A Leading North American Transportation and Supply Chain Company - INVESTOR PRESENTATION MAY 2019 - CN Rail

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

A Leading North American Transportation and Supply Chain Company INVESTOR PRESENTATION MAY 2019 TSX: CNR NYSE: CNI

Forward-looking statements

Certain statements included in this presentation constitute “forward-looking statements” within the meaning of the United States Private Securities

Litigation Reform Act of 1995 and under Canadian securities laws. By their nature, forward-looking statements involve risks, uncertainties and

assumptions. The Company cautions that its assumptions may not materialize and that current economic conditions render such assumptions,

although reasonable at the time they were made, subject to greater uncertainty. Forward-looking statements may be identified by the use of

terminology such as “believes,” “expects,” “anticipates,” “assumes,” “outlook,” “plans,” “targets,” or other similar words.

2019 key assumptions

CN has made a number of economic and market assumptions in preparing its 2019 outlook. The Company assumes that North American industrial

production for the year will increase by approximately two per cent, and now assumes U.S. housing starts of approximately 1.25 million units

(compared to its January 29, 2019 assumption of approximately 1.28 million units) and U.S. motor vehicle sales of approximately 17 million units. For

the 2018/2019 crop year, the grain crops in both Canada and the United States were in line with their respective three-year averages. The Company

assumes that the 2019/2020 grain crops in both Canada and the United States will be in line with their respective three-year averages. CN assumes

total RTMs in 2019 will increase in the high single digits versus 2018. CN assumes continued pricing above rail inflation. CN assumes that in 2019, the

value of the Canadian dollar in U.S. currency will be approximately $0.75, and now assumes that in 2019 the average price of crude oil (West Texas

Intermediate) will be in the range of US$60 to US$65 per barrel (compared to its January 29, 2019 assumption in the range of US$50 to US$55 per

barrel). In 2019, CN plans to invest approximately $3.9 billion in its capital program, of which $1.6 billion is targeted toward track and railway

infrastructure maintenance.

Forward-looking statements are not guarantees of future performance and involve risks, uncertainties and other factors which may cause the actual

results or performance of the Company to be materially different from the outlook or any future results or performance implied by such statements.

Accordingly, readers are advised not to place undue reliance on forward-looking statements. Important risk factors that could affect the forward-

looking statements include, but are not limited to, the effects of general economic and business conditions; industry competition; inflation, currency

and interest rate fluctuations; changes in fuel prices; legislative and/or regulatory developments; compliance with environmental laws and regulations;

actions by regulators; increases in maintenance and operating costs; security threats; reliance on technology and related cybersecurity risk; trade

restrictions or other changes to international trade arrangements; transportation of hazardous materials; various events which could disrupt

operations, including natural events such as severe weather, droughts, fires, floods and earthquakes; climate change; labor negotiations and

disruptions; environmental claims; uncertainties of investigations, proceedings or other types of claims and litigation; risks and liabilities arising from

derailments; timing and completion of capital programs; and other risks detailed from time to time in reports filed by CN with securities regulators in

Canada and the United States. Reference should be made to Management’s Discussion and Analysis in CN’s annual and interim reports, Annual

Information Form and Form 40-F, filed with Canadian and U.S. securities regulators and available on CN’s website, for a description of major risk

factors.

Forward-looking statements reflect information as of the date on which they are made. CN assumes no obligation to update or revise forward-looking

statements to reflect future events, changes in circumstances, or changes in beliefs, unless required by applicable securities laws. In the event CN does

update any forward-looking statement, no inference should be made that CN will make additional updates with respect to that statement, related

matters, or any other forward-looking statement.

2

Non-GAAP Measures

CN reports its financial results in accordance with United States generally accepted accounting principles (GAAP). CN also uses non-GAAP measures in

this presentation that do not have any standardized meaning prescribed by GAAP, including adjusted performance measures, free cash flow, adjusted

debt-to-adjusted EBITDA multiple, adjusted dividend payout ratio, return on invested capital (ROIC) and adjusted ROIC. These non-GAAP measures may

not be comparable to similar measures presented by other companies. For an explanation of adjusted dividend payout ratio, ROIC and adjusted ROIC,

refer to the Appendix to this presentation. For further details of the other non-GAAP measures, including a reconciliation to the most directly

comparable GAAP financial measures, refer to the supplementary schedules entitled Non-GAAP Measures for the 2019 First Quarter Results and for the

years 2013 to 2018, as well as the Company’s 2012 Q4 Financial Statements, available at www.cn.ca/financial-results.

CN's full-year adjusted earnings per share (EPS) outlook excludes the expected impact of certain income and expense items. However, management

cannot individually quantify on a forward-looking basis the impact of these items on its EPS because these items, which could be significant, are

difficult to predict and may be highly variable. As a result, CN does not provide a corresponding GAAP measure for, or reconciliation to, its adjusted EPS

outlook.

All amounts in this presentation are expressed in Canadian dollars, unless otherwise noted.

3

Investment Highlights: Long-term profitable growth

Leveraging network advantages to support our

operational and service excellence

Delivering 15%+ adjusted ROIC year after year since 2012

Solid pipeline of growth opportunities (organic and inorganic)

4

Content

Balancing

1 Company

Highlights 2 Our Key

Strengths 3 Operational

and Service

Experience

Innovating Creating

4 Markets 5 Everywhere

Every Day

6 Value for

Shareholders

5

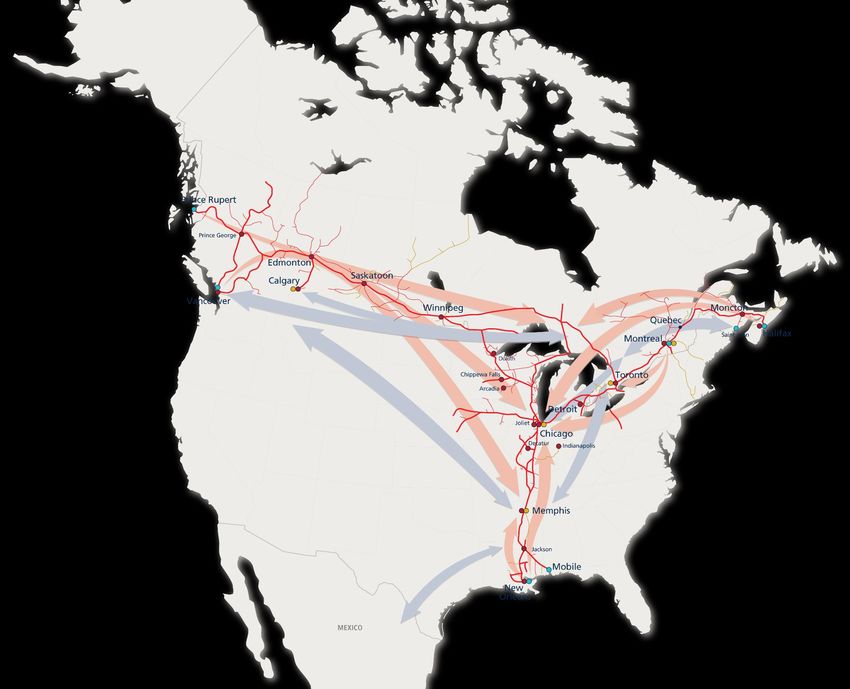

Company Highlights Summary • Market capitalization of ~$90B • True backbone of the North American economy • Uniquely connecting 3 coasts • Strong profitable growth over the years • Solid track record in creating value for customers and shareholders

