THE TRANSCRIPT Quarterly Earnings Calls: Apr-Jun 2021 - DSP Mutual Fund

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

THE TRANSCRIPT Quarterly Earnings Calls: Apr-Jun 2021

This is a compilation of management comments from AGMs/Concalls for the quarter ending June-2021. Forward looking statements are either prophetic or widely off the mark (sadly, we don’t know which). While reading transcripts we are primarily searching for better questions that we should be contemplating about businesses. The compilation should not be used for investment decisions (read our disclaimer below and at the end). Disclaimer Regarding Forward-Looking Statements This content contains forecasts, projections, goals, plans, and other forward-looking statements regarding Company's financial results and other data provided from time to time through AGM/ conference calls transcript, webcasts, presentations, investor conferences, newsletters and similar events and communications. Such forward-looking statements are based on the Company's assumptions, estimates, outlook, and other judgments made in light of information available at the time of preparation of such statements and involve both known and unknown risks and uncertainties. Accordingly, plans, goals, and other statements may not be realized as described, and actual financial results, success/failure or progress of development, and other projections may differ materially from those presented herein. Even when subsequent changes in conditions or other circumstances make it preferable to update or revise forecasts, plans, or other forward-looking statements, the Company disclaims any obligation to update or revise this content.

Segments 1. Buy Now, Pay Later (BNPL) & Fintechs 2. Engineering and Research & Design Services (ER&D) 3. Retail vs. Large Corporate Lending 4. Pharma: US Generic Pricing 5. Direct to Consumer Brands 6. CNG in Energy Mix 7. Li-ion Batteries

QUOTE OF THE QUARTER

I've been in banking circles long enough to know that the key

issue that can really put a bank under risk is really not the

asset side. The liability side - it's probably more important

than anything.

V. Vaidyanathan, IDFC First BankBuy Now, Pay Later (BNPL) & Fintechs

US based payments fintech company Square announced acquisition of Afterpay, an Australian Buy Now,

Pay Later firm for $29 BN. Jack Dorsey (CEO, Cofounder of both Twitter and Square) said, “we built our

business to make the financial system more fair, accessible, and inclusive, and Afterpay has built a trusted

brand aligned with those principles”. Afterpay allows customers to buy a product immediately and pay for

it in 4 equal installments. The convenience to customer is temporary credit line with lower risk of high

credit card fees while the merchant gets a higher cart value as BNPL gives the ability to customers to

spread out the payments. Afterpay founded just 6 years ago has show rapid growth in active customers and

merchants. It had revenues of $693 MN in FY21 and is not yet profitable.

Banks have started to recognize that this is not a stand-alone pure financing offering but an opportunity to

build an integrated shopping platform and engage customers through the entire journey. Affirm, another

BNPL firm is raising $1 BN in loans at exercise equipment company Peloton annually. These are customers

with high credit scores (average 740) and most of them already have a credit card (Source: Buy Now, Pay

Later: Five Busines Models to Compete, Mckinsey, July-2021). PayTm has 114 MN annual transacting users

with 21 MN payment merchants. With this kind engagement engine in place Fintech players are trying to

move towards more profitable lending segment while traditional lenders are moving towards higher

engagement integrated platforms.

Pay-later opportunity is currently estimated to be $15 BN in India which is expected to cross $100 BN by

FY25. The share of pay later in digital merchant payments in India is currently 4.1% (Source: Bernstein).

ICICI Bank highlighted some of the differences between capabilities of Fintechs and a Banks in their

earnings call.

Source: Bernstein

Source: BernsteinWhen we look at various players in the market, the only thing that we found lacking was that

people are doing more, nobody is doing structured reward management work, everybody is

essentially doing when people want to acquire customer they throw in money, and they go

away. Three years ago, lots of millionaires in my office were all using Paytm, then they started

using Google Pay, then they started using PhonePe. People want to acquire customers, throw

money, burn half a billion dollars and go away. We do not have that customer acquisition

problem, we are generating, we have 50 million customers, they are fully KYC that is the second

point I must make. Three, we continue to acquire 1.8 to 2 million customers in 3,000 cities in

India, engagement is really where our entire focus is, that is really why the digital acceleration

stroke transformation is there. In that, payments is critical.

