2020 BOLD MOVES African Emergence - Sanne Group

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

SANNEGROUP.COM

Issue 20 | March 2020

2020 BOLD MOVES

African Emergence

> South Africa’s growth outlook for 2020

> Mezzanine debt – the overlooked asset class

> Securitisation in Africa

> New classification standard for hedge funds

> Private equity firms continue targeting South Africa, new

opportunities and trends for 2020 and beyond

1 / 18 MAKING THE DIFFERENCE FOR OUR CLIENTS

SANNEGROUP.COM

Welcome to our 20th issue of Connect, bold moves bringing with it significant opportunities in the

SANNE’s regular, technical bulletin for fund coming decade is, renewable energy projects.

managers, their intermediaries and

Given the opportunities present in Africa, this edition of

investors.

SANNE Connect invited industry leaders to share their

Leading the way thoughts on Africa and the way forward.

Africa is showing great potential with the expectation for

Africa edition – our experts:

growth across the continent to be 3.9% in 2020 and 4.1% in

2021 with economic progress continuing to outperform that > Erik Nel, Chief Investment Officer at Terebinth Capital

of other regions. Bringing home the Webb Ellis Cup last year

> Adam Bulkin, Head: Manager Research at Sanlam

indeed brought us good fortune as Africa is destined to be

Investments: Multi-Manager

home to seven of the world’s ten fastest-growing economies

over the next five years. > Ryan van Breda, Portfolio Manager at Ngwedi Investment

Managers

Markets upbeat in 2020, but are storm clouds gathering?

> Karlien de Bruin, Head of SANNE ManCo

Having just come out of Cape Town’s ‘Day Zero’ situation, I

for one am always optimistic when the storm clouds gather. > Michael Denenga, Partner and Private Equity Specialist at

Fundamentals are improving with a gradual shift from private Webber Wentzel

consumption toward investment and exports. Achieving Enjoy the read!

sustainable development goals remain key and will shape

policy priorities for African Governments. Tangible

achievements in health and education have been noted,

however, service delivery and infrastructure have lagged, Graeme Rate

primarily due to funding gaps which is presenting new Country Head – South Africa and Malta

opportunities for long-term investors. One sector making graeme.rate@sannegroup.com

2 / 18 MAKING THE DIFFERENCE FOR OUR CLIENTS

SANNEGROUP.COM

KEY TOPICS

> Could we face another recession?

> What do rating agencies predict for

South Africa?

> Are emerging markets at risk of

running large bills?

South Africa’s growth outlook

Global expectations for 2019 were that trade tensions will It’s not all doom and gloom

ease, the global economy will pick up and that the US dollar

In South Africa, 2019 looked a little different. Adverse

will weaken. In reality, 2019 was characterised by a tug of war

macro news headlines hardly impacted markets. Negative

between substantial geopolitical drags and global monetary

rating outlook changes, a very disappointing mid-term

policy easing.

budget policy statement (MTBPS), load shedding,

After eight uninterrupted interest rate hikes by the Fed and crumbling SOEs and infrastructure, service delivery

markets pricing a further four hikes for 2019, a sharp selloff in protests, policy uncertainty, political infighting, and

December 2018 led to major Fed and market capitulation in bailouts and stagnation could not prevent the All Share

January 2019. Despite this reversal, a third slowdown of the Index of returning 12%, Implats almost tripling in value,

growth momentum took hold mid-year, once again creating Sibanye Gold more than doubling in value and Amplats

concerns about the timing and cause of the next recession. growing in excess of 150%. Not to be outdone, the All-Bond

Ironically, despite all these concerns, almost every asset class Index returned an impressive 10.3%.

delivered good returns in 2019.

US-China trade war vs Brexit

We expect that the two major political headaches that

Erik Nel

dominated most of 2019 – the US-China trade war and Brexit –

Chief Investment Officer

will have less impact in 2020. Now the question is whether

at Terebinth Capital

proactive global stimulus will result in growth stabilising at

erik.nel@terebinthcapital.com

current levels and potentially rebound, or whether ongoing

political concerns and the more recent arrival of the Covid-19

virus can bring an end to one of the longest economic

expansions in history.

