Are pay-tv and OTT in the same relevant market in South Africa?* - Econex

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Occasional Note

February 2019

Are pay-tv and OTT in the same

relevant market in South Africa?*

Elize Rich

This research note is aimed at answering the question of substitutability between pay-television services

(e.g. Multichoice’s DStv) and over-the-top services (OTT), (e.g. Netflix), in a South African context. This

question is especially relevant, against the background of the planned listing of Multichoice on the Jo-

hannesburg Stock Exchange during the first quarter of 2019, and the ongoing inquiry into subscription

broadcasting services by the sector regulator, ICASA.

The nub of the issue is the question whether pay-television and OTT services fall in the same relevant

anti-trust market. The answer to this question will determine who has market power and whether ex-ante

regulation of such market power is justified. These are important issues as policy interventions should

not stifle the rapid technological developments that are characteristic of this sector.

This occasional note considers these issues from an economic perspective. We highlight the fact that

relative to markets with high levels of OTT penetration (e.g. the United States and Canada), South Africa

has low levels of internet penetration, slow internet speeds and comparatively high data prices, all of

which limit the potential substitution of pay-TV with OTT services. This requires original thinking and ap-

plication of economic principles about relevant markets, in this country-specific context.

About ECONEX

ECONEX is an economics consultancy that offers in-depth economic analysis, covering competition economics, inter-

national trade, strategic analysis and regulatory work. The company was co-founded by Prof Nicola Theron and Prof

Rachel Jafta during 2005. Both these economists have a wealth of consulting experience in the fields of competition

and trade economics. They also teach courses in competition economics and international trade at Stellenbosch Uni-

versity. For more information on our services, as well as the economists and academic associates working at and with

Econex, visit our website at www.econex.co.za.

* Econex presented comments on ICASA’s inquiry into subscription television broadcasting services on behalf of Econet/Kwesé.

1

Occasional Note

February 2019

1 Introduction relevant antitrust market is cru- must consider when they poten-

cial for determining dominance tially want to substitute pay-TV

and the need for regulatory in- with OTT. However, it first takes

The broadcasting sector as tervention in the broadcasting a step back to look at internet

a whole is evolving, closely sector. Based on South Africa’s access and internet speeds re-

aligned with the fast-paced de- limited internet penetration, quired for streaming content.

velopments in technology. In low internet speed and high We find that South Africa’s in-

South Africa, the sector has cost of data, ICASA found that ternet penetration is low com-

lately been under the spot- OTT does not fall in the same pared to other countries where

light. Towards the end of 2018 relevant market as pay-TV, stat- OTT is prevalent, the internet is

the Competition Commission ing that “…the impact of OTT is generally slow, and data is ex-

found that the channel distribu- expected to remain small but pensive compared to countries

tion agreement between SABC noticeable in the foreseeable with high OTT (specifically, Net-

and Multichoice entered into future.”3 flix) penetration.

in 2013 amounted to a notifi-

able merger1. The sector has Competition economists often To examine the price aspect

also received attention from the rely on the SSNIP test4 to de- in the decision between pay-

communications regulator, In- fine the relevant market, but in TV and OTT services, we com-

dependent Communisation Au- markets that are already highly pare the monthly cost of a pay-

thority of South Africa(‘ICASA’), concentrated the SSNIP test TV subscription with the total

who initiated an Inquiry into could indicate a larger relevant cost of OTT. While it is easy to

Subscription Television Broad- market than is truly the case – think that consumers must only

casting Services. Later this we consider this in Section 2.2. weigh up the cost of the pay-

month the largest provider of Since ICASA estimates Mul- TV subscription and OTT sub-

subscription broadcast services tichoice holds a 98% market scription, they must in fact also

– Multichoice – will list on the share of subscription television take into account the cost of

Johannesburg Stock Exchange broadcasting homes5, it is nec- internet access that is suitable

(‘JSE’)2. essary to rely on a broader set for streaming when calculating

of data to determine whether the total cost of OTT. Even with

In addition to Multichoice, pay-TV and OTT are in the same the conservative assumptions

which owns DStv, pay-televi- relevant market. made in our comparison, we

sion providers in South Africa find that apart from DStv Premi-

include Kwesé/Econet, StarSat, When deciding between pay- um and Deukom subscriptions,

Deukom and OpenView HD. TV and OTT, consumers con- the total cost of OTT for various

Whether or not pay-TV (e.g. sider aspects such as price and combinations of OTT subscrip-

Multichoice’s DStv) and over- content, amongst others. This tions and internet packages are

the-top services (‘OTT’) (e.g. Occasional note focuses on the generally higher than pay-TV

Netflix) forms part of the same de facto price that consumers bouquets. There will therefore

1. https://www.businesslive.co.za/bd/national/2018-11-11-new-twist-emerges-in-sabc-multichoice-saga/

2. https://mybroadband.co.za/news/business/292966-multichoice-group-releases-pre-listing-statement.html

3. Discussion Document: Inquiry Into Subscription Television Broadcasting Services, published under Notice 642 of 2017 in Government Gazette

No. 41070 dated 25 August 2017. (para 4.9.1 – 4.9.5)

4. Small but Significant Non-transitory Increase in Price (‘SSNIP’).

5. Discussion Document: Inquiry Into Subscription Television Broadcasting Services, published under Notice 642 of 2017 in Government Gazette

No. 41070 dated 25 August 2017. (para 4.3.5)

2

Occasional Note

February 2019

be households that would not that consumers consider pay- other countries. Nonetheless,

substitute their pay-TV subscrip- TV and OTT as complementary the experience in other coun-

tion with an OTT subscription products, rather than substi- tries provides context for under-

in the event of a pay-TV price tutes. In addition, it is expected standing the local market.

increase. that in the short-term South Af-

rica’s internet penetration – and In the UK the total number of

Many households already have particularly broadband access – subscriptions to Netflix, Amazon

internet access. The compari- will remain low relative to other and NOW TV recently for the

son of substituting pay-TV and countries with OTT, excluding first time exceeded the number

