American Samoa Economic Forecast 2019

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

American Samoa

Economic Forecast

2019

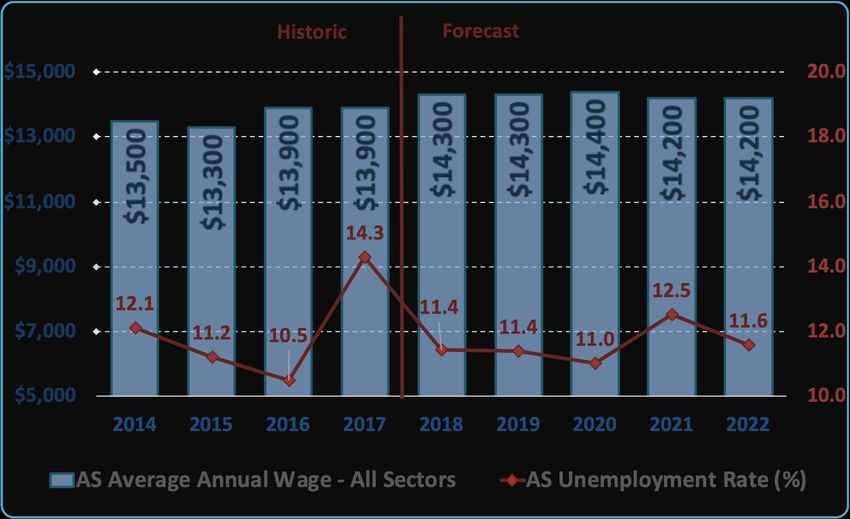

Average Annual Wage vs. Unemployment Rate

Features

Baseline and Alternative Forecasts for 2018 – 2022

FRBSF Article: Nonmanufacturing as an Engine of Growth by Huiyu Li

Lolo Matalasi Moliga, Governor Keniseli Lafaele, Director

American Samoa Government American Samoa Department of CommerceThis page left blank intentionally

American Samoa

Economic

Forecast

2018-2022

Territory of American Samoa

LOLO MATALASI MOLIGA, Governor

LEMANU PALEPOI SIALEGA MAUGA, Lieutenant Governor

KENISELI LAFAELE, Director, Department of Commerce

VAI FILIGA, Chief of Statistics, Department of Commerce

NATHANIEL CLAYVILLE, Senior Economist, Department of CommerceTable of Contents Introduction ........................................................................................................................... 1 Executive Summary ................................................................................................................ 3 Pacific Region Economic Forecast Analysis .............................................................................. 6 Pacific Region Economic Summary .......................................................................................................... 6 Pacific Region Economic Forecast Tables............................................................................................... 11 United States of America Economic Forecast Analysis ........................................................... 13 US Economic Summary .......................................................................................................................... 13 US Economic Forecast Tables................................................................................................................. 19 American Samoa Economic Forecast Analysis ....................................................................... 21 American Samoa Economic Summary ................................................................................................... 21 American Samoa Economic Forecast Tables .......................................................................................... 28 Alternative Forecasts ............................................................................................................ 32 Low Economic Growth and High Oil Price Scenario ............................................................................... 32 High Economic Growth and Low Oil Price Scenario ............................................................................... 37 Feature Article: Nonmanufacturing as an Engine of Growth by Huiyu Li ................................ 42 ASEM: The American Samoa Economic Model ...................................................................... 48

Figures and Tables Figures: Figure I: Samoa Real GDP and Inflation Forecast ........................................................................... 7 Figure II: Tonga Real GDP and Inflation Forecast ........................................................................... 8 Figure III: Fiji Real GDP and Inflation Forecast................................................................................ 9 Figure IV: New Zealand Real GDP and Inflation Forecast ............................................................... 9 Figure V: Australia Real GDP and Inflation Forecast ..................................................................... 10 Figure VI: US Employment and Unemployment ........................................................................... 14 Figure VII: US Inflation .................................................................................................................. 15 Figure VIII: US Real Consumer Spending ...................................................................................... 16 Figure IX: US Real Government Spending..................................................................................... 17 Figure XI: Real US Imports ............................................................................................................ 18 Figure X: Real US Exports.............................................................................................................. 18 Figure XII: American Samoa Employment and Unemployment ................................................... 22 Figure XIII: American Samoa Wages and Income ......................................................................... 23 Figure XIV: American Samoa Inflation .......................................................................................... 24 Figure XV: American Samoa Consumer Spending ........................................................................ 25 Figure XVI: American Samoa Business Investment ...................................................................... 26 Figure XVII: American Samoa Government Spending .................................................................. 26 Figure XVIII: American Samoa Gross Domestic Product ............................................................... 27 Tables: Table 1: American Samoa Economic Forecast Executive Summary Details ................................... 4 Table 2: US Economic Forecast Executive Summary Details .......................................................... 5 Table 3: Pacific Region Countries Real GDP Forecast ................................................................... 11 Table 4: Pacific Region Countries Inflation Forecast .................................................................... 12 Table 5: US Economic Forecast Details ......................................................................................... 19

Table 6: Other Economic Indicators Forecast Details ................................................................... 20 Table 7: American Samoa Economic Forecast Summary Details .................................................. 28 Table 8: American Samoa Nominal GDP Forecast Details ............................................................ 29 Table 9: American Samoa Real GDP Forecast Details ................................................................... 30 Table 10: American Samoa Employment Characteristics Forecast Details .................................. 31 Table 11: American Samoa Low Economic Growth Scenario Details ........................................... 33 Table 12: US Low Economic Growth Scenario Details .................................................................. 34 Table 13: American Samoa Low Economic Growth Scenario versus Baseline Scenario Details ... 35 Table 14: US Low Economic Growth Scenario versus Baseline Scenario Details .......................... 36 Table 15: American Samoa High Economic Growth Scenario Details .......................................... 38 Table 16: US High Economic Growth Scenario Details ................................................................. 39 Table 17: American Samoa High Economic Growth Scenario versus Baseline Scenario Details .. 40 Table 18: US High Economic Growth Scenario versus Baseline Scenario Details ......................... 41 ii

List of Acronyms and Abbreviations AEO – Annual Energy Outlook ASCA – American Samoa Code Annotated ASEF – American Samoa Economic Forecast ASEM – American Samoa Economic Model BEA – US Bureau of Economic Analysis CBO – US Congressional Budget Office CPI – Consumer Price Index EIA – Energy Information Administration FEMA – US Federal Emergency Management Agency GDP – Nominal Gross Domestic Product (Current Values) IMF – International Monetary Fund NIPA - National Income and Product Accounts OLS – Ordinary Least Squares Statistical Method OMB – US White House Office of Management and Budget PICs – Pacific Island Countries PPI – Producer Price Index Real GDP – Real Gross Domestic Product (Inflation-adjusted Values) STP – Samoa Tuna Processors US – United States iii

