THE UGG'LY TRUTH ABOUT - ALLOWABILITY TIFFANY KESSLAR, ESQ. BRUSTEIN & MANASEVIT, PLLC WWW.BRUMAN.COM FEBRUARY 2018 - GFOAA

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

THE UGG’LY TRUTH ABOUT

ALLOWABILITY

TIFFANY KESSLAR, ESQ.

BRUSTEIN & MANASEVIT, PLLC

TKESSLAR@BRUMAN.COM

WWW.BRUMAN.COM

FEBRUARY 2018

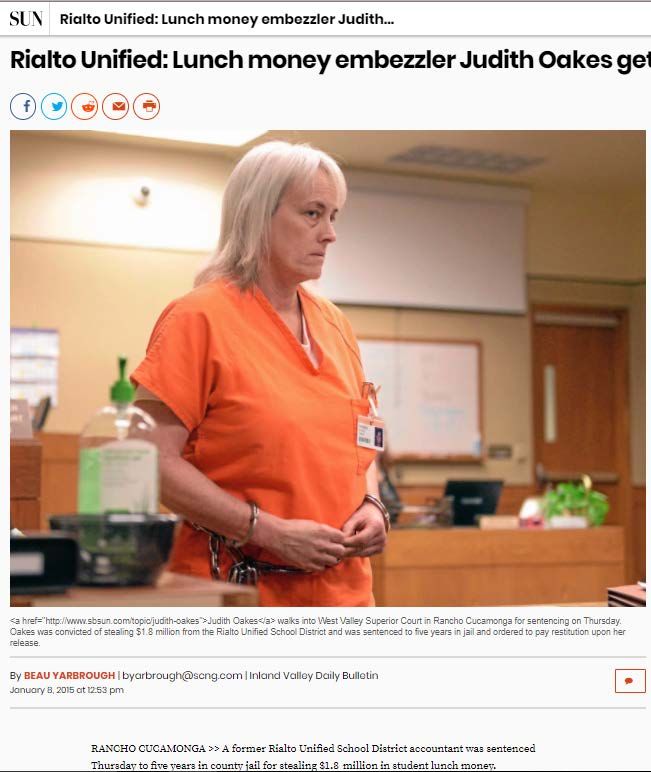

IN THE NEWS

Brustein & Manasevit, PLLC © 2018. All rights reserved. 2

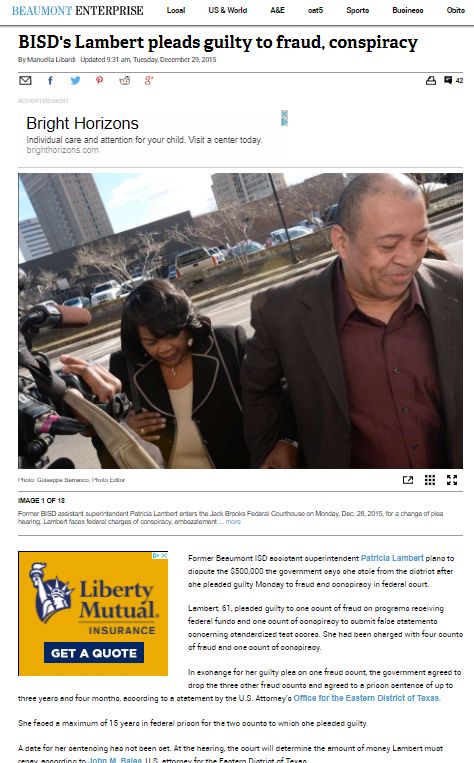

IN THE NEWS

Brustein & Manasevit, PLLC © 2018. All rights reserved. 3

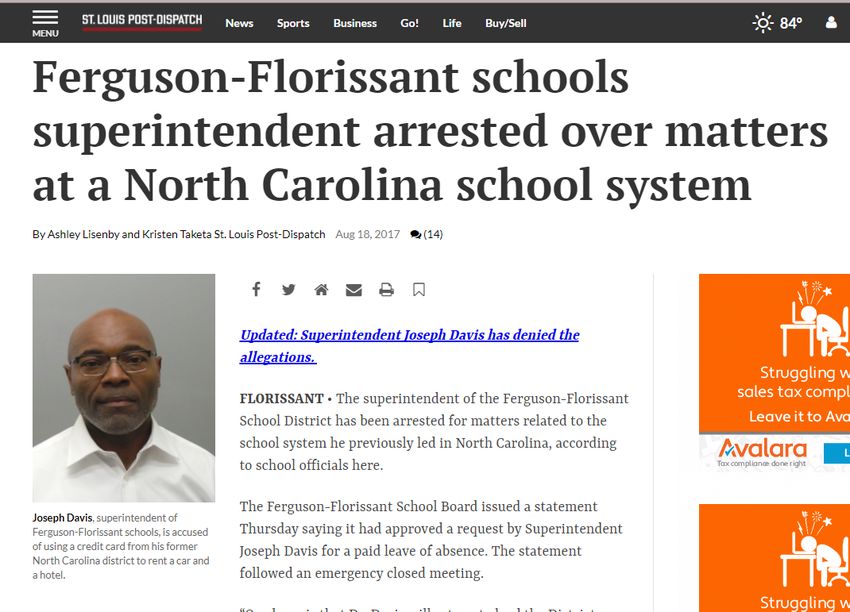

IN THE NEWS

Brustein & Manasevit, PLLC © 2018. All rights reserved. 4

IN THE NEWS

Brustein & Manasevit, PLLC © 2018. All rights reserved. 5

INTERNAL CONTROLS BACK TO BASICS

Brustein & Manasevit, PLLC © 2018. All rights reserved. 7

• S – chedule time to focus on compliance (Control

environment)

• I – nform staff changes (Information and

Communications)

• M – ake sure to identify trouble areas (Risk analysis)

• P – rioritize and improve weaknesses(Control activities)

• L – earn the law

• E – nforce the requirements (Monitoring)

Brustein & Manasevit, PLLC © 2018. All rights reserved. 8

INTERNAL CONTROLS

200.303

a. Non-Federal entities must establish and maintain effective internal control

over the Federal award that provides reasonable assurances that the entity

is managing the award in compliance with federal statutes, regs, and terms

of the award.

• Internal controls “should” be in compliance with:

• The U.S. Comptroller General’s Standard for Internal Controls in the

Federal Government; and

• Internal Control Integrated Framework issued by the Committee of

