Third District Banking Conditions - As of December 31, 2020

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

May

18

2021

www.PhiladelphiaFed.org | @PhiladelphiaFed

Third District Banking Conditions

As of December 31, 2020

PREPARED BY THE RISK ANALYTICS & SURVEILLANCE UNIT

SUPERVISION, REGULATION, AND CREDIT

Third District Conditions

Agenda and Table of Contents

Section 1 Executive Summary Slides 3‒11

Section 2 Commercial Bank Performance Slides 12‒31

Earnings Slides 13‒19

Credit Quality Slides 20‒26

Loan Growth Slides 27

Capital Adequacy Slides 28‒29

Liquidity Slides 30‒31

Problem Banks Slides 32

For any questions about this presentation, please contact the Risk Analytics & Surveillance unit at the Federal Reserve Bank of Philadelphia.

2Section 1

Financial Performance Executive Summary

• Financial performance results for Third District community banking organizations* (CBOs) as of 2020:Q4 continue to

demonstrate solid performance, even with the COVID-19 outbreak. Much of the positive financial performance for the period

can be attributed to strong asset quality metrics, which were propped up to assist borrowers through several government

programs, including government stimulus, emergency lending facilities, and forbearances. As these programs roll off in

coming quarters, however, there could be repayment issues, which may result in an increase in problem loans for community

banks.

• Banks continue to report robust loan performance as noncurrent loans remain in-line with the periods prior to the Great Recession. For

example, median noncurrent loans for both Third District and national community banks were little changed year-over-year (YoY) and fell to

54 and 47 basis points, respectively.

• Earnings ratios have returned to pre-crisis levels, driven primarily by strong loan growth and loan performance indicators. However, the

provision expense has more than doubled YoY throughout the District, increasing to 0.18% of average assets. Much of the increase in

provision expense is for institutions that need to conform with the Current Expected Credit Losses (CECL) guidance. By our community bank

definition (see slide 12), five community banks are reporting based on CECL guidelines.

• All CBOs in the District remain well capitalized, as earnings have been accretive to capital. Additionally, there were several banks that either

announced or raised capital at the beginning of the pandemic, primarily via subordinated debt issuances. Stock buybacks were initially

paused in the first few quarters of 2020 but have started to accelerate.

• The median noncore funding ratio for the Third District fell 592 basis points YoY primarily due to the influx of deposits from government

stimulus checks as well as the Payment Protection Program loans, which funded the Small Business Administration (SBA) government-

initiated emergency loan programs.

* Community banking organizations are defined as national and nonmember banks with less than $10 billion in assets, as well as 3

all state member banks in the Third District.Update on the Impact of COVID-19

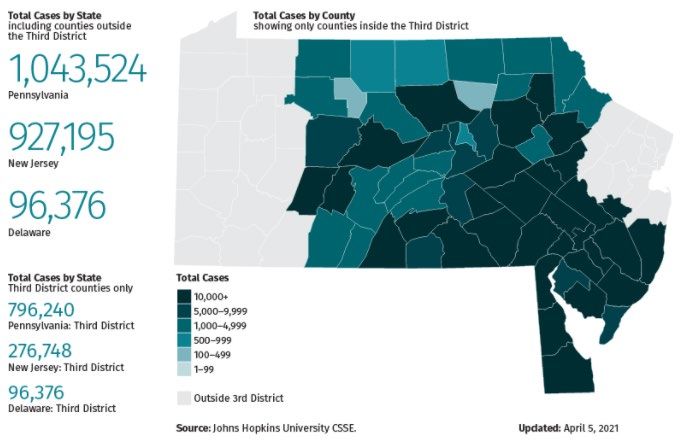

• The coronavirus 2019 disease (COVID-19)

pandemic has created both a public health crisis

and an economic crisis in the United States. The

pandemic has disrupted lives and businesses,

resulting in a global economic slowdown.

• As of May 5, 2021, there have been more than

32.6 million confirmed COVID-19 cases and more

than 579,000 deaths in the United States.

• Vaccinations have been given at record rates,

averaging 3 million vaccines daily in the U.S.,

while cases continue to decline.

