Corporate Presentation - Vincom Retail

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Corporate Presentation

May 2021

Disclaimer

IMPORTANT: The information contained herein is preliminary and subject to change without notice, its accuracy is not guaranteed, has not been independently verified and may not

contain all material information concerning Vincom Retail Joint Stock Company (the “Company”) and its subsidiaries (the “Group”). You should not rely upon it or use it to form the

basis for any investment decision or commitment whatsoever.

None of the Company, its shareholders, or any of their respective affiliates, directors, officers, employees, agents, advisers or any other person makes any representation or warranty

(express or implied) or accepts any responsibility or liability for the accuracy or completeness of this presentation or any or all of the information in this presentation or otherwise made

available. It is not the intention to provide, and you may not rely on these materials as providing, a complete or comprehensive analysis of the financial or trading position or prospects

of the Group. No part of this presentation shall form the basis of or be relied upon in connection with any contract or commitment whatsoever. Further, nothing in this presentation

should be construed as constituting legal, business, tax or financial advice. You should conduct such independent investigations and analysis of the Group as you deem necessary or

appropriate in order to make an independent determination of the suitability, merits and consequences of investment in the Company.

This presentation contains “forward-looking statements”. These forward-looking statements involve known and unknown risks and uncertainties, many of which are beyond the

Company’s control and all of which are based on management’s current beliefs and expectations about future events. Forward-looking statements are sometimes identified by the use

of forward-looking terminology such as “believe”, “expects”, “may”, “will”, “could”, “should”, “shall”, “risk”, “intends”, “estimates”, “aims”, “targets”, “plans”, “predicts”, “continues”,

“assumes”, “positioned” or “anticipates” or the negative thereof, other variations thereon or comparable terminology. These forward-looking statements include all matters that are not

historical facts. Forward-looking statements are not guarantees of future performance. These forward-looking statements speak only as at the date of this presentation, and none of

the company, its shareholders, or any of their respective affiliates, directors, officers, employees, agents, advisers or any other person undertakes to update or revise any forward-

looking statements as a result of new information or to reflect future events or circumstances.

1

Executive Summary

Vincom Retail (“VRE”) is the largest and fastest growing retail developer, owner

and operator in Vietnam

Key investment highlights are as follows:

Vietnam Economy

Remains Resilient

Amidst Covid-19

Outbreak

Modern Retail Set to

Take Off

Largest and Most

Dominant Retail Platform

Proven Track Record of

Ability to Leverage the

Highly Scalable Platform Institutional Level

Best-in-Country

with Strong Operating Corporate Governance

Vingroup Ecosystem

Performance

Market leader in terms of the shopping mall GFA in Vietnam’s major cities…

…the direct proxy for consumer demand

The Dominant and Fastest Growing Retail Platform in Vietnam

2 2

Vingroup & Vincom Retail: Market Leaders In Vietnam

Largest Listed Company in Vietnam

Vincom Retail

A Key Subsidiary of

Largest Real Estate Developer in Vietnam

Vingroup JSC

c. 168 mm sqm of Landbank(1)

Hanoi 80

(8)

Operational

Ecosystem of Complementary Businesses Vincom Retail Malls

Largest Retail

Developer, Owner

and Operator in (9)

Vietnam Ho Chi Minh City 1.7 mn

Retail GFA

Residential Hospitality Healthcare Education Automobile Smartphone ~29% NLA leased to internal (sqm)

and affiliated tenants(2)

Premium Leading Leading Leading First Top 5

and large hospitality hospital private Vietnam- smartphone Vinhomes:

scale real operator in operator school ese smart producer in Vietnam’s largest real estate Unique Multi format Model

estate Vietnam operator and green Vietnam

developer About 750 vehicle

developer

Approx. beds under More than manufactu- 2.8 million

Largest in 17,500 operation 32,000 rer smart- VinFast:

Vietnam rooms students phones sold Flagship automobile and e-

7 full- Vincom Center Vincom Mega Mall

owned & registered 89,900 cars since motorcycle showrooms

No. of Malls: 7

1,592 units managed service at 35 and electric launch(7)

No. of Malls: 4

presold(3) general Retail GFA: 280,026 sqm Retail GFA: 444,098 sqm

facilities(5) motor- Vinschool:

(Contracted hospitals (17% total) (27% total)

cycles sold Leading private school operator

sales of and 5 since

VND 6 clinics launch(6)

trillion(4)) VinMart:

Vietnam’s largest modern grocery

retail chain by presence Vincom Plaza Vincom+

No. of Malls: 54 No. of Malls: 15

Retail GFA: 857,517 sqm Retail GFA: 71,936 sqm

VinID: ~11 mn Members, Largest Loyalty Program in Vietnam(5) (52% total) (4% total)

Vincom Retail is the Ultimate Consumer Play for Vietnam

Note:

(1) Refers to Vinhomes’ landbank (2) MSN-Vincommerce is an affiliated tenant (3) For 1QFY2021, estimated pre-sale under SPAs and pre-sale bookings under deposits, including BCC projects deposits (4) Include retail value only

(5) (6) (7) (8) (9) As of 31 March 2021

3

Emergence Of Vincom Retail As A Clear Market Leader

Establishing Platform Accelerating Growth With

Early Years & Formation For Growth Dominant Market Share

2004 – 2013 2014 2015 2016 2017 2018 2019 – 2020

Royal City launched First Vincom Vincom Mega 10 new Vincom Listed on HOSE in Launched 20 Launched 13 (2019)

shopping mall Mall Thao Dien shopping malls November shopping malls, and 1 (2020)

Times City launched outside Hanoi & launched Introduction H&M opened 2 stores including Landmark shopping malls and

