Unlocking Arctic Potential: Expanding Our Global LNG Footprint to 2030 - Energy Affordability, Security & Sustainability

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Unlocking Arctic Potential: Expanding Our Global LNG Footprint to 2030 Energy Affordability, Security & Sustainability Investor Meetings June 2020

1Q 2020 Financial Highlights

21%

2.8 REVENUE

(US$ bln)

1.5 NORMALIZED EBITDA

(US$ bln)

15%

19%

0.8 NORMALIZED PROFIT*

(US$ bln)

0.3 FREE CASH FLOW

(US$ bln)

7%

0.7 CAPEX

(US$ bln)

15%

NET DEBT

-0.12 TO NORMALIZED

EBITDA** (x)

n/a

*excluding the effect of foreign exchange gains (losses) of subsidiaries and

our proportionate share in foreign exchange gains (losses) of our JVs

** normalized EBITDA from subsidiaries

y-o-y performance

✔ Energy Affordability ✔ Energy Security ✔ Energy Sustainability

2

1Q 2020 Operational Highlights

SALES VOLUMES

Natural Gas LNG Oil Products Crude Oil LPG

18.2 bcm 2.5 bcm 1.7 mmt 1.2 mmt 0.7 mmt

3

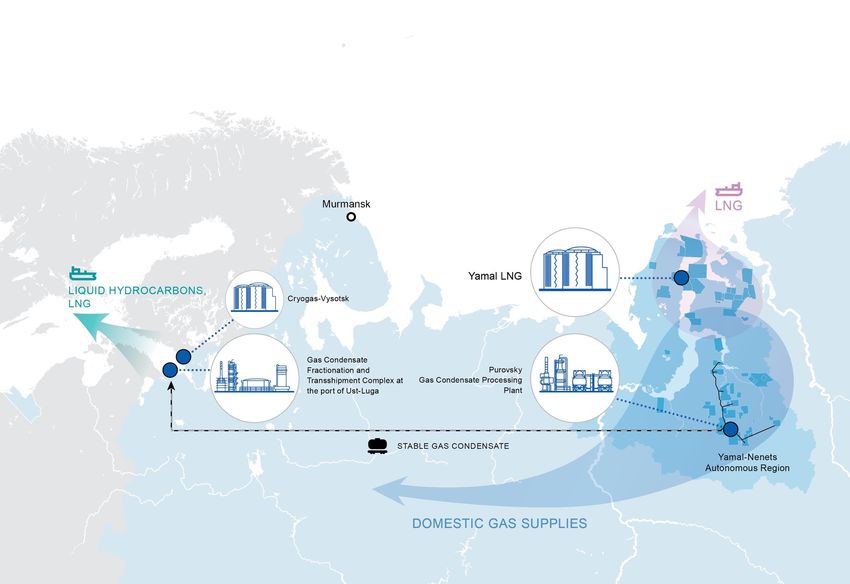

Monetizing Our Resource Base (1Q 2020)

Yamal LNG

(nameplate capacity

– 17,4 mmtpa)

PRODUCING FIELDS

Natural gas LNG

Yamal Trade

Natural gas by pipeline Cryogas-Vysotsk

(nameplate capacity – 660 mtpa)

Separation and

Unstable gas NOVATEK Gas & Power

treatment

condensate by Asia

pipeline LNG

Crude

oil by

pipeline

88% 12%

TO DOMESTIC MARKET TO INTERNATIONAL MARKET BY SEA

18.2 bcm 2.5 bcm

61% / 39%

Purovsky Plant (nameplate capacity - 11 mmtpa) Ust-Luga Complex (nameplate capacity - 6 mmtpa)

TO DOMESTIC/

INTERNATIONAL 2.8 mmt

Stabilization

1.7 mmt

Fractionation

MARKET of gas of stable gas

condensate condensate

1.2 mmt

76%

81% Naphtha Jet fuel Fuel oil Gasoil

24%

Stable gas

condensate 63% 16% 10% 11%

LPG 19%

80% / 20% 90% / 10% ~100%

TO DOMESTIC/ TO DOMESTIC/ TO INTERNATIONAL MARKET

INTERNATIONAL MARKET INTERNATIONAL MARKET BY SEA

0.7 mmt 0.4 mmt 1.7 mmt

4

NOVATEK at a Glance 2019

1.1 BLN BOE 590 MLN BOE 65.7 BCM

Total proved Hydrocarbon Natural gas sales

hydrocarbon addition production in Russia

(SEC)