• The percentage of the fully vaccinated population

in PA (31.2%), NJ (35.1%), and DE (31.2%)

continues to increase as more vaccine supply

becomes available.

* Data Source: Johns Hopkins University CSSE, Federal Reserve Bank of Philadelphia Research

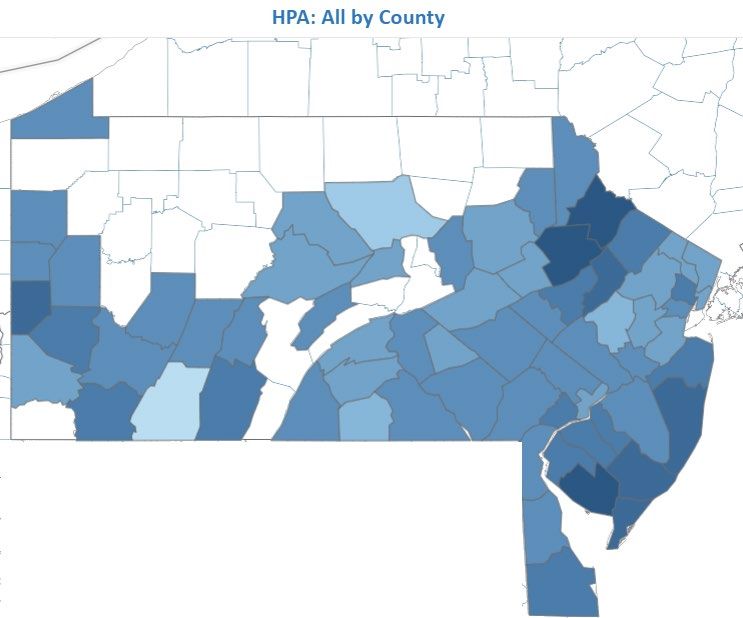

4Home Prices Have Appreciated Significantly YoY, and over 20% in Monroe

County, PA, and Pike County, PA

• Home prices have appreciated significantly YoY throughout the District.

• Some of the counties were severely impacted during the Great Recession but have since rebounded as the housing market

remains robust.

COUNTY STATE HPA Single Family Combined YoY HPA (%)

Top Five YoY HPA (%)

Pennsylvania 9.7

Monroe PA 23.2

Pike PA 21.5 New Jersey 11.4

Cumberland NJ 19.9 Delaware 10.8

Atlantic NJ 19.5

Warren NJ 18.6

Bottom Five YoY HPA (%)

Somerset PA (4.5)

Lycoming PA 0.5

Adams PA 5.1

Hunterdon NJ 5.4

Lebanon PA 5.9

Source: RADAR Data as of February 2021.

5The American Rescue Plan Act of 2021 Was Signed into Law on

March 11, 2021

The $1.9 trillion COVID-19 relief bill expanded federal assistance to renters, homeowners, and

small businesses. Highlights of the bill include:

• An additional $7.25 billion to the Paycheck Protection Program (PPP).

• Expanded weekly unemployment benefits of $300 per week have been extended through

September 16, 2021.

• Direct payments of $1,400 for a single taxpayer or $2,800 for a married couple that files jointly, plus

$1,400 per dependent. This applies to individuals earning up to $75,000 per year and married

couples with incomes up to $150,000.

• The federal ban on foreclosures and mortgage forbearance programs has been extended through

June 30, 2021.

• For borrowers who entered forbearance on or before June 30, 2020, the act provides up to six months of

additional mortgage payment forbearance in three-month increments.

6PA and NJ Were Included within the Top 10 States That Provided

PPP Loans

State Ranking % of Total

Approved Approved Small

State Based on Loan Small % of Count % of Amount

Loans Dollars Businesses*

Amount Businesses

PA 6 101,045 $7,980,972,928 1,100,000 3.47% 2.82% 3.77%

NJ 7 91,532 $6,778,578,088 908,209 2.86% 2.55% 3.20%

DE 48 7,513 $578,584,339 84,675 0.27% 0.21% 0.27%

PPP Approved Loans and Dollar Amounts

Data as of March 28, 2021

400,000 $30,000,000,000

350,000

$25,000,000,000

300,000

$20,000,000,000

250,000

200,000 $15,000,000,000

150,000

$10,000,000,000

100,000

$5,000,000,000

50,000

0 $0

CA

TX

CO

TN

AR

HI

AK

SD

AS

FL

AZ

CT

ID

IL

VA

IN

IA

AL

KY

SC

KS

UT

VT

MN

NH

NM

ND

DC

ME

MT

DE

GU

VI

MP

NY

NJ

OH

MI

GA

MA

NC

MD

MO

LA

NV

NE

MS

WA

OR

OK

RI

WV

WY

PA

WI

PR

Approved Loans Approved Dollars ($MM)