A true backbone of the North American economy

19,500 6.0M

• Only Class I network spanning Canada

Route miles Carloads

and mid-America, connecting North

America to global markets on 3

coasts, providing geographic,

customer and product diversity $250B+ $3.5B

• Co-production agreements, routing Value of goods handled Capital investments

protocols, marketing alliances and

interline agreements providing

additional connections to consumers

across North America $41.2B 25,720

Assets Employees (end of period)

Note: As at or for the year ending December 31, 2018. 7

Financial highlights

Consistently delivering 15%+ ROIC since 2012

Change

Q1 Favorable

2012 2013 2014 2015 2016 2017 2018 CAGR 2019 (Unfavorable) (1)

Total revenues ($M) 9,920 10,575 12,134 12,611 12,037 13,041 14,321 6% 3,544 11%)

Operating income ($M) 3,552 3,819 4,498 5,155 5,032 5,243 5,493 8% 1,080 5%)

Diluted earnings per share ($) 3.06 3.09 3.85 4.39 4.67 7.24 5.87 11% 1.08 8%)

Adjusted diluted earnings per share ($) (2) 2.81 3.06 3.76 4.44 4.59 4.99 5.50 12% 1.17 17%)

Free cash flow ($M) (2) 1,661 1,623 2,220 2,373 2,520 2,778 2,514 7% 286 (11%)

Operating ratio (%) 64.2 63.9 62.9 59.1 58.2 59.8 61.6 69.5 (170 bps)

Adjusted operating ratio (2) 64.2 63.9 62.9 59.1 58.2 59.8 61.5 67.2 60 bps

Share repurchases ($M) 1,400 1,400 1,505 1,750 2,000 2,000 2,000 6% 432

Dividends per share ($) 0.75 0.86 1.00 1.25 1.50 1.65 1.82 16% 0.5375 18%

Adjusted debt-to-adjusted EBITDA multiple (times) (2) 1.71 1.74 1.63 1.77 1.85 1.75 1.94 2.01

Return on Invested Capital (ROIC) (%) (3) 17.3 15.4 16.6 16.8 16.0 22.4 16.7

Adjusted ROIC (%) (3) 16.0 15.2 16.2 17.0 15.8 15.9 15.7

(1) Q1 2019 vs Q1 2018.

(2) Please see website, Financial Results, www.cn.ca/financial-results, for an explanation of these non-GAAP measures.

(3) Please see the Appendix for an explanation of these non-GAAP measures.

8

Managing a balanced set of key metrics

to create shareholder value year after year

Return to

In 2018 Adjusted OR (1) Free Cash Flow (1)

Shareholders

61.5% $2.5B $3.3B

Amongst industry leaders Steady generation Solid distributions balanced

in efficiency ensuring financial between dividends and

flexibility share repurchases

From RTM CAGR Adjusted ROIC (2) Diluted EPS CAGR

2012 to

2018

3.5% 15-17% 11%

Outpacing peers Consistent track record Creating shareholder value

with faster RTM growth based on disciplined year after year

capital deployment

(1) Please see website, Financial Results, www.cn.ca/financial-results, for an explanation of these non-GAAP measures.

(2) Please see the Appendix for an explanation of this non-GAAP measure.

9

Driving long-term profitable growth

Scheduled Railroading was pioneered by CN more than 15 years ago and remains the

foundation of our operating model. Along with our established supply chain focus, we are now

advancing on our strategic agenda, leveraging our strong pool of talent and digitizing

operations to reduce cost, all while maintaining safety as our core value.

Scheduled Railroading Expanding rail business

The foundation Organic growth

Safety Inorganic growth

Technology deployment People talent

People talent

Supply chain service that wins

Disciplined capital allocation

Balancing OR and ROIC

10CN delivers strong profitable growth over the years

Amongst industry leaders in margins

Industry Operating Ratios (%)

(Expenses / Revenues)

90% RTM

CAGR (1)

85%

80% 3.5%

75%

70% 2.2%

65% 1.8%

60% 1.7%

55%

50%

-1.5%

45%

-1.6%

40%

2012 2013 2014 2015 2016 2017 2018

NSC KSU UP CP CSX CN

(1) RTM CAGR is calculated from 2012 to 2018.

11Content

Balancing

1 Company

Highlights 2 Our Key

Strengths 3 Operational

and Service

Experience

Innovating Creating

4 Markets 5 Everywhere

Every Day

6 Value for

Shareholders

12Our Key Strengths Summary • Highly experienced leadership team • Expansive network footprint with diversified product and customer base • Structural network advantage around Chicago • Exclusive access to Prince Rupert’s deep-sea port • Customer-centric structure • Deploying key technology projects

Highly experienced leadership team

JJ Ruest Mike Cory Ghislain Houle

President & Executive VP & Executive VP &

Chief Executive Chief Operating Chief Financial

Officer Officer Officer

• 22 years with CN • 37 years with CN • 21 years with CN

• Served as CMO for 8 years • Led all 3 operating regions • Qualified conductor and engineer

Sean Finn Keith Reardon James Cairns

Executive VP Senior VP Senior VP

Corporate Services & Consumer Product Rail Centric Supply

Chief Legal Officer Supply Chain Chain

• 25 years with CN • 19 years with CN • 31 years with CN

• 10 years in current role • 6 years leading Intermodal at CN • Over 20 years in carload markets

• Operational experience

Michael Foster Kim Madigan Paul Butcher

Senior VP & Senior VP Human VP Investor Relations

Chief Information Resources

and Technology

Officer

• 23 years of experience in IT & logistics • 19 years with CN • 25 years with CN

• Joined CN in 2018 from Fedex • 10 years in current role • 2.5 years in current role

For more information on CN’s company officers, please visit www.cn.ca/company-officers 14Promotion of internal seasoned Scheduled

Railroaders

Derek Taylor James Thompson Doug

VP Southern Region VP Western Region MacDonald

VP Eastern Region

• Deep operational capability • Deep operational capability • Bringing commercial depth to operations

• Quickly converts plans into actions • Focused driver of results • Focused on getting things done

Doug Janet Drysdale Michael

Ryhorchuk VP Financial Planning Farkouh

VP Network VP Railroad and

Operations Network Technology

Deployment

• Deep operational knowledge of network • Versatile and adaptable executive • Deep operational knowledge

