Acquisition of Coates Hire - 20 September 2017

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Acquisition of Coates Hire

20 September 2017

SGH Presentation | 20 September 2017

Important notice & disclaimers

Basis of preparation of slides

Included in this presentation is data prepared by the management of Seven Group Holdings Limited (“SGH”) and other associated entities and investments.

This data is included for information purposes only and has not been subject to the same level of review by the company as th e financial statements, so is

merely provided for indicative purposes. The company and its employees do not warrant the data and disclaim any liability flo wing from the use of this data by

any party.

SGH does not accept any liability to any person, organisation or entity for any loss or damage suffered as a result of relian ce on this document. All statements

other than statements of historical fact are, or may be deemed to be, forward-looking statements, and are subject to variation. All forward-looking statements

in this document reflect the current expectations concerning future results and events. Any forward-looking statements contained or implied, either within this

document or verbally, involve known and unknown risks, uncertainties and other factors (including economic and market conditions, changes in operating

conditions, currency fluctuations, political events, labour relations, availability and cost of labour, materials and equipme nt) that may cause actual results,

performance or achievements to differ materially from the anticipated results, performance or achievements, expressed, projected or implied by any forward-

looking statements.

Unless otherwise indicated, all references to estimates, targets and forecasts and derivations of the same in this material a re references to estimates, targets

and forecasts by SGH. Management estimates, targets and forecasts are based on views held only at the date of this material, and actual events and results

may be materially different from them. SGH does not undertake to revise the material to reflect any future events or circumstances.

Period-on-period changes that are greater than 100%, less than (100)% or change between positive and negative are omitted for presentation purposes.

Non-IFRS Financial Information

SGH results comply with International Financial Reporting Standards (“IFRS”). The underlying segment performance is consistent with the annual financial

statements and excludes Significant Items comprising impairment of equity accounted investees, investments and non-current assets, fair value movement of

derivatives, net gains on sale of investments and equity accounted investees, restructuring and redundancy costs, share of re sults from equity accounted

investees attributable to Significant Items, loss on sale of investments and derivative financial instruments, acquisition transaction costs, significant items in

other income, remeasurement of tax exposures and unusual tax expense impacts.

This presentation includes certain non-IFRS measures including Underlying Net Profit After Tax (excluding Significant Items), total revenue and other income,

Segment EBIT margin and Segment EBITDA margin. These measures are used internally by management to assess the performance of the business, make

decisions on the allocation of resources and assess operational management. Non-IFRS measures have not been subject to audit or review.

SGH Presentation | 20 September 2017 2

Transaction overview

Coates Hire is a market leader in equipment solutions with strong growth prospects

Acquisition of remaining Seven Group Holdings (“SGH”) has entered into binding agreements with an affiliate of Carlyle Asia Partners II,

stake in Coates Hire a fund managed by The Carlyle Group (“Carlyle”), convertible note holders and certain employees to acquire

from equity partners securities in Coates Group Holdings Pty Ltd

(“Coates Hire”) representing an economic interest of 53.3% not currently owned by SGH

Purchase consideration for the 53.3% of Coates Hire is $517m

─ Implies 6.5x EV / FY17 EBITDA for 100% of Coates Hire

In the 12 months to 30 June 2017, Coates Hire generated trading revenue of $918m and

underlying EBITDA of $308m

Coates Hire is the largest equipment hire company in Australia and is well positioned to leverage the strong growth

prospects in the East Coast infrastructure and construction markets

Strategic rationale The acquisition continues SGH’s focus on driving growth opportunities and efficient capital allocation in the

business:

− #1 hire equipment company in Australia

− Increases exposure to Australian East Coast infrastructure activity

− Low risk transaction given long involvement and part-ownership of the asset since 2008

− Enhances SGH’s portfolio as the company expands its industrial services business

− Financially compelling acquisition provides 15% accretion in underlying EPS in FY17 on a full year

(1) (2)

pro-forma basis and 91% increase in underlying FCF per share

(1) Based on the underlying result for the 12 months to 30 June 2017 on a continuing operations basis and assuming completion of the Coates Hire acquisition and sale of WesTrac China. Coates Hire financials based on disclosures as per the

2017 SGH Annual Report

(2) FCF is defined as underlying operating cash flow less net capex divided by the weighted number of shares on issue

SGH Presentation | 20 September 2017 3

Transaction overview (cont’d)