OTT, however, is still not only some consumers from substitut- of subscriptions to traditional

between the monthly subscrip- ing pay-TV with OTT. pay-TV services. The growth

tion costs. This is because some in video-on-demand is helped

of the households considering A final point to note but which by the growth in the number

the switch will have to upgrade is not explicitly dealt with in of devices connected to the

to viewing devices that are this study, is that the type of internet and more people hav-

more suited to watching con- content may also play a role in ing access to faster broadband

tent, upgrade to faster internet, consumer switching behaviour. speeds; in 2018, 44% of house-

and/or higher data allowances, Some content can be classified holds with a TV had a smart TV

all of which will increase their as ‘must-have’ or premium con- or a television connected to the

monthly cost from what it is cur- tent, and in ICASA’s Discussion internet in a different way (e.g.

rently. Document included e.g. live set-top box or games console)

sports. As long as broadcasters and in 2017, 80% of homes

We conclude that pay-TV and own the exclusive rights to such had a fixed broadband con-

OTT in South Africa are current- content, there will be a portion nection. Nonetheless, 71% of

ly in separate relevant markets of consumers that will not sub- those with an OTT subscription

from a competition assessment stitute pay-TV with OTT content. also had a pay-TV subscription,

perspective. The television mar- This emphasises our findings in indicating that consumers see

ket is evolving, however, and it the remainder of this study that the products as complements,

may be that pay-TV and OTT OTT and pay-TV services are of rather than substitutes. Many

may start competing in future. a complementary nature and more OTT subscribers reported

As pointed out when the April not explicitly substitutes. cord-shaving7 (36%) than cord-

2017 Broadcast Research Coun- cutting8 (14%), further empha-

cil of South Africa Television 2 Economic theory and sising that viewers do not deem

Audience Measurement (‘BRC context the products to be substitutes.9

TAMS’) panel universe update

was presented, South Africa’s 2.1 Global and local context A survey of over 140 senior

television landscape is currently television industry participants

about ten years behind Europe.9 As shown later in this note, the from 48 countries found that

Even so, survey data from the South African television market the overall consensus among

United Kingdom (‘UK’) indicate is very different from that of respondents is that, for the time

6. https://themediaonline.co.za/2017/04/the-tv-waiting-game-is-it-necessary/

7. ‘Cord-shaving’ refers to the practice of pay-TV subscribers downgrading to a cheaper bouquet.

8. ‘Cord-cutting’ refers to the practice of pay-TV subscribers cancelling their subscription.

9. Ofcom. (July 2018). Media Nations: UK 2018. Available:

https://www.ofcom.org.uk/__data/assets/pdf_file/0014/116006/media-nations-2018-uk.pdf (p. 13, 16,18)

3

Occasional Note

February 2019

being, pay-TV and OTT are com- to constrain the behaviour of ing they are DStv subscribers

plementary, with consumers subscription television services are also subscribed to Netflix,

likely to sign up for both pay- in the short to medium term.”12 compared to 29% who are not

TV and OTT rather than seeing Econet/Kwesé also agrees with subscribed to any OTT service

them as direct substitutes. The ICASA, stating that “[g]iven the (45% of DStv subscribers are

respondents noted that they niche offering of VOD [video- also subscribed to Showmax,

believe OTT will become more on-demand] services and other although this result is likely in-

important relative to traditional limitations that are characteris- fluenced by the discounts on

pay-TV in the future, with 33% tic to the South Africa market Showmax offered to certain

of respondents expecting that (such as low internet penetra- DStv subscribers).16

pay-TV and OTT will “mostly ad- tion, large price differentials be-

dress the same market, but with tween premium subscription 2.2 Suitability and SSNIP

complementary content offer- bouquets and OTT services, test

ings”.10 and bundled content offerings),

it is reasonable to conclude that As a starting point of the eco-

The South African market is very pay television and OTT services nomic analysis, it must be

different from other markets fall in distinct relevant product considered whether the two

with high OTT penetration. As markets.”13 products can be considered

stated before, based on South substitutes. This can be exam-

Africa’s limited internet penetra- Multichoice, on the other hand, ined from the supply-side as

tion, low internet speed and high does not agree. It states that “… well as the demand-side. Sup-

cost of data, ICASA found in its at the retail level, the relevant ply-side substitution considers a

Discussion Document that OTT market is the electronic audio- supplier’s reaction in response

does not fall in the same prod- vision services market. In this to a change in the relative pric-

uct market as pay-TV. ICASA market traditional Pay TV op- es of two products, taking into

concludes that “…the impact of erators compete with OTT serv- account that two products are

OTT is expected to remain small ices, as well as FTA TV…”14 supply-side substitutes if the

but noticeable in the foresee- supplier of one of the products

able future.”11 In their response A 2018 survey of 9,857 My- already owns all of the impor-

to the Discussion Document, Broadband readers and forum tant assets needed to produce

the Competition Commission members15 shows that many of the other product and has the

similarly notes that “…the emer- these South African consum- commercial incentives and ca-

gence of alternative broadcast ers regard pay-TV and OTT as pabilities to commence produc-

platforms such as internet-based complementary rather than sub- tion of the other product. De-

television does not appear likely stitutes: 52% of those indicat- mand-side substitution consider

10. Digital TV Europe in association with Conviva. (2015). Pay TV and OTT: Partners of competitors. Available:

https://www.digitaltveurope.com/files/2015/09/Conviva-Survey-Aug15v21.pdf (p. 9)

11. Discussion Document: Inquiry Into Subscription Television Broadcasting Services, published under Notice 642 of 2017 in Government Gazette

No. 41070 dated 25 August 2017. (para 4.9.1 – 4.9.5)

12. Competition Commission of South Africa. (19 December 2017). Competition Commission comments on the Discussion Document for the inquiry

into subscription television broadcasting services (para 7.1)

13. Econet Media Limited/Kwesé (4 December 2017) Submission by Econet Media Limited on the Authority’s Discussion Document: Inquiry into

subscription television broadcasting services (para 5.9.5)

14. Multichoice (4 December 2017) Submission on the Discussion Document (Non-confidential version). (para 28)

15. The sample is therefore biased towards those more knowledgeable about the television and streaming industry.

16. https://mybroadband.co.za/news/it-services/263061-the-most-popular-netflix-package-in-south-africa.html

4

Occasional Note

February 2019

whether consumers switch from OTT, or vice versa, in response market power, there is a high

one product to another in re- to a change in the relative prices probability that prices in the

sponse to a change in the rela- of the two products. This note relevant product market have

tive prices of the products.17 will focus on the demands-side already been increased to mo-

substitution of a pay-TV sub- nopoly levels. At such high

In the context of pay-TV and scription with OTT. For consum- prices, products that are not

OTT, supply-side substitution ers substitution of pay-TV with substitutes and therefore do not

takes place if a pay-TV provider OTT services is easier since, un- form part of the same relevant

switches to supplying an OTT like the reverse, consumers do market, could appear to be sub-

platform instead, or vice versa. not need to acquire and install stitutes.