Why are we bringing it now because we had to first get the money making machine going, then

we will get the engagement machine going.

Bajaj Finance

I think, if you traditionally look at the kind of -- at least our own company central

At least at our own company the central experience is, I mean, typically the limits will be minimum

INR30,00 to INR40,000 kind of limit from a unit economics perspective, otherwise it will not work

out for us. But BNPL is in a totally different bracket where it starts with a very small amount of

even INR5,000 and they hover around INR10,000, INR12,000. But with regard to the potential, we

don't rule out the potential. The market will definitely increase and its mostly very popular with

millennials or otherwise the NPC kind of segment.

But way forward will be perhaps some convergence will be there, where the BNPL customers can

potentially become surplus of credit card once they build a good credit history or otherwise, we'll

also the making journey towards it. So, there will be a convergence point.

SBI Cards

I think, if you traditionally look at the kind of -- at least our own company central

We are also building our merchant and SME stack, offering payments, reconciliation and digital

collection. We have acquired more than one lakh merchants on UPI QR, out of which we have

industry best activation of 60%. It gives us a great opportunity to build transaction banking

relationship with these merchants. To further deepen our engagement, we have now started

offering unsecured loans to merchants based on their transaction history.

We are ramping our technology team and plan to have more than 100 full-stack developers,

product managers, and designers to further strengthen our digital and analytics outlook. Other

than these initiatives, we are also building our stack for account aggregator, real-time offers and

BNPL, which we expect to launch this year.

AU Small Finance Bank• There is nothing technically which a Fintech does that a bank cannot do.

• For banks like us, I think first there is a gap on the speed of imagining the solution. Fintechs,

because they are very focused on a problem that they are solving for the customer, generally

they are the first on the block to solve that problem.

• What banks have to do is, we need to have our tentacles far and wide which we have, to see

which problems are getting solved and are those problems relevant for our customer segments

as well. If they are relevant to our customer segment, we have two choices, either we build the

solution on our own or we partner.

• Fintechs, we have seen, they solve the problem correctly, but most of them find it difficult to

scale up, some of course scale up very well. So that is one thing. Second is that, how fast can a

bank do it, because Fintechs are very focused on a particular segment since they don’t have the

complexity of a bank. At times, they can be faster in solutions, and they could be more flexible

and agile, but in the fast and agile, we have seen in our experience, they find it difficult to make

adjustments. They are not able to move into the adjacencies that easily which is that they focus

on one customer segment, one problem and that is it and they are not able to move with us.

And on the customer side if we see, a customer requires a full solution, so if a problem requires

10 solutions, if somebody is giving only four solutions, generally the adoption is not that good.

• Of course, on the banking side, we are a regulated entity, many other Fintechs are not regulated

entities. To that extent, there is some short-term agility or flexibility that they will have, but as

they grow up, there will be clamor for regulations to come in and regulations, they are

sometimes good because they increase trust in the system, but sometimes they also open up

some small arbitrages which makes them more flexible for some time at least, so that is the

positive. So basically the game is evenly spread and banks have natural advantages and it is for

incumbents like us to actually win this market and serve the customers well across their needs,

across their spectrum in a broad way and in a deep way.

ICICI BankEngineering and Research & Design Services (ER&D) ER&D services is essentially outsourcing part of the Research and Design process. This segment has been growing faster than the IT services for Indian companies for some years now. The Global market for IT services is estimated to be about $3 TN while that for ER&D its $1.5 TN. Source: Internal According to Everest Group (an IT focused research firm) the top 5 players in the segment are 1. Capgemini 2. HCL Technologies 3. Alten 4. Accenture 5. Tata Consultancy Services. Source: NASSCOM

We believe that the digital engineering and manufacturing space is the next frontier for our

clients. There’s been a lot and there’s still a lot to do with respect to the front office and the

back office, for lack of a better term. But our clients are building a digital core, they’re

transforming operations and they’re trying to find new waves of growth. But the areas that

have been not as digitized over the last several years as companies have pivoted have been in

core operations, manufacturing and supply chain.

