2021 MEGA CONFERENCE Navigating the Credit Uncertainties of COVID-19 - David H. Ruffin | Principal

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

2021 MEGA CONFERENCE

Navigating the Credit Uncertainties of COVID-19

(February 11, 2021)

David H. Ruffin | Principal

Today’s Speaker

David Ruffin

Principal • Extensive financial industry experience with an

IntelliCredit emphasis on credit risk

• Strategist behind IntelliCredit’s Tools:

Portfolio Analyzer and Smart Loan Review

• Review of credit policies and procedures

• Due diligence for M&A or Capital Raising

919.741.8859

david.ruffin@intellicredit.com

Raleigh, NC

2

QwickRate’s Newest Division…

®

QwickBonds

1986 2013 2017 2019

3

Agenda

• The 2021 credit uncertainties

• AR, national & regional Q4 ‘20 credit metrics

• Changes afoot in lending

• Five key strategies to reduce 2021credit uncertainties

• Q&A

4

The 2021 Credit Uncertainties 5

2021 Credit Uncertainties…because:

• 2020 was a high-performance banking year

— Virtually every bank out-performed financial expectations

— The banking Armageddon feared at the advent of COVID didn’t materialize

— Credit metrics at 10K feet imply nothing onerous has occurred

• Temptations to claim victory

— We’re just that good in managing our institutions through this national

disaster—and making money doing so

— We’re the beneficiaries of years of building more capital

— With the vaccines coming, the worst is over

— Unlike a decade ago, no blame can be ascribed to our industry—just the

reverse as you’ve gained huge plaudits with PPP’s

6

6

2021 Credit Uncertainties…because:

• Now for the rest of the story….

— We experienced unprecedented:

o Regulatory relief

o Massive federal economic stimulus in the early months of the pandemic

o Flush of deposit liquidity and non-organic loan growth through PPP’s and SBA

initiatives, that continue into 2021

— Bankers know intuitively that credit tails outlive economic shocks

— The federal government lifelines eventually will cease

— Our commercial bank credits reside on Main Street—not Wall Street—and

Main Street is in a recession!

— Many of our borrowers are more focused on survival than investing for

growth: normally, a credit red flag!

7

7

2021 Credit Uncertainties…because:

• The 2021 credit realities...

— All the largely government COVID initiatives, while avoiding an economic

calamity, have aligned to create the greatest masking effect of underlying credit

risk in modern banking history

— Unlike the last crisis, where all things 1-4 family housing took us into the Great

Recession, COVID has strewn the landscape with many divergent industries

negatively impacted—more complicating our risk assessments

— Thus, 2021 credit uncertainties among all stakeholders:

o Boards & Management

o Risk Managers

o Investors & Investment Bankers

— Uncertainty is anathema to managing credit risk

— Reducing these uncertainties in 2021 will be priority one!

8

8

2021 Credit Uncertainties…because:

• Other challenges remaining:

— Instances / investigations of PPP fraud

— CECL’s not going away

— LIBOR transition

— Continuing focus on AML/BSA and Cyber risks

— The inexorable question: how long the tie to government to both abate our risks

