Recruiters' Edition February 2021 - FCSA

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

February 2021 Recruiters’ Edition

February 2021

Contents

Page 3 - Commentary

Page 4 – Changes in Demand

Page 16 - Changes in Supply

Page 18 – UK Labour Market Statistics

2

February 2021

Commentary

Industry output down 15% in 2020 as self-employed

numbers plummet 13%, YoY, in Q4

Welcome to the February 2021 edition of the FCSA’s Workforce Barometer in which we continue to

seek to provide data and insights to support members with issues relating to the current pandemic.

This month’s report includes the latest data on the economic impact of the pandemic, including which

sectors have suffered most from redundancies and the impact on Zero Hours Contract working. We

also look at the change in self-employed worker numbers by sector to chart the potential fall out from

the impending off-payroll reforms.

Despite a rally towards the back end of 2020, the all-industry UK economic output was 9.9% lower

across the year than in 2019. In comparison, the employment activities sector recorded output

14.7% lower than in the prior year.

As a backdrop to the on-going challenges facing the industry, whilst not all self-employed work on a

freelance basis into UK plc, the dramatic fall in self-employment numbers – ending the year 13.0%

(652k) lower in Q4 2020 than in Q4 2019 – is undoubtedly hampering the industry’s recovery. And,

whilst temporary employment numbers are buoyant (up 10.0% / 142k, YoY, in Q4 2020), it is the rise

in FTC working that is causing the upward spike, as we evidenced last month.

Looking at the sectors most impacted by the fall in self-employed numbers – carrying 64% of the

losses between them - some are likely casualties of the impending off-payroll reforms:

• A 23% (86k) YoY fall in the number of self-employed engaged within Health & Social Work

• A 20% (62k) fall in the number of self-employed Transport & Storage Workers

• A 22% (86k) fall in the number of self-employed engaged in Admin & Support Services

• A 15% (62k) fall in self-employed workers in Wholesale & Retail

• A 13% (119k) fall in self-employed Construction Workers

Whilst these falls are stark, we continue to hear evidence from members of an increasing number of

employers rationalising and formalising their agency PSL who, in turn, are doing the same with their

supply chain partners – notably in favour of FCSA accredited organisations. With just one month to

go, never has there been a more pressing time to stress the importance of such moves.

Phil Pluck, CEO FCSA

3

February 2021

Changes in Demand

9.9% lower UK economy output across 2020:

14.7% lower in the employment activities sector

Following a 2.7% dip in GDP growth in November, UK output improved by 1.0% in December

rendering it 6.3% below pre-pandemic levels. Across 2020, UK output was 9.9% lower than the prior

year. The fall in 2020 was more than twice the next largest fall of 4.0% in 2009, driven by significantly

weaker growth from services – the historical driver of 80% UK GDP

Figure 1. UK monthly GDP Index: January 2007 - December 2020

110

Monthly Index, 2018 = 100

105

100

95

90

85

80

75

70

Figure 2. 2020 GDP versus 2009 output

-8.9

Index of Services

-2.5

-8.6

Index of Production

-7.8

-12.5

Construction

-13.2

%

-14 -12 -10 -8 -6 -4 -2 0

2020 2009

Source for both: FCSA analysis of ONS data

Across the employment activities sector, an end of year rally resulted in full-year output 14.7%

lower than the prior year.

4

February 2021

Changes in Demand

Number of hours worked: the barometer to watch

Between July - September and October - December 2020, the total actual weekly hours worked by

those in employment in the UK increased by 53.7 million, or 5.8%, to 978.7 million hours. Over the

same period, average actual weekly hours increased by 1.8 hours to 30.2 hours.

Over the year, total actual hours worked in the UK decreased, however, by 72.4m (6.9%), to

978.7 million - a fall of 1.7 hours per week to 30.1.

