SMART STEEL Investor Presentation - March 2018 - Your Platform for Investor Relations ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

SMART STEEL

Investor Presentation

March 2018

1

Agenda

Company set-up and business model

Market trends

Financials

Company outlook

Takeover V.Orlandi S.p.A.

Appendix

2

Company set-up and business model 3

SAF-HOLLAND: Europe’s largest listed commercial vehicle supplier

Facts & Figures Key components and systems

• One of the leading global producers of key

Kingpins

chassis systems and components for mostly the

trailer but also the truck, bus and vocational Fifth wheels Trailer OE

~62 % of sales

vehicle industry

• 27 subsidiaries featuring 17 manufacturing sites

on six continents

• 3,500 employees

• Network of approx. 10,000 aftermarket spare

parts and service stations around the world

Truck OE

~13 % of sales

Key financials FY 2017

Suspensions

• Sales: € 1,138.9 mn for specialty

• Adjusted EBIT: € 91.2 mn trucks Landing gear

• Adjusted EBIT-margin: 8.0 % Axle and suspension systems

• EPS (undiluted): € 0.95

• Free cash flow: € 29.7 mn (67.7)

Aftermarket

• Equity ratio: 30.2 % Spare parts

~25 % of sales

4

SAF-HOLLAND: Core products

Trailer axles and Truck and bus Fifth wheels, kingpins & landing gear

suspension systems suspensions

SAF-HOLLAND offers a comprehensive product portfolio for one-stop shopping also covering the

aftermarket.

5

Key OE customers producing trucks, trailers & buses

Almost every major truck, trailer & bus OEM is a SAF-HOLLAND customer.

6

End customers using trucks & trailers

SAF-HOLLAND focuses on fleet operators (infrastructure, logistics, specialty, heavy duty, port, etc.).

