A LABOUR OF LOVE - ONLINE DATING IN THE AGE OF MOBILE AND SOCIAL MEDIA - GP Bullhound

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

INDEPENDENT TECHNOLOGY RESEARCH

SECTOR INITIATION NOVEMBER 2012 ONLINE DATING

A LABOUR OF LOVE – ONLINE DATING IN THE

AGE OF MOBILE AND SOCIAL MEDIA

Industry Being Re-Energised by New Entrants

As one of the long-standing Internet verticals, online dating is currently being

re-energised by a flurry of new entrants looking to capitalise on (i) the

acceptance of online dating, (ii) social media’s ability to expand the market

beyond traditional dating services, and (iii) mobile’s ascendance to becoming

a key pathway to consumer services.

Through the proliferation of social media and the ubiquity of mobile Internet

the online dating industry is adapting to cater to changing consumer needs.

Some well-established players are pursuing innovation and growth through

acquisitions and a fresh wave of start-ups are looking to capitalise on a rapidly

evolving and potentially much larger market.

Three is no Longer Company…

With the advent of social media, a new online dating category called “social

discovery” is starting to emerge looking to leverage social graphs, integrate

friend’s recommendations and setting up casual events with people that share

similar interests.

With the boundaries between online dating in the traditional sense and social

networks quickly becoming blurred, we think the online dating sector is set for

strong growth, driven by the increasingly social dimension of online dating and

the ease and convenience of mobile dating.

Is Mobile The Killer App?

Mobile is shaping the way singles interact with online dating services as the

mobile phone is ideally suited to leverage the pervasive nature of an

individual’s digital life. Mobile adoption has been rapid in online dating, with

30% of all eHarmony traffic now being originated from the mobile, 40% of

Match.com log-ins stemming from the mobile, and 68% of all Badoo log-ins

coming via the mobile. CLAUDIO ALVAREZ

claudio.alvarez@gpbullhound.com

In the US, the nascent mobile dating market is estimated to be $200m+ in London: +44 207 101 7571

2012 (30% YoY growth) and in Germany it is forecast to reach $40m+ by

2012, with mobile dating penetration across Western Europe estimated to be MANISH MADHVANI

manish.madhvani@gpbullhound.com

around 10%.

London: +44 207 101 7560

ALESSANDRO CASARTELLI

alessandro.casartelli@gpbullhound.com

London: +44 207 101 7594

Important disclosures appear at the back of this report

GP Bullhound LLP is authorised and regulated by the Financial Services Authority in the United Kingdom

GP B ULLHOUND – ONLINE D ATING – A LABOUR OF LOVE

TABLE OF CONTENTS

The Evolution of Online Dating ................................................................................ 2

Introduction ........................................................................................................ 2

Dating Before the Internet ................................................................................. 2

The Birth of Online Dating – A Serious Affair .................................................... 3

Niche Verticals – An Attractive Market .............................................................. 4

Europe Joins the Party ...................................................................................... 5

Monetising Online Dating .................................................................................. 6

White Labelling .................................................................................................. 7

Market Size and Growth ............................................................................................ 8

The Rise of Social Discovery.................................................................................... 9

Social Dating: A Natural Evolution from Social Networks and Online Dating . 10

Social Dating 2.0: A New Crop of Players ....................................................... 13

Challenges Ahead for Social Romance .......................................................... 14

Dating has Become a Key Category in Mobile ..................................................... 16

Mobile Dating Usage Rising Sharply ............................................................... 16

Incumbents and New Players are Pursuing the Mobile Dating Opportunity ... 18

Mobile Dating: The Challenges ....................................................................... 20

Selected Company Profiles .................................................................................... 21

Selected M&A Transactions ................................................................................... 26

Selected Private Placements and IPOs ................................................................. 27

1

GP Bullhound LLP

GP B ULLHOUND – ONLINE D ATING – A LABOUR OF LOVE

The Evolution of Online Dating

Introduction

Services aimed at connecting individuals and enabling them to find partners and start

relationships have existed for as long as living memory. The oldest form – introduction by

relatives – has been the preferred method for centuries and continues to be available today.

Yet in more recent years a series of dramatic changes have fundamentally altered how

singles enter the dating scene and find partners. In the 1900s rising economic prosperity,

urbanisation and increased life expectancy, coupled with the widespread availability of

contraception and the social and sexual liberation of the 60s, brought about a seismic shift in

attitudes towards love, sex and marriage, and consequently dating. In the last few decades

however it is technology – in particular the Internet – which has been the agent of change.

Dating Before the Internet

Before the Internet, dating services were obtained in person through dedicated

intermediaries – matchmakers and introduction agencies. These intermediaries controlled

and charged for access to pools of prospective partners, the size of which were limited by the

depth of the intermediaries’ respective networks. The matchmaking process was fairly

cumbersome and time consuming, as new clients and prospective partners all had to be

assessed in detail to provide the highest chance of success. It was also expensive.

The other route to romance for lonely hearts was to list adverts in the personals sections, on

radio shows, or on TV through dedicated dating channels. Despite being cheaper and

quicker than the matchmaking route, this method was also less than satisfactory – success

was dependent on Mr. or Mrs. Right happening to read the relevant paper or tune in on the

day of the advert, and few people were prepared to pay for repeat listings.

Moreover, both of these methods suffered from a general lack of social acceptance – for

most people, paying to find love was seen as a last resort, not a first port of call. As a result,

these conventional dating channels remained a niche and fractured market, with a blend of

small local agencies and media groups functioning at different levels of the market and

operating under different revenue models. Yet with the arrival of the Internet and the digital

age, all this would change.

EXHIBIT 1: GLOBAL GROW TH IN SINGLES POPULATION AND ONLINE SINGLES

Global Singles (m) Global Online Singles (m) % of Americans who met their partners online

331 23.2%

99

19.3%

69

10.9%

277

3.8%

2.1%

0.02% 0.06%

2011A 2020E 2011A 2020E prior to 79-88 89-93 94-98 99-03 04-06 07-09

'78

Source: Forrester Research, Euromonitor International, Stanford University and City College of New York, GP Bullhound

2

GP Bullhound LLP

GP B ULLHOUND – ONLINE D ATING – A LABOUR OF LOVE

Some of the key drivers that have led to the uptake of online dating are: a rapid rise in the

global online population, a rapid rise in number of single-person households, improved user

functionality and the fading away of the stigma attached to online dating.