Figure 3. UK total actual weekly hours worked (people aged 16 years and over), seasonally

adjusted, between Oct - Dec 1992-2020 (000s)

1,100.0

1,050.0

1,000.0

950.0

900.0

850.0

800.0

Oct-Dec 1992

Apr-Jun 1993

Oct-Dec 1993

Apr-Jun 1994

Oct-Dec 1994

Apr-Jun 1995

Oct-Dec 1995

Apr-Jun 1996

Oct-Dec 1996

Apr-Jun 1997

Oct-Dec 1997

Apr-Jun 1998

Oct-Dec 1998

Apr-Jun 1999

Oct-Dec 1999

Apr-Jun 2000

Oct-Dec 2000

Apr-Jun 2001

Oct-Dec 2001

Apr-Jun 2002

Oct-Dec 2002

Apr-Jun 2003

Oct-Dec 2003

Apr-Jun 2004

Oct-Dec 2004

Apr-Jun 2005

Oct-Dec 2005

Apr-Jun 2006

Oct-Dec 2006

Apr-Jun 2007

Oct-Dec 2007

Apr-Jun 2008

Oct-Dec 2008

Apr-Jun 2009

Oct-Dec 2009

Apr-Jun 2010

Oct-Dec 2010

Apr-Jun 2011

Oct-Dec 2011

Apr-Jun 2012

Oct-Dec 2012

Apr-Jun 2013

Oct-Dec 2013

Apr-Jun 2014

Oct-Dec 2014

Apr-Jun 2015

Oct-Dec 2015

Apr-Jun 2016

Oct-Dec 2016

Apr-Jun 2017

Oct-Dec 2017

Apr-Jun 2018

Oct-Dec 2018

Apr-Jun 2019

Oct-Dec 2019

Apr-Jun 2020

Oct-Dec 2020

Total actual weekly hours

Source: FCSA analysis of ONS data

Underpinning this barometer are two issues creating continuing cause for concern:

o Firstly, there has been a sharp rise in the number of employees remaining officially at work

but not getting paid. This is likely to be, in part, due to those on Zero Hours Contracts –

recorded at 978k in October - December 2020 - who are still appearing in the Labour Market

Statistics as employees but for whom there is no work. This number rose to 278k in

November and to 307k in December after declining to 211k in October.

o Secondly, as we evidenced in previous reports with specific company examples, many

employers have actioned reduced hours for reduced pay policy, from which it is uncertain

how soon or for how many hours will ever be restored. As such, it is not just the rate of

unemployment that we must watch, but also the quantity of work – and corresponding pay –

being done by those in work.

Never, in previous economic downturns, has the average working week been cut so severely.

5February 2021

Changes in Demand

As such, the other barometer to watch is how average working hours rebound amongst full-time, part-

time, and all workers. In relation the same period last year (October - December 2019):

• All worker hours were 5.2% lower

• Full-time worker hours were 5.4% lower

• Part-time worker hours were 7.8% lower

Ongoing economic impacts of the pandemic

Just 72% of UK businesses were operating In the period 8-21 February 2021 – only marginally

higher than the lowest weighted total on record since the start of the pandemic (66% in 15 to

28 June 2020). By size of enterprise, 71% of micro businesses are currently trading, compared with

88% of businesses with 250 or more employees.

Figure 4. The proportion of UK businesses (%) that were trading or had temporary closed /

paused trading, June 2020 – Feb 2021

100

86.3 86.1 84.6

90 82.4 81.5 82.7 83.9 84.4

81.6

80 80.4

72.5 72.2

78.5

70 77.1

71.6 71.0

60 70.6

65.9

50 Currently trading (%)

40

30

20

10

0

Jun-20 Jul-20 Jul-20 Aug-20 Aug-20 Aug-20 Sep-20 Sep-20 Oct-20 Oct-20 Nov-20 Nov-20 Dec-20 Dec-20 Jan-21 Jan 21 Feb-21 Feb 21

Source: FCSA analysis of ONS data

By way of the impact on company turnover, 46% of UK businesses reported that turnover was lower

than normally anticipated at this time of year, compared to 6% who stated that it was higher. The

wholesale and retail trade has the highest proportion with positive revenues (11%).

6February 2021

Changes in Demand

Figure 5. Turnover was lower than prior year: percentage of enterprises, 25 Jan-7 Feb 2021

All Industries -46 38 6

Accom & Food Service -76 11 5

Arts, Ent & Recreation -73 15 4

Education -58 30 4

Wholesale & Retail Trade -50 31 11

Admin & Support Service -49 36 6

Transportation & Storage -48 38 6

Manufacturing -45 40 8

Construction -40 45 4

Utilities -37 47 7

Prof, Scientific & Technical -35 51 4

Human Health & Social Work -34 51 4

Real Estate -30 49 9

Info & Comms -26 57 6

-90 -70 -50 -30 -10 10 30 50 70

Turnover has decreased (%) Turnover has not been affected (%) Turnover has increased (%)

Similar proportions of businesses reported lower profits (44%) than last year, rather than higher levels

(6%).