We believe that product development, design engineering, manufacturing, and the supply

chain make up the next big digital transformation frontier. The impact of COVID-19 is

accelerating the need to transform these core operations. And, for nearly a decade we have

been investing to build the unique capabilities and ecosystem partnerships to combine the

power of data and digital with traditional engineering services.

Accenture

I think, if you traditionally look at the kind of -- at least our own company central

The ER&D space today is about $1.4 trillion as of 2020 spend. Of this $1.4 trillion it is supposed to

grow to anything between $1.75 trillion to $1.95 trillion by 2023. Now, out of this 1.4, that is as of

CY20, $80 billion is outsourced to engineering service providers and India gets 16 billion of that

$80 billion.

We do expect outsourcing to engineering service providers like ourselves and others in India Inc.

as well as western Europe, eastern Europe to grow, we also expect global competency centers to

pick up. Having said that, you may see some more global competency centers spend going to

eastern Europe and LATAM and China slowing down from a global competency center standpoint

LTTS

We see emerging opportunities on various trends in the ER&D space resulting from increased

spending on Digital in areas like Industrial IoT, Cloud adoption, IT/OT integration – making the

manufacturing value chain smarter and faster.

Infosys

I think, if you traditionally look at the kind of -- at least our own company central

What we see as a big positive is the revenue momentum in Engineering and R&D Services both in

Europe and Americas, led by digital engineering demand in hi-tech as well as life sciences. We are

already seeing green shoots of growth from the asset-heavy industries as well. With this, the

outlook for ER&D Services looks strong in the upcoming quarters.

HCl TechRetail vs. Large Corporate Lending

Most large banks have focused on increasing the share of retail loans during the last 5 years. The

granularity of loans, higher margins, higher profitability and cross-sell franchise were some of the drivers

for the move. This was combined with lower demand from the corporate sector due to lower capex and

investment.

High rated large corporate is typically a highly competitive segment. Large banks with low cost of funds

have an advantage here. Banks with low cost of funds can make similar spreads for lower risk and that is

why, while a lot of focus is on the asset side – its typically the liability side (the deposit franchise) that

drives the business.

We got two sets of comments on these segments from two veteran bankers.

Source: RBII've personally done this for like close to about 25, 28 years and I just find that with all my

experience (…) that you have an odd cycle here or there, but in the longer run (…) these are (at)

end of the day individuals (who) are borrowing. Individuals bother about the credit bureau,

individuals don't have a cover or a shell of a company, which can have some limited liability and

they cannot - they don't have those escape routes. They have the personal, in terms of the size

of the relationship, it's always, I mean, the strength of the relationship with the individual

customer is much stronger. So, for many reasons, we wanted the retail.

Corporate banking belongs to someone who really has very low cost of funds straightforward.

And the big banks like ICICI, HDFC, Axis, they are naturals into it, because they pay 3% up to

INR50 lakhs and 3.5% above that. So they are realistic and (with a ) very low CASA rate, I mean,

cost of funds. And then large corporate really ask for really fine prices.

IDFC First Bank

The other important issue is that when you are lending to corporates, you just ask yourself the

tough question, and I am giving you some mathematics. I mean, I am not giving you any rocket

science. The Reserve Bank of India today takes overnight money from banks for its surplus at a

daily compounded rate of 3.35%. You take a one year treasury bill, it’s give or take around

3.75% to 3.8% yield. Now, instead of putting money here if you put money in a corporate loan,

you have straight away an additional cost of priority sector lending. After that, what is your

return or ROE or risk-adjusted return on capital is a tough question you have got to ask. And

therefore, if priority sector lending is a cost, is it better to be doing debentures for those

companies versus giving a loan?

