavansky). Total annual crude oil production is equivalent to 1.7-

1.9 million tonnes and over 2 billion cubic metres of natural gas.

18The Sochi Olympiad:

An Introduction to 2014

Furthermore, the Krai possesses one of the largest European freshwater resources,

located primarily in the Azov-Kuban basin. There are 42 deposits of mineral waters in

the region, with 17 of them currently exploited. Forests are among the most

important natural resources of Krasnodar region – the total area of forests is over

1.5 million hectares, mainly fine wood.

In terms of economic potential the Krasnodar is one of the strongest in the

Federation, with the Krai noted for steady real growth in gross regional product,

based on population growth, output and services provision in key sectors of

economy. Additionally, fertile agricultural land, which provides for a broad production

range of temperate zone crops and sub-tropical crops, with the Krai ranked in the top

echelon of agricultural producers. Growth prospects are supported by the

comparatively well-developed transport infrastructure – three international airports, 8

seaports including one of the largest in Russia and one of the major railway nodes in

the southern Russia. Road infrastructure provision also compares favourably with

other parts of Russia. Given these attributes, Krasnodar acts as a major

international transport corridor between the Russian hinterland, Europe, the

Mediterranean, Middle East and Central Asia.

Economic potential is facilitated by the favourable investment climate – with

Krasnodar is among the top ten regions in Russia by volumes of investment.

Similalrly, in June, Forbes magazine published the ranking of Russia’s cities in terms

of their business environment. Krasnodar topped the list. Sochi took 11th place and

Novorossiisk – 26th. This has fostered the expansion of the regional financial sector,

with Krasnodar ranked amongst the top ten regions of Russia in terms of scope of

banks and branch networks operating in the region. Whilst foreign economic interest

and activity in Krasnodar is expanding steadily the geographic range of its business

links and external trade. In 2007, Krasnodar was awarded long-term ratings by the

main international rating agencies: Fitch Ratings, Standard & Poor’s and Moody’s.

Fitch Ratings gave the Krai a long-term rating of “BB”, with the outlook “Stable”.

Similarly, Moody’s awarded Bal, with a stable outlook, whilst Standard & Poor’s has

improved its outlook from “Stable” to “Positive” on a BB- rating. This compares

favourably to the overall Russian rating, with Standard & Poor’s, for instance,

awarding the sovereign BBB+. This was attributed to the strength of high economic

growth. Furthermore, the ratings reflect positive trends in budgetary performance

supported by positive economic condition, as well as a well-balanced budget policy

and a low level of debt load. However, the ratings take into account the constrained

predictability and flexibility of Krasnodar’s fiscal position, stemming from central

government controls, considerable infrastructure requirements and below-average

income levels. Nevertheless, both the Krai’s economy and revenues are expected to

expand further and the debt burden manageable.

19The principal manufacturing sectors, accounting for in excess of 80% of

manufactured output, are food and beverages, energy, fuel, machine engineering and

metal processing, and construction materials. Production is spread across 700 large

and medium-sized companies and over 4,000 small enterprises. However, food and

food processing is the predominant sector, accounting for 43% of total industrial output.

In total, Krasnodar possess 16 sugar refineries, 10 vegetable and fruit canning

plants, 7 fish canning plants, 42 dairy and 23 meat processing plants, 7 butter

and fat plants, 2 tea and 2 tobacco processing plants, 48 vineyards, 11 wine plants,

4 distillers, and 25 bakeries. Major companies within this sector are:

R OAO Krasnodar Butter and Fat Plant,

R OAO Armavir Butter and Fat Plant,

R OAO Abrau-Durso,

R OAO Krasnodar Meat Plant,

R ZAO Krasnodar Fish Plant,

R Municipal Unitary Company Krasnodarptitsa,

R ZAO Anit Ltd.,

R Subsidiary No. 1 of ZAO Moscow Brewery

R Soft Drink Plant Ochakovo.

The energy sector accounts for 13.5% of total industrial output. OAO Kubanenergo is

the main energy generator and supplier, consisting of the Krasnodar Power Station,

three hydroelectric power stations, high-voltage transmission lines and transformer

substations. Refining and production of fuel products account for 9.6% of total

output. Of the three oil refineries present in the Krai, the largest of which are ZAO

Krasnodareconeft Refinery and OAO Krasnodarneftegeofizika. The machine

engineering and metal processing sector generates an equivalent output, 8.7%, with

over 100 companies produce a wide range of machinery, including metal-cutting and

lumber machines, automation tools, agricultural vehicles, electrical engines,

compressors, pumps, refrigerators, and oil exploration and extraction equipment.

Major companies within the sector are:

R OAO AvtoKuban,

R OAO Krasnodar ZIP,

R OAO Molot,

R OAO Krasny Dvigatel,

R OOO Electro,

R ZAO Agrostroimash.

20The Sochi Olympiad:

An Introduction to 2014

Construction materials accounts for 7.3% of total industrial output, with four

construction materials manufacturers – OAO Kuban Gypsum-Knauf, OAO Novokuban

Ceramic Wall Materials Plant, ZAO Reinforced Concrete Goods Plant, and OAO Ceramic

Goods Plant, which rank amongst Russia’s top construction materials companies.