Figure 6. Profits were lower than prior year: percentage of enterprises, 25 Jan-7 Feb 2021

All Industries -44 36 6

Accom & Food Service -71 13 7

Arts, Ent & Recreation -58 18 2

Education -48 26 3

Admin & Support Service -51 30 5

Wholesale & Retail Trade -47 31 8

Construction -42 43 1

Manufacturing -40 41 6

Transportation & Storage -46 35 7

Human Health & Social Work -31 44 3

Real Estate -35 43 7

Prof, Scientific & Technical -33 47 5

Utilities -45 38 8

Info & Comms -24 55 5

-80 -60 -40 -20 0 20 40 60 80

Profits have decreased (%) Profits have stayed the same (%) Profits have increased (%)

Source for both: FCSA analysis of ONS data

7February 2021

Changes in Demand

Despite CJRS, SEISS and other scheme funds and rates exemptions, 32% of businesses that

had not permanently stopped trading, as at 25 January - 7 February, had either no (5%) or less than

3 months’ cash reserves (27%).

Far from these just being in sectors challenges with lockdowns, they are spread across all industries.

Those with increased proportions with no cash reserves this month included Construction, Admin &

Support Services and Health & Social Work.

Figure 7. Cash reserves amongst enterprises that have not permanently stopped trading, by

industry 25 Jan - 7 Feb 2021

5% 27%

All Industries

Information And Communication

Utilities

Education

Real Estate Activities

Manufacturing

Transportation And Storage

Wholesale And Retail Trade

Professional Scientific And Technical…

Human Health And Social Work Activities

Arts Entertainment And Recreation

Administrative And Support Service…

Construction

Accommodation And Food Service…

Other services

0 10 20 30 40 50 60

No cash reserves Less than 3 months

Source: FCSA analysis of ONS data

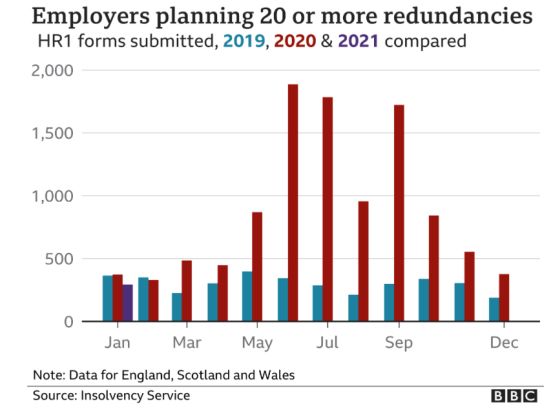

Redundancies abated as furloughing, once again,

protects workers

Just 232 employers submitted HR1 forms to the Insolvency Service in January 2021 – the lowest

figure since the pandemic began. Between them, these employers were proposing 32,000

redundancies from their workforces – a rise of 9% on the figure for January 2020, however.

Additionally, as there is no requirement for consultations on redundancies of fewer than 20 to be

notified, tens, or potentially hundreds of thousands of workers will not be included in these numbers.

8February 2021

Changes in Demand

Figure 18 Employer numbers and aggregate volumes from HR1 submissions, Jan 2019-21

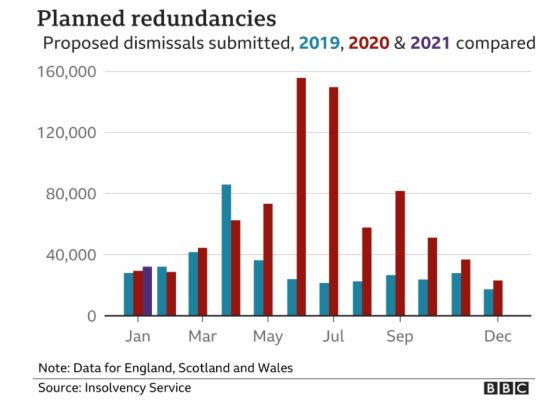

To further set the 2020 spike in context, the dramatic quarterly rise in numbers being made redundant

– despite furloughing – compares starkly to the picture in 2009 when the last economic downturn hit.

Whilst numbers declined in October - December 2020, to 343k from 395k in September - November,

this was still higher than the 2009 peak.