• 36 years with CN • Experienced across multiple functions • Next generation of industry-leading

scheduled railroading technology

Buck Rogers Allen Foster Kelly Levis

VP Petroleum and VP Bulk VP Industrial

Chemicals

Products

• Solid operator • Solid operator • North American market experience

• Experience in petroleum and chemical • Solid commercial experience in grain, • Solid know-how in forest and industrial

markets coal and fertilizer markets markets

For more information on CN’s company officers, please visit www.cn.ca/company-officers 15Advancing our agenda with injection of external

talent with diversified expertise in the last 2 years

Raj Gupta Jim Sokol Paul Harridine

VP System VP Mechanical VP Procurement

Engineering & Supply

Management

• Trinity Rail Products • Southwest Airlines • DS Smith plc

• Rail, Automotive, Aerospace, Industrial • Analytics based reliability strategy • Supply management, procurement and

experience supply chain expert

Mitch Beekman Martin Guimond Mike Jones

VP Safety & VP Multimodal President (TransX)

Environment Operations

• British Petroleum • British American Tobacco • TransX

• Environment, health & safety expert • Strong multimodal know-how • Solid experience in intermodal

Mohit Bhat Nayan Bharadwa

Assistant VP Enterprise Assistant VP Operational

Architect Technology

• Mphasis • Wind River (Intel Sub)

• Digital expert • Proficiency with optimized, scalable

technology

For more information on CN’s company officers, please visit www.cn.ca/company-officers 16Expansive network footprint

enabling a well-diversified portfolio

Global West 25%

• Only Class I railroad

reaching 3 coasts

Domestic Canada 16%

with its network

• Originating carrier for

over 85% of traffic Global East 5%

Transborder 35%

moving on CN’s Southbound 24%

network Northbound 11%

• Over 65% of traffic Well-diversified portfolio

originating and

Domestic U.S. 16% Intermodal 24%

terminating on CN’s

Petroleum and Chemicals 21%

network

Grain and Fertilizers 16%

• Diversified product Forest Products 13%

and customer base Metals and Minerals 12%

limiting exposure to Automotive 6%

economic cycles Global South 3% Coal 4%

Other Revenues 4%

Based on Q1 2019 revenues

The map refers to traffic density based on annualized rates of Q1 2019 gross ton mile (GTM) production (million GTMs per route mile).

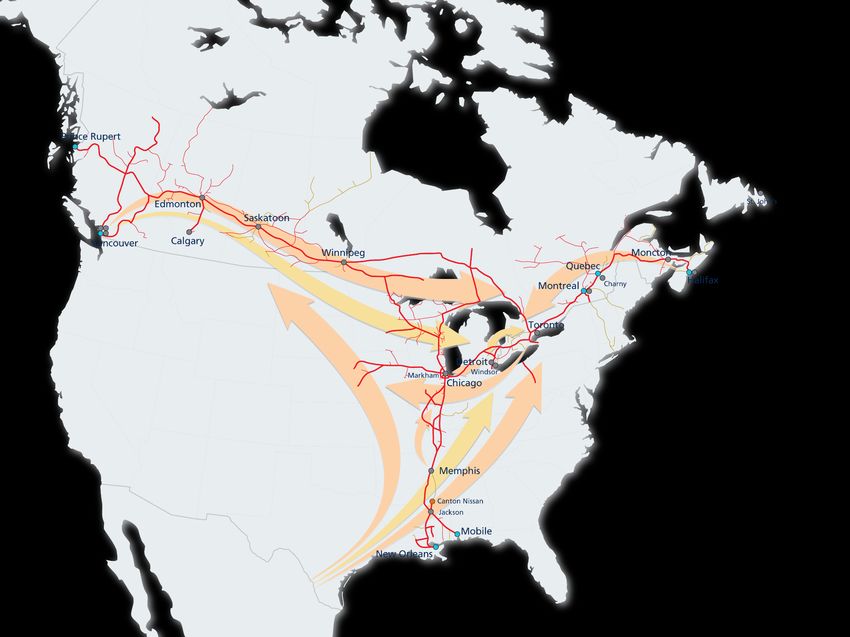

For more information on CN’s network, please visit www.cn.ca/en/our-services/maps-and-network 17Structural network advantage around Chicago

providing speed and service advantages

Chicago is one of North America’s largest To / From Vancouver

and Prince Rupert

freight hubs

• More than 25% of U.S. rail traffic touches

Chicago at some point on its route (1)

• 500 freight trains and 800 passenger trains

pass through Chicago on a daily basis (2)

• Freight volumes shipped from Illinois expected

to rise 30% and shipments passing through

Illinois expected to grow 25% over the next 30

years (3)

CN acquired the EJ&E in 2009 to secure an

exclusive outerbelt around Chicago’s highly

congested downtown area

• 2x speed advantage through Chicago

vs other Class I railroads To / From Montreal

and Halifax

• More efficient interchange points

with other carriers

• More reliable service To / From New Orleans

and Mobile

(1) Kristine Owram, November 18, 2015, http://business.financialpost.com/welcome-to-chokepoint-usa

(2) Chicago Region Environmental And Transportation Efficiency (CREATE) Program, www.createprogram.org

(3) Illinois Section American Society of Civil Engineers, Rail – 2018 Report Card for Illinois’ Infrastructure,

https://www.infrastructurereportcard.org/wp-content/uploads/2016/10/FINAL-REPORT-CARD-FOR-2018-IL-Infrastucture.pdf

18Exclusive access to Prince Rupert, North America’s

fastest growing deep-sea port

• Closest North American deep-sea port to Asia

• Deepest natural harbour in North America

(35 meters channel depth)

• Lowest rail grades of all West Coast railroads across the

Rockies, giving CN a natural cost advantage to and from the

center of the continent

Opportunities to increase natural resources exports from Prince Rupert

19Customer-centric structure providing focus and

accountability to SERVE and GROW different segments

Rail-Centric Consumer Product

Activities + Activities

Segments served Bulk and Merchandise Intermodal and

Automotive

Organizational scope Sales, marketing and Sales, marketing and

non-rail operations terminal first / last mile

operations

Dedicated facilities • 31 transload facilities • 23 container terminals

• 4 Great Lakes • 19 Autoport locations

bulk docks • More than 1,100 CNTL

local delivery truck fleet

Growth levers Organic growth + Relevant bolt-on acquisitions

20Leveraging advanced technology to improve safety,

efficiency and productivity

Smart Network

Mobile device

for conductors

Mobile device for carmen

Robotic Process

Air repeater car Automation

Automation of track

Automation of train inspection inspection

21Content

Balancing

1 Company

Highlights 2 Our Key

Strengths 3 Operational

and Service

Experience

Innovating Creating

4 Markets 5 Everywhere

Every Day

6 Value for

Shareholders

22Balancing Operational and Service Experience Summary • Commitment to operational and service excellence • History of long siding investments to maximize train length • Priority on re-investing in the business to accommodate solid pipeline of growth opportunities • Long-term commitment to running a sustainable railroad

