KBC Group Company presentation - 1Q 2018 - KBC Bank

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

KBC Group

Company presentation

1Q 2018

More information: www.kbc.com

KBC Group - Investor Relations Office – E-mail: investor.relations@kbc.com

1

Important information for investors

This presentation is provided for information purposes only. It does not constitute an offer to sell or the solicitation to buy any

security issued by the KBC Group.

KBC believes that this presentation is reliable, although some information is condensed and therefore incomplete. KBC cannot be

held liable for any loss or damage resulting from the use of the information.

This presentation contains non-IFRS information and forward-looking statements with respect to the strategy, earnings and capital

trends of KBC, involving numerous assumptions and uncertainties. There is a risk that these statements may not be fulfilled and

that future developments differ materially. Moreover, KBC does not undertake any obligation to update the presentation in line

with new developments.

By reading this presentation, each investor is deemed to represent that it possesses sufficient expertise to understand the risks

involved.

21Q 2018 key takeaways for KBC Group

1Q18 financial performance: Capital and liquidity positions:

Very good net result of 556m EUR, despite the large The fully loaded** B3 common equity ratio based on the

upfront bank taxes (371m EUR). ROE of 14%* in 1Q18 Danish Compromise decreased from 16.3% at the end of

Good performance of the commercial bank-insurance franchises 2017 to 15.9% at the end of 1Q18 due to the impact of the

in our core markets and core activities first-time application of IFRS 9 (-41bps)

Q-o-q increase in customer loan volumes and customer deposits Fully loaded B3 leverage ratio, based on current CRR

(excluding debt certificates & repos) in most of our core countries legislation, amounted to 5.7% at KBC Group

Roughly stable net interest income and higher net interest margin Continued strong liquidity position (NSFR at 137% and LCR

q-o-q at 139%) at end 1Q18

High net fee and commission income ** This clearly exceeds the minimum capital requirements set by the competent

supervisors of respectively 9.875% phased-in and 10.60% fully loaded for 2018. On

top of the above-mentioned capital requirements, the ECB expects KBC to hold a

Lower net gains from financial instruments at fair value and higher pillar 2 guidance (P2G) of 1.0% CET1

other net income

Combined ratio of 90% in 1Q18. Excellent sales of non-life and life

insurance products

Strict cost management resulted in a cost/income ratio of 55%

YTD adjusted for specific items

Net impairments releases on financial assets at amortised cost of

63m EUR, mainly driven by Ireland (net release of 43m EUR in

1Q18). We are maintaining our impairment guidance for Ireland,

namely a net release in a range of 100m-150m EUR for FY18

3

* ROE taking into account pro rata bank taxes amounted to 19% in 1Q18Contents

1 1Q 2018 performance of KBC Group

2 1Q 2018 performance of business units

3 Strong solvency and solid liquidity

4 1Q 2018 wrap up

Annex 1: Company profile

Annex 2: Other items

4KBC Group

Section 1

1Q 2018 performance of KBC Group

5Net result at KBC Group

CONTRIBUTION OF BANKING ACTIVITIES

TO KBC GROUP NET RESULT*

750

575

526

461

NET RESULT AT KBC GROUP*

330

855

1Q17 2Q17 3Q17 4Q17 1Q18

691

630

556

CONTRIBUTION OF INSURANCE ACTIVITIES

399 TO KBC GROUP NET RESULT*

137

1Q17 2Q17 3Q17 4Q17 1Q18

111 113

96 102

78

64

78 27 42

82 93 84 75

61

-29 -15

* Difference between net result at KBC Group and the sum of the banking and insurance -33 -52 -34

contribution is accounted for by the holding-company/group items

1Q17 2Q17 3Q17 4Q17 1Q18

Non-Life result Non-technical & taxes

Amounts in m EUR 6

Life resultSummary 2017 pro forma figures

Impact shift 4Q17 4Q17 3Q17 3Q17 2Q17 2Q17 1Q17 1Q17

per P&L line as was pro forma as was pro forma as was pro forma as was pro forma

NII 1,029 1,137 1,039 1,114 1,028 1,094 1,025 1,081

+108 +75 +66 +56

FIFV 235 118 182 94 249 180 191 130

+26 +25 +24 +24

F&C 430 456 408 433 430 454 439 463

+17 +12 +21 +19

AFS gains* 51 6 51 2 52 8 45 14

* Due to IFRS 9, the P&L line ‘net realised result from AFS assets is replaced by ‘net realised result from debt instruments at FV through OCI’

• Interest accrual FX derivatives: shifted from FIFV to NII (in line with the transition to IFRS 9)

• Network income (income received from margins earned on FX transactions carried out by the network for clients): shifted from FIFV to F&C

• IFRS 9: overlay approach for insurance: shift from realised gains AFS shares and impairments on AFS shares to FIFV

• Please note that due to IFRS 9, the realised gains on AFS shares in Banking (26m in 4Q17, 32m in 3Q17, 21m in 2Q17 and 10m in 1Q17) have

been eliminated from net result as they are now booked in equity

7Good net interest income and higher net interest margin

NII (pro forma for 2017*) Amounts in m EUR

1,081 1,094 1,114

2 22

1,137

3 47

1,125

0 27

Net interest income (1,125m EUR)

3 28 3 21 128

143 142 144 135 • Down by 1% q-o-q and up by 4% y-o-y

• The small q-o-q decrease was driven primarily by:

o lower netted positive impact of ALM FX swaps

907 928 946 952 970

o lower reinvestment yields

o more negative pressure on commercial loan margins in

most core countries

1Q17 2Q17 3Q17 4Q17 1Q18

NII - netted positive impact of ALM FX swaps** NII - Insurance

o lower number of days

NII - Holding-company/group NII - Banking partly offset by:

* 2017 pro forma figures for NII as the impact of ALM FX derivatives was ‘netted’ in NII as of 2018

o lower funding costs (due mainly to the call of the CoCo)

** From all ALM FX swap desks o continued good loan volume growth

*** NIM is calculated excluding the dealing room and the net positive impact of ALM FX swaps & repos

o positive impact of both short & long term increasing

NIM (pro forma for 2017***) interest rates in the Czech Republic

2.01%

1.97%

1.93% 1.96% 1.96%

Net interest margin (2.01%)

• Up by 4 bps q-o-q and by 8 bps y-o-y thanks to lower funding

costs and the positive impact of repo rate hikes in the Czech

Republic

Customer deposit volumes excluding debt

1Q17 2Q17 3Q17 4Q17 1Q18 certificates & repos +2% q-o-q and +7% y-o-y

VOLUME TREND

Excluding FX effect Total loans ** o/w retail mortgages Customer deposits*** AuM Life reserves

Volume 143bn 60bn 188bn 213bn 29bn

Growth q-o-q* +1% 0% -3% -2% 0%

Growth y-o-y +5% +4% +3% 0% -2%

* Non-annualised

** Loans to customers, excluding reverse repos (and bonds) 8

*** Customer deposits, including debt certificates but excluding reposHigh net fee and commission income

Amounts in m EUR Net fee and commission income (450m EUR)

F&C (pro forma for 2017*) • Down by 1% q-o-q and by 3% y-o-y

• Positive net sales of mutual funds in 1Q18

463 454 456 450

24 24

433

26 25

• Q-o-q decrease was the result chiefly of:

25

o lower management fees

o lower fees from payment services

511 506 518 502

489 o lower fees from credit files & bank guarantees

o lower securities-related fees

-72 -73 -81 -86 -77

0 partly offset by:

-2 -1 o higher entry fees

1Q17 2Q17 3Q17 4Q17 1Q18

o lower commissions paid on insurance sales

F&C - network income F&C - banking contribution • Y-o-y decrease was mainly the result of:

F&C - insurance contribution F&C - contribution of holding-company/group o lower entry fees

* 2017 pro forma figures as the network income shifted from FIFV to net F&C as of 2018 o lower securities-related fees

o lower fees from credit files & bank guarantees

Amounts in bn EUR partly offset by:

o higher fees from payment services

AuM* o the contribution of UBB/Interlease

214 213 215 217 213

Assets under management (213bn EUR)

