CASE STUDY COMPENDIUM - WUR E-depot

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

JUNE 2020

CASE STUDY COMPENDIUM

This case study compendium was developed as part of the research for ISF Briefing Note 17 on the

Role of Government in Rural and Agri-Finance: Transitioning to private sector involvement.

Please refer to the full briefing note for a full overview of the topic.

AGRICULTURAL FINANCE

HISTORICAL CASE STUDY: MEXICO

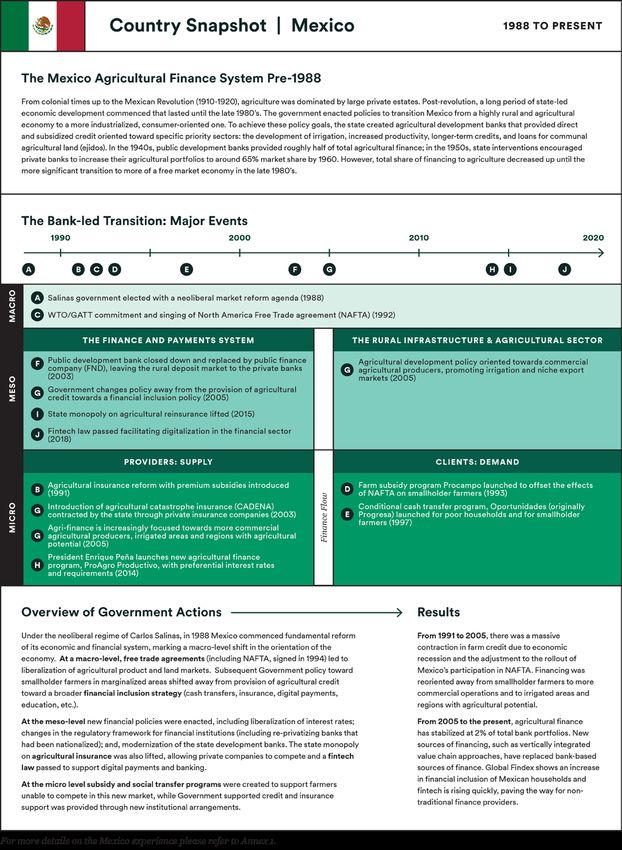

Summary of Mexico’s agricultural With Mexico’s enactment of the North American

development Free Trade Agreement in 1994, the country

opened its agricultural markets to the import

With a population of almost 130 million, Mexico of subsidized food staples from the USA and

is the second largest economy in Latin America Canada, transforming local food markets that

and the 11th largest economy in the world. In were previously protected. Under the Salinas

1950, agriculture accounted for almost 20% of government (1988-1994), policies became more

Mexico’s GDP—but in 2018 it represented only market- and business-oriented, and the govern-

3.4% of GDP. Though agriculture currently ment increasingly treated smallholder agriculture

represents 13% of total employment, that share as a domain for social policy, rather than an area

has shrunk from 33% since the market reforms for productive development.

of the 1990s. Today there are an estimated 6.8

million farmers in Mexico, primarily on farms

of less than five hectares. A brief view of the government-led

era (1930s-1980s)

From colonial times up to the Mexican Revolu-

tion (1910-1920), agriculture was dominated by After the Mexican revolution (1910-1920), a

large private estates. Post-revolution agrarian long period of state-led economic development

reforms redistributed half of existing agricultural started, lasting until the end of the 1980s. In this

land to rural workers and smallholder farmers, period, Mexico transitioned from a highly rural

under the ejido (communal land) system. These and agricultural economy to a more industrialized

ejidos persisted in their original form until 1990, and consumer-oriented economy. The dominant

when new laws liberalized the land market and government party (PRI) consistently followed an

allowed parcels within the ejido to be sold, rented inward-looking development strategy, focused

to outsiders, or pledged as collateral for a loan.

1

on nationalizing oil and railways sectors, imple- neoliberal regime under Carlos Salinas paved the

menting an industrialization programme, and way for fundamental reform of the economic and

creating an active development bank system. In financial system. As Mexico committed to free

agriculture, the state stimulated domestic food trade agreements, agricultural products and land

production and the smallholder economy, while markets were liberalised. The financial sector was

at the same time securing affordable food for the gradually opened to foreign shareholdership, and

urban poor. Government complemented these its regulations converged toward international

strategies with policies focused on land reform, standards. New financial policies included liberal-

price support for food staples and oilseeds, heavy ization of interest rates, changes in the regulatory

investments in irrigation and green revolution, framework for financial institutions and the

and a stimulus to diversify production. capital market (including re-privatizing banks

that had been nationalized), and modernization

Agricultural finance helped the government of the development banks.