3 / 18 MAKING THE DIFFERENCE FOR OUR CLIENTS

SANNEGROUP.COM

National Treasury recently acknowledged investors’ Keeping the rating agencies at bay

nervousness when it commented:

An environment of slowing growth and falling inflation

should usually provide for easy decisions around

monetary stimulus. Yet, to date, the South African

“National Treasury is alive to the great

Reserve Bank (SARB) has been reluctant to cut interest

anticipation for the 2020 Budget Speech

rates. A much lower policy rate seems dependent on

where we are expected to outline details

confirmation of tougher fiscal measures and policy

around fiscal consolidation measures

implementation. Fixed income managers will need to

particularly relating to Eskom and the Wage

appreciate both the nuance of monetary policy and the

Bill. Relevant Government departments will

implications of better or worse fiscal conditions in

be working very hard in the coming weeks to

2020.

meet these expectations where possible.

Again, Government would welcome all If the Government and key stakeholders adopt the

support available to move us forward.” resolutions and savings proposed in the MTBPS and

National Treasury’s economic transformation plan, then

a Moody’s rating downgrade can be averted. The

The IMF highlighted potential challenges the Treasury could President’s 2020 State of the Nation address and the

face: National Budget release were key inputs in Moody’s

pending rating decision, as it reflects the extent of the

Government’s commitment to fiscal consolidation and

“A more decisive approach to reform is implementation of reforms outlined in National

urgently needed. Impediments to growth Treasury’s growth paper.

must be removed, vulnerabilities addressed,

and policy buffers rebuilt. Expediting At present, consensus expectations are firmly biased

structural reform implementation is the only towards a Moody’s downgrade in 2020. Markets also

way to sustainably boost private investment seem to be more aware of further downgrades (deeper

and inclusion.” into sub-investment grade) by S&P and Fitch and the

impact this could have on funding costs and growth

risks to the economy.

4 / 18 MAKING THE DIFFERENCE FOR OUR CLIENTS

SANNEGROUP.COM

The risks are very real The role of hedge funds in building a volatility-

proof portfolio

While investors are aware of Eskom, budgets, rating

agencies, global index rebalancing, elections, We have suggested for some time that investors start

impeachments, populist tendencies, unrest and geopolitics building volatility-proof portfolios. Volatility has been

in general, we need to understand that a spread of more constrained by the proliferation of some investment

than 800bp over US Treasuries, 600bp over South African strategies, but as market expectations adjust,

inflation-linked bonds and a very attractive spread over unexpected volatility spikes are set to become more

cash, nominal Government bonds are hard to pass over. The frequent. To volatility-proof portfolios, investors should

caveat is that Government turns the fiscal ship around. A consider liquid alternative strategies that offer low

further increase in bond issuance or a sovereign rating correlations to traditional asset classes. Hedge fund

downgrade will lead to even more attractive yields on offer. managers with a proven ability to manage volatile

markets, protect the downside and generate

While proactive global stimulus in 2019 appeared to lower

incremental alpha are well placed to provide solutions

recession risks coming into 2020, global impact of the Covid-

in this regard.

19 virus, the upcoming US election, the rise of

deglobalisation and a mature credit cycle with rising liquidity

concerns once again pose risks. “As the Warren Buffet saying goes, predicting

rain doesn’t count, building arks does.”

A major theme to track in 2020 is the anti-establishment/

populist wave that continues to sweep the world, aided and

fanned by social media. Governments are increasingly Risk managers understand that markets face multiple

coming under extreme pressure from populations frustrated outcomes. Tactical, as well as fundamental awareness

with economic inequality, disenfranchisement, corruption will be more important in 2020. Alongside alpha

and fiscal austerity. generation, a reputable manager’s arsenal in 2020 will

have to include strategies that can benefit from positive

A dominant question on the election front is how the US

carry conditions and matching beta when required,

voting will impact the dollar and broader markets.

while being able to manage downside risks as they

Another concern is the explosion in debt during the post- prevail.

crisis period, resulting from falling inflation and record low,

sometimes negative, interest rates. A material weakening in

currencies, and a subsequent rise in inflation, could trigger a

major sell-off in developed market interest rates and

attendant crises in countries that run large current account

and/or budget deficits. Many of the countries that fall into

these categories are emerging markets and are at risk of

running up large bills to address the global climate crisis.

5 / 18 MAKING THE DIFFERENCE FOR OUR CLIENTS

SANNEGROUP.COM

KEY TOPICS

> Is there appetite for mezzanine

debt in Africa?

> What are the cash distribution

expectations?