Figure 9. Redundancies in the preceding 3 month period, Oct-Dec 2007-2020 (000s)

450

400

Number of people made redundant in the preceding 3 months

350

300

250

200

150

100

50

0

Oct-Dec 2007

Jan-Mar 2008

Apr-Jun 2008

Oct-Dec 2008

Jan-Mar 2009

Apr-Jun 2009

Oct-Dec 2009

Jan-Mar 2010

Apr-Jun 2010

Oct-Dec 2010

Jan-Mar 2011

Apr-Jun 2011

Oct-Dec 2011

Jan-Mar 2012

Apr-Jun 2012

Oct-Dec 2012

Jan-Mar 2013

Apr-Jun 2013

Oct-Dec 2013

Jan-Mar 2014

Apr-Jun 2014

Oct-Dec 2014

Jan-Mar 2015

Apr-Jun 2015

Oct-Dec 2015

Jan-Mar 2016

Apr-Jun 2016

Oct-Dec 2016

Jan-Mar 2017

Apr-Jun 2017

Oct-Dec 2017

Jan-Mar 2018

Apr-Jun 2018

Oct-Dec 2018

Jan-Mar 2019

Apr-Jun 2019

Oct-Dec 2019

Jan-Mar 2020

Apr-Jun 2020

Oct-Dec 2020

Jul-Sep 2008

Jul-Sep 2009

Jul-Sep 2010

Jul-Sep 2011

Jul-Sep 2012

Jul-Sep 2013

Jul-Sep 2014

Jul-Sep 2015

Jul-Sep 2016

Jul-Sep 2017

Jul-Sep 2018

Jul-Sep 2019

Jul-Sep 2020

Source: FCSA analysis of ONS data

Recently published ONS data also evidences the sectoral impact of redundancies through to

September - November 2020, which shows the aggregate redundancy rate increased to a record

high of 14.2 per thousand employees between July and November 2020. The redundancy rate

for men (15.5 per thousand) was higher than that for women (12.8 per thousand).

9February 2021

Changes in Demand

The September to November data (reporting redundancies that occurred between July and

November) show that the Administrative & Support services industry had the highest

redundancy rate (35.8 per thousand employees) followed by the Other Services industry group,

which includes Arts, Entertainment & Recreation (30.5 per thousand employees). The lowest

redundancy rate was in the Public Administration, Defence & Social Security industry, at 3.3 per

thousand employees.

Figure 10. Redundancies per 1,000 employees, by sector: Jan-Mar to Sept-Nov 2020

40 All

redundancies

Agriculture, fishing,

energy & water

35

Manufacturing

Construction

30

Wholesale, retail &

repair of motor vehicles

25

Transport & storage

Accommodation & food

20 services

Information &

communication

15 Financial, insurance &

real estate activities

Professional, scientific

& technical activities

10

Administrative &

support services

Public admin &

5 defence; social security

Education

0 Human health & social

work activities

Other services

Source: FCSA analysis of ONS data

10February 2021

Changes in Demand

As to future expectations – with employers now looking at the potential closure of the CJRS a the end

of April 2021 – the forecasts obtained by the ONS in early February (25 January–7 February 2021)

now provide a window into the likely fallout of a cliff-edge scenario. Almost 9% of those within

Accommodation & Food Services plan to make cuts as do 5% in Admin & Support Services.

Figure 11. Percentage of employers planning redundancies in the next three months (25 Jan -

7 Feb 2021)

10.0%

8.8%

9.0%

% of employers planning to make redundancies in the next 3 months

8.0%

7.0% 6.5%

6.0%

5.0%

5.0% 4.4%

3.7% 3.5%

4.0% 3.2% 3.4%

2.8%

3.0% 2.5%

2.0%

2.0% 1.2%

1.0%

0.0% 0.0% 0.0%

0.0%

Source: FCSA analysis of ONS data

A study by the Resolution Foundation, Long Covid in the Labour Market, evidenced that the

number of workers who in January had been on full furlough for at least six months (475,000) is

nearly as large as the number of people in January who we estimate had been unemployed for at

least six months (689,000). Altogether, 1.9 million people had spent the past six months

unemployed or on full furlough (including those who have experienced a combination of

unemployment and full furlough, without reaching six months of either individually).

Furthermore, according to the study, 8% of workers currently employed either expect to lose their

jobs in the next three months, or have been told they would be made redundant. This figure

rises to 21% among those who have been furloughed for at least six months of the crisis.