The Birth of Online Dating – A Serious Affair

The online dating industry was established in 1995 when Match.com and

AmericanSingles.com were launched in the US. Match.com took a more traditional approach

to dating online through matchmaking (i.e. pairing people up dependent upon their personal

profile and goals) and AmericanSingles.com took a much more casual approach by allowing

members to search its database by gender, age and location.

In 1994, when only about 5% of the US population had Internet access and the Internet was

still in its early stages, an entrepreneur named Gary Kremen purchased – from the US

government – the Match.com domain name for $2,500. In 1995, he founded Match.com as a

way to inject efficiency into the traditional matchmaking model. Before Match.com Gary

started a personals classified business that primarily used premium phone numbers to

engage clients. However, he found the phone service inefficient, and thought if he could

create an online database of personal advertisements it would allow people to find potential

partners themselves more quickly, effectively and, most importantly, anonymously. Given the

early stigma around online dating, and the type of users that Match.com was trying to attract,

it was paramount that the service was able to guarantee anonymity but still allow users the

ability to have meaningful interactions. Match.com quickly grew to be one of the leading

players in the online dating space and was sold to IAC in 1999 for $50m. Today, Match.com

generates revenues of over $500m, has over 2.7m subscribers and over 6m unique monthly

visitors.

EXHIBIT 2: ONLINE DATING UNIVERSE (REPRESENTATIVE)

High

Matchmaking

Traditional Online Dating

Pricing

Casual

Niche Dating

Low

Broad Target Group Focus Narrow

Source: GP Bullhound

The other well-known entrant in the online dating market was eHarmony, which was founded

in 2000 by Neil Clark Warren, a psychologist and author of relationship advice books. Neil

3

GP Bullhound LLPGP B ULLHOUND – ONLINE D ATING – A LABOUR OF LOVE

developed a proprietary model of compatibility which is at the core of the company’s

matching system, and which differentiates its matching service by what eHarmony describes

as “a scientific approach to a deeply personal and emotional process.” eHarmony uses a

proprietary algorithm to analyse answers and users’ behaviour on the site in order to

increase the chances of a successful match – hopefully leading to marriage. Because of

eHarmony’s lengthy sign-up assessment process and tailored introductions model (e.g. it

normally takes an individual 40 minutes to complete the introductory questionnaire), it was

able to mitigate the problem many online daters had of being unable to find serious

relationships due to lack of compatibility and information.

Because of eHarmony’s positioning as a site for “the serious relationship seeker”, it was able

to garner a higher proportion of female users and monetise them at a premium compared to

Match.com. Like Match.com, it grew rapidly to become a multi-million dollar company, and

today boasts over 3m unique monthly visitors.

Niche Verticals – An Attractive Market

Serving a wide audience was how the online dating market initially expanded – so as to

benefit from consumer adoption – but as the market expanded, players focusing on niche

verticals started to appear. A number of companies began to make headway by targeting

niche markets, such as same-sex relationships, casual encounters, and specific

demographics filtered by education, wealth, race, occupation and even body weight. In 1997

for instance, Spark Networks was created, launching JDate.com, an online dating service

aimed at Jewish singles, and expanding to over 30 diversified sites. FriendFinder Networks

also successfully combined specialisms with scale, launching over 25 targeted portals to

date which together attract over 2m unique monthly visitors.

Niche verticals became attractive to new market entrants as they could tailor their consumer

proposition to a very specific target group and hence be very effective at acquiring customers

through more direct marketing channels. According to online dating consultant Mark Brooks,

in the US 44% of the market was comprised of niche sites in 2009, up from 35% in 2006.

Jdate.com has demonstrated the willingness of consumers to pay a premium for targeted

dating sites. It has been able to generate ARPU of $25 with a contribution margin circa 90%

throughout the last nine years as it has grown revenues from $8.4m (2002) to $27m (2011).

EXHIBIT 3: AVID LIFE MEDIA’S RAPID REVENUE AND PROFITABILITY GROW TH

42% CAGR 59% CAGR

$57m

$28m

$19m

$8m

Revenues EBITDA

2009 2011

Source: Company information

4

GP Bullhound LLPGP B ULLHOUND – ONLINE D ATING – A LABOUR OF LOVE

The other interesting niche market that has started developing is the casual encounters (i.e.

cheating) market. The biggest player in this market is Avid Life Media – the owner of Ashley

Madison. Ashley Madison specifically targets individuals in relationships looking to have

affairs, and since its launch in 2002 has attracted more than 15m members in 25 countries.

According to the company a new person is said to join every six seconds. Ashley Madison is

also highly profitable as it manages to charge a monthly subscription fee of $49.00 in

addition to value-added-services to help users promote themselves and communicate with

other members. In 2009, it estimated that the business generated EBITDA of $8m (26%

margin). It has grown EBITDA to $19m by 2011, corresponding to a CAGR of 59% and an

EBITDA margin of 33%.

Europe Joins the Party

Until 2001 the burgeoning online dating market was largely confined to the US – then it

began to expand globally. Before 2001, there was only one online dating player – United

People – established in 1996 in Germany. United People was acquired by Scout24 group in

2000 and changed its name to FriendScout24. In 2001, two other players entered the

European online dating market – Meetic and Parship. Meetic was founded by Marc Simoncini

(a well-known French entrepreneur responsible for iFrance – sold to Vivendi for €182m) and

started in its home market of France and then quickly expanded to other territories in Europe

through organic growth and acquisitions. Meetic made five European acquisitions between

2005 and 2009 – eFriendsNet, Lexa.nl, DirectDating.com, Neu.de and Match.com

International. The last transaction – done in 2009 – saw Match.com become a minority

shareholder in Meetic and this would ultimately lay the foundations for Match.com acquiring

Meetic in 2011.

EXHIBIT 4: EUROPEAN -BASED ONLINE DATING PLAYERS

2000 2001 2003/04 2006/08

Source: GP Bullhound

Founded in 2000 and backed by Holtzbrinck Digital GmbH, Parship looked to replicate

eHarmony’s algorithmic matchmaking model for the German-speaking (DACH) market.

Parship established itself as the matchmaking leader in Europe and grew revenues north of

€50m and 10m+ registered users, with key properties in Germany, Switzerland, Austria and

the Netherlands.

As the European market developed, other players started entering the market with

Match.com establishing European operations based out of London in 2003. Elite Partners

(originally backed by Burda Media Ventures and then acquired by Tomorrow Focus in 2009)

5

GP Bullhound LLPGP B ULLHOUND – ONLINE D ATING – A LABOUR OF LOVE

was founded in 2004 and by the time of the Tomorrow Focus acquisition, it had revenues of

€20m+ and was EBITDA profitable.

