CORPORATE PRESENTATION - JUNE 2021 - Shivalik Bank

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

CORPORATE PRESENTATION

JUNE 2021

CONTENTS

§ SHIVALIK SMALL FINANCE BANK OVERVIEW

§ SHIVALIK IN NUMBERS

§ OPERATIONAL OVERVIEW

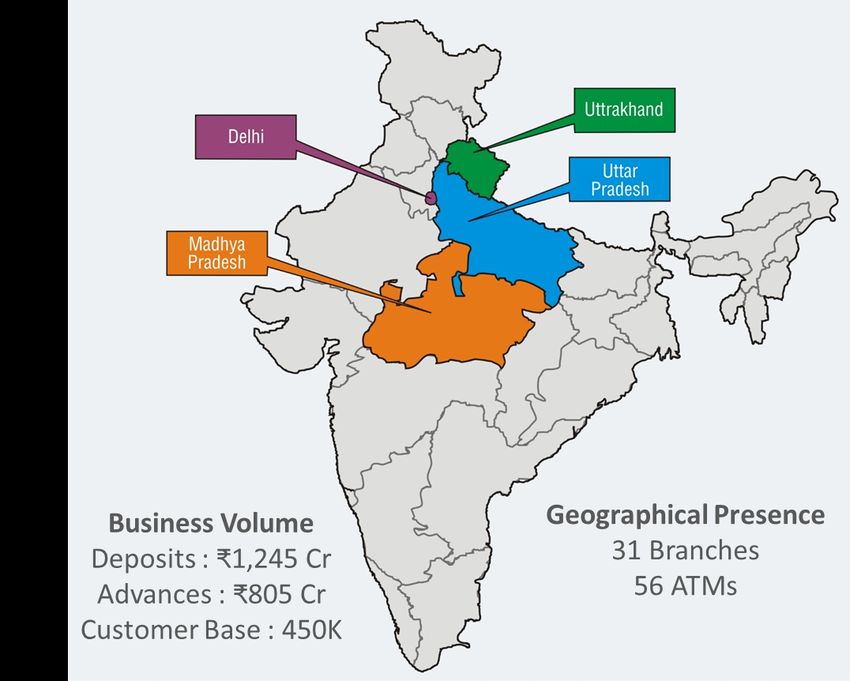

§ GEOGRAPHICAL PRESENCE

§ MANAGEMENT PROFILES

2

SHIVALIK SMALL FINANCE BANK

OVERVIEW

3

INTRODUCTION – A BANK OF MANY FIRSTS

§ Started in 1998, literally from a garage!

§ First UCB to receive a commercial

banking license as a Small Finance Bank

§ First bank to host CBS, Digital Suite and

Payments on Cloud in India

§ Pre-transition, it was the first and largest

multi-state UCB in Uttar Pradesh

Business volume figures are stated as on 31 March 2021

UCB – Urban Co-operative Bank

4OUR JOURNEY

1998 2010 2013 2017 2019 2020

Starts Acquires Centralises Makes Receives in-

Adopts FIS

operations in another UCB major application principle

Profile CBS

Saharanpur, – becomes a banking to RBI to approval to

on Cloud –

Uttar Multi State functions at become a become a

First in India

Pradesh UCB new office SFB SFB

Achieves full Completes Switches

Launches Commences

tech Commences

computeris- second Internet and digital

platform to operations

ation of its acquisition Mobile transformati

Infosys as a SFB

operations of a UCB Banking on project

Finacle

1999 2012 2015 2018 2019 2021

§ A 23 year journey to become India’s first UCB to transition to a Small Finance Bank!

5AN OVERVIEW

§ Started in 1998 by a visionary entrepreneur who believed banking services had to be

improved and made available to the underserved segment of the population

The Beginning § Charted a long journey as a UCB starting as a single district bank, further expanding to the

whole of Uttar Pradesh and then growing to a multi state bank by acquiring banks in

Madhya Pradesh

§ Tech focused from the beginning as the founders had a strong engineering mindset

§ Computerised all services bank in 1999 and first bank to host CBS on cloud in 2013!