achieve its policy goals. The state created agricul-

tural development banks to provide direct and

subsidized credit to agriculture and oriented this Structural adjustments in the

credit to specific priority sectors: the development agricultural finance sector

of irrigation, increase of productivity, longer-term (1988-present)

credits, and loans for the ejidos. During the

1940s, public development banks provided Macro level: The agricultural sector was

roughly half of the total agricultural credit. In the fundamentally repositioned around the reforms

1950s, public interventions encouraged private of the Salinas government. Free trade agree-

banks to increase their agricultural portfolios ments led to major food imports at much lower

(i.e., through the state’s rediscounting facilities prices, creating a need for social transfers to

and guarantees), growing private market share to buffer smallholder farmers from their inability

around 65% by 1960. However, the total share of to compete in the market. In 1993, the Mexican

financing allocated to agriculture still decreased government launched a farm subsidy program

as the sector became a smaller part of the overall (Procampo). By 2005, Procampo was reaching at

economy. least 1.6 million low-income producers with less

than five hectares; yet it failed to reach many of

the poorest farmers. In a later revision (2006),

What changed in the 1980s? the program included a farm capitalization option

that offered an alternative to interest-bearing

Expansionist economic and fiscal policies in the credit. The capitalization option allowed

1970s led to increasing public and international smallholders to receive five years of payments

debt, which in turn became unsustainable during in advance, based on a government-approved

the global economic recession in the early 1980s. proposal for a productive project. Procampo was

The broad economic crisis (public deficit, capital renamed to ProAgro Productivo in 2014.

flight, devaluation pressure) primed Mexico for

a new political and economic model. In 1982, the Meso level: Policies, regulations, and in-

government nationalized private banks to prevent a stitutions were reformed to mirror the macro

collapse of the banking system. The resulting 1988 liberalization agenda. Government support of

2

agricultural finance became increasingly focused platforms. How this digitalization will influence

on more commercial agricultural producers, agricultural finance is still to be seen.

irrigated areas, and regions with internationally

competitive agricultural potential. The primary Micro level: At the same time that the gov-

agricultural development bank (BanRural) was ernment was implementing broad, structural

replaced by a more narrowly defined public readjustment around more open agricultural

finance company (FND since 2003). FND has markets, a structural readjustment was applied

gradually shifted its portfolio from direct agri- to the different financial institutions. Financial

cultural lending to a second-tier role, financing service provision was primarily left to the private

non-bank financial institutions (NBFIs) that sector (banks and NBFIs); public development

operate in proximity to smallholder farmers. banks (FIRA, FND) were repositioned to fa-

Although about half of FND’s current portfolio is cilitate private financing; and NBFIs (in credit

NBFIs, only 8% of its financing goes to the most and insurance) were facilitated with renewed

marginalized municipalities. regulatory frameworks. The FIRA trust remains

the largest public capital fund in Mexican agri-

Since 2005, government policy toward small- cultural finance, with assets under management

holder farmers in marginalized areas has shifted that are larger than the combined agricultural

away from provision of agricultural credit and finance portfolio of all private banks together

toward a financial inclusion policy. This policy (though there is some overlap). Since the liberal

combines cash transfers; insurance against risks market reforms of the 1980s and 1990s, FIRA has

and catastrophe; inclusion in digital payments concentrated its portfolio on private banks (80%)

systems; a broader rural finance concept, includ- and regulated NBFIs (17%), with only a limited

ing non-farm activities and microfinance; and percentage going to public development banks

the roll-out of financial education and consumer (3%). This is a significant change from the policy,

protection. In 2016, 25 million poor households prior to the late 1980s, of equal public and private

and 1.5 million smallholder farmers received cash access to facilities.

transfers through the Prospera program (formerly

Oportunidades, and prior to that Progresa). Pros- In 1991, AgroAseMex shifted its portfolio from

pera was launched in 1997 and targeted women providing direct insurance to farmers toward

and school-age children, some of whom are part reinsuring the commercial farmers’ mutualist

of smallholder households. insurance funds and the private insurance

companies. The government started a large-scale

In 2015, the state monopoly on agricultural rein- premium subsidy program for individual agricul-

surance was lifted, which allowed a few private tural insurance (SPSA, 1991). This was comple-

companies to enter the market. More recently, mented with a collective agricultural catastrophe

the government is investing in digitalization in insurance (CADENA, 2003), contracted by the

the financial sector. Leveraging increased con- state with private insurance companies.

nectivity and mobile phone penetration, gov-

ernment-to-person transfers are moving toward In 2014, President Enrique Peña Nieto launched

digital payments. A fintech law passed (2018) a new agricultural finance program aimed at

and branchless non banks are coming up, putting providing more credit to the Mexican country-

pressure on traditional banks to modernize their side—with preferential interest rates, longer

3credit periods, and fewer credit requirements. innovative agricultural insurance programs.