Sponsoring Organizations of the Treadway Commission (COSO)

9

BRUSTEIN & MANASEVIT, PLLC © 2018. All rights reserved.

INTERNAL CONTROLS (CONT.)

200.303

b.Comply with Federal statutes, regs, and the terms and conditions of

the Federal awards.

c. Evaluate and monitor the non-Federal entity's compliance with

statutes, regs and the terms and conditions of Federal awards.

d.Take prompt action when instances of noncompliance are identified

including in audit findings.

e. Take reasonable measures to safeguard protected personally

identifiable info (PII) and other information designated or deemed

sensitive

10

BRUSTEIN & MANASEVIT, PLLC © 2018. All rights reserved.REQUIRED CERTIFICATION 200.415

• An official authorized to legally bind the non-federal entity must

certify on annual and final fiscal reports or vouchers requesting

payment:

• “By signing this report, I certify to the best of my knowledge and

belief that the report is true, complete and accurate and the

expenditures, disbursements and cash receipts are for the

purposes and objectives set forth in the terms and conditions of

the federal award. I am aware that any false, fictitious, or

fraudulent information or the omission of any material fact, may

subject me to criminal civil or administrative penalties for fraud,

false statements, false claims, or otherwise.”

11

BRUSTEIN & MANASEVIT, PLLC © 2018. All rights reserved.MANDATORY DISCLOSURES

200.113

• Must disclose in writing, in a timely manner:

• All violations of Federal criminal law involving fraud, bribery, or

gratuity violations potentially affecting the Federal award.

