PREVAIL & PROSPER: A view on what's next for the EMEA investment market - WHAT'S NEXT | EMEA - Colliers International

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

WHAT’S NEXT | EMEA

PREVAIL & PROSPER:

A view on what’s next for

the EMEA investment market

PREVAIL & PROSPER: A view on what’s next for the EMEA investment market 1

3 Executive Summary

8 Macro-economic trends

12 Capital Markets Trends

CONTENT 13 Concluding points

Executive Summary

Establishing where markets are at as a result of this Some 95% of investors surveyed by Colliers in The major positive is that momentum is back in the

global pandemic has been like wading through a sea of September expect the European investment market to market as of September, as big-ticket assets and

fog over the last six months. The initial and very deep stabilise in the next 12 months, and we are forecasting portfolios for sale add much greater liquidity to the

‘lock-down induced’ economic and market shocks that a mid-case rebound in activity in Q4 of €70 billion, European market. Pricing has already adjusted over

have been endured globally have been followed by a up to a best-case scenario of €100 billion. It certainly the course of Q2 and Q3, and many markets point to a

swift return to growth over the summer months, almost looks like we have passed the nadir in Q3, which would further adjustment in the next 12 months as the rest of

universally. mean that activity in 2020 is only down by around 15% the fog starts to lift. For our own outline view on how

y/y. A considerable feat, all things considered. specific markets and sectors match up to investment

As of today, despite the threat of a rise in the R-rate opportunities by strategy, we have outlined these in the

driving localised market lockdowns, the fog is lifting table below.

and the impact has been largely as expected. That

doesn’t mean we’re back to where we were, by WHAT’S NEXT: PREVAIL & PROSPER

any means, as COVID-19 has accelerated numerous

structural trends that were developing before the Where to buy:

Table 1: Where to buy: Location/Sector

location/sector strategiesStrategies

pandemic: agile working, omni-channel retailing,

digitisation and a much greater adoption of ‘Proptech’

to manage, view and transact on assets and portfolios. Sector Stable Short-term flux Big Opportunity Upcoming

It will take years for some ‘traditional’ elements of our (Core) (Core-plus) (Value-Add) (Opportunistic)

economies to get back to par, if ever, with business

Offices London, Paris, Dublin London Decentralised locations

sectors, real estate asset types, city and national German7 Warsaw Paris

markets recovering at different speeds and in very Amsterdam Helsinki Milan

Copenhagen Prague Madrid

different ways. Stockholm, Oslo UK Regions *Flex

While the recovery is on track, the current investment Retail Grocery All major cities Decentralised locations

market feels somewhat like ‘wading through treacle’

as one investment agent put it. Treacle is a bit like Retail Parks All major cities

marmite, it is very bitter-sweet. Which sums up the Retail Shopping Dusseldorf Non central shopping centres (car-based, grocery All major city center

Berlin anchor) assets

state of the situation pretty well – there will be a bitter Centres Vienna

pill to swallow for some, especially current owners of Warsaw

assets at the distressed end of the spectrum; much Residential (BTR, Germany, Nordics, Netherlands, UK, Madrid Warsaw

sweeter for those set to prosper with assets that have PRS, Affordable)

Dublin, Milan, Paris Prague

recently appreciated in value on the sale-side, and of

course those with dry powder looking to strike deals at Too early to tell, but southern Europe will be a big area of distress/ opportunity

more favourable pricing levels. Hotel/Hospitality

PREVAIL & PROSPER: A view on what’s next for the EMEA investment market 3

Summary points: by sector WHAT’S NEXT: PREVAIL & PROSPER

Where to buy: I&L sub regions

Where to buy: I&L sub regions

INDUSTRIAL AND LOGISTICS 4

Industrial and logistics is the top pick with almost all investors shifting their

1. WHAT’S

1. Benelux,

Benelux, NEXT: PREVAIL

Rhine-Ruhr

Rhine-Ruhr & & PROSPER

Ile-de-France

& Ile-de-France

allocation to this sector. Many large deals now coming to market are I&L 2. Germany

