Canadian Bank Outlook 2019: Macro Risks Moderating, Rates Rising, And Bail-In-Eligible Borrowings Under Way - S&P Global Ratings

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Canadian Bank Outlook 2019:

Macro Risks Moderating, Rates Rising, And Bail-In-Eligible Borrowings Under Way

AUTHORS

Nikola Swann Shameer Bandeally

Lidia Parfeniuk Amit Tiwari

Contents

Outlook Summary 3

Macroeconomic Backdrop 4

Canadian Banking Risks Still Low Despite 6

Deterioration

Canadian Bank Ratings All Stable But Two 10

Asset And Income Trends Healthy 12

Digitization And Cybersecurity In Focus 16

Capitalization Adequate-To-Very Strong Despite 18

Headwinds

Asset Quality As Good As It Gets 19

Funding And Liquidity Steady As Bail-In Regime 22

Implemented

Jan. 18, 2019 2

The Outlook For Canadian Banks Is Mostly Stable

Improving Neutral Worsening

We expect decelerating but still relatively strong economic growth, with increasing rates. We expect banking industry

Macro

risks to remain stable, and our base case presumes growth in consumer debt and house prices will moderate, albeit

environment from elevated levels, in 2019.

Our expected macroeconomic backdrop implies continued growth, in 2019, in loans and net interest margin (NIM)

Revenues & driven by corporate lending. We also expect wealth management and foreign operations to represent increasingly

Expenses significant proportions of revenue, but market-sensitive income to remain a drag. On the expense side, we expect

gradual progress with digitization to continue to lower input costs, but cybersecurity spending to increase.

We expect profitability to hold largely steady, in 2019, as accelerating net interest income (NII) replaces decelerating

Profitability growth in non-interest income.

We expect mild deterioration in nonperforming assets (NPAs) and net charge-offs (NCOs), reflecting the increased

Asset Quality debt-servicing cost implied by interest rates, but for these metrics to remain near the stronger end of the past

decade’s performance.

We expect capitalization by our (S&P Global Ratings risk-adjusted capital [RAC]) measure to remain unchanged and

Capital ratings neutral for most banks.

Funding & We expect the incremental adding of bail-in-eligible senior resolution notes to not significantly alter prior issuance

Liquidity volumes, nor cost-of-funds. Liquidity is unlikely to improve much beyond its current level.

Jan. 18, 2019 3

Macroeconomic Backdrop: Decelerating But Still Relatively Strong

Growth As Rates Increase, So Long As Trade Keeps Flowing

S&P Global Ratings’ Economic Outlook – Select Economic Indicators Unemployment at its lowest in 40 years

2014 2015 2016 2017 2018F 2019F

Real GDP (%) 2.9 1.0 1.4 3.0 2.1 2.0

CPI (%) 1.9 1.1 1.4 1.6 2.3 2.1

Unemployment (%) 6.6 6.9 7.0 6.3 5.8 5.8

Short-term rate 1.2 0.8 0.8 1.4 2.1 2.5

Long-term rate 1.9 1.5 1.5 2.0 2.5 3.3

U.S.-Mexico-Canada Agreement (USMCA) will present manageable

changes for several industries such as dairy (price, market share) and

automobiles (production costs, tariffs). U.S.-China trade tensions Exports rebounding post-USMCA

continue to temper business sentiment.

We expect Canada’s economic growth to decelerate but remain

relatively strong, as net exports continue to benefit from decelerating

but still relatively strong U.S. growth, while rising borrowing costs,

already high consumer debt burdens, and tighter underwriting

standards continue to dampen housing demand.

Interest rates will continue to climb as the Bank of Canada moves its

policy rate toward its neutral range (2.5%-3.5%), from the current

1.75%. We expect the policy rate to end 2019 at 2.5%.

Sources: S&P Global Ratings, Bank of Canada. CPI--Consumer Price Index.

Jan. 18, 2019 4

USMCA: Little Impact… So Long As It’s Ratified

USMCA Partner Trade – Bil. US$

700 140

600 120

500 100

400 80

300 60

200 40

100 20

- -

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Imports (LHS) Exports (LHS) Net Exports (RHS)

Canadian exports rebounded in the latter half of 2018 and are expected to continue expanding in 2019 along with net exports.

None of the USMCA key updates are expected to present significant challenges to Canadian industries.

Auto + parts quotas should benefit Canada but will be balanced against general competitive forces, evidenced by recent GM

closures

Marginally increased access to local dairy markets for U.S farmers should boost U.S.-to-Canada exports by about $70 million, but

access is still only 3.6% of the market, with heavy tariffs on exceeding quotas

Ratification in 2019 was already least certain in the U.S.; the partial government shutdown can only delay U.S. ratification. If ratification

were to go off the rails, Canadian business sentiment (and related bank revenues, such as those tied to corporate investment spending)

would likely worsen.

Sources: S&P Global Ratings, World Bank.