US$200 million HCMC of Vincom+ format 81 expanded our

in Hanoi and Ho Chi

investment − VCP Ha Long international tenant

Minh City

“Best Retail US$100mm portfolio across key

Zara opened first store malls (Uniqlo,

Developer in follow-on

in Hanoi

Vietnam” by investment First Zara flagship Decathlon, CGV,

Euromoney in 2012 store in Vietnam Key tenants added: Signed leasing H&M, Mango, Muji,

10 new Vincom

First Robins opened at Vincom Inditex brands contracts for Pizza 4P’s, Haidilao)

shopping malls &

department store in Center Dong Khoi in (Stradivarius, Massimo

Acquisition of 5 approximately Pioneer in

Vietnam opened in HCMC Dutti, Pull & Bear), 191,000 sqm NLA

Maximark malls experiential

Royal City in April H&M and Old Navy

c.US$390mm Vingroup and over 1,200 retail-tainment in

2014 follow on investment advertising contracts Vietnam

Retail GFA (‘000 sqm) 7980

7,017

Leasing Revenue (VND bn)

2014 – 2020 CAGR:

6980

(1)

6,008

Leasing revenue: 20.1%

5,506

GFA: 22.0% 5980

1st Retail Mall 1st Integrated

in Vietnam Project in 4,455 4980

Vietnam Investment by 3,805

Warburg

3980

Pincus

IEO and

2,427 listed on 2980

1,927 HOSE

1,598 1,654

1,448

1980

Vincom Center Vincom Center

Ba Trieu Dong Khoi 1,023 1,173

851

467 499 980

42 93

-20

2004 2010 2013 2014 2015 2016 2017 2018 2019 2020

No. of

malls 1 2 5 6 23 31 46 66 79 80

17 Years of Operating Experience Achieving ~1.7 mm sqm of Retail GFA (~35x Increase Since 2004)

Note: As of 31 March 2021

Leasing revenue is based on Vietnam Accounting Standard (VAS) Audited Consolidated Financial Statements for respective years

4 (1) Leasing revenue took into account the impact of Vincom Retail’s supporting package to tenants impacted by Covid-19 in 2020, totaling VND 865bn 4

Retail Consolidates Around The Dominant Local Landlord

dominant local landlord

Global examples clearly demonstrate retail consolidation around the

Vincom Retail

Significant parallels seen between VRE and regional retail leaders

Vietnam’s largest retail developer, owner and

operator

Vietnam's

GFA (mm sqm)

current position at an early, higher growth stage of the retail

1.7

1.0 cycle translates to a stronger growth profile and a more dominant market

share

2016 2020

SM Prime

Central Pattana

Vietnam Philippines’ largest retail real estate developer

Thailand’s largest shopping mall developer arm of

GFA (mm sqm)(3) Market Share by GFA(2)

Central Group

50%

GFA (mm sqm)(1) Market Share by GFA(1) 9.8

Thailand Philippines 28%

20% 2.2

15%

4.7 Singapore

0.9 2007 2019 2007 2019

Total Market Size (GFA sqm)(2)

2013 2020 2013 2020

7.8mm 10.7mm

Total Market Size (GFA sqm)(1) Indonesia

5.6mm 18.9mm

PT. Pakuwon Jati

CapitaLand Integrated Commercial Trust

Indonesia’s largest mall owner and operator

Largest proxy for Singapore’s commercial real estate

NLA (mm sq. ft) Market Share by NLA(3) NLA (mm sqm) Market Share by NLA(4)

15.4%

10.4 0.7 20.4%

5.6% 0.3 13.3%

3.3

2011 2020 2011 2020

Total Market Size (NLA sq. ft)(3) 2012 2020 2012 2020

Total Market Size (NLA sqm)(4)

58.9mm 67.4mm ~2.5mm ~3.2mm(5)

Source: Company filings, Colliers, Statista, Urban Redevelopment Authority, Savills, Urbis.

1. Based on Central Pattana’s retail NLA in Bangkok Metropolitan Area and total shopping mall NLA in Bangkok Metropolitan Area.

2. Based on SM Prime’s retail GFA in Metro Manila and total retail GFA in Metro Manila.

3. Based on retail floor space supply in Singapore (2009-2024), extracted from Capitaland Mall Trust (CMT) Annual Report 2019

4. Based on PT. Pakuwon Jati’s retail NLA as of Dec-2012 and 3Q 2020 vs. shopping mall NLA of Jakarta

5 5

Key Investment Highlights

Key Investment Highlights

Vietnam’s Economy Remains Resilient Amidst Covid-19 Outbreak

1 ‒ Vietnam On A Rebound – The Brightest Spot In SEA’s Economies

‒ Clearer Signs Of A Speedy Recovery; Ready For A “New Normal”

2 Huge Potential for Further Expansion in Vietnam’s Retail Space

Modern Retail Set to Take Off

Only Retail Platform With Nationwide Access

Metro and Bus Infrastructure To Accelerate Retail Mall Footfall

Multi Format Model Covers a Larger Market Opportunity

3

Solidified Position as Dominant Retail Platform in Vietnam

4 Ability to Leverage the Best-in-Country Vingroup Ecosystem

5 Institutional Level Corporate Governance

7

Vietnam On A Rebound – The Bright Spot In South East Asia’s Economies

Vietnam continues to maintain the highest GDP growth among Southeast Asia countries for the next three years

Estimated Real GDP growth (%)

(9.5) 7.1 7.0

6.5 6.3 (5.8) 6.5

(5.0) 5.0 5.0 5.2

4.6 4.8 (1.1)

4.2 3.8

(7.2)

2.6

Philippines Thailand Singapore Malaysia Indonesia Vietnam

2021 2022 2023

Vietnam GDP continues strong growth in 2021 due to domestic consumption rebound, strong FDI inflow due to supply chain shift and accelerated public investment