Coates Hire is a market leader in equipment solutions with strong growth prospects

Funding and expected Purchase consideration to be funded by existing cash reserves and undrawn bank facilities

financial impact

− SGH has significant liquidity through $520m in undrawn bank facilities, $516m in after-tax proceeds from the

sale of WesTrac China and the $420m value of the listed investment portfolio

(1)

− SGH pro-forma leverage (pro-forma net debt / pro-forma FY17 EBITDA) maintained at 3.8x following

completion of the transaction and the receipt of the WesTrac China sale proceeds

Conditions and Expected completion of acquisition: 25 October 2017

expected timing

Completion subject to debt rollover consent from Coates Hire lending group

(1) Based on pro-forma underlying EBITDA for the 12 months ended 30 June 2017, excluding the earnings contribution from WesTrac China. Pro-forma net debt includes Coates Hire net debt of approximately $1,039m as at 30 June 2017 and

includes the receipt of WesTrac China sale proceeds

SGH Presentation | 20 September 2017 4

Strategic rationale

Strengthens SGH’s position as a leading industrial services operator

#1 hire equipment Coates Hire is the leading equipment hire company in Australia, across a range of end markets

company in Australia

Strengthens SGH’s position as a leading provider of diversified industrial services

Diversified across products, customers and end markets

National footprint across >200 branches (1)

Increases exposure to Increases SGH’s direct exposure to Australian East Coast infrastructure, a sector which is underpinned by

growing infrastructure government spending and committed projects

sector activity

Coates Hire is a major beneficiary of current activity levels given its position as the largest equipment hire business

Longstanding and deep SGH has a long-standing involvement with the Coates Hire business, having first invested alongside Carlyle and

understanding of the management in 2008

Coates Hire business

The acquisition of the remaining 53.3% represents a low risk opportunity to obtain control of an attractive asset

Transaction is not subject to the usual due diligence and integration risks given long history

Enhances SGH’s 100% ownership of Coates Hire improves SGH’s portfolio; Industrial Services will contribute ~73% of Group EBIT

portfolio

Provides an opportunity to generate operational efficiencies:

– Significant funding synergy and savings across the Group

– Integration of WesTrac and Coates Hire improves customer solution offerings and operational efficiencies

Financially compelling 15% underlying EPS accretive on an FY17 underlying continuing pro-forma basis(2)

91% accretive on a FCF per share basis through access to 100% of cash flows

WesTrac China sale proceeds of approximately $516m after tax provides additional liquidity

(1) Branch network includes storage facilities and maintenance locations of WesTrac and AllightSykes

(2) Based on pro-forma EBITDA for the 12 months ended 30 June 2017, excluding the contribution from WesTrac China. Pro-forma net debt includes Coates Hire net debt of approximately $1,039m as at 30 June 2017 and WesTrac China sale proceeds

SGH Presentation | 20 September 2017 5Strategic rationale (cont’d)

Strengthens SGH’s position as a leading industrial services operator

FY17 EBIT (1,2) FY17 pro-forma EBIT (1,3)

Other

Energy 3%

Other 6%

Energy 4%

9%

Media

17% WesTrac

40%

Media

24%

$297m WesTrac

55%

$415m

Coates Hire

8%

Coates Hire

34%

Industrial services: 63% Industrial services: 73%

(1) Continuing operations only. Excludes WesTrac China

(2) Coates Hire FY17 reported contribution is based on equity accounted share of associate net profit

(3) Coates Hire FY17 pro-forma contribution is based on consolidation of EBIT

SGH Presentation | 20 September 2017 6Overview of Coates Hire

#1 equipment hire company in Australia

Australia’s largest equipment hire and solutions provider

− Approximately 4x larger than the nearest competitor

− Strong market brand awareness and preference

− Highly diversified end market exposure and customer base

Operates a network of over 200 branches nationwide

− Network / brand / people / customers allows Coates Hire to flex

in the right places

Strongly leveraged to growth from Australian East Coast

infrastructure and construction markets

− NSW and VIC businesses continue to perform well with revenue

up ~15% in both states to Jun-17

− Group revenue up 5% YoY to Jun-17 with EBIT margins

increasing from 11% to 15%

− Fleet relocation, cost control, price realisation and branch

rationalisation initiatives yielded a 46% growth in FY17 EBIT

Strategic initiatives in place to drive future profitability

− Renewed focus on turnaround time to enhance fleet utilisation

− Investment in data and digital to drive customer satisfaction and

business efficiency COATES HIRE’S PRODUCT RANGE

− Establishment of a centralised customer contact centre Access Generators & Power Distribution Materials Handling Tools & Equipment

