ASEAN Strategy Virtual ASEAN Conference 2020 - Macquarie Group

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Macquarie Research | EQUITIES

ASEAN Strategy

Virtual ASEAN Conference 2020

Jayden Vantarakis

Macquarie Securities (Singapore) Pte Ltd

+65 6601 0916

Jayden.Vantarakis@macquarie.com

August 2020

In preparing this research, we did not take into account the investment objectives, financial situation and particular

needs of the reader. Before making an investment decision on the basis of this research, the reader needs to

consider, with or without the assistance of an adviser, whether the advice is appropriate in light of their particular

investment needs, objectives and financial circumstances. Please see disclaimer.

Macquarie Research | EQUITIES

ASEAN Strategy

Pivotal themes and questions for ASEAN

• Reopening or further lockdowns?

• Continuing to mitigate a recession with stimulus, how much can be done?

• Will the spill over of China supply chains come or will it be reshoring direct to DMs?

• Political risks – Thailand and Malaysia in focus for now

• Ongoing digitization of the consumer and new business models

PAGE 2

Macquarie Research | EQUITIES

ASEAN Strategy

Market valuations and ratings – Philippines and Singapore presenting opportunities

Singapore and Philippines at average PEs Big recovery in Malaysia and Indonesia

%

x

60.0

20.0

50.0 45.8

17.9 18.6

18.0 17.8 40.0

29.9 29.6

15.7 16.4 16.1 30.0 23.4

16.0 15.8 16.7

15.4 20.0

14.0

14.0 14.0 10.0

-

12.0 13.3

12.8 -10.0 -1.6

12.0

10.0 -20.0

-16.6

-30.0 -20.5 -22.6 -20.2

9.6

8.0 8.9 -40.0

6.0 -50.0

Singapore Philippines Indonesia Thailand Malaysia Singapore Philippines Indonesia Thailand Malaysia

+/-1 std-dev Average Trading Correction Recovery Ytd

At the stock level, individual ratings Philippines Most bottom-up upside Singapore

%

100

14 13

90 24 25 21

25

80 7

28

70 12 17

15

22

60

50

40 79

30 65 60 59 62

53

20

10

-

Philippines Indonesia Malaysia Singapore Thailand Total

Outperform Neutral Underperform

Source: Gov’t of Singapore, Macquarie Research PAGE 3Macquarie Research | EQUITIES

ASEAN Strategy

Singapore support measures tapering through re-opening

• Suburban and downtown mall traffic at 60-80% and 40-55% of pre-COVID levels

• Office utilisation remains relatively low at 10-30% due to work from home

• Domestic ‘stay-cations’ an attempt at driving up hospitality sector

• Opening up borders? China for business, Malaysia protocol being determined

S$101b Covid-related support (~21% GDP) Job-support scheme levels to taper

S$b %

120 80%

70%

100

60%

80

50%

60 40%

30%

40

20%

20

10%

0 0%

Covid-related fiscal support announced Food/Hospitality Aviation/Tourism Others

Source: Gov’t of Singapore, Macquarie Research PAGE 4Macquarie Research | EQUITIES

ASEAN Strategy

Singapore Elections – Opposition did well at the polls

• 8.6ppt swing away from the ruling Peoples’ Action Party (PAP) with the opposition

winning 3 constituencies and 10% of the Parliament’s seats

• A referendum on the 4th Generation of PAP leaders, including Deputy PM Heng

Swee Keat who is expected to take the helm this term

• Job security, cost of living, housing and welfare key issues

PAP Popular vote at 61.2% Opposition seats in Parliament

% seats

90 12 12%

10 10%

80 10

8 8%

69.9

70 6 6%

6 6

4 4%

60 61.0 61.2

60.1 2 2%

2 2

50 0 0%

1968 1972 1976 1980 1984 1988 1991 1997 2001 2006 2011 2015 2020 2001 2006 2011 2015 2020

PAP popular vote Opposition seats % Parliament (RHS)

Source: Gov’t of Singapore, Macquarie Research PAGE 5Macquarie Research | EQUITIES ASEAN Strategy Singapore – High conviction ideas DBS (DBS SP) • Strong deposit flows, Singapore benefiting relative to Hong Kong. • Potential to parlay into wealth or property investment in coming periods • Ahead of the curve on provision charges and reserving levels vs peers. Negatives in the price • Trading at 1x P/B. Attractive for a franchise able to deliver c. 11% RoTE Frasers Logistics and Commercial Trust (FLT SP) • Logistics a strong thematic to localisation and re-shoring of supply chains • Trades at a wider discount to peers, including MLT, at 0.5x P/B differential • 21% upside, including 5.6% yield. Catalysts are sponsor pipeline asset injections in EU/UK/AU UOL Group (UOL SP) • Redevelopment opportunities, incrementally attractive in a down market • Trading close to insider buying levels with the controlling Wee family accumulating recently • S$8.85 target (35% upside) based on 35% RNAV discount Dairy Farm (DFI SP) • Turnaround play on SE Asia Groceries improving margins. Own brand roll out gathering pace • Levered to a reopening of Hong Kong to Mainland China tourists. • Growth from 7Eleven store roll out in China as well • Core business trading at

Macquarie Research | EQUITIES

ASEAN Strategy

Malaysia – Enjoy the liquidity but mind the gaps

• Economic data to remain weak, but as long as narrative for 2021 remains intact, expect buoyant close into

year end and 1H21. End 2020 KLCI target of 1,648.

