Corporate venturing on the test bench - Analysis by Boris Battistini and Martin Haemmig - SECA

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Global Corporate Venturing

Corporate venturing

on the test bench

Analysis by

Boris Battistini and

Martin Haemmig

All articles first published in Global Corporate Venturing

www.globalcorporateventuring.com

Analysis

CORPO

This is the first in a series of articles by Haemmig and RA

Battistini to keep readers abreast of the latest trends VENTU TE

RING

Great leap forward ON THE

TEST BE

NCH

Over the past few years, analysts and

commentators have described the Boris Battistini, research

new wave of corporate venturing (CV)

activities sweeping across industrial associate, ETH Zurich, and

sectors. Despite adverse macroeco- Martin Haemmig, adjunct

nomic conditions and highly volatile

capital markets, the total number of

professor CeTIM at

CV programmes has grown dramati- UniBW Munich and

cally from 694 in January 2010 to 865 Leiden University

in December last year.

Perhaps most importantly, today’s

corporate venturing landscape is the CV new entrants by parent’s country of origin the resources and assets

35

first truly global one. It is a landscape accessed through interna-

30

characterised by the acceleration of 27

26 tionalisation. Unlike their

the geographic shift of venture invest- 25 23 western counterparts, such

ment patterns and the emergence of 20 16

19

companies are not prima-

new global innovation hotbeds. But 15 13 13 13 rily market and resource-

10

what is the distinguishing feature of 10 seeking investors. They are

increasingly globalised corporate ven- 5 3 3 3 innovation-driven investors

1

turing activities? 0

0 0

in search of highly disrup-

An analysis of the data on new CV 2010

North America Western Europe

2011

Eastern Europe Asia

2012

Middle East

tive technologies and busi-

programme entrants reveals a new ness models, and therefore

generation of corporate ventures – Source: Global Corporate Venturing interested in strategic assets

innovative and fast-growing Asian Asian CV new entrants 2010-12 by sector (n=41) and investments in know-

corporations. In fact, Asian-headquar- how in global entrepreneurial

tered corporations launched 19 CV 2% hotspots.

2% 5% 2% 5%

programmes out of a total of 52 new 5% The most recent exam-

Clean-tech/energy

entrants last year, in so doing sur- 5% 10%

Consumer ple is the announcement of

passing – for the first time – the US Financial services Samsung’s “global platform

and the EU, each of which had fewer Industrial for disruptive innovation” last

IT

new entrants (see figures, right). month. The platform strategy

24% Media

It is worth noting that Asia-based Portfolio is designed to gain access to

39%

corporate investors constitute an Services outside innovations in coun-

increasingly important fraction of Transport tries, such as the US, Israel,

Utilities

overall venturing activities with a total China and India, with exter-

of 189 programs (22%), debunking Source: Global Corporate Venturing nal venturing and partnering

the myth that corporate venturing is a initiatives – for example, a

US phenomenon. $100m catalyst fund with a focus on early stage, and the

The rise of Asian corporate venturers urges us to reflect global $1bn Samsung Venture Investment Corporation –

on the key drivers of this shift as such factors are likely fun- that complement the 24 corporate research and develop-

damentally to redefine the future marketplace for technol- ment centres with a budget of $10.8bn last year.

ogy and innovation. Here are three important – and related Interestingly, Samsung Electronics is the only South

– developments that should not be underestimated. Korean company whose president and chief strategy officer

1 A number of Asian corporations – for example ZTE, LG, is strategically based in America’s Silicon Valley. This is to

Huawei, Samsung and Panasonic – have established ensure Samsung will invest $20bn up to 2020 in novel mar-

themselves as serious international players and innova- kets to identify and capture tomorrow’s business opportuni-

tion leaders, adopting a different strategic approach to ties – wherever they can be found around the globe.