• Failure to make disclosures can result in remedies in 200.338

(remedies for noncompliance) including suspension and

debarment.

Brustein & Manasevit, PLLC © 2016. All rights reserved. 12CONFLICT OF INTEREST DISCLOSURE 200.112 The Federal awarding agency must establish conflict of interest policies for Federal awards. All non federal entities must establish conflict of interest policies, and disclose in writing any potential conflict to federal awarding agency or pass through agency in accordance with applicable Federal awarding agency policy. Brustein & Manasevit, PLLC © 2016. All rights reserved. 13

FALSE CLAIMS ACT

• Liability equals triple damages and

a penalty from $5,500 to $11,000

per claim for anyone who

knowingly submits or causes the

submission of a false or fraudulent

claim to the U.S. government

• Includes whistle-blower

incentive and protection

14

BRUSTEIN & MANASEVIT, PLLC © 2018. All rights reserved.Brustein & Manasevit, PLLC © 2018. All rights reserved. 15

REQUIRED POLICIES AND PROCEDURES • Written Cash Management Procedure – UGG Sections 200.302(b)(6) and 200.305. • Written Allowability Procedures - UGG Section 200.302(b)(7) • Written Conflicts of Interest Policy - UGG Section 200.318(c) • Written Procurement Procedures - UGG Section 200.319(c) • Written Method for Conducting Technical Evaluations of Proposals and Selecting Recipients - UGG Section 200.320(d)(3) • Written Travel Policy - UGG Section 200.474(b) • Procedures for managing equipment - UGG Section 200.313(d) Brustein & Manasevit, PLLC © 2018. All rights reserved. 16

QUICK…WHERE ARE YOUR POLICIES AND PROCEDURES!?! Brustein & Manasevit, PLLC © 2018. All rights reserved. 17

POLICY AND PROCEDURES SUGGESTED SECTIONS

• Organization, Structure and Function

• Grant Application Process

• Financial Management System

• Allowability

• Time and Effort Documentation

• Travel

• Procurement

• Inventory/Property Management

• Record Keeping/Record Retention

• Monitoring and Audit Resolution

• Programmatic Requirements

• Notice of Nondiscrimination and Grievance

Procedures

Brustein & Manasevit, PLLC © 2018. All rights reserved. 18POLICY HOT BUTTON ISSUES

Conflict of Interest (UGG Section 200.318(c)(1))

• How do you define a conflict?

• A conflict of interest arises when any of the following has a

financial or other interest in the firm selected for award:

• Employee, officer or agent;

• Any member of that person’s immediate family;

• That person’s partner; and

• An organization which employs, or is about to employ,

any of the above or has a financial interest in the firm

selected for award.

19

Brustein & Manasevit, PLLC © 2018. All rights reserved.POLICY HOT BUTTON ISSUES

Gifts and Gratuities (UGG Section 200.318(c)(1))

• Rule: Must neither solicit nor accept gratuities, favors, or

anything of monetary value from contractors/

subcontractors.

• However, may set standards for situations in which the financial

interest is not substantial or the gift is an unsolicited item of

nominal value.

• Does your agency define a “financial interest that is not

substantial” or a “nominal value” for an unsolicited item?

Brustein & Manasevit, PLLC © 2018. All rights reserved. 20POLICY HOT BUTTON ISSUES

Reporting Conflict of Interest (UGG Section 200.318(c)(1))

• Is there a chain for reporting potential conflicts?

• Alternative if reporting to employee involved in potential conflict?

• What happens if there is a reported and/or nonreported conflict?

• Recusal

• Sanctions

• How do staff know about the requirements?

• Signed certification that employee received and understands conflicts

policy

• Training on policy

21

Brustein & Manasevit, PLLC © 2018. All rights reserved.POLICY HOT BUTTON ISSUES

Contract Administration (UGG

Section 200.318)

• How is your agency maintaining

oversight to ensure that

contractors perform in

accordance with the terms,

conditions, and specifications of

the contract?