• We are looking for 3.1% GDP decline in 2020 with 5.5% growth in 2021 vs BNM’s -3.5 to -5.5% and +5.5-

8.0% respectively. Good signs of recovery post April lows.

• General Elections in 4Q20 to mitigate concerns on political and policy uncertainty. Expect economic

stimulus measures post GE.

• US-China trade spat supportive of manufacturing sector. FDI approvals from US and China based

investors spiked in 2019.

• Post-election stimulus likely to focus on infrastructure, digitalisation of government and economy and

narrowing the economic divide (higher minimum wages).

• Market positioning – near term gloves likely to outperform on higher ASPs and upcoming flu season

induced demand. As profits taken, rotate into laggards banks, telcos, plantations and construction.

PAGE 7Macquarie Research | EQUITIES

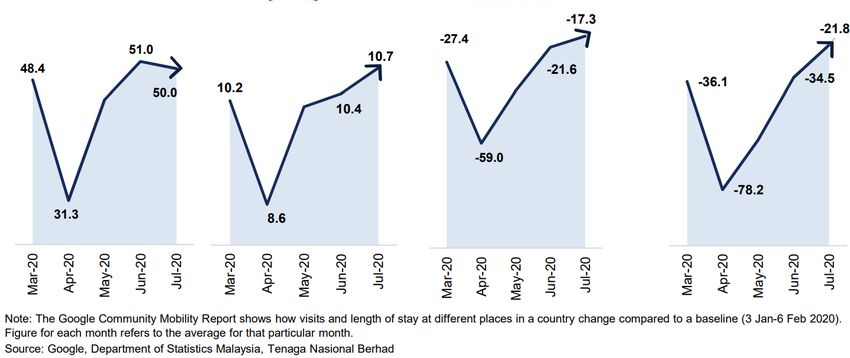

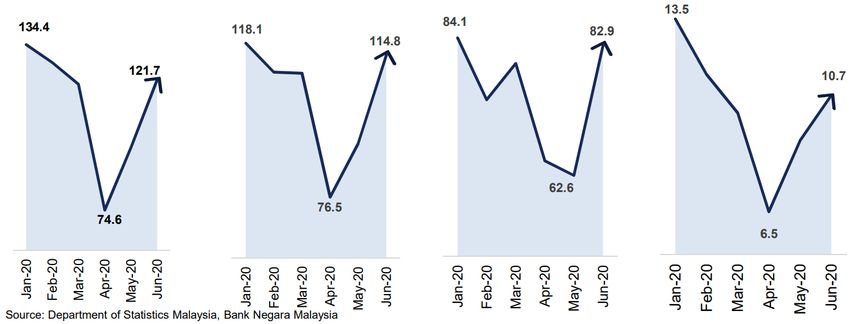

ASEAN Strategy

Malaysia – July indicators suggest continued improvement in economic activity in 3Q20

Index of Wholesale & Industrial Production Malaysia Gross Credit Card Spending

Retail Trade Index Exports (RMbn) (RMbn)

Google Community Mobile Report of Malaysia

Manufacturing PMI Electricity Generation

Mobility Changes Compared to Baseline (% decline)

Index ‘000 Gwh

Workplace Retail & Recreation

PAGE 8Macquarie Research | EQUITIES

ASEAN Strategy

Malaysia – High-conviction ideas

Top Glove (TOPG MK)

• Strong demand for gloves due to Covid causing shortages and driving ASPs higher (up to 2-3x for spot

orders).

• Longer-term demand outlook for gloves could have got a lift from Covid; supply response at least 12

months out.

• Our TP (RM30.40; 20% TSR) implies 23x CY21 PER. In the long run gloves as staples within the

healthcare industry should trade inline with consumer staples.

Genting Malaysia (GENM MK)

• Opening up of casino in mid-June paves the way for return to profitability.

• 60-70% of VIP/Premium Mass players are locals. Inability to travel may raise share of VIP market from

ASEAN peers.

• At 7.8x 21E EV/EBITDA valuations are undemanding while a rebound in dividend yields back to 8.5% (21E)

an added attraction.

Telekom Malaysia (T MK)

• Play on post Covid increase in digitalisation of government and enterprises.

• Large-scale coverage of fibre assets makes TM a play on 5G whether or not it receives spectrum. TM is

focused on being an infrastructure player either way.

• Valuations at 5.2x 21E adj. EV/EBITDA compelling vs domestic peers despite superior growth.

Top short – Maybank (MAY MK)

• Net profits set to fall 40% on NIM compression, higher credit costs and modification losses.

