2021 outlook: recovery & rotation - BlueBay Asset Management

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

2021 outlook:

recovery & rotation

David Riley

Chief Investment Strategist, BlueBay Asset Management

December 2020

Reading time: 5mins

2021 will mark an inflection point for the global economy and markets. We expect to see a

more complete recovery as effective vaccines are deployed, alongside a rotation in market

leadership from defensives and high-quality credit to the most growth-sensitive sectors.

But the path to ‘normality’ will not be without bumps in the road.

Summary

The global economic recovery depends on the

§§ We expect the search for yield in an environment of

§§

deployment of an effective vaccine for Covid-19. zero/negative cash rates and ultra-low bond yields will

We have upwardly revised our growth forecasts for 2021

§§ continue to drive investor demand for investment-grade

on vaccine breakthroughs that should allow a quicker credit against the backdrop of less supply as companies

and more complete economic recovery. reduce their leverage.

Monetary and fiscal policies will continue to support

§§ Confidence in our positive outlook is tempered by

§§

the economy until the recovery is complete. continuing downside risks. The path back to ‘normality’

will not be without bumps in the road.

Sustained global expansion in 2021 and declining

§§

volatility should support risk markets and a rotation We believe exploiting relative-value opportunities

§§

in performance leadership from long-duration growth will require careful and timely asset allocation,

assets (notably US technology), defensive sectors and fundamentally driven credit selection and active

higher-quality credit to the most growth-sensitive assets, management of market risk.

including commodities, cyclicals, Covid-affected sectors

and emerging markets.

Return to ‘normality’

Our positive macro and market outlook for 2021 is underpinned An effective vaccine brings the return to ‘normality’ and a full

by the discovery of effective vaccines against Covid-19. The path economic recovery within much closer reach. We believe a

of the virus and efforts to control it have been the principal broad-based and sustained global recovery will be mirrored

driver of the global economy, greatly ameliorated – but not by a rotation in market leadership. We would expect to

cured – by unprecedented fiscal and monetary policy support. see lower-rated credit, cyclical and Covid-affected sectors

1

2021 outlook: recovery & rotation

Chart 1: Global growth forecast (annual % change)

Source: Consensus forecast as reported by Bloomberg; BlueBay Asset Management forecasts, 1 December 2020

returning to favour, alongside emerging markets (EM), while and effective Covid-19 vaccine will be available in the first

higher-quality, defensive and long-duration growth assets half of next year. The higher-than-expected efficacy rate

could be displaced. suggests that, once rolled out, vastly fewer people should

become seriously ill. This in turn should ease pressure on

Vaccine recovery health services and on governments to maintain restrictions

It was a health crisis that plunged the global economy on economic and social activity.

into its deepest recession in modern history, rather than

unsustainable private-sector imbalances or excessive “Continuing monetary and fiscal support is

tightening of financial conditions by central banks, as has

crucial, in our view, until the recovery

been the case in previous downturns. The policy response was

similarly unprecedented in terms of the scale of interventions is complete.”

by central banks and governments, providing a financial

bridge for households and companies to the other side of Questions remain, including the duration of protection from

the pandemic. Notably, household incomes are higher than in the vaccine, its effectiveness across most-at-risk groups

2019 and the number of company bankruptcies is lower. and the extent that it prevents the spread of infection.

Nonetheless, a more effective vaccine sooner than expected

The latest wave of the pandemic across the northern meaningfully improves the prospects for a robust and more

hemisphere is expected to hinder the economic recovery complete recovery in 2021 and reduces the risk of permanent

into the first quarter of next year. But thereafter, we expect economic ‘scarring’.

activity to rebound as social distancing restrictions ease and

vaccines are widely deployed. We foresee distressed sectors Continuing monetary and fiscal support is crucial, in

such as travel, leisure and hospitality leading this recovery. our view, for supporting the economy until the recovery

is complete. We expect a USD750 billion to USD1 trillion

fiscal package to be passed in Washington in the first

“We expect activity to rebound as

quarter of 2021 in response to the US’s third wave.

