RESULTS PRESENTATION for the year ended 28 February 2019 - www.deltafund.co.za - Delta Property Fund

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

RESULTS PRESENTATION

for the year ended 28 February 2019

P RO P ERT Y F U N D

www.deltafund.co.za

AGENDA P RO P ERT Y F U N D

01 Introduction and Business Update

02 Financial Review

03 Portfolio Review

04 Conclusion

05 Questions & Answers

06 Annexures

P RO P ERT Y F U N D

www.deltafund.co.za

INTRODUCTION AND BUSINESS UPDATE

Sandile Nomvete

INTRODUCTION TO DELTA

Sovereign

Highly Market

underpinned

empowered fund capitalisation of

JSE listed REIT

79.0% Level 2 R1.8bn

B-BBEE

of revenue from sovereign tenants Rating on new sector codes as at 28 February 2019

Average property Assets under

Dominant in

value of management of

Pretoria &

Durban CBDs

R109.1m R11.8bn

(Feb 2018 : R109.6m) By 100% black-owned asset manager

RESULTS PRESENTATION FOR THE YEAR ENDED 28 FEBRUARY 2019

4

BUSINESS UPDATE

Delta experienced its toughest and most challenging year since its listing. Slow pace of lease renewals from DPW,

increased vacancies and higher cost of debt resulted in distributable earnings declining. The board and management

subsequently decided to retain 25% of earnings to facilitate capital expenditure and working capital in the business,

resulting in distribution of 55.39 cents per share being declared.

Leasing Progress

Robust engagement and negotiations held during FY2019

Significant progress in renewals underway in FY2020

New leasing

Vacancies

Tough economic environment with many funds impacted by higher vacancies

Bloemfontein provincial leases continue to impact vacancies with tenants moving to alternate premises

Sunninghill still challenging, however, significant progress seen in the market recently

RESULTS PRESENTATION FOR THE YEAR ENDED 28 FEBRUARY 2019

5

BUSINESS UPDATE cont…

Debt Funding

Low WALE and non-conclusion of DPW renewals significantly impacted our ability to renew expiring facilities for longer

periods

Our long-standing banking partners approved extensions, however, at higher interest costs and associated fees due to

increased risk

Disposals

Our market is limited due to our assets that are configured to sovereign tenants

BEE opportunities to acquire and secure long-term leases prevalent in the market but access to funding seen as barrier

Improvement in economic environment and increased lending by banks post elections should provide traction on

disposals

RESULTS PRESENTATION FOR THE YEAR ENDED 28 FEBRUARY 2019

6

P RO P ERT Y F U N D

www.deltafund.co.za

FINANCIAL REVIEW

Shaneel Maharaj

FINANCIAL PERFORMANCE 2019

Loan to

Extended Fixed

value of facilities totalling debt of

45.1% R2.1billion 59.8%

(Feb 2018 : 41.3%) (Feb 2018 : R941 million) (Feb 2018 : 85.4%)

Debtors outstanding Property Interest

at operating margin at cover ratio

31 days 67.8% 2.1

(Feb 2018 : 18.5 days) (Feb 2018 : 73.5%) (Feb 2018 : 2.4)

RESULTS PRESENTATION FOR THE YEAR ENDED 28 FEBRUARY 2019

8

FIVE YEAR REVIEW

2019 2018 2017 2016 2015

Revenue (R’000) 1 547 365 1 564 053 1 617 344 1 247 582 1 009 207

Net property income (R’000) 1 037 786 1 149 885 1 153 341 925 531 764 884

Finance costs (R’000) 537 281 482 179 470 580 412 713 316 380

Cost to income ratio - gross method 32.2% 26.5% 28.8% 26.4% 26.0%

Cost to income ratio - net method 18.3% 12.1% 12.4% 12.2% 10.2%

Investment property (R’000) 11 350 331 11 507 600 11 381 421 10 095 181 8 420 400