Brustein & Manasevit, PLLC © 2018. All rights reserved. 22POLICY HOT BUTTON ISSUES

Vendor Selection Process (UGG Section 200.320)

• Are types of procurement identified?

• Is sole sourcing only used when allowable?

• The item is only available from a single source;

• There is a public emergency that will not permit delay;

• The Federal awarding agency or pass-through

expressly authorizes noncompetitive proposals in

response to a written request; or

• After soliciting a number of sources, competition is

determined inadequate.

Brustein & Manasevit, PLLC © 2018. All rights reserved. 23POLICY HOT BUTTON ISSUES

Regardless of cost, grantee must maintain effective control and

“safeguard all assets and assure that they are used solely for

authorized purposes.” (UGG Section 200.302(b)(4))

Brustein & Manasevit, PLLC © 2018. All rights reserved. 24POLICY HOT BUTTON ISSUES Travel Costs (UGG Section 200.474) • Does your agency require documentation that participation of individual in a conference is necessary for the program? • Do you charge travel on actual costs or use a per diem rate? • Are there written travel reimbursement requirements? Brustein & Manasevit, PLLC © 2018. All rights reserved. 25

POLICY AND PROCEDURES FOLLOW-UP • Make sure policies and procedures are easy to use and easy to find! • Annual training • Training for new staff • Review and revise annually Brustein & Manasevit, PLLC © 2018. All rights reserved. 26

ALLOWABILITY

FACTORS AFFECTING ALLOWABILITY OF

COSTS 200.403

All Costs Must Be:

1. Necessary, Reasonable and Allocable

2. Conform with federal law & grant terms

3. Consistent with state and local policies

4. Consistently treated

5. In accordance with GAAP

6. Not included as match

7. Adequately documented

28

BRUSTEIN & MANASEVIT, PLLC © 2018. All rights reserved.ALLOWABILITY

• All costs must be necessary and reasonable for the

performance of the Federal award and be allocable.

UGG Section 200.403(a)

Brustein & Manasevit, PLLC © 2018. All rights reserved. 29NECESSARY • Is the cost included in your plan? • Is it aligned with the goals of the district/school? • Does your agency have the capacity to use what you are purchasing? • Is the staff knowledgeable regarding the program? Brustein & Manasevit, PLLC © 2018. All rights reserved. 30

REASONABLE • Did you pay a fair price? (UGG Section 200.404) • Was competitive procurement used? (UGG Section 200.319) • If sole sourced, what was the reasoning? (UGG Section 200.320(f)) • Public emergency? • Permitted by USDE/SEA? • No competition? • Only vendor in the world? Brustein & Manasevit, PLLC © 2018. All rights reserved. 31

ALLOCABLE

• Do you have enough time to implement the cost? (UGG Section

200.405)

• Is the program that bought the product using it?

• Is the program sharing the use of the item(s)?

• If so, how are costs being shared?

• How is the use being documented?

Brustein & Manasevit, PLLC © 2018. All rights reserved. 32TIME AND

EFFORT

DOCUMENTATION

Brustein & Manasevit, PLLC © 2018. All rights reserved. 33DOCUMENTING STAFF SALARIES

• Must document staff salaries (UGG Section

200.403(a))

• Based on records that accurately reflect the

work performed and identify the cost objective

that the employee is working on.

