2018 Income Tax Update - Commercial Real Estate - Stephen M. Lukinovich, CPA, PFS, CVA Andrew J. Ackermann, CPA, CVA

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

2018 Income Tax Update -

Commercial Real Estate

Stephen M. Lukinovich, CPA, PFS, CVA

Andrew J. Ackermann, CPA, CVA

Kentucky Commercial Real Estate Conference

Louisville, KY

October 30, 2018

“Tax Cuts and Jobs Act” A Member of PrimeGlobal – An Association of Independent Accounting Firms 2

Commercial Real Estate Taxation

2018 Agenda

1. Expired income tax provisions

2. New tax reform

3. Depreciation updates

4. Updates on tax incentives

5. Opportunity zones

3

4

Energy Efficient Incentives Expired

Effective 1/1/2018:

• Section 179D Deduction

o Up to $1.80/square foot deduction

• Section 45L - Energy Efficient Home Tax Credit -

$2,000

5

§179D Lookback Rules

• Announced by IRS in December 2010

• Applies for prior year missed §179D

– Now available for more than 3 previous tax years

• Do not amend prior-year tax returns

• Reflect prior year § 179D deductions missed on current

year tax return - Form 3115, § 481(a) full year

deduction - Federal, AMT and State

6

7

Federal Income Tax Reform Legislation

Commercial Real Estate

Substantially unchanged are:

• The rules regarding depreciation tax lives of

commercial real property (39 years)

• Residential real property (27 1/2 years)

• Long-term capital gain tax rates, generally 20%

• The application of the 3.8% Medicare Surtax

• Section 1250 unrecapture rules/tax rate of 25%

• The tax rules regarding Low Income Housing Tax

Credits

8Qualified Business Income Deduction

• Effective for tax years beginning after Dec. 31,

2017, and before Jan. 1, 2026, an individual

taxpayer generally may deduct 20% of domestic

“qualified business income” from a partnership,

LLC, S corporation or sole proprietorship

• Deduction amount for a tax year is the sum of:

1) the lesser of:

a) the “combined qualified business income amount”; or

b) 20% of the excess of taxable income over the sum of i) net capital

gain and ii) qualified cooperative dividends; plus

2) the lesser of:

20% of qualified cooperative dividends; or

taxable income minus the taxpayer’s net capital gain

9QBI Deduction - continued

In the case of a partnership or S corporation, the provision applies at the

partner/shareholder level

• Partnership.

• Each partner takes into account the partner’s allocable share of each

qualified item of income, gain, deduction, and loss, and is credited with W-

2 wages for the tax year equal to the partner’s allocable share of W-2

wages of the partnership

• Partner’s allocable share of W-2 wages is required to be determined in the

same manner as the partner’s share of wage expenses

• S corporation

• Each shareholder of an S corporation takes into account the shareholder’s

pro rata share of each qualified item of income, gain, deduction, and loss,

and is credited with W-2 wages for the year equal to the shareholder’s pro

rata share of W-2 wages of the corporation.

10QBI Deduction - continued

• The deduction is generally limited based on greater of a) 50% of W-2 wages

paid, or b) the sum of 25% of W-2 wages plus 2.5% of the unadjusted basis of

qualified property held by the business (Note: this limitation is phased in

above a threshold amount of taxable income)

• Qualified property must 1) be depreciable tangible property, 2) held at the

close of the tax year, 3) used to produce qualified business income, and 4) the

property’s depreciation period cannot end before the close of the tax year

(later of 10 years or last day of MACRS recovery period).

• The deduction is generally not allowed for certain specified service trades or

businesses (Note: this disallowance is also phased in above the threshold

amount of taxable income)

• Threshold amount is $315k MFJ ($157,500 for other taxpayers)

• Phase-in range is $100k MFJ ($50k for other taxpayers)

• Fully phased in at $415k MFJ ($207,500 for other taxpayers)

11QBI Deduction - continued

• Qualified trade or business – any trade or business other than a specified

service trade or business (phase-in threshold) and other than the trade or

business of being an employee

• Specified service business is any trade or business:

– involving the performance of services in the fields of accounting,

actuarial science, athletics, brokerage services, consulting, financial

services, health, law, or the performing arts; or

– involves the performance of services that consist of investing and

investment management, trading or dealing in securities,

partnership interests or commodities; or

– where the principal asset of such trade or business is the reputation

or skill of one or more employees or owners.