Introduction The national forecast presented in this publication is from the Annual Energy Outlook 2019 reference case forecast of the US economy and of select energy prices, produced by the US Energy Information Administration (EIA)1. Forecast Projections in the 2019 American Samoa Economic Forecast (ASEF) are not predictions of future events, but rather modeled estimates of what may occur, based on historic observations and certain assumptions. ASEF is developed using the American Samoa Economic Model (ASEM), a series of simultaneous multilinear regression equations that represent the statistical relationships between territorial, regional, national, and international economic variables. Whenever feasible, these statistical constructs were based upon the latest National Income and Product Accounts (NIPA) data and approved methodology, as outlined in the Bureau of Economic Analysis (BEA) 2017 NIPA Handbook2 and as prescribed in the American Samoa Statistical Act of 2003 (A.S.C.A. § 13.2104). For more information about ASEM, see the section of this publication titled “ASEM: The American Samoa Economic Model”. Cover The cover graph shows the average annual wage in American Samoa and the calculated unemployment rate for the territory. These two variables are implicitly related and tend to drive consumption, which accounts for approximately 70% of Nominal Gross Domestic Product in the territory. When the unemployment rate is low, employers have to increase wages to compete for qualified workers. If wages rise too quickly, some employers may invest more in equipment and software, shifting some costs from labor to capital, leading to higher unemployment. An elevated unemployment rate gives employees and job-seekers less power to bargain and can lead to lower wages. The average annual wage in American Samoa is expected to increase over the next few years, largely due to higher government spending on disaster relief and the 2020 decennial census. Once the census is complete, there will be a reduction in Census Bureau employment, which is predicted to result in higher unemployment and lower wages in the two years that follow. 1 United States, Department of Energy, Energy Information Administration. “Annual Energy Outlook 2019”. www.eia.gov/outlooks/aeo/. 2 United States, Bureau of Economic Analysis. “Concepts and Methods of the U.S. National Income and Product Accounts.”, Nov. 2017. www.bea.gov/sites/default/files/methodologies/nipa-handbook-all-chapters.pdf. 1

Feature

The feature article chosen for this publication comes from Huiyu Li, an economist in the

Economic Research Department of the Federal Reserve Bank of San Francisco.

In official statistics, manufacturing is the top contributor to U.S. productivity growth despite its

shrinking share of nonfarm employment. However, official numbers tend to understate growth

among new producers that improve on existing producers, which is more prevalent outside of

manufacturing. Accounting for such missing productivity growth shows that it plays a larger role

in sectors such as retail trade and services.

Manufacturing employment is also an ever-shrinking portion of total employment in American

Samoa, yet overall output per worker has remained strong. Spending on services has increased

at an average annual rate of 2.8% since 2008, making it the fastest growing consumption

category in the territory. The findings in the article suggest that nonmanufacturing may be an

increasingly important engine of US growth. It will likely be an essential player in American

Samoa’s economic future, as well.

Scaling on Figures

Please note that the chart figures contained in this publication have axes that feature custom

scaling, which may appear to over-emphasize fluctuations in the underlying data. This data

visualization method was utilized to highlight the annual changes that are described in

accompanying analysis sections. Readers should also evaluate fluctuations in presented data

sets in proportion to the total values of the individual data points.

Updates and Changes

The latest available data was utilized in the estimates contained in this publication.

Readers with any questions should contact Nathaniel Clayville and nathaniel.clayville@doc.as.

American Samoa Department of Commerce Statistics Division

Keniseli Lafaele, Director Vai Filiga, Chief of Statistics

Executive Office Building Nathaniel Clayville, Senior Economist

Utulei, American Samoa 96799 (684) 633-5155

nathaniel.clayville@doc.as

2Executive Summary A deceleration in global economic growth has occurred over the past two years, and the Asia- Pacific region has been no exception to this trend. A series of destructive natural disasters have left many Pacific Island Countries and Territories with hundreds of millions of dollars in damages, some of which have unlocked levels of disaster aid and private capital investment funds rarely seen in small, insular countries. American Samoa is a prime example of this trend. The territory experienced a modest economic expansion in 2014 and 2015, which was spurred, in part, by a large capital investment by Tri Marine International for the purchase and construction of facilities for the processing and packaging of locally harvested tuna. The facility opened early in 2016, but regional competition forced the company to permanently halt operations by the end of that same year. Nominal GDP in American Samoa fell by 0.2% in 2016, although the contraction was closer to 2.5%, when adjusted for inflation. The cannery closure contributed to a spike in the territory’s unemployment rate in 2017, from 10.5% to 14.3%. Both private and public sector consumption languished that year, and the economy contracted by an estimated 3.7%. The territory is expected to have experienced modest deflation in the same year. As a result, Real Gross Domestic Product (Real GDP) is projected to have contracted by a more subdued rate of 1.9% in 2017. This contraction may have extended into 2018, if not for a devastating tropical storm that impacted much of American Samoa in February of that year. By some estimates, Tropical Storm Gita caused as much as $186 million in direct and indirect damages across the territory. Federal disaster agencies and international relief organizations poured millions of dollars into the local economy in the weeks and months after the tropical storm, which helped to lift employment, income, and spending throughout the first half of the year. American Samoa also benefited from recent strength in the broader US economy in 2018, driven primarily by strength in labor markets. With relatively low domestic unemployment rates and consumer inflation, wage growth seems to have finally taken hold in the US during 2018, which appears to have translated to accelerated spending by both households and private businesses. Real government consumption grew by its fastest rate in nearly a decade in 2018, even though nominal federal government receipts were hampered by a series of tax cuts. US real GDP increased by an estimated 2.8% in 2018 and is predicted to continue to grow in each year of the forecast period, through 2022. Ongoing disaster relief funding is expected to contribute to modest consumer and government spending increases in American Samoa in 2018. The GDP growth in the territory was calculated at 3.9% in 2018, or 0.7% when adjusted for inflation. Once the immediate fiscal effects of the tropical storm have diminished, so will much of the economic stimulus. Accordingly, real GDP is forecast to decrease by 3.5% in 2019, 1.0% in 2020, 2.3% in 2021, an 2.0% in 2022. This anticipated multi-year contraction is partially driven by higher inflation and is best viewed as a return to a more sustainable long-term trend, following multiple years of energy price decreases and stronger-than-usual capital investments. 3

American Samoa Economic Forecast 2019 Executive Summary Tables

TABLE 1: AMERICAN SAMOA ECONOMIC FORECAST EXECUTIVE SUMMARY DETAILS

American Samoa Economic Forecast

American Samoa Economic Forecast Summary

Category History Forecast

Year 2014 2015 2016 2017 2018 2019 2020 2021 2022

AS Nominal Gross Domestic Product ($ Million) 643.0 661.0 653.0 634.0 658.5 639.0 646.2 639.3 641.1

Annual Growth (%) 0.3 2.8 -1.2 -2.9 3.9 -3.0 1.1 -1.1 0.3

AS Real Gross Domestic Product (2009$ Million) 641.0 649.0 632.0 598.0 602.0 581.0 575.2 561.9 550.8

Annual Growth (%) 0.9 1.2 -2.6 -5.4 0.7 -3.5 -1.0 -2.3 -2.0

AS Average Annual Wage ($/yr) 13,474 13,348 13,850 13,929 14,282 14,329 14,360 14,249 14,158

Annual Growth (%) 0.8 -0.9 3.8 0.6 2.5 0.3 0.2 -0.8 -0.6

AS Personal Income ($ Million) 341.7 335.9 354.7 354.9 364.9 379.4 384.3 370.3 372.9

