Clean Captive Installations in sub-Sahara Africa - Focus: Industrial clients in South Africa

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Clean Captive Installations in sub-Sahara Africa

Focus: Industrial clients in South Africa

Kick-off meeting presentation

FS-UNEP Collaborating Centre

November, 2019

Supported by:

based on a decision of the German Bundestag

Overview of project

Snapshot of the various stages in the project

Initiating the project Assistance from FS-UNEP Expected outcomes

1 3 6

Desk study Development of tools Implementing the best chosen

through research identifying business models showcase project and replicating the

in-house & consultative expertise selecting financing mechanisms model

2 4

Stakeholder consultation

scoping missions Identifying relevant & key partners

relationship building

5

Selection of replicable designs (best

model); designing selection criteria

for national showcase project

Design process to monitor and verify Understanding best practices & replicability

Awareness creation within both public and

performance of chosen model and showcase by increasing uptakes

private stakeholders, whose feedback will be

viability of said model for easy access to Help countries meet climate and

integrated into project design

public development goals of the Paris Agreement

2

Preliminary findings from the desk study

What have we understood so far

1

South Africa has an acute The national power utility Eskom has over R440 billion of debt due to problems in bill collection from

undersupply of electricity and its customers in recent years and ageing infrastructure

national power utility faces

financial crisis >85% of the country’s electricity is generated by coal power plants which are nearing the end of their lifetimes

2

Growth in local RE markets crucial Since 2011, capacity totalling 6GW has been procured from 92 utility-scale projects

to achieving its NDC targets for

2030 Implementing the proposed 2018 IRP will bring South Africa closer to it the upper-end of its 2030 NDC targets

3

Municipal support for SSEG fosters As of 2018, there were 165 municipal electricity distributors with own tariff structure

commercial and industrial sectors

(Preliminary findings from the desk study

What have we understood so far

1 South Africa has an acute The national power utility Eskom has over R440 billion of debt due to problems in bill collection from customers in

undersupply of electricity and its recent years and ageing infrastructure

national power utility faces financial

>85% of the country’s electricity is generated by coal power plants which are nearing the end of their lifetimes

crisis

The power situation South Africa's installed capacity as of 2018 (totaling 52,404 South Africa’s electricity supply & demand balance

MW) without imports or exports

Electricity market is

dependent on the

state-owned utility 270

Coal 37149

Eskom

Eskom‘s government Gas/ Diesel 3830 260

bailout - plans to

Storage 2912 250

restructure it by 2021,

by separating Eskom Hydro

Electricity (TWh)

2100 240

into Generation,

Transmission and Large Wind 1980 230

Distribution operations Nuclear 1860

220

South Africa still depends

mostly on coal plants Large Solar PV 1474

210

which do not comply with Other (CoGen Biomass Landfill) 499

environmental regulations 200

and are nearing the end of Dist. Gen. (1-10MW) 300

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

their lifetimes

CSP 300

Electricity demand has

steadily decreased in 0 10000 20000 30000 40000

recent years, among other

factors, mainly due to low Demand Production Production less losses

economic growth and rising Capacity (MW)

electricity tariffs

4Preliminary findings from the desk study

What have we understood so far

1 South Africa has an acute

The national power utility Eskom has over R440 billion of debt due to problems in bill collection from customers in

undersupply of electricity and its

recent years and ageing infrastructure

national power utility faces financial

crisis >85% of the country’s electricity is generated by coal power plants which are nearing the end of their lifetimes

2

Growth in local RE markets crucial to Since 2011, capacity totalling 6GW has been procured from 92 utility-scale projects

achieving its NDC targets for 2030 Implementing the proposed 2018 IRP will bring South Africa closer to it the upper-end of its 2030 NDC targets

Is there a need for captive RE? Eskom’s installed capacity and available capacity

In South Africa there are still cases of

multiple load shedding with Eskom’s Customer Demand Current Demand, 30

unplanned breakdowns being the main

contributor Diesel Plants (no fuel left), 2

Eskom's unplanned

Eskom Outages Maintenance, 5

The ageing infrastructure calls for new breakdowns, 17 Imported

Hydro, 1

build ups soon: RE as part of this build up

South Africa has both, the need as well as Supply Resource

Load-

Eskom's available capacity, 23 IPPs, 3

the demand for captive solar. Regulatory shedding, 4

uncertainty, however, holds back

implementation of large-scale projects 0 5 10 15 20 25 30 35

>1MW.