7

Unique business model featuring clear growth path and strong

competitive position

1. Balanced structural and regional set-up with differing regional market trends and

replacement cycles in trucks versus trailers versus buses

2. Strong position in oligopolistic market driven by product innovation and application

engineering excellence

3. Unique selling model featuring direct access to broad end customer base

4. High share of high-margin Aftermarket business counterbalancing cycles in the

truck & trailer OEM industry

5. Structural technological growth drivers supplement market trends

6. Solid financial profile and cash generation as a foundation for financing further

growth and dividend payouts

8

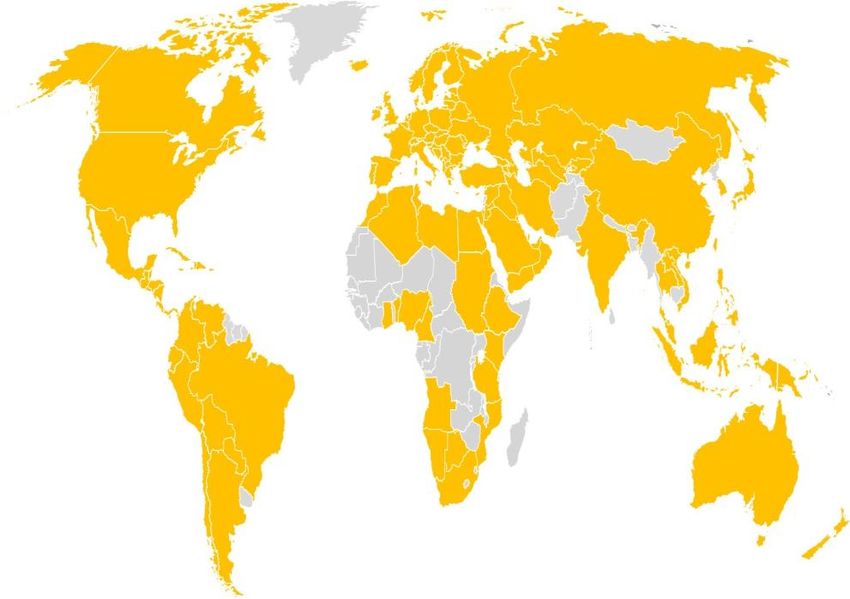

1 A multinational company expanding globally

Sales regions: 90% of sales in Europe and North America

17 production sites

Turkey

Germany Düzce-Istanbul

Canada Bessenbach/Keilberg

Woodstock Bessenbach/Frauengrund

Singen United Arab Emirates

Dubai

China

Xiamen

Bautou

Australia

USA Melton

Cincinnati

Dumas

Warrenton South

Warrenton North

Wylie

Brazil India

Alvorada

South Africa Sriperambadur Taluk

Johannesburg

9

2 Strong market position in oligopolistic markets in Europe and NA

Trailer axles and Truck and bus Fifth wheels, kingpins & Aftermarket service

suspension systems suspensions landing gear points

Among Top 2 Among Top 2 Among Top 2 No. 1

Among market leaders in every product area supplemented by the largest aftermarket network

worldwide.

10 Source: L.E.K. Consulting, April 20153 Unique selling model based upon direct access to broad

end customer base

Customer feedback with regard to technical

and market requirements

Brand stands for Push Pull

superior product

performance and OEM End Customer

aftermarket

excellence

Sales Sales

Sales focusing on fleet managers

> 80% of purchasing decisions taken by the fleets

114 The most comprehensive aftermarket spare parts and service network

worldwide

Approx. 10,000 spare parts dealers and service stations • # 1 Network in Europe and North America: Key asset

in more than 80 countries guarantee spare parts for fleet customers and huge barriers to market entry

availability

• Narrows down volatility from OEM industry cycles and

generates growth based on increasing product

population in the field (“razor and blade” business

model)

• Growth potential from expanding PDC network as well

as GoldLine/Sauer Quality Parts secondary brands

Axle population in EMEAI has more than tripled

4,000,000

3,000,000

2,000,000

North America Europe RoW 1,000,000

60% 36% 4%

0

2003 2005 2007 2009 2011 2013 2015

125a Structural growth drivers in North American markets

From basic axle to fully dressed Trend towards disc brake technology

15 years of experience in disc brake

More and more customers order fully technology integration in Europe

dressed axle and suspension systems Safe, efficient and durable technology

Content per trailer increases significanly

Higher value sold-in & AM potential

135b China legislation opens new doors

GB 1589 “overload ban“ legislation New car carrier law

强制性国家标准《汽车、挂车及汽车列车外廓尺寸、

轴荷及质量限值》(GB 1589-2016) 正式发布实施

As of Jan 2017 From overload to at least 20% undercapacity

No vehicles heavier than 49 tons allowed Regulates overall truck-trailer dimensions in

Light weight products become a noticeable China and eliminates car transporters with

selling proposition double rows until June 2018

Premium segment expanding significantly Maximum length limit for truck and trailer

combinations in phase 2

145b China legislation opens new doors

GB 7258 legislation Hazardous goods transporters

Disc brake technology mandatory for all Many OEM start manufacture of vehicles

wheels of trailers and trucks complying with new standards before formal

as of January 1, 2019 implementation

Air suspension mandatory for trailers and 10 to 15% of trailer market affected

truck rear axles

as of January 1, 2020 Opportunities also in truck and bus air

suspensions

Legislation extends to sidewall and fence

trailers

156 Strong FCF generation allows for consistent dividend payments

Free cash flow pre-dividend and pre-M&A Dividend payments

in € mn in € per share

80 0.60

70 67.7

0.44 0.45*

60

0.40

0.40

50

0.32

40 35.0 0.27

30.8 29.7

30

0.20

20

11.3

10

0 0.00

2013 2014 2015 2016 2017 2013 2014 2015 2016 2017

* To be proposed at Annual General Meeting 2018

Sustained strong cash returns (cash conversion at 81%) providing for 2.5 to 3.2 % dividend yields in recent

years; SAF-HOLLAND dividend policy in general is to distribute 40 to 50 % of available net earnings.