social distancing restrictions ease

and vaccines are widely deployed. In Europe, in addition to the disbursements under

We foresee distressed sectors such the EUR750 billion Next Generation EU fund, national

governments are planning additional fiscal support.

as travel, leisure and hospitality

leading this recovery.” We expect central banks to remain very accommodative and

continue to ease policy until the path to normalisation and a

We revised higher our 2021 growth forecasts following the complete economic recovery is more firmly established. The

Pfizer/BioNTech and Moderna vaccine announcements, European Central Bank (ECB) has committed to extend and

with both treatments showing 90%+ efficacy rates with no expand its asset purchases likely by around EUR400 billion and

serious side-effects. As such, we can assume that a robust the US Federal Reserve (Fed) will maintain quantitative easing

2

2021 outlook: recovery & rotation

and zero cash rates until inflation is sustainably at or above its

2% target and unemployment is close to its pre-pandemic low. Chart 2: Real GDP (Q4 2019 = 100)

Our growth forecasts are higher than consensus, with the

US returning to pre-crisis output level in the second half of

2021. The economic shock of the pandemic was far greater

for Europe than the US and while the euro area is forecast to

expand by more than 5% next year – faster than the US – we do

not expect it to reach its pre-crisis peak until sometime in 2022.

China is the standout and has already surpassed its pre-

crisis output level on the back of more effective containment

of the virus and large fiscal and credit stimulus. The UK is

forecast to experience its most rapid annual growth for

decades in 2021, but this reflects the depth of the downturn

this year – amongst the deepest of the major economies –

and assumes that a ‘thin’ post-Brexit trade deal is reached

with the EU.

The public vaccine rollout across emerging and developing

countries may be slower and later than in advanced countries,

but the risk of repeated waves of infection is reduced and Source: BlueBay Asset Management estimates and forecasts,

1 December 2020

their economies should benefit from the global recovery and

continuing outperformance of the Chinese economy.

“The recovery in global activity should

Taking a micro view, the outlook varies across EM by region, support higher commodity prices and

with emerging Asia predicted to do better than emerging a weaker US dollar. These factors, in

Europe, while Latin America could lag the broad recovery

combination with an ultra-dovish Fed

trend due to the continuing severity of the pandemic and less

room for policy support. and reduced trade and geopolitical risk

from a Biden US presidency, suggest to

Leadership rotation us that the macro backdrop is especially

We expect a vaccine-led re-opening of the economy and

subsequent global recovery to benefit the assets of sectors favourable for EM assets.”

most adversely affected by Covid-19 and social distancing, as

well as lifting cyclical assets. As in 2017, a broad-based and Global recovery and reflation are typically associated with a

sustained global expansion in 2021 and decline in volatility weaker US dollar and stronger EM currencies. The strength

should support risk markets and a rotation in leadership of the Chinese recovery, alongside a rising trade surplus and

from long-duration growth assets (notably US technology), Chinese government bond yields being meaningfully higher

defensive sectors and higher-quality credit to the most than in developed economies, should continue to underpin

growth-sensitive assets, including commodities, cyclicals, a robust renminbi. EM currencies are considered ‘cheap’

Covid-affected sectors and EM. on many measures and should benefit from the investor

rotation into cyclical and ‘value’ assets. Meanwhile, yield

Compression in spreads between higher and lower-rated curves are steep and real yields are considered attractive.

credit and the outperformance of Covid-affected and

cyclical assets, including banks, are what we expect to be Higher medium-term growth and inflation expectations

the dominant themes in credit markets in 2021. We predict may support some modest steepening of core government

safe-haven assets, such as the US dollar and Treasuries, yield curves, but we expect central banks to lean against

will underperform. any meaningful tightening in financial conditions. The Fed’s

3

2021 outlook: recovery & rotation

shift to an ‘average inflation target’ regime, which is likely to

be followed in some form by the ECB, suggests that policy Chart 3: Market implied path of short-term rates

rates and liquidity will continue through next year and until

3.0

inflation is sustainably at or above target.