16.3 BLN BOE 10.1 % 12.8 BCM

Share of natural gas LNG sales

Total proved hydrocarbon

production in Russia

reserves (SEC)

252% +8.6 % 18.4 MMT

Organic reserve Natural gas LNG offloaded from

replacement rate production increase Yamal LNG

Fields and license

12.1 MMT 16.4 MMT

areas

Liquids production Liquids sales

✔ Energy Affordability ✔ Energy Security ✔ Energy Sustainability 5

Internally Funded Investment Program

2 000 20,0

1,724

1 500 15,0

1,260

1 000 10,0

981 1,001

932 889

830 846 842 841

729 751 769

662 684

Operating CF / CAPEX

500 595 5,0

443

US$ mln

0 0,0

-500 - 5,0

Source: Company data

LNG CAPEX

-1 000 2 13 20 27 14 95 32 85 70 165 187 305 385 167 234 410 304 - 10,0

Non-LNG

CAPEX

106 93 71 122 50 68 85 92 117 190 184 279 263 389 322 378 440

-1 500 - 15,0

1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19 1Q20

LNG CAPEX Non-LNG CAPEX OCF OCF / CAPEX (rh)

Core investments funded primarily through internal cash flows

✔ Energy Affordability ✔ Energy Security ✔ Energy Sustainability

6

NOVATEK Robust FCF Generation over Shale

Producers (USD mln)

3 000

2 500

2 000

1 500

2 580

2 087 2 239

1 000 1 950

1 386 1 281 1 350

500 1 038 919

620

0 -62

-182

-501 -532 -505 -519

-700 -773 -737

-500 -1 038

-1 000

-1 500

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

NOVATEK 34 Shale-Focused O&G average

Over the decade, US shale-focused O&G companies reported negative

free cash flows every year, totaling $189 billion

Source: Company data, IEEFA (Shale Producers Spilled $2.1 Billion in Red Ink Last Year)