Tech Focus

§ Invested in a large digital transformation in 2018 including switching over CBS and Digital

Banking Suite to Infosys Finacle on a cloud hosted model – A first in India

§ Registered office is in Delhi, India

Offices and

§ Head Office is in Noida and another administrative office is in Saharanpur

Employees

§ Employee Strength : ~500

6WHAT WE STAND FOR

Our Vision Our Purpose

§ Socially responsible impact lender

§ Digital first approach across products and service

To be a trusted financial services offerings

provider and model employer § Financial inclusion and increasing financial literacy

focusing on small and § Innovator in financial products and processes

underserved segments through

§ Aim to become a complete solution provider to our

the delivery of digitally focused, customers

affordable products and § Environment, Social and Governance (ESG) compliant

differentiated customer § Create value for all stakeholders - Society,

Employees, Customer, Organization and

experience.

Shareholders

7VOLUNTARY TRANSITION TO SFB – A PIONEERING JOURNEY

• On 27 September 2018, RBI released guidelines permitting the voluntary transition of Urban Co-operative Banks

(UCBs) into Small Finance Banks (SFBs).

• Submitted an application to the RBI in January 2019 making it the first bank to apply under the guidelines

• Received in-principle approval from the RBI to transition to a Small Finance Bank on 6 January 2020 – this is

testament to the strength of the business model and internal control systems.

• Received the license to commence banking business as a Small Finance Bank on 1 January 2021, well ahead of the

18 month timeline permitted by the RBI.

• Commenced business as a SFB, India’s newest private sector commercial bank on 26 April 2021

§ A pioneering journey of being the first UCB to become a Small Finance Bank in India

8SHIVALIK IN NUMBERS

9OUR DNA IS OF A SFB

Small Finance Banks were set up with the following objectives by the RBI :

Small & Priority Retail and Financial Technology Enabled

Sector Lending Inclusion Focus Banking Services

Shivalik was born to be a SFB

53% 65% 92% 31% 94.5% 80%

% Loans below Priority Sector Digital Savings Digital

Retail Deposits % CASA Ratio %

₹25 Lakhs Lending % Account Opening % Transactions %

43% : 0.5

90% 40% 65% 5.3%

57% million

% Secured Diversification : Business Financial Inclusion Digital IT Capex Spend as % of

Customer Base

Lending Book – Individual Loans Customers % Penetration1 % revenue2

1. Proportion of customers transacting on digital and assisted digital modes including internet, Mobile Banking and mATM/

handheld devices

2. Average of the last 5 years 10SECURED RETAIL LOAN BOOK

Avg.

2013-16 2016-17 2017-18 2018-19 2019-20 2020-21

Advances 481.1 559.5 611.6 715.2 718.6 804.9

(₹ Crores)

Secured Lending 94% 94% 93% 91% 92% 90%

(%)

Loans below ₹ NA 64.4% 59.3% 50.4% 53.5% 52.5%

25 Lacs (%)

Yield on 13.4% 13.0% 12.4% 12.2% 12.1% 11.8%

Advances (%)

§ Our focus has always been on small ticket lending and building a secured, well diversified loan book

§ Fully aligned with the SFB mandate of retail lending

11GRANULAR DEPOSIT BASE

Avg.

2013-16 2016-17 2017-18 2018-19 2019-20 2020-21

Deposits 661.2 917.0 953.4 1051.2 1139.8 1244.5

(₹ Crores)

CASA Ratio 25% 36% 33% 32% 28% 31%

(%)

Retail Deposits 77%1 86% 88% 91% 92% 92%

(%)

Cost of Funds 8.0% 7.0% 6.4% 6.1% 6.4% 6.1%

(%)

§ Maintained a low cost of funds through focus on building a granular, retail deposit base

§ Working like a SFB for many years focusing on financial inclusion

1

Average of 2014-15 and 2015-16 only 12DIGITAL & OPERATING EFFICIENCIES

Avg.

2013-16 2016-17 2017-18 2018-19 2019-20 2020-21

Net Interest 4.1% 4.0% 4.2% 4.1% 4.0% 4.3%

Margin (%)

Digital Savings NA 28.6% 59.5% 90.4% 84.1% 94.5%

Ac Opening (%)

IT Capex / 0.7% 1.2% 3.0% 3.6% 16.3% 1.3%

Revenue (%)

Credit – Deposit 67.6% 57.6% 60.7% 64.2% 59.9% 61.2%

Ratio (%)

§ High NIM for a diversified secured lender driven by low cost of funds

§ Large tech spends completed to be ready to scale as a SFB

13WELL DIVERSIFIED PORTFOLIO

Credit Portfolio Split Key Credit Portfolio Highlights

Microfinance, % Loans Secured by

10.4%

Cash Credit / ~ 90%

Overdraft, 14.6% Collateral (Remaining portfolio is MF)2

Gold Loans,

5.0%

Loan Average Ticket Size ₹ 3.8 Lakhs

against

Deposit,

7.2% Small Lending % > 50%

(Upto ₹25 Lakhs per borrower)