Annual Growth (%) 6.9 -1.7 5.6 0.0 2.8 4.0 1.3 -3.7 0.7

ASG Revenues ($ Million) 98.9 98.0 90.9 87.9 93.5 95.6 97.2 96.6 96.3

Annual Growth (%) 7.8 -1.0 -7.2 -3.3 6.4 2.2 1.7 -0.6 -0.3

Population 61,811 60,863 60,200 60,300 60,599 61,068 60,891 60,547 59,856

Annual Growth (%) -1.3 -1.5 -1.1 0.2 0.5 0.8 -0.3 -0.6 -1.1

AS Consumer Price Index 98.5 97.7 98.7 101.9 105.4 107.3 109.1 110.3 110.5

Annual Growth (%) 0.0 -0.8 1.0 3.2 3.5 1.8 1.6 1.1 0.2

AS GDP Deflator 100.3 101.8 103.4 106.1 109.4 110.0 112.4 113.8 116.4

Annual Growth (%) -0.7 1.5 1.6 2.6 3.1 0.5 2.2 1.3 2.3

AS Government Revenues ($Million) 98.9 98.0 90.9 87.9 93.5 95.6 97.2 96.6 96.3

Annual Growth (%) 7.8 -1.0 -7.2 -3.3 6.4 2.2 1.7 -0.6 -0.3

4TABLE 2: US ECONOMIC FORECAST EXECUTIVE SUMMARY DETAILS

American Samoa Economic Forecast

US Economic Forecast Summary

Category History Forecast

Year 2014 2015 2016 2017 2018 2019 2020 2021 2022

Real US Gross Domestic Product (2009$ Million) 16,013.3 16,471.5 16,716.2 17,096.2 17,581.6 18,098.7 18,486.9 18,791.9 19,102.1

Annual Growth (%) 2.6 2.9 1.5 2.3 2.8 2.9 2.1 1.6 1.7

Real US Consumption (2009$ Million) 10,868.4 11,264.3 11,572.1 11,890.7 12,179.5 12,461.8 12,755.6 13,036.5 13,295.1

Annual Growth (%) 2.9 3.6 2.7 2.8 2.4 2.3 2.4 2.2 2.0

Real US Business Spending (2009$ Million) 2,762 2,905 2,210 2,314 2,450 2,615 2,754 2,835 2,884

Annual Growth (%) 5.5 5.2 -23.9 4.7 5.9 6.7 5.3 3.0 1.7

Real US Government Spending (2009$ Million) 2,839.1 2,878.5 2,900.1 2,903.3 2,958.3 3,028.2 3,056.6 3,065.9 3,069.4

Annual Growth (%) -0.6 1.4 0.8 0.1 1.9 2.4 0.9 0.3 0.1

Real US Net Exports (2009$ Million) -427.7 -545.3 -586.3 -621.8 -663.5 -707.5 -795.8 -846.0 -858.1

Annual Growth (%) -5.6 -27.5 -7.5 -6.1 -6.7 -6.6 -12.5 -6.3 -1.4

US Employment, Nonfarm (Millions) 138.9 141.8 144.3 146.5 148.8 150.3 151.7 152.5 153.2

Annual Growth (%) 1.9 2.1 1.8 1.5 1.6 1.0 0.9 0.5 0.4

US Unemployment Rate (percent) 6.2 5.3 4.9 4.4 3.9 3.5 3.7 3.9 4.1

Annual Growth (%) -16.1 -14.7 -7.6 -10.6 -11.0 -9.6 4.4 5.8 6.0

US Real GDP per Capita (2009$) 50,221.5 51,277.3 51,661.4 52,455.8 53,542.8 54,727.7 55,507.4 56,030.0 56,563.3

Annual Growth (%) 1.8 2.1 0.7 1.5 2.1 2.2 1.4 0.9 1.0

5Pacific Region Economic Forecast Analysis Pacific Region Economic Summary A deceleration in global economic growth has occurred over the past few years, and the Pacific region has been no exception to this trend. According to the International Monetary Fund (IMF), economic expansion became less homogeneous across countries in 2018, with most emerging markets growing at a faster rate while many advanced economies showed moderate deceleration. One notable exception was China, with Real GDP growth of 6.9% in 2017. It is estimated that China’s economy continued to expand at a similar pace throughout the first half of 2018 but is now also beginning to show signs of slowing. Many of the developed countries in the Pacific region, specifically New Zealand and Australia, have managed to find sustained economic growth through exports to many Asian markets, and through profitable industries, such as mining. Both countries maintain robust aid programs that funnel money into many of the developing Pacific Island Countries (PICs). Foreign aid programs in these countries don’t appear to be at risk in the near-term, especially considering New Zealand’s recently-announced “Pacific Reset” plan, in which the Kiwi government has funded a broad-based set of initiatives to lead the region in identity, security, and prosperity. Meanwhile, the last two years have been a mixed basket for other nations in the Pacific, with a series of destructive cyclones and typhoons wreaking havoc on many PICs, along with historic levels of tourism from developed countries in Asia, Oceania, and North America. In some emerging markets, the storms have worked against other drivers of economic expansion, as was observed in the years after Cyclone Pam clashed with Tuvalu in 2015. Tonga experienced similar constraints following damages from Tropical Storm Gita in early-2018. In some instances, foreign aid from developed countries has provided essential liquidity to affected PICs, supporting efforts to repair or construct critical infrastructure, allowing many island nations that depend on tourism to begin attracting visitors again. Moving forward, it is likely that the region will experience some additional hindrances to unbridled economic growth, such as indirect impacts of global trade feuds or the offshoring of manufacturing operations, which may lead to the erosion of key industries in some countries. Samoa experienced this in 2017, when the country’s largest private employer closed, relocating operations offshore and displacing nearly 700 workers. Notwithstanding downside risks, the Pacific region’s economy is still relatively well positioned to grow over the coming year. IMF estimates that real GDP in the region increased by 1.4% in 2018, which is high in comparison to IMF’s forecast for world-wide economic growth of -2.3% over the same period. Regional Real GDP is anticipated to expand by 4.1% in 2019, versus 0.2%, globally3. 3 October 2018 Regional Economic Outlook: Asia Pacific . October 2018 Regional Economic Outlook: Asia Pacific , www.imf.org/en/Publications/REO/APAC/Issues/2018/10/05/areo1012. 6

Samoa

Coming off of several consecutive

years of relatively strong

economic growth, Samoa is Samoa

expected to report a more 2,500.0 Historical Forecast 4.0

subdued Real GDP increase of 3.0

2,000.0

only 1.8% in 2018, down from

2.5% in 2017. The slowdown was 2.0

1,500.0

2,173.0

primarily due to the lingering

2,126.0

2,080.0

1.0

1,982.0

1,921.0

1,887.0

1,841.0

1,691.0

1,719.0

effects of the closure of the 1,000.0

0.0

Yazaki Samoa factory4, the 500.0

country’s largest private -1.0

employer which had produced 0.0 -2.0

automotive parts in the country 2014 2015 2016 2017 2018 2019 2020 2021 2022

for 25 years before closing their Samoa Real GDP (Tala Million)

doors in late-2017. The closure

Samoa Consumer Inflation Annual Growth (%)

left as many as 700 workers

without jobs. Further FIGURE I: SAMOA REAL GDP AND INFLATION FORECAST

exacerbating the loss of the

country’s largest durable goods manufacturer was the damage caused by Tropical Storm Gita in

February of 2018. The combined impact of these events led to a reduction in output in sectors

such as fishing, financial services, and agriculture. Following the tropical storm, there was also a

notable increase in prices of petroleum products, which led to elevated prices on other goods

and services throughout the country. By mid-2018, the headline inflation rate was as high as

3.7%, ultimately settling at 3.4% for the year. IMF estimates that consumer price inflation will

level off and ease to 3.0% in 2019. IMF is also forecasting that Samoa’s Real GDP will grow by

3.2% in 20195, driven by strength in remittances and visitor receipts.