Power (Gigawatts)

5Preliminary findings from the desk study

What have we understood so far

1 South Africa has an acute

The national power utility Eskom has over R440 billion of debt due to problems in bill collection from customers in

undersupply of electricity and its

recent years and ageing infrastructure

national power utility faces financial

crisis >85% of the country’s electricity is generated by coal power plants which are nearing the end of their lifetimes

2

Growth in local RE markets crucial to Since 2011, capacity totalling 6GW has been procured from 92 utility-scale projects

achieving its NDC targets for 2030 Implementing the proposed 2018 IRP will bring South Africa closer to it the upper-end of its 2030 NDC targets

3

Municipal support for SSEG fosters As of 2018, there were 165 municipal electricity distributors with own tariff structure

commercial and industrial sectors

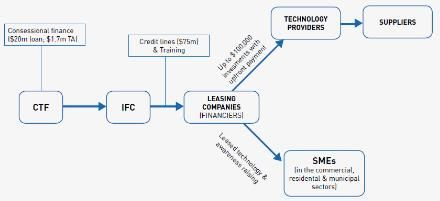

Under REIPPPP, c. 6GW from IPPs has been successfully procured

(Preliminary findings from the desk study

What have we understood so far

4

Many of the major commercial banks have funded large utility-scale solar PV projects as part of REIPPPP; variety of

RE financing is well-established for financing mechanisms offered for rooftop-scale installations, loan products for RE projects by four main retail banks

some market segments

Nonetheless, scalable financing solutions that lower the upfront costs for most captive customers are still lacking

Industry sectors and power consumption

RE financing sector is well-established with major commercial banks funding large utility-scale projects as part of REIPPPP.

Moreover there are five commercial banks (Nedbank, FNB/RMB, Standard Bank, Absa, Investec) as well as public banks

which include local development finance institutions such as the IDC an the DBSA

South Africa’s five main commercial banks have multiple loan products to assist with financing RE projects. Though,

rates tend to be fairly high relative to international standards as they are typically tied to the local prime lending rate (e.g.

10.25% in July 2019)

With the help of international development finance institutions a number of donor and development agency programs for RE

have been introduced. AFD targeted the private EE and RE sectors and KfW, as well as RMB, launched South Africa’s first

debt-fund focused on small RE-projects (Stakeholder consultations

What information do we need to streamline the process of installing captive PVs

1 … through customised and tailored approach in reaching out to potential stakeholders

South Africa has an acute

undersupply of electricity and its

national power utility faces

financial crisis

Bridge gap in data and information…

2

Growth in local RE markets crucial

to achieving its NDC targets for

2030

3

Municipal support for SSEG fosters

commercial and industrial sectors

(Streamlining the process

How does the FS-UNEP collaborating centre help?

1

A. Ownership model C. Equipment leasing model Financing mechanisms

Development of tools B. ESCO financing model

identifying business models

selecting financing

mechanisms

2

Associations/Public Sector Banking sector Financial Institutions

Identifying relevant & key

partners RE private sector Power sector Private Renewable Sector

3

Currently, there is a lack of monitoring and verification of installed captive PV projects

Selection of replicable designs There is also not enough publicly available information explaining the advantages of captive

(best model); designing solar PV and potential risks that exist (e.g. for industrial users: payback period of installations,

savings per year, etc.)

selection criteria for national Implementing one project to showcase it as a replicable model will improve transparency in

showcase project this captive PV market. Monitoring performance of the selected model will prove it to be used as

a viable design for other industrial users

9Final expected outcomes and timeline

Project will run from 2019 - 2023

2019

Component 1: Baseline studies and awareness

raising

2019 - 2020

Component 2: Economic and financial tools and

assessments

2020 - 2023

Component 3: Realisation of one showcase project

per country

2019 – 2023

Component 4: Knowledge dissemination and

outreach

10Thank you for your patience! For further information please visit: Tobias Panofen Madhumitha Madhavan www.captiverenewables-africa.org Email: t.panofen@fs.de Email: m.madhavan@fs.de Supported by: based on a decision of the German Bundestag

You can also read