16 Market trends 17

Market trend 2017 and forecast 2018

Global trailer forecast in thousand Change Change Change Share in group

2014 2015 2016 in % yoy 2017 in % yoy 2018 in % yoy sales FY17*

ACT Trailer Shipm.1) 296 334 313 -6.4 316 +1.0 332 +5.1

North America approx. 20 %

FTR Trailer Build2) 292 331 309 -6.6 314 +2.0 319 +1.6

Change Change Change Share in group

2014 2015 2016 in % yoy 2017 in % yoy 2018 in % yoy sales FY17**

Western & 286 -5.0

Trailer Production4) 261 279 301 +7.8 301 0.0 approx. 40 %

Eastern Europe

Global truck forecast in thousand Change Change Change Share in group

2014 2015 2016 in % yoy 2017 in % yoy 2018 in % yoy sales FY17*

North America ACT Truck Build1) 297 323 228 -29.4 256 +12.0 324 +26.6

approx. 11 %

Class 8 FTR Truck Shipment2) 295 320 227 -29.1 250 +9.5 315 +26.0

Change Change Change Share in group

2014 2015 2016 in % yoy 2017 in % yoy 2018 in % yoy sales FY17**

Western, Central

LMC3) 403 427 445 +4.3 470 +5.5 490 +4.3 approx. 4 %

& East. Europe

End of 2016 NA class-8 truck production was projected to decrease by around 8% and trailer to fall by 14%;

Instead both segments successively picked up in 2017. For 2018 NA class-8 truck and trailer production are

projected up, European trailer market to consolidate at a high level

18 Sources: 1) ACT N.A. Commercial Vehicle Outlook, Feb. 2018, published monthly by Americas Commercial Transportation Research Co., LLC, Columbus, Indiana.

2) North American Commercial Truck & Trailer Outlook, Feb. 2018, published monthly by FTR Associates, Nashville, Indiana.

3) LMC/Global Commercial Vehicle Forecast Q3 2017

4) CLEAR Nov. 2017, Western Europe, Eastern Europe (incl. RU, TR)

* Figure relates to OE business of the Americas region; not only North America

** Figure relates to OE business of the EMEA/I region; not only Western & Eastern EuropePersistent increase in global trailer axle market until 2025

Global trailer axle market volume

in thousands

5,000

4,549

4,349 40

4,153 40

4,000 3,782 3,964 39

3,610 38

3,449 37

3,302 36 2,063

3,167 35

34 1,946

1,833

3,000 33 1,725

1,623

1,528

1,361 1,440

1,292

2,000 1,083

1,028 1,056

974 1,001

922 948

875 898

254 272 291

1,000 206 221 237

169 180 193

859 892 927 963 999 1,035 1,072

798 827

0

2017e 2018f 2019f 2020f 2021f 2022f 2023f 2024f 2025f

North America Latin America Europe APAC MEA

Source: Persistence Market Research, Global Trailer Axle Market, December 2017

19 Financials 20

Key financial figures: Group sales, adj. EBIT and -margin (2010 to 2017)

Sales in € mn Adj. EBIT in € mn and adj. EBIT-margin in %

1250 120

1,138.9 14%

1,060.71,042.0

959.7 100 94.0 91.2

1000 90.4 12%

831.3 859.6 857.0

80 8.9 % 8.7 % 10%

70.7

750 8.0%

631.0 58.0 58.2 59.3 8%

60

7.4 %

500 7.0 % 6.8 % 6.9 % 6%

40 37.1

5.9 % 4%

250

20

2%

0 0 0%

2010 2011 2012 2013 2014 2015 2016 2017 2010 2011 2012 2013 2014 2015 2016 2017

Solid sales and adj. EBIT increase in the past 7 years; CAGR sales +9 % and adj. EBIT +14%;

adj. EBIT-margin improvement from 5.9% in 2010 to 8.0% in 2017.