4

September Quarterly Bulletin 2018. September Quarterly Bulletin 2018,

www.cbs.gov.ws/index.php/dmsdocument/6748.

5

“Samoa.” International Monetary Fund, Countries, www.imf.org/en/Countries/WSM.

7Tonga

The Kingdom of Tonga, which is comprised of 169 islands spread over 270,000 square miles, is

especially susceptible to shocks from natural disasters, climate change, and commodity prices.

With a relatively large portion of the Kingdom’s population dependent on subsistence

agriculture, Tonga is heavily reliant on external support, mainly through foreign aid, direct

foreign investment, and tourism. The Kingdom has been plagued by a series of inflationary

spikes over the last few decades,

Tonga with consumer inflation growth

calculated at 7.4% in 2017, 5.2% in

1,200.0 Historical Forecast 8.0 2018, and is forecast to be 5.3% in

1,000.0 6.0 2019. After sustaining extensive

800.0 damage during Tropical Storm Gita

4.0 in early-2018, a flood of foreign

1,056.0

1,026.0

600.0

989.0

aid eclipsed a falloff in tourism. As

945.0

895.0

870.0

849.0

2.0

815.0

788.0

400.0 a result, real GDP grew by an

200.0 0.0 estimated 2.9%. A projected

0.0 -2.0 increase in tourism from Australia

2014 2015 2016 2017 2018 2019 2020 2021 2022 and New Zealand in the coming

years, along with a steady stream

Tonga Real GDP (Pa'anga Million)

of foreign aid during the ongoing

Tonga Consumer Inflation Annual Growth (%) efforts to rebuild, is likely to

FIGURE II: TONGA REAL GDP AND INFLATION FORECAST contribute to real GDP growth of

5.6% in 20196.

Fiji

Fiji is home to one of the largest and most diversified PIC economies, supporting several goods

producing and service sectors. According to the Reserve Bank of Fiji’s December 2018 Economic

Review7, robust domestic consumption, along with strong public and private investment

spending, has kept the domestic economy in positive territory since the height of the global

financial recession in 2009. One of the country’s largest manufacturing sectors, sugar

production, lagged in late-2018, due to low quality of domestically harvested sugar cane. As a

result, industrial production declined by 1.2% that same year. Excluding sugar, industrial

production increase at an annual rate of 2.5% over the same period. Domestic consumption

also remained firm during 2018, with double-digit annualized growth in categories such as

6

“Tonga.” International Monetary Fund, Countries, www.imf.org/en/Countries/TON.

7

Economic Review - Month Ended December 2018. Economic Review - Month Ended December 2018,

www.rbf.gov.fj/getattachment/86333b1f-d47b-45d2-9546-9766ff4282bb/Economic-Review-December-2018-

(1).pdf?lang=en-US.

8lending and vehicle registrations.

As might be expected, strength in Fiji

household spending has been 10,000.0 Historical Forecast 5.0

accompanied by a rise in 8,000.0 4.0

consumer prices, with the headline

price level indicator growing at a 6,000.0 3.0

8,146.0

7,893.0

7,641.0

7,397.0

7,154.0

5.2% annualized rate of inflation in

6,932.0

6,684.0

6,728.0

6,437.0

4,000.0 2.0

late-2018. IMF has predicted an

2,000.0 1.0

easing of inflationary pressures in

Fiji over the coming year, with an 0.0 0.0

anticipated increase in overall 2014 2015 2016 2017 2018 2019 2020 2021 2022

consumer prices of 3.9% in 2019. Fiji Real GDP (FJD Million)

IMF calculated Real GDP growth of Fiji Consumer Inflation Annual Growth (%)

3.2% in 2018, which is forecast to

FIGURE III: FIJI REAL GDP AND INFLATION FORECAST

rise to a rate of 3.4% in 2019.8

New Zealand

As one of the largest contributors to foreign aid in the Pacific, and a major trade partner to

many PICs, the state of New Zealand’s economy is often an important driver of economic

fluctuations for the entire region. The economy of New Zealand has been growing consistently

since 2008, bolstered by strong domestic demand, a favorable exchange rate, and high levels of

government spending. Real GDP

New Zealand exceeded 4.0% in 2016—the highest

annual increase since before the

300.0 Historical Forecast 2.5

global financial crisis. The country’s

250.0 2.0 economy has since moderated to

200.0 annualized real GDP growth of just

1.5

over 3.0%. Like many other

279.8

272.6

150.0

264.5

256.4

248.9

241.5

234.3

225.0

developed economies, New Zealand

216.0

1.0

100.0

is near, or has possibly already

50.0 0.5

surpassed, the point of full

0.0 0.0 employment. According to the

2014 2015 2016 2017 2018 2019 2020 2021 2022 Reserve Bank of New Zealand’s

New Zealand Real GDP (NZD Billion) November 2018 Monetary Policy

New Zealand Consumer Inflation Annual Growth (%) Statement9, employment at or

above this maximum sustainable

FIGURE IV: NEW ZEALAND REAL GDP AND INFLATION FORECAST level will likely lead to increases to

input costs for firms, which is likely

8

“Fiji.” International Monetary Fund, Countries, www.imf.org/en/Countries/FJI.

9

Monetary Policy Statement November 2018. Monetary Policy Statement November 2018, www.rbnz.govt.nz/-

/media/ReserveBank/Files/Publications/Monetary%20policy%20statements/2018/mpsnov2018.pdf.

9to put moderate upward pressure on consumer prices. IMF estimates that headline inflation

growth rate, which has been contained below 2.0% since 2012, was 1.4% in 2018, and is

forecast to increase to 1.7% in 2019. 2018 real GDP expanded by a calculated 3.1% in 2018 and

is expected to grow by an additional 3.0% in 2019.10

Australia

Australia is another major contributor to foreign aid and capital improvement projects in the

Pacific. This country has maintained year-over-year real economic growth since the early 1990s,

including throughout the global economic recession and the decade since. According to the

Reserve Bank of Australia’s November 2018 Statement on Monetary Policy11, the Australian

economy has drawn strength from low interest rates, a strong global economy, and high levels

of spending on public infrastructure projects. Australia also benefitted from strong exports to

China and a mining boom that began sometime around 2003, and never fully exhausted itself.

These comparative benefits have helped to maintain moderate, yet broad-based increases in

domestic consumer spending, even in spite of the relatively slow growth in household income,

implying the possibility that spare capacity may still exist in the Australian labor market. There

is some evidence to suggest that Australia’s surging housing market is near its peak, with

private residential building

approvals showing signs of waning Australia

in the second half of 2018. 2,500.0 Historical Forecast 3.0

Consumer prices have been quite

2,000.0 2.5

stable, holding between 1.0% and

2.5% over the last five years. This 2.0

1,500.0

trend is anticipated to continue 1.5

1,967.5

1,917.5

1,868.5

1,819.9

1,771.0

1,715.4

1,678.1

1,635.5

1,595.8

into the foreseeable future, with 1,000.0

1.0

the headline inflation rate 500.0 0.5

calculated at 2.2% in 2019, and

2.3% in 2019. Real GDP is 0.0 0.0

2014 2015 2016 2017 2018 2019 2020 2021 2022

estimated to have grown by 3.2%

in 2018, which is forecast to Australia Real GDP (AUD Billion)

decelerate to 2.8% in 2019, Australia Consumer Inflation Annual Growth (%)

potentially as a result of the

sluggishness in the housing FIGURE V: AUSTRALIA REAL GDP AND INFLATION FORECAST

market. 12

Additional details can be found in the following data tables.