Investment in listed securities (R’000) 461 822 381 868 429 588 472 546 502 986

Borrowings (R’000) 5 258 471 4 952 690 5 099 227 5 094 310 4 508 565

Loan to value (LTV) 45.1% 41.3% 41.5% 47.2% 49.9%

Weighted average interest rate 10.2% 9.2% 9.2% 8.8% 8.1%

Average debt expiry period (years) 0.8 1.5 1.9 2.3 2.4

Average debt fix expiry period (years) 2.1 1.5 2.2 2.1 2.4

Fixed: floating debt (excluding revolvers) 59.8% 85.4% 85.1% 83.5% 78.0%

Net asset value per share (exclusive of deferred tax) R9.30 R10.06 R9.91 R10.61 R10.02

RESULTS PRESENTATION FOR THE YEAR ENDED 28 FEBRUARY 2019

9

DISTRIBUTABLE INCOME STATEMENT

Feb 2019 Feb 2018

Net property income (excl. straight line accrual) 1 072 090 1 147 865

Administration expenses (79 727) (53 329)

Net finance costs (511 249) (462 483)

Dividend income - GRIT 39 187 35 666

Other income 6 356 20 287

Antecedent interest 569 257

Prior year retained earnings distributed - 3 378

Distributable income for the period 527 226 691 641

Number of shares in issue 714 229 718 711 844 486

Full year distributable earnings per share (cents) 73.84 97.24

Distribution per share declared for the year (cents) 55.39 97.24

RESULTS PRESENTATION FOR THE YEAR ENDED 28 FEBRUARY 2019

10ANALYSIS OF DISTRIBUTIONS DECLARED

HISTORIC DISTRIBUTION PER SHARE (CENTS/SHARE)

H1 – Interim 23.1% 9.6% 15.6% 7.2% 8.7% 8.0% 7.1% 7.1% 7.1% 1.0% (1.0)% 0% (15.1)% (68.5)% (43,0)%

H2 – Final

Total – Full year

97,24 97,24

90,8

84,1

72,7

55,39

51,3 50,8

47,9 45,9 46,4

44,1 42,9

40,2 40,0 39,4

32,5

23,7

16,0

FY2013 H1 Aug- H2 Feb- FY2014 H1 Aug- H2 Feb- FY2015 H1 Aug- H2 Feb- FY2016 H1 Aug- H2 Feb- FY2017 H1 Aug- H2 Feb- FY2018 H1 Aug- H2 Feb- FY2019

13 14 14 15 15 16 16 17 17 18 18 19

RESULTS PRESENTATION FOR THE YEAR ENDED 28 FEBRUARY 2019

11DISTRIBUTABLE EARNINGS BRIDGE

R’000

5 196 3 521 312 (3 378) (13 931)

691 641 6 466 (19 953)

(36 642)

(48 767)

(57 240)

527 224

H2 Feb 2018 Net property Admin Dividend Antecedent Prior year Other income Vacancies Disposals Net finance Provisions H2 Feb 2019

income expenses income (Grit) dividend retained costs raised

earnings

distributed

RESULTS PRESENTATION FOR THE YEAR ENDED 28 FEBRUARY 2019

12LIKE-FOR-LIKE NET PROPERTY INCOME ANALYSIS

Amount

Description %

(R’000)

Net property income (NPI) Feb 2018 1 147 865

Increased NPI from base portfolio held at 28 Feb 2018 (36 353) (3.2)%

NPI attributable to disposals and non-core assets FY18 (39 422) (3.4)%

NPI Feb 2019 (excl. straight line accrual) 1 072 090 (6.6)%

Increased NPI from base portfolio held at 28 Feb 2018 (36 353)

NPI attributable to Disposals and non-core assets FY19 690

Like-for-like increase in NPI Feb 2019 (35 663) (3.1)%

RESULTS PRESENTATION FOR THE YEAR ENDED 28 FEBRUARY 2019

13STATEMENT OF FINANCIAL POSITION

R’000 Feb 2019 Feb 2018 Change %

ASSETS

Non-Current assets 10 377 347 10 919 425 (4.96%)

Investment property 9 913 811 10 535 000 (5,96%)

Fair value of property portfolio 9 755 209 10 342 418 (5.68%)

Straight line rental income accrual 158 602 192 582 (17.64%)

Investment in other assets 461 822 381 868 20.94%

Other non-current assets 1 714 2 557 (32.97%)

Current assets 453 205 543 256 (16.58%)

Non-current assets held-for-sale 1 436 520 972 600 47.70%)

Total assets 12 267 072 12 435 281 (1.35%)