The new program provided a special product for For example, the coverage of catastrophe insur-

small farmers at preferential interest rates of 7% ance is vast: In 2013, insurance covered ~12M out

annual (6.5% for women farmers). Under this of the 22M hectares at national level, including

scheme, farmers no longer needed collateral for in the poorer regions of Southern Mexico. The

credits; the government provided the necessary Global Findex also shows an increase in financial

guarantees for loans granted by the private inclusion, measured by households having some

banking system, with loans linked directly to type of account with a financial institution or else-

production. where. Fintech is rising quickly in Mexico, challeng-

ing traditional banks to modernize and digitalize

their offer to customers, which may pave the way for

What happened in the agricultural more non-traditional finance providers to provide

finance market? services to smallholder farmers over time.

In the period since the market-oriented reforms,

there were two distinct phases. From 1991 to

2005, there was a massive contraction in farm

credit, in terms of hectares financed (-/- 73%), THE BANK-LED ERA TRANSITION

farmers with access to formal finance (-/- 75%),

and agricultural credit’s share in total bank

portfolios (down from 8% to 2%). This was due

In relative terms, the level of finance provided

to the economic recession and subsequent bank

by private banks in the 1960s (~65% of the

crisis, the opening of local markets to international

agricultural finance market and 17% of bank

competition, and the dismantling of subsidies

lending portfolios) was substantially larger than

to the development banks. This contraction also

it is today (where agricultural finance is less

included a reorientation of credit from smaller

than 2% of private banks’ portfolios). While

producers to more commercial farmers, and

these relative figures have decreased, the

to irrigated areas and regions with agricultural

dramatic shift in the structural orientation of

potential.

the finance sector toward private banks in the

1990s, opening trade and land reforms, marked

From 2005 to the present, the share of agricultural

a clear transition from “government-led”

finance in bank portfolios stabilized at approx-

finance to more free-market models. In this

imately 2% of total credit. While bank-based

way, we mark the bank-led transition not by

sources of finance have decreased, there have

participation rates but by the positioning of

been new models of finance: for example, lead

banks within the broader economy.

firms and processors within their value chains

stepping in to provide forward contracts to enable

financing through local banks and financial

institutions. At the same time, the government

has rolled out a more explicit financial inclusion

policy—encompassing small farmers and rural

households—and the development of more

4

45

AGRICULTURAL FINANCE

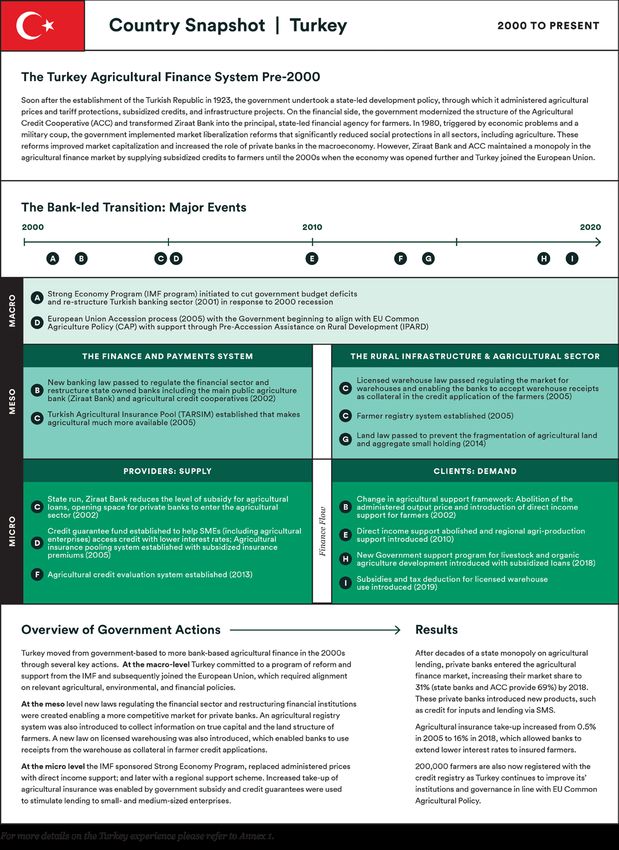

HISTORICAL CASE STUDY: TURKEY

Summary of Turkey’s agricultural structure projects. Agricultural lands were sepa-

development rated into smaller pieces through an inheritance

law passed in 1926; yet, with the support of the

With a population of 82 million and GDP of USD government, smallholdings were able to survive

770 billion, Turkey is the 19th largest economy in and improve production. However, the policies

the world. Agriculture’s share of GDP has contin- drastically changed toward a market-based

uously decreased in Turkey (from 55% in 1960 to economy in the 1980s. In that period, the govern-

5.8% in 2018), although agricultural production ment reduced subsidies and market controls in

has been rising. The contribution of agriculture all sectors, including agriculture. After financial

to the economy in 2018 was USD 45 billion, crises in 1999 and 2001, this transition from

while the annual export of agricultural products state-led development to market-oriented policies

increased from USD 4 billion in 2002 to more began to influence changes in the agricultural

than USD 22 billion in 2018. Over the same time finance market.

period, employment in the agricultural sector in

Turkey dropped from 37% to 19%.

