Winners Supplement 2020 - Sponsored by: FinTech Futures

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Winners

Supplement 2020

Sponsored by:

Visit paytechawards.com to start your entry today

ENTRY DEADLINE: 31 March 2021

The categories open for entries are:

Welcome to the Banking Tech Awards The virtual event saw hundreds of

PayTech Project Awards 2020 supplement! people tuning in from across the globe

Best Consumer Cards Initiative Best Contribution to Economic Mobility in Payments Here, we showcase some of the and was a testament that it can be

Best Corporate Cards Initiative Best Benefits/Loyalty Initiative winners of our flagship Banking Tech entertaining, light-hearted and fun

Best Consumer Payments Initiative Best Use of Biometrics in Payments Awards (now in their 22nd year!) even in a digital environment. If you’d

Best Corporate Payments Initiative Best Prepaid Initiative – commending the most impactful, like to see Tom perform his stand-up

Best SME Payments Initiative Best UX/CX in Payments Initiative innovative and successful projects, and unveil the winners and highly

Best E-commerce Initiative PayTech of the Future commended, check out the video (and

products and services in the financial

Best PayTech Partnership Best Green Initiative it’s just 35min long) – the broadcast is

Best Mobile Payments for Consumer Initiative PayTech for Good services technology space in 2020.

free to view on demand here.

Best Mobile Payments for Business Initiative COVID-19 Response Banking Tech Awards also put in

Best Use of Security/Anti-Fraud Solution in Payments the spotlight the individuals and We would like to thank everyone

teams who have demonstrated who tuned in, and you, our readers, as

skills, leadership, vision, inspiration well as the Awards’ judges, sponsors

Excellence in Tech Awards Leadership Awards and partners, and the FinTech Futures

Best Open Banking Solution Woman in PayTech and dedication to the industry’s

betterment. team for their hard work in putting it

Best Real-Time Payments Solution PayTech Leadership

Best Cross-Border Payments Solution Rising PayTech Star all together.

The 2020 awards ceremony was

Best Smart Payments Solution PayTech Team of the Year broadcast digitally and hosted by a We hope to see you at the 2021

(Smart tech = AI/ML/Robotics/Big Data/etc.) Diversity & Inclusion Excellence stand-up comedian Tom Ward, with Banking Tech Awards in December…

Best Cloud Payments Solution

hundreds of attendees joining us to and maybe this time even in a long-

celebrate businesses and individuals awaited physical environment, to

who have shined in a very difficult enjoy the face-to-face networking and

year. celebration!

The FinTech Futures and

Banking Tech Awards team

SPONSORSHIP OPPORTUNITIES: EDITORIAL

Managing Director & Editor-in-Chief

SALES

Head of Sales

Marketing Executive

Kiran Sandhu

ADDRESS

Fintech Futures

kiran.sandhu@fintechfutures.com

Tanya Andreasyan Jon Robson 240 Blackfriars Road

tanya.andreasyan@fintechfutures.com +44 208 052 0423 London SE1 8BF

Jon Robson Sam Hutton jon.robson@fintechfutures.com

Editor

Head of Sales Business Development Executive Sharon Kimathi Business Development Executive

Email: jon.robson@fintechfutures.com Email: sam.hutton@fintechfutures.com sharon.kimathi@fintechfutures.com Sam Hutton

+44 208 052 0434 © Banking Tech Awards Winners

Tel: +44 (0)20 8052 0423 Tel: +44 (0)20 8052 0434 Deputy Editor

Alex Hamilton

sam.hutton@fintechfutures.com Supplement 2021

All rights reserved; Banking Tech

alex.hamilton@fintechfutures.com MARKETING

Awards Winners Supplement material

Reporter Marketing Manager may not be reproduced in any form

Ruby Hinchliffe David Taylor without the written permission of the

ruby.hinchliffe@fintechfutures.com david.taylor@fintechfutures.com publisher.

FINTECH The BankingTech Awards 2020 | 03

paytechawards.com | #paytechawards FUTURES

Strands Best Open Banking

Solution 2020

Open Hub

Winners & Highly Commended

9 41

One Platform, Multiple 1

ACCO U N T S

Data Sources Ex. Chase, Citibank

BankingTech Project Awards

Strands Open Hub offers

banks a single interface from

Best Tech Overhaul

Winner: which to connect to external

Bank of America - Branch Transformation services in an easy and secure

Highly Commended: way.

Absa Group Limited - Technology Separation Programme

DBS Bank - DBS Hong Kong Core Banking Project

Best Use of IT in Retail Banking

Winner: HIGH COVERAGE. Strands plugs into a wide variety DATA ENHANCEMENT. Aggregated data goes

Sberbank - P2P Subscriptions of data providers and constantly expands to more through a complex standardization process. It is then

banks, financial institutions and countries. categorized before it reaches the bank and the

Highly Commended: end-user, for ease of use.

SINGLE INTERFACE. A single interface allowing

Emirates NBD Liv. Digital Bank - Liv. Digital Bank

access to third-party services. Banks benefit from a SECURE. Your application will never store usernames,

Novo Banco - New Digital Onboarding Experience

single API platform which greatly reduces cost and passwords or security details. All data used is

complexity. encrypted for maximum security.

Best Use of IT in Corporate Banking

Winner: READY FOR OPEN BANKING & PSD2. A single MONITORING. The most comprehensive monitoring

Barclays - Trade OCR Solution interface which allows access to any bank through & analytics platform, to ensure clients have a complete

UK Open Banking and PSD2 legislation. understanding of the API’s performance.

Highly Commended:

Bank of the West BNP Paribas - Digital Channels and Enterprise Payments Hub

Best Use of IT in Private Banking/Wealth Management WHY DO BANKS CHOOSE STRANDS?

Winner:

BTB connecting loans in Israel - B-match. Innovation Experience Security

Continuous design and AI, Big Data, Machine ISO 27001 Certification

Highly Commended: creation of new disruptive Learning & UX/UI audited by AENOR

Bambu (Mangosteen BCC Pte Ltd) - Beanstox solutions

Best Use of IT in Treasury and Capital Markets

Winner:

HSBC - MyDeal

4 | The BankingTech Awards 2020 Visit strands.com/request-demo

FINTECH PODCAST

FUTURES

What the

Fintech?