EQUITY AND LIABILITIES

Total equity 6 641 445 7 158 592 (7.22%)

Liabilities 5 625 627 5 276 689 6.61%

Non-current liabilities 1 470 696 2 720 230 (45.93%)

Current liabilities 4 154 931 2 556 459 62.53%

Total equity and liabilities 12 267 072 12 435 281 (1.35%)

RESULTS PRESENTATION FOR THE YEAR ENDED 28 FEBRUARY 2019

14NAV BRIDGE

Rands

0.11 0.02

0.62

10,06

-0.93

-0.32

9.30

-0.20 -0.02

-0.02 -0.01 -0.01

28 Feb 2018 Contribution Fair value of Dividend Dividend paid Fair value of Deferred Fair value of Debt facilities Disposals FCTR recognised 28 Feb 2019

from operations listed reinvestment investment consideration financial raised in profit and loss

investments property settled instruments &

forex losses

RESULTS PRESENTATION FOR THE YEAR ENDED 28 FEBRUARY 2019

15DEBT SUMMARY

As at 28 February 2019

Facility Type R’ m Weighted Ave. Rate

Floating bank facilities 4 339 11.0%

Fixed bank facilities 212 9.5%

Revolving bank facilities 706 9.7%

Total borrowings, net of accrued interest 5 257 10.2%

Accrued interest 17

Debt Structuring fees (16)

TOTAL 5 258

Total fixed bank facilities 212 9.5%

Interest rate swap contracts 2 020 7.9%

Cross currency swaps 139 Libor + 2.9%

Total fixed 2 371

Fixed % (excluding revolvers) 59.8% 10.2%

RESULTS PRESENTATION FOR THE YEAR ENDED 28 FEBRUARY 2019

16DEBT COMMENTARY

Extended R2.1billion in expiring debt facilities during the year

59.8% (2018: 85.4%) of borrowings are fixed for an average period of 0.8 years (2018: 1.5) using a

combination of interest rate swaps, cross currency swaps and fixed facilities. The deterioration in fix % was

due to fixed facilities being converted into floating facilities when extended

The weighted average cost of debt increased to 10.2% (2018: 9.2%) primarily due to higher interest rates

on facilities extended

Loan to value ratio increased to 45.1% (2018: 41.3%),impacted by the negative fair value adjustment on

investment properties of R227 million coupled with increased borrowings. We expect an improvement in

the LTV once leases are concluded and the portfolio is revalued

Interest cover ratio at 2.1 (2018: 2.4), impacted by higher interest costs and vacancies

RESULTS PRESENTATION FOR THE YEAR ENDED 28 FEBRUARY 2019

17P RO P ERT Y F U N D

www.deltafund.co.za

PORTFOLIO REVIEW

Otis TshabalalaOPERATIONAL PERFORMANCE 2019

Total lease

A distinct focus on

Capital

renewals in a

sovereign tenants expenditure

challenging environment

73.6% R115 million 151 018m 2

Gross lettable area (GLA) (Feb 2018 : R185.4 million (Feb 2019 : 46 833m2)

Bulk lease renewal

Vacancies Total new leases

proposal to DPW

of concluded

(PMTE)

10.8% 12 537m 2 227 550m2

14.4% including assets held for sale

Retail and office other Renewed 88 185m2 (37 leases) post Feb 19

(SAPOA average 11.0%)

RESULTS PRESENTATION FOR THE YEAR ENDED 28 FEBRUARY 2019

19REPRESENTATION BY PROVINCE AND MAJOR TENANTS

BUILDINGS REPRESENTED BY PROVINCE REPRESENTATIVE TENANTS

No of Buildings GLA (m2)