– Note: engineering and architecture are not specified service

businesses

12QBI Deduction - continued

• Commercial and residential rental real estate

activities (for this purpose only) will generally be

considered a trade or business unless in the form of

a triple net lease arrangement

• Self-rental arrangements will need to be carefully

reviewed for eligibility of the 20%/2.5% deduction

• Economic unit self-rental arrangements will require

further guidance

• Owners who are passive, with passive income, will

be entitled to this new 20%/2.5% deduction

1314

Beginning 1/1/2018 – New

EBIDTA Interest Expense Limitations

• 30% EBIDTA Interest Expense limitation applies

• The 30% of EBITDA interest expense limitation applies to

commercial rental real estate activities

• The 30% interest expense limit is determined at the entity

level

• Entities with less than $25 million in annual sales are exempt

• Real estate development activities with sales in excess of $25

million can elect ADS depreciation deductions instead

o 40-year tax life for commercial rental real estate

o 30-year tax life for apartments/single rental residences

o 20-year tax life for QIP

o Real estate developers that elect ADS depreciation will not be

able to take bonus depreciation

15Beginning 1/1/2018 – New Like-Kind

Exchange Rules

• Only commercial/investment real estate activities are

eligible for tax-free exchange treatment

• Personal property is no longer eligible

• If real property (building) has Section 1245 property

(personal property) embedded, especially pursuant to a

cost segregation study, that portion of the property is

ineligible for Section 1031 tax-fee treatment

• Important to determine the value of Section 1245 property

embedded in real property upon pursuing a Section 1031

exchange

• Cost segregation studies on the replacement property,

identifying Section 1245 personal property, with 100%

bonus depreciation expense (especially on used property)

should assist in minimizing the impact to this tax-free

treatment limitation 16Effective 1/1/2018 through

12/31/2025 – New Loss Limitation

• $500,000 Trade or business loss – new annual

loss limitation

• Losses incurred by trade or business activities

will continue to have basis limitations and the

historical passive loss limitations apply

• $500,000 (MFJ)/$250,000 (MFS/Single) loss

limitation

• Excess loss amounts will be carried forward

• Watch Cost Segregation Studies

17Cash Basis Method of Accounting –

Reminder for Commercial Real Estate

Activities

• The new 1/1/2018 $25 million revenue threshold does

not apply to commercial rental real estate ventures

• Since rental real estate ventures do not have inventory,

the cash basis method of accounting is generally available

to pass-through commercial rental real estate ventures

regardless of the level of sales revenue

• Syndicates are generally required to use the accrual basis

method of accounting

If 35% or more of the commercial rental real estate

venture is owned by passive investors, and losses

exist, generally, the activity must be accrual basis

method of accounting

181/1/2018 - Reduced C-Corporate Tax

Rate

• Reduced Tax Rate:

– Tax years beginning after December 31, 2017, all C-

Corporations, including personal service corporations,

will be taxed at a 21% flat corporate tax

– Graduated rate structure is eliminated

– Corporate AMT repealed

– Any unused AMT credit carryforward is refundable

beginning in 2018 – refundable credit is equal to 50% of

excess of the credit over amount allowable against the

regular tax liability (100% beginning in 2021)

191/1/2018 Other New Tax Reform Rules

• Watch for new built in loss rule - applies if

$250,000 loss is allocated to an incoming

member

• Most individual income tax rates are lowered,

and the top marginal rate is reduced from 39.6%

to 37%

– Expires 12/31/2025

• The Tax Reform Bill still permits individuals to

itemize and deduct state and local taxes

(including property taxes), but only up to $10k

20Kentucky State Tax Update

• House Bills 366 & 487 – broaden tax base

• Effective 1/1/18 – Flat 5 % on business &

individuals

• Effective 7/1/18 – Sales tax on services

– Landscaping & lawn services

– Janitorial services

– Labor charges on installation of tangible personal

property

– Others

2122

Rental Real Estate Depreciation

Effective 1/1/2018:

• 39 year and 27 ½ year tax lives maintained

• Special real property depreciation categories

eliminated, except for Qualified Improvement Property

(QIP)

• Section 179:

– $1 Million per year, beginning 1/1/2018

– $500k per year through 12/31/2017

23New Bonus Depreciation %’s -

through 12/31/2027

Bonus Depreciation Rates

09/11/01 – 05/05/03 30%

05/06/03 – 12/31/04 50%

01/01/05 – 12/31/07 0%

01/01/08 – 09/08/10 50%

09/09/10 – 12/31/11 100%

01/01/12 – 9/27/17 50%

9/28/17 – 12/31/22 100%

01/01/23 – 12/31/27 80% - 20%

• Watch property with construction contract prior to 9/28/2017

• Property no longer needs to be “new,” beginning 9/28/2017

24100% Bonus Depreciation

9/28/2017 through 12/31/2017:

• Normal qualified real estate categories remain through

12/31/2017, along with their historical tax lives –

– Qualified Leasehold Improvement Property (“QLHI”)

– Qualified Improvement Property (“QIP”)

– Qualified Restaurant Property and Qualified Retail

Property

• Used commercial property is now eligible for bonus

depreciation, beginning 9/28/2017

• QLHI and QIP property that is acquired during the above-

referenced period of time is now eligible for 100% bonus

depreciation 25100% Bonus Depreciation

9/28/2017 – 12/31/2027:

• Embedded personal property/section 1245 property

acquired during this period of time, pursuant to a cost

segregation study, qualifies for 100% bonus

depreciation, new and used

• You can elect a lower 50% or 0% bonus depreciation

rate, per class – effective 9/28/2017

26Bonus Depreciation Phase Out

• 100% Bonus depreciation 1/1/2018 -12/31/2022

• Bonus depreciation is scheduled to phase-out

beginning 1/1/2023

• The only qualified real estate property provision that

survived, beginning 1/1/2018, is QIP

• QIP’s tax life is now understood to be 15 years

Note: There is an anticipated Technical Correction to be

issued to permit the tax life of QIP at 15 years and make it

eligible for bonus depreciation

27Section 179

• Beginning 1/1/2018 is $1 million/year

• Certain non-residential real property items qualify (QIP,

HVAC, roof, security systems, and fire protection

systems)

NOTE: Normal Section 179 limitations apply. You need

formal trade or business income; commercial rental real

estate income typically does not qualify for Section 179

unless rising to the level of a formal trade or business

activity

28Rev. Proc. 2015-56 – New Retail &

Restaurant Remodel – Refresh Safe Harbor

• Taxpayers engaged in the trade or business of operating a

retail establishment or restaurant with safe harbor

method of accounting - audited financial statements

• Includes owners of shopping centers or corporate office

with retail shopping

• Not included: 1245 property, automotive dealers, other

motor vehicle dealers, gas stations, manufactured home

dealers, nonstore retailers, hotel and motel business

operators, civic or social organizations, amusement parks,

theaters, casinos, country clubs, caterers

29Rev. Proc. 2015-56 – New Retail &

Restaurant Remodel – Refresh Safe Harbor

• 75% deduction of “qualified costs,” remaining 25%

capitalized and depreciated

• No disposition of prior costs capitalized

30Qualified Leasehold Improvement

Property

• Any improvement to an interior portion of a

building that is nonresidential real property;

excludes enlargements, elevators/escalators,

common area work and internal structural

framework

• Recovery period: 15 years

• Straight line method; half-year convention

• Can be included in Section 179 deduction – if

trade or business

31Qualified Leasehold Improvement

Property

• Eligible for 50% bonus depreciation

• 3 year rule applies - placed in service more than three

years after the date the building was first placed in

service

• Landlord or lessee can make interior improvement but

must be made pursuant to a lease

• Landlord and tenant cannot be related parties

• Expires 12/31/2017

32Qualified Restaurant Property

• Any section 1250 property that is a building - new

building or existing structure - or an improvement to a

building,

• If more than 50% of the building’s square footage is

devoted to the preparation of, and seating for on-

premises consumption of, prepared meals

• Recovery period: 15 years

• Straight line method; half-year convention

33Qualified Restaurant Property

• Can be included in Section 179 deduction – trade or

business – normally tenant

• Not eligible for bonus depreciation unless qualified

leasehold improvement property 2015 or Q.I.P. in 2016

• 3 year rule does not apply - placed in service more

than three years after the date the building was first

placed in service

• Encompasses the entire building structure as well as

interior costs. Can be an acquired building

• Landlord and tenant can be related parties

• Expires 12/31/2017

34Qualified Retail Improvement Property

– Effective 1/1/2016

• Any improvement to an interior portion of a

building which is nonresidential real property.