Retail 1

Loans, Business and Business : 43%

62.8% Individual Loans Split Individual : 57%

§ Well diversified portfolio with minimal concentration risk due to low average ticket size and

almost no unsecured exposure

1

Retail Loans refers to Term Loans includes loans to MSME & other retails businesses and individual

loans such as housing, asset purchase and agriculture. 14

2 The remainder of the portfolio is of Microfinance which is also backed by joint liability guarantees.STABLE ASSET QUALITY

Gross NPA (%) Net NPA (%)

3.9 2.4

1.9

2.8

2.3 1.4 1.5

2.1 1.2

1.6

2016-17 2017-18 2018-19 2019-20 2020-21 2016-17 2017-18 2018-19 2019-20 2020-21

§ Gross NPA in FY 20-21 includes ~1.6% of increment from pro-forma NPA being marked NPA at

31 March 2021 as per Hon’ble SC order

15PROFITABILITY

EBITDA (₹ Crores) Operating and Net Profit (₹ Crores)

17.8 17.6 Pre-provisioning Operating Profit

Net Profit after Tax

12.3

9.6 10.3

8.8

7.3

5.4 4.8

10.0 3.1

3.2 3.8 2.3 3.3

2016-17 2017-18 2018-19 2019-20 2020-21 2016-17 2017-18 2018-19 2019-20 2020-21

§ Major transformations completed from

§ Focussed on sustainable EBITDA growth

internal accruals

§ Profitable since inception, the bank has always focused on return to shareholders

§ Increased branch count by 50% and completed a technology transformation since 2017

16OPERATIONAL OVERVIEW

17BRANCH AND BUSINESS BANKING

Description Status for Shivalik

• Branches : 31

Banking Outlets which includes full service branches, on and offsite ATMs and other • ATMs : 57

banking centres • BC Centres : 4

Large Customer Base ~ 4.5 Lacs

Major retail banking deposit and loan products ü

CASA ratio (Low Cost Deposits) ~ 31%

Significant Business Size ~INR 2,050 Cr

Profitable and dividend paying track record Since Inception

§ Strong track record, exceptional CASA ratio and adequate business size poised to scale further

18PAYMENTS SYSTEMS

Description Status for

Shivalik

NEFT/RTGS ü

Debit Cards for use across ATMs in India ü

POS (Point of Sales) machines ü

E-Commerce Transactions ü

IMPS, Aadhar Enabled Payment System (AePS), Aadhar Bridge Payment System (ABPS) ü

NACH, Bill Payments and cheque clearing ü

UPI ü

§ The bank is active on almost all payment channels prevalent in India.

19CHANNEL BANKING

Description Status for Shivalik

Internet Banking ü

Mobile Banking ü

Instant Loan Origination on Digital Channels ü

Tablet Banking through micro ATMs (m-ATMs) ü

Distribution of insurance products ü

Banking centres and Village Level Entrepreneurs ü

Modern and interactive website ü

§ Multiple channels for customer convenience – a good mix of ‘brick’ and ‘click’ offerings.

20BUSINESS OPERATIONS & RISK MANAGEMENT

Description Status for Shivalik

Centralized teams for account opening, credit appraisal and disbursal ü

Dedicated internal audit, risk management and credit monitoring units ü

Custom designed Loan Origination Platform suited to small lending needs ü

Anti-Money Laundering Software for PMLA norms ü

CTS and centralized clearing activities ü

Policy development teams across verticals ü

Adequate insurance coverage incl. cyber risk ü

§ Strong risk management ethos and internal control systems are embedded in our work culture

21TECHNOLOGY PLATFORM

Description Status for Shivalik

Core Banking Solution (Powered by Infosys Finacle on Cloud) ü

Internet and Mobile Banking ü

Paperless Account Opening ü

Cash Recyclers at ATM locations ü

Payments Switch & Fraud Risk Management ü

Internal Business Process Automation such as Office 365, Audit software and others ü

§ Best in class technology platform shows the commitment to keep pace with the modern

advancements.

22SHIVALIK TECH PARTNERS

Core Banking Digital Banking API Gateway Switch and Cards

Micro ATMs UPI IMPS Reg Connect

§ Partnering with the best to deliver a superlative experience!