Gauteng 35 402 382

KwaZulu-Natal 17 278 264

Free State 17 85 980

Mpumalanga 11 30 251

Limpopo 7 44 885

Northern Cape 7 37 275

Western Cape 5 41 889

Eastern Cape 3 23 717

North West 2 5 780

Total 104 950 422 Limpopo

Mpumalanga

Gauteng

North West

Free KwaZulu

State Natal

Northern

Cape

Eastern

Cape

Western

Cape

RESULTS PRESENTATION FOR THE YEAR ENDED 28 FEBRUARY 2019

20PORTFOLIO BREAKDOWN

Office -

Office - Other Industrial Retail Total

Sovereign 1

Number of properties 81 16 4 3 104

Gross lettable area (m2) by building type 4 693 737 192 711 40 258 23716 950 422

Vacancy (%) 10.9% 24.3% 33.1% 5.7% 14.4%

Value R8.8bn R2.1bn R0.2bn R0.3bn R11.4bn

Average rental (R/m2) 2 128.43 87.6 60.3 127.5 119.5

Weighted ave. escalation (%) 2 6.5% 6.5% 7.4% 7.3% 6.6%

Weighted ave. lease expiry

2.1 years 1.8 years 0.7 years 5.2 years 2.1 years

(by revenue) - by building type 3

Weighted ave. lease expiry

2.1 years 1.7 years 0.7 years 2.8 years 2.1 years

(by revenue) - tenant specific 2

Cost to income ratio (net) 12.7% 25.1% 7.1% 30.8% 18.3%

Cost to income ratio (gross) 24.4% 42.1% 29.7% 39.9% 32.2%

1 Multi tenant buildings are classified according to majority tenant type. Office – Other buildings therefore contain a minority element of sovereign tenants

2 This classification looks specifically at the tenant type within each building

3 Renewals in effect. Sovereign rentals & portfolio weighted average leaves expiry at year end were respectively R128.2 and 1.2 years

4 The GLA is classified by the majority of the tenants in the buildings and includes vacancy. Sovereign tenanted GLA is 598 661 m2 with total tenanted GLA of 813 436 m 2

RESULTS PRESENTATION FOR THE YEAR ENDED 28 FEBRUARY 2019

21DETAILED TENANT BREAKDOWN

TENANT PROFILE BY GLA TENANT PROFILE BY RENTAL

1,7%

7,4%1,7%

3,3%

7,4%

6,9%

Office - Sovereign National Government 11,9%

11,9%

38,6%

16,2% 38,7% Office - Other Provincial

Government 7,2%

Retail Local Government

6,8%

11,9%

73,6% Industrial State-Owned 79,0%

12,4%

Enterprise

21,3%

15,7%

2

Excludes vacancies. Total occupied GLA = 813 426m

RESULTS PRESENTATION FOR THE YEAR ENDED 28 FEBRUARY 2019

22UPDATE ON DPW

New cabinet trimmed from 36 to 28 ministers

• is in line with first world countries

• 6 departments have been merged

DPW has been expanded to include Infrastructure & Development and is now known as

the Department of Public Works & Infrastructure Development

Minister De Lille appointed as Minister of Public Works & Infrastructure Development

• widely known as a woman of action and integrity and is generally held in high esteem

RESULTS PRESENTATION FOR THE YEAR ENDED 28 FEBRUARY 2019

23UPDATE ON DPW cont…

Impact on Delta

We believe there will be minimal impact on space requirement from the

departments that have been merged

• The staff component at operational level is expected to largely remain the same

given that

• Government is on a drive to create employment, which has culminated in the Department of

Labour being renamed Department of Labour & Employment

• Organised labour is vocal and active on job creation & job losses

We believe with Minister De Lille at the helm, there will be an impetus to

transacting with DPW

RESULTS PRESENTATION FOR THE YEAR ENDED 28 FEBRUARY 2019

24DPW LEASING UPDATE

Since the interim period, DPW has implemented Supply Chain Management (SCM)

Circular 48 which governs the terms with which DPW transacts with landlords:

The bulk lease renewal process is currently in its final stages

Delta currently qualifies for a maximum of 5 years with DPW

Delta has managed to secure a mixed bag of 3 to 5 year terms on the leases signed

There are ongoing discussions regarding the maximum tenures for REITS

RESULTS PRESENTATION FOR THE YEAR ENDED 28 FEBRUARY 2019

25DPW LEASING UPDATE cont…

At present the final tenure is largely driven by the the user departments’ requirements

Where the user department requires a short-term lease, for reasons such as the

individual space requirements not meeting their needs, DPW is compelled to comply

with the user’s request

Where the user department requests a longer lease term than 5 years, DPW has

proposed an additional 4 year 11 month term as an option to meet the user’s request.