Retail establishments that qualify include those

open to the public and primarily in the business of

the sale of goods (tangible personal property) to

the general public and not services (grocery stores,

clothing stores, hardware stores, and convenience

stores)

• Recovery period: 15 years

• Straight line method; half-year convention

• Can be included in Section 179 deduction – trade or

business

35Qualified Retail Improvement Property

– Effective 1/1/2016

• Now eligible for 50% bonus depreciation

• 3 year rule applies - placed in service more than

three years after the date the building was first

placed in service

• Excludes enlargements, elevators/escalators,

common area work, and internal structural

framework

• Landlord and tenant can be related parties

• Building can be owner occupied

• Expires 12/31/2017

36Qualified Improvement Property –

Effective 1/1/2016

• New category – 1/1/2016

• Qualified improvement property is any improvement to an

interior portion of a building that is nonresidential real

property if the improvement is placed in service after the

date the building was first placed in service, excluding:

enlargements, elevators/escalators, and internal structural

framework

• The improvements do not need to be made pursuant to a

lease, and the building can be owner occupied

• 39 year tax life, through 12/31/2017

• 15 year tax life, beginning 1/1/2018 – Technical Corrections

37Qualified Improvement Property

• Straight line method; mid-month convention

• Can be included in Section 179 deduction – trade or

business

• Eligible for 50% bonus depreciation

• 3 year rule does not apply - placed in service more

than three years after the date the building was first

placed in service

• Excludes enlargements, elevators/escalators, common

area work, and internal structural framework

• Landlord and tenant can be related parties

• Building can be owner occupied

38Section 179 – Commercial Rental

Real Estate

Through 12/31/2017:

• Section 179 deductions of $510,000 with a phase out

starting at $2,030,000

• Trade or Business only

• A deduction of $510,000 of Qualified Real Property

(Qualified Leasehold Improvement Property, Qualified

Restaurant Property, and Qualified Retail Improvement

Property) is retroactive for 2017 – Max $510,000

3940

Historic Tax Credit

• Historic Tax Credit (HTC):

– The 10% credit was repealed for pre-1936 buildings

– The 20% credit for Qualified Rehabilitation Expenses

(QRE) was retained with a modification.

– The credit allowable over a 5-year period

– Making the credit 4% per year of the QREs

411/1/2018 New HTC Rules, continued

Transition rule to determine if the HTC is claimed

under the old law:

– Was the full 20% in the year placed in service or

under the new law, 4% per year over 5 years

– The taxpayer has a 24- or 60-month window to

claim expenditures during rehabilitation

– If the taxpayer selects to start the window outside of

180 days after December 22, 2017, then the new

law applies, otherwise the old law is still in effect

4243

Qualified Opportunity Zones

• Enacted as part of sweeping federal tax legislation commonly referred to as

the Tax Cuts and Jobs Act of 2017.

• Significant tax incentives for taxpayers to reinvest capital gains in certain

property and businesses located or operating in specially designated tracts.

(“QO Zone”).

• Encourage economic development in “low income areas” by providing various

tax incentives for private investments in qualifying areas

• Estimated $6.1 trillion in unrealized capital gain at the end of 2017.

• This significant amount of capital available for reinvestment makes the QO

Zones program potentially the largest economic development initiative in the

country.

• Designed to channel more equity capital into distressed markets

44Opportunity Zone Designation

• Treasury has designated QO Zones in all 50 states, the

District of Columbia, and five U.S. possessions.

– In Kentucky, Treasury designated 144 low-income census tracts in 84

counties across the state as QO Zones.

• 19 designated QO Zones in Jefferson County.

• 2 designated QO Zones in Bullitt County.

– In Indiana, Treasury designated 156 tracts in 58 counties covering all or

portions of 83 cities and towns throughout the state as QO Zones.

• 5 designated QO Zones in Clark and Floyd counties.