A brief view of the government-led

Turkish agriculture is characterized by fragment- era (1930s-2000)

ed smallholder parcels, with ownership generally

divided due to inheritance. As of 2014, there were With the end of the Ottoman era and the es-

three million registered agricultural holdings in tablishment of the Turkish Republic in 1923,

the country. The average farm size has remained Turkey’s agricultural and financial policies signifi-

steady at around seven hectares over the past cantly evolved, following a state-led development

60 years. Despite the recent emergence of more policy. The country passed legislation transferring

commercial farms, 52% of farming enterprises are land ownership from the state to existing farmers

small-sized holdings or family farms less than five and removing high agricultural production taxes

hectares, fragmented to 5.9 parcels on average. in 1926. Next, it reorganized agricultural insti-

tutions to support rural development. Between

Soon after the establishment of the Turkish 1925 and 1937, the government established the

Republic in 1923, the government implemented Agricultural Combines and Agricultural Affairs

policies to support agricultural production of State; modernized the structure of Agricultural

through administered agricultural prices and Credit Cooperative (ACC); and transformed Ziraat

tariff protections, subsidized credits, and infra- Bank—which had been established in 1883 as a

6farmers’ cooperative—into a state organization farmers until the second wave of macroeconomic

and the principal financial agency for farmers. and agricultural reforms in the 2000s.

From the 1930s until the 2000s, the government

supported farmers by purchasing an expanding

list of crops at administered prices and providing What changed in the 2000s?

subsidized credits for inputs and machinery.

Macro level: Two macro factors started to

In this period, Ziraat Bank and ACC were the sole move Turkey from government-based to more

financial service providers to Turkish farmers. bank-based agricultural finance in the 2000s.

Ziraat Bank provided government payments and First, an IMF-supported economic program in

subsidies, and supported ACC to allocate credit to 2001 transformed the banking sector in Turkey.

farmers. As of 2000, Ziraat Bank was extending The country experienced the most profound

58% and ACC was extending 42% of agricul- economic crisis in its history in 2001; after which,

tural loans to Turkish farmers. As they employ with support from the IMF, the government

below-market interest rates, both institutions implemented its Strong Economy Program, which

experienced operational losses that would even- cut budget deficits and restructured the Turkish

tually contribute to financial crises and resulting banking sector. Second, Turkey’s accession to the

market reforms in the 2000s. European Union started in 2005. The government

began to align agricultural policies with those of

The oil crises in 1973 and 1979 put significant the EU. For example, agro-environmental issues

pressure on the Turkish economy. The inflation attained more prominence, as EU law and regula-

rate increased from 8% in 1970 to 64% in 1979, tions emphasize the integration of environmental

and the economy contracted by 0.5% in 1979 and concerns and good practices in land management

2.8% in 1980. At the same time, international in- and rural development. It also facilitated Turkey’s

terest rates were high, limiting Turkey’s access to gradual alignment with the EU’s Common Agri-

global credit markets. These economic problems, cultural Policy (CAP) that involved direct income

combined with political turmoil that ended with a support to farmers, rural development support

military coup in 1980, triggered market liberaliza- through the EU’s Instrument for Pre-Accession

tion reforms that involved a substantial reduction Assistance on Rural Development (IPARD),

in support and protection in all sectors, including establishment of a farmer registry system, and

agriculture. The changes also included a decrease other directed production subsidies.