✔ Energy Affordability ✔ Energy Security ✔ Energy Sustainability 7

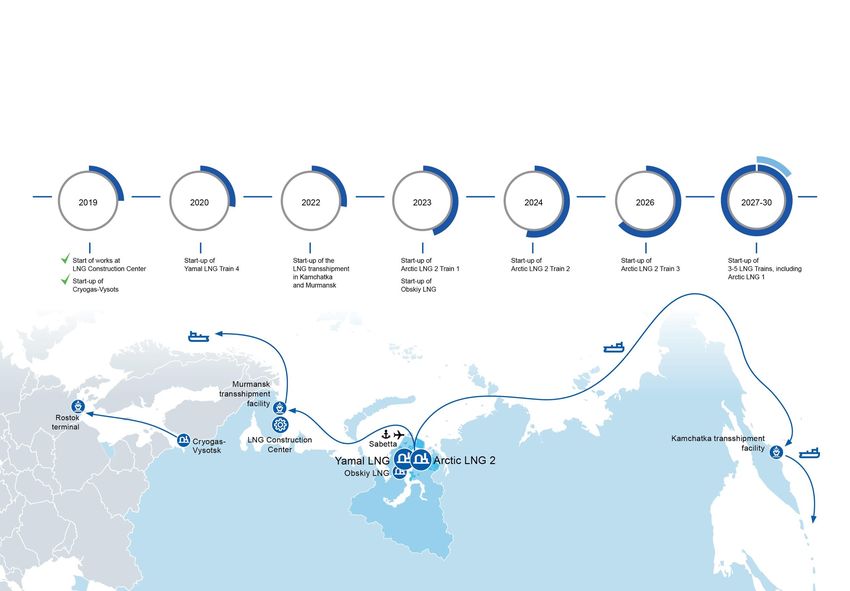

Strategy’s Objectives and Key Events 2018-2020

Cryogas-Vysotsk

FID made for Train 1

Yamal LNG

Start-up of Train 3 ARC7 LNG carriers Yamal LNG

Cryogas-Vysotsk

15 carriers in Start-up of Train 4

Start-up of Train 1

Arctic LNG 2 operation

FEED completion Natural gas liquefaction

ARC4 LNG carriers complex in

Kamchatka 7 carriers in Magnitogorsk

Transshipment operation Launch

Facility

FEED completion

2020

East- East-Tazovskoye field

Yaro-Yakhinskoye field Arctic LNG 2

Urengoyskoye + Commissioning

Commissioning FID made

North-

Esetinskoye field Dorogovskoye field

South-Khadyryakhinskoye field Commissioning Commissioning

Commissioning

North-Russkoye Gas condensate de-

field ethanization unit extension

West-Yurkharovskoye Commissioning for Achimov layers

field

development at the

Commissioning Transshipment Samburgskiy LA

facility in Commissioning

Zeebrugge

Up to 8 MMTPA

✔ Energy Affordability ✔ Energy Security ✔ Energy Sustainability

8

Stable Gas Prices in Russia to Maintain Domestic Business

5

4

3

Henry Hub

$/MMBtu

2

1 Domestic price

in Russia

0

Jan-15 Jan-16 Jan-17 Jan-18 Jan-19 Jan-20

Source: FTS Russia, NYMEX, IHS

Russian domestic gas business still a critical part of our revenues and

operating cash flows

✔ Energy Affordability ✔ Energy Security ✔ Energy Sustainability 9

Global LNG Market

✔ Energy Affordability ✔ Energy Security ✔ Energy Sustainability

10Significant Potential for Increased Gas

Consumption by Emerging Markets

Size of the circle depends on the population

✔ Energy Affordability ✔ Energy Security ✔ Energy Sustainability

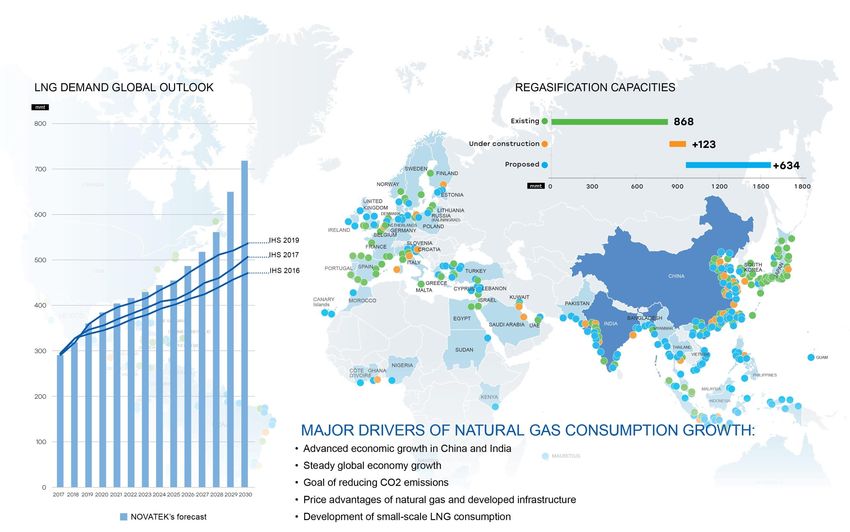

11Global LNG Demand – Stronger than Expected

>740

800

mmtpa

700

600 Europe

500

400 314

300 Asia-

Pacific

200

100

0

2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037 2038 2039 2040

Asia Pacific Europe Middle East North America South America Africa

Source: NOVATEK’s interpretation of Wood Mackenzie data

Asia and Europe will account for 88% of incremental LNG demand

✔ Energy Affordability ✔ Energy Security ✔ Energy Sustainability

12Asian Gas Market Prospects

1400 bcm 1274

1200

1000

Gap to be filled mostly

by LNG and pipeline gas

>780 bcm

800

600 740

400 Domestic production?

200

0

2019 2022 2025 2028 2031 2034 2037 2040

Onstream Under Development Probable Development Technical Reserves YTF Demand

Source: NOVATEK’s interpretation of Wood Mackenzie data

✔ Energy Affordability ✔ Energy Security ✔ Energy Sustainability

13European Gas Market Prospects

700 bcm

600

517

500

548

400

Need for global LNG

300

and pipeline gas >430 bcm

200

100

0

2019 2022 2025 2028 2031 2034 2037 2040

Indigenous Production* Contracted - LNG Contracted - North Africa Piped

Contracted - Norway Piped Contracted - Russia Piped Contracted - Southern Corridor Piped