Mezzanine debt

The overlooked asset class

An asset class within the alternatives category which Interest payments are usually linked to the Johannesburg

does not seem to attract the same attention as others, Interbank Average Rate (JIBAR), and split between cash

particularly in Africa, is mezzanine debt. There are payments and payment in kind debt, which is payable in

relatively few mezzanine debt managers, and this cash if there is sufficient surplus to do so, or rolled up and

could be ascribed to a lack of knowledge and demand payable at the end of the loan term.

from the institutions which would be the natural

investors in this asset class. The equity participation is by way of a preference share,

warrant or similar type of contractual obligation. The value

The nature of mezzanine debt of the equity is usually determined by using a pre-agreed

valuation methodology. Thus, unlike private equity,

Mezzanine debt is a hybrid asset class with both fixed mezzanine debt investments have a definitive exit date,

income and equity-like characteristics. It targets valuation approach and more definitive cash distribution

equity-like returns, with debt-like risk. expectation.

When the mezzanine debt fund extends a loan to a

borrower, the borrower is obliged to repay the

principal amount of the loan plus interest, but in

addition, the fund becomes entitled to participate, to a Adam Bulkin

certain extent, in the equity of the borrower. The debt-

Head: Manager Research

like returns are achieved through the interest payable Sanlam Investments: Multi-Manager

on subordinated debt owed by the borrowing

adambu@sanlaminvestments.com

company, to which contractual obligations on the part

of the borrowing company are attached.

6 / 18 MAKING THE DIFFERENCE FOR OUR CLIENTS

SANNEGROUP.COM

Mezzanine debt’s capital

structures and its return may

be illustrated as follows:

Corporate All-in Exposure Comprehensive Alignment Valuation Board

Covenants

Structure Return to Upside Security of Interest Uncertainty Involvement

Equity

>25% 100% No No Yes Yes, at Exit Yes

20%

No, exit

15% - 25%

Mezzanine Up to 25% valuation

(>Jibar + Always (at least Yes

Debt of equity Comprehensive Yes multiple is

6.00% 2nd ranking) (observer)

30% upside predetermined

plus equity)

upfront

9.5% - 13%

Senior Debt Always

(Jibar + 250 0% Comprehensive No Not Applicable No

50% (1st ranking)

– 550bps)

An example of the return components of mezzanine debt is as follows:

Observations:

Original

Investment Yr1 Yr2 Yr3 Yr4 Yr5 > Contractual interest, enforceable downside protection,

and equity related upside

16.4%IRR

Equity Kicker = R11,75m > The equity kicker is typically structured as a self

PIK interest at exit = R6, 41m liquidating instrument

Final cash interest income = R2,75m

> Unlike private equity, mezzanine investments have

Interest Principal repayment = R32m

Fee Income a definitive exit date

R0,32m R2,37m R2,47m R2,56m R2,66m

Aggregate: Cash Flows R’000 Pot of Flows

Principle Investment R32m

Value of Equity Kicker 11,756 38%

PIK Interest at exit 6,407 21%

Original Investment Fee Cash Pay Interest PIK Interest Paid Equity Cash Interest 12,814 41%

Total Non-Principal Cash Flows 30,977 100%

60% - 70% of investment returns are contractual

Source: Ashburton Investments

7 / 18 MAKING THE DIFFERENCE FOR OUR CLIENTS

SANNEGROUP.COM

Various uses of mezzanine debt > Leverage recapitalisations

Private equity investors can improve their returns on existing

Mezzanine debt fills a gap between senior and equity

investments by using mezzanine debt to refinance and re-

funding. Traditionally, the major banks and life

leverage existing debt structures, thereby providing the

insurance companies played a key role in providing this

opportunity for early IRR-enhancing returns on capital.

type of capital. Since the global financial crisis and the

implementation of Basel Regulations, such entities > Leverage or management buy-outs

have reduced this type of debt financing while demand Management teams and private equity investors can use

continues to build in leverage buyout, BEE and mezzanine debt to enhance their returns on new

infrastructure financing transactions. There is investments by reducing the amount of equity they need for

therefore a demand for mezzanine debt, but it is in a given opportunity.

limited supply, which presents attractive opportunities

> Refinancing of secondary BEE transactions

for those willing to provide such capital.

