Coronavirus impact monitor - 17 April 2020 - Deloitte

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Coronavirus impact monitor 17 April 2020

Corona virus outbreak

Slowdown in transmission in Europe with the US becoming the

centre of the pandemic, no post-Easter peak in Sweden

• Since the publication of the previous edition of the Coronavirus Confirmed COVID-19 cases

1 000 000

impact monitor the number of confirmed cases of COVID-19 671 331

globally has increased from 1,392,000 to 2,114,000, mainly driven 182 816

168 938

100 000

Number of confirmedcases

by the U.S.

81 166 *

• Sweden did not see a post-Easter peak in new cases, as the 10 000 12 545

authorities initially feared. Current data indicate a peak in new

cases before the Easter holidays, with the rate of transmission

1 000

coming down since then. The number of confirmed cases as of 17

April is 12,545, having been only 13 on 1 March. However, these As of

100 17 April 2020

figures are underestimates of actual numbers as testing is reserved

for health care staff and those in need of care.

10

• Several countries seem to have turned a corner with the number of 1 8 15 22 29 36 43 50 57

daily new cases now in decline. In Italy and Spain new confirmed Days after more than 10 cases

cases have begun falling. The US now has the highest number of

Sweden Spain Italy USA China

new cases globally, while China has seen only roughly 2,500 new

cases since 20 March.

Fatalities due to COVID-19

100 000

• In Sweden the number of COVID-19 fatalities as of 17 April is 1,333,

19 130 33 284

having risen from 10 as of 19 March. However, the peak in new 22 172

fatalities seems to have been achieved, with the number of new 10 000

Number of fatalities

3 253 *

fatalities stabilising in the past few days compared with early April.

• Having far surpassed China, the number of fatalities in Spain and 1 000 1 333

Italy has begun to plateau, while the US still seems to be in the

acceleration phase. China saw only 93 new fatalities between 20 As of

100

March and 16 April, although 1,290 new fatalities were added to 17 April 2020

the total on 17 April as city authorities in Wuhan, ground zero for

the pandemic, checked online data against information gathered in 10

person from hospitals, funeral homes and other sources, bringing 1 8 15 22 29 36 43 50 57

the total death toll in China to 4,636. Days after more than 10 deaths

Sweden Spain Italy USA China

Source: European Centre for Disease Prevention and Control 2

* As of 20 March 2020

Impact on financial markets

European equity markets suffering major

losses from the outbreak of COVID-19

• European equity indices suffered material declines at the outbreak of European equity indices

COVID-19 on the continent. 130 Major outbreakin Europe

Indexed to 100 as at 2 January 2020

120

• However, recent weeks have seen signs of stabilisation with most

sectors seeing broad based share price recoveries. 110

100

• Travel and leisure together with the industrial sector continues to be

90

among the most affected sectors as judged by equity market

developments. 80

70

• The EURO STOXX Travel & Leisure remains down by close to 40% since

the beginning of January 2020 while Industrials have seen declines of 60

around 30%. 50

40

• Having initially outperformed other sectors, Utilities have following the 02-jan-20 16-jan-20 30-jan-20 13-feb-20 27-feb-20 12-mar-20 26-mar-20 09-apr-20

initial sharp declines moved largely in tandem with other sectors. Technology Health Care Travel & Leisure Telecom

Utilities Industrials Materials

• No material outperformance can be seen for the Health Care sector

overall albeit certain individual companies have fared relatively well, Bank share prices

including the Swedish Large Cap company Getinge whose operations

include the manufacturing of ventilators. Indexed to 100 as at 2 January 2020

140

• Credit losses are seen mounting at Swedish financial institutions but

share prices of its major financial institutions have stabilised in the 120

most recent period in line with what have been seen in other regions.