• We have, however, advised DPW that we do not consider this as a 9 years & 11 month lease and

view it as a 5 year lease

Where the user department has not reverted back to DPW with its requirements

• DPW is confirming 3 year tenures with a 3 month notice period at prevailing rentals as stipulated in

Circular 48

• We continue to negotiate around these lease clauses

RESULTS PRESENTATION FOR THE YEAR ENDED 28 FEBRUARY 2019

26UPDATE ON SOVEREIGN TENANTS

Bulk renewal progress

• Stage 1 (DPW) and Stage 2 (user department) are 100% complete

• Stage 3 status: 37 leases totalling 88 185m² have been signed to date

• The remaining 139 365 m2 anticipated to be signed between June & July

Number

Status GLA

of Leases

Lease agreements concluded and signed 37 88 185 m²

Under negotiation 22 139 365m²

TOTAL 59 227 550 m²

RESULTS PRESENTATION FOR THE YEAR ENDED 28 FEBRUARY 2019

27LEASING UPDATE

Major leases concluded

151 018m2 were renewed of which 46 833m2 to the value of R113 million were renewed as at Feb 2019

The most notable renewals are:

Building Tenant GLA

In 2 Fruit Building In 2 Food 11 177 m²

Unisa House UNISA 9 068 m²

101 De Korte MMI 6 610 m²

5 Simba Road ESKOM 5 253 m²

Auditor General Auditor General of SA 2 130 m²

Domus National Heritage Council SA 1 127 m²

Du Toitspan Dept. of Correctional Services 1 090 m²

Total 36 455 m²

RESULTS PRESENTATION FOR THE YEAR ENDED 28 FEBRUARY 2019 28

28LEASING UPDATE cont….

Several new leases were concluded measuring 12 537m2 to the value of R71.6 million

The most notable new deals are:

Building Tenant GLA

Liberty Towers Mr Price 3 833 m²

5 Walnut Merchants SA 1 524 m²

TOTAL 5 357 m²

Tenant Retention

Tenant retention remains a significant focus for Delta

RESULTS PRESENTATION FOR THE YEAR ENDED 28 FEBRUARY 2019 29

29GEOGRAPHICAL AND GRADE SPLIT

GLA - BY BUILDING RENTAL - BY BUILDING

Gauteng (42.3%) Gauteng (44.7%)

KwaZulu-Natal (29.3%) KwaZulu-Natal (24.4%)

Free State (9.1%) Limpopo (9.3%)

Limpopo (4.7%) Free State (6.3%)

Western Cape (4.4%) Western Cape (5.5%)

Northern Cape (3.9%) Northern Cape (3.7%)

Mpumalanga (3.2%) Eastern Cape (3.1%)

Eastern Cape (2.5%) Mpumalanga (2.8%)

North West (0.6%) North West (0.5%)

OFFICE GRADE - BY GLA OFFICE GRADE - BY RENTAL

A (15.5%) A (21.4%)

B (84.2%) B (78.5%)

C (0.3%) C (0.1%)

RESULTS PRESENTATION FOR THE YEAR ENDED 28 FEBRUARY 2019

30VALUATIONS

The portfolio including non-current assets held for sale decreased by 1.96% to R10.4 billion

Value Feb 2019 Value Feb 2019

Number of Properties Growth/(Loss) Percentage

Pre Valuation Post Valuation

104 properties R11 577 330 103 R11 350 330 000 (R227 000 103) (1.96%)

94 properties* R10 608 346 640 R10 397 230 000 (R211 116 640) (1.99%)

*Post transfer of 10 Bloemfontein properties to non-current assets held for sale

Marginal decrease in value, in the context of an incredibly difficult trading year not only for Delta but for most listed

REITs in general

Reversions in light of recent renewals with DPW

Average cap rates of between 10% to 12% and the average portfolio value of R11 942 per m 2

Valuers factored prevailing market conditions, rentals and tenures into their valuations