in import tariffs, transition to an export-oriented

strategy, and liberalization of financial markets Meso level: In 1999, Turkey established the

that allowed free movement of capital interna- Banking Regulation and Supervision Agency;

tionally and banks to determine their own interest and in 2001, it passed a new banking law that

rates. Those reforms improved the market cap- regulated the financial sector and restructured

italization of the financial system, increased the financial institutions. As a result, Ziraat Bank had

role of private banks in the macroeconomy, and to increase credit interest rates to market levels

partially opened the market to imports of agricul- in order to lower the banks’ operational losses,

tural products. However, Ziraat Bank and ACC keeping them there until 2004. This enabled the

kept their monopoly positions in the agricultural competitive environment necessary for private

finance market by supplying subsidized credits to

7banks to enter the market. In the same period, In 2014, the government passed a new land law to

the government privatized a small bank owned by prevent the further fragmentation of agricultural

the credit cooperatives of fig, grape, cotton, and land and aggregate small landholdings, when pos-

olive farmers (Tarisbank)—this became the first sible. The law states that agricultural lands cannot

significant commercial bank in the agricultural be divided into multiple parcels that are smaller

finance sector. Additionally, Turkish banks than the limits in the legislation. Moreover, when

started to follow BASEL-II rules, further improv- a farmer plans to sell land, owners of neighboring

ing the financial stability of the system. The credit lands have some priority as buyers. As land sizes

registry bureau of Turkey—which was established increase, farmers can improve their collateral,

by banks in 1995—was enhanced in 2011 with and thus their access to financing.

a new regulation to cover all governmental and

non-governmental financial service providers. Micro level: The Strong Economy Program

abolished administered output prices and de-

In 2005, the Turkish government launched creased, stopped, or reformed agricultural subsi-

new regulations and institutions to support the dies (including subsidized credits by Ziraat Bank

transition toward market-based agriculture, and and ACC). Administered prices were replaced by

to align Turkish agricultural institutions with direct income support; however, this proved un-

the institutions of the EU. Among these new successful in increasing agricultural production,

regulations, the establishment of an agricultural and in 2010 was replaced by a regional support

registry system was one of the most important for scheme (in Turkish: Havza Bazli Destek Sistemi).

the country’s financial system. The government Those support policies were also empowered with

collected information on true capital and land organic agriculture and livestock support pro-

structure of farmers through the system, which grams involving subsidized credits since 2018.

enabled the implementation of other micro

policies (e.g., establishment of insurance pools). The new agricultural insurance law established

In 2013, the agricultural trade credit evaluation the Turkish Agricultural Insurance Pool (TAR-

system (TARDES) became effective under the SIM) to improve farmer access to affordable

credit registry bureau of Turkey. This system insurance by providing a government subsidy.

combines information from the agricultural From 2005 to 2018, the take-up rate for agricul-

registry system and the existing credit registry tural insurance increased from 0.5% to 16%. This

bureau to estimate the annual cash and credits system also helped banks extend loans with lower

of farmers and evaluate their credit applications. interest rates to insured farmers.

The system includes ± 200,000 farmers (±7% of

the registered agricultural holdings) as of 2017. The government established a credit guarantee

fund in 2005 to support small- and medium-sized

The government also passed a new law on li- enterprises (SMEs) to access loans for new or ex-

censed warehousing in 2005. This enabled banks panding businesses, input purchases, investments

to use receipts from the warehouse as collateral in new technologies, moving to a new workplace,

in farmer credit applications (i.e., a warehouse working capital finance, trade finance, and leas-

receipt system). ing. The fund guarantees help banks offer lower

credit loans up to USD 150,000, including to

farming enterprises. The government is currently

8working on a larger guarantee scheme specifically Note on both Turkey and Mexico: In both

for farming enterprises. countries, the structure of agricultural production has

changed substantially after the year 2000. Aggrega-

tors and processors, and foreign direct investment,

What happened in the agricultural have influenced the way in which production and pro-

finance market? cessing are structured, and financed. Also in the two

countries, their proximity and trade agreements with

Turkey had a relatively favorable environment to the EU (Turkey) and NAFTA (Mexico) have boosted

expand private banking in the 2000s. Most con- the emergence of modern value chains, with higher

sumers (including farmers) already had a bank levels of vertical integration (i.e., financing from the

account with a debit card. There were widespread top) and/or partnerships with domestic and foreign

branches of private banks, and ATM and tele- private banks and investors. High-value export crops

communication facilities all over the country. The such as dried fruits and vegetables in Turkey (e.g.,

banking sector was using a credit scoring system, Berk, 2013), or avocados and other high-value horti-

and there was a national ID registry system. After culture in Mexico, have become examples of globally

the meso- and micro-level reforms combined with integrated value chains. This paper does not look in

this favorable environment, private banks entered depth at these structural changes in the agricultural

the agricultural finance market, introduced new market but does acknowledge that these changes have

products (e.g., farmer credit cards to purchase a substantial “demand-side” impact on how primary

inputs, farmers loans through SMS messages), producers and agri-SMEs seek and access credit and

and increased their market share substantially. insurance.

As of 2018, private banks supply 31% of credit to

the agricultural sector while the state banks and

ACC provide about 69%.

There are, however, two important challenges to

improving Turkish farmers’ access to finance and

the role of private banks in that finance. First,

smallholder farmers cannot benefit from the

existing credit guarantee fund targeting SMEs.