100

• The major Swedish banks have overall seen less severe declines in their

share prices compared to European and American peers. 80

60

40

01-jan-18 01-maj-18 01-sep-18 01-jan-19 01-maj-19 01-sep-19 01-jan-20

Swedish Banks Italian Banks Euro stoxx Banks KBW US Banks

Note: 1) EURO STOXX indices for Technology, Health Care, Travel & Leisure, Telecommunications, Utilities, Industrial Goods & Services, Materials, and Banks. 3

2) Swedish and Italian bank indices reflecting an equal weighted portfolioof the largest four banks by market capitalisation in each respective country. Source: S&P Capital IQ

Impact on financial markets

European rate and credit markets also affected

by the outbreak of COVID-19

• Amid a flight to safety and scramble for liquidity, interest rates European interest rate environment

across Europe rose at the outbreak of COVID-19. 3.5

3.0

• However, for the most highly rated countries, and supported by

2.5

intervention from monetary authorities, rates have now stabilised.

2.0

• Nevertheless, a certain change in sentiment can be seen in the 1.5

% rate

wider spread between the German and Italian government bond 1.0

yields following an extended period of contraction. 0.5

• While the spread moderated after an initial spike, the yield -

difference has now again started to increase. (0.5)

(1.0)

• In Sweden, the yield on ten year government bonds has jumped (1.5)

from deeply negative up to a around 0% but subsequently 01-Jan-19 01-May-19 01-Sep-19 01-Jan-20

stabilised. Germany vs. Italy 10YR German sovereign 10YR Italian sovereign

• Interbank and swap rates have also been on the rise but now seen

signs of levelling out.

• Given that a considerable portion of Swedish companies fund Swedish interest rate environment

themselves at floating rates or with short interest fixing periods – 1.4

particularly within the real estate sector – higher interbank rates 1.2

have the potential to translate into increased borrowing costs. 1.0

0.8

• A sharp drop in demand has already put pressure on credit profiles 0.6

of major European companies, with transportation and travel 0.4

% rate

heavily affected. 0.2

-

• Rating agencies have begun downgrading a large number of major

(0.2)

issuers of debt in the European market, and the speculative / high

(0.4)

yield segment has seen a considerable portion of ratings being cut.

(0.6)

• The rating agency Moody’s now expects default rates globally to (0.8)

01-Jan-19 01-Mar-19 01-May-19 01-Jul-19 01-Sep-19 01-Nov-19 01-Jan-20 01-Mar-20

jump from 3.5% in March 2020 to 11.3% by next year March 2021.

10YR Swedish sovereign 3M STIBOR 10YR SEK swap rate

This expectation reflects an assumption of an economic recovery

that begins to take hold towards the end of 2020.

Source: S&P Capital IQ, Moody’s Investors Service 4

Impact on financial markets

US credit markets experiencing major

disruptions from the outbreak of COVID-19

• US credit markets experienced considerable disruptions at the US corporate credit spreads

outbreak of the COVID-19. 3,000

• Credit spreads initially jumped with notable spread widenings

2,500

particularly for the most sensitive non-investment grade

borrowers (“high yield”). 2,000

Spread (bps)

• The impact of the virus prompted the Federal Reserve to launch 1,500

what many analysts have considered to be unprecedented

interventions to stabilise markets. 1,000

• The interventions range from purchasing not only government 500

and asset-backed securities, but also corporate debt.

-

• The Federal Reserve has also committed to support the US 01-Jan-19 01-Mar-19 01-May-19 01-Jul-19 01-Sep-19 01-Nov-19 01-Jan-20 01-Mar-20

commercial paper and municipal bond markets, as well as the 5-year USD AA Z-spread 5-year USD BBB Z-spread

functioning of money market funds, the latter a key funding 5-year USD BB Z-spread 5-year USD CCC Z-spread

source for US corporates.

• Supported by such interventions, credit spreads have started to

moderate, and within the high yield segment in a rather material European and Swedish corporate credit spreads

way. 600

• Similar to US and European corporates, Swedish investment grade 500

companies have also seen increased cost of funding as reflected in

widening spreads. 400

Spread (bps)

• However, as seen in other markets, spreads for SEK issuers have 300

stabilised following intervention of central banks and other

monetary authorities, albeit at significantly higher levels than seen 200

in recent times before the virus outbreak.