Practically, however, there is infrastructure (e.g. satellite dish

effectively unidirectional substi- and/or decoder). The SSNIP test would then in-

tution: OTT providers are very dicate a larger product market

unlikely to have the necessary Turning to the to specific mar- than is truly the case. Multi-

infrastructure (such as satellites) ket definition, the SSNIP test is choice’s perceived dominance

in place to be able to provide typically used as a point of de- of the local pay-TV market

pay-TV services at short notice. parture to identify if products or means that one cannot rely

On the other hand, is it much services fall within the same rel- solely on the SSNIP test to de-

easier for pay-TV suppliers to evant market. This test defines termine whether pay-TV and

provide OTT services. In fact, the relevant market by determin- OTT are in the same market.

many suppliers already offer ing whether a given increase in This note therefore turns to

some variant of it alongside prices (typically 5-10%) would measures such as internet pen-

their traditional pay-TV services; be profitable for a hypotheti- etration, whether enough peo-

in South Africa Multichoice of- cal monopolist in the candidate ple have access to high-speed

fers DStv Now and Showmax market. If the price increase internet sufficient to view OTT

alongside their satellite pay-TV causes a sufficient number of content, and a comparison of

services. While substitution in consumers – in this case, sub- the costs of pay-TV and OTT

this direction may be easier than scribers – to switch to substitute subscriptions.

the reverse, it does pose chal- products and thereby makes

lenges. Multichoice has indicat- the price increase unprofitable 3 South Africans consume

ed that while it plans to launch a for the hypothetical monopolist, content television sets

standalone streaming package the products are considered to rather than internet-

in 2019, securing the rights to be in the same market. enabled devices

all of the entertainment content

it offers on the DStv packages The SSNIP test however needs It is important to understand

has been an obstacle.18 to be applied with caution in which devices South Africans

highly concentrated markets use to access content since

Demand-side substitution takes due to what is known as the this will influence whether they

place if a consumer switches cellophane fallacy: where there watch broadcast or OTT con-

from a pay-TV subscription to is an incumbent provider with tent, or both.

17. Bishop, S. and Walker, M., 2010. The economics of EC competition law: concepts, application and measurement (Vol. 188). London: Sweet &

Maxwell.

18. https://mybroadband.co.za/news/broadcasting/258313-dstv-working-on-streaming-only-package-to-take-on-netflix.html ;

https://mg.co.za/article/2018-05-15-multichoice-to-launch-a-dstv-streaming-only-service-in-2019

5

Occasional Note

February 2019

Figure 1 indicates that televi- Figure 1: Viewing device for consuming content (2017)

sion sets remain the most pop-

ular device on which to watch

content.19 In contrast, devices

which require access to the

internet to view content, e.g.

smartphones, tablets, laptops,

etc., are used at a much lower

frequency. The possibility exists

that the survey results on televi-

sion sets include internet ena-

bled televisions which would al-

low for OTT content. While 9%

of households reported having

an internet-enabled television Source: The Broadcast Research Council of South Africa (BRC): The Establish-

set and only 2% of households ment Survey, October 2017 Release

reported using this functionality.

20 Figure 2: Technology in households (2016)

A crucial factor in determining

whether households are able to

switch from pay-TV to OTT con-

tent is whether a household has

the necessary internet-enabled

device and internet access. Fig-

ure 2 shows that a larger pro-

portion of households have a

cellphone than a television set.21

However, as was shown in Fig-

ure 1, a smartphone was only

used in 8% of the cases when

television content was con-

sumed. More relevant is that a

larger proportion of households Source: International Telecommunications Union (‘ICT’): Core household indica-

tors

have a television set than have

internet access at home22 (since or someone else’s home23), a to have an ADSL/DSL internet

98% of BRC respondents report computer24, or a fixed telephone connection. Few households

watching television at their own line25 that would allow them are therefore able to substitute

19. Respondents were allowed to pick more than one device if it was applicable, hence the total does not add up to a 100%.

20. The Broadcast Research Council of South Africa (BRC): The Establishment Survey, October 2017 Release.

21. Defined as a device capable of receiving broadcast television signals, using popular access means such as over-the-air, cable and satellite.

22. Using any device, on a mobile or fixed network.

23. BRC: The Establishment Survey, October 2017 Release.

24. A desktop, laptop or tablet.

25. A telephone line connecting a customer’s terminal equipment to the public switched telephone network and which has a dedicated port on a

telephone exchange.

6

Occasional Note

February 2019

broadcast content on a televi- Figure 3: Proportion of households with internet access at home (fixed or

sion set with OTT content since mobile) (2017 or latest available)

they do not have the necessary

technology in their households,

in particular internet access.

4 Inadequate internet ac-

cess impedes switching to

OTT

In addition to an internet-ena-

bled device, consumers who

want to stream content over an

OTT platform need an internet

connection, sufficient data, and

a high-speed internet access.

Price is an important part of the

decision whether to sign up for

Source: International Telecommunications Union (ICT): Core household indica-

an internet package that satisfies tors

these conditions. We analyse

these factors in turn, starting Figure 4: Proportion of individuals with fixed broadband subscriptions (2016)

with the availability of internet

(internet penetration), internet

speed and price. These factors

are crucial to understanding

the South African context and

whether consumers are able to

substitute pay-TV with OTT.

4.1 Low internet penetra-

tion

Compared to other countries

where OTT platforms are avail-

able, South Africa has a low in-

ternet penetration rate (56%).

Figure 3 shows that compared

to some of these countries, a

much smaller proportion of

households have internet access

(fixed or mobile) at home. This

suggests that a lack of internet Source: World Bank: World Development Indicators

7Occasional Note

February 2019

access prevents many South Af- Figure 5: Mean download speed (Mbps) (June 2017 – May 2018)

ricans from switching from pay-

TV to OTT.

A MyBroadband Piracy and

Streaming Survey for 2017 re-

ported that 51.5% of 1,587

respondents used ADSL/DSL

to stream content.26 Figure 4

shows some of the top coun-

tries with regards to the propor-

tion of individuals with fixed

broadband subscriptions, as

well as the world average and

the proportion for South Af-

rica. Broadband penetration27

in South Africa is substantially

lower than for the top countries

and falls significantly short of

the world average.