Total requirements†

Source: NOVATEK’s interpretation of Wood Mackenzie data

✔ Energy Affordability ✔ Energy Security ✔ Energy Sustainability

14LNG Demand Increase of around 10% YTD

Import volumes increase/decrease in Jan-May 2020 vs 2019, mmt

0,6 0,5

1,3

1,3

1,4 -1,3

1,4

1,8

1,9

2,3

2,7

161

148 Increase Y-o-Y

Decrease Y-o-Y

Jan-May S. Korea Turkey India UK China Other Spain Belgium Taiwan France Japan Jan-May

2019 2020

Source: NOVATEK’s interpretation of IHS data

Despite pandemic lockdowns the growth of LNG imports to China was 6% YOY

✔ Energy Affordability ✔ Energy Security ✔ Energy Sustainability 15Historical and expected global liquefaction

nominal capacity additions

115 capacity additions 110+ capacity additions

40 39

35 32

28

30 27

23

25 20

17

20

15 13 12

11 11

10 5

5 2

0

-5 -1

-10 -8

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Asia Pacific Europe Middle East Africa North/South America

Delay of 200+ mmtpa projects due to lower prices and COVID-19 already in 2020

Source: NOVATEK’s interpretation of Wood Mackenzie data (includes only projects Operational and Under Construction)

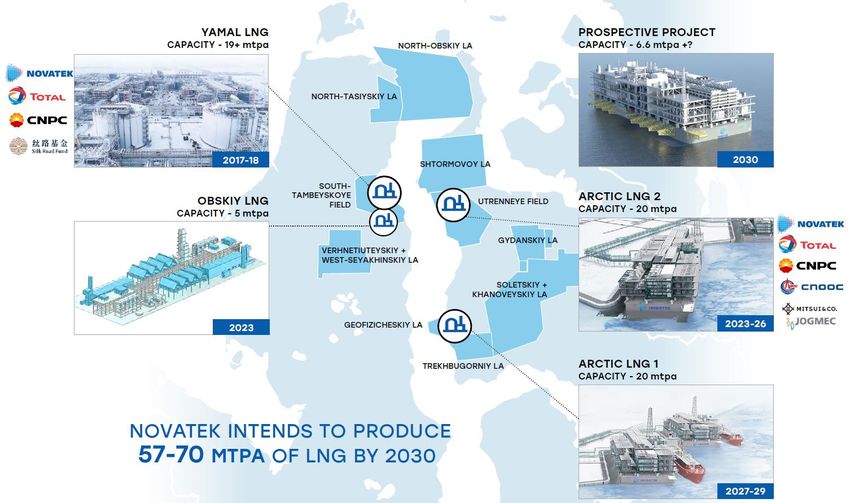

✔ Energy Affordability ✔ Energy Security ✔ Energy Sustainability 16NOVATEK’s LNG Production Platform

2024-25

TREKHBUGORNIY LA

BUKHARINSKIY LA

2027-30

✔ Energy Affordability ✔ Energy Security ✔ Energy Sustainability

17NOVATEK’s LNG Production Timeline

18.6 19.6 19.6 26 38 44 57-70

mmt mmt mmt mmt mmt mmt mmt

18Yamal LNG Runs Above Capacity

Yamal LNG ramp-up ahead of

schedule and on budget

Train 1

completed on schedule

5.5 mmtpa

Train 2 completed 6 months

5.5 mmtpa ahead of schedule

Train 3 completed >12 months

5.5 mmtpa ahead of schedule

Train 4 start-up is expected

0.9 mmtpa in 2020

>30 million tons of LNG produced

…an aggregate share of the global More than 400 Earlier launch of Yamal LNG

LNG market LNG cargos have allows to offtake additional

The largest LNG project in Russia been offloaded since LNG volumes

the start-up

✔ Energy Affordability ✔ Energy Security ✔ Energy Sustainability

19New LNG marketing paradigm

New contracts signed by price indexation Average oil indexations in new contracts

50

15%

40 14.4%

Oil-indexation level

14% 14.1% 13.9%

30

ACQ (mmtpa)

13% 13.0%

20 12.0%

12% 12.1%

11.6%

11.7%

10 11.3%

11%

Only SPA’s to end-users

0 10%

2011 2012 2013 2014 2015 2016 2017 2018 2019 2011 2012 2013 2014 2015 2016 2017 2018 2019

Oil European hub Henry Hub Hybrid

Source: NOVATEK’s interpretation of Wood Mackenzie data

✔ Energy Affordability ✔ Energy Security ✔ Energy Sustainability 20Spot LNG market increasing volumes