2. Germany&&Core CEE

Core CEE

portfolios, with an estimated €3bn worth launched in Q3. 3. Where

3. United

UnitedKingdom to (England)

Kingdom buy: I&L sub regions

(England)

4

The defensive nature of I&L, and the key demand drivers for big box 1. Benelux, Rhine-Ruhr & Ile-de-France

logistics, cold storage and data centres is buoying demand while availability 2. Grade A&I&L

Germany Space

Core CEE (Mn sqm) - by Sub-region 3

120 3. United Kingdom (England)

continues to diminish. These strong fundamentals are supporting rental 100 2

growth in core locations, and even some yield compression. This is driving 80 Grade A I&L Space (Mn sqm) - by Sub-region 3 1

120

core prices up by around 20% since the end of Q2; value-add I&L assets 60

100 2

and portfolios have increased in price by around 10%. 40 80 1

20 60

0

40

5

The structural demand drivers and tight supply/demand fundamentals 20

Benelux+Rhine+Nth Germany+CEE UK 7

0 France 5

of this sector point to further rental growth in core locations over the Benelux+Rhine+Nth

France

Germany+CEE UK 7

next 12-24 months.

4. Nordics (Denmark, Sweden, Norway, Finland) 6

4. Nordics (Denmark, Sweden, Norway, Finland) 6

5. Alpine (Italy,(Italy,

5. Alpine Switzerland,

Switzerland,Austria, SWFrance)

Austria, SW France)

OFFICES 6. Iberia

6. (Spain, Portugal)

Iberia (Spain, Portugal)

The reverse has been seen for offices, with core-plus and value-add pricing 7. 7. South-east

South-east Europe Europe

moving out by up to 20%, depending on the market, but core pricing remains

tight with limited movement in pricing. Headline rents are being buoyed by WHAT’S NEXT: PREVAIL & PROSPER

incentives, but limited vacancy in most markets is limiting price movements.

Rents

Office vs vs

rents Economic Outputlong-term

economic density: or Workforce

pricing Density?

correlation

Mid-term, the use of offices is adjusting as occupiers shift to an agile working

model, yet this model differs by company. Most occupiers are reconsidering CATCH M E N T E con omic Ou tpu t vs Offic e Ren ts & Ou tl ook , [Q2 2020]

Down Stable Up

how their workplace portfolio will function in the future, but a core office HQ is LONDON

here to stay for the majority alongside the adoption of third spaces and home

working.

O f f i c e C B D Re n t s ( E u r / s q m / m o n t h )

80

PARIS

STOCKHOLM

The definition of core, however, is likely to tighten to become a high-tech,

DUBLIN

MILAN

FRANKFURT

ESG-relevant spec asset, in a very accessible location with a flexible 40 BERLIN MUNICH

OSLO

AMSTERDAM

BRISTOL MANCHESTER

MADRID ROME

footprint and fit-out. These assets will maintain their position as key in HAMBURG

BIRMINGHAM

LEEDS

BRUSSELS DUSSELDORF

BARCELONA VIENNA

driving company revenue as the client-facing centre of the brand, as a place to LISBON WARSAW STUTTGART

ATHENS COPENHAGEN

COLOGNE

collaborate and drive company culture. 20 PRAGUE

BUDAPEST

ROTTERDAM

BUCHAREST

BRATISLAVA

The pricing of these assets should be in-line with current values, relative to

the economic density generated by the city they are in. In this regard, London 10

2 4 8 16 32

and Paris are at the apex, as one would expect, but most city office rents look O ffi c e S ec t o r G V A D ens i t y ( E u r M n / s q k m )

in-line with economic density. In fact, some markets such as Manchester and

Dusseldorf look under-priced.