Forecasted domestic consumption grows Vietnam to become the new center of Highest level of public investment in terms

1 at top level of Southeast Asia

2 global supply chain

3 of GDP % to boost domestic economy

Domestic consumption growth (%) Constant FDI disbursement despite ongoing Covid pandemic Public investment as % of GDP (2021 Target)

(USD billion)

10.6 6.8

20.4 20.0

8.8 19.1

8.2 17.5 5.7

15.8

7.0 14.5

4.0 4.1

3.6

4.6 4.4

2.4

3.0

3.8 4.1

0.5 0.5

2015 2016 2017 2018 2019 2020 Q1/20 Q1/21

-2.1 Global corporations continue to relocate and expand factories

-3.6 in Vietnam

-4.7

2020 2021F Free Trade Agreements such as CPTPP, EVFTA and RCEP will Public investment is expected to keep increasing during the

boost Vietnam’s international trades first half of 2021, with suitable monetary policy

Source: GDP consensus from Bloomberg, GSO, CEIC, IMF and BMI

8

Promising Retail Outlook, Ready For A “New Normal"

Mobility to retail malls and entertainment activities in major

cities has returned to pre – Covid level Vietnam posts solid retail sales throughout the pandemic

Mobility to retail malls and entertainment activities has rebounded Nominal Retail sales change YoY (%)

12.0

Vietnam Hanoi HCMC 10.0

7.0

5.7 6.5 4.0 3.7

2.0 1.4 1.4 1.8

-1% 0% 1.5

-0.14

-2.9

-8.4 -10.0

-9%

-15.7

-13% -13% -24.4

-16%

Dec-20 Mar-21

2020 2021F

Rental outlook in Vietnam remains positive compared to regional countries

% change in rental rate forecast

Shanghai Guangzhou Beijing Taiwan Singapore Tokyo Hong Kong Brisbane Sydney Perth Melbourne Auckland HCMC Hanoi

2020 2021F 2019 - 2021 Cumulative

Source: Google Mobility Index, CBRE Research, eMarketer

92 Huge Potential For Further Expansion In Vietnam’s Retail Space

Low and fast growing disposable income per capita compared to neighboring countries, coupled with low

mall NLA, presents an opportunity to enlarge Vietnam’s retail mall space to close the regional gap.

Modern Retail is still at a Nascent Stage… …With the Growing Middle Class Set to Drive

Next Wave of Consumption

Vietnam has a Low Mall NLA compared to Thailand and Philippines(1) Vietnam’s Disposable Income per Capita is similar to Philippines in

2004 and Thailand in 1990, implying huge growth potential (1)

NLA (mm sqm) Disposable income per capita (US$)

7.9

7.3 2,796

2,554

1,808

3.6x 950 1,018

3.3x Vietnam

2.9x

2.2

2017 2018 2019 2023 2024

Hanoi/ HCMC Bangkok Metro Manila 3,818

3,547

2,824

Strong supply which validates the market’s potential, backed by

stable rental rate(2)

Philippines 930

Rental rate (USD/sqm/month) Future Supply (sqm NLA)

150.0 Hanoi 156

120.0 73 29

2004 2019 2023 2024

90.0

60.0 1,054 1,054 1,127 1,209

30.0 6,902 7,246

- 6,221

1Q20 2Q20 3Q20 4Q20 1Q21 2020 2021F 2022F 2023F

HCMC

150.0

70

120.0 114

57 Thailand 999

90.0

60.0 1,106 1,220

1,049 1,049

30.0

1990 2019 2023 2024

-

1Q20 2Q20 3Q20 4Q20 1Q21 2020 2021F 2022F 2023F

Rent rate (CBD) Rent rate (Non CBD) Current Future

Source: EIU, Colliers, CBRE Market Report in Hanoi and HCMC in 2020 and 1Q2021

10 Note: (1) Includes NLA pipeline 2020-2021 (2) As of 31 March 2021 102 Modern Retail Set to Take Off

Vietnam is Starved for Modern Retail Format E-Commerce More Catalyst Than Threat

Significantly Underpenetrated Modern Non-Discretionary Retail Remains E-Commerce Penetration(2)

2020/21(1) NLA per capita (sqm) (%) 2019A 2024E

1.8 40%

1.4

1.1

28%

0.5 0.5 0.5 0.5

21%

0.1 0.1 Low Penetration

15% vs Peers

13%

HCMC Hanoi Beijing Jakarta Shanghai Manila Singapore Bangkok Kuala 11% 11% 10%

9%

Lumpur

4% 5% 4%

Modern Retail Format an Attractive Solution in Vietnam 2% 3%

Attractiveness of Modern

Attractiveness of Modern China Indonesia Singapore Philippines Malaysia Thailand Vietnam

Retail to Consumers Retail to Tenants

Vincom Retail Further Consolidates Leadership

Limited alternatives for Significantly higher footfall and sales Position

entertainment and social activities psm achieved compared to

unorganized retail Malls: A Key Providing the Digital

One stop platform for discretionary + Activity Hub Infrastructure transformation

non-discretionary consumption Provides quality control with

guaranteed infrastructure and logistics

that helps to build brand equity Leading the service quality and customer experience

Stand-alone Department Store Formats have Lost Out Destination for and a trustworthy partner of major international brands to be

present in Vietnam for the first time

Lotte Vietnam on losing streak Progressively applying digital transformation to enhance customers’

Parkson Vietnam shutters store experience via improved service quality

since operations began

…However, during its ten years of

operation in Vietnam, Lotte Mart has

…Parkson Vietnam has closed another

of its stores as it continues to struggle Close and flexible connection between retail malls and e-commerce to support

shoppers and tenants via a network of credible e-commerce partners

never closed a year with profit… to make its business profitable…

Utilize the readily available customer base from VinID

Vincom Retail’s Disruption Has Already Leapfrogged the “Department Store” Phase

Source: EIU, Euromonitor, Vietnam Investment Review, Inside Retail Asia, CBRE Vietnam

(1) Includes NLA pipeline 2020-2021 (2) % E-commerce penetration represented by internet retailing over retailing.