• Cash dividend yields set to drop to 0.4% from 8%.

• At 1x 21E PB valuations are stretched vs domestic peers with ROEs of 6.6%/8.2% in 20/21E.

PAGE 9Macquarie Research | EQUITIES

ASEAN Strategy

Indonesia – Eyeing gradual recovery; gov’t spending a crucial driver heading into 2021

• Sluggish economic recovery likely in 2H 2020 as new COVID-19 cases stay elevated

• We forecast -1 to -1.5% real GDP decline in 2020, followed by +5 to 5.5% growth in 2021. This compares

to the Ministry of Finance’s projections of -1.1 to +0.2% and +4.5-5.5% ranges, respectively

• Gov’t spending will remain crucial to mitigate downside risks; social aid disbursement a bright spot YTD

• FY21 draft budget deficit will narrow YoY. Infra sector is key beneficiary due to +47% uptick YoY off a low

base. Headline figures will decrease off a high base for social aid and healthcare, but core allocations intact

• JCI Index is trading at above +1 StDev. Nonetheless, gov’t policies may provide downside support to

the market, with narrative on 2021 recovery reiterated. COVID-19 vaccine launch in 1Q21 is imperative

• Market positioning – recommend resilient sectors but also having exposure to those benefiting from

improving activities since the gradual economic re-opening in June

• Core picks: Select banks (BBCA, BTPS), telco/towers (TLKM, EXCL), healthcare (HEAL)

• Recovery picks: Consumer (ACES), cement (INTP, SMGR), toll roads (JSMR) PAGE 10Macquarie Research | EQUITIES

ASEAN Strategy

Indonesia - Government spending to the rescue; room for improvement in 2H 2020

In light of tight stimulus program, social aid disbursement speed has been a bright spot

(% of GDP)

30%

25%

25%

20% 18%

15%14%

15% 14%

10%10%10%

9% 9%

10%

7% 6%

5% 5%

4% 4%

5% 3% 3%

1%

0%

Germany

India

Mexico

Korea

Italy

China

Australia

France

Turkey

Brazil

UK

Russia

Indonesia

Canada

South Africa

Argentina

Japan

USA

Saudi Arabia

Stimulus Allocation 3rd July 2020 Mid-August 2020

Sector

(Rp tn) % of Stimulus spent Amount Spent % of Stimulus spent Amount Spent

Social protection 203.9 36% 73.79 42% 86.27

Business incentives 120.61 11% 13.48 13% 16.20

Corporate funding 53.57 0% 0.00 0% 0.00

Sectoral ministries/institutions &

106.11

local gov'ts 5% 5.50 8% 8.50

MSMEs 123.46 24% 30.00 26% 32.51

Healthcare 87.55 5% 4.18 8% 6.94

Total 695.2 18% 126.95 22% 150.42

Source: Ministry of Finance, Macquarie Research, August 2020 PAGE 11Macquarie Research | EQUITIES

ASEAN Strategy

Indonesia - No signs of ending yet for the first wave of COVID-19 cases

Gradual uptick on mall visits but still ~50%

Higher driving activity levels have been seen in Jakarta below pre-COVID levels, per our checks

Source: Ministry of Health, Apple Mobility, Macquarie Research, August 2020 PAGE 12Macquarie Research | EQUITIES

ASEAN Strategy

Indonesia – High conviction ideas

CORE PICKS

Banks - Bank Central Asia (BBCA IJ)

• Remains our preferred major bank stock in Indonesia

• Has the strongest capital position, sector-leading fee income franchise, and best profitability profile

• Valuation premium over state peers can widen as the economic recovery path still uncertain

Telco - Telekomunikasi Indonesia (TLKM IJ)

• Telkomsel and Indihome remain undisputed market leaders amid pressure on TLKM’s legacy business

• Despite recent “unlimited” plans, we believe in stable market; not expecting value destructive price war

• At 6.6x adjusted FY20 EV/EBITDA and 6% dividend yield, we see compelling valuation

Healthcare – Medikaloka Hermina (HEAL IJ)

• Resilient top-line growth drivers with ~50% revenue exposure to the Universal Healthcare; ob-gyn segment

• Further room for EBITDA margin expansion on the back of cost efficiencies

• Reasonable valuation considering wide EV/EBITDA discount relative to best-in-class MIKA

RECOVERY PICK

Cement - Indocement (INTP IJ)

• Among the main beneficiaries of infra budget uptick and continued funding support for low-income housing

• Potential ASP upside risk should supply/demand environment improve in 2021

• Robust net cash position with no debt provides M&A optionality; also a laggard play

PAGE 13Macquarie Research | EQUITIES

ASEAN Strategy

Thailand – Liquidity to lead SET over political risk

⚫ Macro – GDP bottomed at -12% in 2Q20, thanks to Bt1.9trn stimulus. We forecast 2020-21F GDP of -8%

and +3%. Consumption stimulus remain key GDP driver through 4Q20 as travel bubble plans pushed back.