11February 2021

Changes in Demand

UK workforce impacts: furloughed numbers surge

again in January

In their Economic & Fiscal Outlook report in late November, the OBR forecast that an average of

4.5m workers would be fully or partially furloughed across the period November to March

2021, starting with 5.9m in November, dropping to 3.3m by March.

In complete contrast to the forecasts, the figures started much lower than anticipated (3.87m in

November and 3.82m in December, according to provisional figures from HMRC).

Following the move into Lockdown 3 at the end of December, however, numbers rose to 4.7m

(HMRC provisional) by the end of January 2021.

• This was largely driven by an increase in the numbers on full furlough (Figure 15),

which rose to an average of 3.3m across January (68% of all furloughs) from an

average of 2.3m (60%) across December.

• In contrast, the number on partial furlough dropped from c.1.5m (38% of all furloughs)

to c.1.4m (28%).

Furthermore, weekly estimates from ONS surveys show a continuing rise into February – up to

c.20% by the month end. This would equate to 6m now on furlough.

Figure 12. Furlough estimates amongst business not permanently stopped trading, March

2020 – Feb 2021

35

31.3 29.8 29.6 ONS estmate: % workforce on furlough leave

30 28.4

28.1

25 19.9

18.3

24.6

20 17.1

22.3 16.9

15.5

15 15.4 19.2

15.5 15.1 13.7

10 13.7

11.9 10.8

9.4 9.3 9.0

5

7.7

0

Source: FCSA analysis of ONS data

12February 2021

Changes in Demand

Two thirds of furloughed workers remain fully

furloughed

Figure 13. Proportions of furloughed workers on full or partial furlough, or their status

underdetermined, 31 July 2020 – 31 January 2021

100%

90% Furlough

20.8% 28.4% status

80% 31.0%

39.3% 40.7% 35.4% 38.0% undetermin

70% ed

60%

50%

Partially

40% furloughed

73.6%

65.8% 67.6%

30% 58.9% 56.5% 61.0% 59.9%

20%

10%

Fully

0% furloughed

31 July 31 Aug 30 Sept 31 Oct 30 Nov 31 Dec 31 Jan

2020 2020 2020 2020 2020 2020 2021

(HMRC) (HMRC) (HMRC) (HMRC) (HMRC) (HMRC) (HMRC

provisional)

Source: FCSA analysis of HMRC data

ZHC workers still number just shy of 1 million

New ONS data relating to Zero Hours Contract (ZHC) working shows that, having peaked at 1,059k in

Q2 2020, the numbers declined in Q3 (to 957k) before rising again in Q4 (to 978k) – a similar level to

Q4 2019 (974k).

The numbers of UK nationals on ZHCs averaged 852k across 2020 compared to 761k in 2019.

Similarly, the average amongst non-UK nationals was 141k in 2020, compared to 112 across 2019.

Non-UK national numbers declined sharply across the last quarter of the year, however, whilst UK

national numbers rose sharply (as they did in Q2).

13February 2021

Changes in Demand

Figure 14. Number of UK nationals and non-UK nationals on a ZHC, Oct-Dec 2013-2020 (000s)

1,200

UK nationals on a ZHC Non UK nationals on a ZHC

1,000

800

600

400

200

0

Oct-Dec Apr-Jun Oct-Dec Apr-Jun Oct-Dec Apr-Jun Oct-Dec Apr-Jun Oct-Dec Apr-Jun Oct-Dec Apr-Jun Oct-Dec Jan-Mar Apr-Jun Jul-Sep Oct-Dec

2013 2014 2014 2015 2015 2016 2016 2017 2017 2018 2018 2019 2019 2020 2020 2020 2020

In its Labour Market reports, the ONS notes that it is likely that, whilst many ZHC workers remain

officially employed, there are little or no hours for these workers. As such, the similar numbers

remaining on the payroll, year-on-year, is potentially understandable. This likelihood appears borne

out in the underemployment data for ZHC workers, which shows that there was a spike to 34.5%

reporting underemployment in Q4 2020.

