Barclays Global Healthcare Conference Investor Presentation - March 2019

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Barclays Global Healthcare Conference

Investor Presentation

March 2019Forward-looking Statements and Non-GAAP Information

➢ This presentation may include projections and other “forward-looking statements” within the meaning of the Private Securities

Litigation Reform Act of 1995. Such statements relate to future events and expectations and involve unknown risks and

uncertainties. Omega’s actual results or actions may differ materially from those projected in the forward-looking statements.

For a summary of the specific risk factors that could cause results to differ materially from those expressed in the forward-looking

statements, see Omega’s most recent Annual Report on Form 10-K filed with the Securities and Exchange Commission.

➢ This presentation may contain certain non-GAAP financial information including EBITDA, Adjusted EBITDA, Total Adjusted Debt

(a/k/a, Funded Debt), Adjusted FFO, FAD, Total Cash Fixed Charges and certain related ratios. A reconciliation of these non-GAAP

disclosures is available in the Exhibit to this presentation or on our website under “Non-GAAP Financial Measures” at

www.omegahealthcare.com. Other financial information is also available on our website.

➢ Information is provided as of December 31, 2018, unless specifically stated otherwise. We assume no duty to update or

supplement the information provided.

Investor Presentation, March 2019 2What does Omega Healthcare do?

What does Omega Healthcare do?

◼ Among all REITS, Omega has the largest portfolio of Skilled Nursing Facilities (“SNFs”)

Number of SNF Properties

1000

792

800

600

400 335

187

200 140

93 76

0

OHI SBRA WELL CTRE LTC NHI

Source: MedPAC Report to the Congress: Medicare Payment Policy March 2018

◼ We also have a growing Senior Housing portfolio concentrated in areas with

high barriers to entry

◼ We are a “Triple Net” REIT- meaning we own the real estate and improvements

but our tenants are responsible for capex, taxes and insurance

Investor Presentation, March 2019 4What is a SNF?

What is a SNF?

◼ SNFs are post-acute providers of 24 hour nursing care

◼ SNFs are primarily funded through Medicare and Medicaid reimbursement

◼ SNFs are the lowest cost provider of post-acute 24 hour nursing care

◼ SNFs provide care for much higher acuity patients than can be handled in Senior

Housing or Home Health settings – so hospital discharges to SNFs have held steady

Average Cost per Day per Care Setting % of Discharges to SNFs

Acute Care Post-Acute Care

22.0%

$2,500 $2,271 20.2% 20.3% 20.0%

19.3% 19.7%

20.0% 18.9% 19.1% 19.3%

$2,000

$1,512 $1,456 18.0%

$1,500

16.0%

$1,000

$508 14.0%

$500

12.0%

$0

10.0%

Hospital LTACH IRF SNF 2009 2010 2011 2012 2013 2014 2015 2016

Sources: 1999-2015 AHA Annual Survey; MedPAC Data Book, June 2016, NIC Skilled Source: Medicare claims and enrollment, 2009 - 2016

Nursing Data Report, June 2017

Investor Presentation, March 2019 6Why do we like SNFs?

Why do we like SNFs? Accelerating demand from demographics

◼ The aging of the baby boomers will drive a multi-decade increase in demand

for SNFs

◼ Increasing occupancy will improve SNF operator financial performance and

increase their capacity to pay rent

Source: Avalere analysis of Medicare Part A 100% Standard Analytic File (SAF) for 2016 Source: www.cdc.gov

Investor Presentation, March 2019 8Why do we like SNFs? Limited supply growth

◼ Certified facilities and beds have remained steady for many years, with no

net new supply

(figures in 000s, unless

otherwise indicated)

Source: Compiled by American Health Care Association (AHCA) Research Department from CMS OSCAR/CASPER survey data (2009-2018)

◼ Certificates of Need restrictions apply in 36 states and many other states

have various other restrictions, e.g., bed moratoriums, etc.