This is where an existing BEE investment has reached

In more specific detail, there are demands for maturity and the corporate entity is required to enter into a

mezzanine debt in the following types of new BEE transaction. According to Intellidex, as at

transactions in Africa. 1 January 2015, on the Johannesburg Stock Exchange (JSE)

alone, there were outstanding BEE transactions amounting

> Entrepreneur-partnering transactions

to R209.2 billion. Live deals had an average duration of 6.8

These are transactions in which capital is provided in

years as at 1 January 2015, indicating that a large number of

support of established entrepreneurs in profitable

these transactions are close to maturity. Given that banks

businesses that are positioned to take advantage of

have moved away from funding these transactions due to

organic growth and acquisition opportunities, including

the implementation of Basel III, this refinancing activity

platforms for build-up strategies. Mezzanine funding is

provides a significant opportunity for mezzanine debt.

more suitable for entrepreneurs that are not yet ready

to exit or dilute their equity due to growth prospects but > Energy transactions, both primary and secondary provide

would like to have a partner with capital and the ability attractive risk return profile opportunities

to assist with funding that growth strategy. Mezzanine financing can help strengthen a project’s equity

profile because of its flexibility compared to senior debt

> BEE transactions

finance. Mezzanine finance is also attractive as it can lower

This has been one of the growth drivers of mergers &

the cost of financing a project compared to pure equity

acquisitions and private equity investments in South

financing. Mezzanine financing into infrastructure is

Africa and this trend is expected to continue. Working

attractive due to the stability of infrastructure assets through

alongside BEE investors, mezzanine debt provides

changing macro and credit conditions.

funding for BEE transactions.

> Growth capital

Mezzanine debt is less dilutive funding compared to

traditional sources of debt or equity capital (i.e. private

equity). This strategy can enable shareholders to

postpone raising further dilutive equity, achieving much

stronger valuations when they elect to exit later.

8 / 18 MAKING THE DIFFERENCE FOR OUR CLIENTS

SANNEGROUP.COM

Rationale for investing in mezzanine debt

From a global perspective, mezzanine debt presents a highly attractive risk return profile. According to Ashburton

Investments, in 2017 48% of international investors believed it offered the best risk-return profile in the private debt space

and this was supported by actual performance, as illustrated below:

According to research by René Biner and Dr. Michael Studer of Partners Group, in a paper titled ‘Mezzanine Investments:

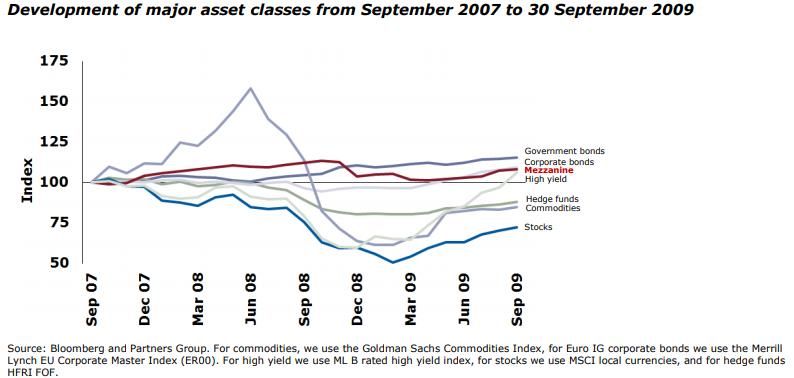

Stability through the storm’, mezzanine debt in Europe outperformed nearly all asset classes during the financial market crisis

from 2007 to 2009. The peak to trough drawdown of the asset class during the crisis was 11%, compared to many other asset

classes that were in the 50-60% range, highlighting the relative stability of mezzanine loans in the crisis. With 50% recovery

rates given default, a mezzanine lender can realise default rates on over half its portfolio and still not experience a loss of

principal. This is due to high historical recovery rates and high contractual coupon payments that generate significant interim

cash flows. This is illustrated below:

Source: Partners Group

9 / 18 MAKING THE DIFFERENCE FOR OUR CLIENTS

SANNEGROUP.COM

Based on their observations through the 2007 to 2009 period, Biner and Studer concluded that, “on a risk-adjusted basis,

mezzanine debt is one of the most attractive investments in the market. The primary characteristics which have enabled the

mezzanine debt asset class to achieve this attractive profile include: high contractual yields, relatively low default rates, high

recovery rates given default, favourable ownership dynamics, and greater control of protective legal documentation.”