PREVAIL & PROSPER: A view on what’s next for the EMEA investment market 4WHAT’S NEXT: PREVAIL & PROSPER

HOSPITALITY Hotels:

Hotel a disappointing

occupancy summer

trends: a disappointing summer

The European summer is not what many in the hospitality business had hoped

for, with occupancy down by 50% on this time last year. Investment volumes

Hotel Occupancy vs Tourism Source

have rescinded over the course of 2020, and with further uncertainty over European Hotel Occupancy

100%

travel restrictions for another twelve months until a vaccine is established, 90

produced and distributed, it will be longer before the hospitality sector truly

90%

80 Finland Germany

hits the bottom. Demand will bounce back eventually, but this is a real 70

80%

Turkey Poland UK

test as to who can prevail in the interim with cash levels and government 70% Russia

60 Romania

Spain

Domestic Tourism %

Czech Republic

support thinning out. 50

60% France

Netherlands

Hungary Ireland

50%

40 Italy

For the private equity houses looking at opportunities, Q4 2020 and Q1 2021 40%

Slovakia

could start to see many interesting opportunities emerge across Europe, not

30 Bulgaria Portugal

Switzerland

30%

Austria

just in the more distressed summer destinations. In the meantime, budget 20

20%

Belgium

3-star hotel operations continue to be robust, especially those supporting car- 10

10%

Greece Croatia

dependent business travel. Some hotels offer the potential for (short-term) 0

June July August 0%

re-use as flexible office space, although is most likely a short-term solution. 2019 Avg 2020 Avg

15.0 20.0 25.0 30.0 35.0 40.0 45.0 50.0

There may be potential for some operations to provide quasi-fractional options Summer Occupancy Rate Average (June, July, August)

in cities where agile working impacts commuting patterns.

Source: Colliers / Worldometers/ GlobalData/ STR

RETAIL WHAT’S NEXT: PREVAIL & PROSPER

Retail has already been impacted by the rise of e-commerce, but physical

Retail

Retail Shopping

shopping Centre

centre values values &

& volumes: volumes:

feeling feeling

the impact the impact

retail space remains an important part of the omni-channel marketing and

purchase journey.

COVID-19 Impact: Shopping Centre volumes, values and 12 month outlook [Q2 2020 vs Q4 2019]

The latest city mobility challenges and retailer insolvency do point to an Down Stable/Down Stable Stable/Up Up

acceleration of lower priced retail space and growth in the use of turnover rents. 80

Outside of the grocery and convenience element, this is likely to push the retail

Investment volumes, % change, past 12M vs 5yr

60 Paris Lisbon

sector through a big, final pricing reset with the need for retailers and owners 40

Berlin

Budapest

to find common ground on acceptable terms that encapsulate turnover rents 20

Rotterdam

Munich

Dusseldorf

and the role of physical space in the omni-channel transaction process. While 0 Moscow Athens

Stuttgart

the initial point of purchase has become increasingly online, with fulfilment

average

-20 Amsterdam

Bristol Hamburg

Stockholm Milan

handled in the logistics chain, the physical store performs a critical role in -40 Vienna

Frankfurt

London

building a brand and ‘showrooming’ in addition to supporting click-and-collect

Brussels

Copenhagen

Birmingham Manchester

-60 Oslo

Rome

and traditional retialing functions. Prague Barcelona Dublin

-80 Madrid

Bratislava Leeds Warsaw

-100 Istanbul Sofia Bucharest

Shopping centres have taken a big hit as footfall has dried up, and the value -120

outlook for the next 12 months looks very weak across Europe, especially in the

-40 -35 -30 -25 -20 -15 -10 -5 0 5

Capital value change, %

bigger cities as this adjustment is ongoing. Meanwhile, appetite continues to grow

for retail parks, especially those that can support a reconfiguration that allows

logistics facilities to be built on site, supporting click and collect in the retail park

units and broader distribution to the local catchment. PREVAIL & PROSPER: A view on what’s next for the EMEA investment market 5RESIDENTIAL

Residential has proven to be most resilient to date, with investment demand The bifurcation of the US housing market from the “have’s” capable of buying

increasing as funds increase their assets under management (AUM) weightings homes in remote locations, pushing up localised house prices outside of the

to this sector. The London and UK markets seem to have been buoyed by the re- city…. To the “have not’s”, struggling to make ends meet and satisfy their rental

distribution of Hong Kong funds in Q2 and Q3 of this year. commitments is an extreme example of how housing markets have been

impacted by the pandemic.