100

-

01-Jan-19 01-Mar-19 01-May-19 01-Jul-19 01-Sep-19 01-Nov-19 01-Jan-20 01-Mar-20

5-year EUR AA Z-spread 5-year EUR BBB Z-spread

5-year EUR BB Z-spread 5-year SEK BBB Z-spread

Source: ThomsonEikon 5

Impact on commodity markets

Sharply lower oil prices affected by both demand

and supply disruptions with metals still relatively

steady

Energy commodities

• The dual impacts of sharply lower demand from the COVID-19 outbreak

and increased Saudi supply have been clearly visible in oil markets. 135

• Since the beginning of 2020, crude prices are down by around 60%. 120

105

• While other energy commodities have held steady, albeit in the case of

natural gas and uranium at already depressed levels, there was initially 90

Index

little respite seen in the persistent decline in the oil price which

75

continued even as financial markets saw some stabilisation.

60

• However, in the beginning of April 2020, oil prices experience a sharp

move upwards on speculation of coordinated production curtailments by 45

producers such as Saudi Arabia, and Russia.

30

02-Jan-20 16-Jan-20 30-Jan-20 13-Feb-20 27-Feb-20 12-Mar-20 26-Mar-20 09-Apr-20

• However, since the production curtailments were subsequently

Brent (USD) / barrel WTI (USD) / barrel Uranium (USD) / pound

announced by a large number of major oil producing countries, the price

Henry Hub (USD) / mmbtu Coal (USD) / ton

development for oil has been lacklustre.

• Contrary to the oil market, both cyclical metals such as copper and zinc,

and safe-haven precious metals such as gold have seen comparatively Metal commodities

resilient prices since the COVID-19 outbreak.

120 800x

• However, the price picture for base metals was subdued already at the 750x

110

outset with marginal operations struggling to achieve break-even.

700x

100

• An increasing ratio of cyclical copper to safe-haven gold continues to 650x

suggest a cautious outlook among investors and consumers of metals. 90

Index

Ratio

600x

• The stability in iron ore, for which China is the key importer and Sweden 80

550x

a major supplier via LKAB, has surprised analysts. 70

500x

• While the iron ore price has been supported by expectations of Chinese 60 450x

infrastructure investments to support a restart of its economy,

commodity analysts point to still plentiful supply and a long way to go 50 400x

02-Jan-20 16-Jan-20 30-Jan-20 13-Feb-20 27-Feb-20 12-Mar-20 26-Mar-20 09-Apr-20

from current price levels in the USD 80 / tonne range, down to estimated Copper (USD) / pound Zinc (USD) / tonne Gold (USD) / ounce

break-even levels around USD 50 / tonne. Iron 62% (USD) / tonne Gold / Copper ratio

Note: 1) Henry Hub represents natural gas delivered at the Henry Hub in Louisiana, USA . Coal represents coal delivered to the Newcastle port, Australia. 6

Source: S&P CapitalIQReal economic impact

The Swedish government presents Corona-influenced 2020 Spring

Amending Budget

High economic uncertainty reflected in the 2020 Spring Budget, signs of severe slowdown and expected recession

Economic measures presented 2020 Spring Budget

11 March 16 March 25 March 30 March 2 April 15 April

Increased government support for regions and

municipalities

Mainly increased unemployment support (“A-kassa”)

Loan guarantees and lower fees (payroll tax) for SMEs, restaurants & hotels

Shortening work hours (“korttidspermittering”), where the state will cover a large portion of

the costs as main feature. Up to 80% shortening of work hours as at 14 April 2020.

(Change of budget)

• The COVID-19 outbreak has pushed both the global and Swedish economy into • The high number of bankruptcies and restructurings reported in March 2020 and

unchartered territory. As per 15 April 2020, the Swedish government presented the 2020 predicted in April 2020 indicates a significantly weaker labour market for a foreseeable

Amended Spring Budget – heavily influenced by the Coronavirus pandemic. Briefly, the future, where the recovery phase is expected to continue for several years.