Air & Air Accessories Industrial Tools & Equipment Portable Buildings & Toilets Traffic Management

− Establishment of a new transport management system to drive Compaction Ladders & Scaffold Propping Training (RTO)

efficiencies across the branch network Concrete & Masonry Landscaping Pumps & Fluid Management Trucks, Vehicles & Trailers

Further opportunities to enhance value by improving time Earthmoving Lift & Shift Shoring Welding

Floor and Cleaning Equipment Lighting

utilisation, pricing, and cost efficiencies

SGH Presentation | 20 September 2017 7Coates Hire key highlights FY17

Achievements and changes

Achievements in FY17 Changes in FY17

Improved safety with a reduction in LTIFR of 48% over FY16 Resized the business:

Assets on hire continue to reach new highs with Jun 17 at 55.7%, – Completed fleet size reductions after the resources boom with

2.2% above pcp $719m of original cost assets disposed over the last three years

FY17 average daily sales were higher than budget and prior year; – Fleet now appropriate for the market

achieved with lower headcount and reduced network footprint

– Reduced headcount in July 2016 with average heads for FY17

Profitability has been restored to the business with a $70m down 10% on FY16

turnaround in PBT from FY16

Movement of equipment from WA to East Coast is complete

Debt reduction achieved while growing revenue:

Customer Contact Centre in place in the North BU

– Completed $75m mandatory repayment of senior debt by Apr 17

Updated business strategy rolled out across the business

– Two months and $18m ahead of budget

Reshaped the ELT in August 2017 to focus the business on product

EBA in place for next 3 years category management and driving alignment between sales and

operations

– 1.5% increase each year in 2018 and 2019

– Certainty of employment conditions until 2020

SGH Presentation | 20 September 2017 8Safety first

Zero harm

Annual Lost Time Frequency Rate (Rolling 12m) Annual Total Recordable Injury Frequency Rate (Rolling 12m)

as at 30 June 2017 as at 30 June 2017

Safety measures are moving in the right direction

But still work to do with further reductions targeted in FY18

LTIFR has reduced by 48% since FY16

TRIFR has reduced by 22% since FY16

SGH Presentation | 20 September 2017 9Coates Hire’s strategic pillars driving long-term success

Sustainable profit delivered safety

Financial Targets Non-Financial Targets

Geographic Footprint Profitable Markets and Products Prioritise Profitable Customers

PEOPLE CUSTOMER PRODUCTS & REVENUE BRAND OPERATIONAL

SERVICES MANAGEMENT EFFICIENCY

Right People Valued Understand Market Recognised National

Right Structure Prioritised our markets Relevant, Relevant Consistent

Customer Profitable and provide matched to Understood Agile

Centric and profitable value Connected

Commercial solutions proposition

Data driven insights into category and product decisions

A workplace culture that values leadership, trust, learning, teamwork, execution discipline and courage

Deep market and customer analysis to drive future investment decisions and enhanced customer experience

Investing in capabilities of the business – data capabilities; online channel; category managers; digitisation

Driving Growth and Returns Through the Cycle

SGH Presentation | 20 September 2017 10Major initiatives in FY18 and beyond

Reinvestment in the $143m in net capital expenditure budgeted in FY18 up from $64m in FY17

business

Long-term purchasing arrangements with OEMs to improve “whole of life” ownership costs

Additional operational spend of $10m in FY18 for improvement initiatives (refer below)

Turn Around Time (TAT) Management and delivery of People, Process and Technology capabilities

Aimed at improving the time an asset spends between being “Off Hire” and being made “Available for Hire”

Customer Contact Improving consistency in process and customer experience

Centre (CCC)

Ultimately assisting in the drive to optimise fleet utilisation

Creating a foundation for transition to digital with real time fleet data

Transport New Transport Management System to improve transport efficiencies across the branch network

Data analytics to provide insights to drive better negotiated contracts and rates with external suppliers