Global Corporate Venturing March 2013 27

Analysis

2 In China, India and other vibrant Asian high-growth mar-

kets – think Taiwan, Indonesia and Singapore – technol-

ogy clusters and entrepreneurial talents are arising, putting

become strategic investors in local incubators and acceler-

ators. High-profile examples include Kyron, a $50m accel-

erator for Indian start-ups based in Bangalore, or Innova-

innovative Asian start-ups on the global technology map. tion Works based in Beijing and Shanghai, which over the

As the copy-cat and production-driven era fades away, last three years has incubated and invested in more than

a number of Asian IT, media and consumer-focused start- 50 local start-ups and recently closed its second fund at

ups have begun to break through with market-leading $275m.

products, often combining frugal, agile and highly scalable

solutions with innovative business models. As examples,

consider the mobile internet gaming sector, where Asian

3 As more western technology ventures consider Asian

markets as an essential part of their expansion and

commercialisation strategy, increasing numbers of Asian,

start-ups have fiercely challenged western market leader- especially Chinese and Indian, investors are financing US

ship, or observe how Twitter has recently started to copy and EU-based start-ups and providing the much-needed

various features from Weibo, a Chinese microblogging support to break into the region. For example, research

website. shows that nearly twice as many Chinese venture capital

Moreover, it is worth observing that recent research firms (VCs) backed US-based start-ups in 2011 compared

suggested that of all US publicly-traded internet compa- with two years earlier. More importantly, the trend is set to

nies only six achieved over-30% top-line growth in 2011 continue well into the next few years, as a number of Chi-

and 2012, and 2012 ebitda (earnings before interest, tax, nese VCs are expected to raise more cross-border funds

depreciation and amortisation) margins of at least 30%. to invest in global transactions.

That means only 5% of the current crop of public internet Beyond exporting Asian venture capital, a number of

companies are in the top echelon in terms of profitability innovative start-up acceleration initiatives, such as Inno-

and growth. Spring, Silicon Valley’s first US-China technology incuba-

Most interesting, all six companies in the top tier are not tor, are emerging and are helping to redefine the role of

western based but from Bric nations (Brazil, Russia, India Asian venture investors in the entrepreneurial ecosystem.

and China), such as China-based Tencent, Baidu and In an increasingly global venture capital landscape, cor-

Qihoo 360. porate venturing has a unique part to play in turning the

As corporates have realised the innovative potential of great potential offered by these transformations into value

Asian markets, they have begun to forge alliances and for their corporate parents. n

Benchmarking investments in global innovation hotbeds

Global VC investment by selected innovation hotbeds

2012 by dollars invested and number of investment rounds

Ranking by amount raised (US$bn) Ranking by number of rounds Of the global total VC amounts invested, the US

(Global total: $42.3bn) (Global total: 5,090) still dominates with $27.9bn (70%) of all

global VC investment (US, Canada, Europe,

Israel, China, India), and of the global 5090 number

of rounds, has 3,363 rounds (66%).

As a VC innovation hotbed, the Silicon Valley

dominates with $11.2bn (26% of global) and 1,128

deals (22% of global) with a huge margin the rest of

the world.

Global corporate participation in financing rounds

2006-12 percentage of CVC to total VC-backed deals

US, Europe, Israel, China, India, Canada

With the financial crisis the proportion of corporates

participating gradually increases. With the recent new

CV funds raised particularly in Asia, the ramp-up of

corporate participation is expected to increase in the

coming years.

Global corporate/CVC participation by geography

2006-12 as percentage of total VC-backed deals (not to scale)

Global Corporate Venturing March

US

2013

Europe Israel

Corporate participation in innovative companies is

continue to grow in the mature markets, while China and

28

India is expected to see an increase CV investments,

both from foreign corporates and the rise of the local

corporates in these two countries, since the 2012 launch

CV funds raised particularly in Asia, the ramp-up of

corporate participation is expected to increase in the

coming years.

Analysis

Global corporate/CVC participation by geography

2006-12 as percentage of total VC-backed deals (not to scale)

US Europe Israel

Corporate participation in innovative companies is

continue to grow in the mature markets, while China and

India is expected to see an increase CV investments,

both from foreign corporates and the rise of the local

corporates in these two countries, since the 2012 launch

of new CV programmes in Asia surpassed those of the US

China Canada India and also of Europe. As a result, Asian corporates

will invest both in their region and also in the mature

markets to seek leading technology and market access.

Global cross-border deals will fuel CV deals.

CVC investments by stage of development

2006-12/Q3 by number of deals (not to scale)

Europe US China India

Start-up Product development

The global sweet spot in number of deals is focused on

revenue generating (preprofit) companies, followed by

product development (prerevenue). This is where the

corporates can add the most value to innovative

companies.