(L-Axis) (R-Axis)

Source: SBA

*Note: Small Business data as of May 2020.

7Loans to Health Care and Professional Services Were the Top

Two Sectors of PPP Loans Nationally

NAICS Subsector Description*

Data Through March 28, 2021

600,000 18%

16%

500,000

14%

400,000 12%

10%

300,000

8%

200,000 6%

4%

100,000

2%

0 0%

and Waste Management…

Retail Trade

Information

Wholesale Trade

Manufacturing

Public Administration

Utilities

Agriculture, Forestry, Fishing

Real Estate and Rental and

Other Services (except Public

Management of Companies

Transportation and

Mining

Health Care and Social

Administrative and Support

Construction

Professional, Scientific, and

Arts, Entertainment, and

Accommodation and Food

Educational Services

Finance and Insurance

Warehousing

Technical Services

and Enterprises

Assistance

Recreation

Administration)

and Hunting

Services

Leasing

Approved Loans % of Amount

(L-Axis) (R-Axis)

* The North American Industry Classification System (NAICS) is the standard used by Federal statistical agencies in classifying business establishments for the purpose of

collecting, analyzing, and publishing statistical data related to the U.S. business economy.

8Total Number and Amount of PPP Loans for Banks Less Than

$50 Billion in Assets

• The Third District accounted for 5.5% of PPP loans nationally.

• Customers Bank is in the top 10 PPP lenders nationally and accounted for 102,765 loans* with an average size of

$21,423.

Total Number of Total Amount of % of Total Loans

District PPP Loans PPP Loans by District

1 Boston 61,792 $ 7,415,055 3.5%

2 New York 345,359 $ 17,336,880 8.1%

3 Philadelphia 159,112 $ 11,784,976 5.5%

4 Cleveland 84,045 $ 9,589,675 4.5%

5 Richmond 144,339 $ 16,663,344 7.8%

6 Atlanta 242,450 $ 25,599,245 12.0%

7 Chicago 177,519 $ 24,054,622 11.3%

8 St. Louis 177,708 $ 15,994,506 7.5%

9 Minneapolis 123,503 $ 13,011,165 6.1%

10 Kansas City 159,313 $ 17,696,353 8.3%

11 Dallas 174,276 $ 19,435,057 9.1%

12 San Francisco 333,976 $ 34,960,445 16.4%

Total 2,183,392 $ 213,541,323

* Source: SBA, Call Report as of December 31, 2020.

9Retail and Office Sectors in the Third District Have Been Negatively

Impacted by the Pandemic

Office Sector

• Center City coworking organizations have driven increases in available office space. Make Offices, which operates three locations in Philadelphia (111 S

Independence Mall, 2001 Market St., and 1635 Market St.) announced it was closing, while Common Grounds (62,000 square feet at 1700 Market St.) and

Industrious (27,000 square feet at Two Liberty Place) were listed for sublease. Additional sublet space may put further pressure on rent growth in the market.

• Philadelphia Metro 12-month net absorption rate* is negative 4.7 million square feet, while asking rent has increased 0.7%. Harrisburg rental rates are flat,

increasing 0.1% YoY. Net absorption is negative 348 thousand square feet, while 61.6K square feet of new office space has been delivered to the market.

The Lehigh Valley 12-month net absorption is negative 25.9 thousand square feet, while the market price per square foot remains stable at $117, which is

largely unchanged since 2016:Q4.

• Permanent work-from-home arrangements or hybrid models continue to pose challenges to the metro’s office performance metrics.