• Fell by 1.5% q-o-q owing entirely to a negative price effect

• The mutual fund business has seen net inflows again, but this

was offset by net outflows in group assets and investment

advice

1Q17 2Q17 3Q17 4Q17 1Q18

* Note that 2017 AuM figures were reduced due to a roughly 2bn EUR adjustment in Institutional Mandates

9Insurance premium income up y-o-y

and good combined ratio

PREMIUM INCOME (GROSS EARNED PREMIUM) Insurance premium income (gross earned

794

premium) at 714m EUR

672 636 660

714

• Non-life premium income (378m) increased by 5%

410 y-o-y

282 336

312 267 • Life premium income (336m) down by 18% q-o-q

and up by 8% y-o-y

360 369 378 384 378

1Q17 2Q17 3Q17 4Q17 1Q18

Life premium income Non-Life premium income

COMBINED RATIO (NON-LIFE)

79%

90%

84% 83%

88% The non-life combined ratio at 1Q18 amounted

to 90%, still a good number despite higher

technical charges due mainly to higher storm

claims in Belgium

1Q 1H 9M FY

2017 2018

10

Amounts in m EURNon-life and life sales up y-o-y

NON-LIFE SALES (GROSS WRITTEN PREMIUM) Sales of non-life insurance products

468 492 • Up by 5% y-o-y thanks to a good commercial

performance in all major product lines in our core

358 349 342 markets and tariff increases

1Q17 2Q17 3Q17 4Q17 1Q18

Sales of life insurance products

• Decreased by 15% q-o-q and up by 5% y-o-y

LIFE SALES • The q-o-q decrease was driven mainly by lower sales of

588 guaranteed interest products in Belgium (attributable

474 498 chiefly to traditionally higher volumes in tax-

415 405 incentivised pension saving products in 4Q17 and extra

318

267 279 sales for individual pension agreements for self-

222 218

employed business leaders, anticipating the reduction

270

of corporate tax as of 2018) and lower sales of unit-

207 193 187 219 linked products in the Czech Republic

1Q17 2Q17 3Q17 4Q17 1Q18 • The y-o-y increase was driven mainly by higher sales of

guaranteed interest products in Belgium and higher

sales of unit-linked products in the Czech Republic

Guaranteed interest products Unit-linked products • Sales of unit-linked products accounted for 44% of total

life insurance sales

11

Amounts in m EURLower FV gains, higher other net income

FV GAINS (pro forma for 2017*)

180

The lower q-o-q figures for net gains from

130 86 118

financial instruments at fair value were

94 96 attributable mainly to:

110 94 • a negative change in market, credit and funding value

73 71 73

adjustments (mainly as a result of changes in the

19

1

21 11 7

19

4 underlying market value of the derivative portfolio)

12 17

1Q17 2Q17 3Q17 4Q17 1Q18 • lower dealing room income

Other FV gains Net result on equity instruments (overlay insurance)

M2M ALM derivatives

* 2017 pro forma figures as:

1) the impact of the FX derivatives was ‘netted’ in NII as of 2018

2) the shift from realised gains AFS shares and impairments on AFS shares to FIFV due to IFRS 9 (overlay approach for insurance)

OTHER NET INCOME Other net income amounted to 71m EUR,

77

71

higher than the normal run rate of around 50m

EUR due to the settlement of an old legal file in

47

Belgium and the sale of a building in Hungary

4

-14

1Q17 2Q17 3Q17 4Q17 1Q18

12

Amounts in m EUROperating expenses up due entirely to higher bank taxes,

but good cost/income ratio

OPERATING EXPENSES Cost/income ratio (banking) adjusted for specific

items* at 55% in 1Q18

1,291

1,229 • Operating expenses excluding bank tax went down by

1,021 371 6% q-o-q due mainly to seasonal effects such as

361 910 914 41 traditionally lower ICT, marketing and professional fee

19 18

expenses, despite a 12m EUR provision for facility

expenses for one specific file in Belgium in 1Q18

891 896 980 920

868

• Operating expenses without bank tax increased by 6%

y-o-y due chiefly to the consolidation of UBB/Interlease,

higher ICT costs, higher staff expenses (wage drift in

1Q17 2Q17 3Q17 4Q17 1Q18 most countries), higher marketing expenses, a 12m EUR

provision for facility expenses for one specific file in

Bank tax Operating expenses Belgium and higher depreciation & amortisation costs

(due to the capitalisation of some projects)

EXPECTED BANK TAX SPREAD IN 2018 (PRELIMINARY)**

TOTAL Upfront Spread out over the year • Pursuant to IFRIC 21, certain levies (such as

contributions to the European Single Resolution Fund)

1Q18 1Q18 1Q18 2Q18e 3Q18e 4Q18e have to be recognised in advance, and this adversely

273 0 0 0 0

impacted the results for 1Q17. The y-o-y increase can

BU BE 273

mainly be explained by the consolidation of UBB

BU CZ 29 29 0 0 0 0 • Total bank taxes (including ESRF contribution) are

Hungary 45 26 19 21 21 21 expected to increase from 439m EUR in FY17 to 461m

EUR in FY18, although still subject to changes

Slovakia 7 3 4 4 4 4

Bulgaria 14 14 0 0 0 0

Ireland 4 3 1 1 1 14

GC 0 0 0 0 0 0

TOTAL 371 347 24 25 25 39 * See glossary (slide 88) for the exact definition

13

Amounts in m EUR ** still subject to changesOverview of bank taxes* Bank taxes of 273m EUR in

1Q18. On a pro rata basis, bank

taxes represented 11.1% of

KBC GROUP Bank taxes of 371m EUR in BELGIUM BU 1Q18 opex at the Belgium BU

361 371 1Q18. On a pro rata basis, 278 273

bank taxes represented 11.1% 53 58

83 98

of 1Q18 opex at KBC Group**

225 215

278 273

41

19 18 0 0

41 -4 -2

-1 20

-6 -7

1Q17 2Q17 3Q17 4Q17 1Q18

1Q17 2Q17 3Q17 4Q17 1Q18

European Single Resolution Fund contribution ESRF contribution Common bank taxes

Common bank taxes

Bank taxes of 70m EUR in

1Q18. On a pro rata basis,

Bank taxes of 29m EUR in bank taxes represented 18.0%

CZECH REPUBLIC BU 1Q18. On a pro rata basis, INTERNATIONAL MARKETS BU of 1Q18 opex at the IM BU

bank taxes represented 4.3%

29 of 1Q18 opex at the CZ BU 70

26

57 18

11

41

22

20

25 25

1 52

46

24

6 1 0 0 6

1Q17 2Q17 3Q17 4Q17 1Q18 1Q17 2Q17 3Q17 4Q17 1Q18

ESRF contribution Common bank taxes

ESRF contribution Common bank taxes

* This refers solely to the bank taxes recognised in opex, and as such it does not take account of income tax expenses, non-recoverable VAT, etc.