Source: Worldwide broadband speed league 201830

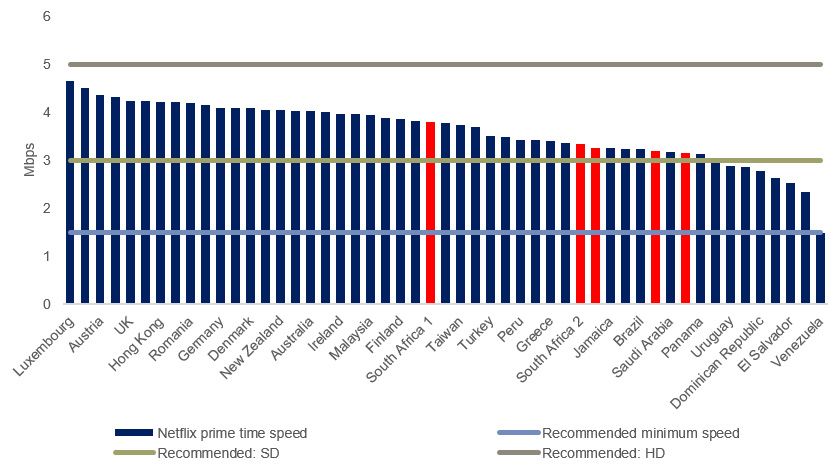

4.2 The internet is slow average (see Figure 5). This is well as Netflix’s minimum rec-

despite it having improved from ommend speed, recommended

4.36 Mbps (Megabits per sec- speed for Standard Definition

For OTT services to act as a ond)28 as measured in June 2016 (‘SD’) streaming and for High

competitive constraint to pay- – May 2017 to 6.38 Mbps.29 Definition (‘HD’) streaming. The

TV, households need internet prime-time speed for South Afri-

access at sufficient speeds. Even Netflix indicates the prime-time can subscribers was just above

households with internet ac- speed for the internet service Netflix’s recommended speed

cess, whether fixed or mobile, providers (‘ISPs’) used by sub- for SD streaming and in most

may not be able to switch to scribers in some countries where cases lower than the fastest

OTT if the internet is too slow. it is active. Figure 6 indicates the speeds available in other coun-

speed for the fastest ISPs for a tries.31

A comparison of the mean selection of countries, the five

download speed of 200 territo- fastest ISPs (specifically for Sep- This indicates that even for those

ries shows that South Africa’s in- tember 2018) used by South households with internet access

ternet speed is below the world African Netflix subscribers, as and who deem their connections

26. https://mybroadband.co.za/news/adsl/228031-favourite-isps-and-internet-connections-of-netflix-users-in-south-africa.html

27. Includes cable mode, DSL, fibre-to-the-home/building, other fixed (wired) broadband subscriptions, satellite broadband and terrestrial fixed wireless

broadband. Excludes subscriptions that have access to data communications via mobile-cellular networks.

28. Based on 2,437,364 stress tests.

29. Notably, the authors of the research caution that while the global average broadband speeds increased by 23% from the previous period, the reality

is that the high increases are concentrated in those countries that already have high internet speeds, whereas those at the bottom end are on the

verge of stagnation.

30. https://www.cable.co.uk/broadband/speed/worldwide-speed-league/

31. A potential reason why the speed of Netflix users are lower than those measured by in Figure 5 is that household internet speeds are generally lower

than those used by businesses, the latter of which are also included in the country-wide measurement.

8Occasional Note

February 2019

fast enough to stream OTT Figure 6: Netflix prime time speed for fastest ISPs in select countries and 5

content, the speed is generally fastest in South Africa (September 2018)

still below that of other coun-

tries with OTT platforms (albeit

slightly above the recommend-

ed speed for SD streaming).

4.3 Internet is expensive

South African households with

fast enough internet access to

stream OTT content may still

be precluded from switching

from pay-TV to OTT platforms

Source: Netflix ISP Speed Index32

due to the cost of data. Figure

Figure 7: Fixed broadband prices as percentage of GNI per capita (2016)

7 and Figure 8 illustrate the cost

of fixed-broadband33 and mo-

bile-broadband34 data in South

Africa compared to 67 other

countries as well as the global

average. It is expressed as a

proportion of average monthly

gross national product (‘GNI’)

per capita, which takes the rela-

tive currency strengths and var-

ying living costs into account. In

both cases, South Africa is sig-

nificantly below the world aver-

age and can be considered low

relative to comparator coun-

tries in Africa and other emerg-

ing markets. However, in the Source: International Telecommunication Union (ITU): Measuring the Informa-

tion Society Report, Volume 2 ICT Country profiles 2017; Note: Refers to the

context of determining whether price of a monthly subscription to an entry-level fixed-broadband plan based on

households will be able to afford a monthly data usage of (a minimum of) 1 GB.

32. https://ispspeedindex.netflix.com/ ; Although Netflix is available in over 190 countries, it does not index the speed in all countries; e.g. South Africa is

the only African country indexed.

33. ‘Fixed-broadband prices’ refers to the price of a monthly subscription to an entry-level fixed-broadband plan. Fixed-broadband prices are based on

a monthly data usage of (a minimum of) 1 GB. For plans that limit the monthly amount of data transferred by including data volume caps below 1

GB, the cost for the additional bytes is added to the sub-basket. The minimum speed of a broadband connection is 256 Kbit/s. Tariffs are collected

from the ISP with the largest market share (as measured by the number of subscriptions). Prices refer to regular (non-promotional) plans and exclude

promotional offers and limited discounts or user groups or any other discounts for services specifically based on type of phone or time of day usage.

34. ‘Mobile-broadband prices 1 GB’ refers to the price of an entry-level computer-based mobile-broadband subscription with a validity of 30 days (or

four weeks). Prices for computer-based mobile-broadband subscriptions are based on prepaid services with a minimum data volume allowance of 1

GB for one of the following technologies: UMTS, HSPA family, LTE family, CDMA EV-DO family and mobile WiMAX (IEEE 802.16e and 802.16m).

Prices applying to WiFi or hotspots are excluded. Tariffs represent prices for residential customers, including taxes, and are based on the cheapest

plan from the operator with the largest market share measured by the number of mobile-broadband subscriptions. Prices refer to regular (non-

promotional) plans and exclude promotional offers and limited discounts or user groups or any other discounts for services specifically based on type

of phone or time of day usage.