Brustein & Manasevit, PLLC © 2018. All rights reserved. 34SALARY DOCUMENTATION These records MUST (UGG Section 200.430(I)(1): 1.Be supported by a system of internal controls which provides reasonable assurance charges are accurate, allowable and allocable; 2.Be incorporated into official records; 3.Reasonably reflect total activity for which employee is compensated; 4.Encompass all activities (federal and non-federal); 5.Comply with established accounting polices and practices; and 6.Support distribution among specific activities or cost objectives. Brustein & Manasevit, PLLC © 2018. All rights reserved. 35

FLEXIBILITY V. INTERNAL CONTROLS

FLEXIBILITY INTERNAL CONTROLS

• Use Percentages or Hours • Accuracy

• No signature required • Reliability

• No set timeframe for • Allocability

documentation

• Official Record

• Electronic system permitted

• Meeting Accounting Policies

and Practices

Brustein & Manasevit, PLLC © 2018. All rights reserved. 36NONCOMPLIANCE

200.430(I)(8)

For a non-Federal entity where the records do not meet these

standards:

• USDE may require personnel activity reports (PARs), including

prescribed certifications or equivalent documentation that support

the records as required in this section.

• PARs are not defined!!

Brustein & Manasevit, PLLC © 2018. All rights reserved. 37AEFFA PROPOSED T&E FLEXIBILITY 1. Certification of Actual Time Worked 2. Blanket Certification 3. Official Record of Employee Activities 4. Electronic Submissions/Approvals 5. Roll-up Time and Effort Tracking 6. Allocation of Effort Using a Basis Other than Time June 15, 2016 Letter from AEFFA, located at www.bruman.com Brustein & Manasevit, PLLC © 2018. All rights reserved. 38

FINANCIAL

MANAGEMENT

CONTROLS

39

BRUSTEIN & MANASEVIT, PLLC © 2018. All rights reserved.IDENTIFICATION OF AWARDS

200.302(B)(1)

All federal “awards” received and expended

• The name of the federal “program”

• Identification # of award

• CFDA Title and Number

• Federal Award I.D. #

• Fiscal Year of Award

• Federal Agency

• Pass-Through (If S/A)

40

BRUSTEIN & MANASEVIT, PLLC © 2018. All rights reserved.FINANCIAL REPORTING

200.302(B)(2)

• Accurate, current, complete disclosure of

financial results of each award in accordance

with 200.327 and 200.328.

41

BRUSTEIN & MANASEVIT, PLLC © 2018. All rights reserved.ACCOUNTING RECORDS 200.302(B)(3)

Source Documentation Must Be Kept On:

1. Federal Awards

2. Authorizations

3. Obligations

4. Unobligated balances

5. Assets

6. Expenditures

7. Income

8. Interest (Eliminated liabilities)

42

BRUSTEIN & MANASEVIT, PLLC © 2018. All rights reserved.INTERNAL CONTROLS

200.302(B)(4)

• Effective control over and accountability for:

1. All funds

2. Property

3. Other assets

• Must adequately safeguard all assets

• Use assets solely for authorized purpose

43

BRUSTEIN & MANASEVIT, PLLC © 2018. All rights reserved.BUDGET CONTROL

200.302(5)

• Comparison of expenditures with budget amounts for each

award

44

BRUSTEIN & MANASEVIT, PLLC © 2018. All rights reserved.WRITTEN CASH MANAGEMENT PROCEDURES

200.302(6)

• Written Procedures to implement the requirements of

200.305 (Payment)

• Insured accounts

• Separate depository accounts NOT required

• Interest bearing (unless certain conditions)

• Interest up to $500 may be retained

• Aggregate across all federal funds

45

BRUSTEIN & MANASEVIT, PLLC © 2018. All rights reserved.WRITTEN ALLOWABILITY PROCEDURES

200.302(B)(7)

• Written procedures for determining allowability of costs in

accordance with Subpart E – Cost Principles

• Procedures can not simply restate the Uniform Guidance Subpart E

• Should explain the process used throughout the grant development

and budget process

• Training tool and guide for employees

46

BRUSTEIN & MANASEVIT, PLLC © 2018. All rights reserved.PROCUREMENT

47

BRUSTEIN & MANASEVIT, PLLC © 2018. All rights reserved.PROCUREMENT STANDARDS

PROCUREMENT BY STATES GENERAL PROCUREMENT STANDARDS

200.317 200.318(A)

• Follow State law • All nonfederal entities must

have documented procurement

procedures which reflect

applicable Federal, State, and

local laws and regulations.