Season 2 Best Use of IT for Lending

Winner:

Bank BRI - BRI Ceria

Highly Commended:

Divido - Powered by Divido

Best Digital Initiative

Tune-in for:

Winner:

DBS Bank - Enabling “invisible banking” through Open APIs on DBS Marketplaces

Trending topics Highly Commended:

In-depth insights Novo Banco - Small Business Finance - Digital Experience

U.S. Bank - Onboarding Tracker

Banished buzzwords Bank of America - Erica AI-Driven Virtual Assistant

Best Mobile Initiative

Winner:

Yolt - Yolt App

Recent episodes cover:

Highly Commended:

Innovation in commercial lending

Bank ABC - ila Bank - Revolutionizing banking across MENA

Back office processing for real-time payments BANCO DE CRÉDITO - YAPE

JPMorgan Chase - Consumer & Community Banking (Chase) - Snapshot

Best Use of AI

Winner:

au Jibun Bank Corporation - AI Japan Market Forecast

Highly Commended:

Bank ABC - ‘Fatema’ - the world’s first AI-powered digital employee with Digital DNA™

Bank of Montreal - BMO AI Cashflow Prediction

Search for ‘FinTech Futures’

Best Use of RegTech

to find us on your favourite podcast streaming service. Winner:

Morgan Stanley - Fundamental Review of the Trading Book (FRTB)

Highly Commended:

Discover Home Loans - Improving efficiency of mortgage regulatory

Listen on compliance through automation

SOUNDCLOUD

The BankingTech Awards 2020 | 7

Best Use of Data

Winner: TCS BaNCS

HSBC - Global Social Networks Analysis (GSNA)

Global Banking

Highly Commended:

Scotiabank - Enhancing the customer digital experience during COVID-19

Volvo Financial Services - Leveraging telematics data for a better customer experience

Platform

Creating Trusted Digital Relationships

Best Use of Fraud Protection Technology

Winner:

Signicat and SurePay - Signicat’s Digital Identity Verification with SurePay Confirmation

of Payee (CoP)

Highly Commended:

CaixaBank S.A. - CaixaBank Sign

Checkprint Limited, A Member of the TALL Group of Companies - UCN Plus® - An Image

Survivable Feature

Best Use of Biometrics

Winner:

Keyless Technologies - Keyless Zero-Knowledge Biometrics

Highly Commended:

Behavox - Behavox Voice Biometrics

Uncertain times beget innovation. Banking is no different. With the right tools and

DBS Bank - DBS Palm Vein Technology Enabled Payments technology, banks the world over are laying the foundation for transforming social

distance into elevated customer management and experiences while bringing in

Best Use of Cloud resilient ways of navigating financial uncertainty.

Winner:

Creating more cohesive and personal digital journeys that engender trust. That’s

UBS - UBS My Hub External

what the TCS BaNCS Global Banking Platform is all about.

Highly Commended: A contemporary digital banking solution with a global footprint, it leverages a rich

Saxo Bank - Saxo’s migration to the Cloud. ecosystem of partners and FinTechs, actionable data insights, cognitive tools and

HSBC - Markets Grid

APIs, to help your bank launch new products and even new business models, acting as

a platform for collaboration. It can help you dynamically define and create digital

Best FinTech Partnership

Winner:

products and services that are contextually right for your customers, while also

ClearBank and Tide - ClearBank Tide Business Banking increasing revenue opportunities for your bank. The solution’s cloud native

architecture and microservices based approach paired with agile methodology, can

Highly Commended: help you scale, innovate and create the experience your customers expect today.

Caixa Geral de Depósitos - Dabox App - an open banking solution

SEB - SEBx/UNQUO & THOUGHT MACHINE

Verrency Talk to us to know more. Write to Visit our website:

tcs.bancs@tcs.com https://www.tcs.com/bancs

8 | The BankingTech Awards 2020

FinTech of the Future

Winner:

FINOS - Open Source Technology

Highly Commended:

Marqeta - Marqeta’s open API issuing and processing platform

Best UX/CX in Finance Initiative

Winner:

United Overseas Bank (UOB) - TMRW by UOB

Highly Commended:

Sberbank

Tinkoff - Tinkoff super-app

Best Green Initiative

Winner:

Mastercard - Mastercard Sustainable Cards Program

Highly Commended:

Enfuce - My Carbon Action

Best Contribution to Economic Mobility in Banking/Finance

Winner:

BPC - Safal Fasal

Highly Commended:

Banque Populaire De Mauritanie (BPM) and Comviva - Bankily

Cebuana Lhuillier Rural Bank - Cebuana Lhuillier Rural Bank: Revolutionizing the Concept

of Saving Money for Every Filipino through Cebuana Lhuillier Micro Savings

FinTech for Good

Winner:

Absa Group Limited - Absa Cybersecurity Academy

Highly Commended:

Affirm - Affrim Cares Employee Foundation

COVID-19 Response by Financial Institutions

Winner:

Starling Bank - Connected card

Highly Commended:

CaixaBank S.A. - Embracing the new normal

Israel Discount Bank - PayBox Payments App: Doing good in days of Corona - “How Social

Payments Can Triumph Social Distance”

10 | The BankingTech Awards 2020

Leadership Awards

Woman in Technology (W.I.T.)

Winner:

Kate Bohn, Accelerator & Incubator Lead, Innovation & Strategy, Lloyds Banking Group

Highly Commended:

Julie Shapiro, Head of Finance, Risk and Analytics Services Technology, UBS

Mitra Roknabadi, Vice President, Global Head of Marketing, OpenFin

Vilve Vene, Co-Founder and CEO of Modularbank, Modularbank

Tech Leadership

Winner:

Jaya Vaidhyanathan, CEO, BCT Digital

Highly Commended:

Gabriele Columbro, Executive Director, FINOS

Nadia Hartman, Vice President, Morgan Stanley

Rising FinTech Star

Winner:

Alexandra Boyle, Director, Head of Strategic Client Group in Europe, OpenFin

Highly Commended:

Sunil Ravva, Portfolio Architect, HSBC India

Tech Team of the Year

Winner:

J.P. Morgan Asset Management, Spectrum Core Team

Highly Commended:

Charles Schwab Investment Management, Investments Technology

Diversity & Inclusion Excellence

Winner:

Sberbank - Online banking for visually impaired entrepreneurs

Highly Commended:

HSBC Technology India - HSBC Technology India: Inclusion and Diversity Workstream

J.P. Morgan Asset & Wealth Management - Societal Tech Matters Hackathon

The BankingTech Awards 2020 | 13

Excellence in Tech Awards

THANK YOU!

