BUILDING A BETTER RESOURCE INVESTMENT COMPANY - JULY 2021

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

BUILDING A BETTER RESOURCE

INVESTMENT COMPANY

JULY 2021

FORWARD LOOKING STATEMENTS

This presentation contains “forward-looking information” within the meaning of applicable Canadian securities legislation and United Stated federal securities laws. Forward-

looking information includes, but is not limited to, information with respect to future operating and development plans, the adequacy of Norvista’s financial resources,

business plans and strategy and other events or conditions that may occur in the future. Generally, forward-looking information can be identified by the use of forward-looking

terminology such as “plans”, “expects”, or “does not expect”, “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates”, or “does not anticipate”, or

“believes” or variations of such words and phrases or state that certain actions, events or results “may”, “could”, “would”, “might”, or “will be taken”, “occur”, or “be achieved”.

Forward-looking information is subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or

achievements of Norvista to be materially different from those expressed or implied by such forward-looking information, including risks associated with the competitive nature

of the resource and financial services markets, the effect of government regulation and compliance on Norvista and its industry, reliance on key personnel and the uncertainty of

future market conditions, including its impact on resource and financial services. Forward-looking information is based on the reasonable assumptions, estimates, analysis and

opinions of management made in light of its experience and its perception of trends, current conditions and expected developments, as well as other factors that management

believes to be relevant and reasonable in the circumstances at the date that such statements are made, but which may prove to be incorrect. Assumptions have been made

regarding, among other things: Norvista’s limited operating history, Norvista’s ability to manage future capital needs and the uncertainty of availability of additional financing,

the competitive nature of the resource and financial services industry, currency exchange risks, the need for Norvista to manage its planned growth and expansion, Norvista’s

ability to protect its proprietary rights, the effect of government regulation and compliance on Norvista and the resource and financial services industry, the ability of Norvista

to maintain properly working systems, reliance on key personnel, global economic and financial market deterioration and impeding access to capital or increasing the cost of

capital, volatile securities markets impacting security pricing unrelated to operating performance and the ability of Norvista to enforce judgments against a foreign corporation

and its management. Readers are cautioned that the foregoing list is not exhaustive of all factors and assumptions which may have been used. Although Norvista has attempted

to identify important factors that could cause actual results to differ materially from those contained in forward-looking information, there may be other factors that cause

results not to be as anticipated, estimated or intended. There can be no assurance that such information will prove to be accurate, as actual results and future events could differ

materially from those anticipated in such information. Accordingly, readers should not place undue reliance on forward-looking information. Norvista does not undertake to

update any forward-looking information, except in accordance with applicable securities laws.

2

OVERVIEW

● Norvista is a publicly listed resource-focused merchant bank

and investment company. This structure provides three key

POSITIONING

advantages over traditional investment vehicles:

NORVISTA

1. Available to All 2. No Investment 3. Liquidity for TO TAKE

ADVANTAGE OF

Investors Restrictions Investors without

Disrupting

Investment Strategy

● Three key pillars of our plan to transform the Company:

THE COMING

$

COMMODITY

1. Scale 2. Diversification 3. Hedging

BULL MARKET

getting AUM to size that reducing single asset mitigate macro risk with

makes sense exposure & liquidity risk commodity-linked hedges

3

BUILDING IT BETTER

Investment Issuers like Norvista have existed for years but there

have been very few long-term successes. Notable issues include:

1. Trading at a Discount to NAV

2. Uneconomic Scale (Operating Costs >2% AUM)

3. Insufficient Investment Liquidity to Manage Costs CREATING A

The issues are solvable – creating the potential for a better

publicly listed resource investment vehicle.