9Occasional Note

February 2019

to substitute pay-TV with OTT Figure 8: Mobile broadband prices as percentage of GNI per capita (2016)

to reach the penetration rates

which would allow OTT to be

a credible constraint on pay-TV,

it is more appropriate to com-

pare the local data costs against

the cost in countries with high

OTT penetration rates. For ex-

ample, the three countries with

the highest Netflix penetration

rates are the US, Norway and

Canada.35 As shown in the fig-

ures below, the cost of data in

all three of countries are lower

than in South Africa.36

The lack of adequate internet

access already precludes a por-

tion of the market from substi-

tuting pay-TV with OTT, while

the price of data may hamper Source: International Telecommunication Union (ITU): Measuring the Information

some households. Society Report, Volume 2 ICT Country profiles 2017; Note: Refers to the price of an

entry-level computer-based mobile-broadband subscription with a validity of 30 days.

Prices for computer-based mobile-broadband subscriptions are based on prepaid

5 Pay-TV subscriptions are services with a minimum data volume allowance of 1 GB. The lack of adequate inter-

generally cheaper than the net access already precludes a portion of the market from substituting pay-TV with

OTT, while the price of data may hamper some households.

full price of OTT access

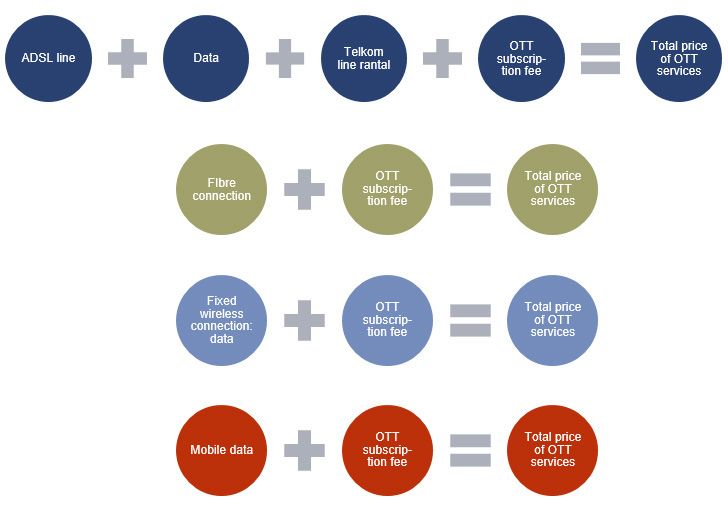

ated with the different options. nologies: ADSL37 (capped and

uncapped), fibre, fixed wireless,

Ultimately consumers can 5.1 Components of the and mobile data.

be expected to weigh up the price of accessing OTT

choice between the price of a The price of each of the com-

pay-TV subscription and the to- ponents needs to be added to-

tal price of OTT before deciding To access OTT content, users gether to find the total price of

to switch from one to the other. need an OTT subscription, in- watching OTT content.

ternet access and data. In the

A large study would be needed case of ADSL, a Telkom line is Our comparison uses conserva-

to accurately calculate the price also necessary. Figure 9 sets tive values and assumptions. For

elasticity of demand, but this outs the cost components for each of the four ways in which

section provides a conservative watching OTT content using to access the internet, the ISP

comparison of the prices associ- the different connection tech- and offering with the lowest

35. https://www.businessinsider.com/netflix-countries-most-popular-user-penetration-2018-7?IR=T#2-norway-624-user-penetration-9

36. In fact, the cost of data cheaper in all countries making up the top ten with the highest Netflix penetration rates: the US, Norway, Canada, Denmark,

Sweden, the Netherlands, Australia, Finland, Germany and the UK.

37. Asymmetric Digital Subscriber Line.

10Occasional Note

February 2019

price were chosen. This does Figure 9: Components of total price of OTT service for ADSL, fibre, fixed wire-

not necessarily amount to the less and mobile data access

best value for money; the price

per gigabyte (‘GB’) of data, for

example, generally decreases

as the size of the data-bundle

increases. The aim of the com-

parison, however, is to show a

reasonable minimum total price

that users need to pay for ac-

cess to OTT content.

We therefore use a download

speed of 4 Mbps, considered

the minimum speed for stream-

ing. For internet packages

where the data is capped, we

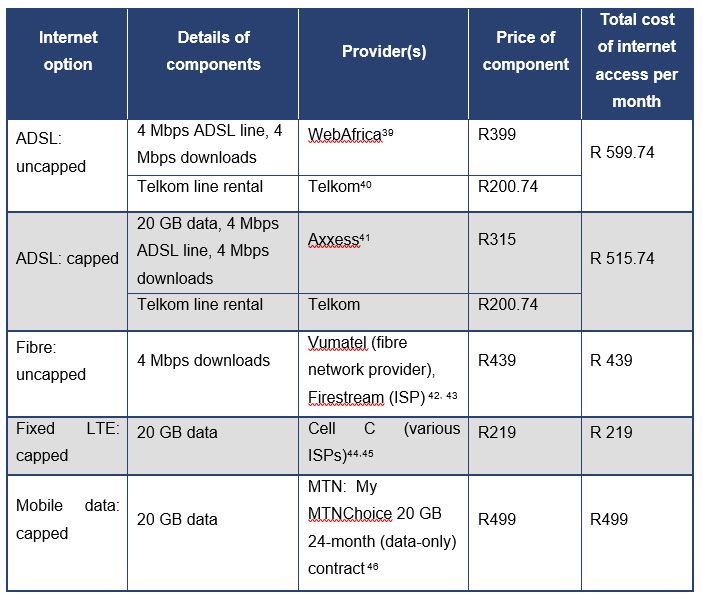

use a cap of 20GB since this Table 1: Total monthly cost of internet access

is the smallest ADSL cap of-

fered by most ISPs. To put his

into perspective, Showmax esti-

mates that 6 hours of streaming

per week with medium band-

width capping (medium video

quality) will use 18.1 GB of data

per month.38

Table 1 summarises the internet

options used in the comparison.

