SOCIETE GENERALE Deep Dive into French Retail Banking and Global Banking and Investor Solutions

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

SOCIETE GENERALE Deep Dive into French Retail Banking and | 07.05.2019 Global Banking and Investor Solutions

AGENDA 8h30-9h00

9h00-9h45

Introduction

Deep dive into

French retail banking

9h45-10h15 Q&A session

10h15-10h30 Coffee break

10h30-11h15 Deep dive into Global Banking and

Investor Solutions

11h15-11h45 Q&A session

OUR MODEL EXPERTISE AND INNOVATION

FOR OUR CLIENTS

FOCUSING ON OUR OUR DNA: EXPERTISE &

CLIENTS INNOVATION

_ Expertise

B2C Advisory to accompany retail clients

COMMITTED TO

POSITIVE in their key projects

TRANSFORMATIONS Structured and Asset Based Finance

Mobility, Africa, Positive Investment solutions

Impact finance _ At the forefront of innovation

(Boursorama, ALD, cross asset

RESPONSIBLE approach, renewable energies

B2B & BANKING financing… )

B2B2C

HIGHLY SYNERGETIC MODEL

ca. 1/3 of Group revenues from synergies

DEEP DIVE 7 MAY 2019 3

OUR MODEL INTEGRATED REGIONS FOR OUR

CLIENTS

AMERICAS

WESTERN CEE RUSSIA

~6%

EUROPE

~11% ~3%

~68%

ASIA - OCEANIA AFRICA

~6% ~6%

%

% of 2018 Group revenues

LEADERSHIP positions in Western Reference bank in HIGH POTENTIAL RETAIL

Presence in SELECTED WHOLESALE

Europe MARKETS

MARKETS for our core clients

A reference RETAIL BANK in Leveraging on GROUP PRESENCE for our corporate

CONNECTING WITH EUROPE

France clients

DEEP DIVE 7 MAY 2019 4

A REFERENCE BANK WITH A PROFITABLE MODEL IN

FRENCH RETAIL BANKING

NETWORKS BOURSORAMA

Digitalise day-to-day banking & leverage our expertise to Undisputed leader in online banking in

CAGR2015-2018

improve our client experience France

# of clients

Targeting >3M clients by 2021 +30%

Enhanced efficiency of the model thanks to the

transformation underway On the road to profitability

2020 RONE: 11.5% - 12.5%

DEEP DIVE 7 MAY 2019 5

GLOBAL BANKING & INVESTOR SOLUTIONS: A RELATIONSHIP,

PIONEER AND RESPONSIBLE BANK

BY FURTHER LEVERAGING ON OUR

PROVIDE THE BEST CLIENT

INNOVATIVE APPROACH

EXPERIENCE WITH THE BEST PRODUCT

Partnerships (ABSA, DBS…)

Open architecture

Developing investment & financing solutions for institutions and

high net worth clients Coverage

B2B market place strategy

Further strengthening leadership in structured and asset finance

for Corporates AND SUPPORTED BY ADJUSTMENT OF

CAPITAL ALLOCATION CONSISTENT WITH

Developing transaction banking OUR STRATEGIC FOCUS

2020 RONE: 11.5% - 12.5%

DEEP DIVE 7 MAY 2019 6

FURTHER STRENGTHENING OUR GROWTH PLATFORM IN

INTERNATIONAL RETAIL BANKING

LEVERAGE ON FAVOURABLE MARKET DYNAMICS

Positive tailwind in Central Europe and Russia | Strong momentum in Consumer Finance | Strong long term outlook in Africa

STRENGTHEN FURTHER IMPROVE

COMMERCIAL PLATFORMS OPERATIONAL EFFICIENCY

State-of-the-art digital improving client experience Refocus central organization of IBFS

in retail banking Switch to agile and integratedorganisation

Best-in-class integrated POS tools & market place Creation of regional hubs and support local IT in

for car dealers & e-commerce Africa and Russia

Further improve strict risk management

Differentiated & integrated offer for Corporates

IBFS 2020 RONE: 17% - 18%

DEEP DIVE 7 MAY 2019 7

FURTHER INVESTING IN OUR HIGH-GROWTH STORY IN

INSURANCE AND FINANCIAL SERVICES TO CORPORATE

EQUIPMENT

INSURANCE ALD

FINANCE

Integrated Bancassurance model to Leader in mobility Leader partner for international

capture synergies Pioneer in partnership model vendors at the heart of the financing of

Partnership to accelerate growth Private lease real economy

#5 Bankinsurance in France # 1 Full service leasing in Europe # 1 in Europe

EUR 2.3bn of synergies revenues in 2018 # 2 Worldwide # 2 Worldwide

(+13% CAGR2016-2018) 1.7 million cars (+10.5% CAGR2013-2018) EUR 28.4bn outstandings*

*Group leasing outstandings as of end of March 2019 IBFS 2020 RONE: 17% - 18%

DEEP DIVE 7 MAY 2019 8

STRONG RISK PROFILE AND CULTURE

WELL MANAGED CONTAINED A STRICT FOCUS ON

CREDIT RISK MARKET RISK OPERATIONAL RISK

HIGH ORIGINATION AND PORTFOLIO QUALITY MARKET RISK CONTINUOUS INVESTMENT IN

~5% of total RWA since 2016 COMPLIANCE

WELL-ESTABLISHED TRACK RECORD OF LOW

COST OF RISK

HIGHLY DISCIPLINED APPROACH TO RISK TRANSVERSAL CULTURE &

ca. 25 bps on average since 2016 APPETITE

CONDUCT PROGRAMME

KEEPING NPL AT A LOW LEVEL VaR*

EXECUTING OUR ROADMAP TO PROFITABILITY

COST OF RISK

GROWING REVENUES COST DISCIPLINE

MONITORING

Fully LEVERAGING OUR Taking advantage of DIGITAL COMFORT in cost of risk trajectory

EMERGING MARKET PRESENCE TRANSFORMATION in all

Working on GROWTH

businesses

Transforming our model, leveraging on digital, in 2020 ROTE

INITIATIVES in more mature

markets

French retail banking

Supporting growth & transformation in

International Retail Banking & Financial Services

9% - 10%

Leveraging on SG markets platform in Global

Banking & Investor Solutions

Revenue objectives taking into

account CURRENT Delivering EUR 1.6bn EFFICIENCY

ENVIRONMENT PLAN

DELIVERING POSITIVE JAWS ACROSS

ALL BUSINESSES BY 2020 AND BEYOND

DEEP DIVE 7 MAY 2019 10DELIVERING OUR ROADMAP TO CAPITAL TARGET

CLOSE

RWA REDUCTION & REFOCUSING ON

MONITORING OF

OPTIMISATION CORE FRANCHISES

ORGANIC GROWTH

+2% CAGR 2018-2020 ca. +25bp from Global Target +80/+90bp by

organic growth of RWA Markets RWA reduction in 2020

2019-2020

ca. +10bp/+20bp optimization

2020 CET 1

in 2019-2020

12%

DISCIPLINED AND SELECTIVE CAPITAL ALLOCATION

RWA CAGR 2018-2020 constant scope and currency which excludes all model reviews (e.g. TRIM) and IFRS 16