Best Core Banking Solution Provider

Winner:

INFOPRO - INFOPRO Digital Core Banking

Highly Commended:

DPR Group - Core banking platform – Servicing and origination for mortgages,

INVESTORS

savings and loans

MANTL - Midwest BankCentre (Rising Bank)

BUSINESSES

Best Digital Banking Solution Provider

Winner:

Moxtra - Moxtra’s Digital Branch Solution

BANKING

Highly Commended:

FintechOS Technology UK Ltd - Retail&SME digital banking TECH AWARDS

Galileo Financial Technologies - Galileo Instant Issuing

Best Smart Banking Tech Solution

Winner:

Mosaic Smart Data - MSX and MSX360

Highly Commended:

ABAKA - Predictive Next Best Actions

Bank of America - Erica AI-Driven Virtual Financial Assistant

NEC X and VACO - A cognitive application, using AI and ML technology to meet compliance

and regulatory requirements for personal identifiable information (PII) Data Redaction

Best Open Banking Solution

Winner:

Strands - SAU, Open Hub

Thanks to the BANKING TECH AWARDS judges who chose

BTB technology in first place in the category of Best Use of

Highly Commended: IT in Private Banking / Wealth Management

Finicity - Finicity Lend: Open Banking Platform for Credit Decisioning

Infosys Finacle - Finacle Digital Banking Suite

COVID-19 Response by Fintechs

Winner:

Automated Financial Systems, Inc. (AFS) - Mass Update Tool for PPP Loans

Our technology is proving itself in protecting our

investors' money every day - and it is gratifying to see

Highly Commended: that our hard work has also gained international

BillGO - BillGO’s Bill Pay Relief Hub

Pollinate - Pollinate Orders launched for hard hit dining sector

14 | The BankingTech Awards 2020

Winner | Best Digital Banking Solution Provider

Winner | Best Digital Banking Solution Provider

Moxtra: Enabling digital

customer experience in

financial services and beyond

Moxtra, a Cupertino-based technology company, has

grown rapidly in financial services and subsequently says. The company describes

in other vertical sectors with its platform for delivering the resultant offering as a

customer service via secure digital channels. platform powering one-stop

customer portals, with a UI/

UX and Workflow layer that

supports conversational

Cupertino, CA-based Moxtra Branding Officer, Leena Iyar, user experiences, tailored to

has grown rapidly by helping says that as a result of the business roles and workflows.

businesses to deliver secure, pandemic, existing business It supports secure

high-touch digital channels to conversations have tended messaging; digital signatures;

their customers. It started with to accelerate and projects transaction processing; video

large enterprises and financial that might have had a two-to- meetings; virtual data rooms;

services and has an extensive three year timeline have been the ability to make visual,

global customer base in the brought forward. vocal, and video annotations

latter sector. The platform’s Moxtra was set up in 2012. on shared files; task

core capabilities of translation Co-founder and CEO, Subrah management; screen-sharing; with its existing enterprise managers in an immersive

of business over digital proved Iyar, was co-founder and CEO cloud storage; and support for systems. environment, maintaining a

to be transferable and it now of WebEx Communications social connectors including A Management Portal continuous overview of the

has users across a wide range until its 2007 acquisition by WhatsApp and WeChat. provides a comprehensive health of their portfolios.

of verticals, including retail, Cisco Systems. Fellow Moxtra Users maintain visibility on overview of all client- There’s now plenty of

real estate, law, education, co-founder and CTO, Stanley all communications and relationship manager additional demand, not least

creative, and event planning Huang, was a senior director it supports cross-border interactions and ensures as banks seek to react to

firms. of engineering at both WebEx regulatory requirements and quality responsiveness fintechs and challenger banks

After early success at and Cisco. The company has geo-specific standards such from internal teams and by increasingly seeking to

Citibank for private banking, been largely self-funded and as MiFID II, GDPR and PSD2. performance to business embed their services into

the company gained good now has around 220 staff There is a white-label goals. It stores a complete their customers’ lifestyles.

traction in this sector, initially across offices in London, New version, says Leena Iyar, that client profile and history “We are seeing a lot of

particularly in Asia Pacific. York, Amsterdam, Sydney, can be rapidly deployed on of conversations, ensuring interest in providing seamless,

Since then, it has broadened Bengaluru, Shanghai and an app store. An example of a persistent relationships and convenient digital journeys

into other areas of financial Singapore. bank that took this approach a smooth transition to any for the customer, banks are

services, including corporate Moxtra started with a free is Bank of Queensland for its relationship manager. paying a lot of attention to it,”

banking, lending, mortgages app but then went “back to Pocket Banker by BOQ app, Among high-profile financial says Leena Iyar.

and insurance, as well as a build out our platform”, says which allows users to connect services clients in the Moxtra was founded around

number of other verticals. In Leena Iyar. It was clear the and chat securely with their public domain are Bank of delivering a new generation

total, it claims almost 500 need for businesses to own BOQ banker at a time and Singapore, OCBC, Raiffeisen of collaboration experiences

customers. the customer experience by place of their choosing. Other Bank International, Standard built for the mobile-first digital

The events of the last year providing their customers with deployments might take Chartered and Van Lanschot. age – a topical area that has

or so have further pushed their own secure, managed longer, she says, depending At Citibank, Moxtra powers Citi only become more pressing

companies to examine their and branded portal that on the extent to which a bank Hello, through which clients within many institutions as this

digital strategy. Moxtra’s Chief ensured data privacy, she wants to integrate workflows can interact with relationship sector evolves so rapidly.

The BankingTech Awards 2020 | 17

Winner | Rising FinTech Star Winner | Rising FinTech Star

Rising FinTech Star:

Alexandra Boyle, OpenFin

Alexandra Boyle, director, head of strategic client group in

Europe at OpenFin and winner of the Fintech Rising Star

award, talks digital transformation in financial trading,

being the youngest person in the room at meetings and the

importance of open technology standards.

You were one of the first ten My formal education was in We grow initial projects into

employees to join OpenFin in finance, not computer science. enterprise-wide strategies, hard? Is the financial services transformation in financial

2014. How has the financial I approached the industry which has made OpenFin industry’s senior management services. Remote work has

desktop technology changed from a business perspective, a foundational layer across becoming more diverse and been a major driver. Apps

since then? starting as an analyst before financial markets OpenfFin is reflective of society? must be able to interoperate

moving into a sales/business now used to deploy over 1,200 It can be difficult. Providing to streamline workflows and

There has also been an

development role at NYSE applications across 275,000 value, as a subject matter compensate for the physical

incredible amount of progress

Euronext. Now I head strategic desktops at 1,500 institutions. expert or making sure the limitations of this new normal.

around digital transformation

as the industry becomes client relationships for Europe. I’m also passionate about right resources are in the What trends do you think will

more educated and coalesces I’ve made it a priority to smaller fintech providers. I room, is key. I’ve definitely dominate 2021 in financial

around ideas such as common invest in myself in becoming dedicate a lot of time to helping made a mental note of some desktop technology?

standards and open source. a subject matter expert in these new players break into of the more diverse senior There will be a sustained push

The needs of our clients web technology. Having deep the industry by helping to management teams I’ve worked for functionalities that help

have changed. We still work knowledge of web, trading coordinate working groups with with over the years. There end users navigate a remote

with many firms that are just architectures and market heads of technology from global is a high positive correlation work environment, such as

getting started on their digital structure has always been banks and facilitating cross- between the most innovative interoperable applications and

transformation journey. Others crucial to my work in interfacing bank collaboration on shared players and diversity. robust notification centers.

are farther along in the process. with clients, and that has technical challenges. One result OpenFin is strongly committed We’ll see a continued focus on

Ultimately, though, our mission continued at OpenFin. from these efforts has been to diverstiy and inclusion employee productivity. That will

has remained the same. The What do you do at OpenFin? FDC3, an OpenFin-founded and we collaborate to this mean an increased emphasis

financial services industry is What do you most enjoy organisation that promotes end where we can. I believe on building more intelligent,

sacrificing efficiency and user about your job? open standards for the financial that the financial services contextual workflows to

experience due to outmoded desktop. industry’s senior management empower the end user with the

I head OpenFin’s strategic

approaches to technology, and The best thing about my job is becoming more diverse, and right tools to quickly access

client group in Europe. Much

we want to help them prepare is meeting talented, diverse that it will continue to do so. information in times of high

of my role is engaging with the

for the digital future. global banks, asset managers individuals from all corners Has the Covid-19 pandemic stress.