21Group sales and adjusted EBIT by quarter

Sales in € mn Adj. EBIT in € mn

400 35

14%

350 30

26.9 26.3 26.7 12%

300.3

300 287.7 287.3 25.1

271.0 273.7 277.1 274.2 25 24.1

258.8 259.9 255.8 252.6 22.6 22.7

21.6 10%

243.2 20.4 20.9

250 19.8

20 9.4 % 9.3 % 9.6 % 18.5

8.7 % 8.9 % 8%

200 8.3 % 8.4 % 8.7 %

8.4 % 7.8 %

7.5 %

15

6.7% 6%

150

10 4%

100

50 5 2%

0 0 0%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2015 2016 2017 2015 2016 2017

In the fourth quarter of 2017, organic sales momentum versus the previous quarter (Q3 2017: 9.6%)

accelerated again with reported sales increasing 8.6% to EUR 274.2 million (py: EUR 252.6 million). Adj. EBIT

margin in Q4 2017 was 6.7% (py: 7.8%).

22US plant consolidation from 7 to 5 sites – where do we stand?

Maine

Washington

North Vermont

Montana Dakota

New

Hampshire

New

Oregon Minnesota Wisconsin York Massachusetts

Michigan

South ConnecticutRhode

Dakota

Idaho

Muskegon Island

Wyoming

Holland Pennsylvania New

Jersey

Iowa

Nebraska

Illinois Cincinnati Maryland Delaware

Nevada Ohio West

Indiana

Missouri Virginia

Utah Virginia

California

Colorado Warrenton North Kentucky

Warrenton

Kansas

South North

Carolina

Tennessee

Arkansas South

Oklahoma Carolina

New

Arizona Mexico

Georgia

Alabama

Wylie Dumas Mississippi

Texas

Louisiana

Florida

SAF-HOLLAND production locations

Transition of production to plant

FY 2017 € 10.9 mn restructuring charges (adjusted for) plus additional € 10.3 mn in operating cost caused by

significantly higher personnel and employee involvement cost, expedited freight and production inefficiencies;

Expected annual savings after completion approx. USD 5.0 mn.

23Share of group sales by channel and region in 2017

8.6 %

(py: 6.8%)

24.4 %

53.7%

(py: 25.9 %)

(py: 54.6%)

37.7%

(py: 38.6%)

75.6 %

(py: 74.1 %)

OE business Aftermarket business EMEA/I Americas APAC/China

Share of OEM business increases due to well-above trend line sales growth; Well-balanced geographic

exposure in the EMEA/I and Americas regions with clear growth strategy until 2020 in APAC/China and

EMEA. In 2017 highest growth rate percentage-wise in APAC/China.

24Key financial figures: Net income and EPS undiluted (2010 to 2017)

Net income in € mn EPS in €

60 1.40

51.7

1.20 1.14

50 43.5 0.98

41.0 0.95

1.00

40

32.7 0.80 0.73 0.72

28.4* 0.68*

30 26.6

24.4 0.60 0.54

20 0.40

10 0.20

0.18

7.4 0.00

0

0 2010 2011 2012 2013 2014 2015 2016 2017

2010 2011 2012 2013 2014 2015 2016 2017 -0.20

-10

-0.40

-8.3 -0.40

-20 -0.60

-0.60

Solid net income development from 2010 to 2017; EPS influenced by higher number of shares.