ca. +5% ca. +4% ca. +1%/+2% ca. +0.5%/+1% RWA organic

Wealth & Asset Global Markets & Group growth offset

Management Investor Services

by

deleveraging

International Financial Financing & French Retail & optimisation

Retail Banking Services Advisory Banking ca. -2%

ca. -9%

DEEP DIVE 7 MAY 2019 11COMMITTED TO POSITIVE TRANSFORMATIONS

TAKING FULL

ADVANTAGE OF

FULLY DIGITALISING THE BUILDING GROWTH

DIFFERENTIATING

BANK FOR A BETTER MODELS, TAILORED TO

POSITIONING IN HIGH

CLIENT EXPERIENCE THE FUTURE OF BANKING

GROWTH POTENTIAL

REGIONS

LEADER IN RESPONSIBLE AND INNOVATIVE BANKING

DEEP DIVE 7 MAY 2019 12DEEP DIVE INTO FRENCH RETAIL BANKING

AN ATTRACTIVE FRENCH RETAIL MARKET

DYNAMIC FRENCH RETAIL MARKET STRUCTURAL CHANGES UNDERWAY

GDP / capita: USD 42,470

Above European Average

CHANGING CLIENT

NEW ENTRANTS

EXPECTATIONS

2019e GDP growth

+ 1.3%

INCREASING RATE ENVIRONMENT

REGULATION LOW FOR LONG

Household financial savings: EUR 5,117 bn

HIGHLY COMPETITIVE PREDOMINANCE OF

SITUATION IN FRANCE RELATIONSHIP MODEL

French population: CAGR18-24 +0.6%

Source : IMF , Banque de France

DEEP DIVE 7 MAY 2019 14SOCIETE GENERALE: A HIGH POTENTIAL CLIENT BASE

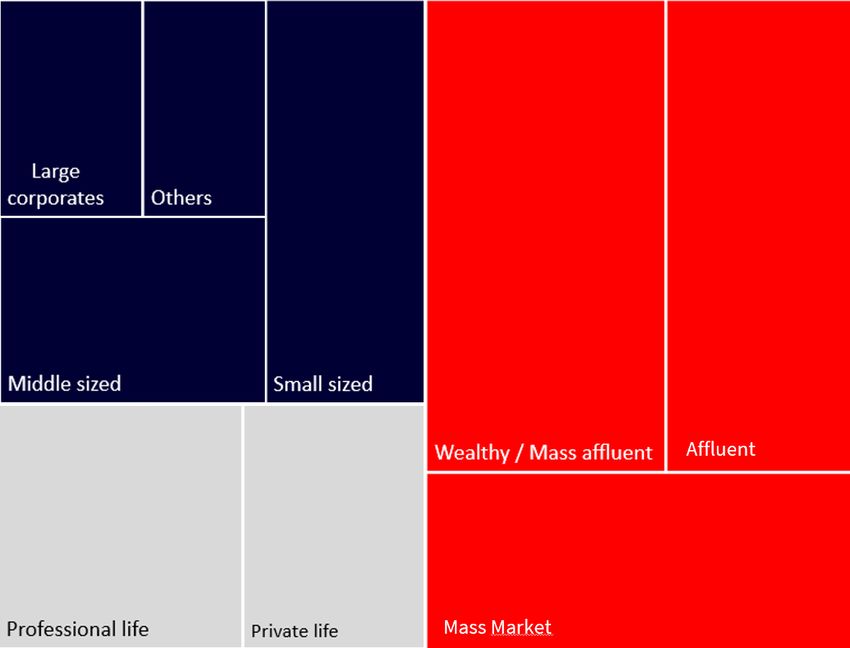

SPLIT OF FRENCH RETAIL BANKING REVENUES

ca. EUR 8 bn

Revenues

Large

corporates Others

>EUR 3 bn

Fees & Commissions

Medium sized Small sized

businesses businesses

Wealthy / Mass

ca. EUR 159 bn

affluent Affluent Wealthy and Mass affluent Assets Under Management(1)

ca. EUR 1.9 bn

Professionals

Insurance Revenues

Professionals Private life Mass market

Based on 2018 data

(1) As of March 2019

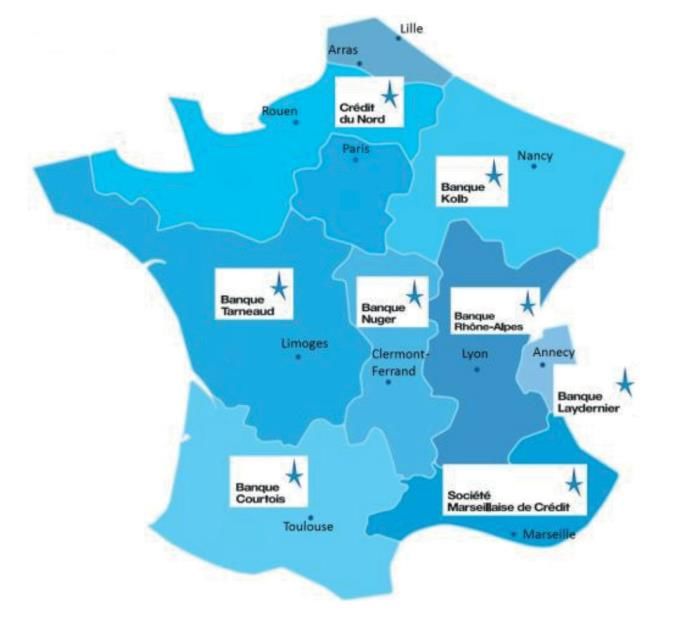

DEEP DIVE 7 MAY 2019 153 COMPLEMENTARY BRANDS ADDRESSING OUR CLIENTS

EXPECTATIONS

3 COMPLEMENTARY THE LEADING FULL

BRANDS WITH UNIVERSAL BANK REGIONAL BANKS

ONLINE BANK

DIFFERENT CLIENT

BASES

Focus on premium clients looking for the highest quality of service Digital & autonomous

clients

Leveraging on a strong Individual clients

Highly recognised

established client base 38 years old on average,

professional franchise

~1% of common clients Focus on wealthy clients mainly city dwellers

High penetration on local

between CDN and SG Strong on nationwide SMEs

SMEs and Entrepreneurs

ca. 15% of Boursorama and large corporates

clients are CDN or SG

clients PHYGITAL MODEL FULLY DIGITAL

2018 REVENUES Individuals Professionals Corporate

DEEP DIVE 7 MAY 2019 16LEVERAGING ON MUTUALISATIONS

BANKING PAYMENT PLATFORM (TRANSACTIS)

AGGREGATION AND ONLINE CAPABILITIES

BEST PRACTICES AND INNOVATIONS SPREAD ACROSS THE BRANDS

IT SYSTEMS AND INFRASTRUCTURE LARGELY SHARED

DATA HUB

60% of Run investments mutualized DIGITAL PROCESS HUB

85% of Infrastructure mutualised

>80% of Digital Hubs mutualised: Exchange Hub, BUSINESS PLATFORM HUB

EXCHANGE HUB

Process Hub, Data Hub and Business Platform Hub

COMPLIANCE, RISK, FINANCE

ORGANISED IN « STREAMS »