Excluded from these options are

the installation and setup costs,

as well as devices (for example

a router). This is because these

are once-off costs, and some

ISPs provide the router for free,

on the condition it be returned

when the consumer leaves the

38. https://www.showmax.com/eng/bandwidth-calculator

39. https://www.webafrica.co.za/adsl/ (Accessed 23 November 2018)

40. https://secure.telkom.co.za/today/shop/plan/landline/

41. https://www.axxess.co.za/dsl/capped (Accessed 23 November 2018) We use the Premium uncapped option rather than the cheaper Home un

capped option since the Premium option is described as “…custom built for the power user to allow unlimited streaming…”

42. Fibre network providers (or infrastructure providers) and ISPs work together to provide internet access via fibre. While fibre is not yet available in all

South African neighbourhoods, coverage is expanding.

43. https://shop.vumatel.co.za/packages/all (Accessed 26 November 2018)

44. ISPs make use of mobile service providers’ LTE infrastructure. As such, WebAfrica and Afrihost, amongst others, make use of Cell C’s LTE

infrastructure to offer LTE at Home.

45. https://www.webafrica.co.za/lte/?gclid=CjwKCAiA0O7fBRASEiwAYI9QAqu_WG31UjMb8fIkxAuhQx-TCP4oe4P0M9vTWyfO_gDcaLH

GadnGcBoCddAQAvD_BwE (Accessed 26 November 2018)

46. https://www.mtn.co.za/Pages/My-MTNChoice-20GB.aspx?ptype=high (Accessed 26 November 2018)

11Occasional Note

February 2019

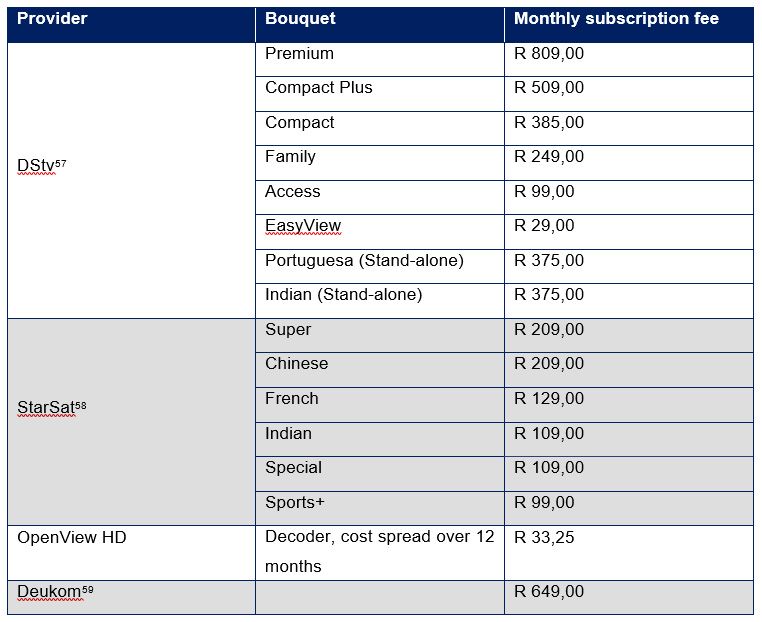

specific ISP. not charge monthly subscrip- decoder at R399.55,56, Since

tion fees, but instead sells their there are no monthly subscrip-

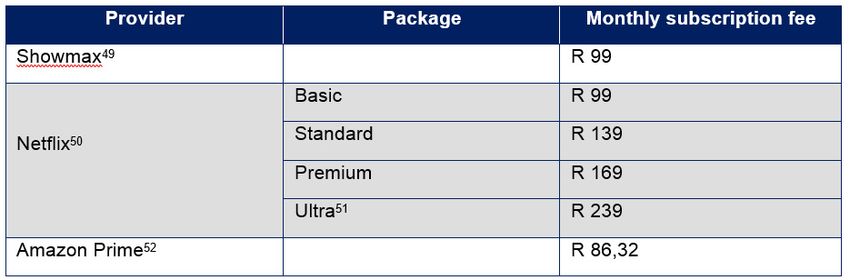

Finally, the subscription fees personal video recorder (PVR) tion fees, we assume that the

for the main OTT platforms in Table 2: OTT monthly subscription fees

South Africa is set out in Table

2. Amazon Prime is billed in

USD, but the monthly cost of

USD 5.99 is converted to ZAR

for the purposes of the analy-

ses47. The monthly subscription

fees shown are after the lower

“introductory prices”, free trials

and discounts.48

Table 3: Monthly subscription fees of pay-TV

Per example, the total monthly

cost of OTT for a household

with uncapped ADSL and a

Netflix Basic subscription will

be calculated as R599.74 for

internet access plus R99 for the

Netflix subscription, for a total

cost of R698.74 per month.

5.2 Price of pay-TV subscrip-

tions

Table 3 sets out the monthly

subscription fees for the differ-

ent bouquets from South Afri-

can pay-TV providers.53 In the

case of DStv, the prices are for

the regular monthly subscrip-

tion.54 OpenView HD does

47. Based on an exchange of 1 USD = R 14.41 (as at 13 November 2018).

48. For example, Showmax is offered at R49 to DStv Compact and Compact Plus subscribers.

49. https://www.showmax.com/eng/dstv (Accessed 13 November 2018)

50. https://www.netflix.com/za/#this-is-netflix (Accessed 14 November 2018)

51. Newly launched in South Africa in November 2018. (https://mybroadband.co.za/news/internet/284536-netflix-launches-new-ultra-package-in-south-

africa-for-r239-pm.html?source=newsletter )

52. https://www.primevideo.com/?ref_=dvm_pds_amz_ZA_kc_s_g|c_231876465301_m_WXma1FyZ-dc_s__ (Accessed 13 November 2018)

53 https://selfservice.dstv.com/products; http://www.openviewhd.co.za/faq/; http://starsat.co.za/packages/;

https://www.deukom.co.za/angebote.php Accessed 20 March 2018.

54. In contrast to the DStv Price Lock option for the DStv Premium bouquet since this also includes a decoder (DStv Explora 2), DStv WiFi connector

and installation in addition to the monthly subscription.