While residential has been robust to date, there are concerns as to how

defensive it will be, given the risk of higher unemployment on those most While there has been a notable shift in demand for ‘Zoom-Towns’ outside of

likely to be renters. Hence investors are increasingly building their AUM in central areas, we don’t anticipate such a clear trend emerging across Europe.

European residential with a focus on affordable Build-to-Rent (BTR) and It seems a little premature to think a broader distribution of working populations

Private Rented Sector (PRS). is going to be sustainable, where it requires a regular long commute. It’s not

very agile to be living too far away from the focus of core office - collaborating

with colleagues and working with clients.

WHAT’S NEXT: PREVAIL & PROSPER

Residential investment momentum

Residential investment momentum: major city destinations

In vestmen t M omen tu m: 2 0 2 0 Yea r-to-da te

[Recent performance vs 5yr average & Covid-19 impact

Bubble size represent activity volumes]

100% Q2 Q3

90%

Ac t iv it y v o lu m es : 12 M r o llin g v s 5 y r a v er a g e

Munich

80% Birmingham London

Stockholm

70% Paris Manchester London

Dublin

60%

Stockholm Paris

50%

40% Munich

Frankfurt

30%

20% Amsterdam

Amsterdam Helsinki

10%

Frankfurt Leipzig

0% Madrid Vienna

Berlin Helsinki

-10% Vienna Hamburg

Madrid

-20% Berlin

Hamburg Malmo (Helsinborg)

-30% Copenhagen

-40% Copenhagen

-50%

0 50 100 150 200 250

12 M r o llin g a c t iv it y v o lu m e in dex: 2 0 19 =10 0

PREVAIL & PROSPER: A view on what’s next for the EMEA investment market 6Summary Points WHAT’S NEXT: PREVAIL & PROSPER

GDP Impact:

City GDPbig cities have

impact: thefelt

biga hit

muchis greater economic impact than mid-sized

to retail/leisure/hospitality/ancillary services

Big Cities Mid-sized Cities

While prevailing will be a real challenge for many existing owners, especially 100% 100%

those in the retail and hospitality sectors, investors remain primed ready for 95% 95%

opportunities in all real estate sectors on a selective basis. 90%

90%

85% 85%

Having fewer people in the centre of cities every day is clearly having a

80%

high impact on city economies, especially in the low-tech ancillary retail

80%

75%

and hospitality sectors which will need to downsize. Any resulting pricing 75%

adjustment will of course have a broader impact on values as competing 70% 70%

use pressure diminishes. Despite this, people travelling to the centre for core 65% 65%

client-facing and collaborative activities will likely see thisWHAT’S

as an opportunity 60%

NEXT: PREVAIL & PROSPER

60%

to enjoy the retail, events and hospitality on offer once markets make it 55% 55%

The redistribution of city economies …and value

through COVID, but a positive re-configuration of cities is inevitable. 50% 50%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Berlin Paris London Milan Madrid Stockholm Amsterdam Frankfurt Brussels Prague Warsaw

Cities will need to adapt as they always have, but economic output and value

is likely to redistribute, rather than be lost as markets recover. This will

create an opportunity for the redevelopment of assets in cities to support

changes in the way we work and live. With an increased focus on supporting

communities and neighbourhoods, this in itself will create more energy-

efficient and sustainable cities to match the increasing shift to ESG-based The redistribution of city economies …and value

strategies that the majority of the investment community has adopted.