DEEP DIVE 7 MAY 2019 17EXPANDING OUR REACH

Clients and services

DEVELOP « NEW TERRITORIES »

CROSS SELL / UP SELL

(B-to-B-to-C / BANK AS A SERVICE)

Target

DEVELOP PARTNERSHIPS (BANK AS A PLATFORM)

KEEP INNOVATING

BIOMETRIC CARD, BIOMETRIC RELATIONSHIP, SYNOE,

CHATBOT, GOOGLE HOME, APPLE / SAMSUNG PAY,

INSTANT PAYMENT, INTERNAL START UP CALL…

OFFER

ACQUIRE NEW CLIENTS

CAPITALISE ON GROUP EXPERTISE

PAYMENT WEALTHY CLIENTS

+6% VS. 2015

SAVINGS ALD, SG Factoring, PROFESSIONALS & CORPORATES

LOANS Insurance, Private

Banking, Investment +5% VS. 2015

PRIVATE BANKING BOURSORAMA

Banking, Transaction

BANK INSURANCE banking… +30% CAGR 2015-2018

REAL ESTATE >3M CLIENTS IN 2021

OTHER : CAR FINANCE, LEASING…

Existing

CLIENT BASE Target

DEEP DIVE 7 MAY 2019 18ADAPTING OUR MODEL

Improve client experience and reduce cost to serve

STANDARD OPERATIONS CUSTOMERS’ KEY PROJECTS

FULLY AUTOMATED ADVISORY

5 LEVERS

FULLY AUTOMATED LEVERAGE ON DATA EXPERTISE & SET UP ADJUSTMENT

APPLI for Selfcare (day-to-day

banking)

AND IA SPECIALISATION Specialised set up for corporates

& professionals

Increase in revenues Training of account

Transfers, online payments, cards,

budget management

Data Marketing for cross-selling and up managers and back-office ~30 business centers /

selling staff

40 features in 2020 (from 17 in 2016) ~150 pro branches & corners

Real time rebound

Fight against fraud in real-time

1 million hours in 2019 in SG Fewer, more adapted branches

Purchase of products and services networks

with electronic signature Automatic decisions on simple

overdraft New dedicated experts for core clients # Branches 2015-2020 ca. –22% in SG

Client Journey digitalisation

Main front-to-back banking processes:

Professionals, Wealthy clients, Liberal

professions network, -9% in CDN network

Account opening, Consumer Credit, Leveraging on call centers

Optimised managerial practices

Mortgage, Corporatecredit… Transforming back-offices

Expert platforms, 6 back offices closed

between 2016 and 2020

DIGITALISED AND DATA CENTRIC IT SYSTEM

DEEP DIVE 7 MAY 2019 19REVENUE GENERATION SUPPORTED BY BUSINESS

INITIATIVES

NET INTEREST MARGIN NORMALISING FOCUS ON FEES GENERATION

DEPOSIT MARGIN DEPOSIT MARGIN FEES DRIVEN BY REVENUE INITIATIVES

EVOLUTION

impacted by negative replacement FRENCH PRIVATE LIFE INSURANCE

BANKING FEES OUTSTANDINGS

rate but progressively normalising 0,0%

Q1 18 Q3 18 Q1 19

CREDIT MARGIN +4%

YoY evolution +14%

Developing with a selective -5,0%

origination strategy

-10,0%

A SUCCESSFUL SELECTIVE ORIGINATION STRATEGY

2016 2018 2016 Mar 19

5%

2018 REVENUES* / LOAN OUTSTANDINGS IN

INSURANCE PENETRATION

FRENCH RETAIL BANKING

4%

P&C Personal Protection

3% 9,4%

17,7% 18,9%

8,2%

2%

1%

0%

2016 2018 2016 2018

Société Générale Bank 1 Bank 2 Bank 3 Bank 4 Bank 5

Source : Companies on published data

* Revenues Ex PEL / CEL as published

DEEP DIVE 7 MAY 2019 20INVESTING IN TRANSFORMATION

OPERATING EXPENSES

TREND

o.w Boursorama

c50% of the investment

2018 2019 2020

TRANSFORMATION COSTS fully supported by the business

Well engaged in TRANSFORMATION OF THE NETWORKS

Delivering COST SAVINGS according to the plan

Cost savings partly offset by INVESTMENTS IN TRANSFORMATION AND GROWTH and REGULATORY & TAX

COSTS

DEEP DIVE 7 MAY 2019 21PROFITABLE FRANCHISES IN FRENCH RETAIL BANKING

2018, in EUR m

FRENCH RETAIL BOURSORAMA

NETWORKS

BANKING FRANCE

REVENUES ex PEL/CEL 7,838 7,673 153

Excluding commercial offers 220

OPERATING EXPENSES -5,629 -5,429 -190

COST OF RISK -489 -474 -16

NET INCOME 1,237 1,271 -35

RONE EXCLUDING INVESTMENT

IN CLIENT ACQUISITION*

RONE 11.0% 11.6% >14%

* Acquisition costs : commercial offers (in revenues) and direct acquisition costs (in costs). On Boursorama France perimeter and with standard method

Boursorama France : excluding Germany and Spain effects

DEEP DIVE 7 MAY 2019 22DELIVERING A PROFITABLE RETAIL BANKING MODEL

PROGRESSIVE REVENUE IMPROVEMENT, OPERATING EXPENSES:

IN THE CURRENT RATE ENVIRONMENT FULLY BENEFITING FROM THE TRANSFORMATION

2019 2020 2019 2020

0% to -1% Increasing revenues +1% to +2% Decreasing cost base

vs. 2018 vs. 2019 vs. 2018 vs. 2019

POSITIVE JAW EFFECT FROM 2020 AND BEYOND

COST OF RISK BETWEEN 35BP AND 40BP IN 2020

2020 RONE 11.5% - 12.5%

DEEP DIVE 7 MAY 2019 23SOCIETE GENERALE NETWORK

A REFERENCE BANK FOR FRENCH CORPORATES

NEEDS

expertise, availability, tailor-made solutions,

beyond the traditional banking needs Trading

Investment

ALD

Banking

LEVERAGING ON SG EXPERTISE

Trade finance, Structured finance, LBO, M&A…

ADAPTED SET UP Specific set up for large

PROXIMITY AND EXPERTISE corporates Private

Factoring

Target 30 business centres by 2020, 9 already rolled out Banking

FOCUS ON GROWTH POTENTIAL Target 30

Start-up offer aiming at supporting 500 companies by

2020 Business centres

Transaction

Sogelease

Important player in « Grand Paris» project financing Banking

Insurance Real Estate

DEEP DIVE 7 MAY 2019 25LEVERAGE ON EXPERTISE FOR

WEALTHY & MASS AFFLUENT CLIENTS

NEEDS

ADVISORY FOR KEY PROJECTS

ca. 489,000 CLIENTS

DIFFERENTIATED PRIVATE BANKING VALUE PROPOSITION FOR

ca. EUR 127 bnAuM | Accretive ROE

FRENCH WEALTHY CLIENTS THROUGH THE CONTINUUM CREDIT

/ ADVISORY, LEVERAGINGON A DEDICATED SETUP

Cumulated net inflows ca. EUR 10bn since 2014

FRENCH WEALTHY CLIENTS

Clients’ AuM > EUR 500k ca. EUR 58 bn AuM

EXTENDING OUR EXPERTISETO FRENCH MASS AFFLUENT

CLIENTS

Reshaping coverage of mass affluent clients leveraging on

FRENCH MASS AFFLUENT CLIENTS private bankingexpertise

Clients’ AuM > EUR 150k ca. EUR 69 bn AuM Dedicated omnichannel setup

Data including 100% of French private banking as of March 2019

Including only Société Générale network

DEEP DIVE 7 MAY 2019 26DIGITALISE DAY-TO-DAY BANKING

NEEDS

SIMPLE AND EFFICIENT DAY-TO-DAY OPERATIONS

DAILY BANKING 100% ONLINE AND STANDARD OFFER 100% DEMATERIALISED BY 2020

MORE AND MORE FUNCTIONNALITIES AVAILABLE x10 DIGITALLY SIGNED CONTRACTS(1)

THROUGH THE APP

. Onboarding MOBILE

. Credit card / account & budget management USE IN 2 ~70%

. Consumerloans YEARS ~70%

. Car & home insurance

. Protection insurance +30% ~30%

~25% ~27%

~13%

. AT THE FOREFRONT OF INNOVATION ON

PAYMENT METHODS 2016 2019 2016 2019 2016 2019

INTERNATIONAL SELFCARE ONLINE REPORTING ON

TRANSFERS (CARD LIMIT) CARD FRAUD

(1) Q4 17 to Q1 19

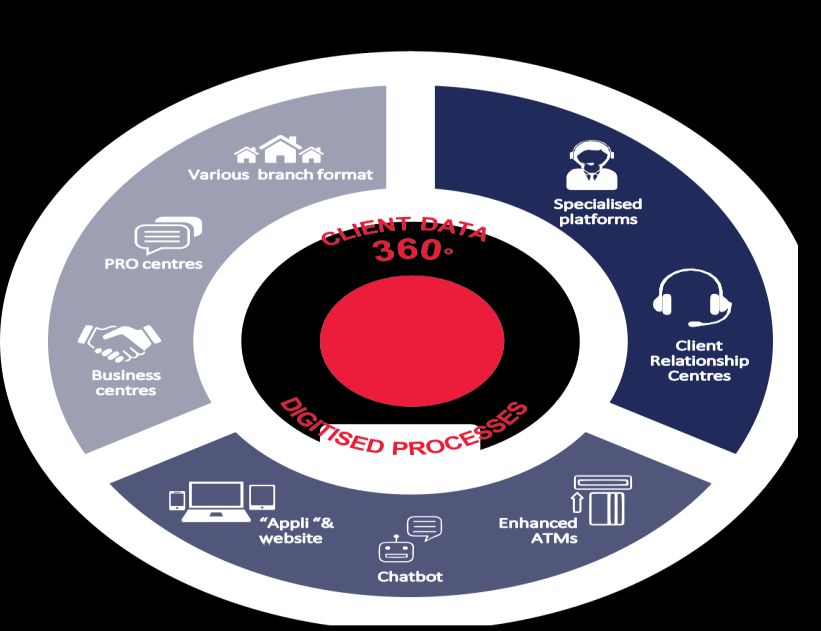

DEEP DIVE 7 MAY 2019 27TOWARDS AN OMNI-CHANNEL BUSINESS MODEL

FEWER BRANCHES, MORE ADAPTED REMOTE PLATFORMS LEVERAGING ON SPECIALISED BACK OFFICES

# OFBRANCHES

ca.2,200 # OF BACK OFFICES

ca. 1,900

ca. 1,700 Multi-site 23

ca. 500 branches 20

ca. 1,200 Fully-operating

4 Customer Relation Centers 17 14

branches

2015 2018 2020 Enlarged scope of banking operations

More proactive calls, follow-up calls…

Client 2013 2017 2018 2020

Relationship

Centres

Various branch formats, Dedicated experts for specific issues

single or multi-site

ca. 13% OF CONSUMER CREDIT PRODUCTIONin

+ PRO centers Targeting 14 back offices specialised by market

Branch network PRO corners Q1 19

covering all client + Individuals vs. Professionals and corporates

Business centers

segments for Corporates Expert platforms for complex home loans,

inheritance…

DESIGN THINKING APPROACH to redefine client Leveraging on artificial intelligence: 300k

experience in branches with a focus on expertise documents directly recognised using A.I,facial

vs. autonomy for day-to-day operations biometry

NO MORE « ONE SIZE FITS ALL » branches

DEDICATED SET UP FOR EXPERTISE

DEEP DIVE 7 MAY 2019 28CREDIT DU NORD

REGIONAL BANKS WITH LOCAL AGILITY, FOCUSED ON

ENTREPRENEURS

HISTORICAL REGIONAL BANKS WITH STRONG CHARACTERISTICS FOCUSED ON CORE CLIENTS

DEDICATED TO LOCAL SUCCESSFUL GROWTH FOR OUR CORE

ENTREPRENEURS ca.18%(2) of penetration rate

CLIENTS (VAR 2014 – 2018)*:

for Corporate clients in France

CLIENT SATISFACTION DRIVEN

EXTENSIVE REGIONALROOTS ca.9.5%(3) of revenue market +10% for Professionals

share for Professional clients in +8% for Corporates

France

ca. 60% +10% for Premium clients

of global revenues generated by 70% of Professionals also have

Professional and Corporate clients their personal accounts

THROUGH AN ADAPTED RELATIONAL MODEL

Client Satisfaction is an essential ADAPTED BRANCHES

component of our DNA (1) FORMAT

FULLY DIGITALISED

#2 #3 #2 CLIENT JOURNEY FOR

for Corporates for Professionals for Retail clients NOMADBANKERS DAILYBANKING

& SPECIFICADVISORS

Agile Organisation with only 3 hierarchical levels between an account

manager and the Head of Credit du Nord MULTI MEDIA

SELF-SERVICE AREA

Source: (1) 2018 CSA Institute / (2) KANTAR survey / (3) Exton Survey EXPERTCENTER