(https://www.dstv.com/commerce/paymentplan/pricelock)

55. https://www.thesouthafrican.com/what-you-need-to-know-about-openview-and-its-open-pvr-capabilities/ (Accessed 13 November 2018)

56. Users also need a satellite dish to watch OpenView HD content, but may use their existing dish.

57. https://self-service.dstv.com/compare-packages/ (Accessed 13 November 2018)

58. http://starsat.co.za/packages/ (Accessed 13 November 2018)

59. https://www.deukom.co.za/angebote.php (Accessed 13 November 2018)

12Occasional Note

February 2019

cost of the decoder is distribut- est OTT subscription, namely on pay-TV.

ed over 12 months, i.e. R33.25 Amazon Prime at R86.32 per

per month. For Deukom the month. Also indicated is the av- 5.3.2 Pay-TV subscriptions are

12-month contract with monthly erage monthly expenditure on generally cheaper than a ‘typi-

payments was selected in order pay-TV in 2018 of R313.4760 as cal OTT combination’

to be comparable to the other calculated by PwC (red bar).

providers (with the exception of As stated above, our compari-

OpenView HD, as explained). In the case of OTT, a conserva- son uses conservative assump-

tive approach was used, e.g. by tions in the case of the internet

In addition to the monthly sub- choosing the cheapest rather packages as well as OTT sub-

scription fees, pay-TV consum- than the most popular Netf- scriptions. To provide a more

ers also need a television set, lix option. Nonetheless, even realistic picture and provide

satellite dish and decoder as when these lower cost internet further context, we now also

well as the initial installation of and OTT subscriptions are used, consider the total monthly price

the devices in order to watch the total cost of OTT is higher of a ‘typical OTT combination’

the pay-TV content. Since these than most pay-TV bouquets. compared to the cost of pay-

are once-off costs, it is not in- With the exception of the com- TV bouquets. We see that the

cluded in the calculation, except bination of Amazon Prime and ‘typical OTT combination’ is

in the case of OpenViewHD, as Fixed LTE (with a 20 GB cap), more expensive than all pay-TV

explained above. all the OTT packages cost more packages, with the exception

than the average expenditure of DStv Premium. This already

5.3 Comparison of pay-TV

and OTT prices Figure 10: Total cost of OTT and pay-TV (2018)

5.3.1 Pay-TV subscriptions are

generally cheaper than the full

price of OTT access using dif-

ferent internet access options

Figure 10 compares the total

price of OTT (blue) and the sub-

scription fees of pay-TV (green).

In the case of OTT, the total cost

for Showmax and the cheapest

Netflix package available (Netf-

lix Basic) – both priced at R99

per month – are shown for each

internet package as described

in section 5.1 (capped and un-

capped ADSL, uncapped fibre,

fixed wireless and mobile data).

This is repeated for the cheap- Source: Providers’ websites (Accessed November 2018); Econex calculations

60. PwC Entertainment and Media Outlook 2017.

13Occasional Note

February 2019

indicates that OTT is generally tween 10 and 20 hours per per month. Rounding down to

the more expensive option rela- week and 19% watched more 20 GB for ease of use indicates

tive to pay-TV. than 20 hours per week.68 Ac- that a ‘typical’ viewer requires

cording to Netflix, watching an internet package of at least

The ‘typical OTT combination’ one hour of content at medium 20GB.

is constructed based on the re- quality (standard definition)

sults of the MyBroadband 2018 uses 0.7GB of data. Assuming Combining this information, a

DStv and Netflix survey.61 Of an average of 7.5 hours69 per ‘typical OTT combination’ of the

the 9,857 respondents, 65% week results in usage of 21 GB most popular option for OTT

are subscribed to Netflix.62 Of

these Netflix subscribers, 42% Table 4: Breakdown of prices for ‘typical OTT combination’

are subscribed to the Standard

package, 41% to the Premium

package and 15% to the Basic

package.63,64

According to the 1,587 ‘IT pro-

fessionals and tech-savvy indi-

viduals’ – i.e. individuals who Figure 11: Monthly price of ‘typical combination’ versus pay-TV subscription

are expected to be relatively (2018)

knowledgeable about the inter-

net and television markets – that

responded to MyBroadband’s

Piracy and Streaming Survey for

2017, 52% used ADSL to ac-

cess a streaming service.65 More

specifically, 23% use Telkom for

their streaming service.66,67

In the 2018 DStv and Netflix

survey, 26% of all respondents

(regardless of their OTT plat-

form) watched between 5 and

10 hours of streaming content

per week, 24% watched be-

61. https://mybroadband.co.za/news/it-services/263061-the-most-popular-netflix-package-in-south-africa.html

62. In second place is Showmax at a much lower 38%, while 23% of respondents are not subscribed to any OTT content.

63. The remaining 2% are unsure to which Netflix package they are subscribed.

64. At the time of the survey Netflix Ultra was not yet available.

65. In second place is Openserve Fibre, which is used by only 11.82%

66. https://mybroadband.co.za/news/adsl/228031-favourite-isps-and-internet-connections-of-netflix-users-in-south-africa.html

67. Followed by Afrihost at a much lower 16.50%.

68. https://mybroadband.co.za/news/it-services/263061-the-most-popular-netflix-package-in-south-africa.html

69. In other words, the average of the category (5 to 10 hours per week) most respondents selected.

70. https://www.netflix.com/za/#this-is-netflix

71. https://secure.telkom.co.za/today/shop/home/plan/faster-adsl/ (accessed 13 November 2018)

72. https://secure.telkom.co.za/today/shop/plan/softcap/ (accessed 13 November 2018)

73. https://secure.telkom.co.za/today/shop/home/plan/plan-variation-landline/ (accessed 13 November 2018)

14Occasional Note

February 2019

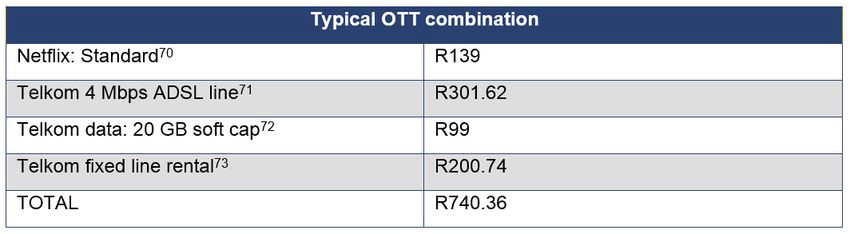

packages and streaming consist Figure 12: Internet penetration in South African households (2013 – 2022)

of a Netflix Standard subscrip-

tion, ADSL from Telkom with an

ADSL line of 4 Mbps and 20GB

of data, and fixed line rental

from Telkom.

A comparison of the combina-

tion typically used by South

Africans to watch OTT, while

conservative, shows that OTT is

more expensive than all pay-TV

subscriptions, with the excep-

tion of DStv Premium.