• A January 2021 PWC survey indicated that less than one in five executives say they want to return to the office as it was pre-pandemic

Retail Sector

• The COVID-19 impact on the retail sector has accelerated both bankruptcies and downsizing of footprints/stores. Locally, Lord & Taylor, which closed its

location at the Moorestown Mall in January 2020, announced it would close a 117,000-square-foot location in Bala Cynwyd. Stein Mart is closing its 28,000-

square-foot location at Concord Square in Wilmington, DE, as well as a location in Ellisburg Circle in Cherry Hill, NJ.

• 12-month sales volume declined 20.8% YoY to $1.1 billion in the Philadelphia Metro area, led by an 82% drop in the mall subsector to 4.7 million from 26.6

million at YE 2019.

• Recently, PREIT announced plans to sell lots within its Plymouth Meeting Mall and Moorestown Mall locations to apartment developers to provide mixed-use

space for the properties.

* Note: Absorption and Completion is a measure of supply and demand. A high absorption rate may indicate that demand is warranted to construct additional units.

Source: CosStar, PwC US Remote Work Survey, January 12, 2021

10E-Commerce Has Helped the Third District Industrial Sector Performance

Industrial Sector

• As consumers began to rely more on home delivery during the pandemic, U.S. e-commerce sales have risen 35%.

• Amazon recently leased 94,000 square feet at 700 Ramona Ave. in North Philadelphia, an 820,000-square-foot facility at a former G.M.

plant in Wilmington, as well as a 1.25 million-square-foot building under development in Carney’s Point, NJ.

• Total industrial leasing hit a record high of 21 million square feet in the Philadelphia metro area last year, up 26% from the annual

average of the previous three years.

• Vacancy rates are 5.2% and are expected to remain near 25-year lows based on CoStar forecasts, which would still allow rents to

increase an average of 3.8% annually over the next five years.

Multifamily

• Asking rents among properties rated 3 stars or lower are up 4.2% YoY as of 2020:Q4; 4-5-star properties rent declined 1.3% YoY for

the first negative YoY growth since 2009 when it declined 80 basis points. Rising homeownership rates among well-off millennials

signal near-term challenges for luxury apartment properties.

• 9,800 units are under construction in the Philadelphia metro area, which amounts to 3.0% of the apartment inventory. This is below the

national average but still comparable to what Philadelphia faced heading into 2016, 2017, and 2018.

Source: CosStar

11Section 2

Conditions of Third District Commercial Banks

Reporting Methodology

The quarterly Reports of Condition and Income (Call Report) and Uniform Bank Performance Report (UBPR) are the primary

sources of all information contained in this report unless otherwise noted.

Slides in this section focus on trends among the 82 commercial banks within the Third District and state member, national, and

nonmember commercial banks (CBs). The banks excluded from this analysis meet at least one of the following criteria as of

December 31, 2020:

• Institutions with total assets > $10 billion;

• Credit card banks (credit card loans and receivables > 50% net loans and credit card receivables);

• Trust banks (income from fiduciary activities > 30% of interest + noninterest income); and

• Banks with loans to depository institutions > 30% of net loans.

All Third District state member banks (SMBs) are included in Third District calculations.

The nation consists of all SMBs, national, and nonmember banks within the nation with less than $10 billion in assets.

This report uses the median, the 25th, and the 75th percentiles to compare Third District and national ratios.

The line graphs in the following pages represent the median for the District and the nation, whereas the bar graphs represent

the range of results from the 25th through the 75th percentiles for the data included in each graph.

12Earnings

Return on Average Assets Ratio

• Third District earnings performance, based on the return-on-average assets (ROAA) ratio, has been impacted by COVID-19 and continue to lag the nation.

However, a 27 basis point increase occurred from 2020:Q1 through 2020:Q4.

• Some of this increase in ROAA is due to a decline in provision expense of 5 basis points quarter-over-quarter (QoQ), as asset quality metrics remain strong.

Additionally, with another round of stimulus approved on March 11, 2021, asset quality metrics may continue to be positively impacted, which would increase

earnings results.

Return on Average Assets

1.8% Annually Quarterly

1.5%

1.2%

0.9%

0.6%

0.3%

0.0%

-0.3%

-0.6%

Third District - P25 to P75 Nation - P25 to P75 Third District - Median Nation - Median

The decline in earnings as of year-end 2017 for the District and nation is primarily due to the change in tax law for deferred tax assets (DTA) and mortgage servicing rights (MSR).