In 2004, Be2 launched in Switzerland and then raised €20m from Index Ventures and Banexi

Ventures in 2008 to expand outside of its home market. It is reported that Be2 European

revenues in 2010 were circa €21m. In 2008, eDarling launched in Germany received backing

from Rocket Internet in 2009 and reached European revenues of €21m by 2010.

Monetising Online Dating

Traditionally, the main way to monetise online daters has been through charging monthly

subscriptions. However, with the advent of Web 2.0, online dating providers have added new

functionalities and launched mobile offerings in order to attract more users and boost

monetisation.

Online dating players have added features which are inherently social but revenue

generating – either ones which help warrant the cost of monthly subscriptions (such as

instant messaging, mini-games and personal ratings) or which are of direct benefit and paid

for when used (such as virtual goods and micro-payments to browse other users’ profiles

anonymously or to enhance a users’ visibility in search listings). Developing value added

services has been a move that traditional online dating players have had to embrace as

daters’ attitudes between paying and free sites have become less stark with regards to the

quality of matches they may find.

EXHIBIT 5: CONSUMERS’ VIEW S ON PAID VERSUS FREE DATING SITES

Paying to belong to a dating site doesn't necessarily

52% 38% 8% 2%

mean you'll find a better match

I believe paying money to contact someone on a dating

38% 41% 17% 4%

site is unnecessary

You are just as likely to meet professionaly oriented 5%

36% 43% 16%

people on free sites as you are on paids sites

Paid dating sites have no advantages over the ones that

31% 39% 24% 6%

are available for free

Strongly agree Somewhat Agree Somewhat Disagree Strongly Disagree

Source: comScore

Given consumers’ attitudes to subscription websites and the flood of new social entrants,

online dating companies focused on subscription-based memberships have experienced

pressure on subscription prices and levels, with users migrating to free dating sites

monetized through advertising revenue. Another factor contributing to this shift in attitudes

towards subscription versus free, is that with the entry of free players into the space, few

users feel that access to a large pool of prospects is worth paying for: dating sites then must

offer more to command a premium.

6

GP Bullhound LLPGP B ULLHOUND – ONLINE D ATING – A LABOUR OF LOVE

Although consumers’ perceptions to paid versus free are blurring, the number of consumers

willing to pay for online dating has been steadily increasing as both the single online

population and social acceptance of the service has continued to grow. According to TNS

data collected from Western European singles, the percentage of European singles willing to

pay for online dating services has grown from 24.3% (9.6m) in 2008 to 28.3% (15m) in 2012,

and is expected to grow to 31.9% (19.8m) by 2015.

EXHIBIT 6: EUROPEAN SINGLES PREPARED TO PAY FOR ONLINE DATING SERVICES

% of total

24% 25% 26% 27% 28% 30% 31% 32% singles

online

19.8m

18.3m

16.4m

15.0m

13.3m

11.9m

9.6m 10.6m

2008 2009 2010 2011 2012 2013 2014 2015

Source: Eurostat, TNS Brand Awareness

Throughout our discussions with several players in the online dating space, one of the

reasons given for the steady growth in online singles willing to pay for online dating services

is that a large portion of these individuals are users of online match-making services, such as

eHarmony, Match.com and Parship to name a few. Match-making users are more willing to

pay for online dating services as they are typically an older demographic with higher levels of

disposable income when compared to those users only willing to use free sites.

White Labelling

The other model which some players have used to enter the online dating market has been

through white labeling – providing publishers affiliates, marketeers, etc. with an online dating

platform for them to monetise their user base and/or traffic.

Two of the most successful European players in this space are Cupid plc and Global

Personals. Cupid was founded in 2005 and hosts over 100 websites through its own network,

white label and technology licensing partnerships. Global Personals was founded in 2003

and has a portfolio of over 7.5k websites in its portfolio.

By operating a portfolio of websites, Cupid and Global Personals are able to address multiple

sectors and dating options without compromising the identity of its key brands. Their

combined databases of over 72m registered users allows for considerable potential for cross-

marketing, with the average customer registering at two or more Cupid/Global Personal sites.

This model has proven to be quite successful with Cupid having revenues of £53m+ and

EBITDA of £10.6m (19% margin) in FY11, and Global Personals reporting annualized

revenues of $62m+ with EBITDA margins of circa 13%.

7

GP Bullhound LLPGP B ULLHOUND – ONLINE D ATING – A LABOUR OF LOVE

Market Size and Growth

Despite being well established, the global online dating market can be difficult to quantify -

most statistics relate to the US market. There are a number of reasons for this. Firstly, there

is no official industry body or trade association regulating the dating industry which provides

official figures. Secondly, the US is essentially the birthplace of online dating and its largest

market. The US makes up close to 50% of global online dating industry, in revenue terms.

With some notable exceptions, such as Russian (Mail.ru) and Chinese (Jiayuan.com) sites,

many non-US sites are in fact owned by or are localised versions of large US players who

have expanded out of their home market, with ownership of the remaining sites being

relatively fragmented across geographies.

The 12 US-based dating companies together account for almost 60% of the traffic of the top

30 global dating companies by unique monthly visitors (UMVs), with Match.com taking the

lion share of global eyeballs.

EXHIBIT 7: TRAFFIC TO TOP 30 GLOBAL DATING SITES DOMINATED BY US PLAYERS

7.4%

5.5% US

12.8%

4.9% China

3.4% Russia

3.3% Australia

2.9% UK

2.6%

France

Germany

Other

India

57.2%

Source: comScore

In spending terms, the US online dating market generated approximately $1.1bn in 2009,

and is expected to rise to almost $2.4bn in 2013, representing a CAGR of 21.5%, with the

global market estimated to be worth $4bn in 2012. According to market research publisher

Tampa, key growth drivers are expected to be geographic expansion and mobile app roll-

outs.

EXHIBIT 8: SIZE OF ONLINE DATING MARKET

2009A 2013F

$4.5bn

$2.4bn

$2.1bn

$1.1bn

US Global

Source: Forrester, Jupiter, Mintel, Marketdata Enterprises, GP Bullhound

8

GP Bullhound LLPGP B ULLHOUND – ONLINE D ATING – A LABOUR OF LOVE

The Rise of Social Discovery

Since the breakthrough of Facebook and social networks, social features (such as Facebook

integration, Like buttons, shareable content, ratings and reviews, commenting functions,

polls, etc.) have been increasingly present in consumers’ everyday online experience. Social

features have been more and more integrated with all sorts of online offering: consumers

have access to such features while reading news, watching video or accessing a wide array

of other content online whether for work (e.g. LinkedIn) or leisure (e.g. travel or games).

