BRISBANE APARTMENT MARKET REVIEW - February 2019 - Ferrier Hodgson

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

BRISBANE

APARTMENT

MARKET

REVIEW

February 2019

ferrierhodgson.com.au

Brisbane Apartment Market Review

azurium.com.au

Brisbane Apartment Market Review 2

CONTENTS

Section Page

Introduction 4

Methodology 4

Summary 5

Supply 6

Project funding 8

Demand 10

Increasing unsold developer stock 11

Other trends 13

Managing settlement risk 13

Expectations for the future 14

Snapshot of the market 14

Our Queensland property team 15

Brisbane Apartment Market Review 3

Introduction

In this review, we provide the latest insights on the Brisbane Apartment Market, based on our ongoing research of

the market over the past two years.

This research emanates from our database of 162 projects of greater than 25 apartments in size, and in turn 19,230

apartments, which are currently under construction or recently completed.

Methodology

In preparing this publication we have collated information from a variety of sources including Core Logic RP Data,

Cordells, Queensland Titles Office, developer websites and kerbside inspections.

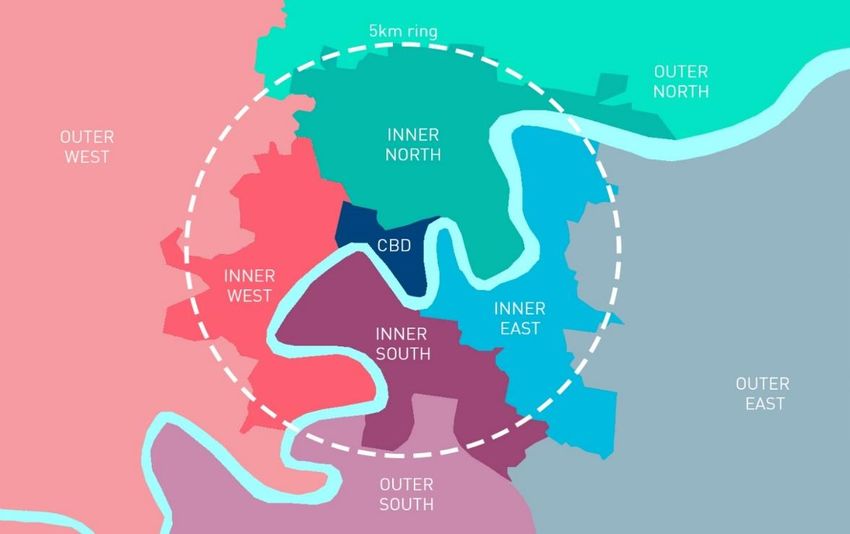

The data is for residential apartment projects completed during 2017 or under construction at 31 December 2017

with 25 or greater apartments situated in identified localities within 12 kilometres of the Brisbane CBD as shown in

the map below. It does not take into consideration development approvals and projects awaiting commencement of

construction.

Data has been collated over a period of time and therefore settlements in a number of projects may have

subsequently completed or be currently underway.

Inner East Outer North

Balmoral, Bulimba, Cannon Hill, Coorparoo, East Brisbane, Alderley, Ascot, Aspley, Chermside, Clayfield, Enoggera,

Kangaroo Point and Stones Corner. Everton Hills, Everton Park, Gaythorne, Grange, Hendra,

Kedron, Lutwyche, McDowall, Mitchelton, Northgate, Nundah,

Inner North Wooloowin and Zillmere.

Albion, Bowen Hills, Fortitude Valley, Hamilton, Kelvin Grove,

New Farm, Newmarket, Newstead, Spring Hill, Teneriffe and Outer South

Windsor. Annerley, Archerfield, Coopers Plains, Eight Mile Plains,

Moorooka, Sherwood, Sunnybank, Yeerongpilly and Yeronga.

Inner West

Auchenflower, Bardon, Milton, Paddington, St Lucia and Outer East

Toowong Carina, Carina Heights, Holland Park, Holland Park West,

Morningside, Mount Gravatt, Mount Gravatt East, Murarrie,

Inner South Seven Hills and Upper Mount Gravatt.

Dutton Park, Greenslopes, Highgate Hill, Norman Park, South

Brisbane, West End and Woolloongabba. Outer West

Ashgrove, Enoggera, Indooroopilly, Kenmore, Taringa and The

Gap.