2020 Spring Budget is a summary of the previously announced support packages aimed at

• Due to containment measures restaurants & hotels have been affected most severely,

mitigating the economic impact of the virus, illustrated in the timeline above.

where the number of bankruptcy filings are predicted to increase by some 197% in April

• The Swedish government has also proposed to raise the level of the expenditure ceiling in 2020 as compared to April 2019. In the retail sector, bankruptcy filings are predicted to

2020 by SEK 350bn, given the high level of uncertainty of its forecast, which is dependent increase by 74%. A prominent example is the listed fashion retailer MQ, that on April 16

on the future spread of the virus. 2020 filed for bankruptcy due to the effects of the corona crisis. Overall a large number of

companies are predicted to file for bankruptcy in April according to the Swedish business

• The Swedish Central Bank has introduced a facility of up to SEK 500 bn for banks to support and credit reference agency UC.

lending to corporates at favourable rates. Additionally the Central Bank has decided to

extend its bond purchases this year to maintain credit supply to Swedish companies and • According to the Swedish government, the Swedish economy is headed towards a

continue to offer loans to banks in USD against collateral. recession with strongly negative GDP growth in 2020. As a base case (worst case) GDP is

expected to decline with around 4% (10%) and unemployment rates are expected at 9%

• As mentioned in the 2nd edition, termination notices and temporary layoffs have increased (13.5%). For comparison, note that GDP growth for 2020 as per January 2020 was

markedly during March, especially with restaurants, hotels and manufacturing. The expected at 0.8% and the unemployment rate as at 2019 was around 6.8%.

development has continued in April, where the number of temporary layoffs as at 10 April

2020 far exceeds the full April 2019 number. • Sweden’s low government debt at around 38.8% of GDP makes the capacity to mitigate

negative economic effects and deal with a potential recession following the COVID-19

• However, both Volvo Cars and Scania (who previously sent home their staff in March) has outbreak via further support measures less constrained compared to many other countries

announced that production will be restarted in week 17. with higher government debt, for example Italy.

Notes: Based on public data from Arbetsförmedlingen, Eurostat , UC and the public domain. 7

Sources: Arbetsförmedlingen, Eurostat, The Government of Sweden, Ministry of Finance Sweden, UC, Deloitte analysisEconomic Outlook: Deloitte survey

Sharp drop in GDP across the world in 2020 means return to

pre-virus levels only after 2021

Results of Deloitte surveys

Economic growth projections

What will be the ultimate impact on economic growth of COVID-19?

78%

Possibly severe but 58%

shortlived 75%

N/A 46%

slowdown 20%

47%

23%

42%

Protracted and 25%

severe downturn 54%

80%

53%

When do you think activity will rebound in your economy?

39%

30%

Q 3 2020 24%

31%

17%

13%

• The IMF released its spring economic forecasts • SBAB and SEB also released updated forecasts 28%

35%

Q 4 2020 40%

on 14 April, in which it expects the global this week. Both see a sharper drop in Swedish 0%

31%

20%

economy to see the worst contraction since the GDP in 2020 than the government, with SBAB at 23%

40%

1930s with global output down 3.0% in 2020, -5.0% and SEB at -6.9%. For 2021 SEB sees a Q1 2021 36%

39%

17%

worse than during the financial crisis when larger rebound, with GDP growth at 5.0% 47%

global GDP decreased by 0.1% in 2009. compared with SBAB’s view of 3.0%. Q2 2021 and

beyond 67%

20%

• The fund sees a partial recovery in 2021, with • Responses from nearly 2,000 participants in a

global growth above trend growth at 5.8%. Deloitte Economics global webinar with

Nevertheless, the level of GDP will remain colleagues and clients on 16 April show that the March 12 March 19 March 26 April 2 April 9 April 16

below pre-virus trends. respondents think the policymakers are

implementing adequate to forceful measures A sharp contraction in GDP is inevitable as a result of a freezing

• Advanced economies are set to take large hits against the economic effects of the virus. activity caused by the lockdown. Policymakers are aiming to

in 2020, with the euro area seeing negative Especially strong actions are the policies sustain the economic capacity through the downturn. How would

growth of 7.5%. Sweden will also see a sharp towards jobs and income with 59% support you rate the response of policymakers in following area:

drop of 6.8%, despite the more relaxed public from the participants.

health measures imposed by the government. 14%

Weak/adequate 6%

11%

• Compared with the forecasts in the Swedish

spring budget, the IMF expects a bigger drop in Probably adequate 35%

57%

2020 with a stronger rebound in 2021, leaving 63%

the Swedish 2021 GDP level relatively similar. 29%

Forceful/strong 59%

26%

1) Deloitte surveys conducted on 12, 19 and 26 March and 2, 9 and 16 April 2020, involving about 2,000 colleagues and clients globally. 8