112 Only Retail Platform With Nationwide Access

Portfolio Leasing Creates Significant Bargaining Power… … and Ability to Attract Best-in-Class Tenant Portfolio, with

more than 1,000 Unique Tenants(1)

HANOI HAI • 80 malls across 43

PHONG

cities and

provinces(1)

Fashion & Beauty

DA

NANG

• 4 retail formats for

specific areas

DONG • Proven and

NAI

scalable retail

CAN HCMC

THO development

platform

Vietnam

First stores in

Entertainment

Vietnam for Zara,

F&B and

H&M

First stores in

Hanoi for Uniqlo

First store in retail

(1)

malls of Decathlon

Anchor

VRE’s dominant position and nationwide scale makes it Vietnam’s “Go-to” platform

for international and established local brands

Source: Company information as of 31 March 2021

(1) Non-controlling interest in a subsidiary of Masan Group which owns MasanConsumerHoldings, the largest manufacturer of consumer products by revenue, and VinCommerce, the largest consumer retail network in terms of number of grocery retail stores

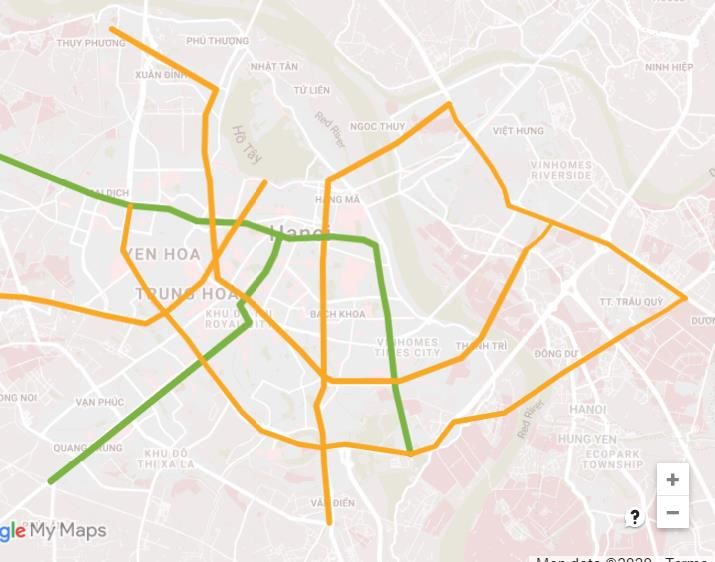

12 122 Metro And Bus Infrastructure To Accelerate Retail Mall Footfall

Most of VRE malls are covered by the upcoming metro lines in Ho Chi Minh City and Hanoi, and major VRE megamalls such as

VMM Ocean Park, Smart City and Grand Park have extra cover of VinBus routes – significant boost in connectivity and footfall

expected

Metro Lines Under Construction Planned Lines Bus routes

Ho Chi Minh City Hanoi

District 9

1 4

VINCOM PLAZA Go Vap District Tay Ho VINCOM CENTER

SAIGON RES VINCOM CENTER PHAM NGOC THACH

District NGUYEN CHI THANH

4

VINCOM MEGA MALL

1

VINCOM MEGA MALL

Ho Chi Minh THAO DIEN GRAND PARK

City Airport 5

VINCOM CENTER

TRAN DUY HUNG

3 1 2 3 4

CBD

1

Long Bien

5 District 1 VINCOM CENTER

3 Distirct Trau Quy

BA TRIEU

2 District 2 VINCOM MEGA MALL

SMART CITY 8

CBD VINCOM MEGA MALL

VINCOM MEGA MALL OCEAN PARK

VINCOM PLAZA TIMES CITY

3/2 1 2 3 4 5

VINCOM CENTER Ha Dong

DONG KHOI District VINCOM MEGA MALL 6 7 8 9 10

ROYAL CITY

2 Hung Yen

District 10 Province

Hoang Mai

Van Dien District

Tan Phu District

Preliminary VinBus routes as of 31 Dec 2020 (*)

1 Grand Park - Emart 2 Grand Park – Tan Son Nhat airport 1 Long Bien – Tran Phu – Smart City 2 Long Bien – Cau Giay – Smart City 3 Giap Bat – Smart City

3 Grand Park – Sai Gon bus station 4 Grand Park- Mien Dong bus station 4 Ho Tay water park – Smart City 5 VCP Long Bien – Smart City

5 Mien Dong bus station – National University NUA 6 Hao Nam – Ocean Park 7 My Dinh – Ocean Park 8 Ham Nghi – Ocean Park

9 Interconnected Complex – Ocean Park 10 Noi Bai – Ocean Park

Vingroup’s mixed use and VRE’s mall models are suited to tap

With urban metro lines opening for the first time in Ho Chi Minh

City and Hanoi and extra coverage of VinBus routes, the shift on this trend, given their targeted positioning and proximity to

from street retail to organized retail (malls) will accelerate the stations

Note: (*) Business plan which is subject to change 133 Multi Format Model Covers A Larger Market Opportunity

Annual Income

Distribution Holistic Segment Coverage Across Formats Competitors

(% of population

in Vietnam)(1) Vincom Center Vincom Mega Mall Vincom Plaza Vincom+

Target Segment:

Affluent Target Segment:

City Center/

(6%) CBD consumers Integrated Lotte

Middle & upper development Target

middle income catchment area AEON

Segment:

Targets families Target

Upper middle

Middle across all Segment:

income

Income income segments Middle

Focus on income /

(24%) shopping – Upper middle

experience based Target Segment: income

shopping to Heart of provincial

enhance customer town plus urban

experience non-CBD

Emerging

consumers of

(32%) key cities

Family & BIG C GO

activity hub Target

Middle income Segment:

Mass to

Aspiring middle income

(17%)

Target Segment:

Regional &

non-CBD Vincom Retail has access

catchment areas to addressable market

Mass Mass to segment of over US$176bn

(21%) middle income

of retail revenue

Source: BCG population and wealth models

(1) MAC (Middle income and affluent customers)

14 143 Solidified Position As Dominant Retail Platform In Vietnam

Distinguished retail formats and focused on wide range of lifestyle oriented consumers

Prime Urban and High Growth Areas in Key Cities Unique Multi – Format Retail Model

(Segmentation by GFA)

43 80 ~1.7mm Vincom Center

Location: City-center, CBD

Vincom Mega Mall

Location: In integrated,

Cities/ Operational Retail GFA Retail GFA: 40,000 – mixed-use projects

60,000 sqm Retail GFA: 60,000 –

Provinces Malls (sqm) No. of Malls: 7 150,000+ sqm

Total GFA: 280,026 sqm No. of Malls: 4

Total GFA: 444,098 sqm

Key Cities

North Vietnam (ex. Hanoi)

19 Vincom Malls

16.9%

16 Vincom Plazas 4.4% 26.9%

3 Vincom+

Hanoi

11 Vincom Malls

5 Vincom Centers

3 Vincom Mega Malls Central Vietnam 51.9%

20 Vincom Malls

3 Vincom Plazas

13 Vincom Plazas

7 Vincom+

Vincom+ Vincom Plaza

Ho Chi Minh City Location: Medium-density, Location: High-density,

13 Vincom Malls non-CBD CDB of cities

2 Vincom Center South Vietnam (ex. HCMC) Retail GFA: 3,000 – 5,000 ex. Hanoi and HCMC

sqm Retail GFA: 10,000 –

1 Vincom Mega Mall 17 Vincom Malls

No. of Malls: 15 40,000 sqm

7 Vincom Plazas 15 Vincom Plazas Total GFA: 71,936 sqm No. of Malls: 54

2 Vincom+ Total GFA: 857,517 sqm

3 Vincom+

Proven and scalable retail

4 retail mall formats

development platform

Note: As at 31 March 2021

154 Ability To Leverage The Best-in-Country Vingroup Ecosystem

c.168mm Access to Landbank from

29% Market Leading Retail Brands Form

NLA leased to

sqm of Vietnam’s Biggest Developer internal and Immediate Tenant Foundations

Landbank(1)

affiliated tenants(2)

Vinhomes’s Landbank Breakdown

c.30 years

worth for mn sqm

development Accelerates concept

to completion

155

pipeline for

Vinhomes Drives consumer

footfall (3)

Unparalleled

land sourcing 13

expertise

Launched Pipeline projects

Up to Largest Loyalty Programme in

Integrated Developments Provide 11m Vietnam Reinforces

100,000 Mega Malls with Natural Catchment Members(2) Captive Spending

Residents(2)

Times City

(opened: 4Q2013)

Ocean Park

(opened 12.2020) Single card,

nationwide access

Guaranteed

Footfall for

Malls Benefits lock in

repeat spending

Note:

1. Refers to Vinhomes’ landbank

2. As of 31 March 2021

3. Non-controlling interest in a subsidiary of Masan Group which owns MasanConsumerHoldings, the largest manufacturer of consumer products by revenue, and VinCommerce,

16 the largest consumer retail network in terms of number of grocery retail stores

165 Institutional Level Corporate Governance

Conflict Area Description Control

• All transactions must be entered into on commercially reasonable

basis as a statutory requirement.

• Vingroup will continue to be VRE’s majority

Decision Making • Significant related party transactions must be approved by the Board

shareholder following the Offering

of Directors or the general meeting of shareholders

• Interested parties must abstain from voting

• Non-compete from Vingroup on retail; VRE has a clear Right of First

• Both Vingroup and VRE are in the business of property

Competition Refusal (“ROFR”) for all stand-alone retail projects, retail

development

components and select mixed-use projects with well-defined criteria

• The ROFR above gives VRE economies of scale in land sourcing,

and delaying early-stage development costs

Land Bank Access • Vingroup holds much larger land bank than VRE • VRE has ROFR on land that can be used for retail, at cost

• VRE has an independent land sourcing team and primarily focuses

on different types of projects than Vingroup

• Allows VRE to expand faster with the key anchor tenants in place in

advance of commencing construction

Related Party Tenants • VRE has related party-tenants (Vingroup entities)

• Leases are negotiated on an arms’ length commercial terms

• Governed by related party rules under “Decision Making”

• Fees are calculated based on comparable third-party service

• VRE has contracts with Vingroup entities such as providers and Vingroup fees are allocated based on number of man

Vinpearl and Vinmec for non-core services such as hours and assets under management

Management Services

lodging rental and periodic health check for

Contracts • Helps VRE to manage expansion with minimum overhead as it can

employees, and Vingroup for headquarters services

share resources and costs with the rest of Vingroup

such as marketing, treasury and corporate HR

17 • Governed by related party rules

171Q2021 Key Highlights

Financial Performance – 1Q2021

Revenue from leasing continued its recovery momentum from the 3rd quarter of 2020

Total revenue Leasing revenue

VND billion VND billion

% of previous year level % of previous year level

73.8% 82.2% 79.7% 116.8% 132.1% 90.6% 78.8% 88.9% 84.3% 118.1%

(3.3%) 84.4%

(2)