Further evidence of the attractiveness of mezzanine debt is provided in the October 2018 paper titled Mezzanine Debt by

Todd Silverman, Mark Watson, John Haggerty and Frank Benham of Meketa Investment Group.

They provide the following risk and return metrics versus other US debt asset classes (reported in US dollars).

Mezzanine Performance vs. Other Private Debt (1997-2017):

Mezzanine Broadly Syndicated High-Yield Middle Market

Debt Loans Bonds Loans

Annualised Return 9.08% 4.90% 6.74% 6.24%

Standard Deviation 6.99% 8.50% 10.12% 6.98%

Sharp Ratio 1.02 0.35 0.47 0.61

Mezzanine Debt Correlations -- 0.46 0.44 0.45

The next growth wave is coming

Mezzanine debt is a valid and important component of a private market portfolio, with an attractive risk and return profile

that provides potential returns close to those offered by private equity, but in a more predictable and lower risk manner, with

a reduced “J-curve”, regular cash pay distributions, strong downside protection and self-liquidating equity-linked bonuses

which are redeemed at maturity at a predetermined valuation methodology.

10 / 18 MAKING THE DIFFERENCE FOR OUR CLIENTSSANNEGROUP.COM

KEYTOPICS

KEY TOPICS

> > What sectorsincreasing?

Is demand need developing?

Securitisation in Whatnew

> > What areavenues

the regulator’s

to explore.

views on securitisation?

> Ensuring digital platforms

South Africa What are

> support newthe liquidity risks?

services.

Securitisation is an off-balance sheet funding mechanism The regulations specify certain conditions for the disposal of

whereby cash-flow producing assets are pooled together and assets from the originator to the issuer SPV. In other words,

sold into a special purpose vehicle (SPV), a bankruptcy remove ensuring that a true sale of assets take place, including

company. The SPV will fund the purchase of these cash-flow conditions in relation to credit enhancement facilities and

producing assets by issuing various tranches of rated notes (AAA liquidity facilities. In addition, the regulation also provides

all the way to B), to institutional investors in capital markets. requirements on the ownership and control of the issuing

The nominal value of the notes, as well as the coupon rate of entity, being the SPV.

the notes, are paid from the underlying cash-flows from the

Asset classes

assets in terms of an agreed cash-flow waterfall.

The most dominant asset class remain residential mortgage-

Regulation of securitisation

backed home loans, but the local market also includes

The legal framework for securitisations is currently governed by instalment leases, equipment leases, commercial

regulations issued under the Banks Act of 1990 published in mortgages, vehicle asset financing and consumable

Government Notice 2, Government Gazette 30628 of 1 January receivables. Generally, the securitisations in our market are

2008. These regulations exempt an issuer SPV from the true-sale physical transactions and not synthetic

obligation to register as a bank, provided that the transaction is transactions.

implemented in accordance with these regulations.

Synthetic transactions gained great traction in the global

markets in 2007 (where they included mortgages on sub-

prime loans). These securitisation vehicles did not own the

underlying physical assets but entered into a series of credit

default swaps (CDS) with the originator of the underlying

asset and repacked a pool of these CDS to investors. This

was generally known as a CDO.

11 / 18 MAKING THE DIFFERENCE FOR OUR CLIENTSSANNEGROUP.COM

It’s good to see that the South African regulator is shying away We believe that liquidity will over time improve as more

from approving synthetic securitisations, which does give investors come to market, but the main reason for the

confidence to the South African market as a whole. The focus in current limited liquidity is because the originating banks are

South Africa is on securitisation as a funding mechanism rather not allowed to make a market in its self-securitised assets

than capital relief. under the current South African regulations. We do find this

perplexing given that for liquidity purposes, self-secured

Pricing and performance

assets are posted as collateral to the South African Reserve

Over the past few years the South African listed credit market Bank (SARB) for drawing down under the committed

continued to see credit spreads grinding lower. Five years ago, liquidity facility (CLF).