** The C/I ratio adjusted for specific items of 55% in 1Q18 amounts to roughly 48% excluding these bank taxes

14Net impairment releases, excellent credit cost ratio and

improved impaired loans ratio

ASSET IMPAIRMENT

31 2 Very low asset impairments

15

8

1 15

32 • This was attributable mainly to:

6 7 6

o net loan loss provision releases in Ireland of 43m EUR

-30

-78 -63 (compared with 52m in 4Q17)

o also small net loan provision reversals in Bulgaria, Hungary,

-56 Slovakia and Group Centre

-71

1Q17 2Q17 3Q17 4Q17 1Q18

• Impairment of 6m on other in the Czech Republic as a result of

Other impairments Impairments on financial assets at AC*

* AC = Amortised Cost. Under IAS 39, impairments on L&R

the review of the residual value calculation on financial leases

for cars in CSOB Leasing

CREDIT COST RATIO

0.42%

0.23%

0.09%

The credit cost ratio amounted to -0.15% in 1Q18 due to

low gross impairments and several releases

-0.06%

-0.15%

FY14 FY15 FY16 FY17 1Q18

IMPAIRED LOANS RATIO

6.8% 6.9% 6.6%

6.0% 5.9%

The impaired loans ratio improved to 5.9%, 3.5% of

which over 90 days past due

3.6% 3.9% 3.7% 3.4% 3.5%

1Q17 2Q17 3Q17 4Q17 1Q18

15

Impaired loans ratio of which over 90 days past dueKBC Group

Section 2

1Q 2018 performance of business units

16BELGIUM BUSINESS UNIT

CFO SERVICES

CRO SERVICES

CZECH INTERNATIONAL

BELGIUM

REPUBLIC MARKETS

CORPORATE STAFF

17Belgium BU (1): net result of 243m EUR

NET RESULT Net result at the Belgium Business Unit

483

amounted to 243m EUR

455 • The quarter under review was characterised by lower

net interest income, roughly stable net fee and

336 commission income, decreased trading and fair value

301 income, higher other net income, an improved

243 combined ratio, seasonally lower sales of life

insurance products, higher operating expenses due

entirely to higher bank taxes and lower impairment

charges q-o-q

• Excluding both the upfront booking of the bank tax in

1Q18 and the one-off negative impact of the reform

1Q17 2Q17 3Q17 4Q17 1Q18 of the Belgian corporate income tax regime in 4Q17,

the net result rose by roughly 3% q-o-q

Amounts in m EUR • Customer deposits excluding debt certificates and

repos rose by 4% y-o-y, while customer loans also

increased by 4% y-o-y

VOLUME TREND Customer deposit volumes excluding debt

certificates & repos +2% q-o-q and +4% y-o-y

Total loans ** o/w retail mortgages Customer deposits*** AuM Life reserves

Volume 96bn 35bn 126bn 199bn 27bn

Growth q-o-q* +1% 0% -5% -1% -1%

Growth y-o-y +4% +1% 0% 0% -2%

* Non-annualised

** Loans to customers, excluding reverse repos (and bonds)

*** Customer deposits, including debt certificates but excluding repos

18Belgium BU (2): lower NII despite stable NIM

Amounts in m EUR

NII (pro forma for 2017*)

681 677 664 677

649 Net interest income (649m EUR)

28 19 20 39

130 129

19 • Fell by 4% q-o-q due mainly to the lower netted impact of FX

132 123 117 swaps, lower reinvestment yields and lower number of days

• Down by 5% y-o-y, driven primarily by:

o lower reinvestment yields

523 529 512 515 513 o pressure on commercial loan margins

o lower upfront prepayment fees (6m EUR in 1Q18 compared

with 9m EUR in 1Q17)

partly offset by:

1Q17 2Q17 3Q17 4Q17 1Q18

o lower funding costs on term deposits

NII - netted positive impact of ALM FX swaps** NII - contribution of banking

o good loan volume growth

NII - contribution of insurance

• 2017 pro forma figures for NII as the impact of ALM FX derivatives was ‘netted’ in NII as of 2018

** From all ALM FX swap desks

*** NIM is calculated excluding the dealing room and the net positive impact of ALM FX swaps & repos

NIM (pro forma for 2017***) Net interest margin (1.73%)

1.78% 1.79%

1.72% 1.73% 1.73%

• Stabilised q-o-q

• Fell by 5 bps y-o-y due to the negative impact of lower

reinvestment yields and some pressure on commercial loan

margins

1Q17 2Q17 3Q17 4Q17 1Q18

19Credit margins in Belgium

PRODUCT SPREAD ON CUSTOMER LOAN BOOK, OUTSTANDING

1.4

1.2

1.0

0.8

0.6

0.4

0.2

0.0

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17 4Q17 1Q18

Customer loans

PRODUCT SPREAD ON NEW PRODUCTION

1.8

1.6

1.4

1.2

1.0

0.8

0.6

0.4

0.2

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17 4Q17 1Q18

SME and corporate loans Mortgage loans

20Belgium BU (3): good net F&C income

Amounts in m EUR

F&C (pro forma for 2017*) Net fee and commission income (318m EUR)

356 • Positive net sales of mutual funds in 1Q18

339 321

10

9 307

8

318

9

• Net F&C income decreased by 1% q-o-q due mainly to:

7

o lower management fees

o lower securities-related fees

o lower fees from credit files & bank guarantees

391 376 352 368 356 partly offset by

o higher entry fees from mutual funds and unit-linked

life insurance products

o higher fees from payment services

-45 -45 -52 -55 -47 o lower commissions paid on insurance sales

1Q17 2Q17 3Q17 4Q17 1Q18

F&C - network income F&C - contribution of banking • Fell by 11% y-o-y driven chiefly by lower entry fees from

F&C - contribution of insurance mutual funds & unit-linked life insurance products (as

* 2017 pro forma figures as the network income shifted from FIFV to net F&C as of 2018 1Q17 benefited from the launch of EasyInvest), lower

securities-related fees, lower fees from credit files &

AuM* Amounts in bn EUR

bank guarantees, slightly lower fees from payment

200 198 200 202 199 services and higher commissions paid on insurance sales

Assets under management (199bn EUR)

• Fell by 1% q-o-q owing entirely to a negative price effect

• Stabilised y-o-y as net inflows (+1%) were offset by a

negative price effect (-1%)

1Q17 2Q17 3Q17 4Q17 1Q18

* Also note that 2017 AuM figures were reduced due to a roughly 2bn EUR adjustment in Institutional Mandates

21Belgium BU (4): higher y-o-y non-life sales and good

combined ratio

Sales of non-life insurance products

NON-LIFE SALES (GROSS WRITTEN PREMIUM) • Increased by 2% y-o-y

323 329

• Premium growth was situated in all classes, except for

‘Accident & Health’

256

241

228

1Q17 2Q17 3Q17 4Q17 1Q18

COMBINED RATIO (NON-LIFE) Combined ratio amounted to 93% in 1Q18

(86% in FY17). 1Q18 was negatively impacted by

93%

81%

86% higher technical charges y-o-y due mainly to

80%

77%

higher storm claims

1Q 1H 9M FY

2017 2018

22Belgium BU (5): lower life sales and good cross-selling

ratios

LIFE SALES Sales of life insurance products

460

• Fell by 12% q-o-q as the sales of guaranteed interest

404

products are traditionally lower in the first quarter

396

(versus traditionally higher volumes in tax-incentivised

340 pension saving products in the fourth quarter and

306

290 extra sales for individual pension agreements for self-

241 250

197 employed business leaders in 4Q17, anticipating the

193 reduction of corporate tax as of 2018). The lower

sales of unit-linked products was the result of

155 143 170 154

commercial efforts in 4Q17 and a less favourable

113 investment climate in 1Q18

1Q17 2Q17 3Q17 4Q17 1Q18 • Increased by 2% y-o-y driven entirely by higher sales

of guaranteed interest products

Guaranteed interest products Unit-linked products • As a result, guaranteed interest products and unit-

linked products accounted for 62% and 38%,

Amounts in m EUR

respectively, of life insurance sales in 1Q18

MORTGAGE-RELATED CROSS-SELLING RATIOS

90

85 86.5%

80 78.9%

75

70 Mortgage-related cross-selling ratios

65 • 86.5% for property insurance

63.7%

60 • 78.9% for life insurance

Property insurance Life insurance

55

50

45 49.5%

40

23Belgium BU (6): lower FV gains and higher other net income

FV GAINS (pro forma for 2017*) The lower q-o-q figures for net gains from

110

financial instruments at fair value were the

61 74 result mainly of negative q-o-q change in

23 51 market, credit and funding value adjustments

36 34 (mainly as a result of changes in the

29 30 36

10

14

17 underlying market value of the derivative

20 21 12

-2

17

-2

19 portfolio)

1Q17 2Q17 3Q17 4Q17 1Q18

Other FV gains Net result on equity instruments (overlay insurance)

