Vegetable Spotlight - Broccoli - Snapshot

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Vegetable Spotlight – Broccoli

Snapshot

• Broccoli is Australia’s 10thth most valuable vegetable crop, accounting for 2.9% of total

vegetable production with a gross value of $87.6m in 2006/07

•The level of production and yields recorded in financial year 2006/07 are significantly

lower than in recent years

• The total area planted was in line with previous levels

• Victoria and Queensland dominate Australian production

• Australia runs a positive but shrinking balance of trade in broccoli

• Strong competition from China is eroding Australia’s share of exports amongst Asian

economies

• Partially offsetting this development is the fact that new markets in the Middle East are

being developed

To ensure the accuracy of its figures, the Australian Bureau of Statistics employed a new methodology in collecting records for the 2005/06 Agricultural Census. The aim was to account for a greater proportion of establishments within the scope of the survey. As a result, the data generated since the census – such as production volumes, area planted and yields – are not directly comparable to historical statistics. Readers should use this material with caution. Current Australian Broccoli Production • Australian broccoli production totalled 40,032 tonnes in 2007, down 8.7% • The area planted to broccoli was 7,136 hectares, up 11.4% • The average yield per hectare over the year was 6.5 tonnes, down 18.1% Long Term Production Trends • The key measurements of broccoli production all displayed growth over the last decade, however there has been a recent fall-off in production • The 2007 figures remain broadly consistent with the long term movements

State Broccoli Production

• Victoria (53%) and Queensland (20%) produce over

70% of the national broccoli crop

• Yields are fairly even across most states, with only

WA significantly outperforming the national average

• Production levels in Victoria and WA are the most

volatile, accounting for most of the variation in national

output in recent years

Broccoli Consumption

• Data on consumption is fragmented and anecdotal.

Vegetable Average for 3 Average for 3

years ending years ending

• AUSVEG Ltd estimates suggest that consumption

1999(kg) 2006(kg ) of broccoli per capita has been rising in recent years

to 2.4 kg.

Broccoli 1.7 2.4 • Comparisons with estimates of per capita

Potatoes 68.0 61.9

consumption of some other major vegetables are

presented in the table to the left.

Carrots 11.1 11.5

•Broccoli growers have been at the forefront of

Tomatoes 22.0 24.2 innovation with new varieties. A new variety launched

in 2008 is expected to boost consumption further.Characteristics of Australian Broccoli Trade • Australia runs a strong but contracting balance of trade in broccoli. • Exports are exclusively fresh with markets developed in local regions such as Singapore and Malaysia, however trade with the United Arab Emirates has become increasingly important • A very small quantity of fresh broccoli was imported from 2007/08, mostly sourced from New Zealand • Due to the labour intensive nature of production, low cost countries, in particular China are now beginning to dominate the export market

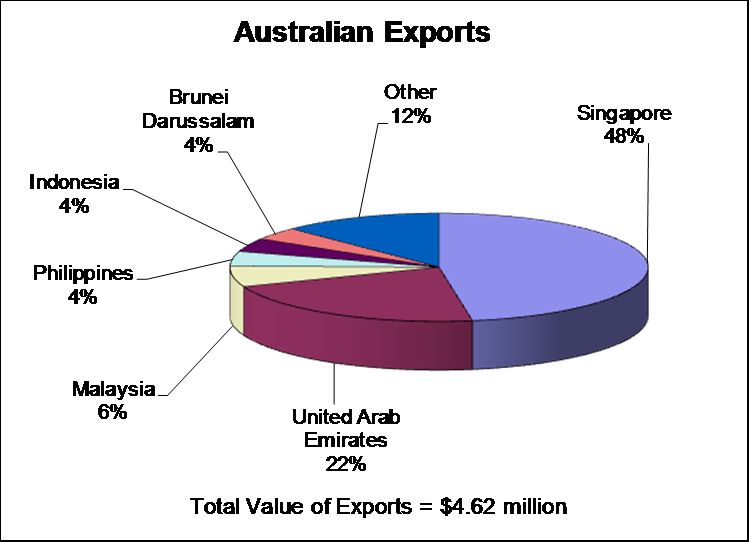

Current Trade Data

Exports

• Export values have fallen dramatically over the last 5

years, with the value dropping from $15m in the

2002/03 financial year to $4.6m in the 2007/08

financial year. This represents a 19% reduction each

year on a compounded basis.

• This fall reflects the increasing dominance of Chinese

agricultural imports which lead to both Singapore and

Malaysia cutting back on Australian exports from

$5.7m and $2.7m respectively in 2002/03 to $2.2m

and $0.8m respectively in 2007/08.

• In contrast new markets have been opened up in the

Middle East, with the United Arab Emirates increasing

exports by 111% over the period, which equates to a

compounded growth rate of 16% p.a.

•Exports of fresh broccoli over the last financial year

totaled $4.6m with Singapore, the UAE and Malaysia

the primary export markets.

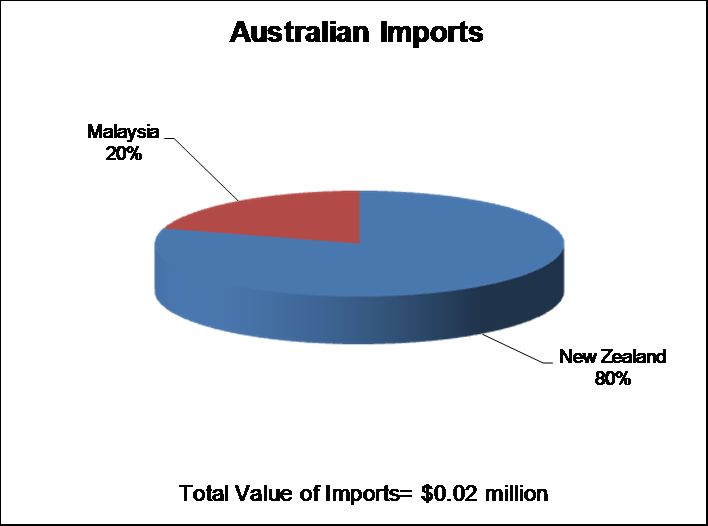

Imports

• Imports of fresh cauliflower and broccoli are minimal

(import data is not segregated) and totaled less than

$20,000 in the 07/08.Market Segments

• The broccoli market consists of the fresh market segment and the processed segment (which is

predominantly composed of freezing)

• There are a wide range of broccoli varieties such as calabrese, sprouting and romanesco.

• Despite the different varieties of broccoli available, most stores only stock the calabrese

variety.

Market Access

• Domestic markets are free and there are no restrictions on broccoli production.

• Imports of fresh broccoli are free to enter Australia whilst a 5% tariff applies on frozen

broccoli (4% for developing nations)

• Access to foreign markets is reasonable with freight costs being the major barrier to

expanded exports.

• Exports to Singapore and Malaysia do not incur a tariff.

• The only significant tariffs in place in the region are in Taiwan, the Philippines and Korea

with tariffs of 27%, 25% and 20% respectively.For more economic analysis of vegetable production, visit the

AUSVEG webpage at:

www.ausveg.com.au

Professional advice is recommended for all strategic and

financial decisions. This document does not represent

professional advice.

AUSVEG and the author do not accept liability for any damage

or loss suffered due to use of information contained in this

document.

© AUSVEG

Suite 9/756 Blackburn Road, Phone: 03 9544 8098

Clayton North, Victoria 3168 Fax: 03 9558 6199You can also read