You started working in fintech and technology vendors of the industry and helping accelerated digital Growth in industry standards

without any formal education on their digital journeys, to solve complex problems transformation among and open-source technology

in computer science or understanding their needs and through technology. financial services, including will continue. Outmoded

technology. Has it been hard leading industry initiatives. Our You’re often the youngest desktop technologies and approaches to technology are

to get a deep understanding customers include Barclays, person in the room with remote working? a collective problem, not just

of the technology and BNP, Standard Chartered, C-suite executives and the The pandemic has an individual one, and firms will

industry trends? HSBC, BidFX, Liquidnet. only woman? Has that been greatly accelerated digital take steps to combat it.

18 | The BankingTech Awards 2020 The BankingTech Awards 2020 | 19Winner | Best Use of IT for Lending

BANKING

Revamping customer lending TRANSFORMATION

through partnerships and STORIES FROM

ACROSS THE

back-office change GLOBE

As the acceleration brought about by the

COVID-19 pandemic continues, banks across

the industry are undergoing a revamp of the

way they deal with customers, particularly Featuring

when it comes to lending. Leaders from

Rajashekara V. Maiya, vice layers of the technology ANZ Bank, Bancolombia,

president and global head landscape through which Infosys Bank of America, Bank of the West,

of business consulting at assists clients like BRI. These big thing, says Maiya. Barclays, BDO, Discover, HSBC,

Infosys Finacle, says banks are are the back-office business “They cannot just depend on Emirates NBD, Fifth Third Bank,

undertaking a great rematching engine and the system of record; a traditional lending, borrowing

of the journeys their customers a middle layer focused on digital Goldman Sachs, HDFC, ICICI, ING,

and payments business and

must take. engagement; and a final layer expect to be a leader in the Jio Payments Bank, Kotak Bank,

“You can no longer expect based on digital experience. industry. Everybody has gone Llyods Bank, Santander,

your customers to come into the Each of these layers is into a platform business, Standard Chartered, Swedbank,

branch and stand in a queue,” independent of one another, and that brings with it the

says Maiya. “They don’t see enabling the vendor to target Westpac, Wells Fargo

marketplace opportunity for

that as the basic level of service the specific needs of a client. banks to become an ideas and more

anymore.” “Say a bank has already export business.”

So, what can banks do? implemented a new core That platform marketplace

Maiya says they must look banking system,” says Maiya, model is what Maiya calls

at partnerships to provide a “but they now want to go digital “the pinnacle of digital

reinvention of their lending for customer experience. engagement” and something

systems in the short term, “We can offer that layer, but that Infosys brings to the

while working on technological further, we can separate out table. The importance of open Starting January 27th

change in the interim. That their needs on that layer. Do banking ecosystems cannot be

change must occur eventually, they want a mobile app, online overstated, he adds. Join from anywhere.

he says, which is where a good banking, or WhatsApp banking? Infosys Finacle has created its

technology partner can help. We can enable any combination own marketplace, available via

Join from any device.

Infosys Finacle worked with of those.” its platform, which offers access

Bank Rakyat Indonesia (BRI) to The use of multiple channels to more than 50 fintech services.

launch Ceria, a new digital credit across for lending has become On top of that, it enables

card designed to appeal to the new standard, says Maiya, banking clients to link into non-

millennials. The project followed and is something that banks up financial gateways, like booking

100+ 45+ 5 2

existing work with the bank and down the tier system are flights or ordering tickets at the

on its development of micro- looking at. cinema.

lending service Pinang. “Slowly banks have moved Maiya uses India as another

Ceria allows Indonesian towards offering the same example of the changing SPEAKERS SESSIONS DAYS TIME ZONES

users to build their credit service across multiple channels. dynamic of the marketplace.

history through the card, and The new challenge is offering More than 80% of banking

has integrations with local that same service not just transactions in the country

e-marketplaces Tokopedia across existing channels, but are anchored by non-banking

Dinomarket, and Panorama. BRI emerging ones as well.” entities. In that scenario, Maiya

claims that most new customers Banks must continually assess adds, “you cannot stay isolated

are approved within ten minutes. their business models to ensure and try to come out on top in Register today

Maiya says there are three they are prepared for the next banking”.