(9.8%) 4.1%

3,253

2,226 1,645 1,712

1,686 1,630 1,760 1,449 1,307 1,608

1Q20 2Q20 3Q20 4Q20 1Q21 1Q20 2Q20 3Q20 4Q20 1Q21

Gross profit Leasing NOI (1) EBITDA

VND billion VND billion VND billion

% of previous year level % of previous year level % of previous year level

78.1% 67.3% 78.4% 112.7% 154.0% 86.1% 81.1% 91.3% 86.5% 132.1% 88.9% 73.1% 94.0% 110.5% 141.2%

(6.3%) 11.5% 43.3%

(2)

86.1% (2) (14.8%)

(14.9%)

1,572 1,746

1,313 1,508

1,168 1,174 1,178 1,218

998 930 1,068 910

759 845

646

1Q20 2Q20 3Q20 4Q20 1Q21 1Q20 2Q20 3Q20 4Q20 1Q21 1Q20 2Q20 3Q20 4Q20 1Q21

Note: Based on VAS Consolidated Quarterly Financial Statements of 2020 and 1Q2021

These financial metrics took into account the impact of the rental support (VND300bn in 1Q, VND375bn in 2Q, VND145bn in 3Q and VND 46bn in 4Q). There was no rental support recorded in 1Q2021

(1) NOI for leasing of investment properties and rendering of related services is calculated by taking total income from leasing activities and from other property-related services less any property-related operating expenses which include land lease costs but exclude

management expenses allocated from parent company

(2) Total revenue, Gross profit, and EBITDA 4Q2020 surged due to revenue from delivery of shophouses

19Key Operational Metrics

Retail GFA Occupancy rate

Change Change Change

(‘000 m2) 1Q2020 1Q2021 1Q2020 1Q2021 4Q2020

(%) (ppts) (ppts)

Vincom Center 280 280 - Vincom Center 92.1% 95.0% 2.3 93.1% 1.9%

Vincom Mega Mall 388 444 14.4 Vincom Mega Mall 87.6% 87.3% 0.3 86.0% 1.3%

Vincom Plaza 858 858 - Vincom Plaza 82.2% 80.4% 1.8 80.2% 0.2%

Vincom+ 72 72 - Vincom+ 76.5% 74.4% 2.1 73.8% 0.6%

Total 1,598 1,654 3.5 Total 84.9% 84.4% 0.5 83.8% 0.6%

Note: As at March 31, 2021

20Footfall Recovery Post Pandemic

1 Footfall

Hanoi HCMC

Million visitors Million visitors

5 2020 2021 5

2020 2021

4 4

3 3

2 2

1 1

0 0

Jan Feb Mar April May Jun July Aug Sep Oct Nov Dec Jan Feb Mar April May Jun July Aug Sep Oct Nov Dec

Other Provinces

Million visitors

● 1Q2021’s footfall stabilized versus 4Q2020, while footfall in March 12 2020 2021

bounced back to reach 90% of the footfall in March 2019

10

● Hanoi experienced a good recovery thanks to tenant upgrade in 8

VCC Pham Ngoc Thach and Tran Duy Hung, which continued to

attract visitors 6

4

● Retail malls in HCMC were still affected due to a lack of

international visitors. However, improvement is expected by the 2

end of 2021 with adoption of “vaccine passport”

0

Jan Feb Mar April May Jun July Aug Sep Oct Nov Dec

21Tenants’ Sale On Track For Recovery

1 Food & Beverage Fashion Enterntainment Cinema

(1) (2)

Covid-19 relative impact in 2020

(1) (2)

Least impact Least impact Medium impact Most impact

Recovery in 1Q2021

Very strong

Gradual recovery Gradual recovery Strong recovery

recovery

Entertainment and Cinema recovery marks a success in our commitment to support tenants overcoming

2

challenges posed by the pandemic

● In 2021, support package comes in the form of shopping vouchers

● The program has been activated since 1Q2021, and will be implemented and disbursed from 2Q2021

Source: Company report as of 31 March 2021

22Business Highlights in 1Q2021

ANCHOR TENANTS COMMIT TO ACCOMPANY AND EXPAND THEIR NETWORKS IN NEW RETAIL MALLS, HIGHLIGHTS FOR

RESIDENTIAL PROJECTS AND SUROUNDING AREAS

FLAGSHIP BRANDS

VMM SMART CITY

Plan to launch in 3Q2021

LEASING PLAN AND TENANT GROWTH

CHAIN TENANTS EXPANSION

Area Achieved

7% 28% leasing target for 2021

23Marketing Activities in 1Q2021

Spring Festival 2021

Lunar New Year International Women’s Day

(15 Jan – 28 Feb 2021) (01 – 08 Mar 2021)

Featured event “Secret Gift For Her” with participation of

Lunar New Year Fair offering a variety of regional specialties, was

held across Vincom malls including VCP Long Bien with “Happy famous singers namely Rapper G.Ducky, singer Hoang Dung,

Tet” Fair, VCP Sky Lake with “Spring Book Festival” singer S.T Son Thach

Retail malls were gorgeously decorated with colorful spring Dating and a surprise gift from a handsome man for first

themes and landscapes

female guest on International Women’s Day

Series of traditional games for families and children: DIY Couple challenge and lucky drawing with vouchers and

lucky money envelope, making toy figurines from sticky rice

gifts by Vincom. Gifts for female customers (cosmetics,

jewelry, accessories) from retail tenants

Footfall in 1Q2021: Over 36.8 million

24Apply Environmental Initiatives To Optimize Operational Activities

“Sustainable Development” is the underlying principle throughout business operations of Vincom Retail. Operation is optimized as a results of:

Energy saving and environmental protection initiatives (using clean energy, recycling waste, reducing chemical use)

Technology application to standardize and automate processes and optimize operations