Jan. 18, 2019 5Canada Still A Low-Risk Country For Banking, Despite Mild

Deterioration

BICRA Brief: Canada

BICRA group: ‘2’

ER/ER trend: 3/Stable

IR/IR trend: 2/Stable

Recent years’ incremental

deterioration led to, in 2018:

ER worsened to ‘3’ from ‘2’…

…but ER trend improved to stable

from negative.

Looking Ahead:

We expect economic and industry risk

trends to remain stable in 2019.

The 2018 worsening of the ER score reflects our concerns over high consumer indebtedness and elevated house

prices leaving the Canadian banks more vulnerable to downside risks, but we think these risks are moderating and

further deterioration is unlikely in 2019.

A BICRA (Banking Industry Country Risk Assessment) is scored on a scale from ‘1’ to ’10’, ranging from the lowest-risk banking systems (group ‘1’) to the highest-risk (group ‘10’). ER –

Economic Risk; IR – Industry Risk.

Source: S&P Global Ratings.

Jan. 18, 2019 6Key Sources Of Credit Risk: Consumers And The Housing Market

Housing Price Growth DSIBs – Median Consumer Loan Growth

200% 10%

180%

160% 8%

140%

120% 6%

100%

80% 4%

60%

40% 2%

20%

0%

0%

Oct-06

Oct-08

Oct-10

Oct-12

Oct-14

Oct-16

Oct-18

Feb-06

Feb-08

Feb-10

Feb-12

Feb-14

Feb-16

Feb-18

Jun-05

Jun-07

Jun-09

Jun-11

Jun-13

Jun-15

Jun-17

-2%

2012 2013 2014 2015 2016 2017 2018

Composite Vancouver Toronto Montreal Credit Cards HELOC Other Personal

Composite includes the 11 largest metropolitan areas.

Housing prices in the two largest and hottest markets (Toronto and Vancouver) cooled in 2018, with year-over-year price growth of about 3%-5%

in major markets, while some western markets (Edmonton, Calgary) declined. We expect residential mortgage (RM) credit and house prices to

continue to increase in 2019, reflecting continued strong underlying demand, but at a more moderate pace, tempered by higher interest rates and

tightened underwriting by the largest lenders, reflecting, among other factors, the B-20 stress test implemented in 2018.

"Other consumer" loan growth has converged in recent years to about a 3%-6% pace (median growth among the big banks).

1. Credit Card activity has been influenced by M&A activity, such as BNS completing its acquisition of BBVA Chile, and acquiring assets or

partnerships in Colombia and Peru. We don’t expect the Aeroplan-Aimia deal to affect card volumes with TD and CIBC, as we expect Air

Canada to seamlessly take over the loyalty program. We expect expansion of this kind to continue in 2019, particularly abroad.

2. HELOC growth decelerated over the past year, likely reflecting rising interest rates, both of which we expect will continue.

3. Other Personal lending is on an uptick--mainly due to automobile lending, such as TD’s U.S. expansion plans in the space, which we

expect will continue in 2019.

Sources: S&P Global Ratings, company filings, Teranet. DSIB--Domestic systemically important bank. HELOC--Home equity line of credit.

Jan. 18, 2019 7Key Drivers Of Our 2018 Revision Remain In Focus

High-profile cases of documentation deficiencies in the RM

Residential Mortgages Continue Increasing;

underwriting process, such as with Home Capital and Laurentian

Bank, have led to renewed efforts to tighten lending frameworks Arrears Improve

against fraud, including talk of officials allowing the Canada 4,400 0.40%

Revenue Agency to share income data with lenders and/or

mortgage insurers. Our move to ER3/Stable assumes a limited 4,350 0.30%

Mil.

amount of further evidence emerges regarding fraud or other RM 4,300 0.20%

underwriting deficiencies.

4,250 0.10%

Positively, RM arrears/loans have been on a downward trend for 4,200 0.00%

many years. Still, we believe rising DTI and house prices 2011 2012 2013 2014 2015 2016 2017 2018

strengthen incentives for fraud, although we expect these Sep.

incentives to moderate, near current levels, in 2019.

Mortgages (LHS) Arrears (LHS) Arrears / Total Mortgages (RHS)

An increasing share of brokered mortgages was another factor in

our move to ER3, as we believe brokers’ incentives differ from

lenders’, but we also expect moderation in the brokers’ share in

Macro Credit Metrics

2019. 180% 15%

10%

130%

Household DTI by Product

5%

80%

0%

0% 50% 100% 150% 200%

30%

Mortgage HELOC Cards Auto Installment Other -5%

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018 F

2019 F

-20% -10%

With anticipated rate hikes and tightened B-20

guidelines constraining refinancing options, we Household DTI (LHS)

Household debt/GDP (LHS)

expect mortgage arrears to tick up in 2019. Credit/GDP (LHS)

Real change in residential house price index (RHS)

Sources: S&P Global Ratings, company filings, Canadian Bankers Association, Canada Mortgage Housing Corp. DTI--Debt-to-income.