Many banks had to revalue their position downward at year-end 2017, which negatively impacted earnings.

13Earnings

Net Interest Margin

• The federal funds rate has fallen 200 basis points since 2019 to a bound of 0.00% ‒ 0.25%, which has negatively impacted

the net interest margin (NIM) as interest income declines.

• The Third District also remains lower than that of the nation before, during, and after the Great Recession.

5.00% Annually Net Interest Margin Quarterly

4.75%

4.50%

4.25%

4.00%

3.75%

3.50%

3.25%

3.00%

2.75%

2.50%

Third District - P25 to P75 Nation - P25 to P75 Third District - Median Nation - Median

The fed funds rate fell from the interest rate bound of 2.00%‒2.25% in July 2019. During the remainder of 2019 and early 2020, there were four decreases in the rates. As of

March 15, 2020, the fed funds rate fell 200 basis points to a bound of 0.00%‒0.25%. Earnings can be negatively impacted due to a lower yield on newly underwritten loans and

14

the inability to reprice deposit and borrowings in a timely manner as to not impact net interest income.Earnings

Yield on Assets and Cost of Funds

• As discussed on the previous slide, the NIM has compressed considerably when compared with that of the nation. The primary reason is because Third District CBOs maintain a lower yield

on assets and a higher cost of funds, driven mostly by a highly competitive rate environment for both loans and deposits.

• With the fed funds rate at the 0.00%‒0.25% bound, earnings may remain pressured for future reporting periods as banks may be forced to underwrite loans at a lower rate. However,

earnings will be positively impacted by the decline in interest expense.

• Given the low-rate environment for the District and the nation, both the cost of funds and yield on assets fell, with the gap between the two falling to 15 basis points in 2020:Q4.

Yields on Assets vs. Costs of Funding

8.00% Annually Quarterly 0.00%

Yield on Assets and Cost of Funds Percentatges

Margin Difference between District and Nation

7.00% -0.10%

6.00%

-0.20%

5.00%

-0.30%

4.00%

-0.40%

3.00% Current difference

has fallen to -0.50%

2.00% 15basis points

1.00% -0.60%

0.00% -0.70%

3D Margin vs. Nation (R Axis) 3D Yield on Assets (L Axis) Nation Yield on Assets (L Axis) 3D Cost of Funds (L Axis) Nation Cost of Funds (L Axis)

15Earnings

Provision Expense

• The provision expense grew during 2020 as publicly traded firms having to comply with CECL guidelines, as five community banks have adopted ASC 2016-13 (CECL).

However, with strong asset quality metrics, many banks reported a lower provision expense as of 2020:Q4.

• Additionally, given the economic stimulus to consumers and corporations, asset quality metrics remain historically strong. As a result, future provision expense to fund the

allowance for capital losses (ACL) or the allowance for loan and lease losses (ALLL) may not experience significant increases. Should the economy begin to wane,

increased provisions could increase, which would have a negative impact on earnings.

Provisions / Average Assets

1.3% Annually Quarterly

1.1%

0.9%

0.7%

0.5%

0.3%

0.1%

-0.1%

Third District - P25 to P75 Nation - P25 to P75 Third District - Median Nation - Median

16Earnings

Noninterest Income

• Historically, noninterest income (fee income, overdraft fees, interchange fees) for the Third District has outpaced that

of the nation. However, in the more recent quarters, the nation has caught up or surpassed the District in certain

instances, placing further pressure on earnings.

1.1% Annually Noninterest Income / Average Assets Quarterly

0.9%

0.7%

0.5%

0.3%

0.1%

Third District - P25 to P75 Nation - P25 to P75 Third District - Median Nation - Median

17Earnings

Overhead Expense

• Median overhead expense has decreased consistently since 2009 for the Third District and the nation. Additionally, as a result of COVID-19, 2020:Q4 salary expense,

occupancy expense, and other personnel expenses have continued to decline. The Third District overhead ratio is the lowest since 2004.

• The reduction in noninterest expenses may also be a sign that banks are trying to run their institutions in an increasingly lean manner so they can control their expenses,

which could have a positive impact on overall earnings.