⚫ Politics – Ongoing student protests. Lack of support from opposition parties as protestor agenda violates

constitutional law. Political risk is likely contained in 3Q but road to violence is possible after.

⚫ Market – Global/domestic liquidity and short-selling limits should still lead SET direction for 6-12 months.

1H20A in-line profit of MACQ covered stocks hinted at less FY20F EPS estimate cuts in aggregate. We

maintain our 2020F SET Index target of 1,380 (1-year fwd 16x P/E) and introduce a 2021F target of 1,430.

⚫ Risks – (i) second wave (if happens, likely in winter) would taper hope of hotel/transport/financial sectors

rally. Less fiscal/monetary policy space to buffer full lockdown for second wave. (ii) political violence could

add on risk to government stimulus spending disbursement.

⚫ Preferred sectors: Food, commerce, telco, energy, and manufacturing. Add stocks/sectors with laggard

valuations and 2021F low-base recovery, in any correction.

PAGE 14Macquarie Research | EQUITIES

ASEAN Strategy

Thailand Covid-19 tracker 2Q20 GDP beat thanks to govt stimulus and -23% import

Growth Rate 2014 2015 2016 2017 2018 2019 1Q20 2Q20 1H20 2020F 2021F

Active Total New Growth Rate (the day Total New

Cases Cases Cases (vs 24hrs ago) before) Deaths Deaths Gross Dom estic Products 0.9 2.9 3.2 3.9 4.1 2.4 -2.0 -12.2 -6.9 -8.0 3.0

Private Consumption 0.9 2.2 3.1 3.2 4.6 4.5 2.7 -6.6 -2.1 -2.0 3.0

Government Consumption 2.8 3.0 1.6 0.5 1.5 1.4 -2.8 1.4 -0.7 2.0 2.5

106 3,269 8 0% 0% 58 0

Gross Fixed Capital Formation -2.2 4.3 2.8 0.9 3.3 2.2 -6.5 -8.0 -7.2 -5.5 3.0

Death Total Recovery Total Cases Total Deaths Total Tests Exports of Goods & Services 0.2 0.7 2.1 5.6 7.0 -3.2 1.4 -17.8 -17.6 -13.0 7.0

Rate Recovered Rate / 1M pop / 1M pop Tests / 1M pop

CPI ann avg 1.9 -0.9 0.2 0.7 1.1 0.7 0.4 -2.7 -1.1 -1.0 0.5

Policy rate 2.00 1.50 1.50 1.50 1.75 1.25 0.75 0.50 0.50 0.25 0.25

2% 3,105 1 47 1 685,316 9,817 USD:THB 32.9 36.0 35.8 32.7 32.3 29.7 32.7 30.9 30.9 31.5 31.0

Govt stimulus – Potential shopping stimulus in 4Q Lost working hours slowed in June

Budget Bt bn

MoF emergency decree 1,000

- Bt600bn for public health and relief measures, comprising

Bt45bn for public health department and Bt555bn for MoF

- Bt400bn for economic, community, and public infrastructure

stimulus

SME soft loan emergency decree 500

Corporate Bond Stabilization Fund emergency decree 400

Major measures

Relief measure for employee & self-employed (Apr-Jun) 240

Relief measure for farmer (Apr-Jun) 150

Relief measure for disabled, new-borned, and senior citizen

(Apr-Jun) 39

Tourism stimulus (Jul-Oct) 22.4

Additional SME soft loan & credit guarantee stimulus under

existing budget 114.1

Source: NESDC, BoT, MoF, Macquarie Research, January 2020

PAGE 15Macquarie Research | EQUITIES

ASEAN Strategy

Thailand – High conviction ideas

Top Buy Top Sell

SCC (OP, Bt364CP, BT400TP) IVL (UP, Bt24.50CP, BT20TP)

⚫ Local cement demand & cost savings ⚫ Integrated spread narrowed from May peak

⚫ IPO of packaging business in 4Q20 ⚫ Unplanned shutdown of US ethane cracker

⚫ Key benefit of government infra spending ⚫ Contribution from mobility and lifestyle segments

turned to negative

HMPRO (OP, Bt15.3CP, BT17.50TP)

⚫ Demand for home renovation AWC (UP, Bt3.84CP, BT3.40TP)

⚫ Limited cost savings vs. hotel peers

⚫ Efficient cost control vs. peers

⚫ More MICE & foreign tourists dependent than peers

⚫ Key benefit of 4Q government shopping stimulus

CPF (OP, Bt33.25CP, BT35TP)

⚫ Solid livestock prices into 2H20

⚫ Strong Thai shrimp business turnaround

⚫ Cash prepared for Tesco acquisition

PAGE 16Macquarie Research | EQUITIES

ASEAN Strategy

Philippines - Reopening provides an opportunity to be more than attractively valued

➢ We see a 10% upside to our bottom-up based PCOMP target to 6,500 by the end of

2020E, which would imply a PER of 16x for 2021.