and enhance our growth

9

9

AR, National & Regional 4Q ‘20

Credit Performance Metrics

10Trifecta of Loan Quality: Banks

Trifecta of Loan Quality: Banks

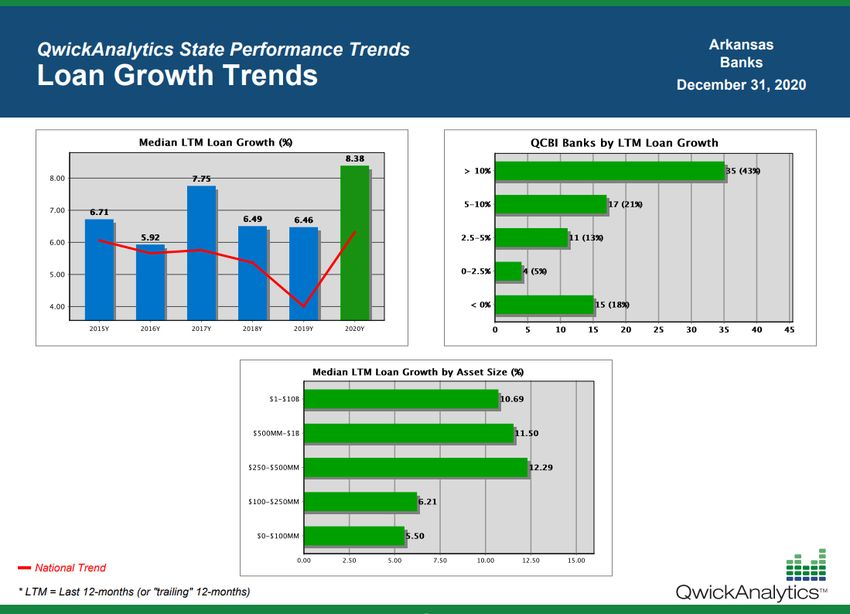

AR Loan Growth Trends: Banks

AR Loan Yields / COF / NIM’s / Wholesale Funding—

Mixed to National Metrics

--As of 12/31/2020

14CRE Concentrations: Banks

Other Concentrations: Banks ≤ $10B

ARNPA’s structural challenge at smaller banks—

when credit is stressed

NPA’S+90 PD / Tang Equity+ALLL (%) ARAR Banks (≤ $10B) ‘Q4 ‘20 NPA’s: 18

Changes Afoot in Lending 19

Changes Afoot in Lending

New focus on lending opportunities

• Looking for the new prospective borrower

• Converting the PPP loans into a more stable organic loan

pool

• Capitalizing on the goodwill related to PPP’s

• Leading on the COVID recovery!

• Relying even more on government guarantee programs for

growth

20Finding Alternative Sources for Loan Growth

December 2020

21Changes Afoot in Lending

New focus on credit risk management

• Pivoting from production (COVID-related modifications, PPP’s) to credit risk

management

• Assessing talent

• Maintaining close borrower contact—virtually, of course

• Tweaking policies & procedures

• Focusing on conservatism without over-reaction

o Stressing without doomsday

o Valuations without fire-sales

o Focus on reserving / moderating charge-offs

22

• Renewing focus on Loan ReviewChanges Afoot in Lending

New focus on M&A

• Predictions of more robust M&A in second half of 2021

• Investment bankers grimacing over unprecedented levels of

uncertainty in underlying credit quality

• It’s beyond 1-4 family housing industry this time

• Loan impairments fade

• There likely will be more what-if scenarios needed

• More focus on cultural synergies

• Even the mechanics of calculating the ever-present credit mark

23 may change…PD’s & LGD’s (Last Financial Crisis)

Default defined: a net charge-off

PD: An informed statistical estimate of a likely default

LGD: A measure estimating severity of loss upon a default*

EL (Loss %): The product of the above*

24

*Applied to loan balances at defaultPD’s & LGD’s (Post COVID)

COVID presenting more reserve-focused sensitivities

Likely expanded definition of a default:

• charge off or write-down*

• ≥ 90-day delinquency

• On non-accrual

• Foreclosure / bankruptcy

*Gold standard in last financial crisis,

skewed by recoveries

25Five Key Strategies to Reduce

2021 Credit Uncertainties

1. Recognize Trap of Focusing Only on Portfolio At-Large

2. Create Portfolio Subsets, Identifying Hotspots

3. Drill Down to Troubled or Stressed Borrowers

4. Adopt Alternative Portfolio Servicing Protocols

5. Write Your Own Script—Before Others Do It For You!

26Let’s start with a critically informing concept…

Public Data Remember:

Non-Public Data

• The external

stakeholders see

Red Flags

you through the lens

Aggregate Affordable /

of public (call report)

Portfolio Trends Practical Portfolio

data.

Loan

Diagnostic Tools

Level Detail

• Only you are privy to

your non-public,

Enhanced Modernized Loan idiosyncratic loan

Loan Review

Findings Review data.

(Interfaced With

Diagnostics)

271. Recognize Trap of Focusing Only on Portfolio At-Large

• Avoiding the all loans are good loans—until they’re bad loans

syndrome

• Knowing that perhaps the most important variable in your credit

quality is the underlying market commodity values of our borrowers’

products and services

• Looking for Red Flags from both public and non-public data.

28Red Flags

29

292. Create Portfolio Subsets, Identifying Hotspots

• Knowing your concentrations

• Focusing on risk grade migrations within the pass

categories

• Understanding the varied COVID impacts on your portfolio.

30Unchecked Concentrations — Like Speed — Kills!

Key Findings

• >70% of 2008-2011 bank failures

were CRE lending focused

• High concentrations and late cycle

growth (vintages), lack of loan

seasoning significantly exacerbated

losses

• High correlation to collateral

dependence coincides with default

rates (worst of both worlds)

• State/regional market forces are

critical co-variants

31CRE Record Exposure at Commercial Banks

--Source: Federal Reserve

32Understand your portfolio concentrations

Concentrations

by Band

(or type)

33Understand your portfolio concentrations

Concentrations

by Average Risk-

based Capital or

Community Bank

Leverage Ratio

34Recognize the Varying COVID Impact

on Your Borrowing Industries

Understand your portfolio subsets, vintages and hotspots

Portfolio Subsets

by NAICS Codes

(Industries)