25 * adjusted for one-time effects from the early redemption of bank loans of € 9.3 mn and swaps of € 3.1 mn as well as unrealized foreign exchange

losses on foreign currency loans in an amount of € 1.2 mn.Inventories and Net Working Capital

Inventories in € mn and days of inventories

180 75

160 145.7 138.9 139.3 Disproportionately low increase in inventories of € 4.3

133.7 65

140 127.2 123.7 124.6 129.4 mn yoy versus sales growth

120

55 The Group was able to reduce inventories by € 5.6 mn

100 57

80

55 54 54 53 in the fourth quarter of 2017 in comparison to levels as

51 51 45

60 of Sept. 30, 2017 (€ 139.3 mn)

40 42 35 Days of inventories at 53 (py: 57) days at the end of

20 Q4 2017

0 25

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2016 2017

Net working capital in € mn and as % of sales

180 20%

160 144.8 142.8 142.7

140 133.3

118.4

125.2

110.3

120.6 15% Net working capital due to strong organic sales

120

100

growth increased by € 10.3 mn to € 120.6 mn yoy

12.2 % 12.2 % 12.6 % 11.9 % 12.9 % 10%

80 11.4 % 10.9 % 11.0% The Group was able to reduce net working capital in

60 the Q4 2017 alone by € 22.1 mn.

40 5%

20

0 0%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2016 2017

26Free cash flow by quarter

in € mn

40

29.3

30 26.8

19.4

20

10.9

10 13.0 7.5

6.1

0

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

-10

2016 -15.6 2017

-20

Free cash flow (net cash flow from operating activities less investments in PPE and intangible assets, pre-

dividend) sequentially improved in Q4 2017 to € 26.8 mn from € 10.9 mn in Q3 2017.

27Net debt reduced to € 105.5 mn - Equity ratio reflecting strong cash

position

Net debt Equity ratio

in € mn

Σ 97.1* Σ 105.5*

500

400

300 30.1 % 30.2 %

200 441.7 442.6

100

0

-100

-200 -344.6 -337.1

-300

-400

Dec 31, 2016 Dec 31, 2017 Dec 31, 2016 Dec31, 2017

Cash Debt

* Net debt incl. cash and cash equivalents and other short-term investments sequentially reduced to € 105.5

mn (Q3 2017: € 128.2 mn); The equity ratio as of Dec. 31, 2017 was 30.2% reflecting M&A related high cash

and cash equivalents (€ 337.1 mn); Figures were impacted by € 20.0 mn dividend payment and neg.

currency effects.

28 Company outlook 29

Outlook: Financial targets 2018 and mid-term planning 2020

FY 2018* Strategy 2020

Organic increase of 4 to 5% Organic: € 1,250 mn

+ potential M&A

Sales

+ M&A: Coops, JVs, acquisitions

Assuming stable FX rates and

unchanged scope of consolidation

Total: € 1,500 mn

Adj. EBIT margin 8 to 8.5% ≥ 8%

NWC ratio 12% 12%

€ 38 to 40 mn

€ 26 mn to € 28 mn p.a.

CAPEX incl. high single-digit Euro mn

amount related to new China plant

30 * Projections assume that there is no significant deterioration of the political, economic or industry-specific environment; organic projections do not

include potential sales and earnings contributions from acquisitions or JVsSMART STEEL provides for add-on business

opportunities in a digitized transport world

1 2 3 4 5

Upgrade to Digitize New business

Integrate &

Mechanics Electro- Information & models & Digital

Connect

mechanics Data solutions

Predictive Maintenance

RECOLUBE SAFH Connect App Big Data Analytics

SAF-HOLLAND combines mechanics with sensors and electronics.

The Company‘s integration and data interpretation know-how enables smart/autonomous drive systems.

31Green SAF-HOLLAND – We acknowledge sustainability!

SAF-HOLLAND acting as a sustainability Our own sustainable business model in

enabler transport and logistics

SAF-HOLLAND’s innovative sustainable Think Ahead program: Environmentally

solutions enable customers to reach their proactive strategies and community support

sustainability targets

SAF-HOLLAND engineering is a trendsetter in Appropriate handling of resources

light-weight products

Group-wide CSR reporting process being

established, complying with GRI Standards

Legislation and tightened safety, weight and

emissions resductions standards are driving

Winner of the 2017 European Transport Award

for Sustainability, category “ Best Overall Entre-

China: “Overload ban” preneurial Concept"