2.5

The recovery in global activity should support higher

commodity prices and a weaker US dollar. These factors,

2.0

in combination with an ultra-dovish Fed and reduced trade

Central bank policy interest rates (%)

and geopolitical risk from a Biden US presidency, suggest

1 .5

to us that the macro backdrop is especially favourable for

EM assets. 1 .0

Yield curves in many EM local debt markets remain relatively 0.5

steep and currencies near historic lows. EM credit, especially

in high yield, has also lagged the performance of investment 0.0

grade and developed-market high yield.

-0.5

We expect the search for yield in an environment of zero/

negative cash rates and ultra-low bond yields will continue -1.0

201 9 2020 2021 2022 2023 2024

to drive investor demand for investment-grade credit, while BoE bank rate US Federal funds effective rate ECB deposit rate BoJ policy rate

we anticipate bond issuance will drop as companies focus on

balance-sheet repair and have ample cash reserves. Note: Implied future policy rate derived from Overnight Index Swap (OIS).

Source: Bloomberg, 1 December 2020

In our view, high yield and distressed credit offer potentially But regulatory delays, low public take-up and logistical

the greater upside for investors, especially in cyclical assets challenges are all potential hindrances.

such as bank subordinated debt and the Covid-impacted

sectors of travel, leisure and hospitality. Mezzanine and sub- Although unlikely in our view, the risk of policy mistakes

investment grade structured credit is also likely to deliver cannot be wholly discounted – especially a premature

positive performance, in our opinion. withdrawal of fiscal support. Finance ministry officials

around the world are worried by record government

A bumpy path borrowing and high and rising public debt, while the political

Confidence in our positive outlook for 2021 is tempered by will to maintain fiscal support may be eroded by the prospect

continuing downside risks. The current wave of coronavirus of vaccines and a lower fatality rate. But with central banks

infections, hospitalisations and renewed social-distancing expected to absorb virtually all net government issuance in

restrictions provide a stark reminder of the health and 2021 and debt-servicing costs at historic lows, we believe it

economic risks posed by the pandemic. The path back to would be a policy mistake to withdraw fiscal support

‘normality’ will not be without bumps in the road. too quickly.

The risk that monetary support is withdrawn is even less

“Confidence in our positive outlook for

likely, in our opinion, but central banks may signal a winding-

2021 is tempered by continuing downside down in asset purchases in the latter half of 2021, even if the

risks. The path back to ‘normality’ will commitment to lower-for-longer policy rates remains. The

withdrawal of the comfort blanket of additional central-bank

not be without bumps in the road.”

liquidity could prove a catalyst for market volatility, as it was

in the summer of 2013.

The logistical challenges of distributing billions of vaccines

globally are daunting. Reaching sufficient population High and rising inflation is the dog that never seems to

coverage to facilitate a return to normality by the middle of bark. Yet, if vaccines pave the way for recovery in demand

2021 seems more likely if multiple vaccines gain approval. and employment, while supply is constrained by under-