Dating is one of the quintessential social activities, and Facebook and the other social

networks have helped people looking to make new friendships and relationships online.

Many people realized that Facebook and other social networks could be very powerful (and

free) instruments to meet new people. As a consequence, in comparison to the early days of

social networks when people would go to social networks to make new friends or interact

with existing ones and to dating websites to find a match, now the boundaries have blurred

considerably. Social networks now clearly focus on promoting “sharing” with a user’s existing

network therefore enabling companies to provide a better user experience and monetise

their user base more effectively. As a consequence, social networks have shied away from

incentivizing users to overly expand their networks but rather are interested in their users

giving access to deeper content and information. This in turn allows Facebook and other

social networks to better monetise their user base through the sale of targeted advertising.

EXHIBIT 9: EVOLUTION OF SOCIAL NETW ORKS AND ONLINE DATING MARKETS

Existing Friends Meet New People

2004 Social Networks Online Dating

Social

2014 Casual Dating Online Dating Matchmaking

Discovery

Source: GP Bullhound

From the online dating point of view, the dating sector in the traditional sense is now more

fragmented than ever, with over 1,500 dating sites in the US alone. Matchmaking and

“traditional” dating are more likely to attract a more mature and wealthy demographic (mainly

through subscription business models), and niche and casual dating sites looking to

monetise younger and more casual users (mainly through freemium business models). In

between social networks and online dating, a new proposition named “social discovery” or

“meet new friends” has been evolving in parallel. Social discovery focuses on bringing

together the casual elements of meeting new people, with a variety of aims which include,

but are not limited to, dating (see Exhibit 9).

9

GP Bullhound LLPGP B ULLHOUND – ONLINE D ATING – A LABOUR OF LOVE

The concept of enabling users to meet new friends is of course not new: in the first

generation of social networks (e.g. MySpace, Bebo, Hi5) there was often an element which

allowed users’ to meet new people online. This is in contrast to the now well known

“someone you might know” functionality of today’s Facebook, LinkedIn, etc., which focuses

on building an online relationship through your existing real life contacts.

New social discovery sites have recently appeared, catering to the specific need of meeting

new people for whatever purpose. Social discovery websites typically gather profile and

contact information from one or more social networks with which the user has an account,

and then use it (as well as users inputs made into their own platforms) to tailor the offering to

that user accordingly, and monetise him or her through the sale of value added services,

membership subscriptions or advertising.

Social discovery is a concept which can be applied to a variety of activities as long as they

are suited for doing something with other people. Dining is an example: Grubwithus is a

Chicago-based start-up which offers a “Social Dining” service, where friends and potential

new friends create and join meals for 6-10 people. Most meals are themed or hosted by a

Grubwithus Group to help bring together interested and similar people as well as to guide

initial conversation topics at the meal. Each individual pays in advance through Grubwithus

for a set menu, and the company takes a fee. In the UK, Dinmill offers a very similar service,

calling itself a “Social Dining Network”.

EXHIBIT 10: SOCIAL DISCOVERY SERVICES (REPRESENTATIVE, EXCLUDING DATING)

Dinner Travel Other

Source: GP Bullhound

Social discovery can also target travelers: services such as Mysocialpassport (founded 2011)

and Travbuddy.com (founded 2005) allow users to search for new people to meet while on

the road, people to organise a trip together, or to share reviews and other travel-related

content. These companies typically monetise their user base through advertising and lead

generation. Tripl (founded 2010) allows users to find out who their friends would recommend

as a “must meet” local when traveling the world. Tripl collects data from the incumbent travel

companies and in return provides them with opportunities to re-target potential travelers with

customized and relevant offers. A B2B proposition such as Tripl may prove winning versus

the C2C ones, where competition for advertising and value-added service revenues is more

intense.

Social Dating: A Natural Evolution from Social Networks and Online Dating

A common way in which social discovery enables people to build connections beyond their

local networks – and find dates – is to link them based on shared interests. In the last 3-5

years, a large number of companies have emerged, specifically focusing their attention on

this aspect of social dating. Why?

10

GP Bullhound LLPGP B ULLHOUND – ONLINE D ATING – A LABOUR OF LOVE

First, there is a monetization / user behavior consideration. Whereas marriage, matchmaking

and “traditional” dating websites have the aim of pairing users which eventually get off the

websites when they have found a match, social discovery tends to lend itself better to

meeting new people for casual dating, as opposed to matchmaking. The matchmaking model

(monetized mostly through subscriptions) lends itself well for demographics with higher

purchasing power looking for a long-term partner, which have a larger disposable income.

On the contrary, freemium monetization models with frequent transactions of a smaller ticket

size can be more attractive to younger demographics who may seek to step in and out of the

casual dating arena for a few years.

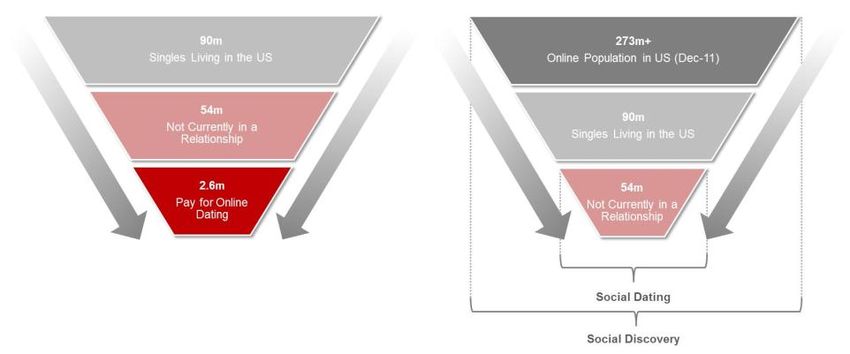

Secondly, the sheer size of the potential market has to be considered. The dating and

matchmaking funnel gets narrow towards the bottom: the vast majority of potential customers

for dating websites are singles, using the internet, who are willing to pay for such services. If

we take the US, for example, there are 90m singles (not married), of which 54m not currently

in a relationship, of which only 2.6m pay for online dating services. Match.com has 1.8m

1

paying members, or 69% of the addressable market . There are exceptions: some non-

singles might still use services like Ashleymadison.com (a website specifically targeted at

affairs); also, a portion of the 54m singles not in a relationship would be willing to pay for

other dating services in freemium or casual dating websites, for instance.