Hazardous good transporters: Disc brake and

air suspension required by new legislation

32 Takeover V.Orlandi S.p.A. 33

Takeover of V.Orlandi S.p.A.: The specialty fifth wheel and coupling

specialist

Headquarter in Flero (Brescia), Italy

Supplier of couplings for trucks and

specialty fifth wheels

Specialty business with couplings and

drawbar eyes for trailers and specialized

commercial vehicles systems

Serves the industrial, agricultural, forestry

and mining segments

Two production sites in Northern Italy,

currently employing around 60 people

Well-established international sales

network for OEM and Aftermarket

SAF-HOLLAND is strengthening its position as the number 2 in fifth-wheels and couplings in the European

market by taking over the number 3 player.

34V.Orlandi S.p.A.: Fully complementary product range

AGRICULTURAL AUTOMOTIVE

DUAL INDUSTRY USE MINING

SAF-HOLLAND is complementing and strengthening its position in coupling systems and specialty fifth

wheels for trucks, trailers, semi-trailers and agricultural vehicles. Significant cross-selling potential of

Orlandi products to be realized within the worldwide set-up of the SAF-HOLLAND Group network.

35V. Orlandi S.p.A.: Sales turnover by region and business unit in 2017

19%

28%

41%

81%

31%

Overseas Europe Italy Automotive Agricultural

Almost two thirds from overseas sales originate from the APAC region besides Russia, South America, the

Middle East and Africa.

36Impressions: A very specialized product range 37

Terms and key financials

SAF-HOLLAND acquires 70% stake in V.Orlandi S.p.A.

Call option for SAF-HOLLAND for the remainder

Expected full year sales: approx. € 22 million

Expected annual growth rate: 3 to 5%

Margin accretive: Adj. EBIT margin in the mid teens

Pro rata tempore inclusion in the SAF-HOLLAND Group scope of consolidation

Closing of transaction expected no later than in Q2 2018

After the takeover, V.Orlandi S.p.A. will continue to operate under its strong, well-established brand. As part

of the SAF-HOLLAND Group, V.Orlandi S.p.A. will benefit from additional growth prospects and attractive

cross-selling opportunities worldwide.

38 Takeover York Transport Equipment

(Asia) Pte. Ltd.

39York Transport Equipment: Company Overview and Highlights

York is engaged in manufacturing and

distribution of trailer axles, trailer

suspensions and trailer components

York employs 220 staff and 90 contract

workers

Manufacturing facilities in India and China;

assembly lines in Singapore and Australia

Market leader in Asia, Africa and Australia

Strong service and spare parts network in

India

Research and development centers in

India, Australia and Singapore

SAF-HOLLAND will become one of the market leaders in trailer axle and suspension systems in India, one of

the fastest growing transportation markets in the world with an excellent set-up in the APAC/China region.

40York Transport Equipment: Core products and market shares

Axles Mechanical Air Fifth Landing

suspensions suspensions wheels gears

Acquisition of York rapidly expands SAF-HOLLAND’s position in the fast-growing Indian and APAC/China

transportation markets.