• Follow UGG

48

BRUSTEIN & MANASEVIT, PLLC © 2018. All rights reserved.CONTRACT ADMINISTRATION 200.318(B)

• Nonfederal entities must

maintain oversight to ensure

that contractors perform in

accordance with the terms,

conditions, and

specifications of the contract

49

BRUSTEIN & MANASEVIT, PLLC © 2018. All rights reserved.CONFLICT OF INTEREST

200.318(C)(1)

• Define What Conflict Is.

• What happens when there is a conflict?

• Removal?

• Reporting?

• Are gratuities permitted?

• Forms?

• Reporting?

• Violations?

• Training?

• Annual Forms or Certifications?

50

BRUSTEIN & MANASEVIT, PLLC © 2018. All rights reserved.ORGANIZATIONAL CONFLICT OF INTEREST

200.318(C)(2)

If the non-federal entity has a parent, affiliate, or subsidiary

organization that is not a state or local government the entity must

also maintain written standards of conduct covering organization

conflicts of interest

51

BRUSTEIN & MANASEVIT, PLLC © 2018. All rights reserved.METHODS OF PROCUREMENT

200.320

• Method of procurement:

• Micro-purchase

• Small purchase procedures

• Competitive sealed bids

• Competitive proposals

• Noncompetitive proposals

52

BRUSTEIN & MANASEVIT, PLLC © 2018. All rights reserved.MICRO-PURCHASE

300.320(a)

• Acquisition of supplies and services under $3,500 or less.

• Updated under the Federal Acquisition Regulations (confirmed in the compliance

supplement)

• $2,000 for construction subject to the Davis-Bacon Act

• Raised to $10,000 or less for IHEs only

• May be awarded without soliciting competitive quotations if

nonfederal entity considers the cost reasonable.

• To the extent practicable must distribute micro-purchases equitably

among qualified suppliers.

53NONCOMPETITIVE PROPOSALS

200.320(F)

• Appropriate only when:

• The item is only available from a single source;

• There is a public emergency that will not permit delay;

• The Federal awarding agency or pass-through expressly authorizes

noncompetitive proposals in response to a written request from non-Federal

entity; or

• After soliciting a number of sources, competition is determined

inadequate.

54

BRUSTEIN & MANASEVIT, PLLC © 2018. All rights reserved.SUSPENSION AND DEBARMENT APPENDIX II(H)

2 CFR PART 180 (OMB DEBARMENT SUSPENSION RULES)

• Cannot contract with vendor who has been suspended or

debarred

• Excluded Parties List System in the System for Award

Management (SAM)

• For contracts over $25,000 you must verify that the person with whom

you intend to do business is not excluded or disqualified.

• This MUST be done by either:

a. Checking SAM.gov; or

b. Collecting a certification from that person; or

c. Adding a clause or condition to the covered transaction with that person.

55

BRUSTEIN & MANASEVIT, PLLC © 2018. All rights reserved.56

PROPERTY

MANAGEMENT

BRUSTEIN & MANASEVIT, PLLC © 2018. All rights reserved.EQUIPMENT SUPPLIES

200.33 200.94

Equipment: tangible, nonexpendible, • All tangible personal

personal property having a useful life property other than

of more than one year and an

acquisition cost of $5,000 or more

equipment

per unit. • Computing devices

Grantee may also use its own (200.20) are supplies is

definition of equipment as long as the less than $5,000

definition would at least include all

equipment defined above.

57

BRUSTEIN & MANASEVIT, PLLC © 2018. All rights reserved.EQUIPMENT

200.313(A) AND (C)(4)

• Conditional Title vests with the non-Federal entity.

• Cannot encumber the property without approval of Federal agency or

Pass-through agency

But

• When acquiring replacement equipment, may use the equipment to be

replaced as a trade-in or sell the property and use the proceeds to

offset the cost of the replacement property.