42021 outlook: recovery & rotation

investment from cautious corporate management teams

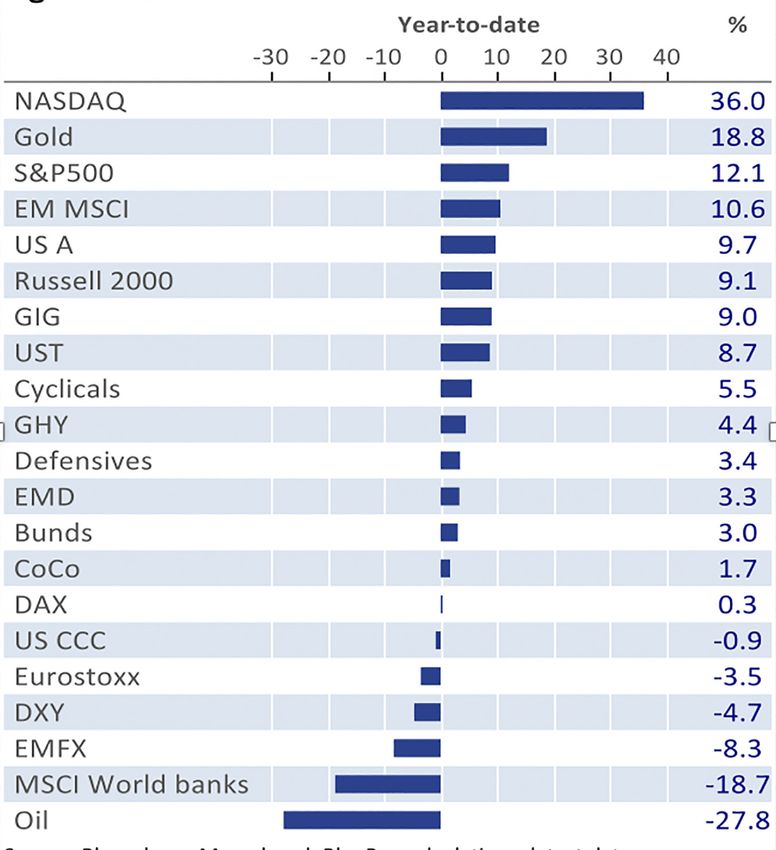

focused on balance-sheet repair, inflation pressures could Chart 4: 2020 YTD returns from selected assets

quickly build. Central banks would likely react even under the

more accommodating average inflation targeting regimes,

which could prompt a dramatic re-adjustment of investor

portfolios, in our view.

Conclusion: positive but not complacent

The discovery of an effective vaccine and continuing policy

support underpin our positive macro and market outlook

for 2021. Unlike previous global recessions, the business

cycle was ended by a health crisis. As such, the economic

recovery will not be held back by the unwinding of financial

imbalances, as it was following the global financial crisis.

But the fight against the coronavirus is not yet won. Success

rests on a public vaccine programme that could take longer-

than-anticipated to be successful. And while permanent

economic damage from the crisis is dramatically less as a

result of central-bank support, the legacy of greater debt and

the risk of a global liquidity trap leaves a diminished policy

space to respond to future economic shocks.

Many assets are at historically high valuations and investors

are rightly wary of the room for further gains. However, the

Source: Bloomberg, Macrobond, BlueBay calculations,latest data at

market rally since March until the vaccine breakthrough 1 December 2020.

in early November had a bearish tone to it, with investors

paying a premium for sources of growth and defence in an A rotation in market leadership that will not necessarily be

environment characterised by extraordinary uncertainty and reflected in big rises in headline indices will be challenging

elevated volatility. for investors to navigate. We believe exploiting relative

value opportunities will require careful and timely asset

Despite the rotation in performance since early November allocation, fundamentally driven credit selection and

with cyclical, value and EM assets outperforming, risk active management of market risk. In our view, investors

premiums on these assets remain relatively elevated. should prepare for a recovery and rotation but not discount

Although expectations for a recovery and rotation is now the downside risks as complacency is invariably punished.

consensus view, valuations and investor positioning suggest

it is far from fully priced. Although markets are forward

looking, they are also grappling with the second wave of the

virus across the northern hemisphere and a deteriorating

near-term economic outlook, as well as uncertainty

around how quickly vaccines will allow a full re-opening of

economies and a return to normality.