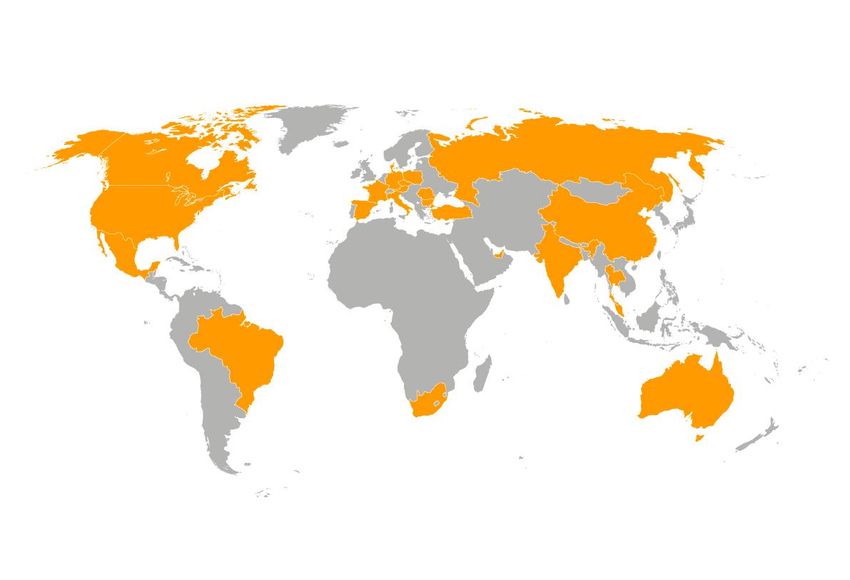

41York Transport Equipment: Geographic footprint

Next to India, York also has

significant operations in

other fast-growing

Southeast Asian markets,

such as Thailand, Indonesia

and Vietnam besides

Australia.

Turkey

York Group has a strong

China service and spare parts

network in India with more

Thailand than two hundred service

Middle India

East Singapore points.

This network will effectively

strengthen the aftermarket

Manufacturing Indonesia

business of the SAF-

HOLLAND Group in the

Warehousing region.

Sales Representative

South Africa

Australia

York has a wide regional sales and a strong service and spare parts network which perfectly fits into SAF-

HOLLAND’s network. York will also strengthen the position of SAF-HOLLAND in the Middle East and Africa.

42Estimated significant growth in APAC fits with Strategy 2020

Global Trailer Market Attractiveness Strategy 2020

The world‘s growing population and increase

in purchasing power are the key drivers for the

expected increase in consumption.

Market growth is mainly seen in the emerging

economies, particularly in the Asia Pacific,

Middle Eastern and Africa markets.

The objective of the Strategy 2020 is to

expand SAF-HOLLAND‘s presence in the

emerging markets by entering new regional

markets outside of the core markets.

A further objective is the expansion of the

aftermarket business.

43 Appendix 44

Strong financial profile supporting further growth & dividend payments

Strong financial profile*

Corporate Bond Revolving Credit Convertible Bond Promissory note Non-current loan

€ 75 mn lines € 100.2 mn (SSD) € 50 mn

due 04/2018 € 155.5 mn due 09/2020 € 200 mn due 06/2026

due 10/2021 with € 140 mn due in 11/2020

option € 17 mn due in 11/2022

of renewal until € 43 mn due in 11/2025

10/2022

Optimized and diversified financing structure

Access to institutional and private investors with

reduced dependency from banks

More flexibility with increased financial headroom and

optimized financing costs

Financing of “Strategy 2020” targets secured

Dividend policy

Dividend payment of € 0.44 per share (py: € 0.40) for FY Distribution of generally 40 to 50 % of available net

2016; € 20.0 mn (py: € 18.1 mn) distribution in total earnings on a sustainable base if reported equity ratio

representing a 46 % (py: 39 %) share of FY 2016 available reaches around 40 %

net earnings

45 * as of September 30, 2017Among TOP 3 market position in every product area

2014

SAF-HOLLAND Market shares

Market Position Europe North America

Europe North America SAF-HOLLAND Σ Top 3 SAF-HOLLAND Σ Top 3

Axles #1 #3 39 % 89 % 8% 90 %

Trailer Systems

Suspensions #1 #2 36 % 90 % 15 % 84 %

Kingpins #2 #1 12 % 89 %1) 77 % 95 %1)

Landing gears #3 #1 6% 89 % 39 % 78 %1)

Powered Vehicle

Fifth wheel #2 #1 23 %2) 96 % 51 % 100 %

Systems

Truck suspensions n/a #2 0% 90 %3) 6 %4) 38 %

market

After-

Service points #1 #1 Approx. 9,000 Aftermarket spare parts and service stations

1) Top 2 players 2) Based on top 7 European truck OEMs (Mercedes Benz, VOLVO, MAN, DAF, SCANIA, Renault, IVECO) 3) Predominantly captive market 4) Commercial market share excluding sales to U.S. Defence Dept.