58

BRUSTEIN & MANASEVIT, PLLC © 2018. All rights reserved.USE OF EQUIPMENT

200.313(C)(1) AND (2)

Equipment must be used by the Non-Federal entity in the program or

project for which it was acquired as long as needed, whether or not

the project or program continues to be supported by the Federal

award.

When no longer needed, may be used in other activities with the

following priority:

1. Projects supported by Federal awarding agency

2. Project funded by other Federal agencies

• When used it may be shared (according to the above priorities) provided such use

will not interfere with work on the original projects/programs.

• Exception – Private Schools 76.661

59

BRUSTEIN & MANASEVIT, PLLC © 2018. All rights reserved.EQUIPMENT PROCEDURES

200.313 (D)

Procedures for managing equipment must meet the following

requirements:

1. Property records

• Description, serial number or other ID, source of funding, title, acquisition date

and cost, percent of federal participation, location, use and condition, and

ultimate disposition date including sale price

2. Physical inventory at least every two years

3. Control system to prevent loss, damage, theft

• All incident must be investigated

4. Adequate maintenance procedures

5. If authorized or required to sell property, proper sales procedures to

ensure highest possible return.

60

BRUSTEIN & MANASEVIT, PLLC © 2018. All rights reserved.DISPOSITION

• Equipment 200.313(e) • Supplies 200.314

• When property is no longer needed in any • If there is a residual inventory of

current or previously Federally-funded unused supplies exceeding $5,000 in

supported activity: total aggregate value upon

• Nonfederal entity must request disposition termination or completion of the

instructions from the federal awarding project or program and the supplies

agency if required by the terms of the grant. are not needed for any other federal

• Otherwise, Over $5,000 – pay federal share award, must compensate the federal

• Under $5,000 – no accountability (still must government for its share.

formally dispose)

61

BRUSTEIN & MANASEVIT, PLLC © 2018. All rights reserved.DOCUMENTATION

KNOW WHERE YOUR DOCUMENTS ARE! Brustein & Manasevit, PLLC © 2018. All rights reserved. 63

HOW LONG? Retention Requirements For Records EDGAR – 2 CFR 200.333 • Financial records, supporting documents, statistical records, and all other non-Federal entity records pertinent to a Federal award must be retained for a period of three years from the date of submission of the final expenditure report. • If educational agency, need to keep records for 5 years because of GEPA - Statute of Limitations 34 CFR 81.31(c) Brustein & Manasevit, PLLC © 2018. All rights reserved. 64

HOW MAINTAIN DOCUMENTATION? o When original records are electronic and cannot be altered, there is no need to create and retain paper copies. (UGG Section 200.335) o When original records are paper, electronic versions may be substituted through the use of duplication or other forms of electronic media provided they: o Are subject to periodic quality control reviews; o Provide reasonable safeguards against alteration; and o Remain readable. Brustein & Manasevit, PLLC © 2018. All rights reserved. 65

DOCUMENTATION HOT BUTTON ISSUES

• Are records kept by school, grant, fiscal year?

• Do you backup documentation?

• Where and how often?

• What happens when staff retire or voluntarily leave?

• What happens when staff are fired?

• What happens when a school closes?

• Staff keep documentation at home?

Brustein & Manasevit, PLLC © 2018. All rights reserved. 66Brustein & Manasevit, PLLC © 2018. All rights reserved. 67

DISCLAIMER • This presentation is intended solely to provide general information and does not constitute legal advice or a legal service. This presentation does not create a client- lawyer relationship with Brustein & Manasevit, PLLC and, therefore, carries none of the protections under the D.C. Rules of Professional Conduct. Attendance at this presentation, a later review of any printed or electronic materials, or any follow-up questions or communications arising out of this presentation with any attorney at Brustein & Manasevit, PLLC does not create an attorney-client relationship with Brustein & Manasevit, PLLC. You should not take any action based upon any information in this presentation without first consulting legal counsel familiar with your particular circumstances. Brustein & Manasevit, PLLC © 2018. All rights reserved. 68

You can also read