And we ask these tough questions and take the tough calls, because finally the priority sector

lending cost is a cost which hits a bank over three to five years. Therefore, I can easily be short-

term in my approach, grow my lending book by taking huge bets end of the quarter and show

higher growth. But I will pay the price over three to five years by putting money at 2.5% for

three to five years. And we don't want to get into that.

Kotak BankPharma: US Generic Pricing

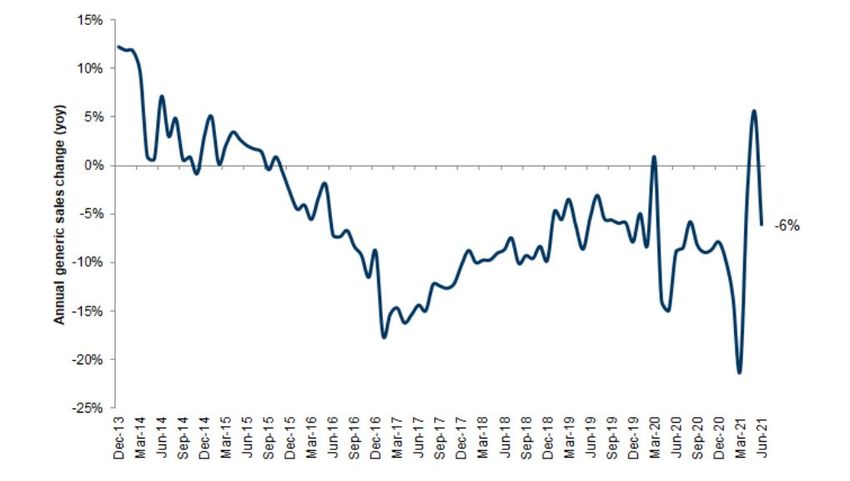

A few early pharma results raised doubts about renewed pricing pressure in US generics. Although most

companies reassured that there was nothing unusual going on. Generics in US are depreciating assets and

new competition constantly keeps entering the market and putting pressure on prices. This price erosion is

usually compensated by new product launches. Companies indicated that new launches were delayed due

to pending inspections from FDA. Some tenders also got bunched up due to the pandemic putting pressure

on the pricing. We would monitor this space and seek more data going ahead before forming a view.

About 90% of pharmaceuticals in US is distributed by just three companies – AmerisoureBergen, Cardinal

Health & McKesson. This consolidation was the primary reason of the generic price erosion during 2015-

2017.

Base Business Price Erosion in US generics

Source: IQVIA, Goldman SachsWe are withdrawing our EPS guidance for the year '21, '22 on account of softness in the U.S.

business due to additional competition, which has led to price erosion as well as in delay in FDA

inspections of our facilities.

There is no business with 100% certainty. If there was, let me know, and I'll get in on with.

Alembic Pharmaceuticals

I think, if you traditionally look at the kind of -- at least our own company central

So as I've said many times, the North American generics and biosimilar space is a space where we

constantly have this, as you say, volume erosion on old products because more competitors come

in and also price erosion on old products because new competitors come in. We are not seeing any

dramatic changes in the market conditions.

We're not seeing a lot less or a lot more suppliers and we're not seeing more or less price erosion

that we've been seeing traditionally.

Teva Pharmaceuticals

Coming to our North America business, happy to report that we have entered the Top 10 generic

companies in the US by prescription driven by the respiratory franchise as well as the strong

limited competition launches over the last two to three years. Our portfolio effort, selection and

execution have limited the impact of price erosion on our portfolio and we hope to continue this

momentum and scale up as new launches come in.

Cipla

Generic deflation is trending relatively in line with our expectations and overall generic deflation

rates are relatively in line with the last couple of years.

AmerisourceBergenDirect to Consumer Brands

In 2009 when Coca-Cola refused to give Costco the price they wanted, Costco pulled Coca-Cola off it’s

shelves. After a month of re-negotiations the brand was back. There has always been a struggle between

distribution and brands for balance of power. Smaller brands earlier had difficulty getting share because

larger brands controlled the distribution and also advertising. E-commerce and digital advertising has been

taking away some of these advantages and a lot of direct to consumer brands have been successful. Larger

consumer companies have tried to launch their own direct to consumer brands and their own e-stores as

well. There are doubts about who will control the data and the consumer once the share of e-commerce

and modern trade increases beyond a threshold. A couple of companies commented on some of these

aspects during the quarter.