➢ Reopening resumption limits potential downside risk our existing GDP forecast of

-4.3% in 2020E. The most recent monthly remittances of +7% YoY reflect a recovery

from the recent -19% YoY

➢ Despite having a strong balance sheet with a debt to GDP of 39%, government

stimulus has been feeble (just 1.5% of GDP thus far) and execution ability is to blame

➢ BSP has been a more even keeled. We forecast policy rates to be cut to 2.0% and

RRR reduced to 10% for the rest of 2020.

Sector View Top Outperform Picks

Telecoms Overweight TEL, GLO

Consumer Overweight URC, CNPF, PGOLD

Banks Neutral BPI, MBT

Utilities Neutral MER, MPI

Conglomerates Underweight AC

Property Underweight SMPH

Source: Macquarie Research, August 2020

PAGE 17Macquarie Research | EQUITIES

ASEAN Strategy

Philippines - Key economic forecasts

2017 2018 2019 2020E 2021E

GDP (%) 6.7 6.2 5.9 (4.3) 5.0

Personal consumption (%) 5.9 5.6 5.8 (6.0) 3.4

Govt spend (%) 7.0 12.8 10.5 15.0 15.5

Capital formation (%) 9.4 13.9 (0.6) (9.0) 8.0

Inflation (Y/Y, %) 2.9 5.2 2.5 2.4 2.8

RRR (%, year end) 20 18 14 10 8

Policy rate (%, year end) 3.00 4.75 4.00 2.00 2.00

Current account (% of GDP) (0.8) (2.4) (1.8) (1.0) (2.5)

Fiscal deficit (% of GDP) (2.2) (2.9) (2.8) (9.0) (9.5)

PHP:USD, year end 49.90 52.56 50.80 50.00 51.00

Remittances growth (Y/Y, %) 5.3 3.0 3.1 -5.0 2.0

Loans growth (Y/Y, %) 16.8 13.1 7.9 7.0 7.0

➢ We currently have retained a forecast GDP of -4.3% for 2020E. We expect this to recover

in 2021E to +5.0%.

➢ We forecast negative real rates to persist given our CPI expectation of 2.4%.

➢ There is room to bring down policy rates and RRR further to 2.0% and 10% respectively.

Source: BSP, PSA, Macquarie Research, August 2020

PAGE 18Macquarie Research | EQUITIES

ASEAN Strategy

Top Outperform picks in the Philippines

PT Sh Price Rating PE(x) EPS Growth (%) PBV (x) ROE (%)

PhP PhP 2020E 2021E 2020E 2021E 2020E 2021E 2020E 2021E

Top Outperformer

TEL PM 1,670 1,368 OP 11.2 10.1 15.7 11.1 2.4 2.2 22.4 22.5

URC PM 158 137 OP 26.1 23.8 1.6 9.8 3.2 3.0 12.5 13.0

BPI PM 90 64 OP 16.8 10.8 -41.0 55.4 1.0 0.9 6.2 9.1

GLO PM 2,300 2,112 OP 12.8 11.1 -1.9 15.7 3.1 2.5 25.6 24.9

PGOLD PM 57 51 OP 20.2 17.6 7.7 14.8 2.2 2.0 11.2 11.7

CNPF PM 20 16 OP 14.6 13.6 18.5 7.9 2.6 2.2 18.9 17.7

ICT PM 122 108 OP 33.6 30.2 -33.1 11.1 3.2 3.0 9.3 10.2

MER PM 310 270 OP 13.8 12.9 -7.1 6.3 3.4 3.2 25.5 25.5

Top Underperformer

JFC PM 80 140 UP nmf 42.8 nmf nmf 2.2 2.1 -17.0 5.0

JGS PM 47 63 UP 42.6 26.5 -57.9 60.6 1.4 1.4 3.4 5.3

PCOMP 20.3 14.7 -35.9 38.0 2.1 2.0 8.5 10.8

Source: FactSet, Bloomberg, Macquarie Research, August 2020, prices as of 20 August 2020

PAGE 19Macquarie Research | EQUITIES

ASEAN Strategy

Summary of our conviction ideas in ASEAN

Market cap Share price Rating Target price TSR PER (x) EPS growth (%) ROE (%) PBV (x) Div yield (%)