It is our belief that the funnel for the dating sector as a whole (including casual and niches) is

larger than the estimate above. However, the potential market for social dating and social

discovery is even larger. In the broadest sense, the market could be defined as every online

adult in the US, and a good proxy could be represented by the over 100m Facebook users in

the US. For social dating, the addressable market could be represented by a high portion of

the 54m singles in the US, and is much larger than the market willing to pay for matchmaking

services (see exhibit 11).

EXHIBIT 11: MATCHMAKING VS. SOCIAL DISCOVERY FUNNEL

US MATCHMAKING FUNNEL US SOCIAL DISCOVERY FUNNEL

Source: GP Bullhound, Match.com, Broker research, Internet World Stats

1

Source: Match.com, Deutsche Bank

11

GP Bullhound LLPGP B ULLHOUND – ONLINE D ATING – A LABOUR OF LOVE

Not surprisingly a large number of companies have sought to commercialise this massive

opportunity. Badoo, the most well-established player, was founded in 2006, and is very open

in its casual dating intentions. The primary connecting factor is the shared location, rather

than interests. The formula has worked so far: Badoo is now one of the largest (and

reportedly most profitable) companies in the space; in May 2012 TechCrunch reported that

Badoo had over 150m users and is one of the largest social networks globally, according to

ComScore. Badoo operates in 35 languages and has been reported to have an annual

revenue run-rate of $150m.

Another very popular service is Zoosk, a social dating community working as a Facebook

app. Founded in 2007, Zoosk is available in more than 25 languages and has subscribers in

more than 60 countries. The other large player in the space is Tagged: originally founded in

2004 as a teen-only social network, it pivoted to its current social discovery focus in late 2007

and has been profitable since 2008. The company’s service is designed to enable anyone to

meet and socialise with new people through social games, customized profiles, virtual gifts,

advanced browsing features and other value added services. Tagged has over 330 million

members in 220 countries. In 2011, the company had revenues of $43m (+35% vs. 2010)

and doubled its staff.

The key to the profitability of Zoosk, Badoo, Tagged and other established social dating

websites is their monetization through freemium models, heavily reliant on Value Added

Services. Registrations to such sites are typically free but users can pay for services such as

the ability to boost themselves up on the display rankings in the form of bidding war, the

ability to see who viewed their profile and rated them highly, or virtual gifts (see exhibit 12 for

more examples). Social games and advertising can be also featured on the platform and

provide additional monetization streams. There might be an option for a monthly subscription

to get all the benefits that can be bought individually thus giving users “premium” status on

the site.

EXHIBIT 12: VALUE ADDED SERVICES TYPICALLY USED IN SOCIAL DATING

Value Added Service Description

On certain sites users have to purchase credits to communicate, special “urgent”

Credits for messages

messages, increase inbox size

Allows users to come on top of search results and landing pages with certain

Highlight / Boost

criteria

No advertising Removes ads from the site

Special filtering Allows users to perform more tailored search, e.g. by attractiveness (measured as

options other users’ ratings, which are typically not public)

Browse Anonymously Allows users to browse other users’ profiles anonymously

See who likes you Allows users to see who rated them highly or “liked” them

Virtual gifts Users can typically send gifts (e.g. virtual flowers) for a fee

Source: GP Bullhound

Another key for these social dating services’ success has been related to user acquisition.

Historically, such sites had an inherent advantage in terms of user acquisition versus the

incumbent dating and matchmaking players. The most successful relied more heavily on

12

GP Bullhound LLPGP B ULLHOUND – ONLINE D ATING – A LABOUR OF LOVE

social networks themselves to increase traffic via viral mechanics, in contrast to the

notoriously expensive acquisition methods of traditional players. This had an enormous

impact in terms of profitability: Badoo’s EBITDA margins were rumored to be over 50% in

2011, vs. margins of the most successful matchmaking services at c.25%-30%.

Social Dating 2.0: A New Crop of Players

Most of the companies mentioned above, in our view, represent a “first generation” response

to the social dating question. Their business model is heavily reliant on casual dating

dynamics and is still dependent on a constant stream of new users in order to maintain

liquidity on the platform and ensure a good product experience. In some instances

consumers have expressed concerns over some of these websites in terms of their actual

quality and reputation: anecdotes of fake profiles run by algorithms (“bots”), difficult

membership cancellations and other aggressive marketing techniques have been reported in

the wider dating industry, in particular, on services with a stronger orientation towards casual

encounters. The reputation of certain websites might end up being counterproductive: less

women liking them starts a vicious cycle which limits the appeal of the service. Nevertheless,

a number of new generation players are emerging with a fundamental difference to compete

with the established social dating incumbents which are in fact social networks pivoted on

casual dating and transactional in nature.

This new breed of social dating players claims to provide a better user experience by

integrating directly with a user’s existing social graph on Facebook, and use and cross-

reference this deeper level of user data. One of these services, Thecomplete.me, is a tool

which integrates with Facebook with a focus on meeting new people who share your

interests and friends. It offers search and filtering functions and control over who sees what

and when. The implicit aim of the website is to provide users with the best possible first date.

If you are not single, as a user you can nudge your single friends to go out on dates by

leveraging your and your friend’s network. Founded in 2011 by Brian Bowman, former head

of product of Match.com, the company has among its early investors; Markus Frind, CEO

and founder of PlentyOfFish, the online dating freemium website.

EXHIBIT 13: SOCIAL DATING SERVICES (REPRESENTATIVE)

Source: GP Bullhound

Another start-up in the space is Likebright, founded by Nick Soman in Seattle in late 2011,

about the same time as Thecomplete.me. The mechanics for Likebright are fairly similar:

seamless and fast integration with Facebook, and focus on meeting new people with shared

interests. The slightly different tilt is that there is a stronger emphasis of getting introduced by

friends, under the assumption that, like in real life, friends’ recommendations and

13

GP Bullhound LLPGP B ULLHOUND – ONLINE D ATING – A LABOUR OF LOVE

introductions can improve the probability of a successful date or match. The interface is also

different from Thecomplete.me, with a simple Pinterest-like way of displaying profiles.

Another difference is the absence of detailed search and filtering functions: the service for

the most part automatically suggests who users could be interested in. Likebright is

particularly aimed at women, who too often don’t have satisfactory experiences on dating

websites: the introduction and friend of a friend mechanics are specifically targeted to

improve women’s trust in the platform.

In November 2012, IAC-owned OKCupid announced the launch of a new “people discovery”

service, Tallygram. The service (now only an Alpha version) uses the Facebook social graph

and the OKCupid’s experience with questionnaires to explore and discover new

relationships. A similar service is offered by Pinstant Karma, which helps connect users with

similar interests: users can create Pinterest-style boards filled with images of their favorite

places, special memories, foods and anything else that helps tell their story (and helps the

site to match them with others).