We intend to revalue the portfolio once all bulk renewals are completed

RESULTS PRESENTATION FOR THE YEAR ENDED 28 FEBRUARY 2019

31DISPOSAL OF NON-CURRENT ASSETS

During the 2019 financial year, Delta sold one building, 12 New Street, for a total of R15.8 million. Subsequently Top Trailers site 1

transferred post year end, for R45 million

Property Building Classification Location GLA (m2) Sales price (R) Transfer Date

12 New Street Office - Sovereign Johannesburg CBD 2 368 15 750 000 27-Nov-18

Transferred FY2019 2 368 15 750 000

As at Feb 2019, Delta had approximately R1.4 billion on the disposal list at book value, of which 4 assets were concluded for

R311.8 million

Property Building Classification Location GLA (m2) Sales price (R) Expected transfer Date

Top Trailers site 1 Industrial Wadeville, Johannesburg 15 741 45 000 000 9-May-19

Broadcast House Office - Sovereign Mthatha, Eastern Cape 4 934 33 000 000 End June 2019

Protea Coin Cape Town Office - Other Saxenberg Park, Cape Town 5 700 10 000 000 End July 2019

Block G Office - Sovereign Pretoria CBD 7 991 230 000 000 End August 2019

Sale agreements concluded 34 366 318 000 000

6 other non-current assets held for sale 53 396 635 100 000

10 other non-current assets transferred

Office - Sovereign Bloemfontein Portfolio 59 427 483 420 000

from Investment Property

TOTAL NON-CURRENT ASSETS HELD FOR SALE 147 189 1 436 520 000

An additional 10 buildings from the Bloemfontein portfolio to the value of R483.4m were added onto the disposal list

• Negotiations on these buildings are well advanced

RESULTS PRESENTATION FOR THE YEAR ENDED 28 FEBRUARY 2019

32CAPEX | EXISTING PORTFOLIO

Budget Tenant FY 2020 FY 2021 FY 2022 Total Capex

Installation

FY2020

Bulk Renewals 70 000 000 98 300 000 117 500 000 68 800 000 354 600 000

Balance of properties 95 000 000 113 000 000 77 900 000 284 900 000

Total Portfolio 70 000 000 193 300 000 230 500 000 146 700 000 639 500 000

Commission Poyntons Fire

Property Embassy Building Beacon Hill 17 Harrison Street

House Project

Approved budget 16 000 000 28 000 000 40 000 000 32 500 000 4 500 000

Remaining budget Completed Completed 26 065 031 5 666 507 Completed

Description Tenant installation to Façade Upgrade, Internal Creating fire lobbies, Tenant installation

all floors for new Lifts and Tenant refurbishment of sprinklers, hydrant and replacement of

tenant secured Installation. Complex tenant space system and smoke escalators

project. Weather Turnkey contractor detection

dependant appointed compliance

RESULTS PRESENTATION FOR THE YEAR ENDED 28 FEBRUARY 2019

33SUSTAINABILITY & GREENING INITIATIVES

Delta Property Fund is investigating the implementation of a Solar PV solution

This would reduce Delta’s carbon footprint

There is renewed focus on environmentally conscious landlords by tenants and investors

Benefits to Delta would include

Generation of carbon credits due to reduced footprint

Generating non GLA rental which will in turn result in increased valuation of the property

Long-term leases which may positively impact the WALE

Opportunity to better manage unforseen percentage increases in the cost of power which

will affect property net income

A pilot project for the installation of the Solar PV systems is being considered on 3 properties

RESULTS PRESENTATION FOR THE YEAR ENDED 28 FEBRUARY 2019

34P RO P ERT Y F U N D

www.deltafund.co.za

CONCLUSION

Sandile NomveteCONCLUSION

The conclusion of South Africa’s sixth democratic election is expected to provide much needed political

stability and improved business confidence within the economy. This transition is expected to materialise

within twelve months, whereby we envisage positive capital inflow and further stability to interest rates

FY 2020 is going to be one of Delta’s most exciting and busiest years:

• Concluding bulk lease renewal

• Formulating, planning and executing capex linked to TI and general building condition

• Refinancing of expiring debt and managing forward looking debt expiry

• Driving significant effort into disposals to reduce debt and generate cash for capex and working capital