Jan. 18, 2019 8Brokered Residential Mortgages: Share Growth To Moderate

Broker Share Of Mortgage Originations

60

50

40

(%)

30

20

10

0

2012 2013 2014 2015 2016 2017

First-time Buyers Repeat Buyers Refinancers Renewers

In light of the latest Canada Mortgage and Housing Corp. (CMHC) consumer survey, we believe the brokered share

declined slightly in 2018, among first-time and repeat buyers, and refinancers, while remaining steady among

renewers.

Nearly 90% of broker market volume flows through 10 dealers.

We expect brokers’ share of the market to continue to grow in 2019, although at a more moderate pace, as house-

priceCMHC.

Sources: growth decelerates.

Jan. 18, 2019 9Canadian Bank Ratings: All Stable But Two

Business Capital & Risk Funding & Group Systemic ICR &

Anchor SACP

Position Earnings Position Liquidity Support Importance Outlook

Bank of Montreal a- Adequate Adequate Strong Avg. & Adeq. a High A+/Stable

Bank of Nova Scotia bbb+ Strong Adequate Strong Avg. & Adeq. a High A+/Stable

Canadian Imperial

a- Adequate Adequate Adequate Avg. & Adeq. a- High A+/Stable

Bank of Commerce

Above Avg. &

Central 1 Credit Union a- Weak Very Strong Moderate a- Low A-/Stable

Strong

Fédération des Caisses

a- Adequate Strong Adequate Avg. & Adeq. a Moderate A+/Stable

Desjardins du Québec

Below Avg. &

Home Capital Group Inc. a- Very Weak Strong Weak b+ Low B+*/Positive

Moderate

HSBC Bank Canada a- Moderate Adequate Adequate Avg. & Adeq. bbb+ Core Low AA-/Stable

Laurentian Bank of

a- Weak Adequate Adequate Avg. & Adeq. bbb Low BBB/Negative

Canada

Above Avg. &

Manulife Bank of Canada a- Weak Very Strong Moderate bbb+ Strategic Low A+/Stable

Adeq.

National Bank of Canada a- Adequate Adequate Adequate Avg. & Adeq. a- Moderate A/Stable

Royal Bank of Canada a- Strong Adequate Strong Avg. & Adeq. a+ High AA-/Stable

Toronto-Dominion Bank a- Strong Adequate Strong Avg. & Adeq. a+ High AA-/Stable

Movements From The Anchor:

Very Weak (-5) Weak (-2) Moderate (-1) Adequate (0) Strong (+1) Very Strong (+2)

Source: S&P Global Ratings. SACP--Stand-alone credit profile. ICR--Issuer credit rating. *Home Trust Co. (lead operating company) ICR. Home Capital Group Inc. (non-operating holding

company or NOHC) ICR is B-/Positive, because we view an NOHC as reliant on dividends and other distributions from its operating companies.

Jan. 18, 2019 10Tiptoeing Into Bail-in-eligibility Since September

Key Takeaways

Canadian Systemically 1. Bail-in-eligible ("senior subordinated" or "senior resolution") issue ratings are gradually

Important Banks Ratings And being assigned to DSIBs

Outlooks Are Unchanged 2. No change to DSIB ICRs (applicable to senior debt ineligible for bail-in) nor outlooks

Following Release Of Draft Bail- No change in our government support assessment on Canada (“Supportive”)

In Regulations, June 19, 2017

3. No resolution counterparty rating assigned to DSIBs

4. We view Canada’s resolution regime as “effective” (as defined in our ALAC criteria1)

We rate bail-in debt at one notch below the SACP, reflecting the common-

A Closer Look At How

equity conversion clause--that we consider to be effective subordination

Proposed Bail-in Regulations

May Affect Canadian Bank

Ratings, July 14, 2017 BMO BNS CM NA RY TD

Anchor a- bbb+ a- a- a- a-

SACP a a a- a- a+ a+

Canadian Systemically Systemic Importance +1 +1 +2 +1 +1 +1

Important Banks Ratings And

ICR A+ A+ A+ A AA- AA-

Outlooks Are Unchanged On

Release Of Final Bail-In Bail-In Debt2 A- A- BBB+ BBB+ A A

Regulations, April 20, 2018

We expect the remaining Canadian D-SIFI, the Desjardins Group, to become subject to a

separate bail-in regime, possibly as early as April 2019, based on the public consultation

Review Of Canadian Bank administered by Desjardin’s regulator (Quebec’s Autorité des marchés financiers or

Resolution Regime Completed; AMF). We plan to comment further on any implications for our ratings on Desjardins,

Ratings And Outlooks On once the AMF’s final regulations are published.

Systemically Important Banks

Unchanged, Aug. 16, 2018 1Bank Rating Methodology And Assumptions: Additional Loss-Absorbing Capacity; April 27, 2015.

2Only RBC, TD, and CIBC have issued bail-in debt, to date.

Sources: S&P Global Ratings. ALAC--Additional loss-absorbing capital. DSIB--Domestic systemically important bank.