As far as e-commerce is concerned, we are also looking at e-commerce from cradle of nurturing our

brands today, with much lesser resources required and doing a test pilot and doing a proof-of-concept

test. It also works as a test marketing for us, and there are not much entry barriers in e-commerce for

us to launch brands, etc.

So, I think this is providing us an avenue to grow and nurture our brands there. And once you scale up,

then we put it to GT. Before e-commerce became significant percentage of business earlier, the cost of

entry or launching a new brand used to be very high and now it's a very easy way.

The second vector is that you can connect with a Millennial and Gen Z very well and you connect with

the brand. As far as the long-term question of eroding the brand equity and it is becoming more of a

commodity and bargaining power shifting in the hands of the Amazons of the world or Big Baskets and

they have the customer data and the consumer data. I completely agree with you, to (fend) that risk

we are also trying to build a D2C model which is direct-to-consumer through our own website so that

we are able to collect the first party data

We can't go against the grain as far as evolution is concerned. And India will very soon leapfrog to the

levels of U.K. and U.S. where also the intellectual property of who’s the consumer who's purchasing,

investing with Amazon or Walmart or others. So, that's the nature of the beast here as far as the

market, and you better go with the flow. And we can't fight with them. The only thing one can do is

build your own platform, so that is what we are doing, building a D2C business and quickly scaling that

business to modern trade and to e-commerce and to connect with the same consumer so that we

know who's buying and who's not.

DaburIf you want to create a digital brand, personal care unit economics works far better simply because

you need an average order value or RSP, the selling price, of at least $8 to $9, which is Rs. 500 to Rs.

600. Usually, personal care is high GM and high (advertising costs).

Food brands, if they operate only digitally, can be successful only if there is a very, very high margin.

So, food brands usually are much better off if they go into brick and mortar and definitely go into

specialty food and modern trade outlets. Personal care, you can actually survive in a D2C plus

marketplace model.

Also some of the brands stand for something, for example, it could be clean beauty, it could be

stands for “Free from”, it could be sustainability. A lot of millennials believe in that. That is how

these brands develop. It is an inspiration for a lot of personal care D2C brands. There are two

brands, which I personally admire, like Glossier and Drunk Elephant. These are US brands, and they

are real fantastic cases of digital marketing.

Marico

We have a dedicated e-commerce P&L. We have also got an entrepreneur in residence. We

launched, Goodness.Me, which is a digital first brand and we have other brands also like Bblunt,

which are very digital. So we really feel, this is an opportunity. The priority number one is to double

down in your core on this but also to build new consumer franchises through this.

Godrej Consumer Products Ltd.

In the last 3 months, the largest selling drain declogger on Amazon is not Drainex, which is the

company leader, but it’s actually a Pidilite product called D-Klog. Now like this, we have been

working with a set of partners and so on and so forth. And a lot of these brands we are looking at

has also B2C. I mean, just to give you an overall perspective, what we did in e-commerce in the full

year in 2019/2020, we are now doing in a single month, for example, in the month of July in this

year. So, we have really upped our lead there. It's a long runway. By no means are we saying that

we are declaring success, but we are absolutely going in the right direction.

PidiliteCNG in Energy Mix

Indian government has committed to increase the share of natural gas in the primary energy mix to 15% by

2030 from current level of about 6%. Primary driver for this are environmental and health concerns.

Cost economics are favourable for CNG vehicles and proliferation of networks by City Gas Distribution

(CGD) companies have led to higher demand for CNG vehicles and conversions from petrol.

Bajaj auto said that every addition of 100 CNG pumps creates demand for 10,000 three-wheelers for the

industry, 90% of which comes to Bajaj Auto.