10

“New Zealand.” International Monetary Fund, Countries, www.imf.org/en/Countries/NZL.

11

Statement on Monetary Policy November 2018. Statement on Monetary Policy November 2018,

www.rba.gov.au/publications/smp/2018/nov/pdf/statement-on-monetary-policy-2018-11.pdf.

12

“Australia.” International Monetary Fund, Countries, www.imf.org/en/Countries/AUS.

10Pacific Region Economic Forecast Tables

TABLE 3: PACIFIC REGION COUNTRIES REAL GDP FORECAST

American Samoa Economic Forecast - Regional Economic Forecast

Real GDP

Category History Forecast

Year 2014 2015 2016 2017 2018 2019 2020 2021 2022

Samoa Real GDP (Tala Million) 1,691.0 1,719.0 1,841.0 1,887.0 1,921.0 1,982.0 2,080.0 2,126.0 2,173.0

Annual Growth (%) 1.2 1.7 7.1 2.5 1.8 3.2 4.9 2.2 2.2

Tonga Real GDP (Pa'anga Million) 788.0 815.0 849.0 870.0 895.0 945.0 989.0 1,026.0 1,056.0

Annual Growth (%) 3.0 3.4 4.2 2.5 2.9 5.6 4.7 3.7 2.9

Fiji Real GDP (FJD Million) 6,437.0 6,684.0 6,728.0 6,932.0 7,154.0 7,397.0 7,641.0 7,893.0 8,146.0

Annual Growth (%) 5.6 3.8 0.7 3.0 3.2 3.4 3.3 3.3 3.2

New Zealand Real GDP (NZD Billion) 216.0 225.0 234.3 241.5 248.9 256.4 264.5 272.6 279.8

Annual Growth (%) 3.2 4.2 4.1 3.0 3.1 3.0 3.1 3.1 2.6

Australia Real GDP (AUD Billion) 1,595.8 1,635.5 1,678.1 1,715.4 1,771.0 1,819.9 1,868.5 1,917.5 1,967.5

Annual Growth (%) -2.6 -2.5 -2.6 -2.2 -3.2 -2.8 -2.7 -2.6 -2.6

11TABLE 4: PACIFIC REGION COUNTRIES INFLATION FORECAST

American Samoa Economic Forecast - Regional Economic Forecast

Consumer Inflation

Category History Forecast

Year 2014 2015 2016 2017 2018 2019 2020 2021 2022

Samoa Consumer Inflation Annual Growth (%) -1.2 1.9 0.1 1.3 3.4 3.0 2.9 2.8 3.0

Tonga Consumer Inflation Annual Growth (%) 1.2 -1.1 2.6 7.4 5.2 5.3 1.9 2.5 2.6

Fiji Consumer Inflation Annual Growth (%) 0.5 1.4 3.9 3.4 3.9 3.2 3.0 3.0 3.0

New Zealand Consumer Inflation Annual Growth (%) 1.2 0.3 0.6 1.9 1.4 1.7 1.9 2.0 2.0

Australia Consumer Inflation Annual Growth (%) 2.5 1.5 1.3 2.0 2.2 2.3 2.5 2.5 2.5

12United States of America Economic Forecast Analysis US Economic Summary The US economy expanded for the 9th consecutive year in 2018, driven primarily by strength in the labor markets. With relatively low unemployment rates and inflation, wage growth seems to have finally taken hold in the US during 2018, which seems to have translated to increased spending by both households and private businesses. Real government spending grew by its fastest pace in nearly a decade in 2018, even though nominal federal government receipts were hampered by a series of tax cuts. US real GDP increased by an estimated 2.8% in 2018 and is expected to continue to grow in each year of the forecast period, through 2022. The US labor markets saw some of the lowest unemployment rates in recent history in 2018. Total nonfarm payrolls increased by an average of 254,000 per month during the fourth quarter of 2018 and the seasonally adjusted unemployment rate ended the year at 3.9%. US nominal disposable personal income grew at an average annual pace of 3.7% from 2014 through 2017 before expansion slowed to 1.2% in 2018. EIA’s 2019 Annual Energy Outlook estimates that this income growth will average 2.7% over the remainder of the forecast period. This more modest rate suggests the possibility that the US is at or near the level of full employment. Between 2014 and 2018 consumer spending grew at an average yearly rate of 2.9%, driven in part by falling oil prices and the associated timid inflation. With employment approaching the natural rate of unemployment, wage growth is anticipated to level off, which should bring household spending back to a more sustainable level. Specifically, real US personal consumption is projected to increase by 2.3% in 2019, 2.4% in 2020, 2.2% in 2021, and 2.0% in 2022. Capital investments by private businesses on residential and nonresidential structures, equipment, intellectual property products, and other business inputs have been growing since 2016. Real business investments fell by 23.9% in 2016, which was primarily a result of falling oil prices disincentivizing spending on new energy structures and associated equipment. Spending in this category bounced back in 2017, increasing by 4.7% that year and 5.9% the following year. Real business investments are expected to grow by 6.7% in 2019, 5.3% in 2020, 3.0% in 2021, and 1.7% in 2022. Recent news about government spending has primarily focused on the effects of the federal government shutdown that started on December 22, 2018 and ended on January 25, 2019. The Congressional Budget Office (CBO) estimated that the five-week shutdown led to a delay in federal discretionary spending of approximately $1.8 billion, reduced fourth quarter 2018 real GDP by $3 billion, and decreased first quarter 2019 real GDP by $8 billion (versus what it was forecast to be without the effects of the shutdown). Federal government outlays were calculated to have grown by 4.8% in 2018, while tax receipts rose by a relatively sluggish 0.7%, primarily due to the lower corporate tax rate and higher standard deductions that were 13

enacted in the Tax Cuts and Jobs Act of 2017. The act was passed and signed into law in late-

2017, with many of the provisions taking effect in 2018. Adjusted for inflation, 2018 US

government spending was estimated to have climbed at a rate of 1.9% in 2018, and is forecast

to grow by 2.4% in 2019, 0.9% in 2020, 0.3% in 2021, and 0.1% in 2022.

2018 was a volatile year for US trade as the trade-weighted value of the US dollar fell for the

second consecutive year after the US imposed new tariffs on approximately 12% of all goods

imported into the country. In response, US trade partners retaliated, collectively, with new

tariffs on around 9% of all goods exported by the US. According to the CBO, the impact of the

new tariffs is expected to reduce real US GDP by an average of 0.1% through 2029. The most

recent BEA monthly trade report showed an 11.4% increase in the year-to-date deficit, versus

the same period in 2017. Adjusted for inflation, net exports are projected to be -$663 billion in

2018, -$708 billion in 2019, -$796 billion in 2020, -$846 in 2021, and -$858 in 2022.

Continued momentum in the leading consumption categories is anticipated to continue the

trend of real GDP growth through 2022. Specifically, inflation-adjusted GDP is estimated to

have increased by 2.8% in 2018, and is forecast to expand by 2.9% in 2019, 2.1% in 2020, 1.6%

in 2021, and 1.7% in 2022.

Additional analysis on specific US economic indicators can be found in the following sections.