35Recognize the Varying COVID Impact

on You Borrowing Industries

Understand your portfolio subsets, vintages and hotspots

Portfolio with

COVID / PPP /

SBA Subsets

36Recognize the Varying COVID Impact

on Our Borrowing Industries

Understand your portfolio subsets, vintages and hotspots

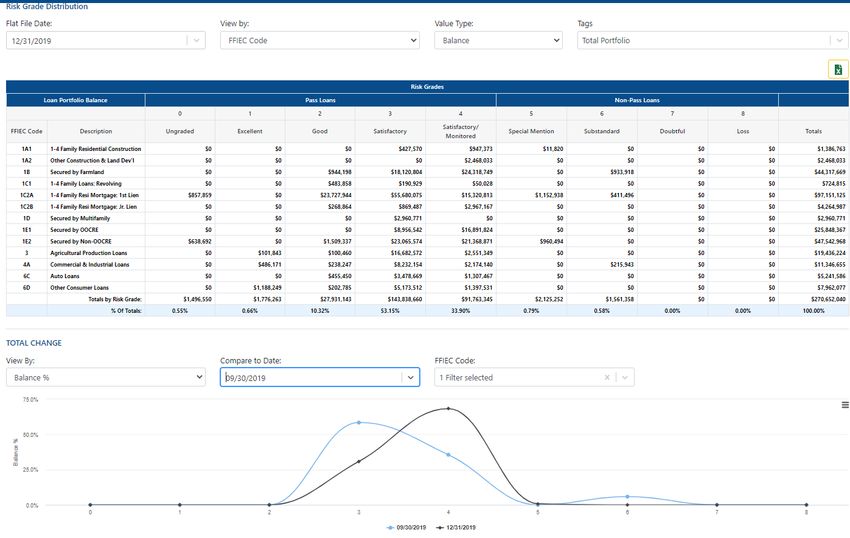

Whole Portfolio Risk Grade Migrations Residential Construction

37 Key to early detection: RG migrations within pass categories!3. Drill Down to Troubled or Stressed Borrowers

• Aggregate trends are only meaningful if you can efficiently

identify the borrowers comprising those trends

• And peeling the onion further, which are or likely to

become stressed…

38Trends must identify loan level detail

39

39Then, the switch to the qualitative tedium of

analyzing the stressed borrowers

40

404. Adopt Alternative Portfolio Servicing Protocols

• Update loan polices to reflect current conditions

• Be more risk-focused; one size doesn’t fit all. All aspects of

post-booking loan servicing should have a risk/reward

component to its implementation (e.g. annual review

minimums may be quite different among loan types and

risk grade segmentation)

• Embrace portfolio and loan level stress testing

• Catch up on and enhance all aspects of loan review

41Why Stress Testing is a Must at Community Banks

Stress testing:

1. Gives early warnings.

2. Ties traditional transactional credit risk to modern macro

portfolio management.

3. Provides in-depth concentration management.

4. Documents defense of strategic/capital initiatives.

5. Engenders confidence in management.

Source—BankDirector.com, May 4, 2014

42 42Is Your Bank’s Loan Review Good Enough?

Key Questions:

• Is reviewer talent qualified and

effective?

• Is it in sync culturally with all aspects

of the credit process?

• Does it have relevance on real time

portfolio risk assessment?

• Is it truly independent?

• Is suppressing today’s loan review

costs exacerbating more losses later?

BankDirector.com | May 4, 2017

43 43Interagency Guidance of Credit Risk Review Systems (Issued)

Regardless of structure (or size of the institution), an effective credit risk review system accomplishes the

following objectives:

✓ Identifies loans with credit weaknesses

✓ Validates risk ratings

✓ Identifies relevant trends

✓ Assesses internal credit policies and loan administration procedures / compliance with laws and

regulations

✓ Evaluates lending personnel, including their compliance with lending policies risk assessment

✓ Provides management and the boards of directors with portfolio quality assessments

✓ Opines on problem loan management plans

✓ Provides management with timely credit quality information for regulatory, reporting, and ALLL

44

445. Write Your Own Script—Before Others Do It For You!

• The It’s beyond my control defense is no longer workable.

• 2021 will demand that banks provide evidence of proactive risk assessments.

That’s the quantitative—

now write the qualitative

narrative of your own

credit risk profile!

• All outside stakeholders, especially regulators, must perceive you as the

experts on your own credit risk profile. Taking the above steps should enable

you, credibly, to write our own scripts.

45Greatest Value Takes from Implementing the Five Key Strategies:

• Confirming you as captain of your own ship

• Minimizing credit surprises at board /regulator levels!

• Supporting the proven correlation between early detection of emerging credit risk, and:

— Reduced levels of loss / nonperformance

— Greater flexibility in managing problem loans out of the bank

• The magnitude of today’s credit uncertainties adds to your challenges in realizing this maxim—

46 but they can be overcome!Q&A 47

You can also read