Environmental protection initiatives Technology application in operation

1 2 1 2

Solar panels Cooling water treatment Optimize air- Automated

technology for air- conditioning parking system

conditioning system system

Finish installing and deployment Replace chemical water Test – drive intelligent algorithm Complete trial of automated car

of solar panels for 50 retail malls treatment system with E-water to control the air-conditioning parking system at Royal City.

cooling technology for all retail system with a Singaporean Plan for implementation across

malls partner large retail malls such as Times

City, Đong Khoi, Ba Trieu

Save nearly 9% of energy costs Eliminate the environmental Minimize human errors in Reduce headcount to operate

of the entire retail malls system chemical pollutants used operation Reduce cash frauds

Reduce carbon emission by Save costs by minimizing errors Improve customers’ experience

7,157 tons/ year and automating processes at retail malls

252021 Strategy Plan

2021 Strategies And Plan

Continue to develop Vincom Center (VCC)/Vincom Mega Mall

(VMM)/Vincom Plaza (VCP) in the big and Tier-1 cities to offer a dynamic

and engaging experience to the residential community in Vinhomes’ 5 new shopping malls

Product mega projects and surrounding areas New malls’ occupancy target: VMM 85%,

Strategy Enhance customer experience, embrace digital technologies, and VCP and VC+ 95% (including committed

ascertain the number one destination for customers by expanding and tenants)

diversifying tenants’ portfolio with international and Vietnamese brands

Expand the group of international, large, chain and anchor tenants

(Fashion, F&B, Furniture, Home accessories, Supermarket, etc.) in Upgrade tenant mix at VCC Metropolis

Tenant existing shopping malls (Hanoi), VCP Phan Van Tri (HCMC), VCP

Strategy Pioneer in reaching and bringing international, prestigious brands Hung Vuong (Can Tho)

and attractive retail models to Vietnam for the first time

Accompany and support Vietnamese tenant groups

Roll out Tenant Portal

Digital

Build data warehouse system

Transform- Apply digital transformation initiatives to create a dynamic, engaging Enhance Vincom web/ Vincom app to

ation customer experience and maximize operational efficiency facilitate customer experience to and at

Vincom malls

Implement marketing and communication

Marketing Solidify Vincom Retail’s leading position for effective cooperation and plans for the grand openings of major

consumers’ trust

Strategy projects namely Grand World and Vincom

Expand channels for brand communication: Web/App Mega Mall Smart City

Enhance a quality service program to offer

Customer Provide a safe shopping environment with quality products and services impressive shopping experience for the

Optimize operating costs and energy costs

Services continuously increasing end-users and

customers

Note: Company information 27Sale Goals And Action Plan

Goals

Leading shopping malls Shopping malls of Vietnamese

Pioneer in bringing shopping experiences from

with presence across Vietnam

prestigious domestic and international brands

Action Plan

3 projects, including 1 Vincom Mega Mall 2 Vincom Plaza

New opening

100,000 sqm GFA Increase nationwide

retail GFA to

~1.8mn sqm

Upgrade

tenant mix 3 projects, including 1 Vincom Center 2 Vincom Plaza

Number of stores Target tenants for finalizing

Chain and 20%

anchor

tenants Area

development

>20%

Note: Company information

28Financial Update

Financial Performance In 1Q2021 vs 1Q2020

Figures in VND billion 1Q20 1Q21 YoY (%) Commentary

Leasing of Investment

Given the strong recovery of retail market in 1Q2021, no more support

Properties and Rendering of 1,449 1,712 18.2

package in the form of rental rebates in the quarter

Related Services

Handed over 111 units from Bac Lieu, My Tho, Uong Bi in 1Q21

Sale of Inventory Properties 201 452 124.9

compared to 54 units in 1Q20

Mainly from commission fee for real estate brokerage at Grand World –

Other Revenue 36 62 72.2 approx. VND 20 billion (no similar transaction in 1Q20), the rest was an

increase in management fee of Condotels

Total Revenue 1,686 2,226 32.0

Gross Profit(1) 759 1,168 53.9

Operating Profit / (Loss) 575 960 67.0

Profit / (Loss) before Tax 619 980 58.3

Profit / (Loss) after Tax for the

492 781 58.7

Period

Profit / (Loss) after Tax and

492 781 58.7

Minority Interest

Note: VAS Consolidated Quarterly Financial Statements in 2020, 2021

(1) Gross profit already subtracted D&A relating to investment properties accounted for under VAS

30Financial Performance

Total revenue Gross Profit (1)

VNDbn VNDbn

Gross Profit Margin (%)

50.8% 39.9% 47.6% 45.9% 45.0% 52.5%

9,124 9,259

185 215 8,329

172 4,404

2,027 (84) 3,825 (164)

3,433 2,149 3,641 (47) 735

5,518

2,801 806 1,034

951 112 48

2,226 411

7,017 6,008 62 3,752 1,169 (20)

5,506 1,686 36 2,882 2,954

4,455 452 2,342 759 (44)

201

1,449 1,712 668 135 1,002 187

2017 2018 2019 2020 1Q20 1Q21 2017 2018 2019 2020 1Q20 1Q21

Leasing of Investment Properties Sale of Inventory Properties Other Revenue Leasing of Investment Properties Sale of Inventory Properties Other Revenue

Depreciation & amortization of Investment properties (VNDbn)

829 1,042 1,331 1,357 339 346

Leasing Net Operating Income (NOI) (2) Profit After Tax and Minority Interest

VNDbn VNDbn

Leasing NOI Margin (%)

69.3% 69.5% 70.6% 71.3% 69,2% 76.9%

2,851

4,955 2,404 2,385

4,274

3,829 1,905

3,089

492 781

998 1,313

2017 2018 2019 2020 1Q20 1Q21 2017 2018 2019 2020 1Q20 1Q21

Note: Based on VAS Audited Consolidated Financial Statements for respective years and VAS Consolidated Financial Statements for 1Q2021

(1) Depreciation and amortization relating to investment properties is below the graph and should be added back (to Gross Profit) under IFRS. Since 2018, “Other” segment includes results from management of Da Nang condotels which was incurring loss as the property

was still ramping up after launch in May 2018.