US Labor Markets

The US labor markets saw History Forecast

$160.0 10.0%

some of the lowest

$155.0

unemployment rates in recent 8.0%

history in 2018. Total nonfarm $150.0

payrolls increased by an $145.0 6.0%

average of 254,000 per month $140.0

during the fourth quarter of $135.0 4.0%

2018 and the seasonally $130.0

adjusted unemployment rate 2.0%

$125.0

ended the year at 3.9%.13

Wage growth had been $120.0 0.0%

anemic from 2010, following the

14

15

16

17

18

19

20

21

22

20

20

20

20

20

20

20

20

20

global economic recession, and

remained subdued through US Employment, Nonfarm (Millions)

mid-2014, during which time

US Unemployment Rate (percent)

annualized wage increases

FIGURE VI: US EMPLOYMENT AND UNEMPLOYMENT

13

United States, Department of Labor, Bureau of Labor Statistics. “The Employment Situation - December 2018.”

The Employment Situation - December 2018. www.bls.gov/news.release/pdf/empsit.pdf.

14never exceeded 2.5%.14 US wages broke that threshold in September of 2016, and have grown

at an annualized rate of at least 2.8% in each month since, with the most recent data suggesting

that wages are currently rising at a 3.9% annualized pace. US nominal disposable personal

income grew at an average rate of 3.7% from 2014 through 2017 before slowing to 1.2% in

2018. EIA’s 2019 Annual Energy Outlook estimates that this rate will average 2.7% through

2022, suggesting the possibility that the US is at or near the level of full employment. Total

nonfarm payrolls in the US increased by 1.6% in 2018, from 146 million to 149 million, and are

expected to grow to approximately 153 million nonfarm workers in the US by 2022. The flagship

unemployment rate averaged 3.9% in 2018 and is forecast to be 3.5% in 2019, 3.7% in 2020,

3.9% in 2021, and 4.1% in 2022.

US Inflation

US inflation has been subdued since the Great Recession, when the Consumer Price Index (CPI)

surpassed an annualized growth rate of 5% for a handful of months in 2008. Tepid aggregate

demand kept pressure on prices through 2014. It was that year in which personal consumption

in the US surged, yet most inflation indicators increased only moderately, and the CPI even fell

into deflationary territory for the first two months of 2015. The reason for this counterintuitive

inflationary response to higher aggregate demand was an erosion in the price of crude oil,

which helped to stimulate the economy by decreasing freight and transportation costs. By the

time oil prices had begun to rise more rapidly in 2016, many supply chain systems in the US had

established economies of scale and were able to absorb a certain amount of growth in freight

costs. Prices began to rise, but slower than anticipated, given the increase in oil prices.

Consumer price growth nearly reached

3.0% History Forecast 3% by the beginning of 2017, and then

again in mid-2018, before oil prices

2.5% began to fall again. The Producer Price

2.0%

Index (PPI), which measures the prices

that domestic producers pay for input

1.5% goods and services, is typically a

leading indicator of movements in

1.0% consumer prices, increased by 4.3% in

0.5% 2018, and is forecast to grow by 2.2%

in 2019, 2.7% in 2020, and 1.6% in

0.0% both 2021 and 2022. The CPI for all

urban consumers in the US rose by

14

15

16

17

18

19

20

21

22

2.4% in 2018 and is projected to

20

20

20

20

20

20

20

20

20

US CPI All Items (% Growth) increase by 2.1% in 2019, 2.6% in

2020, and 2.4% in both 2021 and 2022.

FIGURE VII: US INFLATION

14

The Federal Reserve Bank of Atlanta, Wage Growth Tracker, www.frbatlanta.org/chcs/wage-growth-

tracker.aspx.

15US Consumer Spending

Personal consumption

expenditures account for $13,280 History Forecast

approximately 70% of US GDP,

$12,780

and includes household

spending on durable goods, $12,280

nondurable goods, and

$11,780

services. Real consumer

spending in the US declined in $11,280

the years leading up to the

$10,780

prior recession, but has been

on the rise ever since, growing $10,280

at an average annual rate of

$9,780

2.4% from 2009 through 2018.

Spending was lackluster in the

14

15

16

17

18

19

20

21

22

20

20

20

20

20

20

20

20

20

years immediately following

the recession, increasing at an US Real Consumption (2009 CW $ Billion)

average annual pace of only

1.8% from 2009 to 2013. It FIGURE VIII: US REAL CONSUMER SPENDING

wasn’t until 2014 that US

households finally began to believe that the economic recovery could be sustained. Between

2014 and 2018 consumer spending rose at an average yearly rate of 2.9%, driven in part by

falling oil prices and the associated timid inflation. By 2015, wage growth was beginning to pick

up again and year-over-year inflation-adjusted consumer expenditures rose by 3.6%, followed

by 2.7% in 2016, 2.8% in 2017, and 2.4% in 2018. With employment approaching the natural

rate of unemployment, wage growth is expected to level off, which should bring household

spending back in line with a more sustainable, long-term trend. Specifically, real US personal

consumption is forecast to increase by 2.3% in 2019, 2.4% in 2020, 2.2% in 2021, and 2.0% in

2022.

US Private Fixed Investment

Capital investments by private businesses on residential and nonresidential structures,

equipment, intellectual property products, and other business inputs have been growing since

2016. Real business investments fell by 23.9% in 2016, which was primarily a result of falling oil

prices disincentivizing spending on new energy structures and associated equipment. Spending

in this category bounced back in 2017, increasing at a rate of 4.7% that year, followed by 5.9%

in the following year. Real business investments are projected to grow by 6.7% in 2019, 5.3% in

2020, 3.0% in 2021, and 1.7% in 2022.

16US Government Spending

Federal government spending has increased at an average rate of 3.9% each year from 2013. It

was that year that Congress approved a budget deal raising taxes and postponing automatic

spending cuts, known as “sequestration”, and avoiding the so-called “fiscal cliff”. As a result,

total tax receipts grew by 13.3% that year and total outlays shrunk by 2.3%. Each year since

then, both receipts and spending have grown by 3.8% and 3.9%, respectively15. More recently,

government spending news has revolved around the federal government shutdown that

started on December 22, 2018 and ended on January 25, 2019. The Congressional Budget Office

(CBO) estimated that the five-week shutdown led to a delay in federal discretionary spending of

approximately $1.8 billion, reduced fourth quarter 2018 real GDP by $3 billion, and decreased

first quarter 2019 real GDP by $8 billion (versus what it was expected to be without the effects

of the shutdown)16. Federal

$3,070 History Forecast

government outlays were estimated to

have grown by 4.8% in 2018, while tax

$2,970

receipts increased by a relatively

$2,870 sluggish 0.7%, primarily due to the

$2,770 lower corporate tax rate and higher

$2,670 standard deductions that were

enacted in the Tax Cuts and Jobs Act of

$2,570

2017. The act was passed and signed

$2,470 into law in late-2017, with many of the

$2,370 provisions taking effect in 2018.

$2,270 Adjusted for inflation, 2018 US

government spending was calculated

14

15

16

17

18

19

20

21

22

to have increased by 1.9% in 2018, and

20

20

20

20

20

20

20

20

20

US Real Government Spending (2009 CW $ Billion) is forecast to grow by 2.4% in 2019,

0.9% in 2020, 0.3% in 2021, and 0.1%

FIGURE IX: US REAL GOVERNMENT SPENDING in 2022.