Scan the QR code

or write to

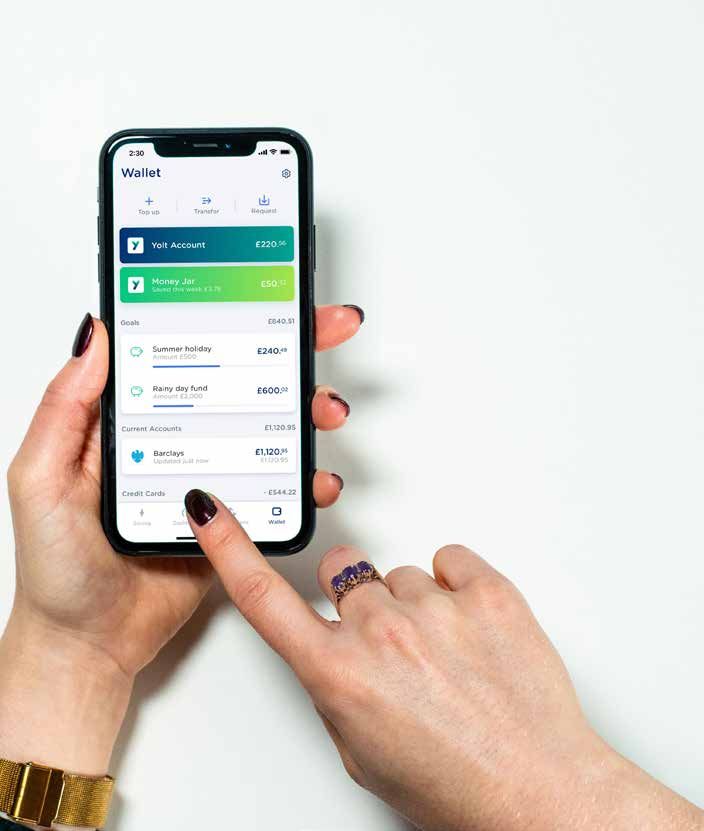

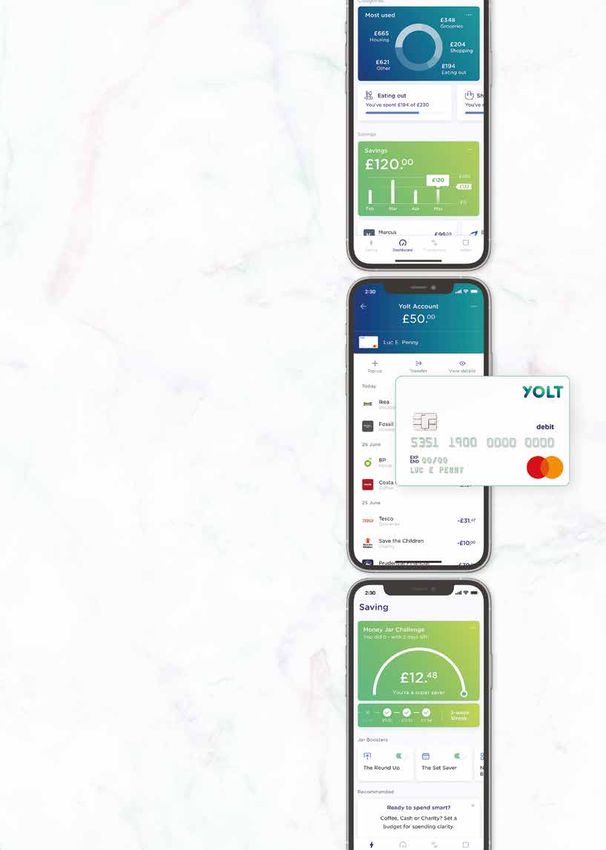

20 | The BankingTech Awards 2020 finacle.conclave@infosys.comWinner | Best Mobile Initiative Winner | Best Mobile Initiative

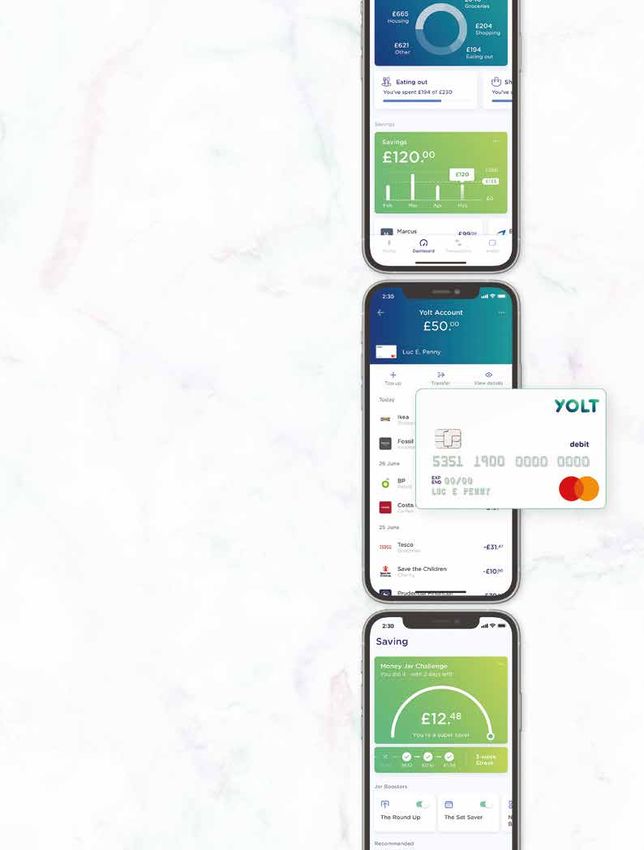

Nudge techniques, open

banking and smarter

personal finance:

Yolt’s new mobile app

Interview with Pauline van Brakel,

chief product officer at Yolt.

Congratulations on winning the search and switch to more

Best Mobile Initiative. Tell us competitive household bills. API and platform available

about your mobile app, what are In October last year, to leading financial

some of its main features? Yolt launched an updated institutions and ambitious better solutions to manage

Yolt is a money platform that version of the app. The app tech businesses as an open these pressures.

empowers people to be smart uses behavioral science banking technical service One of the new features

with their money. Since Yolt techniques to help users provider. This tied in well with in the new version of the

launched in 2017, it has harnessed spend smarter and save. the requirement from UK mobile app is a Yolt card,

the power of Open Banking to New features include an regulations for all European which is a contactless debit

deliver a better banking solution option to round up purchases banks to make an API Mastercard. It’s powered by

to customers by giving them a to the nearest pound, for available for open banking the Yolt app. It gets users into

totally transparent view of their example, and automatically connections from September the habit of saving, through

finances, in one central place. put the “extra” money into 2019. easy everyday steps with

Our app users can see balances a “money jar”. The money The market you’re in − round ups and cashback on

and transactions across multiple jar feature also offers handy money management, selected brands.

accounts, keep track of what tips and reminders for users app-based, is becoming The Yolt Card works

they’re really spending and watch to increase their savings. It’s increasingly competitive. alongside the virtual Money

out for upcoming bills. They can trained to recognise and save What features/technology Jar to help users get into the

set budgets and savings goals, refunds, salary raises and of your mobile app help it habit of saving.

pay friends and family, and even even bonuses. stand out? Yolt is a venture of ING

How important is the mobile The UK fintech sector bank. Has being owned

app to your business? is thriving. According to by a big bank helped Yolt

Yolt’s mobile app is hugely research last year by KPMG, grow its mobile app and

important to the business. the UK fintech sector business? Do you try to

We now have 1.6 million received $48 billion of combine the nimbleness of

registered users across the investment in 2019, over 80% a start-up with the stability

UK, France and Italy. Yolt is of Europe’s overall fintech of a corporate?

powered by our company’s funding. As a venture of ING, we

business-to-business (B2B) Yolt recognises that the have benefitted greatly from

arm – Yolt Technology pandemic crisis has created the business’ market know-

Services (YTS), an open many additional financial how, expertise and continued

banking provider in Europe. pressures for consumers and support. ING’s support has

In 2019, YTS made its therefore consumers need been integral to helping

22 || The

16 The BankingTech

BankingTech Awards

Awards 2020

2020 The BankingTech Awards 2020 | 23Winner | Best Mobile Initiative

grow the Yolt business to such as Amazon and Apple on the sharp increase in

what it is today, serving 1.6 offer has trickled into the consumers using online

million registered users in financial services sector. services.

just under four years. We can The post-Covid economy It’s not just money

balance this with the agility may also bring greater management tools

of a start-up as a relatively adoption of open banking consumers are turning to in

small organisation, with big services. Demand will come lockdown. UK consumers

ambitions across Europe. not only from consumers may feel more comfortable

What are the most looking for digital tools to help with online processes, such

important trends in mobile them manage their finance as mortgage applications,

apps in your market for in but also from businesses sharing account information,

2021 and beyond? who will be looking at how and executing transactions

Covid-19 has hugely to reduce business costs, digitally.

accelerated the expectation offer a seamless customer This could pave the way for

for financial services to be experience and a safe and a truly open financial system

completely digitalised, so the secure method of handling in the next few years, with

adoption of personal finance payment data. While any consumers and businesses

apps and online banking are investment during a period able to access their entire

likely to increase. Likewise, of economic uncertainty may financial footprint, from

the consumer expectation seem risky, those adopting mortgage applications to bills

for the same seamless open banking during this and smart meter readings, in

experience that tech giants time will be able to capitalise one place.