Jan. 18, 2019 11Balance Sheet: Corporate Lending To Continue To Drive Growth

Loan Growth By Type - All Rated Average Loan Mix – All Rated Canadian Banks

Canadian Banks 100%

90%

50%

80%

40% 70%

60%

30% 50%

40%

20%

30%

10% 20%

10%

0% 0%

2012 2013 2014 2015 2016 2017 2018 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Residential Real Estate Commercial & Corporate Residential Real Estate Commercial & Corporate

Commercial Real Estate Other Consumer Commercial Real Estate Other Consumer

Post-2011 (generally accepted accounting principles to International Financial Reporting Standards [IFRS]) balance-sheet growth has been

relatively stable, averaging about 6% per year over the past few years.

Commercial/corporate lending has driven loan growth in recent years and is becoming a larger part of the loan mix for many banks, a trend

we expect will continue, in light of our macroeconomic assumptions.

We expect DSIBs to increase foreign assets more aggressively, augmented by mergers and acquisitions (M&A) activity, particularly in the

U.S. where many DSIBs have subsidiaries.

We expect aggregate DSIB loans to grow at about 5%-6% into 2019, with deposits growing at a similar rate.

Source: S&P Global Ratings, company filings.

Jan. 18, 2019 12M&A: Investments In Wealth & Technology To Continue

Two key spheres dominated M&A activity in 2018: wealth and technology.

Banks are continuing to make bolt-on acquisitions of small-to-midsize asset management firms, with BNS leading the way in 2018 with

several high-profile multi-billion-dollar acquisitions.

Notably, DSIBs are also gobbling up niche tech startups, such as the acquisition of artificial intelligence startup Layer 6 by TD, and tech-

savvy specialty finance firm Wellington Financial by CIBC--part of a broader move by banks to effectively analyze the mass amounts of

customer data on hand, both for better cross-sell and to find and better realize cost efficiencies.

RBC has been investing in AI research as well, having opened labs in Toronto and Edmonton.

We expect more of the same M&A in 2019 as wealth revenues show no sign of slowing down, and competitive pressures re: technology

continue, in Canada and abroad.

Buys… For… Industry

Bank of Montreal KGS-Alpha Undisclosed Capital Markets

Bank of Nova Scotia Jarislowsky-Fraser $1 Billion Wealth Management

Bank of Nova Scotia MD Financial $2.5 Billion Wealth Management

Bank of Nova Scotia Misc. LatAm/Caribbean Undisclosed P&C, Cards

Canadian Imperial Bank of Commerce Wellington Financial Undisclosed Advisory, Venture Capital

Toronto-Dominion Bank Greystone Investments $800 Million Wealth Management

Toronto-Dominion Bank Layer 6 Undisclosed Artificial Intelligence

Source: S&P Global Ratings, company filings. P&C--Personal & commercial.

Jan. 18, 2019 13NIMs Are Rising And Will Continue To Do So

The Bank of Canada increased the policy (overnight) rate three

A Tale of Two Rates times in 2018, from 1.00% to 1.75% as part of its efforts to

2.65% normalize monetary policy amid tight labor markets, rising exports,

1.50% and relatively strong macroeconomic data. We expect the bank’s

2.60% policy rate to end 2019 at 2.5%.

1.00%

2.55%

The rate hikes are helping domestic NIMs upward as DSIBs have

2.50% 0.50% succeeded in raising lending rates more quickly than their funding

costs are increasing, sustaining profitability despite decelerating

2.45% 0.00% growth in non-interest income. The latter was largely a result of

Q1 17 Q2 17 Q3 17 Q4 17 Q1 18 Q2 18 Q3 18 Q4 18 market volatility causing declines in underwriting, trading, and

DSIB Domestic NIM (LHS) BoC Overnight Rate (RHS) other market-sensitive income; we are assuming negative impact

from market volatility continues in 2019.

DSIBs+ Profitability (Mostly) Steady In 2019

5% 18%

4% 16%

14%

3%

12%

2% 10%

1% 8%

We expect NIMs to slightly increase in 2019, on

average across the big banks. 6%

0%

4%

-1% 2%

-2% 0%

2015 2016 2017 2018 2019F

Average Operating Leverage (LHS) Return On Equity (RHS)

Growth in Operating Revenues (RHS) Growth In Noninterest Expenses (RHS)

Growth In Net Interest Income (RHS) Growth in Noninterest Income (RHS)

Source: S&P Global Ratings. DSIBs+ is DSIBs plus Laurentian Bank.

Jan. 18, 2019 14Revenues: Wealth Management & Foreign Operations Increasingly Important

Since 2012, wealth management (WM) revenues have increased in Revenue Contribution By Business Line

revenue contribution to 21.7% from 18.1%. 100%

80%

We expect these revenues to gain further traction while capital markets

revenues decline in relative importance. 60%

40%

Foreign revenues are also becoming more important, helped by

acquisitions that are being progressively integrated--such as those by 20%

CIBC in the U.S., and BNS in Latin America and the Caribbean.