Share of major spot exporters in 2019, mmt Volume of non long-term LNG trade, mmt

120 35%

30%

100

25%

80

20%

60

>115 MMT

15%

40

10%

20

5%

0 0%

1996

2001

2008

1995

1997

1998

1999

2000

2002

2003

2004

2005

2006

2007

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

Source: NOVATEK’s interpretation of IHS data

Non long-term trade % of gross trade

✔ Energy Affordability ✔ Energy Security ✔ Energy Sustainability 21Large-Scale LNG Sales

LNG Sales of

NOVATEK Gas & Power Asia

1Q Total (1)

2020 from 2017

Yamal LNG

Number of Norway

cargos 23 200

Volumes, mmt 1.7 14.0 United Kingdom

Netherlands

Belgium

Total dispatched from Yamal LNG

France

Number of Spain

cargos 67 436

China

Volumes, mmt 5.0 31.9 Thailand

India

transshipment

Brazil delivery point

NOVATEK sales

(1) as of 31 March 2020

(2) taking into account all supplies from the Project

(2)

29 countries consumed natural gas molecules from Yamal LNG

✔ Energy Affordability ✔ Energy Security ✔ Energy Sustainability

22Arctic LNG 2

Natural gas production at Utrenneye field, bcm

35

30

25

20

15

10

5

0

2023 2024 2025 2026 2027 2028 2029 2030

Gas condensate production at Utrenneye field, mmt

2,0

1,5

1,0

0,5

0,0

2023 2024 2025 2026 2027 2028 2029 2030

Project Participants

FID made (September 2019)

CAPEX is estimated at US$21.3 bln equivalent

60%

2P reserves under PRMS of the Utrenneye field : 10%

• 1,180 bcm of natural gas

• 62 mmt of liquids

19.8 10%

More than 5,000 people working at the field. Completed the mmtpa

backfilling of the Gas Treatments Unit-1 for the first dome, well

pads 1, 2, and 3 for production drilling 10%

Received official permission on completing Dry Dock #1, 10%

continue with rock blasting at Dry Dock #2

23Cryogas-Vysotsk

Medium-tonnage LNG plant

on the Baltic Sea

LNG production facility and

a transshipment terminal

thousand tons per annum –

660 initial design capacity

designed to handle 30 mcm

capacity LNG carriers

51% Our participation interest

26 shipments by tankers and 195 by

trucks in 1Q2020 = 112 thousand tons

Medium-scale LNG target niche markets and customer segments

✔ Energy Affordability ✔ Energy Security ✔ Energy Sustainability

24All 15 ARC7 Ice-Class LNG Tankers in Operation

Speed in open Speed in ice 1.5 m

water thick

LNG tanker Vessel power

capacity

✔ Energy Affordability ✔ Energy Security ✔ Energy Sustainability

25LNG Logistics to Asia

12

days

85

36

days 29

2019 2040

160

110

79

6 35

days

2019 2040 2019 2040

145 26

days

46 14 7

days

days 4

2019 2040 days

15 86

days

76

2019 2040

Source: NOVATEK’s interpretation of IHS data

✔ Energy Affordability ✔ Energy Security ✔ Energy Sustainability

26Sustainable Development – Integral Part of Strategy*

Sustainable

reporting with

GRI

recommendations

from 2005

* Corporate Strategy 2018-2030

✔ Energy Affordability ✔ Energy Security ✔ Energy Sustainability

27Sustainability Reports Since 2005

Longest history of sustainability reporting in the Russian O&G

✔ Energy Affordability ✔ Energy Security ✔ Energy Sustainability

28Commitment to Developing Sustainable Value

NOVATEK is ranked among top ESG companies FTSE Russell Ratings confirms that NOVATEK

by Thomson Reuters ESG Scores in Russia remains a constituent of the

across all industries FTSE4Good Emerging Index in 2019

Rating

3.4/5

NOVATEK maintained Average Performer NOVATEK is assigned BBB rating

by Sustainalytics in 2019 by MSCI in 2019 - 6 consecutive years

Average Rating

Performer

BBB

64

NOVATEK is among top contributors consistently included in the

MSCI Emerging Markets ESG Leaders Index since inception in 2013*

*MSCI ESG Research, Feb 2020

✔ Energy Affordability ✔ Energy Security ✔ Energy Sustainability

29Dividends: Sharing Our Success

DIVIDEND PAYOUT(1), (RR per ordinary share)