Digital Development of an online channel to meet customer demands

Streamline processes to drive efficiencies throughout the business including capabilities for fleet optimisation and

enhanced analytics

Culture Focus on workforce engagement, reduced turnover, training and leadership

Redefining culture to align to achieving strategic objectives

Market Focus on growing market share in a buoyant rental market

Projected market growth of 3.1% per year from FY17 to FY22 (1)

Network Looking at opportunities to open branches – Weipa and Grafton have been successful in FY17

(1) Rental market growth based on IBISWorld estimate for machinery and scaffolding rental growth, October 2016

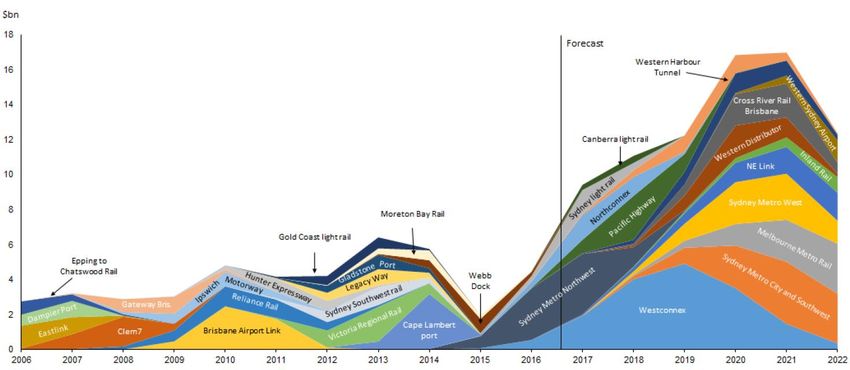

SGH Presentation | 20 September 2017 11Supportive market outlook

Positive outlook for infrastructure projects

Coates Hire set to capture further upside

Strong growth in infrastructure activity on the Australian East Coast has improved demand for construction equipment and heavy machinery

Further upside to be captured given that peak investment for committed projects is expected to occur in 2020 / 2021 with further projects to emerge

Source: Deloitte Access Economics Investment Monitor June 2017

SGH Presentation | 20 September 2017 12Coates Hire outlook underpinned by major

long-term projects

Melbourne Arrium Bauxite

1 Barangaroo 2 WestConnex 3 Pacific Highway 4 Metro Rail 5 Weipa

Type Construction Road Infrastructure Road Rail Mining

Commence Jan-12 Mar-16 Jul-16 Jan-18 Mar-16

Finish Jan-20 Jun-20 Dec-21 Dec-23 Dec-18

SGH Presentation | 20 September 2017 13Diversified business model

Diversified end markets with strong leverage to Diversified blue chip customer base

1 infrastructure market 2

More than 17,000 customers

FY17 sector revenue split

No single customer represents more than 3% of revenues, with the

Government Oil & gas top 100 representing < 40%(1)

5% 7%

Non-residential Mining & resources

13% (production)

10%

Mining & resources

Residential

(development)

4%

6%

Industrial

maintenance

6%

Events

3%

Engineering & Commercial &

Construction manufacturing

34% 12%

(1) Based on FY17 results

SGH Presentation | 20 September 2017 14Strong fleet metrics and utilisation rates, enhancing return

on invested capital

Fleet on hire experiencing positive trends Efficient return on invested capital via reduction in

1 2 redline equipment and improved turnaround time

58% 30%

55.7%

56%

53.5% 27.6%

54% 28%

52%

50% 26%

47.4%

48%

46% 24% 23.5%

23.0%

44%

42% 22%

Jun-15 Jun-16 Jun-17 Jun-15 Jun-16 Jun-17

Targeted capex investment program... …supported by data driven disposals program

3 4

(YTD Actual capex approvals $m) (YTD Actual Disposals $m)

140.0 150

120.0 125

100.0

100

80.0

75

60.0

50

40.0

20.0 25

– 0

Oct-16

Mar-17

Apr-17

Oct-16

Mar-17

Apr-17

Jan-17

Jun-17

Jan-17

Jun-17

Feb-17

Feb-17

Aug-16

Sep-16

Nov-16

Dec-16

Aug-16

Sep-16

Nov-16

Dec-16

May-17

May-17

Jul-16

Jul-16

SGH Presentation | 20 September 2017 15Coates Hire benefiting from positive market trend

Trading revenue ($m) Underlying EBIT ($m)