0%

-20%

BMO BNS CM NA RY TD

P&C S&T Wealth Insurance Other

DSIB Revenue by Activity DSIB Revenue Trends By Geography

25% 70% 40%

24%

23% 68% 38%

22%

21% 66% 36%

20%

19% 64% 34%

18%

17% 62% 32%

16%

15% 60% 30%

2012 2013 2014 2015 2016 2017 2018 2014 2015 2016 2017 2018

WM / Total Revenues (%) S&T / Total Revenues (%) Canada (LHS) International (RHS)

Sources: S&P Global Ratings and company filings. S&T--Sales & trading.

Jan. 18, 2019 15Digitization To Continue To Lower Input Costs, Offsetting Increased

Cyber-Risk Spending

$14 Billion spent on cybersecurity in 2017 by Canadian businesses

36% Business leaders planning to refresh their security architecture for digital transformation

52% Executives in Canada’s financial sector who believe that cyber-risk will be the most

disruptive trend in the next 24 months

We expect further penetration in digital sales, adoption, and self-

service among all Canadian banks, particularly in mobile banking and DSIBs - Technology Spend

among smaller Canadian banks that lack the pre-existing 15% 60%

infrastructure and scale for branch banking.

13% 58%

Increased digitization brings its own risks: the big five banks are

11% 56%

among the top 100 most-phished brands in North America (according

to VadeSecure). 9% 54%

Cybersecurity spending thus far has been modest, despite, in 2018, 7% 52%

several high-profile security breaches in large Canadian banks, such

as BMO, CIBC, and RBC. 5% 50%

2013 2014 2015 2016 2017 2018

We expect technology spend to continue increasing as companies CES / NIE (LHS) NIE / Operating Revenues (RHS)

invest more into their systems and modernize their digital

architecture.

Sources: S&P Global Ratings, VadeSecure, Statistics Canada, PWC. CES--Computer, equipment, software. NIE--Noninterest expense.

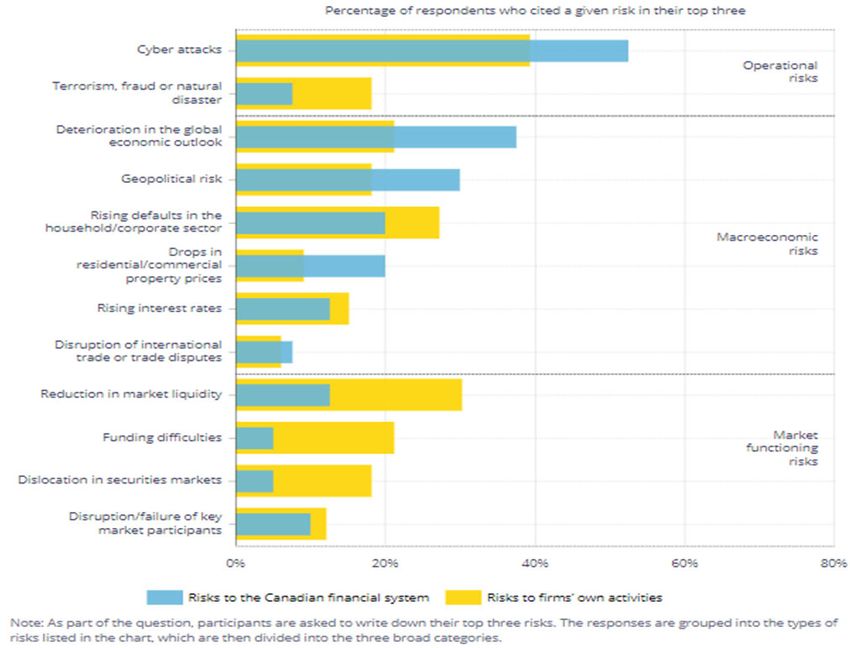

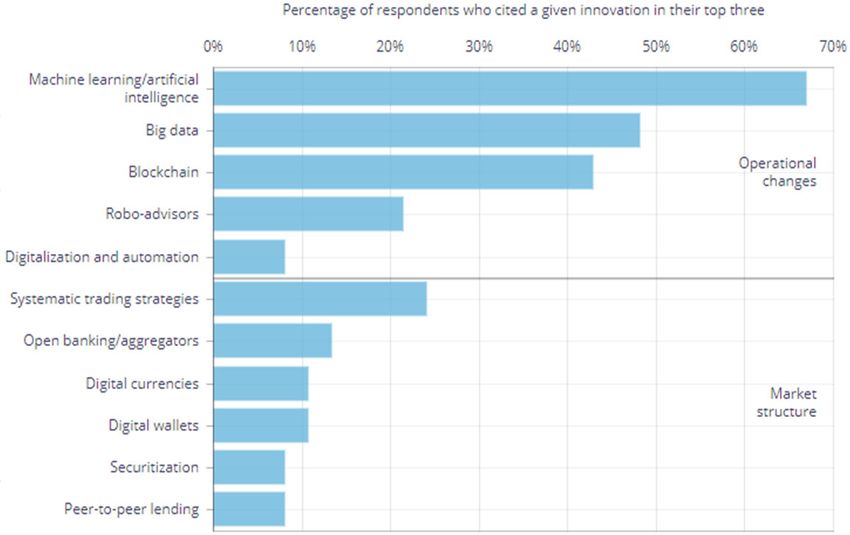

Jan. 18, 2019 16Digitization & Cyber-Risk To Remain Top-Of-Mind

From the Bank of Canada’s Financial System Survey, it appears respondents believe:

• Machine learning and artificial intelligence will have the largest impact, of the types of innovation cited, on the operations

of the Canadian financial services industry in the next three years.