24 | The BankingTech Awards 2020Winner | Best Use of Cloud Winner | Best Use of Cloud

All together now

How UBS’s innovative hub helped

60,000 work remotely with virtually

no downtime during the pandemic experienced very little IT is secure and compliant with aspect of private and business

– interview with Nej Adamian, head downtime during remote working, regulations. lives was impacted – shopping,

of digital engineering, UBS Group meaning colleagues could spend Alongside the hub, we also chatting, banking. According to

Technology. more time on clients during the provided support and training for several surveys, the pandemic

pandemic. our employees to help them work has accelerated digitalisation by

The hub’s technology from home, including an app for three to four years. We expect

leverages several services mental health. this trend to continue and see a

Last year, 95% of your from home, it was during a time of

within Microsoft’s Azure Cloud What have been the main boost especially for automation

organisation started working high volumes and volatility in our

including: Azure Functions, Key benefits of My Hub External? and technological capability

from home, almost overnight, financial markets. Thanks to the

due to the Covid-19 pandemic. stability of our IT, we successfully Vault, SQL Database, WebApps (stability, cloud, remote working),

My Hub External is built for

What were the challenges of managed March’s high volumes and application insights. The hub digitalisation on the client side

remote working. The hub’s

doing this? and activity across our trading also uses proprietary technology and working from home after the

benefits include, being a

and client platforms enabling us developed in house by our UBS pandemic as more employees

Remote work was already an single page that gives users an

to gain market share and share of Digital Engineering team. will want to work partially and

integral part of UBS’s way of overview of their remote working

wallet with our clients in the first How did you adapt the My capabilities and health of their more flexible from home.

working before Covid-19 so we

had all processes and systems quarter of 2020. External Hub to support the personal devices based on UBS Do you plan to develop the hub

in place. When the pandemic What is UBS’s My Hub External. surge in remote working? standards and enabling users to over the coming year?

struck, past investments paid What tech does it use? Pre-Covid, the site was a self-service their IT and other As with any digital product,

off as we were on the last mile My Hub External is a website concept under development as needs. the tool is constantly being

to implement what we call we developed for our 70,000+ part of a suite of services. When Has the Covid-19 pandemic improved for performance

“A3” – anytime, anywhere, with employees who work all over it became clear that most of UBS accelerated digital transformation and design and is having new

any device. We accelerated the the world. Its purpose is to allow had to start working remotely, among financial services, features and capabilities added.

closure of implementation of A3 employees to access the tools we immediately accelerated the including desktop technologies As remote working appears

and provided a secure and fast they need while they are all development of the tool. and remote working? to be part of the “new normal”

infrastructure for remote working working remotely. For example, The speed of deployment was The pandemic has increased around the world, the tool will be

for over 95% of our staff via our if an employee is locked out of the biggest challenge. We were digital savviness in general. Every here to support our employees.

“My Hub External” website. their account because they’ve able to roll it out quickly by using

Working from home as a mass forgotten their password, the cloud technologies.

experience had of course a My Hub helps them reset their We worked to make sure that “The cloud is an essential part

substantial impact on our systems. account securely. They can do the tool was as simple to use of our strategy. Our work on My

For example, we have about this without having to call an IT as possible. We had to consider Hub is a perfect example – our

60,000 people working remotely helpdesk or needing access to the design of the service to meet

at the same time, making about bank’s secure network. massive spikes in demand during

ability to seamlessly pivot to

three million calls globally each The site also has diagnostic peak times – which the cloud is remote working helped UBS

week. Our systems remained tools which can detect whether perfect compared against on- colleagues focus on delivering

stable and resilient. We even saw an employee is having technical premise alternatives. As we built throughout the pandemic.”

record stability in some of those issues with their computer, such the product natively in the cloud,

months. as if software needs updating. we adopted our testing strategy Mike Dargan, group chief information

When we shifted to working The tools meant that we have accordingly – to ensure that it officer, UBS

26 | The BankingTech Awards 2020 The BankingTech Awards 2020 | 27Winner | Best Open Banking Solution Winner | Best Open Banking Solution

Strands: Opening up

banking and account

aggregation services managing third-party APIs and

offers a unique API that makes

have to open up and allow

the sharing of a customer’s

generate new opportunities

to accelerate the bank’s

dealing with each of them financial data, such as innovation efforts, enabling

Strands’ Open Hub was launched seamless spending habits and payments, its complete digital

Why did you build the hub? with authorised third-party transformation and using

in 2017. It’s used in more than ten providers. artificial intelligence to create

financial insti-tutions in the UK, Strands’ money

personalised and contextual

management solutions try Open Hub is a simple

Europe, Asia and Latin America. interface that leverages third- offering for their customers

to provide banks with a full

We talk with Claudio Cungi, head overview of their customers’ party connections, i.e. Open and bring new products and

of product at Strands. financial situation. For this Banking, to connect multiple business models to market,

reason, it is essential to external services securely such as a cloud version of its

connect the information of in one place. It helps banks personal finance software

Strands’ Open Hub was get additional information about information, such as financial the user that is held outside create new revenue streams or an integrated platform of

launched in 2017. It’s used invoices and bills through the transactions the customer has the bank. Maintaining external from the distribution of digital cash management

in more than ten financial business financial management in other bank accounts and connections is always a services over third parties. and commercial payment

institutions in the UK, Europe, (BFM) solution. This way, banks other financial information held challenge and an extra effort We partner with third tools specifically designed

Asia and Latin America. We talk get a more realistic picture of in accounting software used by that depends on a third party’s parties such as invoicing to benefit banks’ small-to-

with Claudio Cungi, head of the finances of their customers’ the customer, for example in roadmap more than your own. providers (Xero, Quickbooks), medium enterprise (SME)

product at Strands. businesses. Quickbooks or Xero. Oracle or Mastercard to customer base.