All logos are the registered trademarks of the respective companies

23OTHER FACTORS

Description Status for Shivalik

Appropriate channels for customer service and grievance redressal ü

Alignment in HR and Learning & Development Teams ü

Strong Corporate Governance Framework and experienced management team ü

Significant supporting infrastructure including state of the art head office(s) ü

Payments Switch & Fraud Risk Management ü

Significant partnerships and tie ups with a number of supporting service providers such as

insurance, payments switch, bill payments, POS installation and others ü

§ Significant investment made to get the bank ready to scale in the future

24PRODUCTS & SERVICES

Savings Fixed Deposits Flexi Recurring Deposits

Deposits Current Door-to-Door Deposit

Home Loans Personal And Gold Loans Car/Auto Loans

Consumption Loans

Two-Wheeler Loans Loans for Working Capital Reverse Mortgage Loans Roof Top Solar Loans

Loans Loans to Professionals Loans for Micro/SSI Units Retail Traders Loans Commercial Building

And Self Employed Loans

Commercial Vehicle Self Help Groups (SHG) Loans Against Warehouse Shivalik Green Card

Loans And Mini SHG Receipts (Kisan Credit Card)

Net Banking Mobile Banking Debit Card ATM Banking

Digital Recyclers SMS Banking AEPS (Aadhaar Enabled Fund Transfer (UPI

Services Payment System) /RTGS/NEFT/IMPS/NACH)

e-commerce POS Machine

Add-on Insurance Remittances Lockers

Services Business Correspondents Forex PAN Card services

25GEOGRAPHICAL PRESENCE

26AREA OF OPERATIONS

27PRESENCE IN UTTAR PRADESH

28PRESENCE IN MADHYA PRADESH

29MANAGEMENT PROFILE

30MANAGEMENT TEAM

Education and

B.Tech. (Electrical) Hons. From NIT, Kurukshetra

Qualification

Total

23+ Years

Experience

Suveer Kumar Gupta • Co-founded the Bank in 1998 to enhance banking services in the region.

Managing Director & • Under his leadership, the Bank has achieved a number of firsts including

Chief Executive Officer becoming the first and largest multi-state UCB in Uttar Pradesh and being

the first bank in the country to be transitioning to a Small Finance Bank.

Overall • Through his deep focus on technology, he has led the bank towards

Experience automation and tech driven services from the outset. His emphasis on

customer matters has helped Shivalik remain customer centric over the

years.

• He joined the bank after having worked with Tata Consultancy Services

(TCS).

31MANAGEMENT TEAM

Education and He holds a Bachelors in Arts and Law and holds a Certificate in Risk

Qualification Management in Financial Services from CISI, UK

Total

39+ Years

Experience

Navleen Kundra • Before joining the bank, he was working in Oriental Bank of Commerce,

where he retired as General Manger – Risk Management.

Chief Risk Officer

• In his previous role he was leading a team, chartering policies and models

Overall and was involved in marquee projects.

Experience

• Prior to heading the risk department, he headed various branches

including Rural, Urban and Metropolitan (Delhi and Mumbai), large

corporate branch in Mumbai, post which he shouldered responsibilities as

the Regional Head of Jaipur Region & later New Delhi Region.

32MANAGEMENT TEAM

He is

A Chartered Accountant

management from Institute

professional of Chartered

from MDI, NIPM, Accountants in England

Mr. Ghoshal also and

has

Education and Wales (ICAEW)from

certifications and Bachelors in Electronics

DDI and LaMarsh USA and Communications

in Change Engineering

& Leadership. from

He is also a

Qualification University coach

Certified of Leeds, United

from CPIKingdom

Global with more than 180 leadership coaching

hours. He is certified in People Assessments with SHL & Hewitt.

Total

28+ Years

Experience

Suvendu Ghoshal

Chief Human Resource • With more than 28 years of experience in the corporate sector, Mr.

Officer Ghoshal has held multiple senior roles in his career. He has been VP-HR

with Hewitt Associates, CHRO with JCT Ltd, AVP HR with Xansa, Corporate

People Engagement Head with Airtel. He has led many interventions on

Overall Organisation transformation, design restructuring and change

Experience management. He has also worked very deeply in the areas of culture

building, strategy, leadership development and talent management.

• He is author of `21st century Professionals Handbook’ and Co-edited`

Perform of Perish’- the People Dimension with IIM-A Professor.

33MANAGEMENT TEAM

Education and M.Sc. (Finance) From University of Strathclyde Business School, Scotland,

Qualification United Kingdom and B.Com. (Hons.) From University of Delhi

Total

20+ Years

Experience

• Gaurav Mittal has been working with the bank since 2013. He is

Gaurav Mittal responsible for Strategy, Operations, Business Development, HR and

Marketing functions.