• From a market structure perspective, two key innovations--systematic trading strategies and open banking, which allows

clients to share their banking data with other financial institutions--will have the largest impact.

• From a risk perspective, cyber attacks were cited as the biggest threat to the financial system.

Jan. 18, 2019 17Capitalization To Remain Ratings Neutral For Most

DSIBs - Average Capital Position RAC Ratio Distribution, All Rated Canadian

10.0% 5.0%

Banks

9.5% 70%

4.5%

9.0% 60%

8.5% 4.0%

50%

8.0%

3.5%

7.5% 40%

7.0% 3.0% 30%

20%

10%

July 2017 RAC Criteria ER 3

0%

S&P RAC (LHS) S&P Leverage (RHS) Adequate (7% - 10%) Strong (10% - 15%) Very Strong (>15%)

The majority of rated Canadian banks are expected to maintain an adequate RAC ratio during 2019, which is ratings neutral.

The worsening of the economic risk score to '3' from '2' in 2018, combined with the new assumption that a small (5%) proportion of uninsured RMs are non-

prime, had a 40 bps-50 bps negative impact on DSIBs RAC ratios, bringing the average down to 8.2% in second-quarter 2018. The effect was more

pronounced on the smaller Canadian banks (100 bps on average), reflecting both a higher concentration in Canadian exposures and our assumption that the

proportion of non-prime among uninsured RMs is slightly higher (10%), but the majority of these started from a stronger capital position than the DSIBs. No

rating actions directly resulted from these changes.

We expect the DSIB RAC ratios to moderately increase in 2019, in concert with leverage ratios and regulatory capital, as these banks build resources for

future acquisitions. The impending phase-out of old Tier 1 innovative instruments is not expected to affect our RAC assessments.

A surprise 25 bps increase in the domestic stability buffer of DSIB capital ratios in December is manageable, with the average Common Equity Tier 1 for

DSIBs at 11.5%, far above the 9.75% prescribed minimum. We don’t anticipate any impact on DSIBs' S&P Global Ratings RAC figures.

Source: S&P Global Ratings. 2018 RAC average is forecast.

Jan. 18, 2019 18Oil & Gas Exposures Remain Less Important Than You Might Think

Crude oil (West Texas Intermediate) prices dropped over 60% in the last four months of 2018, ending at a two-and-a-half year low of $45.4.

Despite price volatility, risks to banks remain low, as the DSIBs' oil and gas exposure is less than 2% of total loans, and less than 5% of business and government

loans, on average.

Asset quality in the sector remains strong as well, with oil and gas NPAs making up less than 2% of oil and gas loans for most banks.

Western Canadian Select exposure remains low, at about 10% of total oil and gas exposure, with the majority of the exposure being investment-grade.

Provisions for credit losses (PCLs) in the sector have not been affected by IFRS 9, with most banks posting reduced PCLs year-over-year in energy.

We expect PCLs overall to increase about 12% in 2019, in-line with the previous year. We could see a spike in PCLs akin to the energy price decline of 2014-2015,

but, similar to then, modest exposures limit the significance of asset quality concerns.

Oil & Gas - Assets & Asset Quality Oil & Gas Exposure Breakdown

3.0% 100%

2.5% 80%

2.0% 60%

1.5%

40%

1.0%

20%

0.5%

0%

0.0% BMO BNS CM NA RY TD

BMO BNS CM NA RY TD

Exploration & Production Drilling & Services

Net O&G Loans / Total Loans Net O&G NPAs / O&G Loans (%) Midstream & Downstream (RMD) Other

Source: S&P Global Ratings. RMD--Refining, marketing, distribution.

Jan. 18, 2019 19Underwriting: Trend Toward Lower Insurance (But Lower Loans-to-Value) To

Continue But Decelerate

Insured Mortgages / Total Mortgages (%) DSIBs - Average Uninsured LTV (%)

75% 60%

70%

65% 58%

60%

56%

55%

50%

54%

45%

40%

52%

35%

2013 2014 2015 2016 2017 2018

50%

BMO BNS CM NA RY TD 2013 2014 2015 2016 2017 2018

The proportion of insured mortgages has declined as portfolio insurance falls away.

Uninsured loan-to-value ratios (LTVs) on the Canadian book were on a slight uptick in 2018 after years of decline, a trend we expect will

continue into 2019. Uninsured LTVs on new originations averaged around 67% at fourth-quarter 2018.

On average, uninsured mortgages with high (>75%) LTVs and low (< 650) FICO/Beacon scores have made up less than 1% of uninsured

mortgages among DSIBs.

Insured mortgage volumes have historically been low for the smaller banks, and we expect these lenders to issue more uninsured mortgages

as well.