Overhead Expense to Average Assets

4.0% Annually Quarterly

3.6%

3.2%

2.8%

2.4%

2.0%

Third District - P25 to P75 Nation - P25 to P75 Third District - Median Nation - Median

18Earnings

Core Profitability

• As of 2020:Q4, the Third District’s median core profitability ratio increased by 2 basis points YoY to 1.33%, while the nation decreased

8 basis points to 1.44%. The lower-core profitability measure for the District is due primarily to a lower NIM but has increased slightly

on a quarterly basis to lead the nation by 7basis points.

Core Profitability

Pre-Tax Income Excluding Provisions / Average Assets

2.50% Annually Quarterly

2.00%

1.50%

1.00%

0.50%

0.00%

Third District - P25 to P75 Nation - P25 to P75 Third District - Median Nation - Median

19Asset Quality

Noncurrent Loans

• Asset quality metrics continue to exhibit strong performance. However, asset quality performance for 2020:Q4 and

the previous quarters could have masked some problem loans, which were kept current due to the government

stimulus, emergency lending facilities, and forbearances. As some of these programs end, obligors may not be able

to service their debt, which could result in an increase in problem loans.

4.0% Annually Noncurrent Loan Rate Quarterly

3.5%

3.0%

2.5%

2.0%

1.5%

1.0%

0.5%

0.0%

Third District - P25 to P75 Nation - P25 to P75 Third District - Median Nation - Median

20Asset Quality

Noncurrent Loans by Category

• Third District loan performance continues to show ongoing improvement among the principal loan categories, which are near

or below 2006–2007 metrics. As the median C&I noncurrent loans ratio has fallen 54 basis points to 0.53% YoY, there was a

small uptick in noncurrent loans for total CRE loans (up 17 basis points to 0.83%) and nonfarm nonresidential CRE (up 23

basis points to 0.92%).

Noncurrent Loan Ratios by Loan Category

8.00% Annually Quarterly

7.00%

6.00%

5.00%

4.00%

3.00%

2.00%

1.00%

0.00%

All Loans Single & Multifamily Consumer C&I C&LD CRE (Total) Nonfrm Nonres

This chart uses a 10% capped mean, or winsorized mean, to compute the average District and national ratios. The capped mean is a statistical measure of central tendency

without losing observations, especially robust for a small sample. The capped mean is used to reduce the effects of outliers on the calculated average by “capping” values of the

21

upper and lower 5% bounds of institutional data reported.Asset Quality

Nonperforming Assets

• Additionally, the Third District’s median level of nonperforming assets has been decreasing steadily since 2012. The

decline is primarily due to the lower level of other real estate owned (OREO) within the District as compared with the

nation.

Nonperforming Assets*

6.0% Annually Quarterly

5.5%

5.0%

4.5%

4.0%

3.5%

3.0%

2.5%

2.0%

1.5%

1.0%

0.5%

0.0%

Third District - P25 to P75 Nation - P25 to P75 Third District - Median Nation - Median

* NPAs (nonperforming assets) are the total of other real estate owned (OREO) + noncurrent loans (loans 90+ days past due + nonaccrual loans).

22Asset Quality

The ALLL Reserve Coverage Ratio

• The ALLL reserve coverage ratio for both District and national CBOs continues to increase, primarily because of the higher unemployment rate from the pandemic.

• The increase in the ALLL coverage ratio was two-fold: Provision expense more than doubled from 2019:Q4, from $130 million to $337 million. Additionally, asset quality

remains strong through 2020:Q4, with noncurrent loans decreasing to pre-Great Recession performance.

Allowance for Loan & Lease Loss Coverage Ratio*

325% Annually Quarterly

275%

225%

175%

125%

75%

25%

Third District - P25 to P75 Nation - P25 to P75 Third District - Median Nation - Median

* The reserve coverage ratio, or ALLL coverage, is calculated by dividing noncurrent loans by the allowance for loan and lease losses.

23Asset Quality

Net Charge-off Rates

• Net charge-off rates have declined steadily since 2010 and are now below pre-crisis loss levels for both the

District and the nation. This may change in coming quarters as stimulus other emergency loan programs begin

to tail off, which may, in turn, lead to an increase in charge-offs within the District and nation.