* Variation in number of core clients

DEEP DIVE 7 MAY 2019 30COMMITTED TO A “CLIENT-DRIVEN” TRANSFORMATION

BETTER KNOW OUR CLIENTS BETTER IDENTIFY THEIR NEEDS BETTER SERVE THEM

THANKS TO NEW BEHAVIOURALPROFILING REFLECTEDTHROUGH 28CLEARLY IDENTIFIED THANKS TO AN OPEN ARCHITECTURE MODEL

BASED ON AI & BIG DATA APPROACHES CLIENTNEEDS -THE CDN PLATFORM-

INTERNAL CREDIT DU

NORD PRODUCTS AND

SERVICES

Digital SYNERGIES WITH THE GROUP

Secondary Family with PAYMENT

bank children

INSURANCE CIB CAR LEASE OFFER

WITH ALD

REAL ESTATE PRIVATE

SOLUTION BANKING

Need for strong support

(high cost) Foreign travel

CONSUMER

EXTERNAL FACTORING OFFER FINANCE

PARTNERSHIPS WITH CGA Specific credit

PARTNERSHIPS insurance dedicated to

FINTECH & INSURANCE OXATIS medical professions

Students Personal website creation

protection

PAYZEN & HIPAY

Web payment solution EXPENSYA

Expenses reporting

FIZEN solution

Aggressive Financial Control offer for

Price-sensitive investors very small enterprises

Big spenders

11 PRIORITY SEGMENTS OTHER SEGMENTS

TO BE ENHANCED WITH BEING EXAMINED MORE THAN 100 SIGNED PARTNERSHIPS UP TO NOW

NEW SERVICES

DEEP DIVE 7 MAY 2019 31BOURSORAMA

THE UNDISPUTED FRENCH ONLINE LEADER

THE LEADING ONLINE BANK IN FRANCE ACCELERATING CLIENT ACQUISITION

2018 ACQUISITION ( THOUSANDS OF CLIENTS) # of clients ca. + 30% CAGR2015-2018 , x2.2 in 3 years

ca.3% yearly churn rate

# of clients RECORD CLIENT ACQUISITION in April 19

PEER 1

LEADER

PEER 2 with >53K new clients >2M CLIENTS

PEER 3 1 YEAR EARLIER

# MILLION CLIENTS - EOY

THAN PLANNED

PEER 4

NEOBANK

ONLINEBANKS

PEER 6

PEER 5 PEER 7 PEER 9

PEER 8

PEER 10

# OF CLIENTS END OF

#1 in number of clients : ca. 1.8M clients as of April 19 2018(MILLION CLIENTS)

#1 in new clients acquisition : +465K new clients over the last HIGH POTENTIAL CLIENTS

12 months

38 years old on average Penetration rate(3)

#1 in notoriety : 1st top of mind among online banks(1) 50% have been clients for less than 2 6% of 30-somethings

ca.30% market share in online banking (2) years 8% of Parisians

Large proportion of managers (35%) 14% of French managers

Capturing ca. 8% of banking mobility in France(4)

Mainly city dwellers (70%)

(1) SmartTest D2D April 2019 (2) Based on ACPR September 2018 study (3) Based on INSEE data (4) Arcane research and Internal Data

Sources: press, companies, ACPR, internal data

DEEP DIVE 7 MAY 2019 33A FULL-SERVICE BANKING MODEL

A FULL-SERVICE BANKING MODEL ACTIVE AND EQUIPED CLIENTS

A SIMPLE BUT COMPREHENSIVEOFFER (30 PRODUCTS)

+ 48% YOY(3)

DEPOSITS EUR 5 BN (1) CONSUMER CREDIT EUR 0.9 BN (1) + 47% YOY(3)

+ 38% YOY(4) + 30% YOY (3)

+26% +9% +108% +6%

CAGR 15-18 CAGR 15-18

CAGR 15-18 CAGR 15-18

MARKET(2) MARKET (2) WEB & APPLI CARD TOTAL

CONNECTIONS TRANSACTIONS/ SUBSCRIP # OF CLIENTS

/ MONTH MONTH TIONS / MONTH

SAVINGS EUR 5.1 BN (1) MORTGAGES EUR 6.4 BN (1)

18M(3) 18M(3) 180K(3)

+24% +5% +23% +5% FIRST QUARTERS WITH BOURSORAMA FOR A NEW CLIENT

CAGR 15-18 CAGR 15-18 CAGR 15-18 CAGR 15-18

MARKET (2) OUTSTANDING DEPOSITS TREND(5)

MARKET (2) ca. x4 in 18 months

Consistent trend since

LIFE INSURANCE EUR 5BN (1)

SECURITIES & MUTUAL FUND EUR 4.6 BN (1)

2011

+10% +2% +1%

CAGR 15-18 CAGR 15-18 CAGR 15-18

MARKET (2) NEW CLIENT

AUA / CLIENT CA. EUR 12 000 & LOANS / CLIENT CA. EUR 4 500 (1)

(1) As of December 2018 and including all recent clients at that date (2) Source Banque de France, Boursorama (3) As of March 2019 and including all recent clients, YoY: from March 2018 to March 2019 (4) From December 2017 to December 2018

(5) Average outstandings of a new client (deposits and regulated savings) rebased on 100

DEEP DIVE 7 MAY 2019 34A SUCCESS BASED ON SINGLE MODEL FOCUSED

ON CUSTOMER AUTONOMY

A FULL DIGITAL AND AUTOMATED

MODEL

. A full online offer, with 0 paper

. 850 functionalities & services

. More than 100 types of notifications / alerts

. Continuous automation

EFFICIENT COST BASE CUSTOMER SATISFACTION CUSTOMER AUTONOMY A CUSTOMER SERVICE

ALLOWING AGGRESSIVE #1 in France - NPS > + 40 (1) DESIGNED TO PROCESS

< 1.4 contacts / year

PRICING Recommendation rate(2) per client with client service

EXCEPTIONS

. More than 2300 clients per employee

. +800K clients since end 2016 (+80%) vs. +80 staff >90% fuelling > 50% of new clients . No branches

(+10%) . Chatbot answering mostquestions

. #1 in pricing : Least expensive Bank for the last LEVERAGING ON OPEN BANKING . Human advisors available 6/7 until 10pm

11 years TO PROPOSE THE BEST OFFERS

. Acquisitionpartners

. Best services

. Best products

. Bestcontents

#1 economic and financial website in France with

>32M visits per month (3)

Towards traditional banks STRONG DIFFERENTIATION Towards neobanks through the

through pricing power comprehensive offer

(1) Source Opinionway, (2) Source Boursorama (3) ACPM-OJD March 2019

DEEP DIVE 7 MAY 2019 35A FLEXIBLE MODEL INTRINSICALLY PROFITABLE

BOURSORAMA FRANCE

153 REVENUES

2018 ACTUAL VIEW (EUR M) THEORETICAL VIEW: NO CLIENT EXCLUDING COMMERCIAL OFFERS

ACQUISITION (EUR M)

220 +458 K CLIENTS 220 +13% CAGR

Commercial

offers

>14% RONE 2016 2017 2018

under standard method

153 OPERATING COSTS

EXCLUDING DIRECT ACQUISITION COSTS

+5% CAGR

OPERATING

INCOME NET

-157 -16 INCOME

NETCOST

47

OPERATING NET 47

OF RISK INCOME INCOME 31 2016 2017 2018

-157

Direct OPERATING NETCOST INVESTMENT IN CLIENT ACQUISITION*

REVENUES

acquisition -52 -35 EXPENSES OF RISK

costs

-190 -16 EXCLUDING INVESTMENT IN CLIENT ACQUISITION* INVESTMENT IN CLIENT

REVENUES OPERATING ACQUISITION* BY 8%

EXPENSES FIXEDCOSTS

CLIENT

Modular, Variable and Efficient model -19% BETWEEN 2017 92%

AND 2018 VARIABLECOSTS

* Including commercial offers recognized in revenues and direct acquisition costs recognized in operating expenses