Improving operating and service metrics

Port Dwell Grain Spotting Order Fulfillment

Days Cars per week % of orders receiving cars

Prince Rupert Delta Port 2017/18 2018/19 2018 2019

8.0 120%

6,000

6.0 100%

5,000 ~5,160 95%

4.0 80%

4,000

2.0 3,000 60%

~2 days

0.0 2,000 40% Week Week Week Week Week Week Week Week Week Week Week Week Week Week Week Week Week Week Week Week Week Week Week Week Week Week

01 03 05 07 09 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47 49 51

11

13

17

21

25

27

29

31

33

35

37

39

May

43

47

51

3

5

7

9

Nov

Jan

Aug

Dec

Jun

Jul

Apr 18 Jun 18 Aug 18 Oct 18 Dec 18 Feb 19 Apr 19 Aug Oct Dec Feb Apr Jun Jan Mar May Jul Sep Nov

Car Velocity Through Network Train Speed Through Dwell

Car miles per day mph hours

2018 2019 2018 2019 2018 2019

250 13.0

225 225 21.0

11.0

200 19.7

19.0

175 9.0

150

17.0 7.0 7.0

125

100 15.0 5.0

Jan Mar May Jul Sep Nov Jan Mar May Jul Sep Nov Jan Mar May Jul Sep Nov

24Investing in long sidings to enable longer trains

and capacity

~200 long siding and double track

investments since 2000

New long siding, long siding extension

or double track investment since 2000

Pre-2000 long siding, long siding

extension or double track investment

miles of track

~ 600 installed in each

of last few years

ties

~ 2M installed in each

of last few years

252019 network infrastructure and high horsepower

locomotive additions

Legend New long siding / track Double track

Taverna – Prince Rupert

Prince Rupert 3 miles double track

1 new siding

New locomotive delivery:

Winnipeg – Edmonton

Edmonton

Q1 063 (delivered) Taverna 49 miles double track

Q2 052

Vancouver Winnipeg

Regina

Q3 020 Edmonton – Vancouver

18 miles double track

Q4 005 Chicago – Winnipeg

8 miles double track

1 new siding

Total 140 (~$500M) Detroit

Chicago

Capacity Equipment Deploying key technology projects Meeting PTC milestones

Supporting our solid pipeline of growth opportunities in diverse markets

26CN Railroaders: Strong pool of human assets

to leverage

Talent to win • Put best 2% talent into most critical value roles

• Invest into those critical roles of the future

• Recruit and acquire missing value roles – to attain strategic agenda

• De-layer, reduce management structure – reduce bureaucracy / labour cost, be more agile

Position Number of employees (1) Expiration

Labour stability Conductors and yard coordinators 3,630 July 22, 2019

Canadian Track forces 2,772 December 31, 2023

Shopcraft 2,043 December 31, 2022

unionized

Locomotive engineers 2,094 December 31, 2022

workforce Clerical and Intermodal 1,789 March 31, 2019 (pending ratification)

Signals and communications 733 December 31, 2021

(1) As at December 31, 2018. Excludes rail traffic controllers, special agents and other.

27Delivering safely and responsibly

Building safety into all we do Reducing carbon emissions

FRA Train Accident Ratio (1) Fuel Efficiency

(accidents per million train miles) (GTMs per US gallon )

2.73 1,061 1,063

1,060

2.06 2.02

1.83 1,040

1.42

1,019

2014 2015 2016 2017 2018 2014 2015 2016 2017 2018

Moving freight by rail instead of heavy truck

CN continues to invest in our infrastructure, reduces greenhouse gas emissions by 75% (2)

technology, processes and people to improve

safety and enhance our safety culture CN is ~15% more fuel efficient than the rail

industry average (3)

(2) Association of American Railroads

(1) U.S. Federal Railroad Administration

(3) Based on 2017 data.

28Leading in Sustainability

CN’s commitment to sustainability

Environment People

is a long-term strategic priority,

Conduct our operations with Provide a safe, supportive and

extending to all aspects of the minimal environmental impact, diverse work environment

business, from the field to the while providing cleaner, more where our employees can

sustainable transportation grow to their full potential and

boardroom, to customer services to our customers. be recognized for their

interactions. contribution to our success.

Our vision guides how we conduct Safety Community

our business every day and Be the safest railroad in North Build safer, stronger

defines our contribution to building America by establishing an communities by investing in

uncompromising safety community development,

a more sustainable future. Five key culture and implementing a creating positive socio-

areas of focus anchor our management system designed economic benefits and

to minimize risk and drive ensuring open lines of

sustainability commitment: continuous improvement. communication.

Governance

Continuously improve our

culture of integrity and ethical

business, building trust and

confidence with all our

stakeholders.

For more information on CN’s sustainability strategy, please visit www.cn.ca/delivering-responsibly

29Content

Balancing

1 Company

Highlights 2 Our Key

Strengths 3 Operational

and Service

Experience

Innovating Creating

4 Markets 5 Everywhere

Every Day

6 Value for

Shareholders

30Markets Summary • Growth opportunities remain solid across our diverse book of business • Intermodal remains a key growth driver • Coal business has potential to reach record levels • Canadian grain is a positive story for CN • Short-term crude by rail opportunities remain strong

Market outlook remains solid

Rail Centric • Short-term softness in crude by rail related to mandated production curtailment and

crude spread below US$15

Supply Chain • Mid-term outlook remains positive as new pipeline capacity continues to be pushed back

Growth • New resource export business starting in May

• Vista coal mine in Alberta shipping thermal coal to Asia

• New Alberta propane export via Prince Rupert to Asia

• U.S. thermal coal exports neutral on high stockpiles in Europe

• Securing frac sand volumes (Northeast U.S. and Western Canada) through strong

partnerships

• Lumber orders remain solid

• Continue to move record amounts of Canadian grain

Consumer • International intermodal traffic remains steady

• Zim Integrated Shipping Services now calling Port of Prince Rupert

Product Supply • Strong international reefer volumes

• New auto parts import business into North America starting mid-Q2

Chain Growth

• Strengthening our position in the domestic consumer economy

• Cross-pollination has begun between CN and TransX

• 500 new interline Equipment Management Pool (EMP) containers expected to be fully in service mid-Q2

• Growth in CargoCool® ̶ working closely with wholesale partners

• North American motor vehicle sales remain soft

• Original Equipment Manufacturer (OEM) production backlog expected to support solid Q2

• Renewed contract with Ford on vehicles and parts

Continue to expect high single-digit RTM growth in 2019, with pricing above rail

inflation

Rail Centric Supply Chain Growth is comprised of the following: Petroleum and Chemicals, Metals and Minerals, Forest Products, Coal, and Grain and Fertilizers.

Consumer Product Supply Chain Growth is comprised of the following: Intermodal and Automotive.

Please see Forward-Looking Statements at the beginning of this presentation.