Second, private banks cannot distribute subsi-

dized or zero interest government credits, a role

that is reserved for Ziraat Bank.

910

AGRICULTURAL FINANCE

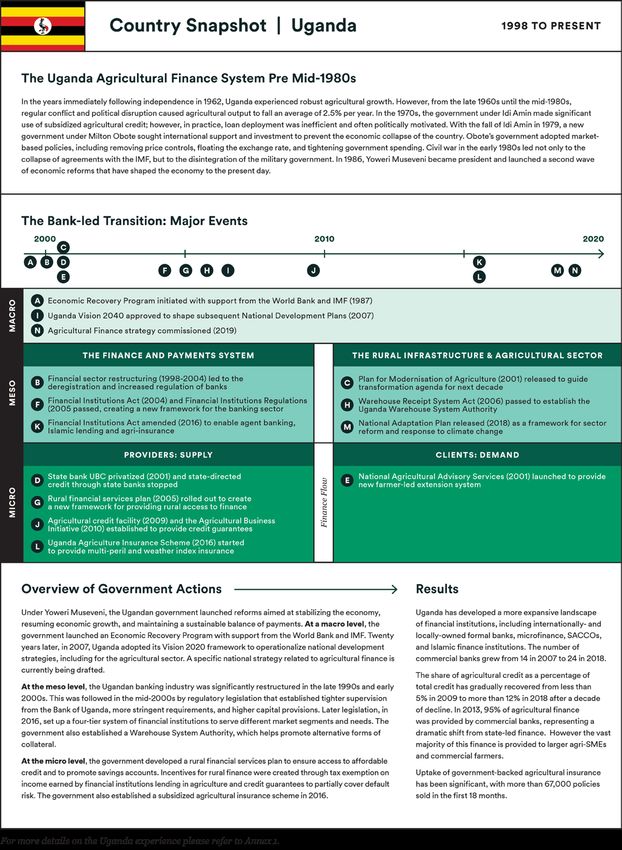

HISTORICAL CASE STUDY: UGANDA

Summary of Uganda’s agricultural in Uganda; one of many reasons why private

development sector investment in Ugandan agriculture has

been modest compared to Kenya, Tanzania,

With a population of 44 million and a population or Ethiopia.

growth rate of 3.3% per year, Uganda is one of the

fastest-growing countries in East Africa. Current-

ly, agriculture accounts for 24.2% of GDP, 50% of A brief view of the government-led

all exports, and 65% of employment, overwhelm- era (1962-1987)

ingly on small farms under 2 hectares.

Following independence in 1962, the Ugandan

In Uganda, agricultural growth was robust in the government followed inward-looking economic

years immediately after independence in 1962. policies based on import substitution, central

The late 1960s until the mid-1980s were, how- planning, and licensing for mining and other

ever, characterized by disruption and conflict— industries. When Idi Amin came to power in

particularly during the 1970s, when agricultural 1971, he expelled many Ugandan-Asian business

output fell at an average rate of 2.5% per year. families while dramatically expanding the public

Today agriculture is confronted with multiple sector. There were only 10 parastatals in 1972.

structural challenges, such as the predominance By the mid-1970s the number of parastatals

of smallholdings, practicing rain-fed low-yielding increased to 23 and were responsible for up to

agriculture, tenure insecurity, and poor infra- 250 different business enterprises.

structure. In 2014, only 16% of farmers purchased

inputs. Uganda is among the most vulnerable and A significant public expense in this period was the

simultaneously least adapted countries to climate use of subsidized agricultural credit. The govern-

change, and increasingly frequent climatic shocks ment established specific institutions—such as

take a heavy toll on rural livelihoods and the the now defunct Uganda Commercial Bank (UCB)

economy. and the Cooperative Bank—to make relatively

cheap credit widely available to farmers and

The average size of Ugandan farms is shrinking. facilitate the modernization of agriculture. Under

From 2006 to 2016, the share of all household this scheme, loans were provided at subsidized

farms that were less than two hectares in size interest rates (highly negative interest rates in

rose from 75% to 83%. These challenges hamper real terms). In reality, these interventions became

agribusiness development and commercialization an instrument for outreach and influence, with

11little attention paid to the financial health of both domestic and foreign sources. International

the lending institutions. Politically motivated aid has provided a crucial cushion since the

loan forgiveness, major natural calamities or reforms started: first, for the repair of essential

price slumps, and inefficient loan deployment infrastructure, and second, to enable the country

weakened the repayment culture in rural Uganda. to undertake reform measures. Of particular note