DEEP DIVE 7 MAY 2019 36TARGETING >3M CLIENTS BY 2021

# clients >3M PHASE 1

CLIENTS

Focus on CLIENT ACQUISITION to reach

adequate scale within the French retail market

>2M and to confirm our LEADERSHIP POSITION IN

CLIENTS

ONLINE BANKING

TARGET >3M CLIENTS IN 2021

0.8M

CLIENTS

PHASE 2

IMPROVED PROFITABILITY

2015 2019

Post acquisition phase, mid term RONE

2021

between 20% and 25% (IRBA method)

DEEP DIVE 7 MAY 2019 37DEEP DIVE INTO GLOBAL BANKING AND INVESTOR SOLUTIONS

RECOGNISED LEADERSHIP IN GROWING SEGMENTS

STRUCTURAL MARKET-LEADING

GROWTH DRIVERS EXPERTISE

SAVING FOR RETIREMENT GLOBAL LEADER IN INVESTMENT PRODUCTS

45

40 STRUCTURED PRODUCTS “Societe Generale is, by far, our most efficient

Global retirement savings US$ trillion

35

(OECD)

HOUSE OF THE YEAR counterpart for Structured Products”

30 (RISK MAGAZINE)

Structured Products Specialist at a Tier 1 European Private Bank

25

2012 2014 2016

INFRASTRUCTURE AND ENERGY TRANSITION NEEDS GLOBAL LEADER IN STRUCTURED FINANCE

5

GLOBAL PROJECT

“Societe Generale's speed of execution as well as its

4 Annual Infrastructure Investment, Current

3 Trends US$ Trillion FINANCE ADVISOR OF significant knowledge in the fibre space was

2

(Global Infrastructure Hub) THE YEAR instrumental...”

1 (PFI)

2007 2017 2027 2037 German Telco CFO

NEEDS OF MULTINATIONAL AND EXPORTING CORPORATES REGIONAL LEADER IN TRANSACTION BANKING

1000 “Societe Generale’s expertise, innovation spirit and

Volume of global exports, 1980 = 100 LEADER IN EMEA

500 (IMF)

daily customer service has been essential for the

setup of our global payment & reporting factory

0

1980 1991 2002 2013 2024 across CEEMEA”

Luxury Goods Company

DEEP DIVE 7 MAY 2019 39LEVERAGING ON LONG TERM CLIENT RELATIONSHIPS

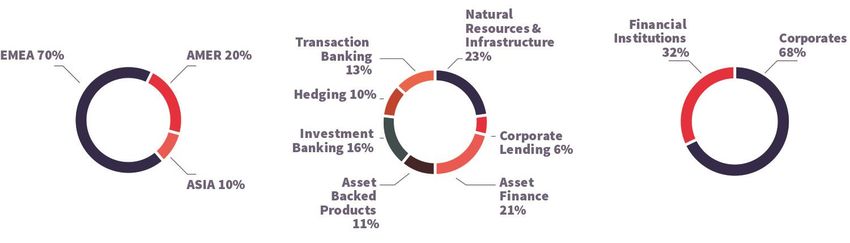

_WHOLESALE CLIENT REVENUES (EUR BN) FOCUS ON CLIENT SELECTIVITY AND CLIENT

48% OF REVENUES WITH CORPORATES PROFITABILITY

52% WITH FINANCIAL INSTITUTIONS

8.5 800 Strategic Clients: 55% of total client

8.1

7.0 revenues

25%

NPS constantly improving with both

28%

corporate clients and financial institutions

More than 70% of Strategic Client revenues

47% is from clients that work with us in 3 or

more regions*

2014 2016 2018

Global Banking & Advisory Transaction banking, ALD,

Equipment finance, Retail, Other

Global Markets and Investor Solutions

*Western Europe, Americas, CEEMEA, Asia-Pacific

DEEP DIVE 7 MAY 2019 40AN INTERCONNECTED MODEL FOR OUR CLIENTS

Americas Asia, Pacific & Other

17% 15%

of 2018 of 2018

revenues EMEA revenues

STRONG POSITIONS IN 68% CONNECTING ASIA TO THE

of 2018

TARGETED SEGMENTS revenues

WORLD

Top foreign bank in Equity Derivatives & leading

position in Structured Finance Financial Institutions: focused on distribution of

investment solutions to private banks.

LEADERSHIP POSITION IN CIB

SUCCESSFUL GROWING

CORPORATE CLIENT BASE Corporates: increased penetration with EMEA

World leader in Equity derivatives

clients

21%

World leader in Structured Finance

EMEA leader in Investment Banking

17%

of Asia Pacific &

of Americas

revenues with

EMEA leader in Transaction Banking other revenues

with European

European French Leader in Private Banking clients

clients

DEEP DIVE 7 MAY 2019 41ALLOCATING CAPITAL TO MOST RELEVANT FRANCHISES

% OF 2018 SYNERGIES 2020 ROADMAP:

2018 RWAs RETURN STRATEGIC PRIORITIES

GLOBAL MARKETS INVESTMENT SOLUTIONS ~15% 10-15% STRENGTHEN LEADERSHIP

AND INVESTOR PROMOTE CROSS-ASSET AND

FINANCING ~10% > 15% INNOVATIVE SOLUTIONS

SERVICES

FLOW* ~25% < 5% RESTRUCTURE

STRUCTURED & ASSET FINANCE,

FINANCING &

INVESTMENT BANKING, ~30% > 15% GROW

TRANSACTION BANKING

ADVISORY

CORPORATE LENDING ~10% < 5% INCREASE SELECTIVITY

WEALTH & ASSET ~10% < 5%

GROW PRIVATE BANKING IN

FRANCE

MANAGEMENT AND ETFs

VERY HIGH GOOD LEVEL FEWER

*Including Securities Services

LEVEL OF OF SYNERGIES SYNERGIES

SYNERGIES

DEEP DIVE 7 MAY 2019 42REFOCUSING ON CORE EXPERTISE IN GLOBAL MARKETS

OUR STRATEGY IN GLOBAL CONCENTRATE RESOURCES EUR 8 BN RWA REDUCTION

MARKETS IS BASED ON ON MOST PROFITABLE 2020 TARGET*

THREE FRANCHISES ACTIVITIES & RESTRUCTURE

FLOW

STRENGTHEN LEADERSHIP IN

CROSS-ASSET INVESTMENT

SOLUTIONS Closure of OTC commodities

INCREASE EXECUTION Closure of Descartesproprietary trading FLOW

CAPABILITIES IN FINANCING 80% PRODUCTS

Increase client selectivity in Prime Services

OPTIMISE FLOW PRODUCTS Downsize Fixed Income and Currencies

LEVERAGING ON GROUP

CORPORATE FRANCHISE

EUR 2.3 BN ACHIEVED IN

Q1 19

* At constant regulatory environment

DEEP DIVE 7 MAY 2019 43ADJUSTING THE COST BASE

STRATEGIC ACTIONS % OF EUR 500M additional savings plan

GLOBAL MARKETS AND INVESTORSERVICES INTERNAL Business closures,

STAFF optimisation of IT budget, 69%

Global Markets: business closures and staff reduction,

automation and offshoring

mainly in FICC

Securities Services: exit from wealth management

GLOBAL MARKETS &

EXTERNAL IT Business closures, fewer

services and clearing in the UK

AND SUPPORT external contractors, 15% 76% INVESTOR SERVICES

FINANCING & ADVISORY STAFF automation

Merger of Global Finance, Coverage and Investment

Banking Consultants, legal fees,

OTHER COSTS marketing, travel, market 16%

ASSET & WEALTH MANAGEMENT data FINANCING &

Restructure private banking headquarters 14% ADVISORY

EUR 250-300M RESTRUCTURING COST IN 2019 ASSET &

GLOBAL REORGANISATION

10% WEALTH MANAGEMENT

OF IT AND OPERATIONS

DEEP DIVE 7 MAY 2019 44REACHING OUR 11.5%-12.5% 2020 RONE TARGET

2020 REVENUES > 2018

2020 COST OF RISK ~20 bps

REVENUES

REDUCING COSTS FROM 2020 RWAs ~ 2018 RWAs

EUR 7.2BN IN 2018 TO EUR including TRIM mostly impacting

6.8BN IN 2020 Global Markets

_RETURN ON NORMATIVE EQUITY* (%)

14.7%

2020 Target

11.2% 11.5% 11.5% - 12.5%

10.8% 10.6%

7.8%

2013 2014 2015 2016 2017 2018 2020

*Adjusted for regulatory fines in 2013 and in 2016 (EURIBOR fine and partial reimbursement)

2013 and 2014 as published in 2014, 2015 and 2016 as published in 2016, 2017 and 2018 as published in 2018

DEEP DIVE 7 MAY 2019 45OUR VISION: A RELATIONSHIP, PIONEER AND

RESPONSIBLE BANK

INTEGRATED GLOBAL EXPERTISE AND INNOVATION POSITIVE

PRESENCE IMPACT

Serving the sophisticated needs of our clients is

Europe is our domestic market part of our DNA Leadership in renewables

US and Asia are dynamic markets where we Creating new investment and structured finance

solutions Investment products and

are growing our presence positive impact finance

Africa is a differentiating factor

PROFITABILITY ABOVE COST A WHOLESALE B2B MARKETPLACE

OF CAPITAL

SG Markets: one interface for clients and teams

Selective capital allocation Successful partnerships

Focused on areas of strength New services and features at a lower cost

Adapted to a new regulatory environment Best in class client experience

(capacity to limit FRTB impact)

DEEP DIVE 7 MAY 2019 4647

GLOBAL MARKETS

GLOBAL MARKETS FOOTPRINT: A POWERFUL CROSS

ASSET DERIVATIVES & SOLUTIONS HOUSE

INVESTMENT SOLUTIONS

(30%)

Structured Products

FICC Equities

FLOW & HEDGING SOLUTIONS

Warrants/Certificate (50%)

Proprietary Indices Liquidity provider on cash assets and

Equities derivatives

3 “PRODUCT” PILLARS Leading execution and clearing broker

in Listed Derivatives

FINANCING SOLUTIONS FICC

(20%) FICC

High velocity collateral trading Equities

Structured Financing

FINANCIAL INSTITUTIONS CORPORATES RETAIL INVESTORS

62% 19% 19%

ALM, hedging and financing solutions for own Holistic risk management & Investment solutions design for third-

account hedging solutions party distribution to retail investors

OUR CLIENTS INVESTMENT

INVESTMENT

11%

14%

FINANCING INVESTMENT

9% 100%

FLOW &

HEDGING 62% FINANCING

24% FLOW &

HEDGING 80%

DEEP DIVE 7 MAY 2019 49INVESTMENT SOLUTIONS: CORE ACTIVITY, LEADING

POSITION

WHATWEDO: WE SOLVE CLIENT COMPLEXITY TO PROVIDE INVESTMENT SOLUTIONS TARGETING ENHANCED RETURN

INVESTMENT PRODUCTS OUR AMBITION:

Structured products: High client demand for Autocall structures, leading innovation on underlying asset

design, diversification towards rates and credit products MAINTAIN OUR LEADERSHIP IN

Warrants and certificates: Leading player in Asia, breakthrough in Germany with the acquisition of EMC INVESTMENT SOLUTIONS

activities

INVESTMENT DERIVATIVES STRATEGIC ACTION:

Societe Generale’s risk exposure generated by Investment Products turned to opportunities for EMC ACQUISITION

sophisticated clients

Key risks offset: >70% of quanto and index correlation risk, 50% of credit recovery sensitivity OUTLOOK

+ High demand for

INVESTMENT STRATEGIES investmentproducts

Quantitative Index Strategies: Systematic strategies for institutional clients with proven low volatility + Push on Quantitative Index Strat

and superior return over the medium term. Generate no market risk and low Balance Sheet consumption

- Risk appetite and market shocks

Custom Fixed Index Annuity Strategies: Designed for US insurers’ fixed index annuity activity

- Market concentration in some product

areas

DEEP DIVE 7 MAY 2019 50FINANCING SOLUTIONS: RECURRENT REVENUES AND

RWA LIGHT

WHATWEDO: WE LEVERAGE OUR CROSS-ASSET CAPABILITIES TO MONETISE OUR ALLOCATED BALANCE SHEET

OUR AMBITION:

FLOW FINANCING

Continued presence to facilitate client needs in OFFER BEST IN CLASS SOLUTIONS

Traditional Repo and Secured loans capabilities on all liquid assets (G10 Govies, Equities, Convertibles, FOR OUR CLIENTS

Credit and EM Credit)

Growth on STRATEGIC ACTION:

Synthetic prime brokerage: Total Return Swaps / Dynamic Portfolio Swaps activity

FURTHER PROMOTE CROSS-

Collateral Exchange: Client need since new Capital Requirement Regulation. Requires cross-asset trading

capabilities ASSET AND INNOVATIVE

Cutting edge IT Investments underway SOLUTIONS

STRUCTURED FINANCING OUTLOOK

+ Additional eligible collateral and

Sophisticated assets & maturities: Large suite of eligible assets, under expansion (Private Equity, Life structures

Settlement, Single HF shares, emerging market assets) + Regulation

Tailor-made solutions to meet new client needs driven by regulation

- Abundant liquidity leading to spread

compression

DEEP DIVE 7 MAY 2019 51FLOW AND HEDGING SOLUTIONS: FOCUSED AMBITION

WHAT WE DO: WE PROVIDE ADDED VALUE CONTENT, DIGITAL SERVICES & QUANTITATIVE TRADING CAPABILITIES

CASH PRODUCTS OUR AMBITION:

Support ECM and DCM franchises A SYNERGETIC BACKBONE

Work on efficiency FOCUSED ON AREAS OF EXPERTISE

CLEARING AND LISTED PRODUCT EXECUTION

STRATEGIC ACTION:

Leading execution and clearing broker in Listed Derivatives

Adjustments to reduce capital consumption while preserving the franchise GROW CONTENT DRIVEN FLOW

DERIVATIVES

OUTLOOK

Equity derivatives: A worldwide franchise based on innovative content and advisory and our ability to

+ Strong appetite for content

execute very large transactions in liquid and illiquid markets

Fixed income: Leveraging our leading corporate franchise on EUR Rates and our Emerging Markets - Extended period of low volatility

presence to act as a premium additional liquidity provider on FX and Rates (CEE, Africa) - Increased competition, in particular on

corporates clients

DEEP DIVE 7 MAY 2019 52FINANCING AND ADVISORY

DIVERSIFIED FINANCING AND ADVISORY SOLUTIONS

SERVING THE NEEDS OF WHOLESALE CLIENTS

REVENUES BY REGION REVENUES BY BUSINESS REVENUES BY CLIENT TYPE

Recognized industry

knowledge thanks to a

long-standing presence

in core markets

First-class expertise in

structured finance

Global approach of the

financing markets

. Worldwide footprint

businesses

. From capital markets to

banking markets

Strong risk awareness

DEEP DIVE 7 MAY 2019 54DELIVERING OUR BUSINESS INITIATIVES TO BRING

MORE VALUE TO OUR CLIENTS

GLOBAL BANKING & ADVISORY REVENUES BUSINESS PUSHES DELIVERING

_NBI in MEUR

2,293

2,264 2,273 NBI CAGR

2,180

1,980 2016-2018

1,744 9%

Asset finance

Asset-backedproducts 19%

Renewable finance x2

2013 2014 2015 2016 2017 2018

SOURCE FY2017 FY2018

Global Securitisation in euros IFR #2 #1

8.7% mkt share 10.1% mkt share

Real Estate Finance in EMEA (volume by MLA) Dealogic #5 #2

GAINING MARKET SHARE 4.8% mkt share 8.2% mkt share

IN MOST MARKETS Global Project Finance by Financial Advisor PFI #11 #1

EMEA Project Finance by MLA PFI #5 #2

All International Euro-denominated bonds IFR #4 #3

5.9% mkt share 6% mkt share

DEEP DIVE 7 MAY 2019 55INCREASED TRANSACTION BANKING MARKET SHARE

IN WESTERN EUROPE

GROUP REVENUES FROM GLOBAL TRANSACTION ADVANTAGES FOR THE GROUP

BANKING*

EUR 2.0bn

EUR 1.9bn + Client proximity helps to cross-sell all

EUR 1.6bn

Group products

+ Stable revenue base

+ Accretive

2013 2016 2018

NBI growth & market share gains in cash management in Western Europe – double digit volume growth

From #10 to #7 ranking in Western Europe for Payment and Cash Management (Source: Euromoney)

Investments ongoing to complete a pan-European product suite in line with highest standards

Leveraging synergies with SG clients worldwide

*Management data

DEEP DIVE 7 MAY 2019 56ACTIVE CAPITAL MANAGEMENT BASED ON AN

EFFICIENT OTD MODEL

A STRONG CAPITAL MARKETS APPROACH AND ACTIVE PORTFOLIO MANAGEMENT TO SUCCEED IN AN

INCREASINGLY DISINTERMEDIATED MARKET

FINANCING BUSINESSES*: CREDIT RISK RWA AND NBI/AVERAGE CREDIT RISK RWA FINANCING BUSINESSES*: NEW PRODUCTION AND PRIMARY DISTRIBUTION (EURm)

Primary New

55,000 5.0% distribution production

50,000 100,000

45,000 4.0%

40,000

35,000 3.0% 75,000

30,000

25,000 2.0% 50,000

2015 2016 2017 2018 20,000

Credit Risk RWA (EURm) NBI/Average Credit Risk RWA 25,000

10,000

- -

FINANCING BUSINESSES*: PORTFOLIO MANAGEMENT ACTIONS (EUR M) 2015 2016 2017 2018

Nominal Primary distribution New production (excl. Short Term financing)

15,000

10,000 FEES: 49% OF 2018 REVENUES

5,000

A FEE-DRIVEN MODEL BASED ON

2015 2016 2017 2018 STRONG ADVISORY CAPABILITIES

Derisking (Insurance, CDS, 1st loss) Secondary sales

*Financing businesses: F&A excluding GTB and JVs on market activities

DEEP DIVE 7 MAY 2019 57STRONG RISK MANAGEMENT TRACK RECORD

AVERAGE NET 1,000

COST OF RISK F&A NCR (EUR m) Expected Loss Q4 2018

800

BELOW Average Net Cost of Risk (2006-2018)

EXPECTED LOSS 600

OF THE 400

PORTFOLIO

200

-

(200)

(400)

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

NET COST 300

OF RISK OF

COMMODITY 200

FINANCE AND 100

LEVERAGE

FINANCE SINCE -

2006 (in MEUR)

(100) Commodities Leverage

(200)

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

DEEP DIVE 7 MAY 2019 58DISCLAIMER

This presentation contains forward-looking statements relating to the targets and strategies of the Societe Generale Group. These forward-

looking statements are based on a series of assumptions, both general and specific, in particular the application of accounting principles and

methods in accordance with IFRS (International Financial Reporting Standards) as adopted in the European Union, as well as the application of

existing prudential regulations. These forward-looking statements have also been developed from scenarios based on a number of economic

assumptionsinthecontextofagivencompetitiveandregulatoryenvironment. The Groupmaybeunableto:- anticipatealltherisks, uncertainties

or other factors likely to affect its business and to appraise their potential consequences; - evaluate the extent to which the occurrence of a risk

or a combination of risks could cause actual results to differ materially from those provided in this document and the related presentation.

Therefore, although Societe Generale believes that these statements are based on reasonable assumptions, these forward-looking statements

are subject to numerous risks and uncertainties, including matters not yet known to it or its management or not currently considered material,

and there can be no assurance that anticipated events will occur or that the objectives set out will actually be achieved. Important factors that

could cause actual results to differ materially from the results anticipated in the forward-looking statements include, among others, overall

trends in general economic activity and in Societe Generale’s markets in particular, regulatory and prudential changes, and the success of Societe

Generale’s strategic, operating and financial initiatives. More detailed information on the potential risks that could affect Societe Generale’s

financial results can be found in the Registration Document filed with the French Autorité des Marchés Financiers. Investors are advised to take

into account factors of uncertainty and risk likely to impact the operations of the Group when considering the information contained in such

forward-looking statements. Other than as required by applicable law, Societe Generale does not undertake any obligation to update or revise

any forward-looking information or statements. Unless otherwise specified, the sources for the business rankings and market positions are

internal. Figures in this presentation are unaudited.

DEEP DIVE 7 MAY 2019 59You can also read