Figure 15. Employees on ZHC / not on ZHC reporting underemployment, Oct-Dec 2013-20 (%)

40.0

34.5

35.0 31.8

31.4 27.9

30.0 27.3 26.5 25.3 26.5

28.9 27.9 24.1

25.0

26.2 26.8 26.1 25.4 26.5

22.1

20.0

All workers on a ZHC: % reporting underemployment

15.0

All workers not on a ZHC: % reporting underemployment

10.0

5.0

0.0

Oct-Dec Apr-Jun Oct-Dec Apr-Jun Oct-Dec Apr-Jun Oct-Dec Apr-Jun Oct-Dec Apr-Jun Oct-Dec Apr-Jun Oct-Dec Jan-Mar Apr-Jun Jul-Sep Oct-Dec

2013 2014 2014 2015 2015 2016 2016 2017 2017 2018 2018 2019 2019 2020†1 2020†r 2020† 2020†

Source for both: FCSA analysis of ONS data

14February 2021

Changes in Demand

Job postings at c. 81% of the prior year levels

In the week ending 12 February 2021, data from Adzuna, reported by the ONS, showed that the total

number of online job adverts had reached 81% of the level in the same week a year earlier.

Figure 16. Weekly UK job vacancy index, versus same week in previous year

120

100 12/02/21

81%

80

60

40

Adzuna weekly vacancies…

20

0

Out of the 27 Adzuna categories listed below, just 4 occupational groupings had returned to prior year

levels, however. Regionally, rates range from 110% of prior year job ad numbers in Northern Ireland

to 66% in London.

Figure 17. Adzuna Job Ad category index, w/e 12 Feb 2021 versus the same week last year

140

128 125 Job vacancy index: 12 Feb 2021 v same week last year (%)

115

120 105

98 96

100 90 88

82 80 78 78 76 81

74 76

80 71 70 69 68

64 62 61

57 54

60

46

40

23

20

0

Source for both: Adzuna, reported by ONS

15February 2021

Changes in Demand and Supply

Figure 18. Adzuna regional Job Ad index: w/e 12 Feb 2021 v last year

120%

110%

100% 94% 95% 89%

87% 87% 86%

81% 79% 77%

80%

76% 75%

75%

60% 66%

40%

20%

0%

All England Wales Scotland Northern North North Yorkshire East West East of London South South

Regions Ireland East West and The Midlands Midlands England East West

Humber

Job ad volumes (%), w/e 12 Feb 2021 versus the same week last year

Source: Adzuna, reported by ONS

Company incorporations remain high

In the week ending 12 February 2021, there were a total of 16,882 company incorporations – a figure

10.5% higher than in the same week last year (15,116).

Having trended below prior-year figures since late February 2020, incorporation numbers jumped in

early May - around the time of the announcement of the Bounce Back Loan Scheme - and have since

remained higher than the previous year.

Figures 19. Number of weekly incorporations, Jan 2019 – Feb 2021

20000

18000

16000

14000

12000

10000

8000

6000

2019 2020 2021

4000

2000

0

Week 1

Week 2

Week 3

Week 4

Week 5

Week 6

Week 7

Week 8

Week 9

Week 10

Week 11

Week 12

Week 13

Week 14

Week 15

Week 16

Week 17

Week 18

Week 19

Week 20

Week 21

Week 22

Week 23

Week 24

Week 25

Week 26

Week 27

Week 28

Week 29

Week 30

Week 31

Week 32

Week 33

Week 34

Week 35

Week 36

Week 37

Week 38

Week 39

Week 40

Week 41

Week 42

Week 43

Week 44

Week 45

Week 46

Week 47

Week 48

Week 49

Week 50

Week 51

Week 52

16 Source: FCSA analysis of Companies House dataFebruary 2021

Changes in Supply

In contrast, the number of dissolutions was kept artificially low by the temporary suspension of strike-

offs/dissolutions on 2 April (through to 10 September), since which time they have started to increase

but continue to trend below prior year figures. And notably, by w/e 12 February 2021, at 5,659, they

were 7.8% lower than in the same week last year (6,140).

Figures 20. Number of weekly dissolutions, January 2019 – January 2021

9000

8000

2019 2020 2021

7000

6000

5000

4000

3000

2000

1000

0

Week 1

Week 2

Week 3

Week 4

Week 5

Week 6

Week 7

Week 8

Week 9

Week 14

Week 33

Week 50

Week 10

Week 11

Week 12

Week 13

Week 15

Week 16

Week 17

Week 18

Week 19

Week 20

Week 21

Week 22

Week 23

Week 24

Week 25

Week 26

Week 27

Week 28

Week 29

Week 30

Week 31

Week 32

Week 34

Week 35

Week 36

Week 37

Week 38

Week 39

Week 40

Week 41

Week 42

Week 43

Week 44

Week 45

Week 46

Week 47

Week 48

Week 49

Week 51

Week 52

Source: FCSA analysis of Companies House data

17February 2021

UK Labour Market Statistics

Furloughing continues to shield workers

The UK employment rate (the proportion of people aged from 16 to 64 who were in work) was 75.0% in

October - December 2020 - 1.5 percentage points lower than the same period last year and 0.3

percentage points up on the previous quarter (July-September 2020). This equated to 32,393k

people in work, in 34,685 jobs (in September – the latest available data - down 475k (1.4%) from

35,160k jobs in June 2020).