The timber and furniture sector for 5.5% of total industrial output and is represented

by 35 large and medium companies producing lumber, chipboard, parquet flooring,

and home and office furniture. Industrial timber export amounts to 100,000 cubic

meters per year. Major companies include OAO Krasnodar Furniture Firm, OAO Kuban

Furniture, and OOO SBS-Furniture Company. Agriculture accounts for some 17.3% of

gross regional product and over 5% of Russia’s gross agricultural product, including

10% of grain output, 19% of sugar beet output, and 15% of sunflower seeds output.

The Krai has 4.4 million hectares of arable land, including 3.9 million hectares of

ploughed fields, 77,000 hectares of orchards, and 35,000 hectares of vineyards.

Given the Mediterranean-type climate, warm seas, mineral water springs, and

therapeutic mud, Krasnodar is one of the most ecologically advantaged regions

ensuring its popularity as a tourist and recreational destination across the country.

With over 1,300 recreation and tourism enterprises, which can accommodate some

220,000 people at any one time, generating an estimated US$333.5 million per year

in Krasnodar. Krasnodar is home to all of Russia’s major seaside resorts, including

Sochi, Anapa, Gelendzhik, Tuapse, and Yeisk.

The transport sector accounts for 17% of the GRP. The Territory has 10,400

kilometres of roads, including the following: Krasnodar – Novorossiysk, Krymsk-Port

– Caucasus, and federal roads Krasnodar – Baku and Don (Moscow – Voronezh –

Rostov-on-Don – Krasnodar – Novorossiysk). The Krasnodar Territory has 2,200

kilometres of railroads. The main route going through the Territory is the Krasnodar

section of the North-Caucasus railroad. The main freight flow goes in the direction of

the seaports. Freight is dominated by oil, oil products, timber, lumber, grain, sugar,

construction materials, and equipment. Additionally, Krasnodar has international

airports at Krasnodar, Sochi, Anapa, and Gelendzhik

There are eight seaports in the territory: Novorossiysk, Tuapse, Sochi, Anapa,

Gelendzhik, Yeisk, Temryuk, Caucasus, and the Krasnodar river port. These account

for up to 40% of the Russian Federation’s ports freight turnover. Major shipping

companies are OAO Novorossiysk Sea Ship Line, OAO Novoship, and OOO Barwel

Novorossiysk. As a principal oil and gas pipelines export route, sections of major oil

pipelines including Makhachkala – Grozny – Tuapse, oil pipelines of OAO Transneft,

OAO Chernomortransneft, ZAO Caspian Pipeline Consortium, and the Lazarevskoe –

Tuapse – Nebug gas pipeline, all pass through Krasnodar. Whilst plans are being

developed to establish a gas pipeline from Tyumen to Turkey through Krasnodar.

21The Territory’s enterprises supply over one third of Russia’s output of granulated sugar (2

million tons), some 40% of concentrated fruit juice output, 100% of canned meat for

infants, and 6% of cheeses and canned dairy products. Other products include vegetable

oil (320,000 tons) and canned fruit and vegetables (376 million conventional cans).

Furthermore the Krai produces 10 million decilitres of wine per year (including 2.5 million

decilitres of sparkling wine and 4.8 million decilitres of grape wine). A favourite of the

Russian market, the classic sparkling wine Abrau-Durso, is produced at the Abrau-Durso

Plant. All in all, the Krasnodar Region produces over 120 brands of alcoholic beverages.

2002 tobacco output amounted to 37.1 billion items. The 2002 gross grain yield totalled

8,481,200 tons, sunflower seed – 732,400 tons, sugar-beet – 4.2 million tons, dairy

products – 436,000 tons, and meat (including by-products) – 88,800 tons. In 2002, the

Territory’s enterprises produced 6,300 tons of paints and varnish, 105,300 tons of

mineral fertilizers, 7,000 electric mixers, 31,000 cubic meters of lumber, 33,300 tons of

cardboard, 2.4 million tons of cement, 580 million conventional bricks of wall construction

materials, 3 million square meters of fabric, and 9,757,000 pairs of footwear.

The Territory’s foreign trade turnover amounted to $2 billion in 2002 (extra-CIS trade

accounted for 91% and CIS trade for 9%). Major trade partners include Turkey, Bulgaria,

Italy, Greece, the Netherlands, Germany, Spain, and the USA. Additionally, the Territory

maintains close links with Ukraine, Kazakhstan, and Uzbekistan. Exports to extra-CIS

countries amounted to $944.9 million in 2000, with exports to CIS countries totalling

$50.8 million. The respective figures for 2001 were $912.6 million and $79 million, and

$986.9 million and $96.3 million for 2002. The main goods exported by the Territory are

crude oil, sunflower seeds, sugar, tobacco products, raw timber, and grain.