Right now, you know the discount levels are almost 66% and something like 47% as compared to

petrol and diesel, so such scenario continues or if this differential even widens, we might be in a

position to take the price rise even within one shot also, but any time we take any pricing decision,

we make a combination of what is the cost impact for us, at the same time our primary motto of the

company is always to offer value proposition and keep encouraging new conversions and adoption of

CNG vehicle owners

Mahanagar Gas

On demand side the customer preference for CNG continued to increase.

We are also very hot on the way natural gas is progressing in the country. The prime minister has a

mission to increase the natural gas mix in the energy basket from 6.3% to 15%. CNG and PNG are

two new pillars for that and we will participate in that. Many new cities have come up and the

penetration of CNG cars you would have seen have gone up dramatically.

Maruti

We also have been doing very well on CNG because the opportunity is very strong in the light and

medium duty trucks on the CNG side and because of the support from government and very good

cost economics.

Eicher MotorsLi-ion Batteries

Decarbonization and electrification can drive demand for batteries from 166 GWH currently to 12.1

TWH by 2050. Electric Vehicles will be biggest drivers for this accounting for almost 70% of the demand

by 2050 (Source: Bernstein). Because of scale advantages the battery industry remains heavily

consolidated with top 6 players accounting for 84% of the demand currently. CATL from China, alone

accounts for more than 20% of global capacity. There are over 180 Giga factories in development

globally. Different battery chemistries and technologies are also competing amongst each other. This

will stay a rapidly evolving space.

Battery Technologies:

So right now, we kind of have the Baskin Robbins of batteries situation, where there's so many

formats and so many chemistries, that it's like we've got like 36 flavors of battery at this point. This

is just -- this results in an engineering drag coefficient where each variants of cell chemistry and

format requires as to an amount of engineering to maintain it and troubleshoot, and this inhibits

our forward progress. So it is going to be important to consolidate to maybe -- ideally two form

factors, maybe three, but ideally two. And then just one nickel chemistry and one iron chemistry,

so we don't have to troubleshoot so many different variants

Tesla

Next year, we believe the demand for the battery capacity is going to go up significantly, especially

considering the new product lineup. We believe the battery production capacity demand is going

to jump significantly compared with this year. We are having intense discussions with CATL

regarding the battery capacity supply.

NIO Inc.

We intend to lead on all aspects of battery development and cost reduction, and we are moving

quickly on every front. Our vertical integration approach to battery technology, which includes

building our own cells, will help us scale quickly and efficiently to deploy new innovative chemistries

that boost energy density and reduce cost over time.

General Motors (Q1 2021)Nobody Knows

The growth of the internet will slow drastically, as the

flaw in Metcalfe’s law becomes apparent: most people

have nothing to say to each other*! By 2025, it will be

clear that the internet’s impact on the economy has been

no greater than the fax machines.

Paul Krugman, 1998

(Nobel Memorial Prize in Economic Sciences, 2008)

*WhatsApp is now delivering roughly 100 BN messages a day. (Source: Facebook)Disclaimer This document is for information purposes only. In this document DSP Investment Managers Private Limited (the AMC) has used information that is publicly available, including information developed in- house. Information gathered and used in this document is believed to be from reliable sources. While utmost care has been exercised while preparing this document, the AMC nor any person connected does not warrant the completeness or accuracy of the information and disclaims all liabilities, losses and damages arising out of the use of this information. The statements contained herein may include statements of future expectations and other forward looking statements that are based on prevailing market conditions / various other factors and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. The recipient(s) before acting on any information herein should make his/their own investigation and seek appropriate professional advice. Past performance may or may not be sustained in the future and should not be used as a basis for comparison with other investments. The sector(s)/stock(s)/issuer(s) mentioned in this Document do not constitute any research report/recommendation of the same and the Fund may or may not have any future position in these sector(s)/stock(s)/issuer(s). All opinions, figures, charts/graphs and data included in this Document are as on date and are subject to change without notice. This Document is generic in nature and doesn’t solicit to invest in any Scheme of DSP Mutual Fund or construe as investment advice. “Mutual Fund investments are subject to market risks, read all scheme related documents carefully”. Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

You can also read