• Filling vacancies across the portfolio

Delta’s board and management remain committed to its sovereign strategy

RESULTS PRESENTATION FOR THE YEAR ENDED 28 FEBRUARY 2019

36P RO P ERT Y F U N D

www.deltafund.co.za

THANK YOU

Questions & AnswersANNEXURES P RO P ERT Y F U N D

01 Government Precinct Pretoria

02 Top 10 properties by value

03 Lease Expiry Profile

04 Sectorial Split

05 GLA and vacancy reconciliation

06 Leasing Outlook

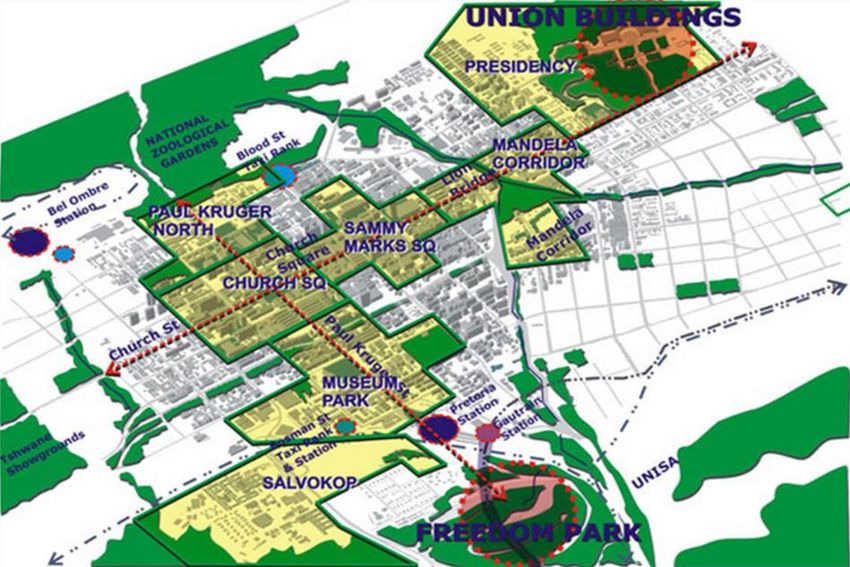

07 Growth / ReversionGOVERNMENT PRECINCT | PRETORIA

RESULTS PRESENTATION FOR THE YEAR ENDED 28 FEBRUARY 2019

39TOP 10 PROPERTIES

Forum Building Poyntons Liberty Towers Hallmark Building Delta Towers

Location Pretoria Location Pretoria Location Durban Location Pretoria Location Durban

Office - Office - Office -

Sector* Sector* Sector* Office - Other Sector* Sector* Office - Other

Sovereign Sovereign Sovereign

GLA 41 003 m2 GLA 73 396 m2 GLA 40 080 m2 GLA 26 255 m2 GLA 41 677 m2

Valuation R673 mil Valuation R576 mil Valuation R426 mil Valuation R410 mil Valuation R405 mil

* Building sector determined by majority occupation of a tenant type. Some buildings have different types in occupation

RESULTS PRESENTATION FOR THE YEAR ENDED 28 FEBRUARY 2019

40TOP 10 PROPERTIES | CONTINUED

Isivuno House Embassy Building Hensa Towers The Marine NPA Building

Location Pretoria Location Durban Location Polokwane Location Durban Location Cape Town

Office - Office - Office - Office -

Sector* Sector* Sector* Sector* Office - Other Sector*

Sovereign Sovereign Sovereign Sovereign

GLA 23 694 m2 GLA 32 829 m2 GLA 13 675 m2 GLA 24 655 m2 GLA 10 552 m2

Valuation R373 mil Valuation R338 mil Valuation R303 mil Valuation R260 mil Valuation R249 mil

* Building sector determined by majority occupation of a tenant type. Some buildings have different tenant types in occupation

RESULTS PRESENTATION FOR THE YEAR ENDED 28 FEBRUARY 2019

41LEASE EXPIRY PROFILE AT 28 FEBRUARY 2019

TOTAL PORTFOLIO - BY GLA TOTAL PORTFOLIO - BY RENTAL

Vacant (14.4%) Month to Month (38.6%)

2,8%

3,0%

14,4% 6,3% 2,5%

2,4% Month to Month (34.0%) 2,1% 29 Feb 20 (17.8%)

8,3%

29 Feb 20 (15.7%) 9,8%

38,6% 28 Feb 21 (22.9%)

28 Feb 21 (19.4%)

19,4% 28 Feb 22 (9.8%)