Sources: International Monetary Fund, Swedish Ministry of Finance, SBAB, SEB, Deloitte surveys Support for businesses Support for jobs and income Support for financial marketsKey messages

The global economic slowdown is set to

hit the Swedish economy, but strong

public support has been announced by

the government

• The number of new confirmed COVID-19 cases finances are also know to be highly sensitive to

in Sweden is showing signs of slowing down, economic downturns.

having peaked before Easter. The number of

• According to a Global Deloitte Economics survey

cases currently stands at 12,545, with the

among 2,000 colleagues and clients from all

number of fatalities at 1,333.

over the world on 16 April 2020, expectations

• COVID-19 has caused severe damage on the are that the economic slowdown will be deep

world economy. The equity markets have and last throughout 2020.

suffered major losses, and equity market

• Deloitte Sweden will continue monitoring the

volatility has spiked to levels not experienced

impact of the Coronavirus in Sweden and

since the global financial crisis. Supply chain

globally.

disruptions and negative demand shocks have

spread from China to the rest of the world.

• In Sweden, the high number of bankruptcies and

restructurings reported in March 2020 and

predicted in April 2020 indicates a significantly

weaker labour market for a foreseeable future,

where the recovery phase is expected to

continue for several years.

• To counter the effects on the real economy, the

Swedish government has announced a series of

relatively ambitious support measures over the

past couple of weeks, while proposing to raise

the expenditure ceiling in its spring budget.

Sweden heads into the downturn with a

comparatively large degree of fiscal space with

debt to GDP at 38.8%. However, Swedish public

9For questions on the contents

of this report, please contact:

Mats Lindqvist

Partner, Financial Advisory

Mobile: +46 73 397 21 14

Email: mlindqvist@deloitte.se

Gareth Greenwood

Partner, Risk Advisory

Mobile: +46 70 080 23 15

Email: ggreenwood@deloitte.se

Disclaimer: The information in this document is intended for knowledge sharing only. 10Appendix

11Industry Outlook | Financial Services (1/2)

Major Swedish banks maintaining comfortable capital

positions and seeing regulatory support

Core equity tier 1 capital ratios Consumer bank share prices3

18.5% Collector Resurs Bank

17.0% 17.6% 17.4%

16.3% TF Bank Top 4 Swedish Banks

14.4% 14.3% 14.5%

11.9%

Swedbank Nordea SHB SEB Average Average Germany France Spain

Major Swedish Banks¹ ECB Supervised Banks²

02-Jan-20 02-Feb-20 02-Mar-20 02-Apr-20

Banking Consumer finance

• Leading Swedish banks maintain comparatively strong • Covered bonds are also a highly rated, key asset class for • Already under pressure from rising loan losses prior to

capital positions in a European context at the outset of the Swedish institutional investors such as insurers and COVID-19, Swedish consumer banks have until now

COVID-19 outbreak. pension funds. fared less well compared to their larger, more

• The capacity of Swedish banks to continue lending during • The Central Bank has provided certain indirect support to diversified major bank peers.

the virus outbreak and its aftermaths has also seen banks through its decision to now also include bonds • Rising unemployment rates due to virus containment

support from the Swedish FSA who has reduced the issued by non-financial companies in its ongoing SEK measures may put further pressure on this segment as

contracyclical capital requirement from 2.5% down to 0%. 300bn of security purchases. new loan volumes fall and loan loss provisions rise.

• Bank liquidity will be further underpinned by interventions • In a scenario where companies would otherwise have

from the Central Bank, notably a decision to broaden the been unable to roll over outstanding bonds amid a loss of

pool of covered bonds eligible as collateral. confidence among fixed income investors, they would

• The covered bond market and its smooth functioning is a likely have had initial recourse to their committed bank

vital component of the Swedish financial sector as it facilities, thus increasing risk exposures among banks.

represents a key funding source for the nation’s banks. • Cognizant of the heightened degree of uncertainty, all

four major Swedish banks have put dividends on hold.