Hence, periodic capital injections were required was the debt relief provided by the Paris Club of

to keep the lending institutions alive. Both banks multilateral lenders. Under the Highly Indebted

were eventually rendered insolvent in 1998/99. Poor Countries (HIPC) initiative, Uganda was

forgiven its debt in different cycles in 1998 and

With the fall of Idi Amin in 1979, a new gov- 2000. This enabled the country to, among other

ernment under President Milton Obote sought things, save funds and used this to fund the

support from the IMF and World Bank to prevent growth of its economy.

the economic collapse of the country. To encour-

age foreign investment, the new government

adopted market-based policies including removing Structural adjustments in the

price controls, floating the exchange rate, and agricultural finance sector

tightening government spending. Owners of

expropriated firms and properties were encour- Macro level: The National Resistance Move-

aged to return. The collapse of the IMF’s stand-by ment launched the Economic Recovery Program

arrangements in mid-1984 and the disintegration (ERP) in May 1987, with support from the

of the military government in early 1986 after World Bank and IMF. The goals of the program

five years of civil war marked substantial deteri- remained more or less intact in the following

oration in economic performance in Uganda. In decade: to stabilize the economy, bring about a

January 1986, Yoweri Museveni became president, resumption of growth, and enable maintenance

a role he has held to the present day. of a sustainable balance of payments position.

Macroeconomic stability has ensured contain-

ment of inflation to single-digit levels, positive

What changed in the late 1980s? GDP growth rates (above 4.5% per year), and a

reasonable level of international reserves. This

From 1987 onward, the government of Yoweri stabilization of the macro-economic environment

Museveni launched the second wave of reforms created new space for agricultural finance to

aimed at stabilizing the economy, resuming slowly re-emerge over the following years.

economic growth, and maintaining a sustainable

balance of payments. Changes touched the public In 2007, Uganda Vision 2040 was approved to

sector, markets, and prices, as well as exchange provide development paths and strategies to op-

rates and trade. Since 1992, Uganda has managed erationalize Uganda’s vision statement, which is

to combine high levels of economic growth with “A Transformed Ugandan Society from a Peasant

low levels of inflation. However, while the first to a Modern and Prosperous Country within 30

bout of growth was partly ascribed to the recovery years.” Successive National Development Plans

of production capacities—as peace returned to the sought to operationalize this vision and included

country and policies became more predictable— a reform framework for the agricultural sector.

subsequent growth demanded investment from While there has never been a specific national ag-

12ricultural finance policy, in 2019 the government, In 2006, the Warehouse Receipt System Act

through the Ministry of Finance Planning and established the Uganda Warehouse System

Economic Development developed one which is Authority, an independent regulatory body that

currently going through the final approval process. started to operate in 2015. With this measure, the

government is attempting to promote alternative

Prior to 2005, policy efforts to improve access to forms of collateral that could enhance agricultural

financial services in Uganda focused on enabling lending.

microfinance institutions to transform into

deposit taking institutions, supported by the In 2016, the government amended the Finan-

Microfinance Deposit Taking Institutions Act 2003. cial Institutions Act (FIA) that allowed for the

provision of agent banking, Islamic finance, and

Meso level: In the late 1990s and early 2000s, bancassurance (selling insurance through bank

the Ugandan banking industry underwent signif- channels). A four-tier system of financial insti-

icant restructuring. Several indigenous commer- tutions was also set up to serve different market

cial banks were declared insolvent, taken over by segments and needs. One of the most significant

the central bank, and eventually sold or liquidat- recent developments, in 2017, was the enactment

ed. This restructuring was followed by the passing of prudential and non-prudential regulations for

of the Financial Institutions Act in 2004 and the Tier-4, previously unregulated financial insti-

Financial Institutions Regulations in 2005, which tutions. These regulations apply to about 1,749

created a new framework for the banking sector operational SACCOs; 81 licensed Non-Depos-

that included tighter supervision from the Bank it-Taking Institutions; at least seven microfinance

of Uganda, more stringent requirements, and wholesale lenders, 446 licensed money lenders;

higher capital provisions. During 2008 and 2009, and thousands of informal Village Savings and

several of the existing banks accelerated branch Loan Associations (VSLAs)

expansion through mergers and acquisitions or

new branch openings. Another significant development is the enactment

of the Movable Property Security Interest Act no.