Chief Operating Officer

Chief Strategy Officer • He has worked in Worlds Windows Group, as a DGM Strategy. As a part of

the strategy team, working with the Group Chairman, his role was to

Overall identify new business opportunities, M&A targets and streamline existing

Experience business operations. He has also worked in SKIL Infrastructure where he

was responsible for setting up and launching Strathclyde Business School

(SBS) India campus at Greater NOIDA. He was Research Manager in CEB

(now Gartner) and managed a team of research associates working on

research reports in Retail, Corporate, and Private Banking for senior

executives at leading financial institutions in US, Europe & Asia.

34MANAGEMENT TEAM

Chartered Accountant

He is Chartered from

Accountant theInstitute

from InstituteofofChartered

Chartered Accountants

Accountants in England

in England and

Education and

and

WalesWales

(ICAEW)(ICAEW) and in

and Bachelors Bachelors

ElectronicsinandElectronics and Communications

Communications Engineering from

Qualification

University of from

Engineering Leeds,University

United Kingdom

of Leeds, United Kingdom

Total

14+ Years

Experience

Harsh Mittal • Harsh Mittal has been working with the bank since April 2016. He holds

responsibilities for Finance, Technology, Compliance and Credit functions.

Chief Financial Officer

• Before joining the bank, he was working in Swiss Reinsurance Company

Overall Ltd, London as a Head of Group Performance Management in their Group

Experience Finance team. He was Head of Transaction Analysis in Swiss Re Life Capital

(a subsidiary of Swiss Re Group), London where his main responsibility was

to support all M&A and valuation activity. He was Assistant Manager in

KPMG LLP UK where he was involved in the audit and transaction services

practice as a part of the financial services segment.

35DISCLAIMER

This presentation has been prepared by Shivalik Small Finance Bank Limited solely for information purposes, without regard to any specific objectives, financial

situations or informational needs of any particular person. All information contained has been prepared solely by the Bank. No information contained herein

has been independently verified by anyone else. This presentation may not be copied, distributed, redistributed or disseminated, directly or indirectly, in any

manner. This presentation does not constitute an offer or invitation, directly or indirectly, to purchase or subscribe for any securities of the Bank by any person

in any jurisdiction. No part of it should form the basis of or be relied upon in connection with any investment decision or any contract or commitment to

purchase or subscribe for any securities. Any person placing reliance on the information contained in this presentation or any other communication by the

Bank does so at his or her own risk and the Bank shall not be liable for any loss or damage caused pursuant to any act or omission based on or in reliance upon

the information contained herein. No representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy,

completeness or correctness of the information or opinions contained in this presentation. Such information and opinions are in all events not current after the

date of this presentation. Further, past performance is not necessarily indicative of future results. This presentation is not a complete description of the Bank.

This presentation may contain statements that constitute forward-looking statements. All forward looking statements are subject to risks, uncertainties and

assumptions that could cause actual results to differ materially from those contemplated by the relevant forward-looking statement. Important factors that

could cause actual results to differ materially include, among others, future changes or developments in the Bank’s business, its competitive environment and

political, economic, legal and social conditions. Given these risks, uncertainties and other factors, viewers of this presentation are cautioned not to place undue

reliance on these forward-looking statements. The Bank disclaims any obligation to update these forward-looking statements to reflect future events or

developments. Except as otherwise noted, all of the information contained herein is indicative and is based on management information, current plans and

estimates in the form as it has been disclosed in this presentation. Any opinion, estimate or projection herein constitutes a judgment as of the date of this

presentation and there can be no assurance that future results or events will be consistent with any such opinion, estimate or projection. The Bank may alter,

modify or otherwise change in any manner the content of this presentation, without obligation to notify any person of such change or changes. The accuracy of

this presentation is not guaranteed, it may be incomplete or condensed and it may not contain all material information concerning the Bank. This presentation

is not intended to be an offer document or a prospectus under the Companies Act, 2013 and Rules made thereafter , as amended, the Securities and Exchange

Board of India (Issue of Capital and Disclosure Requirements)Regulations, 2009, as amended or any other applicable law. Figures for the previous period / year

have been regrouped wherever necessary to conform to the current period’s / year’s presentation. Total in some columns / rows may not agree due to

rounding off. Note: All financial numbers in the presentation are from Audited Financials or Limited Reviewed financials or based on Management estimates.

3637

You can also read