PREVAIL & PROSPER: A view on what’s next for the EMEA investment market 7Macro-economic trends and outlook

BUSINESS SECTOR IMPACT: THE K-SHAPED RECOVERY

A long-term view of FDI into Europe shows the market will most likely be at its lowest to bounce back within the next year. Professional services operate at a lag, although the

ebb since pre-2003 when FDI was first recorded, and almost half of the level of FDI seen lawyers and accountants are undoubtably busy, but low-tech services and manufacturing

in 2019. It simply highlights the extent to which occupier decisions have been put on hold don’t get back until 2022/23….and some of these jobs and sectors may never come back

until the future for many businesses becomes clearer, and there is an identifiable K-shaped to the same levels. In particular, major structural changes in the energy and automotive

recovery happening depending upon the business sector. sectors had already begun pre-COVID, while city centre low-tech services and the aviation

industry are on for a significant reset as the world shifts to a new normal.

There is clearly a diversified impact with retail services/hospitality not expected to recover

until 2023 - thus a drag on national and city economies dependant on it. Whereas health,

public administration and what could be broadly aggregated as the ‘high-tech’ or value-add

services

WHAT’SofNEXT:

IT, comms, finance

PREVAIL & insurance, and scientific/life sciences sectors are due

& PROSPER

The K-shape: When sectors get back to parity

The K-shape: when sectors get back to parity

ADMIN PROFESSIONAL

& SUPPORT ACCOMMODATION

HUMAN HEALTH/ PUBLIC ADMIN SERVICES AVIATION

SOCIAL WORK AND DEFENCE IT & COMMS AND FOOD SERVICES

REAL TRANSPORTATION

ESTATE AND STORAGE RESOURCES/

ENERGY

ARTS, ENTERTAINMENT,

RECREATION

LIFE FINANCE

SCIENCES & INSURANCE

AGRICULTURE

LOW-TECH CITY

ELECTRICITY SERVICES

& UTILITIES

MANUFACTURING

AUTOMOTIVE

Source: Colliers/OxfordEconomics/

EDUCATION

National statistics offices

Source: Colliers/OxfordEconomics/National statistics offices

PREVAIL & PROSPER: A view on what’s next for the EMEA investment market 8THE NATIONAL ECONOMIC IMPACT: THE ‘SWOOSH’

National economies across Europe function in many different ways, subject to the business Whilst Q2 2020 ploughed the depths, most markets started to recover in June this year

sectors that drive them and the ways in which national governments have decided to manage the generating an almost immediate large, but ‘partial-V’ or ‘Swoosh’ rebound. But a rebound to

pandemic via a balance of lockdowns and stimulus. This has generated a clear immediate impact positive annual economic and employment growth will not happen until 2021.

on national economies and employment, and we can see those countries more dependent on retail

and hospitality have suffered a deeper initial impact - Italy, Spain, Portugal, France and the UK have Even then, the multi-speed recovery is even more telling when it comes to getting back to

been some of the worst hit during Q2 2020. The DACHS and Nordic regions, the Netherlands and parity, as outlined in Table 2 below. If we look at the period 2021 to end 2023 we can see the

Poland have been the least impacted. overall economic recovery reversion takes from Q4 2020, in resource rich Norway, out to Q2

2022 in Spain and Italy, with other major economies somewhere in between. The impact on

unemployment and household spending is even more marked, with consumption/household

income levels not expected to get back to parity until the end of 2022 for Italy and Spain. The

NOKIA Client Call: Office Market Trends, Sept 2020 more positive DACHS, Nordic & core-CEE markets will see spending revert back to par at almost

Table the same time as the economic recovery.