NEW BREED OF

We plan to take the following steps that we believe will address

all three issues: INVESTMENT

1. Scale – merge with similarly undersized companies plus

equity raises to get to an economic scale

2. Diversify & Hedge the Portfolio

ISSUER

3. Buybacks & Dividends Once at Scale

4. Minimize Operating Expenses

We expect the transformation process to take 18-24 months to

complete

4Goal

The Path Forward Become a >C$250M

Publically Listed Resource

+24 Months Investment Company

• Institute a regular dividend and

First Six Months buyback program

• Continue Portfolio Transition • Continue Acqusitions & Share Swaps

• One or more Acqustions of Similar

Companies Objective: +C$50M Market Cap

• One or more Share Swaps

• Develop & Implement Marketing

THE PATH TO

Strategy

CREATING A

Objective: +C$20M Market Cap

SUSTAINABLE

First 12-18 Months BUSINESS

• Portfolio Repositioned for Long

Term Strategy

Day One • Two or more Acqustions of Similar

Companies

• New Management • Two or more Share Swaps

• Start Portfolio Transition to Long

Term Strategy Objective: +C$40M Market Cap

5A DIFFERENT INVESTMENT APPROACH

● Investments are split into three portfolios: Merchant Banking, Quantitative & Hedging

Merchant Banking – Driving Alpha Quantitative – Liquidity with Plus Beta Performance

to Resources

Focuses on taking advantage of value dislocations Uses a seven-step quantitative methodology 1 to

within the junior resource space identify equity investment opportunities in junior and

The mandate for this portfolio is broad and could mid-cap resource space

include investments like: Demonstrates outperformance vs traditional ETFs

• Equity investments in undervalued publicly listed over the long-term 2

companies

• Equity investments in private companies

• Royalties Hedging – Downside Protection

• Convertible or Traditional Debt

Hedges are put in place to protect the portfolios value

• Direct property interests against significant negative moves in the underlying

commodities

Norvista management will take a hands-on approach The additional benefit is that this provides liquidity

with the investee companies where warranted when markets are weak

1. See Appendix for methodology details

2. Based on back-testing the quantitative methodology, actual performance may differ from historical returns 6Capital Markets Profile

CAPITAL STRUCTURE SHARE OWNERSHIP

Ticker TSX-V: NVV Management & Directors

5.6%

Share Price (July 21, 2021) C$0.10

52-Week Trading Range C$0.095 – C$0.23 Institutions

16.1%

Basic Shares Outstanding 70.1M

Options1 6.4M

FD Shares Outstanding 76.5M

Market Capitalization (Basic) C$7.0M

Cash ~C$0.76M

Market Value of Equity Portfolio2 C$9.0M

Debt Nil

Net Asset Value per Share2 C$0.129

Retail & High Net Worth

Discount to Net Asset Value 22% Investors

1. 6,400,000 options outstanding with a weighted average exercise price of C$0.128 per share

78.3%

2. Reflects market prices of equity portfolio as of July 31, 2021 plus net working capital divided by fully diluted

in-the-money shares outstanding

7Current Portfolio Construction 1 Asset Breakdown (%)

Other Investments &

Working Capital,

12.8%

Investments C$ Per Share

Rockcliff Metals (CSE:RCLF) C$0.078 Minera Alamos

(TSXV:MAI),

Rockcliff Metals

Minera Alamos (TSXV:MAI) C$0.035 27.0%

(CSE:RCLF),

60.2%

Other Investments & Working Capital C$0.016

Total C$0.129

Asset Breakdown by Location (%) Asset Breakdown by Commodity (%) Asset Breakdown by Stage (%)

USA, 10% Africa, 0.1% Uranium, 0.2% Exploration,

Zinc, 9%

4%

Mexico, 27% Precious

Production,

Metals, 30%

27%

Canada, 63%

Development,

Copper, 60% 69%

Latin America,

0.5%

1. As at July 31, 2021

2. Working Capital is based on Cash on Hand, minus managements estimate for known liabilities and may change with future estimates/financial reports 8Core Investments