Note: 1) Nordea is domiciled in Finland but retains significant operations in Sweden. 2) Institutions in the Euro Zone directly supervised by the European Central Bank and categorised as a “Significant Entity”.

3) Share prices indexed to 2 January 2020. Top 4 Swedish banks represent a basket equally weighted across the shares prices of SEB, SHB, Swedbank, and Nordea. Source: Company reports, Riksbanken, ECB, 12

Finansinspektionen, Fondbolagens Förening, S&P Capital IQ.Industry Outlook | Financial Services (2/2)

Low liquidity in bond markets see some Swedish mutual

funds freeze redemptions while equity funds experience large

outflows

Net new money flows for Swedish mutual funds

30.0 12.0

10.0

10.0

8.0

Net flows (% of AUM)

Net flows (SEKbn)

(10.0) 6.0

4.0

(30.0)

2.0

(50.0) -

(2.0)

(70.0)

(4.0)

(90.0) (6.0)

01-Jan-19 01-Feb-19 01-Mar-19 01-Apr-19 01-May-19 01-Jun-19 01-Jul-19 01-Aug-19 01-Sep-19 01-Oct-19 01-Nov-19 01-Dec-19 01-Jan-20 01-Feb-20 01-Mar-20

Equities Bonds Money market Equities (RHS) Bonds (RHS) Money market (RHS)

Asset management

• Reminiscent of the financial crisis, when global asset managers were forced to limit • Looking at net new money flows across Swedish mutual funds, strong inflows into

redemptions as markets in asset-backed securities froze, a number of Swedish asset equity products at the end of 2019 and briefly into 2020 reversed sharply during

managers have recently restricted fund withdrawals. March amid massive outflows corresponding to around 3% of AUMs.

• The freeze in redemptions have not only affected individuals, but also institutional • As a share of AUM, bond funds experienced even larger redemptions.

investors, as well as investment products invested in the funds.

• As a sign of the flight to safety, money market funds instead saw large inflows.

• The majority of freezes have been for funds targeting corporate bonds, a segment that

has seen steady growth in recent years amid low interest rates, but that remains a

relatively small and illiquid market segment.

• With lower AUMs1 and the possibility of reduced confidence among investors, already

compressed margins on the back of relentless shifts into passive investment vehicles

could translate into further pressure on industry profitability.

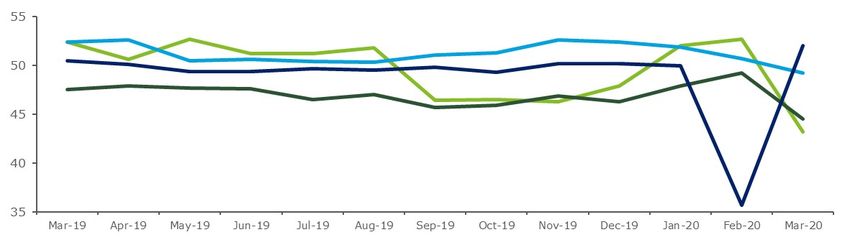

Note: 1) AUM: assets under management. Source: FondbolagensFörening. 13Industry Outlook | Manufacturing

Efforts to contain COVID-19 impact short-term

manufacturing output and demand

Manufacturing PMI Index as of 1 April 2020

Expansion

Contraction

Industry impact Economic outlook

• Coronavirus continues to be a critical supply chain risk for many European companies, as

• Swedish manufacturing PMI saw the largest drop on record in March, plummeting with 9.5

closed factories and transport restrictions increase average delivery times. Some relief can

points to 43.2. This represents a major disruption in the production plans of Swedish

be expected from the gradual reopening of factories in China, decreasing the supply chain

manufacturers.

risks for European companies.

• After a record drop in February due to efforts to contain COVID-19, Chinese manufacturing • Top priorities for manufacturers are to reduce operating costs, review spend, ensure that

PMI rose to 52.0, reflecting the reopening of many Chinese factories. However, this does financing remains viable and secure continued supply.

not mean a return to normal economic operations.

• Many European factories will remain shut down or running on less capacity until the

• For the euro area, PMI dropped to levels not seen since 2013. This fall was led by Italy, with COVID-19 spread in Europe has stabilised.