But 2:the

National

lengtheconomies

of the- timing

GDP of reversion

‘swoosh to economic parity

tail’ varies significantly: economy vs consumption

Country Peak Q4 2020 Q1 2021 Q2 2021 Q3 2021 Q4 2021 Q1 2022 Q2 2022 Q3 2022 Q4 2022

Eco Con Eco Con Eco Con Eco Con Eco Con Eco Con Eco Con Eco Con Eco Con

Norway Q4 2019 X

Poland Q1 2020 x

Sweden Q1 2020 X

Austria Q4 2019 X

Czechia Q4 2019 X

Denmark Q4 2019

Hungary Q4 2019 X

Germany Q3 2019 X

UK Q4 2019 X

Netherlands Q4 2019 X

Finland Q3 2019 X

Ireland Q1 2020

Belgium Q4 2019 X

France Q3 2019 X

Italy Q4 2019 X Source: Colliers/OxfordEconomics

Spain Q3 2019 X *nominal figures

Source: Colliers/OxfordEconomics *nominal figures

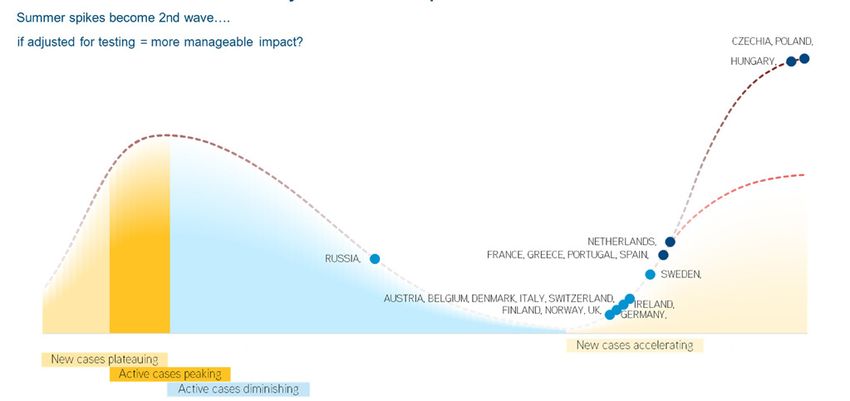

PREVAIL & PROSPER: A view on what’s next for the EMEA investment market 9THE COVID CURVE: MANAGING THE SECOND WAVE

Given the likelihood that a vaccine for COVID-19 will not be available en-masse until H2 2021, relative to the first wave, testing levels are now significantly higher - on average four times

the pressure is on national governments to manage any localised spikes in active cases while higher than during the first wave of infections in March/April and May. By adjusting these

keeping the economy open and ticking over. Thankfully, most major European governments figures relatively to the first wave, we can see that most countries have got a hold on infection

have had time to plan and adjust in preparation for the winter season, and many either have rates. For the likes of the UK, Spain, Netherlands and France that have exercised new

embedded support mechanisms in place, and/or have extended their support into 2021. The lockdown measures, these appear to be pre-emptive strikes in stemming localised contagion.

UK recently announced its shift to a more focused employee support scheme, reflecting more The exceptions to this rule are Poland, Czechia and Hungary - but second-wave infection

targeted policies that have been brought in by many national European governments. Hopefully rates are currently much higher as there were very few initial cases in these countries, given

this will mitigate against a much starker rise in unemployment, so as not to delay any broader the immediate lockdown measures that were put in place in March.

economic/consumption recovery in due course.

This may lead to a marginal second ‘mini-dip’ in economic output in some countries over the

The return of people from summer holidays, schools going back and more people winter months, but with cases laready shown to be easing in some of these countries there

getting back to the office has created an inevitable rise in cases across Europe, but this does are positive signs that a second economic dip will be very short-lived. That said, maintaining

need to be put into context. Firstly, whilst there are many higher numbers of active cases the economic recovery which is at a fragile early stage, will be a critical balancing act. More

stimulus measures may be brought forward, especially when considering that the cost to

the public purse of rising unemployment claimants could be the same as an extended, more

COVID-19 active cases cycle: 28th Sept focused furlough program.