US$m LC$/sh LC$/sh (%) 20e 20e 20e 20e 20e

Singapore

DBS SP 38,898 20.7 OP 24.1 20.5 11.8 -29.5 8.6 1.0 4.2

FLT SP 3,449 1.4 OP 1.6 21.0 20.8 -21.1 6.0 1.3 5.1

UOL SP 3,972 6.4 OP 8.9 38.8 266.4 -95.7 0.2 0.5 1.2

DFI SP 5,614 4.2 OP 5.7 41.4 24.0 -27.7 19.8 4.8 4.1

Malaysia

TOPG MK 17,612 27.1 OP 30.4 13.1 46.2 304.4 47.9 18.9 1.1

GENM MK 3,273 2.3 OP 3.2 44.3 nmf nmf -10.2 0.8 5.2

T MK 3,382 3.7 OP 5.3 43.7 30.2 -46.2 6.3 1.9 2.5

MAY MK 20,583 7.6 UP 7.2 -2.5 15.8 -34.1 6.6 1.0 3.3

Indonesia

BBCA IJ 52,829 31,650 OP 34,500 10.8 35.0 -21.9 12.6 4.4 1.8

TLKM IJ 20,120 3,000 OP 4,100 42.7 12.7 16.3 22.8 2.8 6.0

HEAL IJ 634 3,150 OP 3,810 22.0 35.6 3.1 11.8 4.1 1.1

INTP IJ 2,941 11,800 OP 15,400 34.7 23.0 -1.7 8.2 1.9 4.2

Thailand

SCC TB 13,758 358.0 OP 400.0 15.2 14.7 -8.9 10.2 1.5 3.5

HMPRO TB 6,486 15.4 OP 17.5 15.7 37.9 -13.4 24.7 9.1 2.1

CPF TB 9,101 33.0 OP 35.0 8.5 18.2 14.6 9.0 1.6 2.5

IVL TB 4,351 24.2 UP 20.0 -14.3 14.2 -20.0 7.4 1.0 3.1

AWC TB 3,853 3.8 UP 3.4 -9.4 299.6 -61.9 0.5 1.6 0.1

Philippines

TEL PM 6,085 1,368 OP 1,670 27.0 11.2 15.7 22.4 2.4 4.9

URC PM 6,226 137 OP 158 17.5 26.1 1.6 12.5 3.2 2.3

BPI PM 5,900 64 OP 90 44.6 16.8 -41.0 6.2 1.0 2.8

GLO PM 5,802 2,112 OP 2,300 13.6 12.8 -1.9 25.6 3.1 4.7

PGOLD PM 3,029 51 OP 57 12.7 20.2 7.7 11.2 2.2 0.9

CNPF PM 1,181 16 OP 20 24.8 14.6 18.5 18.9 2.6 1.4

ICT PM 4,518 108 OP 122 16.1 33.6 -33.1 9.3 3.2 3.1

MER PM 6,267 270 OP 310 19.6 13.8 -7.1 25.5 3.4 4.8

JFC PM 3,181 140 UP 80 -41.2 nmf nmf -17.0 2.2 1.4

JGS PM 9,357 63 UP 47 -25.3 42.6 -57.9 3.4 1.4 0.6

Source: Macquarie Research. Share price reflects closing price on 20th Aug’20. PAGE 20Macquarie Research | EQUITIES

ASEAN Strategy

Appendix - Relief measures being supported through the region’s commercial banks

Interest

Moratoria Liquidity support Credit relief NPL recognition

capitalisation?

Rp3t per bank for 12 small, illiquid Credit insurance coverage of 50- Restructured loans due to Covid

Up to 12 months, principal and

and near insolvent banks 100% up to Rp1t loan size remain at current status

interest holiday for consumer,

Indonesia No

micro and small business loans

Rp30t provided to state banks, Capital injection in Bahana, Provisions being built in anticipation,

(Macquarie Research | EQUITIES Important Disclosures: Recommendation definitions Volatility index definition* Financial definitions Macquarie – Asia and USA This is calculated from the volatility of historic price All "Adjusted" data items have had the following Outperform – expected return >10% movements. adjustments made: Neutral – expected return from -10% to +10% Added back: goodwill amortisation, provision for catastrophe Underperform – expected return 10% appraisal value uplift, preference dividends & minority Neutral – expected return from 0% to 10% High – stock should be expected to move up or down at interests Underperform – expected return

Macquarie Research | EQUITIES

Important Disclosures:

Company-Specific Disclosures:

Important disclosure information regarding the subject companies covered in this report is available publicly at www.macquarie.com/research/disclosures. Clients receiving this report can

additionally access previous recommendations (from the year prior to publication of this report) issued by this report’s author at https://www.macquarieinsights.com.

Sensitivity Analysis:

Clients receiving this report can request access to a model which allows for further in-depth analysis of the assumptions used, and recommendations made, by the author relating to the subject

companies covered. To request access please contact insights@macquarie.com.

Analyst Certification:

We hereby certify that all the views expressed in this report accurately reflect our personal views about the subject company or companies and its or their securities. The views were reached

independently, without any attempt of influence from anyone outside of Macquarie’s Research business. Any and all opinions expressed have a reasonable basis, which are the result of the

exercise of due care and skill. To the best of our knowledge, we are not in receipt of, nor have included in this report, any information considered to be inside information. We also certify that no part

of our compensation was, is or will be, directly or indirectly, related to the specific recommendations or views expressed in this report. The Analysts responsible for preparing this report receive

compensation from Macquarie that is based upon various factors including Macquarie Group Ltd overall revenues, a portion of which are generated by Macquarie Group’s Investment Banking

activities.