5-year senior floating bank bonds priced at around 3 million

The CLF was created to offer the local banking industry the

Jibar +1.60%, whereas now 9-year senior floating bank bonds

ability to borrow money from the SARB to meet the

price at around the same level. Securitisations are starting to

requirements of the Basel III Liquidity Coverage Ratio given

show significant spread compression, but currently offer a

the shortage of high-quality liquid assets.

relative yield pickup - relative to other good quality credits

available in the market, where we believe the underlying The Association of Savings and Investment of South Africa’s

collateral to be of the same quality due to an illiquidity Fixed Income Standing Committee is currently in discussions

premium. with the Prudential Regulatory Authority regarding

amendments to the regulations which will allow originating

The performance of the underlying pool of assets held in the

banks to retain notes for the purposes of making a market

securitisation vehicles has been good over many credit cycles,

without compromising legal true sale. Over time this will

with no losses to noteholders recorded in the South African

increase liquidity which will attract a greater pool of

market.

investors to the market.

In the current market, liquidity is thin but is improving as more

investors consider the asset class. We believe that this is one of

the reasons why investors price the notes higher, not

necessarily for their inherent risk but for their liquidity. Ryan van Breda

Portfolio Manager

Ngwedi Investment Managers

ryan@ngwedi.com

12 / 18 MAKING THE DIFFERENCE FOR OUR CLIENTSSANNEGROUP.COM

KEYTOPICS

KEY TOPICS

> > What

Whatsectors

are theneed

newdeveloping?

classifications

> What new avenuesandto

impact on

explore.

managers?

> Ensuring digital platforms

> Is there any additional

support new services.

benefit?

ASISA Hedge Fund

Classifications

– positive move for the hedge

fund industry in South Africa

The hedge fund industry has grown substantially since the first Classification tiers for asset managers

hedge fund was established in 1949. The array of investment

strategies have now expanded to include traditional asset The ASISA Hedge Fund Classification Standard provides

classes, more esoteric strategies such as currency trading, four tiers of classification. The first tier splits hedge funds

derivatives (futures and options) on financial indices, into the type of portfolio, i.e. either Retail Hedge Funds or

commodities and even outliers like weather and funds trading in Qualified Investor Hedge Funds. This is the most

physical assets such as art and wine. fundamental split as it is aligned to the schemes that are

currently enacted in the legislation.

The number of operating hedge funds in the market have grown

significantly, which makes it hard for investors to compare, The second tier classifies hedge funds according to their

analyse and select the appropriate hedge fund or combination geographic exposure. This geographic exposure classifies

of hedge funds to execute their investment strategy, hence the funds as South African, worldwide, global or regional.

need for a standardised classification methodology. The third tier classifies hedge funds according to the

Importance for investors investment strategy of the portfolio, represented by the

asset class from which returns are predominantly

It is important for investors to know what assets a fund is generated.

investing in to generate its returns and the risk profile taken to

achieve these returns, prior to making their investment These have been classified into long short equity, fixed

decisions. income, multi-strategy, and other, i.e. funds that invest in

other assets such as property, commodity or other

ASISA (Association for Savings and Investments South Africa), physical assets.

the industry membership body that represent the interests of

the South African investment community, recently released a The fourth tier only applies to the Long Short Equity

Hedge Fund Classification Standard. The aim of the standard is Hedge Fund classification as this asset class covers a wide

to classify all hedge funds into different categories to make it variety of equity driven funds. The fourth tier expands the

easier for investors to assess and compare funds and select Long Short Equity class further into long bias equity hedge

hedge funds appropriate for their risk profiles and investment funds, market neutral hedge funds and other equity.

appetite. The standard came into effect on 1 January 2020. Hedge fund managers are now obliged to include this

fund classification on their fund fact sheets.

13 / 18 MAKING THE DIFFERENCE FOR OUR CLIENTSSANNEGROUP.COM

Benefits for the industry

With these classifications as a backbone, investors can now

compare and analyse hedge funds in each category and match

their own risk appetite and objectives with that of the hedge

fund universe, much easier.

In addition, ASISA will for the first time be able collect and

compare its own data on the hedge fund industry in South

Africa. This in itself will be a huge benefit for the asset

management industry in South Africa, as the industry will now

have access to local statistics and trends to use in their

investment decision making.