PREVAIL & PROSPER: A view on what’s next for the EMEA investment market 10NATIONAL ECONOMIC ‘MACRO’ OUTLOOK/POSITION

In summary, the country macro outlook is depicted in Table 3 below. The table uses a RAG format The big economies of France and the UK have a positive balance of economic

(Red, Amber, Green) to depict how each nation is positioned across a range of metrics: such as the conditions, but the next six months remain uncertain in terms of the management

forecast date of the economic recovery, how well the covid pandemic is being managed at present, of the pandemic. It will become financially challenging to buoy the economy for any

the capacity to spend on stimulus and long-term demographics to sustain a broader mid-long term extended period of time, especially in France.

recovery. Those with more green (ideally dark green) elements look much more stable than those

with splashes of orange and yellows. The Benelux and core CEE markets of Poland and Czechia look in a good

position, provided they can weather the large second COVID-19 wave.Belgium will

Germany and the Nordic region, especially Norway, Denmark and Sweden look the most be more challenged if it needs to continue funding the economy, given its reliance

appealing countries based on these metrics. Tech-centric Ireland also benefits from many on the EU recovery fund to maintain targeted stimulus measures until end 2020.

positive factors.

At the other end of the spectrum, Spain and Italy have some difficult years ahead,

but this distress will create multiple opportunities for investors engaging in the

NOKIA Client Call: Office Market Trends, Sept 2020

Table 3: National economic ‘macro’ outlook/position riskier end of the spectrum.

National Economic ‘Macro’ Outlook/Position

Country Country COVID COVID-19 Consumer Long-term Government Govnt Debt/GDP Credit Rating

2nd Wave Economic Recovery Path Demographics Stimulus/Debt 2020f% (20 = AAA)

% of 1st Peak Recovery Path Position

Germany Low Q2 2021 Q2 2021 Challenging Positive 69 20

extension

Denmark Low Q3 2021 Q1 2021 Good OK 54 20

Generally Stable,

Sweden Low Q1 2021 Q4 2021 Good Embedded 52 20

Positive Growth

Drivers

Netherlands Moderate Q3 2021 Q3 2021 Moderate Positive 70 20

extension

Ireland Low Q4 2021 Q3 2021 Good Limited 60 16

UK Low Q2 2021 Q4 2021 Good Uncertain 107 16

France Moderate Q4 2021 Q2 2022 Moderate Positive 155 18

extension

Belgium Moderate Q4 2021 Q1 2022 Moderate Partial Extension 138 18

Positive, but Hungary High Q3 2021 Q3 2021 Challenging Limited 77 12

challenges

Czechia High Q3 2021 Q3 2021 Challenging Limited 37 17

Portugal Moderate Q3 2021 Q4 2021 Challenging Limited 156 12

Poland High Q1 2021 Q1 2021 Problematic Limited 56 14

Italy Low Q1 2022 Q3 2022 Problematic Partial Extension 174 11

Challenging

Conditions Spain High Q2 2022 Q4 2022 Problematic Uncertain 139 14

PREVAIL & PROSPER: A view on what’s next for the EMEA investment market 11Capital Markets

The events of the past six months have already significantly changed the global interest rate The appreciation of the Euro has re-balanced the hedging benefits of investing in Euro

dynamic. The onset of COVID-19, coupled with geopolitical friction between US and China vs other denominated assets, notably GBP, which is leading to some interesting pricing

has seen the Euro rise sharply against most major global currencies. The EU27 agreement dynamics across European markets – from both an investment and debt perspective.

to create a 750 billion-euro ($855 billion) ‘COVID-19’ recovery fund, is a sign of improving While global cross-border sales are only marginally down by around 4% (from 22% to

internal cohesion, and combined with the EU’s collectively strong credit rating, this has led 18%), inter-regional cross-border activity has remained steady throughout the Q2 and

to a continued and prolonged euro appreciation and low interest rate regime. The hedging Q3 2020 COVID-dip in activity, with German, French and Swiss investors particularly

benefits of buying Euro denominated assets may have diminished since the end of 2019, but active.

the region is adopting more of a global safe-haven status, and major European currencies

continue to offer a positive gain (for a 5yr cross-currency swap) for

a basket of global currencies.