Figure 21. UK workforce composition, Oct-Dec 2020 and quarterly/annual changes

Category Number % of all in Change on Change from a year

(000) employment previous quarter earlier

All in employment 32,393 100% -114k -541k

Employees 27,895 86.1%

+48k +169k

(of which)

Zero Hours 978 3.0%

contract (Q4 2020) (3.5% of all

+21k +4k

employees employees)

(Q4 2020)

(of which) 1,564 4.8%

Temporary (5.6% all +110k +142k

employees employees)

Self-employed 4,374 13.5% -152k -652k

Source: FCSA analysis of ONS Labour Force Survey data

With the total workforce decreasing by 114k, rolling quarter-on-quarter, the balance was achieved by

39k (0.2%) more people working full-time and 153k (1.9%) fewer officially part-time

workers. This number includes a significant number of people registered as employed, however –

likely to include many of the UK’s 978k Zero Hours Contract workers - but receiving no hours or

money. A flash estimate from HMRC, from PAYE Real Time Information, shows 726k fewer

people on payrolls in early January 2021 than in February 2020 – and 2.5% (730k) lower than a

year earlier.

Year-on-Year, the balance of 541k fewer people in the workforce resulted from 560k (6.6%) less

people in part-time jobs and 19k (0.1%) more in full-time work.

18February 2021

UK Labour Market Statistics

Self-employment down 652k (13%), YoY, whilst temp up

142k (10%)

From a contingent worker perspective, self-employment fell 152k (-3.4%) QoQ. The self-

employment rate is now 13.5%. In contrast, temporary employment – in all its guises –

increased by 110k (7.6%), QoQ. The temp rate for the quarter was 4.8%. Year-on-year,

temporary employment also increased by 142k (10.0%), although this was largely courtesy of a

rise in FTC working. In contrast, self-employed numbers were 13.0% (652k) lower than a year

earlier.

5.1% (1.74m) unemployment: sharp rises amongst

older workers

The unemployment rate increased to 5.1% in October - December 2020 from 5.0% last rolling

quarter and 3.8% in the same period last year. At 1,744k, this represented a 121k (7.4%) increase

on the previous quarter and was 454k (35.2%) higher than the same period a year earlier:

• The estimated unemployment rate for men was 5.4% whilst it was 4.8% for women

• There were 124k (32.5%) more unemployed 18-24 year olds in October-December 2020 than

in the same quarter in 2019

o The rate was 15.4% amongst men & 11.3% amongst women (13.4% both)

• There were 208k (39.9%) more unemployed 25-49 year olds than a year earlier

• There was also a 47.8% (138k) YoY increase in unemployed people aged 50+

Figure 22. Unemployment numbers and rates, by age band, Oct-Dec 2020

Category Number Unemployment Change on Change from a

(000) rate previous quarter year earlier

16–17 year olds 82k 25.3% -7k -16k

18-24 year olds 507k 13.4% -5k

+124k

25-49 year olds 729k 3.8%

+79k +208k

50+ year olds 426k 3.9%

+54k +138k

Source: FCSA analysis of ONS data

19February 2021

UK Labour Market Statistics

At 307k in December, the number temporarily away

from work receiving no pay rose increased again

The increase in the officially unemployed number may be remaining artificially low as the

numbers in other groups who are out of work and could potentially be seeking employment is

countering it. Little has been published on this cohort this month, however, apart from the following:

• Estimates of the number of people in employment on the Labour Force Survey (LFS) are

consistent with the International Labour Organization (ILO) definition of employment

• Under this definition, employment includes both those who are in work during the reference

period and those who are temporarily away from a job

o The number of people who are estimated to be temporarily away from work includes

furloughed workers, those on maternity or paternity leave and annual leave

• Prior to the coronavirus (COVID-19) pandemic, there were on average 2 to 2.5 million people

temporarily away from work. The number of people temporarily away from work rose to

almost 7.9 million people in April to June 2020 but, by October 2020, had fallen to an estimate

of 3.7 million. It rose in November to 4.1m people, however.