France, Ireland and Spain also recording multi-year lows.

• Lead times have markedly deteriorated as manufacturers face significant obstacles in

securing supplies.

• Factory jobs have been cut globally at the fastest rate since August 2009, as companies

scale back production capacity in line with falling demand and reduced supply.

Source: Swedbank/Silf, IHS Markit, Chinese National Bureau of Statistics. 14Industry Outlook | Metals & Mining

Suppliers to the mining industry likely to

experience lower demand even as metal prices

hold steady

Metals & mining sentiment

• While Sweden boasts few mining companies, Swedish firms 135

feature among leading global suppliers to the industry. 120

• Having seen sharp declines in early March, share prices of both 105

Boliden (major EU base metals producer) and leading mining

equipment and consumables suppliers Epiroc and Sandvik have 90

Index

regained ground and begun converging back to the price 75

performance for the underlying metals.

60 Copper 75% marginal cost percentile (est.)

• Despite a stable price picture, operational risks that could

materially affect suppliers to the mining industry are nonetheless 45

Copper 50% marginal cost percentile (est.)

now crystalizing in a material way. 30

02-Jan-20 16-Jan-20 30-Jan-20 13-Feb-20 27-Feb-20 12-Mar-20 26-Mar-20 09-Apr-20

• Major mine closures began to gain momentum in South America Brent (USD) / barrel Gold (USD) / ounce Copper (USD) / pound

but have now spread across the entire globe with mining Boliden Epiroc Sandvik

operations from Africa to North America seeing reduced output

or even being put on care and maintenance.

Price trends for Africa-sourced critical metals

• Altogether, developments to date continue to suggest that while 3,000 50

metal prices may hold steady, operational disruptions are likely to

45

depress production rates, thus in turn translating into lower 2,500

40

equipment and consumables demand for suppliers.

35

Price - Palladium

2,000

Price - Cobalt

30

1,500 25

20

1,000

15

10

500

5

- -

01-Jan-18 01-May-18 01-Sep-18 01-Jan-19 01-May-19 01-Sep-19 01-Jan-20

Palladium (USD) / ounce Cobalt (USD) / pound

Source: S&P Capital IQ, Wood Mackenzie, Deloitte estimates. 15

Note: Index set to 100 at 1 January 2020.Industry Outlook | Automotive

The Automotive industry plunges due to severe supply chain issues

European automotive company share prices

110

100

90

80

Autoliv

70

Volvo

60

Index

TRATON

50

EURO STOXX 600 Automobiles & Parts

40

30

20

10

0

02-jan 09-jan 16-jan 23-jan 30-jan 06-feb 13-feb 20-feb 27-feb 05-mar 12-mar 19-mar 26-mar 02-apr 09-apr 16-apr

• The impact of COVID-19 on today’s globally integrated automotive sector has been swift • The exogenous shock of the pandemic exacerbates an existing downshift in global

and significant. demand that will likely lead to increased M&A activity as opportunities for sector

consolidation emerge for private equity players.

• On the supply side, initial concerns over a disruption in Chinese parts exports quickly

pivoted to large-scale manufacturing interruptions across Europe, with assembly plant • The potential long-term impact may include auto companies being forced to divert capital

closures in the US adding to the intense pressure on an increasingly distressed global to shore up continuing operations, starving R&D funding for advanced technology

supply base. This leaves companies at risk of defaulting on covenants, potentially initiatives and other discretionary projects, while strategic decisions to exit unprofitable

requiring banks to step in. global markets and vehicle segments may be accelerated, significantly lowering output as

manufacturing capacity is rationalized/consolidated.

• In Europe, demand has collapsed, with new car registrations in March in Italy, France,

Spain and the UK down 85%, 72%, 69% and 44% respectively, compared with March • Suppliers facing liquidity issues may succumb to rapidly deteriorating market conditions,

2019. This represents a steeper drop than during the 2009 financial crisis. causing widespread disruption and potentially catastrophic consequences across the

entire global automotive manufacturing ecosystem.