29 Feb 22 (8.3%)

34,0% 22,9% 28 Feb 23 (2.1%)

28 Feb 23 (2.4%)

29 Feb 24 (6.3%)

15,7% 29 Feb 24 (3.0%)

17,8%

Beyond 28 Feb 2024 (2.8%) Beyond 29 Feb 2024 (2.5%)

RESULTS PRESENTATION FOR THE YEAR ENDED 28 FEBRUARY 2019

42SECTORAL SPLIT

GLA - BY BUILDING GLA - BY TENANT*

2,5% 4,2% 6,9% 3,3%

Office - Sovereign (73.0%) Office - Sovereign (73.6%)

Office - Other (20.3%) 16,2% Office - Other (16.2%)

20,3%

Retail (2.5%) Retail (6.9%)

73,0% Industrial (4.2%) Industrial (3.3%)

73,6%

RENTAL - BY BUILDING RENTAL - BY TENANT

2,1% 1,7% 1,7%

7,4%

14,9%

Office - Sovereign (81.3%) Office - Sovereign (79.0%)

11,9%

Office - Other (14.9%) Office - Other(11.9%)

Retail (2.1%) Retail (7.4%)

Industrial (1.7%) Industrial (1.7%)

81,3% 79,0%

*

Excludes vacancies. Analysis focuses on what category the specific tenant falls into, rather than the category of the building

RESULTS PRESENTATION FOR THE YEAR ENDED 28 FEBRUARY 2019

43GLA AND VACANCY RECONCILIATION

Properties (No.) Total GLA (m2) Vacant GLA (m2) Vacancy (%)

As at 28 February 2018 105 952 428 112 225 11.8%

Disposals 1 (2 368) -

Leases terminated - - 36 789

New letting of vacant space - - (12 537)

Adjustments - 361 508

As at 28 February 2019 104 950 422 136 986 14.4%

RESULTS PRESENTATION FOR THE YEAR ENDED 28 FEBRUARY 2019

44LEASING | OUTLOOK

Anticipated budgeted sovereign renewals

W.A. Expiry W.A. Proposed Escalation /

Sector No of Leases Total Area

Rate / m2 * Rate / m2 * (Reversion)

Leases on month-to-month or expiring by 31 August 2019

National government 49 198 559 109.87 100.74 (8.31%)

Provincial government 12 53 767 169.38 124.23 (26.65%)

Local government 4 38 650 144.76 103.31 (28.64%)

State-owned enterprise 15 36 752 110.96 107.62 (3.01%)

TOTAL 80 327 728 123.87 105.67 (14.69%)

*

All rentals quoted are gross rentals

RESULTS PRESENTATION FOR THE YEAR ENDED 28 FEBRUARY 2019

45GROWTH / REVERSION

Total leases concluded 1 March 2018 – 28 February 2019

W.A Term W.A. Expiry W.A. Achieved Growth / W.A. Esc.

No of Leases Total Area (m2)

(months) Rate (R / m2) * Rate (R / m2) * (Reversion) achieved

Renewed leases 50 46 833 19.12 112.22 107.93 (3.82%) 7.04%

Renewals by Sector

W.A. Term W.A. Expiry W.A. Achieved Escalation / W.A. Esc.

Sector No of Leases Total Area

(months) Rate / m2 * Rate / m2 * (Reversion) Achieved

National Government 1 1 090 36.00 100.26 112.36 12.07% 6.00%

State-owned enterprise 3 7 603 23.72 148.25 115.82 (21.87%) 6.32%

Industrial 4 11 177 6.00 77.17 83.34 8.00 0.00%

Office – other 21 23 593 20.05 105.90 103.84 (1.95%) 6.76%

Retail 21 3 370 40.48 191.42 196.78 2.80% 7.91%

Total 50 46 833 19.12 112.22 107.93 (3.82%) 7.04%

*All rentals quoted are gross rentals

RESULTS PRESENTATION FOR THE YEAR ENDED 28 FEBRUARY 2019

46NOTES

RESULTS PRESENTATION FOR THE YEAR ENDED 28 FEBRUARY 2019

47NOTES

RESULTS PRESENTATION FOR THE YEAR ENDED 28 FEBRUARY 2019

48You can also read