M2M ALM derivatives

* 2017 pro forma figures as:

1) the impact of the FX derivatives was ‘netted’ in NII as of 2018

2) the shift from realised gains AFS shares and impairments on AFS shares to FIFV due to IFRS 9 (overlay approach for insurance)

OTHER NET INCOME

Other net income amounted to 59m EUR in

59 1Q18, higher than the normal run rate of

46

51 around 50m EUR due to the settlement of an

40 38 old legal file

1Q17 2Q17 3Q17 4Q17 1Q18

24

Amounts in m EURBelgium BU (7): higher opex due entirely to higher bank

taxes, lower impairments, good credit cost ratio

OPERATING EXPENSES Operating expenses: +45% q-o-q and stable y-o-y

822 822

• Operating expenses without bank tax fell by 3% q-o-q due

mainly to traditionally lower marketing, professional fee

and ICT expenses in the first quarter, despite a 12m EUR

278 273

544

566 provision for facility expenses for one specific file in 1Q18

520 0

• Operating expenses without bank tax increased by 1% y-o-y

as lower staff and marketing expenses were more than

offset by a 12m EUR provision for facility expenses for one

544 550 527 566 549 specific file in 1Q18, higher ICT & professional fee expenses

• Cost/income ratio: 77% in 1Q18, distorted mainly by the

bank taxes. Adjusted for specific items, the C/I ratio

-6 -7

amounted to 56% in 1Q18 (53% in FY17)

1Q17 2Q17 3Q17 4Q17 1Q18

Bank tax Operating expenses

ASSET IMPAIRMENT

60

1 Loan loss provisions amounted to 14m EUR in 1Q18

(compared with loan loss provisions of 12m EUR in

34

4Q17), so continuously overall low gross impairments

59

(in all segments) in 1Q18. Credit cost ratio amounted

13 24

to 5 bps in 1Q18 (9 bps in FY17)

12 13

21

14

Impaired loans ratio improved to 2.6%, 1.3% of which

12

3 -1

over 90 days past due

-4

-2

1Q17 2Q17 3Q17 4Q17 1Q18

Other impairments Impairments on financial assets at AC*

* AC = Amortised Cost. Under IAS 39, impairments on L&R

Amounts in m EUR 25Net result at the Belgium BU

CONTRIBUTION OF BANKING ACTIVITIES TO

NET RESULT OF THE BELGIUM BU*

385

336

271

NET RESULT AT THE BELGIUM BU* 208

165

483

455

336

301 1Q17 2Q17 3Q17 4Q17 1Q18

243

CONTRIBUTION OF INSURANCE ACTIVITIES TO

NET RESULT OF THE BELGIUM BU*

119

1Q17 2Q17 3Q17 4Q17 1Q18

93 98

79

48 65 78

64 9 20

70 80 74 63

50

-5

-21 -20 -19

-40

* Difference between net profit at the Belgium Business Unit and the sum of 1Q17 2Q17 3Q17 4Q17 1Q18

the banking and insurance contribution is accounted for by the rounding up

Non-Life result Life result Non-technical & taxes

or down of figures

Amounts in m EUR 26CZECH REPUBLIC BUSINESS UNIT

CFO SERVICES

CRO SERVICES

CZECH INTERNATIONAL

BELGIUM

REPUBLIC MARKETS

CORPORATE STAFF

27Czech Republic BU (1): net result of 171m EUR

NET RESULT

Net result at the Czech Republic Business Unit of

181 183

170 167 171 171m EUR

• Q-o-q results were characterised by higher net

interest income, higher net fee and commission

income, lower but still good net results from financial

instruments at fair value, stable net other income, an

improved combined ratio, lower sales of life insurance

products, higher operating expenses (due entirely to

higher bank taxes) and lower impairment charges

• The net result rose by 2% q-o-q. Excluding the upfront

booking of the bank tax in 1Q18, the net result was

even up by 16% q-o-q

1Q17 2Q17 3Q17 4Q17 1Q18 • Profit contribution from the insurance business

remained limited in comparison to the banking

business

Amounts in m EUR

VOLUME TREND

Excluding FX effect Total loans ** o/w retail mortgages Customer deposits*** AuM Life reserves

Volume 23bn 11bn 31bn 9.7bn 1.2bn

Growth q-o-q* +1% +1% +1% +1% +7%

Growth y-o-y +5% +10% +3% +10% +13%

* Non-annualised

** Loans to customers, excluding reverse repos (and bonds)

*** Customer deposits, including debt certificates but excluding repos

28Czech Republic BU (2): higher NII and NIM

NII Net interest income (248m EUR)

248 • Up by 6% q-o-q and by 15% y-o-y to 248m EUR.

216 220 218

234 Corrected for FX effects, NII rose by 5% q-o-q and by

8% y-o-y pro forma

• The pro forma q-o-q increase was the result primarily

of the positive impact of both short & long term

increasing interest rates and the growth in retail loan

volumes, which were partly offset by pressure on

lending margins in mortgages and consumer finance

• Loan volumes up by 5% y-o-y, driven mainly by growth

in mortgages and consumer finance and, to a lesser

1Q17 2Q17 3Q17 4Q17 1Q18 extent, in SME loans

• Customer deposit volumes up by 3% y-o-y

Amounts in m EUR

NIM (pro forma for 2017*)

Net interest margin (3.02%)

3.02%

2.93% 2.91% 2.84% 2.95%

• Up by 7 bps q-o-q and by 9 bps y-o-y to 3.02%

• The q-o-q increase was driven mainly by the positive

impact of repo rate hikes, partly offset by pressure on

lending margins

• The y-o-y increase was the result of the positive impact

of repo rate hikes, partly offset by pressure on lending

margins (especially in mortgages and consumer

finance)

1Q17 2Q17 3Q17 4Q17 1Q18

* NIM is is calculated excluding the dealing room and the net positive impact of ALM FX swaps & repos

29Czech Republic BU (3): higher net F&C income

Amounts in m EUR

F&C (pro forma for 2017*) Net fee and commission income (67m EUR)

67 • Rose by 5% q-o-q and by 19% y-o-y on a pro forma

64 basis

56 56 10

53 10 • The q-o-q increase was driven by lower paid

9 9

10 commissions to the Czech Post (from this year on,

Czech Post receives more support than in the past,

booked in opex). Besides this effect, there is impact of

47 47

53 57 higher entry fees, higher securities-related fees, but

43 lower fees from payment services (seasonal effect of

Christmas) and lower fees from credit files & bank

guarantees

1Q17 2Q17 3Q17 4Q17 1Q18 • The y-o-y increase was attributable chiefly to higher

management & entry fees, higher fees from payment

F&C - network income F&C - banking & insurance

services, higher securities-related fees and due to less

* 2017 pro forma figures as the network income shifted from FIFV to net F&C as of 2018 fees paid to the Czech Post

AuM Amounts in bn EUR

9.7

8.8

9.2 9.3 9.6

Assets under management (9.7bn EUR)

• Increased by 1% q-o-q owing to net inflows (+2%) and

a negative price effect (-1%)

• Y-o-y, assets under management rose by 10%, driven

by net inflows (+6%) and a positive price effect (+4%)

1Q17 2Q17 3Q17 4Q17 1Q18

30Czech Republic BU (4): higher premium income, good

combined ratio

PREMIUM INCOME (GROSS EARNED PREMIUM)

155

Insurance premium income (gross earned

124 117

premium) stood at 117m EUR

97 100

96 • Non-life premium income (57m) rose by 10% y-o-y

68 60

48 47 excluding FX effect, due to growth in all products

53 56 59 57

• Life premium income (60m) went down by 39% q-o-q

49

and increased by 17% y-o-y, excluding FX effect. Q-o-q

1Q17 2Q17 3Q17 4Q17 1Q18 decline entirely in unit-linked single premiums

Life premium income Non-Life premium income

COMBINED RATIO (NON-LIFE)