• There were also around 307k people away from work because of the pandemic and

receiving no pay in December 2020. Whilst this has fallen from 658k in April 2020, it was

a notable increase from 211k recorded in October and 278k in November 2020.

2.6m low and no pay claimants – up 111% YoY

At 2,597k, the provisional Claimant Count in January 2021 was 20k (0.8%) lower than the

previous month but 1,368k (111.4%) higher than a year earlier.

Vacancy levels down 26%, YoY, but up 12% QoQ

There was an average of 599k job vacancies open across November 2020-January 2021 – a

quarterly increase of 12% (64k) vacancies. This figure was, however, 211k (26.0%) lower than a

year earlier.

20•

26,500,000

27,000,000

27,500,000

28,000,000

28,500,000

29,000,000

29,500,000

26,000,000

o

January 2015

February 2015

March 2015

April 2015

May 2015

June 2015

July 2015

August 2015

September 2015

October 2015

November 2015

December 2015

January 2016

February 2016

March 2016

April 2016

May 2016

across March 2020 – January 2021.

June 2016

July 2016

August 2016

September 2016

down 2.5% (730k) YoY

October 2016

November 2016

December 2016

January 2017

February 2017

March 2017

April 2017

May 2017

June 2017

July 2017

August 2017

UK Labour Market Statistics

21

September 2017

Payrolled employees

October 2017

November 2017

December 2017

January 2018

February 2018

March 2018

April 2018

May 2018

June 2018

July 2018

August 2018

September 2018

October 2018

November 2018

December 2018

January 2019

February 2019

March 2019

by 0.3% in January 2021 - equivalent to 83,000 people

April 2019

May 2019

June 2019

2.5% (730k) compared with the same period of the previous year

July 2019

August 2019

September 2019

October 2019

November 2019

December 2019

January 2020

February 2020

March 2020

Figure 23. Paid employees, seasonally adjusted – to Jan 2015-2021

April 2020

May 2020

June 2020

July 2020

August 2020

September 2020

October 2020

November 2020

December 2020

January 2021

Workers on payroll in January up 0.3% (83k) MoM, but

HMRC analysis of RTI returns has enabled a flash estimate of the significantly reduced UK payrolls

Compared with the previous month, the number of payrolled employees increased

In January 2021, HMRC estimates that there were 28.3 million payrolled employees, a fall of

Source: FCSA analysis of HMRC data

February 2021February 2021

UK Labour Market Statistics

Real-terms pay growth continues to surge, due to a

reduction in the number of lower paid jobs

In real-terms (when adjusted for CPI), regular pay growth (for GB employees, excluding bonuses)

continued to surge in the year to October - December 2020, recovering to +3.3% (up from 2.8% last

rolling quarter). Similarly, real-terms total pay growth further improved to 3.8% in the year to October-

December 2020 from an adjusted 3.0% last rolling quarter. Moreover, for the single month of

December, real-terms regular pay improved by 3.6% whilst real-terms total pay rallied

significantly by 4.4%.

o The higher percentage growth figure for total pay reflected an increase in bonus payments,

because of bonus payments being postponed from earlier in the year.

Between October to December 2019- 2020, average pay growth varied by industry sector.

o The finance and business services sector saw the highest estimated growth in total

pay, at 6.8%.

o All sectors saw positive growth, although construction (1.9%) and manufacturing (1.5%)

had smaller growth than the other sectors.

o This is an improvement on the growth rates in April to June 2020, the three-month

period with the biggest falls in average pay, when all these sectors except for the

public sector had negative growth rates.

Figure 24. Regular & Total Pay real-terms wage growth, year to Oct-Dec 2009-2020

5.0

+3.8%

4.0

+3.3%

3.0

2.0

1.0

0.0

-1.0

-2.0

-3.0

Dec 14

Dec 10

Dec 11

Dec 12

Dec 13

Dec 15

Dec 16

Dec 17

Dec 18

Dec 19

Dec 20

Dec-09

Regular Pay Total Pay

Source: FCSA analysis of ONS data

ONS has cautioned, however, that current average pay growth rates are being impacted upwards

by a fall in the number and proportion of lower- paid jobs compared with before the

coronavirus pandemic.

22February 2021

Stay Connected with FCSA

23You can also read