General Disclaimers:

Macquarie Securities (Australia) Ltd; Macquarie Capital (Europe) Ltd; Macquarie Capital (USA) Inc; Macquarie Capital Limited, Taiwan Securities Branch; Macquarie Capital Securities (Singapore)

Pte Ltd; Macquarie Securities (NZ) Ltd; Macquarie Capital Securities (India) Pvt Ltd; Macquarie Capital Securities (Malaysia) Sdn Bhd; Macquarie Securities Korea Limited and Macquarie Securities

(Thailand) Ltd are not authorized deposit-taking institutions for the purposes of the Banking Act 1959 (Commonwealth of Australia), and their obligations do not represent deposits or other liabilities

of Macquarie Bank Limited ABN 46 008 583 542 (MBL) or MGL. MBL does not guarantee or otherwise provide assurance in respect of the obligations of any of the above mentioned entities. MGL

provides a guarantee to the Monetary Authority of Singapore in respect of the obligations and liabilities of Macquarie Capital Securities (Singapore) Pte Ltd for up to SGD 35 million. This research

has been prepared for the general use of the wholesale clients of the Macquarie Group and must not be copied, either in whole or in part, or distributed to any other person. If you are not the

intended recipient you must not use or disclose the information in this research in any way. If you received it in error, please tell us immediately by return e-mail and delete the document. We do not

guarantee the integrity of any e-mails or attached files and are not responsible for any changes made to them by any other person. MGL has established and implemented a conflicts policy at group

level (which may be revised and updated from time to time) (the "Conflicts Policy") pursuant to regulatory requirements which sets out how we must seek to identify and manage all material conflicts

of interest. Nothing in this research shall be construed as a solicitation to buy or sell any security or product, or to engage in or refrain from engaging in any transaction. In preparing this research,

we did not take into account your investment objectives, financial situation or particular needs. Macquarie salespeople, traders and other professionals may provide oral or written market

commentary or trading strategies to our clients that reflect opinions which are contrary to the opinions expressed in this research. Macquarie Research produces a variety of research products

including, but not limited to, fundamental analysis, macro-economic analysis, quantitative analysis, and trade ideas. Recommendations contained in one type of research product may differ from

recommendations contained in other types of research, whether as a result of differing time horizons, methodologies, or otherwise. Before making an investment decision on the basis of this

research, you need to consider, with or without the assistance of an adviser, whether the advice is appropriate in light of your particular investment needs, objectives and financial circumstances.

There are risks involved in securities trading. The price of securities can and does fluctuate, and an individual security may even become valueless. International investors are reminded of the

additional risks inherent in international investments, such as currency fluctuations and international stock market or economic conditions, which may adversely affect the value of the investment.

This research is based on information obtained from sources believed to be reliable but we do not make any representation or warranty that it is accurate, complete or up to date. We accept no

obligation to correct or update the information or opinions in it. Opinions expressed are subject to change without notice. No member of the Macquarie Group accepts any liability whatsoever for any

direct, indirect, consequential or other loss arising from any use of this research and/or further communication in relation to this research. Clients should contact analysts at, and execute

transactions through, a Macquarie Group entity in their home jurisdiction unless governing law permits otherwise. The date and timestamp for above share price and market cap is the closed price

of the price date. #CLOSE is the final price at which the security is traded in the relevant exchange on the date indicated. Members of the Macro Strategy team are Sales & Trading personnel who

provide desk commentary that is not a product of the Macquarie Research department or subject to FINRA Rule 2241 or any other regulation regarding independence in the provision of equity

research.

PAGE 23Macquarie Research | EQUITIES

Important Disclosures:

Country-Specific Disclaimers:

Australia: In Australia, research is issued and distributed by Macquarie Securities (Australia) Ltd (AFSL No. 238947), a participating organization of the Australian Securities Exchange. Macquarie

Securities (Australia) Limited staff involved with the preparation of research have regular interaction with companies they cover. Additionally, Macquarie Group Limited does and seeks to do

business with companies covered by Macquarie Research. There are robust information barriers in place to protect the independence of Macquarie Research’s product. However, recipients of

Macquarie Research should be aware of this potential conflict of interest. New Zealand: In New Zealand, research is issued and distributed by Macquarie Securities (NZ) Ltd, a NZX Firm. United

Kingdom and the EEA: In the United Kingdom and the European Economic Area, research is distributed by Macquarie Capital (Europe) Ltd, which is authorised and regulated by the Financial

Conduct Authority (No. 193905). Hong Kong & Mainland China: In Hong Kong, research is issued and distributed by Macquarie Capital Limited, which is licensed and regulated by the Securities

and Futures Commission. In Mainland China, Macquarie Securities (Australia) Limited Shanghai Representative Office only engages in non-business operational activities excluding issuing and

distributing research. Only non-A share research is distributed into Mainland China by Macquarie Capital Limited. Japan: In Japan, research is Issued and distributed by Macquarie Capital

Securities (Japan) Limited, a member of the Tokyo Stock Exchange, Inc. and Osaka Exchange, Inc. (Financial Instruments Firm, Kanto Financial Bureau (kin-sho) No. 231, a member of Japan

Securities Dealers Association). India: In India, research is issued and distributed by Macquarie Capital Securities (India) Pvt. Ltd. (CIN: U65920MH1995PTC090696), 92, Level 9, 2 North Avenue,