TSXV:MAI CSE:RCLF

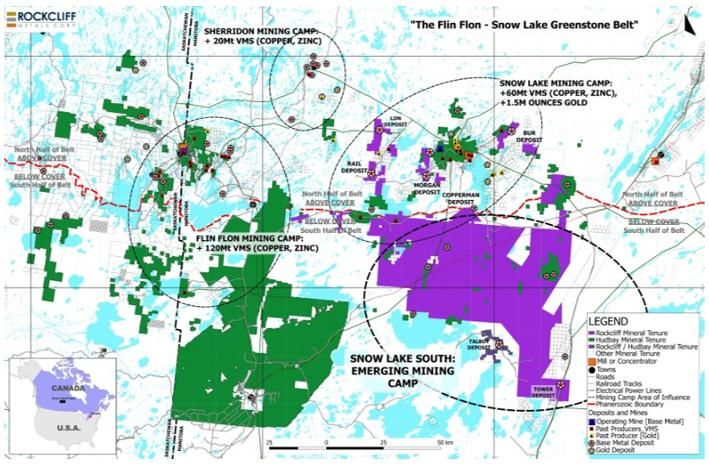

• Proven mine builders with three low-CAPEX gold projects in Mexico • Large project portfolio: 7 high-grade, copper rich VMS deposits

− Santana Project (Sonora, Mexico): commissioning open pit heap leach gold − Total NI 43-101 resources of 530M lbs CuEq at 4.16% CuEq

operation in scheduled for first production in Q3 2021

• Premier mining region: Flin Flon – Snow Lake Mining District in Manitoba

− Cerro de Oro Project (Zacatecas, Mexico): maiden inferred resource of

640,000 oz Au at 0.41 g/t Au amenable to low-cost heap leach • Near-term development potential: PEA on just 2 of its deposits outline a

7-year underground mine producing 41M lbs CuEq per year and an after-

− La Fortuna Project (Durango, Mexico): permitted gold-silver-copper project

with robust PEA for a 50K oz AuEq/year open pit mine at low AISC of

tax NPV8% of C$122M (US$3.55/lb copper price)

US$440/oz with 93% IRR at US$1,250/oz gold price − PEA in the process of being updated

• Emerging producer with +150K oz/year potential over next 3-5 years • Compelling value: trading at an EV/Project NPV of only 0.13x

Share Price C$0.60 Share Price C$0.07

% from 52-Week High 23% % from 52-Week High 50%

Market Capitalization (Basic) C$265M Market Capitalization (Basic) C$22M

Cash & Cash Equivalents C$21M Cash & Cash Equivalents C$6M

Debt Outstanding Nil Debt Outstanding Nil

Shares Owned 3,717,000 Shares Owned 72,544,000

Market Value of Holdings C$2.4M Market Value of Holdings C$5.4M

Rockcliff Land Position in the Flin Flon – Snow

P/NAV (Consensus Research) 0.56x Santana gold recovery plant (commissioning) EV/Resource C$0.03/lb CuEq Lake Greenstone Belt

Consensus Research Target Price C$1.08 EV/Project NPV8% 0.13x

Highlights based on publicly available information from each investee company 9INVESTMENT THEMES BEYOND THE CORE

● As we transition the Company’s Investments in both the Merchant Banking and Quanitative portfolios are focused

on the following macro themes

Precious Metals

• The combination of the negative real rates (low nominal rates plus high inflation) coupled with significant U.S. debt

and U.S. deficits should benefit the gold price and by association the silver price

• The reduction in COVID restrictions should result in increased M&A focused on pipeline growth for cashed up major

and mid-cap companies

Green Metals

• Both government recovery spending and global sentiment is pushing towards electrification

• Benefits multiple metals but several have limited quality investment opportunities plus underlying cyclical

supply/demand fundamentals need to be favourable

• Norvista Focus – Copper, PGMs, Lithium, Nickel

Uranium

• Fits the decarbonization/green theme but different fundamentals

• Inventory decline, restarts, lack of new production has started pushing the price higher – we expect more to come

• Focus – Producers, Developers that work at reasonable prices

10THE TEAM DRIVING THE CHANGE

Derek Macpherson • 10 years of capital markets experience primarily in research at both bank owned and boutique investment banks

(P.Eng, MBA) • As a Mining Analyst identified numerous early-stage and turnaround opportunities that were mispriced by the market

•

Executive Chairman Previously Senior VP, Investment Banking as well as a Mining Analyst at Red Cloud Securities Inc.