52021 outlook: recovery & rotation DISCLAIMER This document may be produced and issued by the following entities: In the United Kingdom (UK) by BlueBay Asset Management LLP (BBAM LLP), which is authorised and regulated by the UK Financial Conduct Authority (FCA), registered with the US Securities and Exchange Commission (SEC) and is a member of the National Futures Association (NFA) as authorised by the US Commodity Futures Trading Commission (CFTC). In United States, by BlueBay Asset Management USA LLC which is registered with the SEC and the NFA. In Luxembourg, by BlueBay Funds Management Company S.A. (the ManCo), which is regulated by the Commission de Surveillance du Secteur Financier (CSSF). In Germany and Italy, the ManCo is operating under a branch passport pursuant to the Undertakings for Collective Investment in Transferable Securities Directive (2009/65/EC) and the Alternative Investment Fund Managers Directive (2011/61/EU). In Switzerland, by BlueBay Asset Management AG where the Representative and Paying Agent is BNP Paribas Securities Services, Paris, succursale de Zurich, Selnaustrasse 16, 8002 Zurich, Switzerland. The place of performance is at the registered office of the Representative. The courts of the registered office of the Swiss representative shall have jurisdiction pertaining to claims in connection with the distribution of shares in Switzerland. The Prospectus, the Key Investor Information Documents (KIIDs), the Articles of Incorporation and any other applicable documents required, such as the Annual or Semi-Annual Reports, may be obtained free of charge from the Representative in Switzerland. In Japan, by BlueBay Asset Management International Limited which is registered with the Kanto Local Finance Bureau of Ministry of Finance, Japan. In Australia, BlueBay is exempt from the requirement to hold an Australian financial services license under the Corporations Act in respect of financial services as it is regulated by the FCA under the laws of the UK which differ from Australian laws. In Canada, BBAM LLP is not registered under securities laws and is relying on the international dealer exemption under applicable provincial securities legislation, which permits BBAM LLP to carry out certain specified dealer activities for those Canadian residents that qualify as “a Canadian permitted client”, as such term is defined under applicable securities legislation. The BlueBay group entities noted above are collectively referred to as “BlueBay” within this document. The registrations and memberships noted should not be interpreted as an endorsement or approval of BlueBay by the respective licensing or registering authorities. Unless otherwise stated, all data has been sourced by BlueBay. To the best of BlueBay’s knowledge and belief this document is true and accurate at the date hereof. BlueBay makes no express or implied warranties or representations with respect to the information contained in this document and hereby expressly disclaim all warranties of accuracy, completeness or fitness for a particular purpose. Opinions and estimates constitute our judgment and are subject to change without notice. BlueBay does not provide investment or other advice and nothing in this document constitutes any advice, nor should be interpreted as such. This document does not constitute an offer to sell or the solicitation of an offer to purchase any security or investment product in any jurisdiction and is for information purposes only. This document is intended only for “professional clients” and “eligible counterparties” (as defined by the Markets in Financial Instruments Directive (“MiFID”) ) or in the US by “accredited investors” (as defined in the Securities Act of 1933) or “qualified purchasers” (as defined in the Investment Company Act of 1940) as applicable and should not be relied upon by any other category of customer. No part of this document may be reproduced, redistributed or passed on, directly or indirectly, to any other person or published, in whole or in part, for any purpose in any manner without the prior written permission of BlueBay. Copyright 2020 © BlueBay, is a wholly-owned subsidiary of RBC and BBAM LLP may be considered to be related and/or connected to RBC and its other affiliates. ® Registered trademark of RBC. RBC GAM is a trademark of RBC. BlueBay Asset Management LLP, registered office 77 Grosvenor Street, London W1K 3JR, partnership registered in England and Wales number OC370085. The term partner refers to a member of the LLP or a BlueBay employee with equivalent standing. Details of members of the BlueBay Group and further important terms which this message is subject to can be obtained at www.bluebay.com. BlueBay Funds Management Company S.A., registered office 4, Boulevard Royal L-2449 Luxembourg, company registered in Luxembourg number B88445. All rights reserved. Disclosure ® / TM Trademark(s) of Royal Bank of Canada. Used under licence. © RBC Global Asset Management Inc. 2020

You can also read