We believe the majority of uninsured mortgages outstanding lent by DSIBs have a FICO/Beacon score above (better than) 700.

Source: Company filings.

Jan. 18, 2019 20Asset Quality: Non-Mortgage Consumer Lending To Weaken, Slightly, But

Overall Strength To Remain

Credit Metrics: All Rated Canadian NPAs: All Rated Canadian Banks (% Loans)

Banks 4.0%

1.4% 3.5%

1.2% 3.0%

1.0% 2.5%

0.8%

2.0%

0.6%

0.4% 1.5%

0.2% 1.0%

0.0% 0.5%

0.0%

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

NCOs (% loans) NPAs (% loans) Residential RE C&C CRE Other Consumer

NPA – Nonperforming Assets.

Asset quality has largely remained resilient in the face of growing

consumer debt and housing prices, with NPAs and NCOs holding NCOs: All Rated Canadian Banks (% Loans)

steady, or improving, across most segments. 1.0%

0.9%

0.8%

Other consumer debt remains the area with the highest loss rates,

0.7%

but has been declining since 2017 due to higher recoveries in

0.6%

various products such as cards and auto. 0.5%

0.4%

We expect aggregate asset quality to deteriorate slightly in 2019, 0.3%

reflecting the increased debt-servicing cost implied by interest 0.2%

0.1%

rates, but remain near the stronger end of the past decade’s

0.0%

performance. 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Residential RE C&C CRE Other Consumer

Sources: S&P Global Ratings, company filings. C&C--Corporate and commercial. CRE--Commercial real estate.

Jan. 18, 2019 21Funding: Incremental Adding Of Bail-In Debt To Continue

Canadian Banks – Funding Metrics Subordinated

Debt Bank Deposits

150% 105% 4% 5%

100% Other

140% 95% Securitization

90% 16% Other BDNs, CD, CP

130% 32%

85% 2%

80% Covered

120%

75% Bonds 2014

110% 70% 10%

65%

100% 60% Senior Notes

ABCP

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 29%

2%

Loans / Deposits (LHS) S&P Stable Funding Ratio (RHS)

DSIBs Wholesale Funding Mix

DSIBs - Covered Bonds / Wholesale Funding Subordinated Bank

Debt Deposits

Other 3% 2%

15%

Securitization

13% 12% Other

4% BDNs, CD,

11% CP

9% Covered 32%

Bonds

7% 14%

2018

5% Senior

2014 2015 2016 2017 2018 Notes ABCP

31% 2%

Most rated banks enjoy an S&P-calculated stable funding ratio of 100% or more.

Covered bond issuances have increased 40% on average from five years ago.

We expect DSIBs to increasingly issue senior resolution notes (following the lead of TD and RBC) without significant disruption to prior

issuance volumes, nor cost-of-funds.

Sources: S&P Global Ratings, company filings. CDs--Certificates of deposit. CP--Commercial paper. ABCP--

Asset-backed commercial paper. NSFR--Net stable funding ratio.

Jan. 18, 2019 22Liquidity Unlikely To Improve Much More

DSIBs - Liquidity Metrics Cash

NHA MBS 11%

1.20x 140% 14% Bank Deposits

1.15x 135% Other 3%

2%

1.10x 130%

1.05x 125% Corporate

Equity 2013 Government

1.00x 120% 21% Debt

MBS, ABS, 33%

0.95x 115%

CMO

0.90x 110% 2%

Corporate Debt

0.85x 105%

14%

0.80x 100%

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Liquidity Coverage Ratio (RHS) BLA / ST (LHS)

DSIBs Liquid Asset Mix

All DSIBs have a liquidity coverage ratio of well over 100%, as well as a

BLA/ST ratio comfortably over 1.0x, despite a slight downward trend in

2018. Barring further regulatory incentive, we do not expect the banks (as Cash

a group) to significantly improve their liquidity, as rising interest rates NHA MBS 10%

10%

raise the opportunity cost to holding it. Bank Deposits

Other 4%

Corporate 2%

Banks are well-positioned to handle liquidity stresses. In particular, Home Equity

Capital has made significant progress in pulling back from the liquidity 15%

run of 2017. 2018

Government securities have become a higher portion of unencumbered MBS, ABS, Government

Corporate Debt CMO

liquid asset holdings, a trend we view as positive given the majority of Debt

13% 2%

holdings in the sub-category are Canadian, U.S., and other highly rated 44%

governments.

Sources: S&P Global Ratings, company filings. BLA/ST--Broad liquid assets to short-term wholesale funding.