Brisbane Apartment Market Review 4

Summary

The key findings from our database of 19,230 apartments within 162 projects that were under construction as at 31

December 2017, or were completed during 2017, are:

— 8,032 apartments completed in 2017 with a number of settlements pending, compared to our forecast of

10,169 apartments to complete during 2017 in our report as at 31 December 2016. This decrease can be

attributed to slower than expected construction progress across several projects.

— 11,198 apartments were under construction as at 31 December 2017, of which:

• 7,750 are forecast to complete in 2018

• 1,967 are forecast to complete in 2019

• 1,481 are forecast to complete in 2020 and beyond.

— The market is awash with incentives for purchasers ranging from deferred settlement periods to price

reductions and other arrangements including vendor finance, payment of stamp duty, furniture packages and

rent guarantees.

— An increasing reliance on other financing arrangements with only 38% of financing coming from the big 4

banks. This contrasts to Sydney where our research shows 67% of all apartment projects are financed by the

big 4 banks.

— There is a considerable number of projects with no mortgagee, further demonstrating that developers are

pursuing alternative methods to fund their projects as the major banks have pulled back, due to highly

publicised supply concerns.

Number of apartments under construction – 12 month comparison by mortgagee

7,000

6,008

6,000

5,000 4,825

4,748

4,192 4,250

3,994

4,000

3,000

2,485

2,080

2,000

1,402

1,000 701

567

469

-0

Big 4 banks Other Australian banks Other banks and private No mortgagee

lenders

31-Dec-16 30-Jun-17 31-Dec-17

Brisbane Apartment Market Review 5

Supply

Building approvals for non-house residential construction in Brisbane decreased for the second year running during

2017, after the substantial increase between 2013 and 2015.

Brisbane building approvals, dwellings excluding houses

25,000

20,300

20,000

16,437

15,000

12,208

10,546 10,725

10,000

7,413 7,290

6,755 6,557 6,625

6,196 6,391

6,035

5,413

4,806 4,659

5,000

2,140

-0

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Source: ABS

Building approvals peaked in 2015 following the introduction of Brisbane City Plan 2014 which allowed higher

density development in areas close to the Brisbane CBD and public transport hubs coupled with increased risk

appetite from developers and investors in a low interest rate environment.

However, as shown above, 2016 and 2017 have demonstrated a steady decrease in approvals. Factors working to

constrain future supply, include:

— Oversupply concerns, as evidenced by the level of recent completions with residual unsettled (developer

owned) stock

— Increased construction costs

— Expectations for price discounts, following increased provision of marketing incentives.

Based upon available 2018 data we project that building approvals will plateau in the short to medium term.

However, given the significant lag time between approvals and apartment completion there remains some time to

go before the Brisbane apartment market returns to sustainable levels.

Brisbane Apartment Market Review 6

The most recent RLB Crane Index reflects the decrease in activity with the number of cranes used in apartment

construction in Brisbane decreasing from 91 (Q2 2016) to 43 (Q2 2018).

Number of cranes used in residential sector

300

250

200

150

100

50

0

Q3 2014 Q2 2015 Q2 2016 Q3 2016 Q2 2017 Q4 2017 Q2 2018

Brisbane Sydney Melbourne Gold Coast

Source: RLB

While there has been a slow down in approvals, there are still 11,198 apartments within 12km of the Brisbane CBD

currently under construction due for completion between 2018 to 2020.

Forecast completion dates

9,000

7,750

8,000

7,000

6,000

5,000

4,000

3,000

1,967

2,000 1,481

1,000

-0

2018 2019 2020 and beyond

Source: Cordell Connect, Azurium Real Estate

A total of 8,032 apartments were completed during 2017 which compares to our estimate of 10,169 made at the

beginning of the year. This decrease is largely the result of slower than expected construction progress on a

number of projects.