100%

93% 98% 97% 97% Combined ratio: 93% in 1Q18 (compared with

97% in FY17) due to very good claim experience

(no large claims and mild winter)

1Q 1H 9M FY

2017 2018

CROSS-SELLING RATIOS

Mortg. & prop. Mortg. & life risk Cons. Fin. & life risk

Cross-selling ratios remained at a good level

65% 61% 60% 63% 57%

47% 48% 45% 53%

2016 2017 1Q18 2016 2017 1Q18 2016 2017 1Q18 31Czech Republic BU (5): higher opex due entirely to higher

bank taxes, excellent credit cost ratio

Operating expenses (189m EUR)

OPERATING EXPENSES • Fell by 10% q-o-q and rose by 8% y-o-y, excluding FX

effect and bank tax

189

165

177

0

• The q-o-q decrease excluding FX effect and bank tax

29

151 153 was due mainly to traditionally lower marketing

26 0

1 expenses and professional fees, lower ICT costs and

facilities expenses in the first quarter

176

• The y-o-y increase excluding FX effect and bank tax was

139 150 152 160 attributable primarily to higher staff expenses (mainly

due to wage inflation) and higher support to the Czech

Post (which is compensated by lower paid fee)

• Cost/income ratio at 47% in 1Q18. Adjusted for specific

1Q17 2Q17 3Q17 4Q17 1Q18 items, the C/I ratio amounted to roughly 42% in 1Q18

(and 43% in FY17)

Bank tax Operating expenses

Very limited loan loss provisions due to several

ASSET IMPAIRMENT releases (which almost fully offset the low gross

11 11 impairments)

Impairment of 6m EUR on ‘other’ as the result of

7 a revaluation of leased cars in CSOB Leasing

Credit cost ratio amounted to 0.01% in 1Q18

3

2014 2015 2016 2017 1Q18

CCR 0.18% 0.18% 0.11% 0.02% 0.01%

-1 Impaired loans ratio stabilised at 2.4%, 1.6% of

1Q17 2Q17 3Q17 4Q17 1Q18 which over 90 days past due

32INTERNATIONAL MARKETS BUSINESS UNIT

CFO SERVICES

CRO SERVICES

CZECH INTERNATIONAL

BELGIUM

REPUBLIC MARKETS

CORPORATE STAFF

33International Markets BU (1): net result of 137m EUR

Net result: 137m EUR

NET RESULT The pro forma q-o-q results were characterised by:

• lower net interest income. NIM amounted to 2.88% in

177

5

1Q18 (2.84% in 4Q17)

• lower net fee and commission income (in BG & HU)

137

• higher result from financial instruments at fair value

21

114 99 • sharply higher net other income (especially in IRL, as 4Q17

4

was impacted by an additional provision related to the

78 74 57 tracker mortgage review)

67

22 18 • a very good combined ratio of 86% (especially in HU & SK)

47

3

• higher life insurance sales (in SK & BG)

40 34

20 39

• higher costs due entirely to higher bank taxes

22 25 16 16 23 • higher net impairment releases

-1

1Q17 2Q17 3Q17 4Q17 1Q18 Profit breakdown for International Markets (next

Bulgaria Ireland Hungary Slovakia slides): 23m EUR for Slovakia, 34m EUR for Hungary,

Amounts in m EUR

57m EUR for Ireland and 21m EUR for Bulgaria

VOLUME TREND

Excluding FX effect Total loans ** o/w retail mortgages Customer deposits*** AuM Life reserves

Volume 24bn 15bn 23bn 4.5bn 0.7bn

Growth q-o-q* 0% 0% +1% -11% +6%

Growth y-o-y +13% +8% +24% -21%**** +7%

* Non-annualised

** Loans to customers, excluding reverse repos (and bonds)

*** Customer deposits, including debt certificates but excluding repos

**** The decrease can partly be explained by the divestment of KBC TFI in Poland in December 2017 (-0.93bn AuM in 4Q17)

34International Markets BU (2): Slovakia

Net result of 23m EUR characterised by (pro

NET RESULT forma q-o-q):

• slightly lower net interest income as volume growth

25 was more than offset by margin pressure

23

22 • stable net fee & commission income as the strong

performance in sales of mutual funds was offset by

lower income from banking services

16 16

• lower net other income

• an excellent combined ratio (87% in 1Q18); roughly

stable technical insurance result in life

• lower operating expenses driven by traditionally lower

ICT & marketing expenses in the first quarter and lower

staff expenses

• net impairment releases (mainly in consumer finance

1Q17 2Q17 3Q17 4Q17 1Q18 and leasing)

• credit cost ratio of -0.20% in 1Q18

Amounts in m EUR

VOLUME TREND Volume trend:

Total loans ** o/w retail mortgages Customer deposits*** • Total customer loans rose by 1% q-o-q and by 7% y-o-y,

amongst other things due to the continuously

Volume 7bn 3bn 6bn increasing mortgage portfolio and consumer finance

Growth q-o-q* +1% +3% +3% • Total customer deposits rose by 3% q-o-q and by 9%

y-o-y thanks to retail as well as corporates

Growth y-o-y +7% +12% +9%

* Non-annualised

** Loans to customers, excluding reverse repos (and bonds)

*** Customer deposits, including debt certificates but excluding repos

35International Markets BU (3): Hungary

Net result of 34m EUR characterised by (pro forma

NET RESULT q-o-q):

• lower net interest income due to a one-off effect (2m

47 EUR)

40 39

• lower net fee and commission income as higher

management fees were more than offset by traditionally

34 lower fees from payment transactions in the first quarter

• higher net results from financial instruments thanks to

higher M2M ALM derivatives

20

• higher net other income due to the sale of a building

• good non-life commercial performance y-o-y in all major

product lines and growing average tariff in motor retail;

an excellent combined ratio (84% in 1Q18); stable sales of

life insurance products q-o-q

1Q17 2Q17 3Q17 4Q17 1Q18 • lower operating expenses excluding bank tax (45m EUR)

due mainly to lower staff & ICT expenses

Amounts in m EUR • net impairment releases (mainly in retail and corporates)

• credit cost ratio of -0.44% in 1Q18

VOLUME TREND

Excl. FX effect Total loans ** o/w retail mortgages Customer deposits*** Volume trend:

Volume 4bn 2bn 7bn • Total customer loans stabilised q-o-q and rose by 11%

y-o-y, mainly in mortgages and corporates

Growth q-o-q* 0% 0% -3% • Total customer deposits fell by 3% q-o-q, but rose by 6%

Growth y-o-y +11% +7% +6% y-o-y due to strong growth in corporates

* Non-annualised

** Loans to customers, excluding reverse repos (and bonds)

*** Customer deposits, including debt certificates but excluding repos

36International Markets BU (4): Ireland

Net result of 57m EUR characterised by (pro forma

NET RESULT q-o-q):

• higher net interest income due mainly to lower funding

99 costs

• net other income in 4Q17 was impacted by an additional

provision of 61.5m EUR related to the industry-wide

review of the tracker rate mortgage products originated

67 in Ireland before 2009

57

• higher operating expenses excluding bank tax due mainly

to higher ICT expenses and regulatory levies (mainly CBI

Industry Funding levy)

• lower net impairment releases (-43m EUR in 1Q18

compared with -52m EUR in 4Q17), as 4Q17 benefited

from 31m EUR IBNR parameter changes. Releases in

3

1Q18 are driven by:

-1 o an increase in the 9-month average House Price

1Q17 2Q17 3Q17 4Q17 1Q18 Index and an improved portfolio performance

Amounts in m EUR o lower provisions on existing non-performing loans

driven by improved macro-economic conditions and

provision releases following deleveraging for

VOLUME TREND corporates

Total loans ** o/w retail mortgages Customer deposits*** • credit cost ratio of -1.36% in 1Q18

Volume trend:

Volume 11bn 10bn 6bn

• Total customer loans fell by 1% q-o-q and stabilised y-o-y.