An alternative approach is taken by Huntcha: a social dating service with the aim of helping

users discover who their secret love is without the risk of rejection. Huntcha pairs someone

with people also registered on the service through Facebook. Only when they have both

expressed interest in one another, Huntcha privately reveals a “crush” connection.

All these second generation social dating companies mentioned above are a response to the

fact that a universal front door for people interested in dating does not exist. At least it does

not exist in the same way as Facebook is the front door to connect with your existing friends

online. Instead, users now look for a date on a myriad of alternatives in the form of dating

websites and social networks. The underlying belief motivating many social dating

entrepreneurs is that, whoever is successful in creating a new generation social dating

service which is not just a good dating website disguised as “meet new people”, but benefits

from the integration with the social graph and a person’s existing network of friends, has the

possibility to become a mass market service.

Challenges Ahead for Social Romance

Typically, a dating company is successful by attaining critical mass through the acquisition of

increasingly costly traffic. Gone are the days where virality on Facebook could propel a social

service company into the stratosphere with a disproportionately low marketing spend. New

rules on Facebook limit the sharing and re-posting of such applications due to concerns of

social graph pollution. Furthermore, even if some industry participants say that the stigma of

dating is largely gone in most developed markets, there still is a certain understandable

reluctance attached to publishing your membership to a social dating or social discovery

service on Facebook timeline.

In the past, certain dating and social discovery companies chose to rapidly scale their

member base, exploiting the fact they were the first of their kind, and only then improve their

product (e.g. POF, Zoosk, BranchOut). Now, the second generation players are focused on

getting the product intrinsically right, mainly through social content and deep integration with

Facebook, and only then attempting to exploit the underlying liquidity of the Facebook

14

GP Bullhound LLPGP B ULLHOUND – ONLINE D ATING – A LABOUR OF LOVE

platform to grow. Companies need to demonstrate that they can provide valuable,

transparent services and make money at the same time without using aggressive or

questionable techniques that has led to some of the past PR scandals.

Social discovery businesses are mostly reliant on micro transactions, advertising and a

subscription component to make money. Other social discovery players (e.g. e-commerce or

travel players mentioned earlier in this report) would need to find alternative ways of

monetizing their platforms with more emphasis on lead generation and advertising. The

growth of social discovery is evident; the execution is difficult but the potential rewards are

sizable. Some players are creating new offerings, and others are just rebranding themselves

from online dating to social discovery in order to exploit the buzzword. Those who get the

model right, however, will be able to command a slice of a much larger pie than the existing

dating or business networking markets. It is our belief that in the future traditional dating

models will still exist, however a growing portion of the online population, boosted by younger

demographics, will use social discovery as their “front door” to online dating.

15

GP Bullhound LLPGP B ULLHOUND – ONLINE D ATING – A LABOUR OF LOVE

Dating has Become a Key Category in Mobile

Arguably, the major trend currently sweeping the digital landscape is the inescapable rise of

the mobile Internet. Increasing smartphone and tablet penetration, progress in mobile

operating systems, mobile’s always-on nature, and other popular features such as geo-

location, has led to the spectacular growth of mobile social media, applications (apps),

games, and a vast array of solutions for consumers and businesses.

EXHIBIT 14: US MOBILE DATING MARKET EVOLUTION

$415m

$381m

$340m

$295m

$251m

$213m

$165m

$109m

$43m

2009A 2010A 2011A 2012E 2013E 2014E 2015E 2016E 2017E

Sources: IBISWorld June 2012

The worldwide mobile app market was estimated at $7.3bn in 2011 by IDC, and is set to

grow over 50% annually to $35bn in 2015. This switch to mobile is inevitably affecting the

online dating world: the global mobile dating market was estimated to be $1bn in 2011 and is

forecast to reach $2.3bn in 2016 (Juniper Research). In the US, the market has grown over

70% per year to $212m in 2012, accounting for c.4% of the US mobile app market. The

industry is forecast to grow 14% per year to over $400m in 2017 (See exhibit 14). In

Germany, Mobile Dating reached €25m in 2011, accounting for c.10% of the overall German

online dating market, and is forecast to grow by 30% in 2012.

This rapid growth has been facilitated by a number of drivers:

Firstly, getting a date is an inherently social activity which people have conducted

on mobile phones as soon as the first mobile phones appeared, by calling and

sending SMS.

Furthermore, the two top activities that users look for on dating websites, browsing

and sending messages, lend themselves extremely well to mobile.

As smartphone penetration and mobile network speed have dramatically increased

over the past few years, they have facilitated online dating apps.

Mobile Dating Usage Rising Sharply

The time users spend on mobile has greatly increased, and mobile dating apps have

improved considerably to reflect the increasingly social nature of the dating proposition.

Users – thanks to similar features in social networking applications – can transition

seamlessly and become accustomed to browsing potential partners and uploading pictures

16

GP Bullhound LLPGP B ULLHOUND – ONLINE D ATING – A LABOUR OF LOVE

and other personal information on their dating profiles via mobile. Another key consideration

is that, with a proprietary mobile app handling communication between dating users at any

time in any place, there are less concerns related to sharing private information such as

phone numbers. Within the world of mobile apps, the largest category on US Smartphones,

behind gaming, is Social Networking, in which dating apps appear (ComScore, July 2011).

EXHIBIT 15: DAILY TIME SPENT ONLINE DATING IN THE US – ONLINE VERSUS MOBILE

Online Dating (Websites) Mobile Dating (Apps)

8.9mins 8.4mins

8.4mins 8.3mins

4.8mins

3.7mins

Jun 2010 Dec 2010 Jun 2011

Sources: comScore, Alexa, Flurry Analytics.

Enhanced functionality and a proliferation of dating apps have been driving up both the sheer

number of users dating on mobile, and the average time spent on mobile dating applications.

In the US for instance, in the space of one year the average daily time spent on mobile

dating has risen from 3.7 minutes (less than half that spent on dating websites) in June 2010,

to 8.4 minutes, exceeding time spent on online dating sites in June 2011 (see Exhibit 15).

The transition towards mobile dating is reflected not just in the length of time spent accessing

mobile apps, but also in the frequency with which this is done. In 2011 the average US user

opened a dating application twice a day, for a little under 2 minutes each time. Now he or she

typically opens their app over 5 times a day, but for shorter periods of time. This is a

reflection of the “always on” nature of mobile dating apps.