2000 imports from extra-CIS countries amounted to $501.4 million, while imports from

CIS countries totalled $70.3 million. The respective figures for 2001 were $558 million

and $69.2 million, and $872.7 million and $82.1 million for 2001. Imports from CIS

accounted for 12% of total imports, and imports from extra-CIS, for 88%. The main

goods imported by the Territory are raw sugar, fertilizers and pesticides, agricultural

equipment, citrus plants, oil products, and medicine. The main exporters to the region

are Ukraine, Germany, Italy, France, Turkey, China, Cuba, Greece, and the USA.

Due to the structure and attributes of trade in Krasnodar, export and import

operations are performed mainly by industrial companies. The Krai is home to 781

companies with foreign investment from 60 countries. Major companies are OAO

Krasnodartabakprom, ZAO Sochi Pepsi-Cola Soft Drinks Plant, OAO Kuban Gypsum-

Knauf, and JV Tetra-Pak Kuban. Investors from the USA account for 47% of total

investment, the Netherlands – 29%, Cyprus – 14%, and the UK – 7%.

For further information on the available investment projects and fdi potential of

Krasnodar contact mail@forrestresearch.co.uk

22The Sochi Olympiad:

An Introduction to 2014

4. City of Sochi

The City of Sochi has developed along a relatively narrow littoral ribbon between

the Black Sea and the western fringe of the Caucasus Mountains, and it is claimed,

at 145 kms in length, to be the longest city in Europe. Administratively Sochi,

is divided into four districts: Adler, Khosta, Central and Lazarevsky. According to the

2002 census, it had a population 328,809, down from 336,514 recorded in the

1989 Census.

As an already long Sliding Centre

established resort, it is

often referred to as the

Russian Riviera, with an

existing provision of

infrastructure, Sochi

provided the successful

basis for the 2014

Winter Olympics bid.

Traditionally, through

the later Nineteenth

and much of the

Twentieth Century,

Source: Sochi 2014

Sochi was a pre-

eminent holiday destination. It has remained Russia’s most popular tourist

destination through the transition period, and currently boasts with over four million

visitors a year. In addition to its expanse of beaches and coastline, within one hour’s

drive from the Sochi coast is the mountain resort of Krasnaya Polyana, offering both

quality and quantity of snow to develop the highest provision of winter sports.

Notably, Mount Elbrus, at 5,642 m in the Russian Caucasus is considered the

highest mountain in Europe, in comparison Mont Blanc stands at 4,810 m. Indeed,

the average height of the Caucasus mountains adjacent to Sochi is 2,000m.

Sochi borders the Caucasus State Biosphere Reserve, a UNESCO World Heritage

site and one of a number of specially protected natural zones in the vicinity.

Accordingly, the accommodation of the potential and perceived environmental impact

have been central to the planning and design process for both the 2014 Olympiad

development and the longer-term project of establishing Sochi as a global resort

destination.

The Sochi Administration has been working in conjunction with the Federal Ministry

of Natural Resources to develop a list of specific state-of-the-art ecological projects

to ensure minimal environmental impact. The Federal Olympic programme also

includes funding for SEER review, monitoring of the environmental impacts of all

projects as well as the creation of infrastructure for environmental preservation.

23This includes a commitment to environmental awareness and education, with Sochi

2014 allocating substantial funding as part of the Winter Games budget to regional

educational administrations to promote environmental awareness. This strengthened

focus on existing educational institutions, combined with the establishment of

Sochi’s Environmental Discovery Centre is designed to ensure that the principles of

environmental stewardship and sustainability remain a key part of the longer-term

development and promotion of the Sochi resort.

Mayoral elections were initially planned for October, but these were brought forward

following Victor Kolodyazhny’s resignation on his appointment as head of Olympstroi,

the Olympic implementation organisation, in April. Kolodyazhny was elected as Sochi

Mayor in 2004, with the term of office expiring in October. Vladimir Afanasenkov, who

became acting Mayor, won the Sochi mayoral elections that were held on June 29,

polling 85.1% of the total number of votes. His nearest rival secured 12.17%, the

Head of the Communist Party City Committee Yuri Dzagania. More than 132,000

local residents or 46.6% of the total number of registered electors came to the

polling stations on the day of the voting. Given the technical nature of inputs to the

Olympiad, from the Mayor’s office, it is unlikely that the election will result in either

major change in the thrust of policy or the organisation of the Games.

Although, the Duma has passed the “Olympic law” which will speed up the

expropriation of the property, as in previous Olympiad as well as London, there are

serious concerns regarding the implementation of the law. Initial unofficial estimates

suggest over 4,000 people are facing compulsory purchase orders ahead of the

Games. Within Sochi, a 2014 Olympic office, headed up by Alexander Remezkov, has

been established. The office will be responsible for issues related to securing land

plots from Sochi residents of Sochi, the purchase of which is necessary to facilitate

the Olympiad. A key role of this office will be to alleviate as much of possible the

negative consequences of the purchase. Tensions have nevertheless risen recently,

with Governor Tkachyov, calling for law enforcement agencies to counter protests.

A recent demonstration by local residents, took place in full view of International

Olympic Committee coordinating commission. The authorities believe that plans to

build a new village for local residents displaced from their homes by Olympic

construction will be sufficient. Olympstroi have said that within months the land for

Olympic construction will be expropriated.

24You can also read