Annually

Net Charge-offs / Loans

1.4% Quarterly

1.2%

1.0%

0.8%

0.6%

0.4%

0.2%

0.0%

-0.2%

Third District - P25 to P75 Nation - P25 to P75 Third District - Median Nation - Median

24Asset Quality

Troubled Debt Restructurings*

• Third District troubled debt restructurings continue to decline annually; however, the metrics

remain somewhat elevated when compared with the nation.

Annually

Troubled Debt Restructurings** Quarterly

2.4%

2.1%

1.8%

1.5%

1.2%

0.9%

0.6%

0.3%

0.0%

Third District - P25 to P75 Nation - P25 to P75 Third District - Median Nation - Median

* Troubled debt restructurings (TDRs) were not included on the Call Report until the March 2009 reporting period.

** Under the new standard, a holding company will recognize the entire gain, if any, and derecognize the OREO at the time of sale if the transaction meets the requirements of

25

FASB Topic 606 and its five criteria.Asset Quality

Other Real Estate Owned and Foreclosures

• One- to four-family other real estate owned (OREO*) continues to decrease; however, the Third District continues to trail in the

foreclosure process because of the judicial foreclosure process in Pennsylvania, Delaware, and New Jersey.

• Foreclosures have continued to decline due to the stimulus checks and the moratorium of foreclosures, which was recently extended

until June 30, 2021. Additionally, loans in forbearance continue to decline as consumers catch up on past payments.

1-4 Family OREO*** Loans in Process of Foreclosure**

1.6% Annually Quarterly 1.0% Annually Quarterly

1.4% 0.9%

0.8%

1.2%

0.7%

1.0%

0.6%

0.8% 0.5%

0.6% 0.4%

0.3%

0.4%

0.2%

0.2%

0.1%

0.0%

0.0%

Third District - P25 to P75 Nation - P25 to P75 Third District - P25 to P75 Nation - P25 to P75

Third District - Median Nation - Median Third District - Median Nation - Median

* As a percentage of one- to four-family loans.

** Loans in the process of foreclosure were not included in the Call Report until the March 2008 reporting period. Pennsylvania, Delaware, and New Jersey are all judicial foreclosure states that can extend

the foreclosure process. 26

*** Under the FASB’s new revenue recognition standard (Topic 606), a bank or holding company will recognize the entire gain, if any, and derecognize the OREO at the time of sale if the transaction meets

the requirements of FASB Topic 606 and its five criteria.Loan Growth

Third District Commercial Bank Median Loan Growth*

• Third District commercial bank median loan growth* in most categories YoY was positive; however, loan contraction continues to occur in the

junior lien, HELOC, and leases categories.

• The significant increase in the C&I portfolio was due to the PPP emergency loan program, which totaled ~$10 billion in loans for the District as of

2020:Q4.

Leases 0.22%

HELOC -2.23%

Construction & Land Development 14.07%

Junior Liens -5.41%

Nonfarm Nonresidential CRE 6.86%

Consumer -6.73%

Multifamily 8.58%

Farmland -3.20%

1-4 Family Mortgages 2.31%

Commercial & Industrial 80.22%

Total Loans 12.38%

-20% -10% 0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

* This chart shows the median YoY percentage loan growth for Third District commercial banks that meet the community bank definition on Slide 8.

27Capital Adequacy

Total Risk-Based Capital Ratio

• Although capital ratios have increased post-crisis, Third District and national total risk-based capital (RBC) levels have mostly flattened since 2011, with the exception of 2020. The decline

for the first six months is due to banks opting-in to the community bank leverage ratio (CBLR), which included 26 community banks in the Third District as of 2020:Q4. Most of these banks

had ample levels of total RBC as of 2019:Q4 prior to the CBLR opt-in.

• The total RBC ratio also remains well below the level of the nation, a difference of 103 basis points as of 2020:Q4. Much of this can be attributed to Third District CBOs having a larger

concentration of commercial real estate (CRE) loans, which require a higher amount of capital.