279

1,241

+5%

1,095

188 +46%

919 873 918

142

104 97

FY13 FY14 FY15 FY16 FY17 FY13 FY14 FY15 FY16 FY17

Underlying EBIT margin Underlying EBITDA & net capex ($m)

22.5%

+4ppts 534

17.2%

15.5% 432

11.4% 11.1% 310 308

267

230

125

84 79 64

FY13 FY14 FY15 FY16 FY17 FY13 FY14 FY15 FY16 FY17

EBITDA Net capex (excluding UK)

SGH Presentation | 20 September 2017 16Pro-forma financial impact

SGH financial profile – pro-forma impact(1) Pro-forma financial impact (FY17)

Reported Pro-forma

FY16 FY17 FY16PF FY17PF

15% underlying EPS accretive on FY17 continuing

Revenue 2,237 2,282 3,110 3,193 pro-forma basis(2)

Growth (%) (pcp) 2.0% 2.7% 91% accretive on a FCF / share basis through access

to 100% of cash flows(3)

Other income 70 52 68 55

Pro-forma net debt / pro-forma FY17 EBITDA maintained

Share of results from equity at current level of 3.8x(4) following transaction completion

90 121 86 98

accounted investees

Strong deleveraging expected given cash flow profile

Operating expenses (2,092) (2,127) (2,698) (2,735)

of combined business

EBITDA 305 328 566 611

EBITDA margin (%) 13.6% 14.4% 18.2% 19.1%

Depreciation & amortisation (33) (31) (202) (196)

EBIT 272 297 364 415

EBIT margin (%) 12.1% 13.0% 11.7% 13.0%

(1) Financials only include continuing operations. FY16 and FY17 numbers include income from associates

(2) Based on the underlying result for the 12 months to 30 June 2017 on a continuing operations basis and assuming completion of the Coates Hire acquisition and WesTrac China sale are completed

(3) FCF defined as operating cash flow less net capex divided by the weighted number of shares on issue

(4) Pro-forma net debt calculated as SGH pro-forma debt less pro-forma cash and cash equivalents as at 30 June 2017, Coates Hire net debt of approximately $1,039m, and the receipt of WesTrac China sale proceeds

SGH Presentation | 20 September 2017 17Acquisition funding

Purchase Price Purchase consideration of $517m for 53.3% economic stake not owned by SGH

Purchase consideration to be funded via:

Funding ─ Existing cash / undrawn debt facilities

─ Expected proceeds of approximately $516m after tax from the sale of WesTrac China

SGH will assume Coates Hire’s cash of $48m(1) and Coates Hire’s debt of $1,087m(1)

Debt Transaction is contingent on bank rollover consent

If satisfactory waivers cannot be obtained, SGH may seek to refinance the debt

Timing Expected acquisition close: 25 October 2017

(1) Coates Hire cash and debt as at 30 June 2017

SGH Presentation | 20 September 2017 18Trading update and outlook

Coates Hire

Poised to benefit from Coates Hire is expected to continue to benefit from branch rationalisation and fleet redeployment undertaken in the prior year, together with

infrastructure activity price realisation strategies as the New South Wales and Victoria infrastructure projects are delivered

Strong start to the FY18 financial year with July and August tracking ahead of both pcp and YTD budget, with the market remaining

Strong start to FY18 buoyant, driven by strong growth from the Australian East Coast infrastructure and construction markets

Coates Hire guidance Underlying FY18 EBIT on track to achieve growth of 10% on FY17

SGH

WesTrac’s strong parts performance is expected to continue while service revenues will be impacted by ongoing cost reduction programs

WesTrac continuing to including insourcing of maintenance work being undertaken by some customers

benefit from mining

Product sales in the mining market are anticipated to remain subdued; however there has been an increase in forward orders coupled with

production cycle extended lead times from Cat, signalling an impending fleet renewal cycle

Energy assets well Earnings from Beach Energy are expected to increase with production to be maintained near record levels in FY18 as demand strengthens,

positioned in East Coast driven by the current East coast gas shortage

Seven West Media should benefit from Commonwealth Games broadcast to underpin its robust TV market share growth in a challenging

Media to deliver ongoing advertising market. Publishing trends are set to continue with targeted costs reductions to offset the uplift in AFL costs.