The overall trend in online dating is towards both greater internet and mobile app usage –

they are not mutually exclusively and each is capable of driving the other. The main

takeaway though, is that analyses performed by Flurry Analytics on ComScore and Alexa

data show how mobile dating is already more popular than desktop dating: 17% of unique

internet users use mobile dating apps, vs. c.13% in desktop dating in June 2011 (see Exhibit

16).

17

GP Bullhound LLPGP B ULLHOUND – ONLINE D ATING – A LABOUR OF LOVE

EXHIBIT 16: % OF ALL UNIQUE INTERNET USERS DATING ONLINE BY METHOD

17%

15%

13%

12%

Internet Mobile Apps

Jun 2010 Jun 2011

Source: Compete, comScore, Alexa, Flurry Analytics

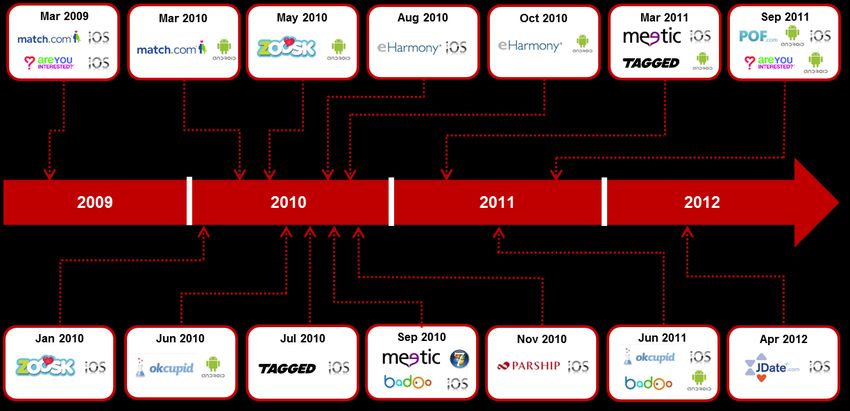

Incumbents and New Players are Pursuing the Mobile Dating Opportunity

Not long after smartphones were introduced, the large incumbent players in the dating space

realized the potential of the mobile market, and began launching their own mobile version of

their services shortly after, typically in the form of lighter, mobile-accessible websites,

Facebook mobile apps and dedicated mobile applications. Match.com launched its iPhone

app in March 2009, the first company to allow its mobile users to edit their profile, upload

photos, and even locate singles in their area using an opt-in to a location-based feature.

SNAP Enteractive’s AreYouInterested? launched a casual dating app with similar

functionalities in the same month. Others followed suit with similar adaptations of their

desktop services for iPhone, Android and other mobile operating systems (see Exhibit 17).

EXHIBIT 17: ONLINE DATING INCUMBENTS MOBILE APP LAUNCHES

Source: company press releases, press articles, GP Bullhound.

The decision to bet early on the mobile market has proved to be a wise one; for many of

these players, mobile apps represent the strongest growth driver in terms of users and

revenues. In May 2012, Badoo announced its mobile usage has risen over 100% in the last

six months, and that 68% of new users came on the service via mobile. The Social Discovery

service MeetMe (formerly MyYearbook), in August 2012 reported $1.3m in mobile revenues,

up 73% Q-o-Q and 152% Y-o-Y, and accounting for c.10% of the company’s revenues for

18

GP Bullhound LLPGP B ULLHOUND – ONLINE D ATING – A LABOUR OF LOVE

the quarter. As incumbents such as Match.com have been quick to capitalise on their

established user bases by migrating users to mobile, and focused on gaining a share of the

quickly growing mobile dating market, a large number of new entrants have launched mobile-

only propositions. Many of these new entrants offer fairly standard dating applications such

as the one offered by the incumbents, which might be focused on a niche or place more

reliance on geographical location.

As happened in eCommerce, a lot of emphasis and hope has been put on geo-location for

mobile dating. Most online mobile apps have geo-location functions; however, so far geo-

location dating has remained a niche segment, mainly due to concerns about privacy and

safety. Many users are hesitant to give away their location to strangers, especially after a

number of crime cases related to geo-location apps have been brought to the public

spotlight. Geo-location has enjoyed more success in the gay community, with apps such as

Gaydar and Grindr, where same-sex members appear to be less reluctant about using such

services. Since launching in early 2009, Grindr, a male-only application, has grown to reach

more than 4m users worldwide in June 2012 (with 500,000 new users in Q2 2012 alone) and

more than 1m active unique daily visitors. A large number of straight mobile geo-location

apps exist and are all fairly similar, often lacking the necessary liquidity: users have to install

multiple apps to figure out which one works best in a given place in a given time.

SingleSquare, for instance, is a freemium app that uses FourSquare technology to find

potential matches nearby.

Another much talked about space in the mobile dating sector is Video-dating. With

increasingly fast mobile connectivity and good quality cameras on smartphones and tablets;

it is now possible to have an efficient video-conversation. A plethora of start-ups have

naturally translated the concept to dating, in a video speed dating model. Companies such as

Flikdate, Mobilevideodate, SpeedDate, WhosHere, offer such services. Users typically sign

up (usually with their Facebook login), filter which kind of potential dates they are interested

in – male or female, height, weight, body types, etc., add a short profile and add a photo.

Once matched users can send messages and have a short introductory video date.

Typically, every conversation is limited to a set time and costs users a fixed amount; after

that, users can pay with credits for longer video dates.

EXHIBIT 18: MOBILE DATING APP LANDSCAPE (REPRESENTATIVE)

Source: GP Bullhound

Speed dating and video dating concepts have proved to be an attractive product for a niche

audience, however the market has so far demonstrated to not be ready yet for such a

19

GP Bullhound LLPGP B ULLHOUND – ONLINE D ATING – A LABOUR OF LOVE

proposition on a larger scale. Live video communication with strangers and video dating have

been tried in the past on the desktop format with mixed fortunes: Chatroulette, although not

specifically aimed at dating, has enjoyed enormous popularity and media attention, but was

highly penalized by the lack of moderation. Airtime, founded by former Facebook and Skype

executives, has resorted to Facebook identification to try and limit such risks, and pulls data

from Facebook to increase match probability by pairing shared interests. WooMe.com

launched with a similar speed date proposition in 2007 and raised over $10m from Index

Ventures, Mangrove Capital Partners and Atomico Ventures; the company was reportedly

acquired by Zoosk in November 2011 in a rumoured fire sale.

Mobile Dating: The Challenges

Many challenges exist in order to build successful mobile dating companies: user

monetization is, as for the rest of mobile, complicated. The best models have proven to be

freemium apps monetised by advertising and by charging for value added services.