Investor Presentation, March 2019 9Why do we like SNFs? Limited disintermediation

◼ Per the most recent MedPAC data, the average SNF margin is 0.7%. This low margin

provides little opportunity for disintermediation.

Average SNF Profit Margin

2.0% 1.90% 1.90%

1.80%

1.60%

1.5%

1.0%

0.70%

0.5%

0.0%

2012 2013 2014 2015 2016

◼ Low disintermediation risk provides additional clarity into investing in the

SNF asset class.

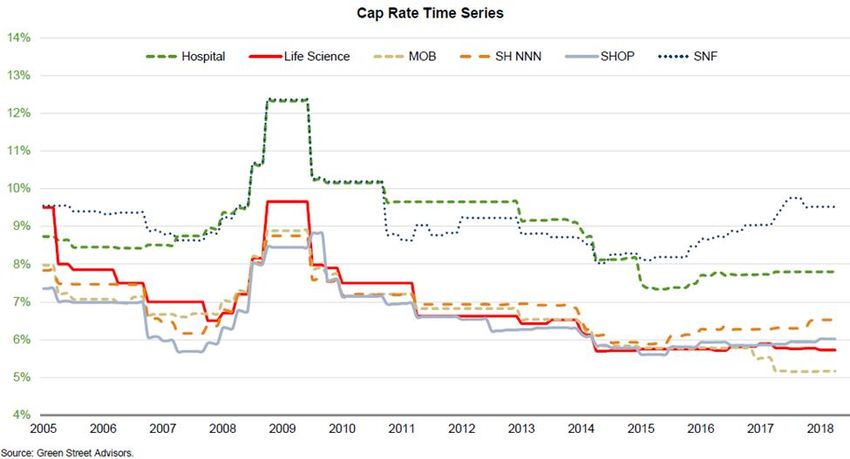

Investor Presentation, March 2019 10Why do we like SNFs? Excellent investment yields

◼ Investing in SNFs is able to provide an excellent entry yield of ~9.5%

◼ This yield compares very favorably with all other healthcare real estate sub-

sectors.

◼ Our standard annual rent escalator is 2.5%, providing a compelling and

growing return for investors.

Investor Presentation, March 2019 11Why do we like SNFs? Long growth runway

◼ Even though Omega is the largest owner of SNFs, we still only own about 5%

of the market.

% of SNF Ownership

CTRE

WELL

SBRA LTC

OHI NHI

5% OHI

SBRA

WELL

CTRE

Other LTC

89%

NHI

Other

◼ Given the accretion created from acquisitions, the fragmented ownership of

SNFs provides a significant opportunity for further growth.

Investor Presentation, March 2019 12How are Omega’s tenants faring?

How are Omega’s tenants faring?

◼ Overall, tenants are faring quite well considering average EBITDAR coverage, a proxy

for an operator’s capacity to pay rent, has declined in recent years.

◼ Caused by multiple headwinds:

❑ Baby bust

❑ Migration to Medicare Advantage and reduction in length of stay

❑ Increase in observation stays

❑ Wage pressures

◼ These headwinds are starting to moderate and the demographic tailwinds will help

occupancy and operator performance going forward

Investor Presentation, March 2019 14How has Omega performed?

How has Omega performed?

◼ Omega has a history of strong shareholder returns

Omega’s Total Returns vs Healthcare REIT Averages (1) Omega Share Price Growth, 12/31/2002 to 2/15/2019

(Years ending 12/31/2018)

◼ We believe we will continue to provide solid shareholder returns through:

❑ Accretive capital allocation

❑ A strong dividend yield

❑ Built-in escalators

❑ A value-enhancing development platform

1) Source: KeyBanc Capital Markets The Leaderboard, December 28, 2018. Peer returns are simple average of returns of NHI, HR, LTC, SABRA, VTR, WELL, and HCP

Investor Presentation, March 2019 16Questions?

You can also read