TV ratings performance

Assuming a similar television market outcome, Seven West Media FY18 EBIT is estimated to be 5 per cent down on FY17

Strong start to the year for WesTrac in July and August, reflecting the core demand of the mining production cycle and East Coast

Strong start to FY18 infrastructure

Sale of WesTrac China is expected to complete in October subject to regulatory approval from MOFCOM

SGH provided guidance at its annual results announcement on 22 August 2017 that FY18 underlying EBIT from continuing operations is

Group EBIT guidance expected to be 5-10% up on FY17

SGH Presentation | 20 September 2017 19Appendix

SGH Presentation | 20 September 2017 20SGH pro-forma balance sheet

Basis of preparation:

- Acquisition calculated as a step acquisition with an assumed 30% control premium in accordance with AASB 3 Business Combinations

- Goodwill on acquisition subject to change within 12 months of transaction close pending finalisation of detailed purchase price accounting

- The step acquisition will result in the recognition of a ~$47m gain in the Group's FY18 P&L due to the remeasurement to fair value of the Group's existing 46.5% equity accounted interest

SGH Presentation | 20 September 2017 21SGH pro-forma free cash flow

SGH Presentation | 20 September 2017 22Branch network overview

Coates Hire tailors its branch model based on location and customer needs

#1 Generalist branch structure #2 Hub and spoke structure #3 Project site facilities

Typically used in regional areas that do not Typically adopted in metro regions to For certain large customers / projects,

have sufficient scale for hub branches ensure efficient coverage and use Coates Hire will establish a project facility

of space on the customer’s site to service their key

Larger branches which are stocked to

needs

cater for regional needs Multiple non-specialist 'spoke' stores set

up in strategic, highly visible locations and Typically these sites are for large

Will typically include a broad range of

stocked with non-specialist equipment engineering or mining projects which

equipment across all categories

require a high level of product expertise /

– Target market is smaller contractors,

service capability, and broad range of

tradesman and retail. However, also

services major customers with projects equipment to be located on the site

within their geographical territory Dedicated Coates Hire personnel are on

hand to assist the customer and provide

Large specialised 'hub' facilities created to

training where needed

support spoke branches with specialist

equipment and service major customers

– Generally located in less visible

locations, but with access to major

transport routes

– Target customers include larger

construction, engineering clients

SGH Presentation | 20 September 2017 23Overview of product offering

Coates Hire has the broadest range and largest fleet in Australia

Broad range of product, largest fleet and wide end market exposure

Continuous investment in new equipment means Coates Hire has broadest range and largest fleet in Australia, including special ised equipment to

meet specific mining, LNG and infrastructure market requirements

Focus on highly flexible fleet, which can be used across multiple end-markets

Maintains strong partnerships with only the highest quality equipment manufacturers

The fleet is rigorously maintained to the highest standards through a customised integrated equipment management system

With >200 branches, Coates Hire has the logistics capability and infrastructure to deliver equipment to locations anywhere in Australia

A team of dedicated product specialists providing quality advice

Access Air and air Compaction Concrete and

accessories masonry

Earthmoving Floor and Generators Ground

cleaning and power equipment

equipment distribution

Industrial tools Ladders and Landscaping Lift, shift and

and equipment scaffolding propping

Lighting Materials Offshore Tools and

handling equipment

Pumps and fluid Site Traffic Welding

management accommodation management

Trucks, vehicles

and trailers

SGH Presentation | 20 September 2017 24Fleet management cycle

Comprehensive strategy across the full equipment life cycle

#5 #1

Disposal Hire fleet investment

Equipment which is uneconomic to #5 Formalised hire fleet investment process

maintain is disposed of through a Hire fleet

which provides an approval framework

number of market channels Disposal investment

for new purchases

Dedicated disposal managers ensure Process includes an assessment of

strong commercial outcomes operational opportunity and financial

#1 profile of investment

#4 Final investment approved by CEO/CFO

#4

Fleet maintenance

Coates Hire’s ‘RUSC’ program is a #2

leading maintenance program in the Fleet procurement

Fleet Fleet

industry maintenance procurement Full technical and commercial

Assets undergo a detailed fleet assessment

inspection after each hire Detailed tender processes

Regular scheduled services are #2

Strong, long-standing relationships with

undertaken in accordance with the #3 Fleet key suppliers provides a competitive

RUSC program monitoring advantage for Coates Hire

#3

Fleet monitoring

Regular monitoring of key KPIs: dollar and time utilisation, slow moving

and underperforming assets, capital returns

Regular reports generated, summarising areas of underperformance,

to ensure problems can be quickly identified and addressed

Relocation of underperforming assets to areas of higher demand

SGH Presentation | 20 September 2017 25Customer value proposition

Unmatched brand, product and service offering

Our vision: right equipment, right place, right time

Unmatched branch network of >200 branches Formal national account management teams