WHAT’S NEXT: PREVAIL & PROSPER WHAT’S NEXT: PREVAIL & PROSPER

Interest

Interest rates

rates & &appreciating

FX…the FX…theEuro appreciating Euro More continental

European activity, than

activity more continental thanglobal,

global….despite a

but cross-border activity remains active

EUR vs Global Currencies: FX 5yr Hedging Gain/Loss GBP vs Global Currencies: FX 5yr Hedging Gain/Loss

10.0% 8.0%

I n ve s t m e n t vo l u m e s E M E A

By quarter and domicile

8.0%

6.0% 400 40%

36%

350 35%

6.0% 28% 28% 28%

4.0% 300 26% 27% 26% 26% 30%

25%

24% 23%

250 21%

25%

20% 26%

EUR Bn

4.0%

200 23% 23% 20%

22% 22% 22%

2.0% 21%

150 17% 18% 15%

2.0% 16%

100 10%

- 50 9% 9% 5%

- CNY AUD USD CAD HKD KRW TWD JPY SGD MYR ZAR 7%

CNY AUD USD CAD HKD KRW TWD JPY SGD MYR ZAR 0 0%

2010

2012

2013

2014

2015

2016

2017

2018

2019

2011

2008

2009

2020

-2.0%

-2.0%

Q1 Q2 Q3 Q4 % Continental % Global

-4.0% -4.0%

Sep-19 Aug-20 Sep-19 Aug-20

PREVAIL & PROSPER: A view on what’s next for the EMEA investment market 12Concluding Points

Overall, YTD activity has been very robust with H1 2020 volumes across EMEA down by This would leave the market down by around 15% y/y which is a good

only 10% y/y, which compares far more favourably to the 28% declines seen in AsiaPac result considering the upheaval brought about by the pandemic.

and the Americas (although AsiaPac recorded a significant quarterly rise in volumes in

Q2).

As we enter the final quarter of 2020, it looks more and more likely that Q3 will be

the nadir for the EMEA investment market, with bigger deals making a comeback post

holidays in September. Q3 volumes could reach EUR 50 billion, matching those of Q2,

and with more larger deals coming to market, Q4 could reach up to EUR 100 billion.

WHAT’S NEXT: PREVAIL & PROSPER

EMEA: GDP, sentiment and investment outlook

EMEA Investment volumes vs GDP/PMI: history and outlook

Investment Activity Qrtr+ Best-case Mid-case Worst-case

Index GDP Growth

(2007 =100) % Y/Y

180 20.0

Q1 70 70 70

Q2 50 50 50

160 15.0

Q3 *50 *40 *30

140 10.0 Q4 *100 *70 *40

58 2020 *270 (-14%) *22 (-26%) *190 (-40%)

120 57 5.0

53 54 53 54

51 52 51

49

100 46 0.0

48

80 -5.0

“95% of buyers think

31

the market will stabilise

60 -10.0

40 -15.0

20 -20.0

in the next 12 months”

07Q4

08Q2

08Q4

09Q2

09Q4

10Q2

10Q4

11Q2

11Q4

12Q2

12Q4

13Q2

13Q4

14Q2

14Q4

15Q2

15Q4

16Q2

16Q4

17Q2

17Q4

18Q2

18Q4

19Q2

19Q4

20Q2

20Q4

21Q2

21Q4

22Q2

22Q4

GDP GR% Y/Y Volumes (Rolling Annual) PMI Composite

PREVAIL & PROSPER: A view on what’s next for the EMEA investment market 13Contact Details:

Damian Harrington

Head of Research, EMEA

damian.harrington@colliers.com

+44 7867 360489

Richard Divall

Head of Cross Border

Capital Markets I EMEA

richard.divall@colliers.com

+44 20 7487 1605

PREVAIL & PROSPER: A view on what’s next for the EMEA investment market 14You can also read