For more information on the different markets CN serves, please visit www.cn.ca/en/your-industry 32International intermodal: Volumes driven by unrivaled

access to the 3 coasts through 14 different port terminals

PORT OF HALIFAX

(2 terminals)

• CN-exclusive

PORT OF PRINCE RUPERT • Capacity: 1,400k TEUs

(1 terminal) • Closest port to Europe

• CN-exclusive • Volume growth of 16% in 2017

• Closest port to Asia TOTAL ADDRESSABLE PORT OF MONTREAL

• Capacity: 1,350k TEUs MARKET (TAM) (4 terminals)

• 1,600k TEUs by 2021 10-12 M TEUs* • Capacity: 1,850k TEUs (+250k TEUs to come)

• 1,800k TEUs by 2022 • New terminal in Contrecœur adding 1,150k

TEUs by 2023

PORT OF VANCOUVER

(4 terminals)

• Capacity: 3,600k TEUs

• DeltaPort expanded by 600k TEUs in late 2018

• Centerm expansion of 600K by 2022

• Vanterm expansion of 250K by 2022

PORT OF QUEBEC (Beauport)

• Potential capacity of 500K TEUs

by 2020

CN Network

23 intermodal terminals across N.A. advantage

in Chicago PORT OF MOBILE

(1 terminal)

• 11 in Canada, serving all major cities • Near-dock rail service and

• New Regina terminal opening in 2019 vessel calls from Asia

• Capacity: 475k TEUs

• 12 U.S. terminals covering key markets • Expansion of 175k TEUs to be

completed by end of 2019

PORT OF NEW ORLEANS

(2 terminals)

* TEU: Twenty-foot equivalent unit (intermodal shipping container) • On-dock rail service

• Capacity: 900k TEUs

Please see Forward-Looking Statements at the beginning of the presentation. 33International Intermodal: Prince Rupert continues to add

capacity

2019-2021 Looking ahead to 2020-2022

Prince Rupert • June 2018 announcement of next expansion

at Prince Rupert

1,350k TEUs of rail capacity in place • + 250,000 TEUs by 2021

• 100% CN share

• + 200,000 TEUs by 2022

• Logistics park in Prince Rupert (dry & cold

supply chain, free trade zone logistics)

$300–325M • New inland destination terminals

Est. incremental revenues over 2019-2021

Please see Forward-Looking Statements at the beginning of the presentation. 34International Intermodal: CN investing in rail capacity in

the Vancouver area to support growth

2019-2021

North

Vancouver

Deltaport

Lynn Creek Yard 600,000 TEUs of new rail capacity in

Centerm Vanterm

late 2018

• At 70% CN share, the CN historical rail

capacity

Vancouver Yard • Aiming to be near 80% capacity 3 years

from start-up

$250–275M

Est. incremental revenues over

2019-2021

Lulu Island Yard

South Shore Capacity Projects:

Vancouver

Double track to the expanding

South Shore Centerm & Thornton Yard

Vanterm terminals Vancouver

• $85M jointly funded by CN, Fraser Surrey Intermodal

PMV, Federal Docks Terminal

• Q3 2017 – expression of

interest filed with

Government of Canada

• February 2019 – agreement

signed

• Q3 2021 – expected North Shore Capacity Projects:

completion of project Staging track and tunnel

improvements to increase capacity

for expanding North Shore terminals

• $214M jointly funded by CN, PMV, CN

Federal

• Q3 2017 – expression of interest CN Trackage Rights

filed with Government of Canada

• April 2019 – agreement signed Container terminals

• End of 2020 – expected CN Yard

completion of project

Deltaport

Please see Forward-Looking Statements at the beginning of the presentation. 35Domestic Intermodal: $250-375M opportunity

of potential incremental revenues over 2019-2021

Gaining market share through strong

Expect 4-6% Wholesale partnerships with the industry’s best

CAGR Full membership in EMP program

Acquisition of TransX

Retail Gaining market share through

door-to-door

Strong growth

with Cargo Cool

Significant investments in intermodal terminals and equipment

Please see Forward-Looking Statements at the beginning of the presentation. 36Coal: CN’s franchise is well-positioned to take

advantage of coal export opportunities

Q1 2019 CN Coal Revenue Breakdown

Thermal Metallurgical Total

Canadian coal

Export 41%

U.S. coal

Export 33% - 33% 59% U.S.

Domestic 26% - 26%

41% Canada

Coal 80%

Pet coke 20%

37Coal: Up to $350M of potential incremental revenues

over 2019-2021

Canadian Export Coal U.S. Export Coal

Metallurgical coal Thermal coal

• Brule mine opened in Q4 2016 • Export market from Illinois Coal Basin

• 3M tons annual capacity

• Wolverine mine opened in Q1 continues to expand to feed emerging

2017 markets such as India, North Africa, Turkey,

• 1.7M tons annual capacity in addition to Western Europe

• Willow Creek mine opened

• Sugar Camp mine: 13.5M tons capacity

in Q3 2018

• 1.7M tons annual capacity • Williamson mine: 7.5M tons capacity

• CN provides the only direct access unit train

• Opened in Q3 2018 from the Illinois Basin to major export

• 2M tons annual capacity with the

potential to go up to 4M tons

terminals on the Gulf Coast

• Convent Marine Terminal (LA)

• Mobile Port (AL)

Thermal coal

• These modern terminals are equipped with

• Vista mine opening in May 2019

• 6M tons annual capacity, with the loop tracks to unload coal for stock pile or

potential to go up to 12M tons directly into vessels

Please see Forward-Looking Statements at the beginning of the presentation.

38Grain: CN investing in its network and equipment

to better serve its customers

Canada United States

Canadian Grain Production (1)

(millions of metric tonnes) 68% U.S. Corn and Soybean Production

CN Draw Territory (IL, IA, MI, WI) 32%

(billions of bushels)

of CN grain 7.3 of CN grain

73.0

70.5 70.3

(2)

revenues 7.1

(3) revenues

originate from 7.0 originate from

65.0 6.8

63.0 Canada (4) the U.S. (4)

6.6

Regulated grain: Domestic U.S.

78% of Canadian grain: 54% of U.S.

grain revenues (4) grain revenues (4)

14/15 15/16 16/17 17/18 18/19 E 14/15 15/16 16/17 17/18 18/19 E

• Leveraging our investments in longer sidings and new high-horsepower locomotives

to accommodate longer trains

• Working closely with grain customers

• 1,000 new generation hopper cars (up to 10% more capacity per car)

• Close to 400 delivered in Q1 2019

• Increased customer participation in CN’s Western Canada fleet integration program

• Increased number of private unit trains in CN’s Western Canadian grain service

(1) Six major grains (wheat, barley, canola, oats, flax, rye) + lentils and peas.

(2) Statistics Canada, September 2018.

(3) USDA WASDE Estimates, September 2018.

(4) Based on Q1 2019 revenues.

Please see Forward-Looking Statements at the beginning of the presentation.