15

United States, White House Office of Management and Budget. “Table 1.1—Summary of Receipts, Outlays, and

Surpluses or Deficits (-): 1789–2023.” Table 1.1—Summary of Receipts, Outlays, and Surpluses or Deficits (-): 1789–

2023. www.whitehouse.gov/wp-content/uploads/2018/02/hist01z1-fy2019.xlsx.

16

United States, Congress, Congressional Budget Office. “The Effects of the Partial Shutdown Ending in January

2019.” The Effects of the Partial Shutdown Ending in January 2019. www.cbo.gov/system/files?file=2019-

01/54937-PartialShutdownEffects.pdf.

17US Net Exports

2018 was a volatile year for US trade as the

trade-weighted value of the US dollar fell $3,630 History Forecast

for the second consecutive year after the US $3,430

imposed new tariffs on approximately 12% $3,230

of all goods imported into the country. $3,030

Some of these new tariffs were broadly $2,830

applied to certain products from all US $2,630

trade partners, including the tariffs on $2,430

washing machines, solar panels, and steel $2,230

and aluminum products, while others were

$2,030

targeted at specific countries (namely,

China). In response, US trade partners

14

15

16

17

18

19

20

21

22

20

20

20

20

20

20

20

20

20

retaliated, collectively, with new tariffs on US Real Imports (2009 CW $ Billion)

around 9% of all goods exported by the US.

The immediate impact of the tariffs was a FIGURE X: REAL US IMPORTS

surge in trade activity, boosting real

annualized GDP growth to 4.5% in the second quarter of 2018 international buyers placed large

orders that would fill before the new tariff schedule took effect. However, the surge in exports

is widely anticipated to have been a one-time phenomenon. According to the CBO, the impact

of the new tariffs is expected to reduce real US GDP by an average of 0.1% through 202917. The

most recent data shows that the seasonally-adjusted goods and services US trade deficit

widened over the last half of 2018. The

History Forecast

most recent BEA monthly trade report

$2,690

showed an 11.4% increase in the year-to-

$2,490 date deficit, versus the same period in

201718. Still, real US exports are estimated

$2,290

to have grown by 5.4% in 2018 and are

$2,090 projected to rise at an average annual rate

of 5.2% through 2022. Real US imports

$1,890

climbed by an estimated 5.7% in 2018 and

$1,690 are expected to grow at an average annual

rate of 5.6% over the same period. Adjusted

14

15

16

17

18

19

20

21

22

for inflation, net exports are forecast to by -

20

20

20

20

20

20

20

20

20

US Real Exports (2009 CW $ Billion) $663 billion in 2018, -$708 billion in 2019, -

$796 billion in 2020, -$846 in 2021, and -

FIGURE XI: REAL US EXPORTS $858 in 2022.

17

United States, Congress, Congressional Budget Office. “The Budget and Economic Outlook: 2019 to 2029.” The

Budget and Economic Outlook: 2019 to 2029. www.cbo.gov/system/files?file=2019-01/54918-Outlook.pdf.

18

United States, Congress, Bureau of Economic Analysis. “U.S. International Trade in Goods and Services, October

2018.” U.S. International Trade in Goods and Services, October 2018. www.bea.gov/system/files/2018-

12/trad1018.pdf.

18US Economic Forecast Tables

TABLE 5: US ECONOMIC FORECAST DETAILS

American Samoa Economic Forecast

US Economic Forecast Summary

Category History Forecast

Year 2014 2015 2016 2017 2018 2019 2020 2021 2022

Real US Gross Domestic Product (2009$ Million) 16,013.3 16,471.5 16,716.2 17,096.2 17,581.6 18,098.7 18,486.9 18,791.9 19,102.1

Annual Growth (%) 2.6 2.9 1.5 2.3 2.8 2.9 2.1 1.6 1.7

Real US Consumption (2009$ Million) 10,868.4 11,264.3 11,572.1 11,890.7 12,179.5 12,461.8 12,755.6 13,036.5 13,295.1

Annual Growth (%) 2.9 3.6 2.7 2.8 2.4 2.3 2.4 2.2 2.0

Real US Business Spending (2009$ Million) 2,762 2,905 2,210 2,314 2,450 2,615 2,754 2,835 2,884

Annual Growth (%) 5.5 5.2 -23.9 4.7 5.9 6.7 5.3 3.0 1.7

Real US Government Spending (2009$ Million) 2,839.1 2,878.5 2,900.1 2,903.3 2,958.3 3,028.2 3,056.6 3,065.9 3,069.4

Annual Growth (%) -0.6 1.4 0.8 0.1 1.9 2.4 0.9 0.3 0.1

Real US Net Exports (2009$ Million) -427.7 -545.3 -586.3 -621.8 -663.5 -707.5 -795.8 -846.0 -858.1

Annual Growth (%) -5.6 -27.5 -7.5 -6.1 -6.7 -6.6 -12.5 -6.3 -1.4

US Employment, Nonfarm (Millions) 138.9 141.8 144.3 146.5 148.8 150.3 151.7 152.5 153.2

Annual Growth (%) 1.9 2.1 1.8 1.5 1.6 1.0 0.9 0.5 0.4

US Unemployment Rate (percent) 6.2 5.3 4.9 4.4 3.9 3.5 3.7 3.9 4.1

Annual Growth (%) -16.1 -14.7 -7.6 -10.6 -11.0 -9.6 4.4 5.8 6.0

US Real GDP per Capita (2009$) 50,221.5 51,277.3 51,661.4 52,455.8 53,542.8 54,727.7 55,507.4 56,030.0 56,563.3

Annual Growth (%) 1.8 2.1 0.7 1.5 2.1 2.2 1.4 0.9 1.0

19TABLE 6: OTHER ECONOMIC INDICATORS FORECAST DETAILS

American Samoa Economic Forecast

Other Economic Indicators Summary

Category History Forecast

Year 2014 2015 2016 2017 2018 2019 2020 2021 2022

US CPI All Items (Index, 1982-84=100) 236.7 237.0 240.0 245.1 251.3 256.6 263.4 269.7 276.1

Annual Growth (%) 1.6 0.1 1.3 2.1 2.5 2.1 2.6 2.4 2.4

US PPI All Items (Index, 1982=100) 205.3 190.4 185.4 193.6 202.3 206.8 212.5 215.8 219.4

Annual Growth (%) 0.9 -7.2 -2.7 4.4 4.5 2.2 2.7 1.6 1.6

US GDP Deflator (Index, 2009=100) 108.8 110.0 111.4 113.4 115.7 118.5 121.8 125.0 128.2

Annual Growth (%) 1.8 1.1 1.3 1.8 2.0 2.5 2.8 2.7 2.5

US Federal Funds Rate (Average %) 0.1 0.1 0.4 1.0 1.8 2.8 3.4 3.5 3.5

Annual Growth (%) -17.1 48.6 198.1 153.6 82.9 54.9 19.7 1.9 0.3

US 10yr Treasury Note (Average %) 2.3 2.9 2.9 2.3 3.1 3.6 3.7 3.8 3.7

Annual Growth (%) 15.9 -23.8 -0.3 18.8 -32.0 -16.1 -5.0 -0.9 1.3

US Industrial Production (Index 2007=100) 105.2 104.1 102.1 103.7 107.8 111.3 113.6 115.2 115.2

Annual Growth (%) 3.1 -1.0 -1.9 1.6 3.9 3.3 2.1 1.5 0.0

Broad Trade Weighted Dollar Index 87.2 97.5 107.0 105.8 102.2 101.7 102.9 103.8 110.2