• The zones will effectively not change

• IRS has a listing by state

• States have websites for confirming QOZ locations

45Designated O Zones in Kentucky Source: http://www.thinkkentucky.com/OZ/ 46

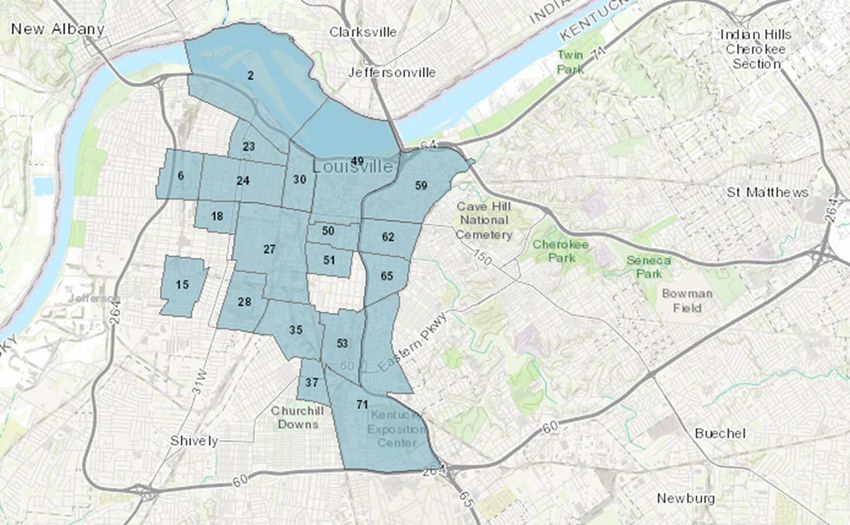

Designated O Zones in Louisville Source: https://louisvilleky.gov/government/louisville-forward/opportunity-zones-louisville47

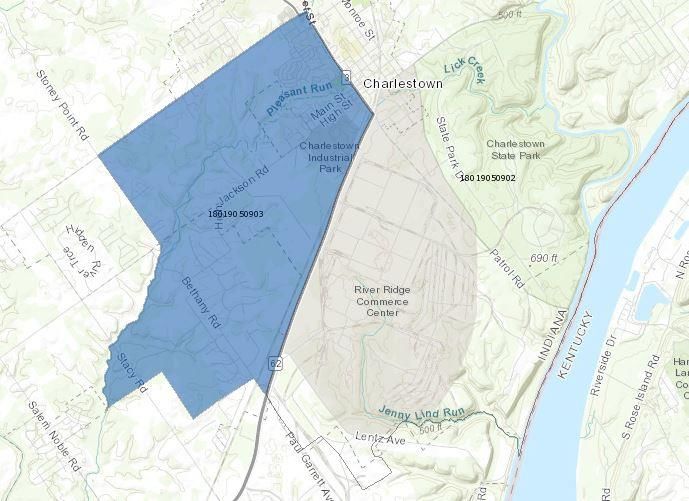

Designated O Zones in Southern IN Source: https://www.cims.cdfifund.gov/preparation/?config=config_nmtc.xml 48

Designated O Zones in Southern IN Source: https://www.cims.cdfifund.gov/preparation/?config=config_nmtc.xml 49

QO Zone Benefits

Qualified Opportunity

Zone Funds (QOFs)

Defer taxes by making when invested in

timely investments

Taxpayers Qualified Opportunity

Zone Property

50QO Zone Benefits

There are three separate investment incentives that a taxpayer can elect to

take advantage of with respect to their investment.

1. Initial gain deferral

2. Partial forgiveness

3. Permanent exclusion of gain

on appreciation

51Gain Recognition

• Gain deferral is temporary because the taxpayer

must recognize the income in the tax year the

investment is sold or the tax year that includes

December 31, 2026, whichever is earlier.

• Gain is calculated as the lessor of:

1. Amount of gain deferred

OR

2. The fair market value of investment in QOF interest less

the basis in the QOF interest *

* Basis is QOF is initially deemed to be zero

52Deferral Period

The period of capital gain tax deferral ends upon the

earlier of:

53Partial Forgiveness and Permanent

Exclusion of Additional Gains

Basis increased by Basis increased by Basis is equal to

10% of the deferred Additional 5% of the Fair Market Value

Within

180 Days gain deferred gain

Exclusion of

Up to 90% taxed Up to 85% taxed gains on appreciation

of investment

54Example

April 28, 2029

April 28, 2026 (10 years) Taxpayer

(7 years) Taxpayer’s sells its investment for

Before April 28, 2019 basis in investment in $3M. The basis is equal

Taxpayer contributes QOF makes a timely investment of QOF increases another to the FMV. No

the $1M of capital gain the $1M in Qualified Opportunity 5% from $100k to additional tax is owed

to a QOF Zone Property $150k on the appreciation.