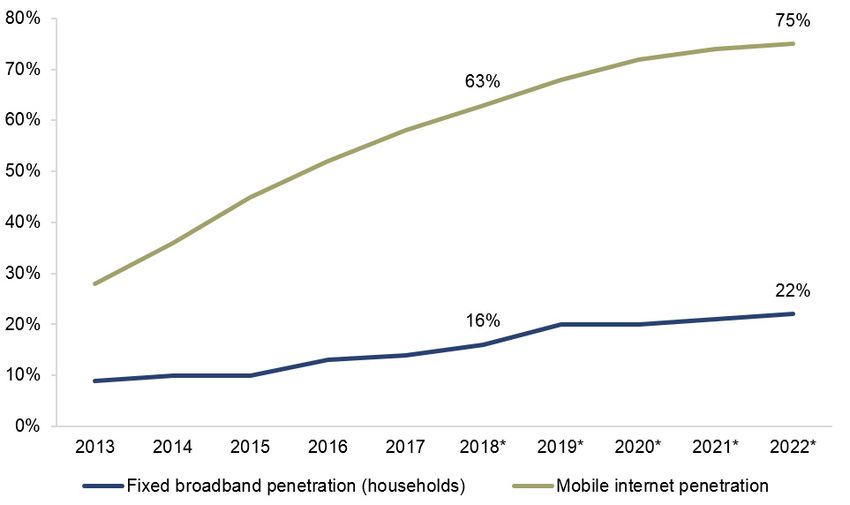

6 Internet access and costs Source: PwC Entertainment and Media Outlook: 2018-2022; * indicates esti-

mates

expected to remain pro-

hibitive in the future Figure 13: Average monthly spending on pay-TV

Policy should be forward look-

ing. The data presented in the

previous sections all refer to the

South African situation as it is

now. It is argued, however, that

in the foreseeable future, sub-

stitution of pay-TV with OTT is

expected to remain limited and

they will, for now, remain in

separate markets.

Source: PwC Entertainment and Media Outlook 2017; * indicates estimates

As shown in Figure 12, fixed Both the Competition Commis- before the effect on data prices

broadband74 access by house- sion of South Africa and ICASA – and therefore the total price

holds is expected to remain are investigating the data serv- of OTT – would potentially be

relatively low. While mobile ices market.75,76 This may po- felt by consumers.

internet access is expected to tentially bring about a decline in

increase significantly, it is still the cost of data. In addition, South Africans’ av-

much lower than the levels of erage monthly expenditure on

internet penetration seen else- Since both of these processes pay-TV is expected not to in-

where in the world where OTT are still ongoing, however, it will crease substantially, as illustrat-

platforms are prevalent. be at least a couple of months ed in Figure 13, with the effect

74. Includes fibre, LTE and ADSL connections.

75. http://www.compcom.co.za/data-market-inquiry/

76. https://www.icasa.org.za/legislation-and-regulations/inquiries/priority-markets-inquiry

15Occasional Note

February 2019

that it is likely to remain below OTT combinations that satisfy with the exception of DStv Pre-

the total price of OTT. As argued these conditions that takes the mium.

before, the combination of low total price of OTT into account,

broadband penetration and i.e. the OTT subscription (Show- It can be argued that for those

high internet prices make it like- max, Netflix Basic or Amazon households that already have

ly that there will be consumers Prime), internet access, data internet access, the addition-

unable to substitute pay-TV with and Telkom fixed line rental, if al expense of switching from

OTT in the future due to a lack necessary. These combinations pay-TV to OTT is only the OTT

of internet access and/or higher are all based on conservative as- subscription (while possibly si-

total price of OTT. Pay-TV and sumptions. multaneously cancelling their

OTT are therefore expected to pay-TV subscription and saving

remain in separate relevant mar- The total prices of these OTT that money). However, some

kets in the short term. combinations are compared of the households with internet

to the price of monthly pay-TV access will currently not have a

subscriptions for different bou- connection that is fast enough,

7 Conclusion quets. We find that even when sufficient data and/or only have

these lower price internet and access to internet via a “non-

OTT subscriptions are used in optimal” device for watching

This note considers whether the comparison, the total cost content, such as a smartphone

pay-TV and OTT services are of OTT is higher than most pay- with a small screen.

in the same relevant market in TV bouquets.

South Africa. Survey evidence For these households the choice

in South Africa and the UK sup- In addition, only one of the con- to switch from pay-TV to OTT

port the notion that consum- structed combinations (Amazon entails weighing the price of the

ers currently deem pay-TV and Prime and Fixed LTE with a 20 pay-TV subscription against the

OTT content as complementary GB cap) cost more than South price of an OTT subscription as

products rather than substitutes. Africans’ average expenditure well as upgrading to faster inter-

on pay-TV in 2018. In general, net, more data and/or buying a

In South Africa’s pay-TV mar- then, some households may not new device to watch the OTT

ket where smaller providers are be willing to substitute the rela- content on. It is possible that

eclipsed by DStv, one must be tively cheaper pay-TV with OTT. some of these households will

wary of a blanket SSNIP test ap- not be willing to incur the ad-

proach to define the relevant Since the first comparison is ditional expenses necessary to

market. We therefore turn to conservative, we construct a substitute their pay-TV subscrip-

evidence beyond the SSNIP ‘typical combination’ of OTT tion with OTT.

test to answer the question at subscription and internet access

hand. We compare the price of based on survey information’ Regulation must be forward-

a pay-TV subscription to the to- that indicate the OTT subscrip- looking. Projections, however,

tal price of OTT. To access OTT tion and internet access the show that internet penetration

platforms, it is necessary that most respondents report using. in South Africa is not expected

the consumer has internet ac- to increase to levels compa-

cess, enough data and that the The total price of the ‘typical rable to other nations where

internet download speed is high combination’ is more expensive OTT are prevalent within the

enough. We construct a set of than all pay-TV subscriptions, next few years. While there is

16Occasional Note

February 2019

a movement towards lowering ers in a couple of months, if at term, pay-TV and OTT cannot

data prices, this is expected to all. We conclude that based on be considered to be in the same

only filter through to consum- these constraints, in the short relevant market.

admin@econex.co.za

+27 21 887 5678

Stellenbosch

+27 21 887 5678

76 Dorp Street

Stellenbosch

7600

7You can also read