• In Sweden, Volvo and Scania have announced their intention to start production again in

week 17, having shut down their plants in March, while Autoliv withdrew its planned • A significant amount of restructuring may be expected in the auto retail sector as dealers

dividend. The share prices of Swedish automotive companies have been performing are unable to pivot quickly enough to changing demand conditions.

largely in line with their Europeans peers since the pandemic outbreak.

16

Sources: Svenska Dagbladet, The Society of Motor Manufacturers and Traders in the UK

Note: Index set to 100 at 1 January 2020.Industry Outlook | Consumer products: Non-Food

Serious supply disruption, high consumer demand for certain

product categories with sales moving online

Swedish consumer products (non-food) company share prices

110

100

90

80

H&M

70 Fenix Outdoor

Index

60 Clas Ohlson

50 OMX30

40

30

20

10

02-jan 09-jan 16-jan 23-jan 30-jan 06-feb 13-feb 20-feb 27-feb 05-mar 12-mar 19-mar 26-mar 02-apr 09-apr 16-apr

• Because the COVID19 crisis started in China, the production hub of the world for • Clas Ohlson’s sales declined with 17% in March, while their online sales went up with 50%.

electronics, footwear, apparel, and other non-food products, Consumer Products The same goes for H&M with -46% in total sales while online sales increased by 17%. As of

companies are facing serious disruption in the supply of raw materials, critical components, 15 April 2020, 72% of H&M stores were closed. However, stores in China have started

and finished products. opening again since the easing off in disease transmission there.

• The peak of COVID-19 in China was in parallel with Chinese New Year, and this has • The potential impact for this sector is a short peak in consumer demand in certain

softened the impact as inventories had been built up because of the national holiday. categories once the situation starts to normalize. However, an economic recession looms

Demand for electronics, hygiene, and specific sports categories is high, and consumers are as consumer spending is expected to decrease in the medium term. Consumers will

shifting to online. Demand for luxury goods has fallen sharply. continue to shift to online sales which will require Consumer Products companies to revisit

their B2C strategies.

• In Sweden, retail sales in the fashion sector are in a free fall. Figures show that in March

shoe and clothes sales declined with 47% respectively 39% in comparison to last year. The • Another likely impact is a backlog of orders waiting to be cleared by manufacturers when

e-commerce market indicates declining figures for all consumer products. However, data capacity returns to normal levels, putting further pressure on supply chains. As a result

suggest that people consume to a larger degree online than previously. alternative sourcing options will need to be explored. Considering the impact of changing

commodity prices and other costs-to-serve, as well as ways to increase demand, companies

• COVID-19 has already started putting companies out of business. Fashion retailers Joy and

will be forced to revisit their pricing and promotion strategies.

MQ have gone bankrupt while the sport chain Intersport has applied for restructuring.

17

Sources: Svensk handel, Postnord and Svenska Dagbladet

Note: Index set to 100 at 1 January 2020.Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited (“DTTL”), its global network of member firms, and their related entities (collectively,

the “Deloitte organization”). DTTL (also referred to as “Deloitte Global”) and each of its member firms and related entities are legally separate and

independent entities, which cannot obligate or bind each other in respect of third parties. DTTL and each DTTL member firm and related entity is liable only

for its own acts and omissions, and not those of each other. DTTL does not provide services to clients. Please see www.deloitte.com/about to learn more.

Deloitte is a leading global provider of audit and assurance, consulting, financial advisory, risk advisory, tax and related services. Our global network of

member firms and related entities in more than 150 countries and territories (collectively, the “Deloitte organization”) serves four out of five Fortune Global

500® companies. Learn how Deloitte’s approximately 312,000 people make an impact that matters at www.deloitte.com.

This communication contains general information only, and none of Deloitte Touche Tohmatsu Limited (“DTTL”), its global network of member firms or their

related entities (collectively, the “Deloitte organization”) is, by means of this communication, rendering professional advice or services. Before making any

decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser.

No representations, warranties or undertakings (express or implied) are given as to the accuracy or completeness of the information in this communication,

and none of DTTL, its member firms, related entities, employees or agents shall be liable or responsible for any loss or damage whatsoever arising directly or

indirectly in connection with any person relying on this communication. DTTL and each of its member firms, and their related entities, are legally separate

and independent entities.

© 2020 Deloitte AB

18You can also read