39Grain: CN operating the majority of new grain

elevators built in Canada since 2015

Est. incremental revenue range Annual crop tonnage CN export grain share

2019-2021 growth est. growth

$100 – 150M 2 – 2.5% CAGR 50% (2018) / 55%+ (by 2022)

21 new grain elevators built on CN lines:

Waterfront export facilities

Ray-Mont Logistics Announced

In operation 14

20 CN Viterra

Completed

exclusive

Announced 6

G3

GrainsConnect, Viterra

P&H G3

Shared 1 Grains Grains

GrainsConnect

Connect Connect ILTA

G3 P&H Viterra

G3

Viterra P&H

Other 4 Fraser Grain Terminal, G3

G3, Fibreco P&H

G3

G3

Viterra

Please see Forward-Looking Statements at the beginning of the presentation.

40Lumber and Panels: Steady

growth in U.S. housing market

CN Lumber / Panel Volumes to the U.S.

(thousands of carloads)

Panels Lumber U.S Housing Starts (000s)

200,000

187 2,000

1,801 170 168 164

160

180,000 1,800

150 149

141

160,000 1,600

140,000 1,400

1,327

1,211 1,262 1,250

1,174 *

1,200

1,139

120,000

1,112

100,000

1,003 1,000

925

80,000

781 800

60,000 600

40,000

38 37 400

20,000

CAGR 3% 200

- -

2006 2012 2013 2014 2015 2016 2017 2018 2019* Q1 18 Q1 19

• Largest carrier of forest products among

Class I railroads

• Opportunities available in our Western Canadian lumber

and panel franchise

• Over 10% of CN revenues tied to housing

• U.S. remains an important market for Canadian

lumber producers

• Acquiring 850 new centerbeam cars in 2018-2019

CN volumes include Canadian and U.S. origins.

*Please see Forward-Looking Statements at the beginning of this presentation.

41Wood Pellets: Growth driven by Asian market

Total Short Tons Shipped Pinnacle Renewable Energy Pacific Bioenergy

(millions) Legend

2.2 Canfor Energy North Premium Pellet

2.1 2.1

1.7 1.7 1.7

1.6

Fort St. John

Chetwynd

2012 2013 2014 2015 2016 2017 2018

Prince Rupert

• Exports to Asia represent ~20% of CN Houston

shipments (Japan, South Korea) Burns Lake

Prince George

• Further upside from new renewable energy Vanderhoof

targets in Japan, requiring a shift away from

coal Colebank Entwistle, AB

• Expansion projects at Smithers, BC Williams Lake

and Entwistle, AB

• Production efficiency project at

Watson, BC

2019-

2020 • Agreement to purchase all wood

Outlook pellets produced at Skeena’s new

state-of-the-art pellet plant at Terrace, Armstrong

BC

Vancouver

• Long term supply agreement with Japanese Lavington

power producers

42Automotive: CN network providing direct access to 15

major metropolitan dealer markets across North America

Access to 13 assembly plants in Ontario,

Michigan and Mississippi

• CN has a 70% rail share of

motor vehicles sold in Canada

• Rail-direct service from West

Coast to Detroit to handle

imported vehicle parts in

containers

43Automotive: Higher demand for SUVs and light trucks

SUVs and light trucks still gaining SUVs produce 50% more carloads

share in North America than sedans

North American SUV and light truck sales • 10 SUVs in a 2-level carload

(M units)

25 70%

20 60%

50%

15

40%

10 30%

5

20%

• 15 sedans in a 3-level carload

10%

0 0%

2012 2013 2014 2015 2016 2017 2018

Car Truck % Truck

Source IHS: January 2019

44Crude oil: Growth expected when Western Canada

Select spread widens to US$15

Crude oil shipments: carloads

Significant ramp-up in

crude volumes in H2 2018, Volumes in Q1 2019

with December as peak declined from

mandated production

curtailments

~127,000

~98,000 ~36,000 ~13,000

~82,000 ~10,000

~52,000 ~61,000 ~20,000 ~20,000 ~6,000 ~7,600

~4,000

~11,000 ~15,000

2014 2015 2016 2017 2018 Q1-18 Q2-18 Q3-18 Q4-18 Q1-19 Dec-18 Jan-19 Feb-19 Mar-19 Apr-19

Annual carloads Quarterly carloads Monthly carloads

Crude oil shipments: barrels per day (bpd)

~251,000

~232,000

~209,000 ~187,000

~162,000 ~129,000 ~131,000 ~145,000

~133,000 ~101,000 ~116,000

~85,000 ~99,000 ~69,000 ~86,000

2014 2015 2016 2017 2018 Q1-18 Q2-18 Q3-18 Q4-18 Q1-19 Dec-18 Jan-19 Feb-19 Mar-19 Apr-19

Annual bpd Quarterly bpd Monthly bpd

Please see Forward-Looking Statements at the beginning of the presentation.

45Petrochemical: $200-250M opportunity

of potential incremental revenues over 2019-2021

Alberta Industrial Heartland

Prince Rupert

• Nauticol

• Inter pipeline Ontario

Unit trains will feed Prince

Rupert’s propane export • Pembina

terminals by 2019-2020 • NOVA (Sarnia, ON)

• Greenergy terminal

• Altagas/Vopak RIPET (Johnstown, ON) (2020)

terminal

• Pembina (Watson Island)

U.S. Gulf

• Westlake (Geismar, LA)

• Exxon (Baton Rouge, LA)

• Wanhua (Convent, LA)

2019-2023 4 new petrochemical plants announced 3 new petrochemical major

expansions announced

outlook Inter pipeline (2021)

Westlake Chemical

(2019)

Wanhua (2021)

NOVA Chemicals

Nauticol (2021) (2022)

Pembina/PIC ExxonMobil (2021)

Heartland (2023)

46Content

Balancing

1 Company

Highlights 2 Our Key

Strengths 3 Operational

and Service

Experience

Innovating Creating

4 Markets 5 Everywhere

Every Day

6 Value for

Shareholders

47Innovating Everywhere Every Day Summary • Focus on select number of technology projects that can be implemented and drive value in the short-term • Digitizing rail operations improves costs • Rolling out pilot projects in 2019 • Leveraging technology for a safer and more efficient network

Track Evaluation System (TEST) cars

Leveraging technology to improve inspection productivity

• Utilize multiple technologies to automate

Engineering track inspections

• Improve quality and reliability by

providing consistent, reliable and

objective inspection results

• Reduce track inspection labour costs

while maintaining and improving network

integrity and safety

• Decrease track time requirements and

reduce safety risks associated with

performing visual inspections

• Provide richer and more frequent data

sets to generate stronger predictive

analytical models

Plan to add 5 TEST cars in 2019

49Automated Inspection Portals (AIP)

Deploying the next generation of inspection technologies

First AIP installed in Winnipeg Next Steps

• Improve asset reliability and availability • Network-scale rollout (Toronto, Memphis

• Shift toward predictive maintenance (versus and Fulton)

reactive) • Assessing broad spectrum of relevant use

• Better workforce utilization cases for visual recognition across CN’s

• Reduce disruptions operations

• Enhance network safety and security • Prioritizing applications that improve safety,

effective capacity, and operational

• Create effective capacity

efficiency

• Improve overall customer experience

In 2019, 7 portals expected to be operational in Winnipeg (4), Toronto (1),

Memphis (1) and Fulton (1)