Absolute growth: 36x 32.33

CAGR: 29%

26.06 18.10

2H

14.95

13.90 14.23

13.50

1H

10.30

7.89

6.86

6.00

4.00

1.65 2.35 2.52 2.75

0.9

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Committed to increasing shareholder returns

(1) Dividend payout is adjusted for non-recurring items and items not related to core activities

✔ Energy Affordability ✔ Energy Security ✔ Energy Sustainability 30Disclaimer – Forward Looking Statement

Matters discussed in this presentation may constitute forward-looking statements. Forward-looking statements include statements concerning plans, objectives, goals, strategies, future

events or performance, and underlying assumptions and other statements, which are other than statements of historical facts. The words "believe," "expect," "anticipate," "intends,"

"estimate," "forecast," "project," "will," "may," "should" and similar expressions identify forward-looking statements. Forward-looking statements include statements regarding: strategies,

outlook and growth prospects; future plans and potential for future growth; liquidity, capital resources and capital expenditures; growth in demand for our products; economic outlook and

industry trends; developments of our markets; the impact of regulatory initiatives; and the strength of our competitors.

The forward-looking statements in this presentation are based upon various assumptions, many of which are based, in turn, upon further assumptions, including without limitation,

management's examination of historical operating trends, data contained in our records and other data available from third parties. Although we believe that these assumptions were

reasonable when made, these assumptions are inherently subject to significant uncertainties and contingencies which are difficult or impossible to predict and are beyond our control and

we may not achieve or accomplish these expectations, beliefs or projections. In addition, important factors that, in our view, could cause actual results to differ materially from those

discussed in the forward-looking statements include:

changes in the balance of oil and gas supply and demand in Russia, Europe, and Asia;

the effects of domestic and international oil and gas price volatility and changes in regulatory conditions, including prices and taxes;

the effects of competition in the domestic and export oil and gas markets;

our ability to successfully implement any of our business strategies;

the impact of our expansion on our revenue potential, cost basis and margins;

our ability to produce target volumes in the event, among other factors, of restrictions on the Company access to transportation infrastructure;

the effects of changes to our capital expenditure projections on the growth of our production;

inherent uncertainties in interpreting geophysical data;

commercial negotiations regarding oil and gas sales contracts;

changes to project schedules and estimated completion dates;

potentially lower production levels in the future than currently estimated by our management and/or independent petroleum reservoir engineers;

our ability to service our existing indebtedness;

our ability to fund our future operations and capital needs through borrowing or otherwise;

our success in identifying and managing risks to our businesses;

our ability to obtain necessary regulatory approvals for our businesses;

the effects of changes to the Russian legal framework concerning currently held and any newly acquired oil and gas production licenses;

changes in political, social, legal or economic conditions in Russia and the CIS;

the effects of, and changes in, the policies of the government of the Russian Federation, including the President and his administration, the Prime Minister, the Cabinet and the

Prosecutor General and his office;

the effects of international political events, including changes in the foreign countries’ and their governments’ policy towards the Russian Federation and Russian companies;

the effects of technological changes;

the effects of changes in accounting standards or practices; and

inflation, interest rate and exchange rate fluctuations.

This list of important factors is not exhaustive. When relying on forward-looking statements, you should carefully consider the foregoing factors and other uncertainties and events,

especially in light of the political, economic, social and legal environment in which we operate. Such forward-looking statements speak only as of the date on which they are made.

Accordingly, we do not undertake any obligation to update or revise any of them, whether as a result of new information, future events or otherwise.

We do not make any representation, warranty or prediction that the results anticipated by such forward-looking statements will be achieved, and such forward-looking statements represent,

in each case, only one of many possible scenarios and should not be viewed as the most likely or standard scenario.

The information and opinions contained in this document are provided as at the date of this review and are subject to change without notice. In order to avoid inconsistency, any person who

made themselves acquainted with any information provided in this presentation shall rely on their own analysis of factors and figures that may be related to or may be linked with the facts,

phenomena or events described, and shall be guided by their own conclusions when making any decisions, including whether any investments are justified or not. By participating in this

presentation or by accepting any copy of this document, you agree to be bound by the foregoing limitations.You can also read