Jan. 18, 2019 23Related Research

Americas Economic Snapshots, Dec. 21, 2018

Global Banks 2019 Outlook: Bracing For More Volatility, Dec. 3, 2018

Review Of Canadian Bank Resolution Regime Completed; Ratings And Outlooks On Systemically Important Banks

Unchanged, Aug. 16, 2018

Laurentian Bank of Canada Ratings Affirmed; Off CreditWatch; Outlook Negative On Concentrated Mortgage

Exposure, April 27, 2018

Canada Economic Risk Higher On Elevated House Prices And Household Debt And Mortgage Fraud; No Ratings

Affected, Feb. 23, 2018

Canadian Banks Midyear 2018 Outlook: Bail-In, Mortgage Tightening, Tax Reform, And IFRS Affecting The Canadian

Banks, Aug. 17, 2018

How IFRS 9's Expected Credit Loss Framework Will Affect Canadian Banks' Loss Provisioning In 2018 And Beyond,

Dec. 18, 2017

Jan. 18, 2019 24Analytical Contacts

Nikola Swann Lidia Parfeniuk

Toronto Toronto

+1 416 507 2582 +1 416 507 2517

nikola.swann@spglobal.com lidia.parfeniuk@spglobal.com

Amit Tiwari Shameer Bandeally

Toronto Toronto

+1 416 507 3224 +1 416 507 3230

amit.tiwari@spglobal.com shameer.bandeally@spglobal.com

Robert Palombi Devi Aurora

Toronto New York

+1 416 507 2529 +1 212 438 3055

robert.palombi@spglobal.com devi.aurora@spglobal.com

Jan. 18, 2019 25Copyright © 2019 by Standard & Poor’s Financial Services LLC. All rights reserved.

No content (including ratings, credit-related analyses and data, valuations, model, software or other application or output therefrom) or any part thereof

(Content) may be modified, reverse engineered, reproduced or distributed in any form by any means, or stored in a database or retrieval system,

without the prior written permission of Standard & Poor’s Financial Services LLC or its affiliates (collectively, S&P). The Content shall not be used for

any unlawful or unauthorized purposes. S&P and any third-party providers, as well as their directors, officers, shareholders, employees or agents

(collectively S&P Parties) do not guarantee the accuracy, completeness, timeliness or availability of the Content. S&P Parties are not responsible for

any errors or omissions (negligent or otherwise), regardless of the cause, for the results obtained from the use of the Content, or for the security or

maintenance of any data input by the user. The Content is provided on an “as is” basis. S&P PARTIES DISCLAIM ANY AND ALL EXPRESS OR

IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR

PURPOSE OR USE, FREEDOM FROM BUGS, SOFTWARE ERRORS OR DEFECTS, THAT THE CONTENT’S FUNCTIONING WILL BE

UNINTERRUPTED OR THAT THE CONTENT WILL OPERATE WITH ANY SOFTWARE OR HARDWARE CONFIGURATION. In no event shall S&P

Parties be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs,

expenses, legal fees, or losses (including, without limitation, lost income or lost profits and opportunity costs or losses caused by negligence) in

connection with any use of the Content even if advised of the possibility of such damages.

Credit-related and other analyses, including ratings, and statements in the Content are statements of opinion as of the date they are expressed and not

statements of fact. S&P’s opinions, analyses and rating acknowledgment decisions (described below) are not recommendations to purchase, hold, or

sell any securities or to make any investment decisions, and do not address the suitability of any security. S&P assumes no obligation to update the

Content following publication in any form or format. The Content should not be relied on and is not a substitute for the skill, judgment and experience of

the user, its management, employees, advisors and/or clients when making investment and other business decisions. S&P does not act as a fiduciary

or an investment advisor except where registered as such. While S&P has obtained information from sources it believes to be reliable, S&P does not

perform an audit and undertakes no duty of due diligence or independent verification of any information it receives.

To the extent that regulatory authorities allow a rating agency to acknowledge in one jurisdiction a rating issued in another jurisdiction for certain

regulatory purposes, S&P reserves the right to assign, withdraw or suspend such acknowledgement at any time and in its sole discretion. S&P Parties

disclaim any duty whatsoever arising out of the assignment, withdrawal or suspension of an acknowledgment as well as any liability for any damage

alleged to have been suffered on account thereof. S&P keeps certain activities of its business units separate from each other in order to preserve the

independence and objectivity of their respective activities. As a result, certain business units of S&P may have information that is not available to other

S&P business units. S&P has established policies and procedures to maintain the confidentiality of certain non-public information received in

connection with each analytical process.

S&P may receive compensation for its ratings and certain analyses, normally from issuers or underwriters of securities or from obligors. S&P reserves

the right to disseminate its opinions and analyses. S&P's public ratings and analyses are made available on its Web sites, www.standardandpoors.com

(free of charge), and www.ratingsdirect.com and www.globalcreditportal.com (subscription), and may be distributed through other means, including via

S&P publications and third-party redistributors. Additional information about our ratings fees is available at www.standardandpoors.com/usratingsfees.

Australia: Standard & Poor's (Australia) Pty. Ltd. holds Australian financial services license number 337565 under the Corporations Act 2001. Standard

& Poor’s credit ratings and related research are not intended for and must not be distributed to any person in Australia other than a wholesale client (as

defined in Chapter 7 of the Corporations Act). STANDARD & POOR’S, S&P and RATINGSDIRECT are registered trademarks of Standard & Poor’s

Financial Services LLC

Jan. 18, 2019 26You can also read