Branch network Enables Coates Hire to service the entire National offering to manage and meet demand from major

Australian market customers for national agreements

Broad sector and project coverage with over Largest hire fleet of equipment in Australia

130 years industry experience Equipment range and

Market expertise ~340,000 individual pieces of equipment

Track record of partnering successfully with availability covering general hire and special project

customers on projects across various markets needs

Broad range of project site facilities that

Ability to co-ordinate logistics of transporting provide unparalleled service levels

Transportation offering equipment to customers’ sites Project site facilities

Ability to tailor a project site facility to meet

customer site-specific requirements

Industry leading equipment management

Integrated equipment Safety, environmental ISO accreditation in health, safety, quality

system, ensuring equipment has been

management and compliance management and environmental compliance

maintained to the highest safety standards

Provides customers with a Registered Training

National product teams

Organisation for their training requirements

Product expertise Dedicated team of Product Specialists trained Training – RTO nationally

to support customers and internal staff

Compliant with relevant legislation

Provides fleet and asset management services

Specialist engineering Engineered solutions for shoring, propping and for any industrial operation

water management Industrial shutdowns

solutions

Clear industry leader

SGH Presentation | 20 September 2017 26Equipment rental industry structure and trends

Coates Hire well positioned as a national industry player

Industry structure: highly fragmented with national scale

Fragmented market Fragmented with a limited number of players of scale

Coates Hire footprint:

– Extensive branch network; rental fleet spanning > 20 product categories and > 7,500 models of equipment

Advantages of scale

– Service capability to comply with manufacturers standards and meet customer requirements for reliability and safety compliance

– Specialist product capabilities, such as dewatering and shoring, delivered through systems, people and processes

Limited financial capacity Financial resources allow Coates Hire to respond to market opportunities and compete strongly

of competitors

Key trends: customers increasingly amenable to rental equipment and preference for single provider with broad range

Larger customers continue to look for a single, national provider of equipment

Customers want a single

– Coates Hire has established national agreements and experienced national account management teams serving

rental provider

major customers

The prevalence of larger mining, energy and infrastructure projects in Australia will favour rental providers who can offer a full product suite

Customers need a broad and associated services to their customers

product / service offering

Coates Hire is one of the few companies with the fleet size and financial capacity to service projects of this scale

Customer focus on health and safety is influencing customer decision-making

Health and safety

SGH Presentation | 20 September 2017 27Overview of SGH structure

Diversified industrial services and investment group

Industrial services(1) Media investments Energy Other investments

Listed Investments

Business

Australia Property Investments

Business Diversified Media

Caterpillar dealer in Industrial and general Industrial lighting, Diversified Diversified

(Broadcast, Publishing

description WA NSW and ACT equipment hire pumps, generators Oil & Gas investments

and Digital)

Listed portfolio: Store of value

Supplies one of the world’s Uniquely positioned to and liquidity for the Group

#1 equipment solution Australia’s largest

Strategic Largest equipment hire broadest ranges of lighting take advantage of the

company in WA , NSW diversified media

position and ACT

company in Australia towers, pumps, generators,

company

Australian East Coast Property portfolio: Proven

engines and compressors gas shortage ability to create value through

realisation of property assets

34%

FY17 EBIT 40%

contribution Minimal

(Pro-forma)(2)

17% 6% 3%

Seven Group SGH Energy 100%

100% 100% 100% 41% Beach Energy 23% 100%

ownership

(1) Pro-forma for sale of WesTrac China; expected to complete by October 2017

(2) Based on Segment EBITDA for the 12 months ended 30 June 2017. Segment EBITDA comprises profit before depreciation and amortisation, net finance expense, income tax and significant items. WesTrac Australia segment results have been

reduced in relation to the elimination of sales to Coates Hire. Media investments comprise investments accounted for using the equity method and financial assets fair valued through other comprehensive income. Excludes AllightSykes given

the negative contribution from the segment

SGH Presentation | 20 September 2017 28You can also read