SANNE’s management company is a leading provider of hosted

ManCo services to the long and hedge fund industries. Our team Karlien De Bruin

is working with hedge fund managers to implement the new

Head of ManCo, SANNE

classification standard into their investment reporting

processes. karlien.debruin@sannegroup.com

Congratulations to our clients

2020 Hedge News Africa Award Winners*

Long Short Equity Fund of the Year Multi Strategy Fund of the Year

Anchor Accelerator SNN QI Hedge Fund Fairtree Wild Fig Multi Strategy SNN QI Hedge Fund

Market Neutral and Quantitative Fund of the Year Ten-year Performance – Single Manager

X-Chequer SNN Diplo QI Hedge Fund Polar Star SNN QI Hedge Fund

Five-year Performance – Single Manager (Joint Award) Fund of the Year 2019

Acumen AcuityOne SNN Retail Hedge Fund Fairtree Assegai Equity L/S SNN QI Hedge Fund

Fairtree Assegai Equity L/S SNN QI Hedge Fund

Pan Africa Fund of the Year

Gondo Visio Metsi Fund

14 / 18 MAKING THE DIFFERENCE FOR OUR CLIENTSSANNEGROUP.COM

KEY TOPICS

KEY TOPICS

> What are the trends and

opportunities in private equity?

> Will Mauritius continue being a

favourite for offshore funds?

What is in store for private equity

in Africa?

With experts predicting that South Africa's economy will We will see increased opportunities for investors to

grow by less than 1% in 2020, this year is likely to be participate in general partner led re-structures and

challenging. Although economic challenges will have an secondary deals to orderly transfer "long in the tooth"

effect on private equity (PE), the industry will most likely assets to alternative investors or structures.

show resilience, following the continued upward trend

seen over the last decade. There is however, speculations This is further pronounced by the exit challenges that some

that market conditions may bring about new trends and managers have experienced in recent years. Secondary

opportunities. buyout (sales to other PE firms) remain the most common

exit mechanism and we do not anticipate an increase in

What is on the horizon for 2020 conversions to listed funds, due to the illiquidity and high

transaction costs associated with African exchanges and

For 2020, the expectation is that PE in Southern Africa will the fact that the recently listed vehicles have been trading

once again perform admirably. Internationally, PE has at a significant discount to NAV. We can expect more exit

remained buoyant despite all signs that we are at the top opportunities from trade partners and selling to strategic

of the economic cycle. Globally, fundraising activity has partners including other PE managers.

remained high with almost US $2 trillion in global PE

capital available for investment, with large amounts of > Increased flexibility, innovation and transparency

these funds earmarked for emerging markets, including To attract capital and larger ticket sizes, we may see PE

sub-Saharan Africa (SSA). fund managers expanding their product ranges across

New trends and opportunities different asset classes and strategies in order to grow their

fee base, consolidate costs and minimise risks associated

Mitigating the effects of a strained local economy, we will with a single asset class or market.

likely witness new trends and opportunities for PE in 2020.

These expectations include the following: New product lines may well encompass private debt funds

which continue to grow in number each year given the lack

> Increased exit opportunities of available credit for small to mid-sized companies. In

Following political uncertainty and currency elasticity, keeping with a theme of flexibility, we also expect to see

some SSA fund managers have found themselves holding changes or adjustments in fund structuring or fund

more assets at the end of the fund life than what they documentation.

anticipated.

15 / 18 MAKING THE DIFFERENCE FOR OUR CLIENTSSANNEGROUP.COM

This is partly as a result of the Abraaj collapse which led In 2019, guidelines were put in place for defining and

the International Limited Partners Association (ILPA) to stress testing impact investing with the International

spearhead several investor friendly boilerplate provisions. Finance Corporation developing a set of nine operating

principles for impact management. The greater clarity

Transparency will also be key as investors push for more

provided by the guidelines should encourage asset

disclosure, enhanced due diligence, access to financial

managers and investors alike.

information and early step-in rights. This increased focus

on stewardship will provide opportunities for fund Fund domicile decisions

administrators to provide independent, third-party

Mauritius will most likely continue to be a favourite

oversight for fund managers that traditionally preferred to

jurisdiction for establishing offshore Africa focused funds.

do so in-house. More deal-by-deal structures may emerge

Although Mauritius received some criticism in 2018 from

as some managers will consider foregoing management

some quarters resulting in DFIs, increasing pressure on

fees for more frequent carried interest. We may also see a

managers to ensure that their operations in Mauritius had

hybrid of permanent capital and traditional funds as

substance; the OECD, the Dutch list and the European

managers look for ways to secure more time for value

Union have since then all confirmed that Mauritius is not a

creation in African markets while at the same time

harmful tax jurisdiction. Enhanced substance requirements

maintaining alignment in terms of fees and performance.

have also given DFIs greater confidence that managers that

> Impact investing choose Mauritius do so for commercial, rather than tax

reasons. We are, however, likely to see an increase in on-

The past two years have also shown that impact investing

shore fund structuring particularly in SA as more and more

does not negate profitability. Impact investing cuts across

DFIs take comfort in investing directly into SA for South

various asset classes and will provide managers with

African and Africa focused funds.

optionality in their quest to expand their product ranges.