This is why we built an

Strand’s Open Hub platform We also provide bank feeds Open Hub can put customer interface that allows banks

“provides banks with a single services. Open Hub connects to transactions into different to connect their online

interface from which to connect the same invoice aggregation spending categories, such banking applications with

to external services in an easy services to facilitate the as groceries, home apparel, third parties but that remains

and secure way”. information about the bank restaurants etc, using Strand’s fully independent. This

What kind of services does accounts into these tools. AI-driven software. Each bank way, a change in the third

this include? In the UK, Strands’ AI- has its own categorisation party’s software or API

Connecting external services based BFM platform has been systems. Open Hub lets a bank’s won’t compromise in any

to their financial management authorised by HM Revenue customer with accounts in way its connection to the

platform allows banks to enrich & Customs to manage and more than one bank can see all banking platform. This makes

their 360-degree view of their submit digital tax returns in the their transactions categorised maintenance so much easier.

customers. UK on behalf of organisations. following a common style in a How does the technology

Open Hub acts as a meta- Banks can use our white-label single platform. These could use “open banking”

aggregator, by connecting to fintech software help UK small be recurring payments in a technology standards?

third-party account aggregation and medium-sized businesses separate business account or The continued effort behind

providers such as CRIF’s (SMBs) keep on top of their expenses on a shared account. Open Banking reform means

Account aggregation service, finances. Finally, Open Hub can that banks and financial

which act as Strands’ partners in How does Open Hub help integrate with all IT systems institutions, using APIs, will

different geographies. banks and their customers? and apps used by banks. It

We also provide account It gives banks and enhanced does this by using Application

invoice aggregation services. view of their customers Program Interfaces (APIs that

Open Hub connects to by taking into account meet international standards,

most widely used invoice both internal, such as their such as such as the OpenAPI

management tools, including customer’s bank account Specification (OAS). Open

Quickbooks, Xero and Sage, to transaction data, and external Hub eliminates the hassle of

28 | The BankingTech Awards 2020 The BankingTech Awards 2020 | 29Winner | Best UX/CX in Finance Initiative Winner | Best UX/CX in Finance Initiative

Tailor made: TMRW

– the digital bank

for ASEAN’s young

all banks’ ATMs in Thailand good savings behaviour the technologies in-house,

and Indonesia to withdraw and real-time expense leveraging UOB’s existing

cash for free. tracking – which just exited technology assets. We also

Our app includes a feed Beta and was designed partnered with fintechs,

professionals

of financial updates, advice to help customers curb including Personetics and

and information, in a = impulse spending. Meniga, to lower the cost

similar format to Facebook How long did the service of producing innovative

or Instagram. The feed is take to develop and when technologies and services.

a series of “cards” that was it launched? TMRW has been built on

Interview with Kevin Lam, head of TMRW Digital Group. give personalised financial We began working a modern microservices

updates to the customer, on the idea in 2017. We architecture which provides

Why did you design lifetime of a young ASEAN catered to their needs was such as a reminder to launched TMRW Thailand us the flexibility to adapt

a digital banking professional. the next logical next step. pay a credit card bill, the in March 2019 and in quickly and to scale the

service aimed at young customer’s spending in Indonesia in August platform. We integrate

Our target segment is What are some of the most

professionals? a month or an unusual 2020. Our learnings in rapidly using APIs with best-

young professionals and important and innovative

charge in the banking Thailand meant we were of-breed fintechs as well

The market for millennials young professional families features for the new

transactions. TMRW uses able to launch quicker in as our own in-house core

in Southeast Asia is in ASEAN. Based on our banking app?

technologies including Indonesia. In the long term, banking systems. TMRW

particularly important research, we found that TMRW is a digital, mobile- artificial intelligence (AI) we aim to expand across has leveraged the wider

for TMRW [pronounced they are digitally advanced, only proposition with no and data analytics to South East Asia. UOB investments in data

“tomorrow”], whose dislike complex, universal bank branches. However, analyse customers’ financial and analytics infrastructure.

parent company is United and opaque banking and customers still need to What technologies does

data to provide them with This has enabled us to build

Overseas Bank (UOB). We’ve would prefer a friend who withdraw cash from time the banking app runs on?

personalised content. out advanced data and

estimated that it could be understands them, rather to time. As such, we have Did you develop them

Other innovative features data science solutions very

worth SGD 10 billion ($7.5 than a traditional bank. leveraged our partnerships in-house?

of the app include gamified rapidly.

billion) in revenue over the Building a digital bank that to allow customers to access We developed most of

savings which encourages What were the main

30 | The BankingTech Awards 2020 The BankingTech Awards 2020 | 31Winner | Best UX/CX in Finance Initiative

BY UOB.

Meet ASEAN’s best digital bank for the

digital generation. A full suite of banking

solutions through a smart, mobile-only app.

In just a under two years

of operations in Thailand, a

market with one of the highest Best UX/CX in Finance Initiative Best Digital Bank ASEAN 2020 Best Initiative in Innovation

digital banking standards in Banking Technology Awards Best Bank for Millennials 2020 The Asset ESG

ASEAN, our engagement- Global Retail Banking Innovation Corporate Awards 2020

focused business model is Awards by the Digital Banker

bearing fruit. In the most

recent survey conducted by

Bain & Co in January 2021,

TMRW is now second in the

market with an NPS of 40

Kevin Lam, head of TMRW Digital Group.

and is ranked number one for

credit cards and for current

challenges when developing offer both forms of biometrics account/savings account.

the banking app? How did to enhance the account Based on our monthly

you overcome them? opening experience. customer assessments

Given the diversity of the Local regulations require conducted internally, we have

different ASEAN markets, we face-to-face video calls in achieved a high NPS of more

had to consider the regulatory Indonesia. After studying than 60 since our launch in

differences in both countries the customer experience we Indonesia. Our Indonesian tmrwbyuob.com

we launched the app in. realised that connectivity customers are also highly

We needed to comply with and bandwidth was an issue. engaged. A recent TikTok

regulations while meeting our We moved from full two- campaign to encourage better

aim of simple and intutitive way video conferencing spending and saving habits

customer experiences, to a text-and-video mix to among millennials received

including the onboarding of minimise the drop-calls and about 1.2 billion impressions

customers. data usage for our customers. in less than a month and more

When onboarding a new This onboarding method was than 7,000 submissions from

bank customer, it’s important timely as customers are able consumers who pledged

that we are able to validate to onboard from their homes to spend and to save more

the customer’s identity in less than seven minutes wisely.

without having the customer during the Covid pandemic. TMRW has received 26

take time out to visit a bank What have been the industry awards, including

branch. benefits of the new banking Best UX / CX in Finance

In Thailand, we used app for customers? How Initiative from the Banking

the country’s national ID have you measured its Technology Awards, Best

database , facial recognition success? Digital Bank (ASEAN) and

and fingerprint matching Net Promoter Score Best Bank for Millennials

technologies to verify (NPS) is a key KPI we from the 2020 Global Retail

customers’ indentites. TMRW track to measure customer Banking Innovations Awards

is the first bank in Thailand to satisfaction. by the Digital Banker.