• Also worked six years as a metallurgist

• President & CEO of Gold79 Resources (TSXV:AUU)

• Bachelor of Engineering and Management from McMaster University and MBA from the Schulich School of Business (York University)

Samuel Pelaez • Dedicated the past decade to financing natural resource projects while serving as Chief Investment Officer and Portfolio Manager at

Galileo Global Equity Advisors, and as an analyst at US Global Investors

(CFA, M. Fin) • Early investor in numerous resource discoveries and has been an active participant in Canadian resource corporate transactions

President, Director, • President, CEO & Director of Gossan Resources (TSXV:GSS)

CEO & CIO • Bachelors of B. Administration from the Schulich School of Business and Masters in Finance from The University of Cambridge

Carmello Marrelli • CFO since 2014

(CPA) • Principal of Marrelli Support Services Inc. and DSA Corporate Services Inc.

• Previously he was a partner with Marrelli & Drake Corporate Services

CFO

• Bachelor of Commerce degree from the University of Toronto

19BOARD OF DIRECTORS

Derek Macpherson • 10 years of capital markets experience primarily in research at both bank owned and boutique investment banks

(P.Eng, MBA) • Previously Senior VP, Investment Banking as well as a Mining Analyst at Red Cloud Securities Inc.

•

Executive Chairman President & CEO of Gold79 Resources (TSXV:AUU)

• Bachelor of Engineering and Management from McMaster University and MBA from the Schulich School of Business (York University)

Samuel Pelaez • Dedicated the past decade to financing natural resource projects while serving as Chief Investment Officer and Portfolio Manager at

Galileo Global Equity Advisors, and as an analyst at US Global Investors

(CFA, M. Fin) • Early investor in numerous resource discoveries and has been an active participant in Canadian resource corporate transactions

President, Director, • President, CEO & Director of Gossan Resources (TSXV:GSS)

CEO & CIO • Bachelors of B. Administration from the Schulich School of Business and Masters in Finance from The University of Cambridge

Darren Koningen • CEO and Director of Minera Alamos Inc.

(P.Eng) • Previously the CEO of NWM Mining Corp., VP Project Development at GoWest Gold Ltd., VP Operations and VP Engineering at

Castle Gold Corp and a Senior Process Engineer (mining and metallurgy) with Kvaerner Engineering

Independent Director • Bachelor of Applied Science, Mineral Process Engineering from Queen’s University

David Regan (MBA) • Extensive career in business operations, management consulting and financial services

• CEO of Sona Nanotech Inc. and previously served as EVP, Strategy and Corporate Development at WildBrain Ltd

Independent Director

• Previously worked in New York for global management consulting firm A.T. Kearney in the Financial Institutions Group

• MBA degree from INSEAD

Jeffrey Singer (MBA) • Over 25 years of experience in the asset management industry

• Previously the Executive Vice President and Chief Investment Officer at Investors Group Inc. in Winnipeg

Independent Director

• Previously the Senior Vice President-Global Equities and Head of Global Research at the Caisse de Depot

• Spent 17 years in New York as a portfolio manager with Bernstein Investment Research and Management

• MBA degree from Harvard Business School

19CONTACT 82 Richmond Street East Toronto, ON, M5C 1P1 Derek Macpherson Executive Chairman Email: dmacpherson@norvistacapital.com Phone: 416-294-6713

Appendix 1: QUANTITATIVE PORTFOLIO PROCESS

1 Quantitative Single Factor Testing

2 Statistical Multi -Factor Construction

3 “Safe Harbour”

4 Asymmetric Risk Profile Selection

5 Active Trading Discipline Matrix

6 Options Overlay

7 Quarterly Reassessment

14Appendix 2: MODEL QUANTITATIVE PORTFOLIO PERFORMANCE1 1. Based on back-testing the quantitative methodology, actual performance may differ from historical estimates of returns 15

Appendix 3: MERCHANT BANKING PORTFOLIO

INVESTMENT EVALUATION

1 Management – track record and capability

2 Balance Sheet – capital to move the project to the next stage

3 Scarcity – good assets in good jurisdictions are rare

4 Potential – what could this be? what does that mean to value?

5 Valuation – what do we see that the market is missing?

6 Catalysts – what events are going to close the valuation gap?

16You can also read