The restructuring led to significant growth in 8 of 2019 and the attendant regulations, which

both formal (banks, credit institutions, and makes it possible to use moveable property as

microfinance deposit-taking institutions) and security and establishes security interests in other

semi-formal (SACCOs and VSLAs) financial assets such as livestock, furniture, and produce.

service providers. The number of commercial

banks (Tier-1) grew from 14 in 2007 to 24 in Micro level: Since the mid - 1980s, the gov-

2018. Currently, most banks in the country are ernment of Uganda has implemented several

foreign-owned, including major international targeted agricultural financing schemes. For

institutions such as Stanbic, Citibank, Barclays, example, the Government of Uganda through the

and Standard Chartered. However, several locally then Development Finance Department (DFD) of

owned banks have been established, including Bank of Uganda managed several credit programs

DFCU Bank, Postbank, Housing Finance Bank that supported various investment projects in

and Centenary Rural Development Bank. the different sectors of the economy, including

agriculture, agro-industry, manufacturing and

others. DFD also coordinated a number of

13credit related programs including; the Linkage Since the mid-2000s credit guarantees have been

Banking Program under the Africa Regional used to partially cover default risk, ensuring secure

Agricultural Credit Association (AFRACA); the repayment of all or part of formal sector agribusi-

Capacity Building Program (CBP) for micro ness loans. Several facilities supporting the agri-

finance institutions under the Cotton Sub-sector cultural industry have been established, including

Development Project; Research and advocacy on USAID’s DCA Guarantee Scheme, the Agricultural

Government programs, policies and processes Business Initiative (aBi Trust, a multi-donor trust)

from a gender perspective under the Gender and and the Agricultural Credit Facility (ACF), which

Economic Reform for Africa (GERA) initiative of was set up by the government of Uganda in partner-

the North - South Institute of Canada; Capacity ship with Participating Financial Institutions (PFIs).

Building for Rural Women Financial Intermedi-

aries Program financed by a grant sourced from In 2016, the government established the Uganda

IFAD; and the DANIDA-funded Rural Financial Agriculture Insurance Scheme (UAIS) as a

Services Component (RFSC), which was aimed at multi-peril and weather-indexed insurance pilot

widening financial services outreach to the rural whose objective is to cushion farmers from losses

areas. Although the above schemes yielded some arising from natural disasters and to attract

individual successes, they did not necessarily lead financing to agriculture. As part of this program,

to the sector-wide transformation as they did not the government provides premium subsidies. The

resolve what continually constrains the moderni- program has achieved significant uptake with more

sation of agriculture and what makes smallholder than 67,000 policies sold in its first 18 months.

farming and agri-MSMEs very risky for financing.

In 2001, the agricultural state bank UCB was pri- What happened in the agricultural

vatized into the hands of the South African Stan- finance market?

dard Bank group. By that time, UCB represented

two-thirds of the branch network in the country The transition from directed credit through

and held around 50% of the bank deposits in UCB in the early 2000s to a more pluralistic,

the country. In 2005, the government developed private sector-oriented financial system was

a rural financial services plan to create a new a process that has played out over the past 20

framework for providing rural access to finance years. Structurally, Uganda has developed a more

through new channels. The plan had six objec- expansive landscape of financial institutions

tives, including to ensure access to loanable funds and a more robust policy framework that has

at affordable interest rates and the promotion of facilitated the entry of a number of new products,

savings accounts. Moreover, the fiscal incentives including mobile money, value chain finance,

included tax exemption on income earned by and micro-insurance. The share of agricultural

financial institutions lending to agriculture credit as a percentage of total credit has gradually

(introduced in 2006/07), income tax exemptions recovered from less than 5% in 2009 to over 12%

for new rural agriprocessing investments, and no in 2018 after a decade of decline. In 2013, 95%

value added taxes (VAT) on most agricultural in- of all agricultural finance was provided by com-

puts and services. This policy promoted SACCOs mercial banks, demonstrating the dramatic shift

as the primary delivery channel; because they are in the structure of the sector since the late 1990s.

member-owned and -controlled, SACCOs were However, this increase in agricultural lending

ideal channels for the government’s aspirations.

14has been highly concentrated in credit provision

to mid- and large-sized companies operating in a

small number of primarily export-oriented value

chains.

Over the past two decades, smallholder farming

households and micro agricultural SMEs have

become primarily the customers of SACCOs, mobile

money providers, donor-funded development pro-

grams, and government insurance. These offerings

have increased the level of formal financial inclusion

in Uganda, with 58% of rural adults having an

account at a financial institution or a mobile money

account in 2017, up from 20% in 2011 (World Bank,

2017). However, at the same time from 2006 to

2016, the share of all household farms that were less

than two hectares in size rose from 75 percent to

83 percent, greatly increasing the fragmentation of

smallholder production in the country.

Today, a gradually maturing and pluralistic

financial system continues to develop within the

governments’ 2040 vision, national development

plans and the draft National Agricultural Finance

Policy. Donor and government subsidies continue to

support affordable credit, insurance, and extension

of financial inclusion through savings accounts.

However, progress remains slow for the vast majori-

ty of smallholder households and micro-SMEs.

1516

You can also read