According to the Africa Impact Report 2019, impact

investing has concentrated on energy and financial services

in Africa. The Public Investment Corporation and Impact

Investing South Africa will be looking to encourage

investment in other areas such as manufacturing and social

Michael Denenga

infrastructure. The increasing demand for impact investing Partner and Private Equity Specialist

at Webber Wentzel

will open new commercial avenues for fund managers in

renewable energy, health, affordable housing and food michael.denenga@webberwentzel.com

and security funds, amongst others.

16 / 18 MAKING THE DIFFERENCE FOR OUR CLIENTSSANNEGROUP.COM

Global alternative asset and

Graeme Rate

corporate administration done Country Head – South Africa and Malta

differently t. +27 (0) 21 402 1600

e. graeme.rate@sannegroup.com

SANNE has undertaken to engage with all

of the markets in which it operates to

share knowledge, collaborate with peers

and hear from industry leaders as to their

thoughts on the key issues and topics Karlien De Bruin

affecting the industry and its practitioners. Head of Manco

t. +27 (0) 21 202 8263

Established for over 30 years and listed on the Main e. karlien.debruin@sannegroup.com

Market of the London Stock Exchange, SANNE has

more than 1,800 employees worldwide and has in

excess of £250 billion assets under administration.

Our network of offices provide global managers with

highly skilled and director-led teams of asset class

specialists.

Werner Gerber

Senior Client Relationship Manager

t. +27 (0) 21 402 8289

e. werner.gerber@sannegroup.com

“We take great pride in understanding the

unique needs of each individual client to

create tailored business solutions.”

GRAEME RATE Should you wish to find out more about our

services and operations please speak to us, we

would be delighted to hear from you.

AMERICAS EMEA ASIA-PACIFIC

BVI* Belgrade London Hong Kong

Cayman Islands Cape Town Luxembourg Japan

New York Dubai* Madrid Mumbai

San Diego Dublin Malta Shanghai More than 1,800 FTSE 250 In excess of

Frankfurt* Mauritius Singapore people worldwide listed business £250bn AUA

*Affiliated partner Guernsey Netherlands Tokyo

Jersey Paris

17 / 18 MAKING THE DIFFERENCE FOR OUR CLIENTSSANNEGROUP.COM

To find out more about SANNE, please email Graeme Rate, our Country Head,

South Africa and Malta, graeme.rate@sannegroup.com or alternatively visit us

online, sannegroup.com

*Disclaimer:

Collective Investment Schemes are generally medium to long-term investments. The value of participatory interests (units) may

go down as well as up. Past performance is not necessarily a guide to future performance. Collective investments are traded at

ruling prices and can engage in scrip lending and borrowing. The collective investment scheme may borrow up to 10% of the

market value of the portfolio to bridge insufficient liquidity. A schedule of fees, charges and maximum commissions, as well as

detailed description of how performance fees are calculated and applied, is available on request from SanneManagement

Company (RF) (Pty) Ltd (“the Manager”). The Manager does not provide any guarantee in respect to the capital or the return of

the portfolio. The Manager may close the portfolio to new investors in order to manage it efficiently according to its mandate.

Additional information, including, Minimum Disclosure Document (“MDD”), as well as other information relating to the basis on

which the Manager undertakes to repurchase participatory interests offered to it, and the basis on which selling and repurchase

prices will be calculated, is available, free of charge, on request from the Manager. The Manager is registered and approved by

the Financial Sector Conduct Authority (“the Authority”) under the Collective Investment Schemes Control Act No. 45 of 2002

(“CISCA”). The Manager retains full legal responsibility for the portfolio.The full details and basis of the award can be obtained

from the Manager.

EDITOR: Sivani Pillay – Head of Communications

DESIGN: Kieran Blake – Marketing & Corporate Communications Administrator

Information on Sanne and its regulators can be accessed via sannegroup.com

18 / 18 MAKING THE DIFFERENCE FOR OUR CLIENTSYou can also read