Growth q-o-q* -1% 0% +5% The q-o-q decrease resulted from the further deleveraging

of the corporate loan portfolio

Growth y-o-y 0% +2% +8%

• Retail mortgages: new business (written from 1 Jan 2014)

* Non-annualised +7% q-o-q and +49% y-o-y, while legacy -2% q-o-q and -7%

** Loans to customers, excluding reverse repos (and bonds) y-o-y

*** Customer deposits, including debt certificates but excluding repos • Total customer deposits rose by 5% q-o-q and

37 by 8% y-o-yInternational Markets BU (5): Bulgaria

Net result of 21m EUR

NET RESULT

Net result was characterised by (pro forma q-o-q):

Amounts in m EUR

22 • In banking (CIBank & UBB/Interlease):

21

o slightly lower net interest income, as volume growth was

18 more than offset by margin pressure

o lower net fee and commission income due to traditionally

lower fees from payment transactions in the first quarter

o lower net results from financial instruments

o lower operating expenses excluding bank tax due mainly to

lower staff & ICT expenses

5

4 o higher bank tax y-o-y due to UBB/Interlease acquisition

o net impairment releases. Credit ratio of -1.09% in 1Q18

• In insurance (DZI): higher net result

1Q17 2Q17 3Q17 4Q17 1Q18 o good earned premiums both in Life and Non-Life, offset by

higher technical charges. Combined ratio amounted to 93%

VOLUME TREND Volume trend:

• Total customer loans rose by 1% q-o-q and by 231% y-o-y

Excl. FX effect Total loans *** o/w retail mortg. Customer deposits**** (11% y-o-y excluding UBB/Interlease), amongst other things

due to the continuously increasing mortgage portfolio and a

Volume 3bn 1bn 4bn strong pick-up in corporates in 1Q18

Growth q-o-q* +1% +1% +3% • Total loans: new business +3% q-o-q and +186% y-o-y, while

legacy -7% q-o-q and +787% y-o-y

Growth y-o-y +231%** +239%** +396%**

• Total customer deposits rose by 3% q-o-q and by 396% y-o-y

(9% y-o-y excluding UBB/Interlease)

* Non-annualised

** Y-o-y growth excluding UBB/Interlease amounted to +11% for total loans, +20% for retail mortgages and +9% for customer deposits

*** Loans to customers, excluding reverse repos (and bonds)

**** Customer deposits, including debt certificates but excluding repos

38GROUP CENTRE

CFO SERVICES

CRO SERVICES

CZECH INTERNATIONAL

BELGIUM

REPUBLIC MARKETS

CORPORATE STAFF

39Group Centre: net result of 5m EUR

NET RESULT Net result: 5m EUR

33 The net result for the Group Centre comprises the results coming

from activities and/or decisions specifically made for group

12 purposes (see table below for components)

5

-12

The q-o-q improvement was attributable mainly to:

-179 o one-off upfront negative P&L impact of 126m EUR due to the

1Q17 2Q17 3Q17 4Q17 1Q18

Belgian corporate income tax reform in 4Q17

o higher NII due to lower debt costs (as a result of the call of the

CoCo)

o lower operating expenses

o net impairment releases

BREAKDOWN OF NET RESULT AT GROUP CENTRE

1Q17 2Q17 3Q17 4Q17 1Q18

Group item (ongoing business) -50 0 -31 -157 -17

- Operating expenses of group activities -14 -14 -20 -25 -17

- Capital and treasury management -18 17 5 -5 -4

o/w net subordinated debt cost -9 -9 -9 -13 -6

- Holding of participations -9 -13 -13 18 1

o/w net funding cost of participations -2 0 0 -1 -1

- Group Re 5 6 5 10 7

- Other -14 5 -9 -154 -3

Ongoing results of divestments and companies in run-down 83 11 19 -22 23

Total net result at GC 33 12 -12 -179 5

Amounts in m EUR 40Overview of results based on business units*

Amounts in m EUR

NET PROFIT – KBC GROUP

1Q18 ROAC: 21%

2,639 2,575

2,427

1,762

2,129 1,945

2,035

1,415

556

510 392 630

347

2014 2015 2016 2017 1Q18

2Q-4Q 1Q

NET PROFIT – BELGIUM NET PROFIT – CZECH REPUBLIC NET PROFIT – INTERNATIONAL MARKETS

1Q18 ROAC: 15% 1Q18 ROAC: 40% 1Q18 ROAC: 25%

1,516 1,564 1,575 702

1,432

596

529 542 428 444

1,165 1,234 1,274 521

1,223 390 399 467 245 330

368

171 137

243 221

351 330 301 138 143 129 181 114

209 24 60

2014 2015 2016 2017 1Q18 2014 2015 2016 2017 1Q18

-156

2Q-4Q 1Q 2Q-4Q 1Q -26

-182

2014 2015 2016 2017 1Q18

2Q-4Q 1Q

* Note that the 1Q18 results & ROAC were impacted by the upfront booking of the bank tax

41Balance sheet (1/2):

Loans and deposits continue to grow in most core countries

Y-O-Y ORGANIC* VOLUME GROWTH FOR KBC GROUP

4% 4%

1%

Loans** Retail mortgages Deposits***

* Volume growth excluding FX effects and divestments/acquisitions

** Loans to customers, excluding reverse repos (and bonds)

*** Customer deposits, including debt certificates but excluding repos

42Balance sheet (2/2):

Loans and deposits continue to grow in most core countries

Y-O-Y ORGANIC* VOLUME GROWTH FOR MAIN ENTITIES

12%

9%

10%

7%

4% BE CZ

5%

3%

1%

0%

Loans** Retail Deposits*** Loans** Retail Deposits*** Loans** Retail Deposits***

mortgages mortgages mortgages

20%

11%

11%

7%

6% 9%

8%

2%

0%

Loans** Retail Deposits*** Loans** Retail Deposits*** Loans** Retail Deposits***

mortgages mortgages mortgages****

* Volume growth excluding FX effects and divestments/acquisitions

** Loans to customers, excluding reverse repos (and bonds)

*** Customer deposits, including debt certificates but excluding repos 43

**** Retail mortgages in Ireland: new business (written from 1 Jan 2014) +49% y-o-y, while legacy -7% y-o-yKBC Group

Section 3

Strong solvency and

solid liquidity

44Strong capital position

Fully loaded Basel 3 CET1 ratio at KBC Group (Danish Compromise) The common equity ratio* decreased from

15.9% 16.3% 16.3% at the end of 2017 to 15.9% at the end

15.7% 15.7% 15.9%

of 1Q18 based on the Danish Compromise,

14.0% ‘Own Capital Target’ due to the impact of the first-time application

of IFRS 9 (-41bps). This clearly exceeds the

10.6% fully loaded regulatory minimum

minimum capital requirements** set by the

competent supervisors of 9.875% phased-in

for 2018 and 10.6% fully loaded and our ‘Own

Capital Target’ of 14.0%

The pro forma*** fully loaded CET1 ratio

amounted to roughly 15.7% at the end of

1Q17 1H17 9M17 FY17 1Q18

1Q18

* Note that as from 01/01/2018 onwards, there is no difference

Fully loaded Basel 3 total capital ratio (Danish Compromise) anymore between fully loaded and phased-in

** Excludes a pillar 2 guidance (P2G) of 1.0% CET1

20.7% *** Also taking into account the impact of the share buy-back

19.7%

2.3%

2.3% T2

2.6%

1.5% AT1

The fully loaded total capital ratio amounted

to 19.7% at the end of 1Q18. Including the

15.9% CET1 15.9% successful issuance of 1bn EUR additional Tier-

1 instrument in April 2018, the pro forma fully

loaded total capital ratio amounted to 20.7%

Total capital Pro forma total

ratio 1Q18 capital ratio 1Q18 45Fully loaded Basel 3 leverage ratio and Solvency II ratio

Fully loaded Basel 3 leverage ratio at KBC Group Fully loaded Basel 3 leverage ratio at KBC Bank