Annual Growth (%) 2.1 11.8 9.7 -1.1 -3.4 -0.4 1.2 0.9 6.1

Brent Crude Oil Average Nominal Price (USD) 99.0 52.3 43.7 55.2 74.4 73.3 73.3 74.4 74.4

Annual Growth (%) -8.8 -47.1 -16.4 26.2 34.8 -1.6 0.0 1.6 0.0

20American Samoa Economic Forecast Analysis American Samoa Economic Summary The economy of American Samoa has been in a state of flux over the last few years. The territory experienced modest economic growth in 2014 and 2015, which was spurred, in part, by a large capital investment by Tri Marine International on the purchase and construction of facilities for processing and packaging locally harvested tuna. The cannery opened early in 2016, under the name Samoa Tuna Processors (STP). Competition from Asian-based canneries immediately put the company in a precarious position and processing operations permanently halted in late-2016. Nominal GDP in American Samoa fell by 0.2% that year, although the inflation-adjusted contraction was closer to 2.5%. STP laid off at least 400 employees during the closure, which led to hundreds of additional job losses in related and support industries over the following year. Starkist Samoa Co., American Samoa’s last remaining tuna processor, also faced setbacks in 2017. Availability of landed fish, along with a number of federally-mandated equipment upgrades, forced the company to temporarily halt operations for five weeks in the fourth quarter of 2017. The shutdown left thousands of employees without salaries to cover basic expenses and cost the local government more than half-a-million dollars in income tax revenues. The combined impact of the cannery closures contributed to a spike in the unemployment rate in the territory in 2017, from 10.5% in 2016 to 14.3%, and led to stagnant spending in both the private and public sectors. The economy contracted by 3.7% in 2017. The territory also experienced modest inflation in the same year and Real GDP contracted by 5.3%. The recession may have extended into the following year, if not for a devastating storm that impacted much of American Samoa in February of 2018. By some estimates, Tropical Storm Gita caused as much as $125 million in direct and indirect damages across the territory.19 At least 50% of all individuals in the territory were faced with significant damage to real and/or personal property during the storm. Food, water, and other basic necessities were in high demand throughout the days and weeks that followed. During that time, automated teller machines were persistently low on cash supplies as the people of the territory scrambled to draw enough to cover immediate repair and replacement costs. Additionally, international relief agencies distributed pre-loaded gift cards to families and individuals that were most affected by the storm. Disaster relief funding is expected to contribute to consumer and government spending in 2018. Specifically, real GDP in American Samoa is forecast to have grown by 0.7% in 2018. Once the immediate effects of the tropical storm have diminished, so will many of the economic stimulus benefits. Real GDP is predicted to decrease by 3.5% in 2019, 1.0% in 2020, 2.3% in 19 Clayville, Nathaniel. “Impact of Cyclone Gita on the Economy of American Samoa.” American Samoa, Pago Pago, 12 Apr. 2018. 21

2021, and 2.0% in 2022. This anticipated multi-year contraction is partially driven by higher

inflation and is best viewed as a return to a more sustainable long-term trend, following

multiple years of energy price decreases and stronger-than-usual capital investment.

Additional analysis on specific American Samoa economic indicators can be found in the

following sections.

Employment

The economy of American

Samoa benefitted from a History Forecast 20.0%

number of government and 18,100

18.0%

private capital investment 17,600

16.0%

projects for most of the 17,100

years since 2009, including 16,600 14.0%

a $60 million investment in 12.0%

the STP tuna cannery and 16,100 10.0%

more than $100 million in 15,600 8.0%

combined funds from 15,100 6.0%

Federal Emergency 14,600 4.0%

Management Agency

14,100 2.0%

(FEMA), from US

Department of Labor, and 13,600 0.0%

from grants awarded

14

15

16

17

18

19

20

21

22

through the American

20

20

20

20

20

20

20

20

Recovery and Reinvestment 20 AS Employed Forecast

Act of 2009 (ARRA). As a AS Unemployment Rate Forecast

result, total nonfarm

payrolls in the territory had FIGURE XII: AMERICAN SAMOA EMPLOYMENT AND UNEMPLOYMENT

grown to more than 18,000

by 2016. Following the closure of the STP cannery in late-2016, cannery employment in the

territory fell by 400 in 2017. The impact to the rest of the economy led to an additional loss of

approximately 500 workers from other private sectors in the territory, and 100 government

employees. Subsequently, the unemployment rate in the territory rose from 10.5% in 2016 to

an estimated 14.3% in 2017.

This trend was temporarily bucked in early-2018, when Tropical Storm Gita impacted many of

the islands of American Samoa. The storm left hundreds of millions of dollars of damage to

public and private structures, property, and infrastructure. There was an immediate response

from the federal government, and a wave of disaster relief funds from FEMA and international

relief organizations soon followed. Initial support from FEMA funded emergency management

operations, helping to bankroll the expensive tasks of debris removal and restoration of public

utilities, while the Red Cross injected as much as a million dollars into the local economy

22through direct donations to affected households. The flood of new consumer and government

spending contributed to a calculated 3.1% increase in total nonfarm payrolls in 2018, from

around 17,200 to over 17,700, and reduced the unemployment rate from 14.3% to 11.4%.

The majority of the employment impacts from the tropical storm were contained in the six

months immediately following the disaster. As such, federal and territorial government payroll

impacts have likely already occurred and are forecast to remain near 7,900 through 2019

before swelling to more than 8,100 in 2020, when the decennial census survey is carried out.

Following the completion of the 2020 Census, the Census workforce will be reduced and

government payrolls in American Samoa are anticipated to decrease to approximately 7,500 in

2021, and 7,600 in 2022.

Private nonfarm payrolls are likely to follow a similar trajectory. However, the post-census dip

in the outer years of the forecast period will likely be cushioned by modest growth in cannery

employment, as Starkist Samoa Co. is expected to increase production of pouch tuna products.

Total nonfarm payrolls are projected to rise by 1.9% (18,100) in 2019, and 0.9% (18,200) in

2020, before contracting by 6.7% (17,000) in 2021, and then growing by 0.8% (17,100) in 2022.

Accordingly, the unemployment rate is forecast to be 11.4% in 2019, 11.0% in 2020, 12.5% in

2021, and 11.6% in 2022.

Wages and Income

Strong government and business spending in the territory since the 2009 tsunami has

contributed to average annualized wage growth of 2.8% over the last decade. Personal income,

which is the sum of all wages and incomes earned in American Samoa, climbed by 5.4% in 2016,

which was the final year of

History Forecast construction on the STP cannery.

$5,740 Disposable personal income,

$14,000 which excludes tax and debt

$5,540

payments and essentially

$5,340

$13,500 represents household buying

$5,140 power, rose by 5.1% in the same

$4,940 year. In 2017, after the cannery

$13,000

closure, personal income and

$4,740

disposable personal income

$4,540 $12,500 growth slowed to 0.1% and

$4,340 0.7%, respectively. Each of these

$4,140 $12,000 income variables would have

contracted that year, if not for a

14

16

18

20

22

steep increase in transfer

20

20

20

20

20

payments from government

AS Disposable Personal Income per Capita (USD) Forecast

AS Average Annual Wage - All Sectors

entities to individuals, namely

pension distributions, social

FIGURE XIII: AMERICAN SAMOA WAGES AND INCOME security benefits, and

23You can also read