Maker Maxity, Bandra Kurla Complex, Bandra (East), Mumbai – 400 051, India, which is a SEBI registered Research Analyst having registration no. INH000000545. During the past 12 months,

Macquarie Group Limited or one of its affiliates may have provided securities services to companies mentioned in this report for which it received compensation for Broking services. Malaysia: In

Malaysia, research is issued and distributed by Macquarie Capital Securities (Malaysia) Sdn. Bhd. (Company registration number: 199801007342 (463469-W)) which is a Participating Organisation

of Bursa Malaysia Berhad and a holder of Capital Markets Services License issued by the Securities Commission. Taiwan: In Taiwan, research is issued and distributed by Macquarie Capital

Limited, Taiwan Securities Branch, which is licensed and regulated by the Financial Supervisory Commission. No portion of the report may be reproduced or quoted by the press or any other

person without authorisation from Macquarie. Nothing in this research shall be construed as a solicitation to buy or sell any security or product. The recipient of this report shall not engage in any

activities which may give rise to potential conflicts of interest to the report. Research Associate(s) in this report who are registered as Clerks only assist in the preparation of research and are not

engaged in writing the research. Macquarie may be in past one year or now being an Issuer of Structured Warrants on securities mentioned in this report. Thailand: In Thailand, research is

produced, issued and distributed by Macquarie Securities (Thailand) Ltd. Macquarie Securities (Thailand) Ltd. is a licensed securities company that is authorized by the Ministry of Finance,

regulated by the Securities and Exchange Commission of Thailand and is an exchange member of the Stock Exchange of Thailand. The Thai Institute of Directors Association has disclosed the

Corporate Governance Report of Thai Listed Companies made pursuant to the policy of the Securities and Exchange Commission of Thailand. Macquarie Securities (Thailand) Ltd does not

endorse the result of the Corporate Governance Report of Thai Listed Companies but this Report can be accessed at: http://www.thai-iod.com/en/publications.asp?type=4. South Korea: In South

Korea, unless otherwise stated, research is prepared, issued and distributed by Macquarie Securities Korea Limited, which is regulated by the Financial Supervisory Services. Information on

analysts in MSKL is disclosed at http://dis.kofia.or.kr/websquare/index.jsp?w2xPath=/wq/fundMgr/DISFundMgrAnalystStut.xml&divisionId=MDIS03002001000000&serviceId=SDIS03002001000

Singapore: In Singapore, research is issued and distributed by Macquarie Capital Securities (Singapore) Pte Ltd (Company Registration Number: 198702912C), a Capital Markets Services license

holder under the Securities and Futures Act to deal in securities and provide custodial services in Singapore. Pursuant to the Financial Advisers (Amendment) Regulations 2005, Macquarie Capital

Securities (Singapore) Pte Ltd is exempt from complying with sections 25, 27 and 36 of the Financial Advisers Act. All Singapore-based recipients of research produced by Macquarie Capital (USA)

Inc. represent and warrant that they are institutional investors as defined in the Securities and Futures Act. Singapore recipients should contact Macquarie Capital Securities (Singapore) Pte Ltd at

+65 6601 0888 for matters arising from, or in connection with, this report. United States: In the United States, research is issued and distributed by Macquarie Capital (USA) Inc., which is a

registered broker-dealer and member of FINRA. Macquarie Capital (USA) Inc, accepts responsibility for the content of each research report prepared by one of its non-US affiliates when the

research report is distributed in the United States by Macquarie Capital (USA) Inc. Macquarie Capital (USA) Inc.’s affiliate’s analysts are not registered as research analysts with FINRA, may not be

associated persons of Macquarie Capital (USA) Inc., and therefore may not be subject to FINRA rule restrictions on communications with a subject company, public appearances, and trading

securities held by a research analyst account. Information regarding futures is provided for reference purposes only and is not a solicitation for purchases or sales of futures. Any persons receiving

this report directly from Macquarie Capital (USA) Inc. and wishing to effect a transaction in any security described herein should do so with Macquarie Capital (USA) Inc. Important disclosure

information regarding the subject companies covered in this report is available at www.macquarie.com/research/disclosures, or contact your registered representative at 1-888-MAC-STOCK, or

write to the Supervisory Analysts, Research Department, Macquarie Capital (USA) Inc, 125 W.55th Street, New York, NY 10019. Canada: In Canada, research is distributed by Macquarie Capital

Markets Canada Ltd., a (i) member of the Investment Industry Regulatory Organization of Canada (IIROC) and the Canadian Investor Protection Fund, and (ii) participating organisation of the

Toronto Stock Exchange, TSX Venture Exchange & Montréal Exchange. Important disclosure information regarding the subject companies covered in this report is available at

www.macquarie.com/research/disclosures. IIROC Rule 3400 Disclosures can be obtained by writing to Macquarie Capital Markets Canada Ltd., 181 Bay St. Suite 3100, Toronto, ON M5J2T3.

© Macquarie Group

PAGE 24You can also read