5.7% 5.8% 6.1%

5.7% 5.7%

4.8% 4.7% 4.7% 5.0%

4.7%

1Q17 1H17 9M17 FY17 1Q18 1Q17 1H17 9M17 FY17 1Q18

Solvency II ratio

4Q17 1Q18 The increase (+6%-points) in the Solvency II ratio

was mainly the result of lower equity markets

Solvency II ratio* 212% 218%

* On 19 April 2017, the NBB retroactively relaxed the strict cap on the loss-absorbing capacity of deferred taxes in the calculation of the required capital. Belgian insurance

companies are now allowed to apply a higher adjustment for deferred taxes, in line with general European standards, if they pass the recoverability test. This is the case for KBC

46Solid liquidity position (1)

KBC Bank continues to have a strong retail/mid-cap deposit base in its core markets – resulting in a stable funding mix

with a significant portion of the funding attracted from core customer segments & markets

Customer funding further increased in 1Q18. The elevated amount in short-term wholesale funding is on the back of

short-term arbitrage opportunities

Funding from customers (m EUR)

162.536

143.690 155.774

10% 129.555 131.914 132.862 133.766 139.560

3% 6% 3% 2% 4% 5% 8% 12%

0% 2% 2% 7%

9% 10%

8% 8% 8% 8% 7%

7% 9%

9% 8% 9% 8% 8% 8%

9% 3% 2% 3% 3% 10% 6%

8% FY11 FY12 FY13 FY14 FY15 FY16 FY17 1Q18

3%

0% 7%

21%

75%

72%

69% 73% 73% 73% 70% 72%

69% customer

driven

72%

-1% -4%

-6%

FY11 FY12 FY13 FY14 FY15 FY16 FY17 1Q18 Retail and SME

Mid-cap

Net unsecured interbank funding Total equity

Debt issues in retail network

Net secured funding Certificates of deposit

Government and PSE

Debt issues placed with institutional investors Funding from customers

47Solid liquidity position (2)

Short term unsecured funding KBC Bank vs Liquid assets as of end March 2018 (*)

(bn EUR)

486%

68,14

411% 65,39

58,30

KBC maintains a solid liquidity position, given that:

56,23 57,79

• Available liquid assets remained very high at more than

3 times the amount of the net short-term wholesale

309%

funding

271%

288% • Funding from non-wholesale markets is stable funding

25,10

22,70 from core-customer segments in core markets

18,71

14,19

11,56

1Q17 2Q17 3Q17 4Q17 1Q18

Net Short Term Funding Available Liquid Assets Liquid Assets Coverage

* Graph is based on Note 18 of KBC’s quarterly report, except for the ‘available liquid assets’ and

‘liquid assets coverage’, which are based on the KBC Group Treasury Management Report

Ratios FY17 1Q18 Regulatory NSFR is at 137% and LCR is at 139% by the end of

requirement 1Q18

NSFR* 134% 137% ≥100% • Both ratios were well above the regulatory requirement

of at least 100%

LCR** 139% 139% ≥100%

* Net Stable Funding Ratio (NSFR) is based on KBC’s interpretation of the proposal of CRR

amendment

** Liquidity Coverage ratio (LCR) is based on the Delegated Act requirements. From EOY2017

onwards, KBC discloses 12 months average LCR in accordance to EBA guidelines on LCR

disclosure

48KBC Group

Section 4

1Q 2018 wrap up

491Q 2018 wrap up

Strong commercial bank-insurance results in our core countries

Successful earnings track record

Solid capital and robust liquidity position

50Looking forward

We expect 2018 to be a year of sustained economic growth in both the euro area, the US and in each of our

core markets

Management guides for:

• solid returns for all Business Units

• loan impairments for Ireland towards a release in a 100m-150m EUR range for FY18

• the impact of the reform of the Belgian corporate income tax regime: a recurring positive P&L impact as of 2018

onwards and the one-off negative impact in 4Q17 will be fully recuperated in roughly 3 years’ time

• B4 impact for KBC Group is estimated at roughly 8bn EUR higher RWA on a fully loaded basis as at year-end 2017, which

corresponds with a RWA inflation of 9% and an impact on the CET1 ratio of -1.3%

Next to the Belgium and the Czech Republic Business Units, the International Markets Business Unit has

become a strong contributor to the net result of KBC Group thanks to:

• Ireland: re-positioning as a core country with a sustainable profit contribution

• Bulgaria: the legal merger of CIBank into UBB was approved. The new group UBB has become the largest bank-insurance

group in Bulgaria with a substantial increase in profit contribution

• Sustainable profit contribution of Hungary and Slovakia

51KBC Group

Annex 1

Company profile

52Business profile

BREAKDOWN OF ALLOCATED CAPITAL BY BUSINESS UNIT AS AT 31 MARCH 2018

Czech Republic

16%

Belgium 61%

20%

International Markets

3%

Group Centre

KBC is a leading player (retail and SME bank-insurance, private banking, commercial and local investment

banking) in Belgium, the Czech Republic and its 4 core countries in the International Markets Business Unit

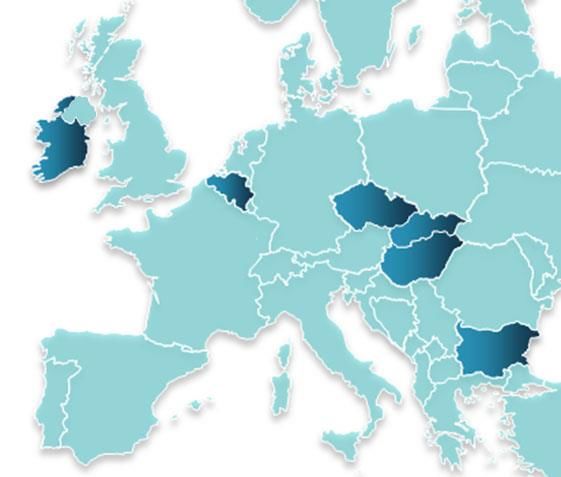

53Well-defined core markets provide access to ‘new

growth’ in Europe

MARKET SHARE (END 2017)

BE CZ SK HU BG IRL

KBC Group’s core markets Loans and 20% 20%

11% 11% 10% 8%*

deposits

Investment 33%

22% 13% 13%

funds 7%

NETHERLANDS Life 21%

14% 8%

IRELAND UK insurance 4% 3%

BELGIUM Non-life 11%

GERMANY insurance 9% 7% 7%

CZECH REP 3%

SLOVAKIA

* Only for retail segment

REAL GDP GROWTH OUTLOOK

FRANCE HUNGARY

FOR CORE MARKETS1

BE CZ SK HU BG IRL

64%

% of

BULGARIA Assets 20%

3% 3% 2% 4%

ITALY 7.8%

4.6% 3.4% 4.0% 3.6%

2017 1.7%

SPAIN

PORTUGAL

Macroeconomic outlook 6.0%

GREECE 3.9% 3.8% 3.6%

Based on GDP, CPI and unemployment trends 2018e 1.9% 3.3%

Inspired by the Financial Times

3.9% 3.5% 3.5% 4.0%

2019e 1.7% 2.8%

1. Source: KBC data, May 2018

54Key strengths

Well-developed bank-insurance strategy and strong cross-selling capabilities

Strong commercial bank-insurance franchises in Belgium and the Czech Republic with stable and solid returns.

The International Markets Business Unit also has become a strong contributor to the net result of KBC Group

Successful earnings track record

Solid capital and robust liquidity position

55Shareholder structure

SHAREHOLDER STRUCTURE AT END 1Q18

Other core

MRBB

7.4%

Cera 11.4%

2.7%

KBC Ancora 18.5%

60.0%

Free float

Roughly 40% of KBC shares are owned by a syndicate of core shareholders, providing continuity to pursue long-term

strategic goals. Committed shareholders include the Cera/KBC Ancora Group (co-operative investment company),

the Belgian farmers’ association (MRBB) and a group of industrialist families

The free float is held mainly by a large variety of international institutional investors

56KBC Group going forward:

Wants to be among the best performing financial institutions in Europe

KBC wants to be among Europe’s best performing financial institutions.