Annually

Total Risk-Based Capital

22% Quarterly

20%

18%

16%

14%

12%

10%

Third District - P25 to P75 Nation - P25 to P75 Third District - Median Nation - Median

28Capital Adequacy

Dividend Payments*

• As of 2020:Q4, median dividend payments* in the Third District climbed to levels seen prior to the COVID-19 outbreak. Many banks took an abundance of caution to

preserve capital given the economic uncertainty. However, as asset quality remains strong and earnings have increased, banks did increase their dividends.

• Some banks have provided dividends to their holding companies to service debt; for example, 13 banks in 2020 have issued subordinated debt.

Annually

Dividends Quarterly

100%

80%

60%

40%

20%

0%

Third District - P25 to P75 Nation - P25 to P75 Third District - Median Nation - Median

* Some banks pay dividends semiannually; therefore, 1Q and 3Q dividends are normally lower than those for 2Q or 4Q. However, the dividend payout (DPO) ratio for the Third

District is above the value when compared with a year ago, which may indicate that banks may have paid out more of their net income as dividends in 2020.

29Liquidity

Short-Term Investments and Loans to Assets

• Third District banks continue to hold fewer short-term investments compared with that of the nation. Rather, Third District institutions

have opted to grow their loan portfolio, and while organic loan growth was not robust, PPP loans have helped increase the growth of

total loans and assets. However, loan growth was not as strong as 2020 progressed, with the 2020:Q4 Third District median loan to

asset ratio equal to 2015 metrics.

Short-Term Investments / Assets* Loans / Assets

22% Annually Quarterly 85% Annually Quarterly

20%

80%

18%

16% 75%

14%

70%

12%

10% 65%

8% 60%

6%

55%

4%

2% 50%

0%

45%

Third District - P25 to P75 Nation - P25 to P75

Third District - P25 to P75 Nation - P25 to P75

Third District - Median Nation - Median Third District - Median Nation - Median

* Short-term investments equals the sum of interest-bearing bank balances + federal funds sold + securities purchased under agreements to resell + debt securities with a

remaining maturity of one year or less.

30Liquidity

Noncore Funding Dependence Ratio

• Many Third District banks depend on noncore funding sources to fund balance sheet growth given the competition for deposits. As a

result, Third District exposure to these noncore sources of funding continues to outpace that of the nation. However, there has been a

decrease in noncore funding in 2020 due to increased deposits as a result of the PPP emergency loan program as well as the

government stimulus packages for consumers. At present, banks are flush with liquidity and should be for some time.

Net Noncore Funding Dependence*

40% Annually Quarterly

35% In 2010, the FDIC increased the

30% insurance limit from $100,000 to

the current $250,000 threshold.

25%

20%

15%

10%

5%

0%

-5%

-10%

-15%

-20%

Third District - P25 to P75 Nation - P25 to P75 Third District - Median Nation - Median

* Net noncore funding dependence measures the degree to which banks fund longer-term assets with noncore funding sources.

31Problem Banks

• Problem banks within the nation increased by 5 YoY to 56 as of 2020:Q4; however, a downward trend has continued since the peak in 2011.

• Four banks failed 2020, including Ericson State Bank in Ericson, NE, The First State Bank in Barboursville, WV, First City Bank of Florida, and

Almena State Bank, in Almena KS.

Problem Bank Changes

250 1000

■ Bank failures during quarter 900

200

■ Quarterly change in problem banks 800

150 700

600

100

500

50

400

0 300

200

-50

100

-100 0

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13

2Q13

3Q13

4Q13

1Q14

2Q14

3Q14

4Q14

1Q15

2Q15

3Q15

4Q15

1Q16

2Q16

3Q16

4Q16

1Q17

2Q17

3Q17

4Q17

1Q18

2Q18

3Q18

4Q18

1Q19

2Q19

3Q19

4Q19

1Q20

2Q20

3Q20

4Q20

Δ Problems (L axis) Failures (L) Problem Bks (R axis)

Source: FDIC; problem banks are defined as having a CAMELS composite rating of 4 or 5. CAMELS is an acronym for the components assessed at a safety and soundness

examination. The components are Capital, Asset Quality, Management, Earnings, Liquidity, and Sensitivity to Market Risk.

32

The 20-year high of problem institutions reached 888 as of 2011:Q1.You can also read