Brisbane Apartment Market Review 7

Project funding From our research across the Brisbane, Gold Coast and Sydney apartment markets, we have identified the following bank and other financier exposures. Percentage of apartments under construction – as at 31 December 2017 by mortgagee Mortgagee Brisbane Sydney Gold Coast Big 4 bank 38% 67% 28% Non-Big 4 bank 40% 22% 41% No mortgagee 22% 11% 31% Source: Azurium There is an increasing reliance on other financing arrangements with only 38% of financing coming from the Big 4 banks in Brisbane. This contrasts to Sydney where our research indicates 67% of all major projects (over 50 apartments) are financed by the Big 4 banks. There is also a considerable number of projects with no mortgagee, further demonstrating developers are pursuing alternative methods to fund their projects as the major banks have pulled back, due to highly publicised supply concerns. Financier exposure by locality The charts opposite show the percentage of all apartments under construction by locality. Our research confirms that the Inner South is the current hotspot for development with the suburbs of West End (742 apartments), South Brisbane (1,821 apartments) and Woolloongabba (991 apartments) seeing considerable new development. As forecast in our report as at 31 December 2016, the number of apartments under construction in the Inner North has decreased from 32% (4,264 as at 31 December 2016) to 26% (2,926 as at 31 December 2017). This is in part due to the completion of high profile developments, FV – Valley House and Flatiron (combined 594 apartments), Newstead Central – St Tropez and Laguna (combined 420 apartments) and The Yards development (combined 390 apartments). The Big 4 banks in particular have been highly active in the Inner North with 43% of the Big 4 banks’ exposure in the Inner North. Contrastingly, whilst the number of apartments under construction in the Inner South has decreased from 4,215 (as at 31 December 2016) to 3,879 (as at 31 December 2017), this locality represents the highest percentage of stock under construction (35% as at 31 December 2017). Brisbane Apartment Market Review 8

2% 14%

3%

3%

CBD Outer North

4%

26% Inner North Outer South

5% Inner South Outer East

All projects Inner East Outer West

11,198 apartments

8% Inner West

35%

1%

1%

5% 43%

18%

No mortgagee 6% Big 4 banks

2,485 apartments 4,250 apartments

46% 7%

29%

29%

10%

5%

21% 28%

3%

22% 7% 14%

26%

Other Australian

Other financiers

banks 3,994 apartments

469 apartments 7%

13%

17% 27%

14%

Brisbane Apartment Market Review 9Demand

The graph below shows the volume of apartments sold from December 2011 to March 2018, together with the

weighted average price of apartment sales within Inner Brisbane (0-6km).

Inner Brisbane apartment sales

Sale Price $ Sales (#)

750,000 2,000

700,000 1,600

650,000 1,200

600,000 800

550,000 400

500,000 0 -0

Sep-15

Dec-11

Jun-12

Sep-12

Dec-12

Jun-13

Sep-13

Dec-13

Jun-14

Sep-14

Dec-14

Jun-15

Dec-15

Jun-16

Sep-16

Dec-16

Jun-17

Sep-17

Dec-17

Jun-18

Mar-12

Mar-13

Mar-14

Mar-15

Mar-16

Mar-17

Mar-18

Weighted average sale price Number of Sales

Source: Place Projects

The weighted average sales price has fallen during the year whilst sales volumes have remained at record lows.

Owner occupier demand has continued relative to investor demand over the past year, noting the peak volume of

sale contracts in late 2014 and early 2015, was driven primarily by interstate and foreign investors.

Many of these investors were sourced by investment marketeers who typically charge commissions of 5% to 8%

per apartment.

The total cost to some of those developers is up to 14%, once seminar costs are paid and investors are offered

various monetary / promotional incentives,

These rental incentives include free Wi-Fi, rent free periods and furniture packages amongst others.

Brisbane does however remain an attractive investment option due to its comparative affordability relative to both

Sydney and Melbourne.

Brisbane Apartment Market Review 10Increasing unsold developer stock

There has been increasing concern with regard to Unsettled apartments as at 31 December 2017 as a

settlement risk over the past year. percentage of total apartments completed

In order to gain a deeper understanding of this risk for 40%

developers and financiers we investigated the number of

apartments within completed projects that were yet to

settle as at 31 December 2017.

To do this we undertook searches to identify which 35% 34%

apartments in projects completed during 2017 were still

recorded in the name of the developer as at 31

December 2017. We acknowledge that some of the

30%

apartments may be contracted with settlements yet to

occur.