(2) NOI for leasing investment properties and rendering of related services is calculated by taking total income from leasing activities and from other property-related services less any property-related operating expenses which include land lease costs but exclude

management expenses allocated from parent company. 31Balance Sheet

Total Assets Total Borrowings, Cash and Cash Equivalents

VNDbn VNDbn

5,726 5,686

38,684 39,816 39,780

35,839 4,945

10,911 11,125 11,423 4,122

7,121

3,133

2,780 2,785

2,177

27,773 28,718 28,691 28,357

31/12/2018 31/12/2019 31/12/2020 (2) 31/03/2021 31/12/2018 31/12/2019 31/12/2020 (2) 31/03/2021

(1)

Investment Properties and Investment Properties Under Construction Other Assets Borrowings Cash & equivalent

(3)

Total Equity (Net Debt / (Net Cash)) / Equity

VNDbn VNDbn

28,509 26,954 29,336 30,117

2.7%

2.3%

1.0%

31/12/2018

(2) (2)

31/12/2018 31/12/2019 31/12/2020 31/03/2021 31/12/2019 31/12/2020 31/03/2021

Net cash

Note: Based on VAS Audited Consolidated Financial Statements for respective years and VAS Consolidated Financial Statements for 1Q2021

(1) Investment Properties and Investment Properties Under Construction (IP/IPUC) are valued at development cost minus depreci ation and amortization and are not fair valued

(2) Decline in other assets, cash and cash equivalents, total equity as well as increase in gearing ratio as of 31 December 2019 was due to the payment of cash dividends of VND 2,445bn in April 2019 and buy back 56.5 mil treasury shares completed in November 2019

(3) Net Debt / (Cash) = (Short-term Borrowings + Long-term Borrowings) – (Cash & Cash Equivalents + ST Investments).

32Appendix

Updated Mall Openings Plan Until 2026

No. Model Number of projects Location Retail GFA (sqm)

To be developed 2021 – 2026

1 VCC 2 Hanoi 95,000

Hanoi, HCMC, Hung Yen, Dong Anh, Can

2 VMM 27 2,413,000

Gio, Cam Ranh

Hanoi, HCMC, My Tho, Bac lieu,

3 VCP 19 489,000

Hai Phong, etc.

4 VC+ 1 Thanh Hoa 3,000

TOTAL 49 3,000,000

● 49 new shopping malls, increasing GFA retail floor from nearly 1.7 million sqm to approx. 4.7 million sqm

● Land bank for retail mall development is sourced from Vincom Retail self-developed projects and through Vingroup and its

subsidiaries

● Depending on the pandemic situation, Vincom Retail can be flexible in development progress and openings of new retail malls

Note: Numbers are rounded to the nearest thousand ('000)

34Bridging VAS to IFRS

Unit: VND Billion

VAS Adj. IFRS Commentary on Adjustments

1Q2021 1Q2021

Leasing revenue and other related Realized unearned revenue of deposit from customer in relation to

1,712 45 1,757

services amortization of deposit

Sale of inventory properties 452 452

Other revenue 62

Total revenue 2,226 45 2,271

Cost of leasing activities and other related

(710) 367 (343) Mostly depreciation of malls included in VAS; excluded under IFRS

services

Cost of inventory properties sold (266) (266)

Others (82) (82)

Cost of goods & services (1,058) 367 (691)

Gross profit 1,168 412 1,580

Selling expenses (92) (92)

General and administrative expenses (64) 18 (46) Amortization of Goodwill included in VAS; excluded under IFRS

Other income 21 21

Other expense (1) (1)

Finance expense (154) (44) (198) Amortization of Deposit from customer

Finance income 102 15 117 Amortisation of Deposit under BCC

Profit before tax 980 402 1,382

Tax expense (199) (80) (279) Deferred tax arising from above adjustments

Profit after tax 781 322 1,103

Note: Based on VAS Consolidated Financial Statements for 1Q2021 and conversion to IFRS by management, excluding impact from Investment Property and Investment Property Under Construction (IP/IPUC) revaluation gain/loss

35Vietnam Swiftly Controlled Covid-19

More than 511,000 people have been vaccinated against Covid – 19 as of May 2nd, 2021(1). The Vietnamese Government plans

to vaccinate 30 million people (~ 30% of its population) by the end of this year

1st wave of Covid-19 2nd wave of Covid-19 3rd wave of Covid-19

40% growth within 2 Visitors to shopping centers Pandemic was well under controlled

months after social +40% 15 grew 32% after social by the end of March. Retail malls’

distancing was lifted distancing was lifted visitors are expected to grow

14

strongly from Q2

2nd Outbreak 13 13

(Jul 28 – Sep 20) 14 14

+40%

12

+32%

12

667

10

1st Outbreak 11

(Mar 5 – Apr 30) 10

9

Million visitors

433

317

4

155

109

59

30

0 0 1 0 0 3

Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20 Oct-20 Nov-20 Dec-20 Jan-21 Feb-21 Mar-21

Community cases Shopping mall visitors

Source: Minitry of Health, Company report as of March 31, 2021, (1) Our World in Data

36Investor Relations Department Vincom Retail JSC 7 Bang Lang 1, Vinhomes Riverside, Viet Hung Ward Long Bien District, Hanoi, Vietnam Tel: +84 (24) 3974 9999 ext. 9545 Fax: +84 (24) 3974 8888 Website: ir.vincom.com.vn/en E-mail: ir@vincom.com.vn

You can also read