50Mobile applications

A new breed of connectivity targeting Operations productivity

Mobile device for carmen

• Streamline the process for Car Mechanics to report their work directly on

device

• Improve supervisors’ visibility of work progression and efficiency with

remote communication of instructions

• Increase data accuracy and scope of work billed

• Serve as a platform for future mobile mechanical information exchange

• Rollout started in Q1 2018 (500 devices)

Mobile device for conductors

• Increase operational visibility, productivity and fluidity as conductors receive

their work instructions directly on a mobile device

• Speed up information flow to customers and increase accuracy in reporting

• Enable dynamic planning and work assignment, staying current on progress

• Pilot rollout scheduled for Q3 2019 (9,500 devices)

Documentation on mobile device

• Improve safety and productivity with easier navigation and access to rules,

customization of content and more robust update process

• Improve ergonomic experience for crews and reduce environmental footprint

• Rollout scheduled for Q3 2019

51Seamless border crossing

Live-Lift at Ranier and Port Huron

Robotic Process Automation

Border Crossings

Live-Lift for single container inspection minimizes train Robotic Process Automation (RPA) is used to automatically

delays - speeding up border crossings for our customers and proactively monitor shipments crossing the border for

completeness of customs information, in an effort to speed

CN efficiently facilitates the handling of containers and train

up the traffic through the border, minimize stops and

loading plans for inspection releases. Live-Lift has

reduce overall clerical effort

eliminated the majority of U.S.-rejected containers -

reducing transit times and delays Designed to automate low value, high volume manual

clerical activities, allowing greater focus of human capital

In March 2018, CN completed a major expansion project

on more value-added tasks

and nearly doubled our Ranier border crossing facility.

Implemented Live-Lift at Port Huron, MI border crossing in Since spring 2018, a total of 12 out of 13 borders are now

Q4 2018 monitored via RPA, resulting in a 70% reduction of related

border stops. Expect to implement RPA at Rainer border

CN’s Ranier facility now provides a full range of inspection

crossing in Q4 2018

services similar to those found at U.S. major ports of entry

52Procurement & Supply Management transformation $70M

savings achieved after one year with potential $130M

cumulative savings upon completion

People Process Technology

• Strengthening the team and • Implementing category • Moving spend through

upgrading skills through management, structuring preferred channels to

training, development and portfolios of spend that increase spend visibility,

external recruitment

mirror the supply market strengthen compliance

• Leveraging cross-functional to ensure CN leverages its and help identify

category teams to identify total spend opportunities through

and deliver on performance data analytics

improvements across quality, • Procurement strategy

cost, reliability and innovation driven by a total cost of • Implementing leading

KPIs ownership approach contract management and

eProcurement systems

• Driving a continuous

improvement culture focused

on value creation, teamwork

and problem-solving

Currently ahead of target on expected cost savings from investment of $25M to

transform our Procurement & Supply Management function over 3 years

53Content

Balancing

1 Company

Highlights 2 Our Key

Strengths 3 Operational

and Service

Experience

Innovating Creating

4 Markets 5 Everywhere

Every Day

6 Value for

Shareholders

54Creating Value

for Shareholders

Summary

• Delivering solid results over the years

• Solid free cash flow generation

• Strong focus on re-investing in the

business while generating 15%+

adjusted ROIC (1)

• Rewarding shareholders through

dividends and share buybacks

• Consistently increasing dividends per

share every year since IPO in 1995

(16% CAGR)

(1) Please see the Appendix for an explanation of this non-GAAP measure.Delivering solid results over the years

Revenues ▲11% Net Income ▲6%

Q1 19 vs Q1 18 Q1 19 vs Q1 18

$M $M

14,321 5,484

13,041

12,134 12,611 12,037

9,920 10,575

4,328

3,538 3,640

3,167

2,680 2,612

3,194 3,544

CAGR 6% CAGR 8% 741 786

2012 2013 2014 2015 2016 2017 2018 Q1 18 Q1 19 2012 2013 2014 2015 2016 2017 2018 Q1 18 Q1 19

Diluted EPS ▲8% Adjusted Diluted EPS (1) ▲17%

Q1 19 vs Q1 18 Q1 19 vs Q1 18

$ per share $ per share

7.24

5.87 5.50

4.67 4.59 4.99

4.39 4.44

3.85 3.76

3.06 3.09 2.81 3.06

CAGR 11% 1.00 1.08 CAGR 12% 1.00 1.17

2012 2013 2014 2015 2016 2017 2018 Q1 18 Q1 19 2012 2013 2014 2015 2016 2017 2018 Q1 18 Q1 19

(1) Please see website, Financial Results, www.cn.ca/financial-results, for an explanation of this non-GAAP measure.

For more financial information, please visit www.cn.ca/en/investors

56Free Cash Flow

Steady cash flow generation

Free Cash Flow (1)

$M

2,778

2,520 2,514

2,373

2,220

1,661 1,623

322 286

2012 2013 2014 2015 2016 2017 2018 Q1 18 Q1 19

(1) Please see website, Financial Results, www.cn.ca/financial-results, for an explanation

of this non-GAAP measure.

57Disciplined capital investments

Investing to support our business and committed to investing

for the long-term

Capital Investments and Adjusted ROIC (1)

in $M & % respectively

4,500 30.0%

4,000

3,900 28.0%

3,500

3,531 PTC (2)

26.0%

• Strong capital

Equipment program driving

2,752

safety, fluidity and

3,000 24.0%

2,706 2,703

2,297

productivity

2,500 22.0%

2,017

2,000

1,825 20.0%

17.0% Infrastructure • Adjusted ROIC (1)

maintenance

1,500 18.0%

16.2%

1,000

16.0%

15.2%

15.8% 15.9% 15.7%

16.0%

used to measure

efficiency of CN’s

long-term capital

500 14.0%

Capacity /

Growth

investments

- 12.0%

2012 2013 2014 2015 2016 2017 2018 2019F

Capital Investment Ratio (3)

18% 19% 19% 21% 23% 21% 25%

Over $22B capital investments over the last 10 years

(1) Please see the Appendix for an explanation of this non-GAAP measure.

(2) Positive Train Control.

(3) Capital investments as a percentage of revenues.