26%

Our findings show that settlements are taking longer to

finalise with 19% of apartments completed in the first 25%

half of 2017, 34% of apartments from the second half of

2017 and 26% of all apartments completed during the

year remaining unsettled as at 31 December 2017.

20% 19%

These settlement delays, at a time of peak debt for the

developer, add substantial interest costs, diminishing the

return to mezzanine providers and eroding the

developer’s equity position. We are also aware of 15%

developers being charged roll over fees where their

facility was not paid back on time.

Our research demonstrates that some localities have a 10%

higher number of unsettled apartments. In particular, the

following suburbs have the highest number of unsettled

apartments as at 31 December 2017:

5%

— South Brisbane (410 apartments)

— West End (280 apartments)

— Chermside (181 apartments) 0%

— Albion (141 apartments) 1st half 2017 2nd half 2017 All of 2017

— Bowen Hills (121 apartments)

Number of apartments completed vs number of apartments unsettled in 2017 by locality

2,926

3,000

2,695

2,500

2,000

1,500

937

1,000 800

583

487 481

500 288

197 150

120 85 54 109 50

45 44 5

0

CBD Inner North Inner South Inner East Inner West Outer North Outer South Outer East Outer West

Number of apartments completed in 2017 Number of apartments completed in 2017 that are unsettled

Brisbane Apartment Market Review 11Despite fewer apartments being completed in the Inner South than the Inner North during 2017, the Inner South

had a higher number of unsettled apartments as at 31 December 2017.

Further, while the number of apartments completed in the Outer North in 2017 was approximately a third of the

number of apartments completed in the Inner North, the number of apartments unsettled in the Outer North was

half of the number of apartments unsettled in the Inner North.

Unsettled apartments as a percentage of total apartments completed in each locality as at 31

December 2017

45%

40%

40%

35%

31% 30%

30%

30% 27%

25%

25%

20%

20% 18%

15%

10%

10%

5%

0%

CBD Inner North Inner South Inner East Inner West Outer North Outer South Outer East Outer West

Settlement risk is certainly not confined to the Inner North, Inner South and Outer North. As the following graph

shows, there were projects with greater than 25% of unsettled apartments in all localities.

Number of projects completed in 2017 vs number of projects completed in 2017 with greater than 25%

of apartments unsettled as at 31 December 2017 by locality

25

25

20

20 19

15

11 11

10 8

6

5 4

3 3 3

2 2 2

1 1

0

CBD Inner North Inner South Inner East Inner West Outer North Outer South Outer East

Number of projects Number of projects with greater than 25% unsettled apartments

Although the Inner South had the highest number of apartments yet to settle as at 31 December 2017, the number

of projects with greater than 25% of apartments unsettled was relatively low at 44% of all projects completed in the

Inner South.

As demonstrated above, the outer localities had a higher proportion of projects with greater than 25% of apartments

unsettled as at 31 December 2017.

Brisbane Apartment Market Review 12Unsettled apartments as at 31 December 2017 as a percentage of total apartments for projects completed in

2017 by development size

The following graph demonstrates an inverse relationship between a project’s size and settlement risk. That is, as a

project’s size increases the percentage of apartments within the project that are unsettled decreases. While not

within the scope of this report, we see this relationship extending to projects of less than 25 apartments.

40%

31%

30%

25%

21%

20%

10%

0%

Large (>100 apartments) Medium (50-99 apartments) Small (25-49 apartments)

While high profile developments in inner city areas such as Newstead and South Brisbane may attract the majority

of attention, we retain our concerns for smaller projects located in the middle to outer ring suburbs.

It is here that the headwinds facing the apartment market will be felt most strongly as buyers become more

discerning due to increased supply.

Other trends

Other noticeable trends include:

— Foreign (particularly Chinese) purchasers who are unable to obtain finance from Australian lenders rescinding

contracts, with new contracts being entered into by local residents, usually family members.

— Early discounting of some projects to clear residual stock.

— Pre-sales on yet-to-commence projects are not meeting expectations resulting in project deferrals

— The quantity of new stock resulting in significant losses upon resale on recently purchased off-the plan prices

of up to 30%.