We are among the TOP 2 players in almost every product area we are in; significant expansion

potential in the Americas with trailer axles and suspensions as well as vocational truck suspensions.

46 Source: L.E.K. Consulting, April 2015Disclaimer

Not for general release, publication or distribution in the United States, Australia, Canada or Japan.

By attending this presentation you agree to be bound by the following limitations:

This presentation has been prepared by SAF-HOLLAND S.A. (“SAF-HOLLAND”) and comprises written materials concerning SAF-HOLLAND. It is furnished to you solely

for your information and may not be reproduced or redistributed, in whole or in part, to any other person. It contains summary information only and does not purport to be

comprehensive and is not intended to be (and should not be used as) the sole basis of any analysis or other evaluation. No representation or warranty, express or implied,

is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of any information, including projections, estimates, targets and

opinions, contained herein, and no liability whatsoever is accepted as to any errors, omissions or misstatements contained herein, and, accordingly, neither SAF-HOLLAND

nor any of its directors, officers, employees or advisors nor any other person shall have any responsibility or liability whatsoever (for negligence or otherwise) arising,

directly or indirectly, from the use of this presentation, or its contents or otherwise in connection with this presentation.

This presentation contains certain statements related to our future business and financial performance and future events or developments involving SAF-HOLLAND and/or

the industry in which SAF-HOLLAND operates that may constitute forward-looking statements. These statements may be identified by words such as “believes,” “expects,”

“predicts,” “intends,” “projects,” “plans,” “estimates,” “aims,” “foresees,” “anticipates,” “targets,” and similar expressions. Forward-looking statements are not historical facts,

but solely opinions, views and forecasts which are based on current expectations and certain assumptions of SAF-HOLLAND’s management or cited from third party

sources which are uncertain and subject to risks. Actual events may differ significantly from the anticipated developments due to a number of factors, including without

limitation, changes in general economic conditions, changes affecting the fair values of the assets held by SAF-HOLLAND and its subsidiaries, changes affecting interest

rate levels, changes in competition levels, changes in laws and regulations, environmental damages, the potential impact of legal proceedings and actions and the Group’s

ability to achieve operational synergies from past or future acquisitions. Should any of these risks or uncertainties materialize, or should underlying expectations not occur

or assumptions prove to be incorrect, actual results, performance or achievements of SAF-HOLLAND may (negatively or positively) vary materially from those described,

explicitly or implicitly, in the relevant forward-looking statement.

The information contained in this presentation, including any forward-looking statements expressed herein, speaks only as of the date hereof and reflects current legislation

and the business and financial affairs of the SAF-HOLLAND which are subject to change and audit. Neither the delivery of this presentation nor any further discussions of

SAF-HOLLAND with any of the recipients thereof shall, under any circumstances, create any implication that there has been no change in the affairs of SAF-HOLLAND

since such date. Consequently, SAF-HOLLAND neither accepts any responsibility for the future accuracy of the information contained in this presentation, including any

forward-looking statements expressed herein, nor assumes any obligation, to update or revise this information to reflect subsequent events or developments which differ

from those anticipated.

This presentation is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident or located in any state, country or other

jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or which would require any registration or licensing within such

jurisdiction. This presentation is for information purposes only and does neither constitute an offer to sell securities, nor any recommendation of, or solicitation of an offer to

buy, any securities of SAF-HOLLAND in the United States, Germany or any other jurisdiction. In the United States, any securities may not be offered or sold absent

registration or an exemption from registration under the U.S. Securities Act of 1933.

47Investor Relations

SAF-HOLLAND GmbH

Stephan Haas

Hauptstraße 26

63856 Bessenbach

Phone +49 6095 301-617

Telefax +49 6095 301-102

Mobile +49 170 306 64 97

Stephan.Haas@safholland.de

www.safholland.com

48You can also read