Gamification and social aspects are top of mind for mobile dating app providers. Handmade

Mobile, the company managing the Flirtomatic mobile site and app, has reported 6m

registered users and most of their revenues and profits come from mobile value added

services. The main challenge is that mobile dating is not immune from the inherent churn

dynamics of the wider dating market, and the user acquisition cost for a mobile user is higher

than for a desktop user. Companies are under more pressure to get their user acquisition

and monetization strategies right from the start, or else they will face serious difficulties in

reaching or maintaining profitability, once the initial viral growth stops. Other challenges have

not been solved yet: geo-location dating carries serious privacy and safety risks and has to

be improved in order to offer better user experiences. Mobile video dating is still a niche in its

infancy.

Ultimately, we are convinced that mobile dating will be a vast industry, and has the potential

to grow more rapidly than other mobile categories. Much trial and error is still needed, and a

universal model on how to make mobile dating work on a large scale has not been found to

date. But by making it easier for people to meet and date spontaneously, mobile dating is not

so much a trend within the online dating industry, but a natural progression of the entire

concept of online dating itself. Whoever is able to capitalise on this underlying trend will be in

a position to reap significant rewards.

20

GP Bullhound LLPGP B ULLHOUND – ONLINE D ATING – A LABOUR OF LOVE

Selected Company Profiles

Founded in 2002, Ashley Madison is a niche dating player which actively encourages and

enables people to have affairs, with a strong emphasis on protecting member privacy. The site

provides a freemium service which requires members to purchase credits to unlock custom-

mail messaging and chat sessions, and to send virtual gifts. Ashley Madison is famous for its

provocative ad campaigns and bold PR stunts: in April 2012 it offered $1m to any woman who

could prove she slept with football player Tim Tebow, a self-professed virgin. The site attracts

over 1.4m UMVs, has over 8.5m users and in 2011 reported revenues of close to $60m.

Ashley Madison is owned by Avid Life Media, a niche dating site operator which also owns

gay dating portal Man Crunch, and CougarLife, which connects older women with younger

men.

Founded in 2006, Badoo is a social dating network accessible via both computer and a mobile

app. It operates a freemium model which enables users to sign up and send messages for

free, but charges them to promote themselves to the top of search listings and to activate

“super powers” such as seeing who has been reading their messages, and viewing other

profiles anonymously. Badoo reported to have over 150 million registered users in over 180

countries and a revenue run rate of $100m. In 2012, Badoo acquired Hot or Not, a site which

allowed users to rate the attractiveness of photos submitted by others. The company is owned

by investors including Finam Capital, which invested $30m in 2008.

Founded in 2005, Cupid is a listed UK and International dating player which operates a broad

portfolio of 25 portals across traditional, casual and niche dating. It also operates a mobile app

and a white label dating service, and has a broad affiliate network. Active in 15 countries,

Cupid attracts over 3.6m UMVs and more than 480,000 paying subscribers, with 56m member

profiles registered and over 16m active users. In 2011, the company doubled its revenues to

£54m. In July 2012, Cupid acquired French Genie Logiciel for €3.7m, and in September niche

dating site Uniformed Dating for £7m. The company has been publicly listed since 2010 and

has a market capitalisation of c. £150m.

Founded in 2008, eDarling is a Germany-based freemium dating site which operates 14 local

language portals across Europe. It also publishes dating-related content through its “Science

of Love” blog. The site is 30% owned by eHarmony and its main competitor is Match.com-

owned Meetic. eDarling attracts more than 1.4m UMVs and claims more than 12m members.

The company is expecting 2012 revenues to be up 30% on 2011 to around €50m, making it

one of the top European dating players by revenues. Other investors in eDarling include the

venture arm of German publishing group Holtzbrinck, IBB Beteiligungsgesellschaft and Rocket

Internet.

21

GP Bullhound LLPGP B ULLHOUND – ONLINE D ATING – A LABOUR OF LOVE

Founded in 2000, eHarmony is a subscription-based matchmaking site with a strong focus on

compatibility matching via its proprietary algorithm. It does not allow users to browse profiles

freely, but sends them regular samples of compatible matches. eHarmony focuses on

attracting quality, relationship-minded people and filtering out undesirables through its lengthy

registration questionnaire. The site attracts over 2.4m UMVs. It is estimated to have achieved

$300m of revenues and EBITDA margins of c.30% in 2011, and to have converted around

24% of its active members into paying subscribers, nearly three times the industry average.

eHarmony is active in Australia, Canada, the UK and Brazil and has a European presence

though a 30% stake in Germany-based eDarling. The company is privately owned by

investors including Juvo Capital, Saints Capital, Sequoia Capital and Technology Crossover

Ventures.

Founded in 1997, FriendScout24 is a freemium dating site which operates across seven

European countries and has a leading position in Germany, Austria and Switzerland. It

operates a freemium business model with a basic free service and a monthly fee-paying

membership with enhanced features. FriendScout24 reported to have more than 10 million

members, over 200,000 daily active users and more than 12,000 new users per day. In 2011

FriendScout24 launched Secret, a portal for people interested in flirting and casual

encounters. The company is a subsidiary of Deutsche Telekom and part of the Scout24 group,

a series of content portals which also cover cars, electronics, personal finance, real estate,

jobs and travel

Founded in 1997, Global Personals is a diversified dating player which operates its own

portals and provides white label dating services for thousands of others. Global Personals’

own sites cover generic, casual, and niche dating. Its white label offering provides dating

software (including mobile, API and social network integration), membership databases,

payment processing and customer support for over 7,500 sites. The white label dating client

provides the site’s brand, design and marketing, and is monetised through a revenue sharing

model. Global Personals reported over 200 million page views per month, over 8 million daily

interactions, and annualised revenues in excess of $74m. The company is privately owned.

Founded in 2009, Grindr is a location-based mobile app which enables gay, bi-sexual or bi-

curious men to meet other like-minded men in their vicinity. Grindr operates a hybrid business

model, offering its app as both a free ad-driven version (Grindr) and a monthly fee-paying

alternative (Grindr Xtra) with enhanced features such as push notifications, quick menus and

ad-free browsing. The app is available across a wide range of devices including the iPhone,

iPad, Android devices and selected Blackberry models. Grindr claims to have more than 4

million users in 192 countries, 1 million daily users and around 10,000 new users every day.

The company is owned by its founder and CEO, Joel Simkhai, who has subsequently

launched a social dating app for straight people, called Blendr.

22

GP Bullhound LLPYou can also read