58Maintaining a strong balance sheet

Prudent financial management Investment Grade Credit Ratings

Moody’s Investors

Adjusted debt-to-adjusted EBITDA multiple (1)

Service A2

times

Dominion Bond Rating

Service A

1.97 2.01

1.94

1.85

1.71 1.74

1.63

1.77 1.75 Standard & Poor’s A

2012 2013 2014 2015 2016 2017 2018 LTM LTM Je pourrais metre une

ended ended

Mar 18 Mar 19

photo en backgroud

(1) Please see website, Financial Results, www.cn.ca/financial-results, for an explanation

of this non-GAAP measure

59Rewarding shareholders

~82% of adjusted net income (1) returned to shareholders in 2018

Total shareholder distribution Dividends

$M

• Dividends increased every year

Share repurchases since 1995 IPO

Dividends 3,333

3,159 3,239

Total • CAGR of 16% over 23 years

2,746

• Targeting a 35% adjusted dividend

2,323 1,159 1,239 1,333

2,052 2,124 payout ratio (2) (3)

996

818

652 724

967

2,000 2,000 2,000 821

1,400 1,400 1,505

1,750 336

389

Share repurchases

631 432

• Normal course issuer bid (NCIB) of

2012 2013 2014 2015 2016 2017 2018 Q1 18 Q1 19

up to 22 million common shares

Dividend Payout Ratio (2) from February 1, 2019 to January

24% 28% 26% 28% 32% 23% 31%

31, 2020

• Over $21B of share repurchases

Adjusted Dividend Payout Ratio (2)

since 2000

27% 28% 26% 28% 32% 33% 33%

(1) Please see website, Financial Results, www.cn.ca/financial-results, for an explanation of this non-GAAP measure.

(2) Please see the Appendix for an explanation of these measures.

(3) Please see Forward-Looking Statements at the beginning of the presentation.

60Solid Track Record

Market cap ~$90B

CNR, CNI vs TSX, S&P 500

350

CNR

300

250 CNI

200 S&P 500

150

TSX

100

CAD/US $

50

0

2012 2013 2014 2015 2016 2017 2018 2019

Jan 2012 = 100

Up to April 30, 2019

For more stock information, please visit www.cn.ca/en/investors/stock-information 61Reaffirming 2019 financial

outlook

• Expect to deliver adjusted diluted EPS growth

in the low double-digits range versus 2018

adjusted diluted EPS of $5.50 based on (1) (2):

• Volume growth expected to be in the high

single-digit range in terms of RTMs

• Overall pricing above rail inflation

• Canadian to U.S. dollar exchange rate of

approximately 75 cents

• Capital envelope at approximately $3.9B

for 2019 to support a solid pipeline of growth

opportunities (2)

• Balanced shareholder distribution

• Dividend increase of 18% ̶ Targeting an adjusted

dividend payout ratio of 35% (3)

• 12-month NCIB from February 1, 2019 to January

31, 2020 to repurchase up to 22 million common

shares

(1) Please see website, First Quarter Results, www.cn.ca/financial-results, for an explanation of this

non-GAAP measure.

(2) Please see Forward-Looking Statements at the beginning of the presentation for a summary of

key assumptions and important risk factors and underlying CN’s 2019 financial outlook.

(1)

(3) Adjusted dividend payout ratio is defined as dividends as a percentage of adjusted net income .

Please see Forward-Looking Statements at the beginning of the presentation. 62Appendix: Non-GAAP measures

This presentation makes reference to non-GAAP measures that do not have any standardized meaning prescribed by GAAP,

including adjusted dividend payout ratio, ROIC and adjusted ROIC. These non-GAAP measures may not be comparable to

similar measures presented by other companies. These non-GAAP measures should not be considered in isolation or as a

substitute for financial measures prepared in accordance with GAAP.

Adjusted Dividend Payout Ratio

Management believes that the adjusted dividend payout ratio is a useful measure of the Company’s financial strength as it

demonstrates the sustainability of the Company’s dividend payments. The Company calculates the dividend payout ratio as

dividends divided by net income. The Company calculates the adjusted dividend payout ratio as dividends divided by adjusted

net income.

In $M, unless otherwise indicated 2012 2013 2014 2015 2016 2017 2018

Dividends 652 724 818 996 1,159 1,239 1,333

Net income 2,680 2,612 3,167 3,538 3,640 5,484 4,328

Dividend payout ratio (%) 24.3 27.7 25.8 28.2 31.8 22.6 30.8

Dividends 652 724 818 996 1,159 1,239 1,333

Adjusted net income (1) 2,456 2,582 3,095 3,580 3,581 3,778 4,056

Adjusted dividend payout ratio (%) 26.5 28.0 26.4 27.8 32.4 32.8 32.9

(1) Please see website, Financial Results, www.cn.ca/financial-results, for an explanation of this non-GAAP measure

63Appendix: Non-GAAP measures (continued)

ROIC and Adjusted ROIC

Management believes that ROIC and adjusted ROIC are useful measures of the efficiency in the use of capital funds. The

Company calculates ROIC as return divided by average invested capital. Return is defined as net income plus interest expense

after tax, calculated using the Company’s effective tax rate. Average invested capital is defined as the sum of total

shareholders’ equity, long-term debt and current portion of long-term debt less cash and cash equivalents, and restricted cash

and cash equivalents, averaged between the beginning and ending balance over a twelve-month period. The Company

calculates adjusted ROIC as adjusted return divided by average invested capital. Adjusted return is defined as adjusted net

income plus interest expense after tax, calculated using the Company’s effective tax rate, excluding the tax effect of

adjustments used to determine adjusted net income.

In $M, unless otherwise indicated 2012 2013 2014 2015 2016 2017 2018

Net income 2,680 2,612 3,167 3,538 3,640 5,484 4,328

Interest expense 342 357 371 439 480 481 489

(1)

Tax on interest expense (91) (97) (102) (120) (125) (124) (116)

Return 2,931 2,872 3,436 3,857 3,995 5,841 4,701

Average invested capital 16,913 18,650 20,711 23,014 24,905 26,019 28,192

ROIC (%) 17.3 15.4 16.6 16.8 16.0 22.4 16.7

Adjusted net income (2) 2,456 2,582 3,095 3,580 3,581 3,778 4,056

Interest expense 342 357 371 439 480 481 489

(3)

Adjusted tax on interest expense (93) (95) (103) (116) (126) (124) (120)

Adjusted return 2,705 2,844 3,363 3,903 3,935 4,135 4,425

Average invested capital 16,913 18,650 20,711 23,014 24,905 26,019 28,192

Adjusted ROIC (%) 16.0 15.2 16.2 17.0 15.8 15.9 15.7

(1) The effective tax rates from 2012 to 2018 used to calculate the tax on interest expense are 26.7%, 27.2%, 27.4%, 27.4%, 26.1%, 25.8% and 23.8%, respectively. Due

to the negative effective tax rate reported by the Company in 2017, tax on interest expense for 2017 periods was calculated using an adjusted effective tax rate.

(2) Please see website, Financial Results, www.cn.ca/financial-results, for an explanation of this non-GAAP measure.

(3) The adjusted effective tax rates from 2012 to 2018 used to calculate the adjusted tax on interest expense are 27.3%, 26.6%, 27.7%, 26.5%, 26.2%, 25.8% and

24.5%, respectively. 64Investor Relations Contacts

Paul Butcher

Vice President, Investor Relations

Paul.Butcher@cn.ca

514-399-0052

Michaël Archambault

Senior Manager, Investor Relations

Michael.Archambault@cn.ca

514-399-4654

For more information, please visit www.cn.ca/en/investors/investor-contacts

TSX: CNR NYSE: CNI 65You can also read