32 | The BankingTech Awards 2020Winner | Best Use of IT in Private Banking/Wealth Management Winner | Best Use of IT in Private Banking/Wealth Management

Spreading the risk

for P2P investors

Israel-based peer-to-peer (P2P) lending specialist,

BTB, has a business model that has brought

annual average returns of seven per cent in the

last seven years with low defaults. Part of its

success is a technology platform called B-Match

that rebalances and recalculates the investors’

portfolios on a daily basis across all of its loans. result, sometimes a single decreases every day when “fifth line of defence” after

loan could form a relatively the B-match system scans all the others including

large proportion of an the entire pool of existing having a guarantor for

BTB stands for “Be The defaults from the investor Investments can be investor’s portfolio. Despite loans and reshuffles all each loan, means BTB can

Bank”, reflecting its intention perspective. for any amount; usually the very low default rates portfolios to have the boast a 100% rate of loan

at launch in 2014 to directly The company was a loans are up to ILS1 million and the mutual guarantee smallest portion possible repayment. Despite the

link investors to borrowers pioneer in the Israeli market (€250,000). BTB’s platform fund that effectively in each of the loans. many challenges of 2020,

on P2P basis, cutting out the with its P2P offering. “We spans all aspects of P2P, cancels out the defaults, In this way, it achieves BTB’s default rates at the

banks. It has an interesting, had to teach the market, it including tax and fees, with that situation brought a the biggest possible end of the year were lower

risk-averse model whereby was very challenging, there graphical displays of an perceived element of risk. diversification for each than at the end of 2019.

investor funds are spread were a lot of strange and investor’s portfolio by sector, “We wanted everyone to portfolio and means every BTB’s team of 30 staff

across all BTB borrowers sometimes hard questions amount invested (with the be as safe as possible,” investor, regardless of comprises specialists in

(currently each investor to answer, we were – and ability to have sub-users, says Katz. size, has the same level of risk assessment, legal and

holds more than 800 still are – changing the way such as children), interest, Its technical solution to return. regulatory compliance,

different loans in their people and businesses accumulated net interest this issue is called B-Match. “The use of the B-Match government relations, IT,

portfolios). perceive economics,” and investment forecasts This divides all investors’ technology has made marketing and other areas.

In addition, 1% of all says co-founder and of up to 60 years. “From the money dynamically and the investment in the There are around 600,000

deposits and returns reside co-CEO, Alon Katz. BTB first day, the investors love automatically across all platform safer for every SMEs in Israel and this

in a mutual guarantee fund was established with the what they can see,” says existing loans. The first investor, large and small,” number is increasing very

which is used to reimburse aim of, on the one hand, Katz. “As well as excellent version of B-Match did this says Katz. It is part of fast, says Katz, so there is

the investors for the original resolving the credit crunch customer service that using calculations created the success story that plenty of scope for further

investment and interest if of small business owners provides investors with by BTB’s staff. The current has seen BTB double its growth in its domestic

any borrower defaults. BTB and, on the other, offering the information they seek, version, launched in 2020, business each year since market. However, “what we

only accepts around nine investors a profitable and we provide lots of data does it automatically, using launch and provide its did here in Israel, we could

per cent of its SME borrow stable investment with to investors in the digital an in-built smart algorithm, investors with average do anywhere” with what he

applicants as a result of social value. It now has personal area to be as on a daily basis. annual returns of seven feels is a unique business

technology alongside a thousands of investors transparent as possible.” This model means that per cent. The platform model. So international

team of analysts to verify including private individuals, Initially, an investor’s currently an average has gained almost ILS800 expansion is planned. “A

their suitability. Therefore, companies, municipalities, funds would only be of less than 0.1% of million (€200 million) in few countries are in our

defaults are rare. Add in the investment houses, family allocated to news loans each investor’s money investments. That default sights now, it won’t be

mutual guarantee fund and offices and even some from the day that investor is allocated to a single protection model, which tomorrow, but it is not so

this effectively means zero Kibbutz funds. arrived as a client. As a business loan. This amount Katz describes as the far ahead.”

34 | The BankingTech Awards 2020 The BankingTech Awards 2020 | 35Winner | Best Core Banking Solution Provider Winner | Best Core Banking Solution Provider

Innovation to drive

positive change

Chuah Wan Pin, CEO at Infopro Digital Banking, says

that leveraging technology and processes has brought

about tangible benefits for banks.

Infopro artificial intelligence challenger banks. To date,

(AI) driven digital banking there have been over 100 enabled solutions powered This makes for a more where we have applied AI and

platform is a banking system implementations in 32 by AI and machine learning granular breakdown of credit ML – we’ve made processes

that has customer centricity countries that include banks to transform the banking worthiness factors and better frictionless and quicker for our

via digital transformation that might have just one processes. accuracy. customers and theirs too.”

at its heart, explains CEO, branch right up to those with The anti-money laundering Customer analytics and Innovation, says Chuah,

Chuah Wan Pin. “The solution branch networks numbering (AML) function has been intelligent segmentation is a is at the heart of the firm’s

moves core banking into the the hundreds. The biggest one beneficiary of this with third area. The AI allows banks efforts and it is very process-

next generation. It is built for customer has 1,000 branches. AI-powered AML solutions to segment and develop orientated, having been

modularity allowing an API “The past two years have having a significant impact better customer acquisition appraised at CMMI level 5

[application programming seen a particular focus on on reducing false positives. and retention strategies such (Capability Maturity Model

interface] enabled ecosystem, digitisation and everything Intelligent customer profiling as cross-selling/up-selling Integration) as well as being

has reduced processing that comes with that in has also served to effectively products and services using ISO 9001 certified.

times and is also in the

terms of improved processes identify high-risk individuals hyper-personalised marketing

cloud, providing in demand Partnership

automation, sleeker systems and reduce false negatives. communications.

scalability.

and overall better customer AI credit decisioning, Many other banking Being able to pivot and

“We aim to free our banking experience in terms of the respond to opportunity and

meanwhile, now uses solutions and processes have

customers up to focus on their design and function at the change within the market –

automated financial also been embedded with

own business growth and front end,” says Chuah. evolving with it rather than

document upload and AI. Chuah comments: “The

with the knowledge that the lagging behind, is supported

AI information extraction via intention is to have AI woven

underlying banking system is by a partnership approach.

AI-based optical character through the platform and

a capable partner,” he says. A key facet to this has been recognition (OCR) and has extending to each and every “We see our customers

The solution is aimed bringing efficiency and power an AI Scorecard Builder module feeding back into the as partners and the ethos is

at existing banks looking via the use of AI and machine that automatically builds a core. We’ve been happy to one of working together for

for digital transformation, learning (ML) with a mission credit scorecard customised see significant improvements a common aim – to prioritise

as well as new digital of bringing cognitive digitally to a bank’s customer data. to our offering in the spaces customer centricity and

36 | The BankingTech Awards 2020 The BankingTech Awards 2020 | 37You can also read