Oct. 30, 2018

April 28, 2024

Taxpayer enters into a December 31, 2026

(5 years) Taxpayer’s basis

sale that generate $1M $850k of the $1M of

in investment in QOF

of capital gain initial capital gains are

increases 10% from $0 to

$100k taxed and the basis in

QOF investment

increases to $1M

Notes:

• The Taxpayer’s initial basis is deemed to be $0 in the QOF investment

55Investment Types in Opportunity Zones

Real Estate New Businesses created in

Development and Rehab Project Opportunity Zones

in Opportunity Zones

Expansion of

Businesses already Businesses expanding into

in Opportunity Zones Opportunity Zones

56Qualified Opportunity Fund - Purpose

• A QO Fund is any investment vehicle organized as either a

partnership (including an LLC treated as a partnership for

tax purposes) or corporation that was formed for the

purpose of investing in qualified opportunity zone

property (“QOZ Property”).

• At least 90 percent of the QO Fund’s assets must consist

of QOZ Property.

• Fund can self certify

57Qualified O Zone Property

There are three categories of QOZ Property permitted:

1. Qualified Opportunity Zone Stock

(Qualified Opportunity Zone Business)

2. Qualified Opportunity Zone Partnership Interest

(Qualified Opportunity Zone Business)

3. Qualified Opportunity Zone Business Property

58Qualified O Zone Stock and

Partnership Interests

• The investment must be acquired after December 31, 2017

solely in exchange for cash;

• Must be a qualified opportunity zone business, or is being

organized for the purpose of being a qualified opportunity zone

business;

• Must remain a qualified opportunity zone business for

substantially all of the qualified opportunity fund’s holding

period

59Qualified O Zone Businesses

• A trade or business in which substantially all of the tangible

property owned or leased by the taxpayer is qualified o zone

business property

• At least 50% of income derived from active conduct

• Less than 5% of unadjusted basis of property is nonqualified

financial property

60Ineligible Businesses

“Sin Business”

Golf courses Country clubs

Race tracks Massage parlors

Gambling facilities Hot tub facilities

Liquor stores Tanning facilities

61Qualified O Zone Business Property

• Tangible property used in a trade or business

• Acquired by purchase from an unrelated party (20% threshold) after

December 31, 2017

• During substantially all of holding period, substantially all the use is in a QOZ

• Substantially all is defined as 70%

• Original use in the QOZ commences with the taxpayer

• OR

• Taxpayer substantially improves the property

• during any 30-month period after acquisition, additions to basis exceed an amount equal to the

adjusted basis of such property at the beginning of such period

• Guidance allows for reasonable working capital

62Basic Model for Rental Real Estate

or direct ownership of

QOZ Business Property

within

180 days

Investors QOF QOZ QOZ

Partnership Business Property

Rental Real Estate

• New construction

• Substantial improvement of adjusted basis excluding land

63Civil Penalties for Noncompliance

• Failure to meet investment standard results in

per month penalty

• % of shortfall multiplied by underpayment rate

• No penalty if failure is due to reasonable cause

64Questions?

65IRS Circular 230 Disclosure

As a result of perceived abuses, the Treasury has

recently promulgated Regulations for practice before

the IRS. These Circular 230 regulations require all

accountants to provide extensive disclosure when

providing certain written tax communications to

clients. In order to comply with our obligations under

these Regulations, we would like to inform you that any

advice given in this presentation, including any

attachments, cannot be used to avoid penalties which

the IRS might impose, because we have not included all

of the information required by Circular 230, nor have we

performed services that rise to this level of assurance.

66Thank You!

Stephen M. Lukinovich, CPA, PFS, CVA

Stephen.Lukinovich@mcmcpa.com

Andrew J. Ackermann, CPA, CVA

Andy.Ackermann@mcmcpa.com

502.749.1900

www.mcmcpa.com

67You can also read