This will be achieved by:

• Strengthening our bank-insurance business model for retail, SME and mid-cap

clients in our core markets, in a highly cost-efficient way

• Focusing on sustainable and profitable growth within the framework of solid

risk, capital and liquidity management

• Creating superior client satisfaction via a seamless, multi-channel, client-centric

distribution approach

By achieving this, KBC wants to become the reference in bank-insurance

in its core markets

57KBC Group going forward:

The bank-insurance business model, different countries, different

stages of implementation

Level 4: Integrated distribution and operation

Acting as a single operational company: bank and insurance operations Belgium

working under unified governance and achieving commercial and non-

commercial synergies

Level 3: Integrated distribution

Acting as a single commercial company: bank and insurance

Target for Central

operations working under unified governance and achieving Europe

commercial synergies

Level 2: Exclusive distribution KBC targets to reach at

Bank branches selling insurance products from intra-

least level 3 in every

group insurance company as country, adapted to the

additional source of fee income

local market structure and

KBC’s market position in

Level 1: Non-exclusive

distribution

banking and insurance.

Bank branches selling insurance

products of third party insurers as

additional source of fee income

58More of the same… but differently…

• Integrated distribution model • Client-centricity will be further • Investment in our digital

according to a real-time fine-tuned into ‘think client, but presence (e.g., social media) to

omni-channel approach design for a digital world’ enhance client relationships and

remains key but client anticipate their needs

interaction will change over • Digitalisation end-to-end, front-

time. Technological and back-end, is the main lever: • Easy-to-access and convenient-

development will be the • All processes digital to-use set-up for our clients

driving force • Execution is the

differentiator • Clients will drive the pace of

• Human interface will still play action and change

a crucial role • Further increase efficiency and

effectiveness of data management • Further development of a fast,

simple and agile organisation

• Simplification is a • Set up an open architecture IT structure

prerequisite: package as core banking system for

• In the way we operate our International Markets Unit • Different speed and maturity in

• Is a continuous effort different entities/core markets

• Is part of our DNA • Improve the applications we offer

our clients (one-stop-shop offering) • Adaptation to a more open

via co-creation/partnerships with architecture (with easy plug in

Fintechs and other value chain and out) to be future-proof and

players to create synergy for all

59Summary of the guidance at KBC Group level

as announced at our Investor Visit in June 2017

More of the same …

Guidance… by…

CAGR total income (‘16-’20)* ≥ 2.25% 2020

C/I ratio banking excluding bank tax ≤ 47% 2020

C/I ratio banking including bank tax ≤ 54% 2020

Combined ratio ≤ 94% 2020

Dividend payout ratio ≥ 50% As of now

* Excluding marked-to-market valuations of ALM derivatives

Regulatory requirements… by…

Common equity ratio*excluding P2G ≥ 10.6% 2019

Common equity ratio*including P2G ≥ 11.6% 2019

MREL ratio** ≥ 25.9% May 2019

NSFR ≥ 100% As of now

LCR ≥ 100% As of now

* Fully loaded, Danish Compromise. P2G = Pillar 2 guidance.

** See slide 83 for more details

60Summary of the guidance at KBC Group level

as announced at our Investor Visit in June 2017

… but differently…

Make further progress in our bank-insurance model

Guidance by… Guidance by…

CAGR Bank-Insurance clients CAGR Bank-Insurance stable clients

(1 Bank product + 1 Insurance product) (3 Bk + 3 Ins products in Belgium; 2 Bk + 2 Ins products in CE)

BU BE > 2% 2020 BU BE > 2% 2020

BU CR > 15% 2020 BU CR > 15% 2020

BU IM > 10% 2020 BU IM > 15% 2020

Guidance on inbound omni-channel/digital behaviour*

Guidance by …

% Inbound contacts via omni-channel and

digital channel

KBC Group** > 80% 2020

• Clients interacting with KBC through at least one of the non-physical channels (digital or through a remote advisory centre), possibly in addition

to contact through physical branches. This means that clients solely interacting with KBC through physical branches (or ATMs) are excluded

** Bulgaria & PSB out of scope for Group target

61Digital Investments 2017-2020

Cashflow 2017-2020 = 1.5bn EUR Operating Expenses 2017-2020 = 1bn EUR

Regulatory driven Organic growth

developments (IFRS or operational

48 55

9, CRS(*), MIFID, Regulatory efficiencies 43 44

etc.) 20% Strategic

78 83 90

Growth 94

36%

Strategic Transformation 112 125 127 128

44%

2017 2018 2019 2020

Omni-channel Strategic Grow Strategic Transform Regulatory

and core-banking

system

(*) The Common Reporting Standard (CRS) refers to a systematic and periodic exchange of information at international level aimed at preventing tax evasion. Information on the

taxpayer in the country where the revenue was taken is exchanged with the country where the taxpayer has to pay tax. It concerns an exchange of information between as many as 53

OECD countries in the first year (2017). By 2018, another 34 countries will join.

62Digital sales are increasing (examples: BU Belgium)

20.000 1.200

18.000

16.000 1.000

14.000 800

12.000

10.000 600

8.000

6.000 400

4.000

200

2.000

0 0

Q1 Q2 Q3 Q4 Q1 Q1 Q2 Q3 Q4 Q1

2017 2018 2017 2018

Consumer loans Travel insurance

8.000 35.000

7.000 30.000

6.000

25.000

5.000

20.000

4.000

15.000

3.000

10.000

2.000

1.000 5.000

0 0

Q1 Q2 Q3 Q4 Q1 Q1 Q2 Q3 Q4 Q1

2017 2018 2017 2018

Pension savings Current accounts

63Omnichannel is embraced by our customers (examples: BU Belgium)

Digital signing after contact with the branches Digital sales @ KBC Live increases,

or KBC Live in 2017-2018 strong performance in non-life

90,00%

80,00%

30.000

70,00%

25.000

60,00%

KBC Live cumulative sales 2017-2018

20.000

50,00%

15.000

40,00%

10.000

30,00%

17Q1 17Q2 17Q3 17Q4 18Q1

5.000

Digital signing of consumer loans

Digital signing of debt protect cover life insurance

0

Digital signing mortgage loans Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mrt

Digital signing housing insurance

Non life insurance Life insurance Housing loans

Digital signing car insurance

Consumer loans Investment plans

64Impact of Basel 4 agreement

On 7 December, the Basel Committee reached an agreement on the remaining Basel 3 post-crisis regulatory

reforms (commonly known as Basel 4). The main elements of the Basel 4 agreement are:

o credit risk: changes to the internal ratings-based approach and a revised standardised approach;

o market risk: FRTB postponed to 2022;

o operational risk: a revised and more risk sensitive standardised approach, replacing all existing approaches;

o an aggregate output floor (gradually phased-in between 2022 and 2027), which will ensure that banks' risk-weighted assets

based on internal models are not lower than 72.5% of RWAs as calculated by the revised standardised approaches

For KBC Group, the RWA increase related to Basel 4 is estimated at roughly 8bn EUR higher RWA on a fully

loaded basis as at year-end 2017, which corresponds with a RWA inflation of 9% and an impact on the CET1 ratio

of -1.3%. This figure is based on our current interpretation of Basel 4, a static balance sheet and the current

economic environment. It also does not take into account possible management actions

We no longer see evidence that KBC is impacted significantly more than our peers. As a consequence, the 1%

buffer for Basel 4 in our management targets is no longer required

The Basel agreement now needs to be implemented in EU regulation (CRR/CRD package), which might influence (in

a positive or negative way) the final impact for KBC

Elements that are not included in above mentioned RWA impact (and which might affect KBC earlier):

o the ongoing Targeted Review of Internal Models (TRIM) exercise by ECB;

o the potential impact of the EBA review of the IRB approach (PD & LGD estimation; treatment defaulted exposures);

o any impact on the Pillar 2 requirements (given that pillar 1 more adequately captures the risks)

65You can also read