Managing settlement risk

To manage settlement risk, it is critical to comprehend:

— Current market conditions and how buyers may be positioned

— The supply and demand for similar competing products

— The advantages and disadvantages of given product compared to the competition including other new stock

and older stock

— Legal disputes such as the enforceability of pre-sale contracts relating to:

• Building specification differences to marketing plans

• Any looming sunset dates

• Body corporate disclosure statement variances

— Level of deposit

— Buyer origin, being either local, interstate or foreign

— Nature of purchasing entity

Brisbane Apartment Market Review 13Expectations for the future The pressure on owners of older stock will continue to intensify as the choice for buyers and renters, who hold the higher ground in rental property negotiations, increases. Anecdotally, owners are preferring to hold on to properties for a longer time period, rather than crystallise losses. The longer this downward trend in apartment values continues, the greater the likelihood that off the plan purchasers simply elect to walk away. If this eventuates, it will not only be the equity and mezzanine funders who will incur losses, but senior lenders may also be at risk, depending on their exposure. Those developers with an effective and streamlined approach to managing settlements are faring better than those developers who do not have an appropriate strategy in place to work with purchasers. With all the headwinds facing the residential apartment sector in Brisbane, we anticipate sales prices for new apartments will decline following decreases in sales volumes for off-the-plan apartments, with settlement risk being a significant concern. While both inner city and middle ring suburban areas have large numbers of projects completing throughout 2018, we retain confidence in high quality projects. Specifically, we consider the defining factors of successful projects to include: — Location — Building quality and visual appeal — Number of apartments — Size — Layout — Extent of allocated and unallocated parking — Views — Amenity — Price point — Purchase price compared to valuation The flight to quality will pick up speed as buyers and renters begin leveraging their negotiating positions. This phenomenon will be felt the most in the middle ring suburban areas such as Albion, Nundah, Cannon Hill and Chermside. Financiers exposed to the larger residential projects in this sector need to be prepared to work closely with developers to mitigate the risk of loss. Snapshot of the market From our research, we have formed the opinion that sale prices have fallen, the volume of sales has decreased, greater measures are being offered to motivate agents and buyers to act, and settlement periods are lengthening. Brisbane Apartment Market Review 14

Our Queensland In Queensland we have a team of experienced real estate

real estate team professionals with extensive experience in the residential

apartment sector. We can provide a detailed private briefing on

the market, and where appropriate, advise developers and

financiers on updated options analysis of any exit, hold or develop

out strategies, project completion, mitigating settlement risk and

project marketing.

To find out more, or for further information as to how we can

assist, please contact one of our real estate team today.

Will Colwell Brett McAuliffe

Queensland Practice Head Executive Director

Ferrier Hodgson Azurium Real Estate

+61 7 3834 9205 +61 7 3834 9233

will.colwell@fh.com.au brett.mcauliffe@azurium.com.au

Tim Michael Peter Gumbley

Partner Director – Sales & Project Marketing

Ferrier Hodgson Azurium Real Estate

+61 7 3834 9228 +61 7 3834 9222

tim.michael@fh.com.au peter.gumbley@azurium.com.au

Sallyanne Pitt Cameron Mana

Director Director – Development

Ferrier Hodgson Azurium Real Estate

+61 7 3834 9214 +61 7 3834 9222

sallyanne.pitt@fh.com.au cameron.mana@azurium.com.au

Campbell Munro Andrew Willsford

Property Senior Analyst Valuation Specialist

Ferrier Hodgson Azurium Real Estate

+61 7 3834 9235 +61 7 3834 9222

campbell.munro@fh.com.au andrew.willsford@azurium.com.au

Jackson Adcock Andrew Keeble

Property Analyst Retail Leasing Specialist

Ferrier Hodgson Azurium Real Estate

+61 7 3834 9247 +61 7 3834 9222

jackson.adcock@fh.com.au andrew.keeble@azurium.com.au

Disclaimer:

This publication is produced by Ferrier Hodgson and Azurium Real Estate. It is intended to provide general information in summary form on real estate

topics, current at the time of publication. The contents do not constitute advice and should not be relied upon as such. Formal advice should be sought in

particular matters.

This publication is subject to copyright. No part of it may be reproduced, adapted or transmitted without the written permission of the copyright owner.

Brisbane Apartment Market Review 15Level 7, 145 Eagle Street

Brisbane, QLD 4000

Brisbane Apartment Market Review T +61 7 3831 14833

February 2019 16You can also read