It is obvious that China and India are still small in scale

Revenue (pre-profit) Profitable on corporate deals and focus mainly on revenue

generating and profitable companies.

CVC investments by stage of development

2006-12/Q3 by percentage of US$

Europe US China India

Start-up Product development The global sweet spot of CV capital investments is in

revenue generating (pre-profit) companies, with over

60% of the entire amounts.

In the US and Europe, 20%-40% goes into

companies in product development (pre-revenue)

companies and the large bulk in to revenue pre-profit.

Revenue (preprofit) Profitable

India has recently seen almost all CV money funneled

into revenue pre-profitable deals, while China is the

outlier with a significant portion into profitable companies

(although decreasing now).

CVC: foreign vs domestic corporate co-investors

2006-12 percentage of VC deals with at least one foreign corporate co-investor

The low ratio in the US of foreign corporate

US Europe

investors has to do with the very strong presence of local

CV players, with a blend of European and Asian

corporates sharing the deals.

In contrast, the bulk of foreign corporate investments in

Europe stem mostly from mature US MNCs.

Foreign HQ corporate investor

China Domestic corporate India The number of deals with corporate investors in China

and India is still marginal, and a few additional deals on

either side will rapidly move the needle in either direction.

Although local CVs are on the rise, it is difficult to

predict if the foreign MNCs will outgrow them as

they are desperate to access the growth markets.

n

Source: Dr Martin Haemmig (CeTIM) and Ernst & Young (VC Insights Team); data: DowJones/VentureSource

Any reproduction or reuse of the graphs is permitted only with the agreement of Martin Haemmig

Global Corporate Venturing March 2013 29

Comment

Top-level focus on

technological discontinuity

Corporate venturing (CV) funds are

often established to generate strate- In our series of articles

gic value for the corporate parent. The

success of CV activities is therefore Corporate Venturing on

not only measured in terms of growth, the Test Bench,

but also how well CV can complement

internal research and development

Boris Battistini and

efforts or gain early access to poten- Martin Haemmig

tially disruptive technologies and busi- review and analyse

ness models. For this reason, CV

investments are often seen as a win- the latest trends

dow on emerging technologies and

business models – a sophisticated radar set up to identify rations in four information and communication technology

potential technological discontinuities. industry sectors, Maula and colleagues found that corpo-

Technological discontinuities are fundamental changes rations can direct top management’s attention to techno-

from a dominant technology to another that result in quickly logical discontinuities, by establishing appropriate inter-

rendering products and services obsolete, and transform- organisational relationships such as strategic alliances or

ing industry dynamics in ways that are difficult to antici- venture capital networks.

pate, especially among incumbents. More interestingly, the results suggest that among the

Such discontinuities are what former Intel chief execu- various forms of the interorganisational relationships in

tive Andrew Grove termed “strategic inflection points”. In which incumbents engage, only CV investments appear

his book Only the Paranoid Survive, he suggests that what to play a crucial role in guiding top management’s atten-

such a discontinuity does to a business is profound, and tion to technological discontinuities. In particular, their

how executives manages this transition determines its analysis shows that “ties with high-status partners through

future. coinvestments with high-status VCs [venture capital firms]

Discontinuous technological change therefore requires positively affect top managers’ timely attention, whereas

effective managerial responses. In fact, according to a homophilous interorganisational relationships (ie industry

recent article in Organization Science by M Maula and alliances) do not have a significant impact”.

T Keil of Aalto University, Finland, and S Zahra of the Uni- Why are CV investments so important for the recogni-

versity of Minnesota, US, effective and timely responses tion of technological discontinuities? The authors argue

are made particularly difficult as such transformations often an “incumbent may be able to gain access to more

occur at the fringes of an industry and are usually driven diverse information and diverging viewpoints that can

by highly innovation and venture capital-backed start-ups. help to reshape attention patterns within the incumbent.

Based on a longitudinal study of the largest US corpo- … In addition to the diversity of the information sources,

the status of an information source plays an

important role because knowledge and infor-

CV investments are often seen as a window on mation from these sources carry different

weights with corporate decision-makers. The

emerging technologies and business models – a high status of partners, such as syndication

with high-status VCs, may increase the cred-

sophisticated radar set up to identify potential ibility that top managers attach to information

from these ties”.

technological discontinuities In short, this research suggests that CV

activities can play a critical role in influenc-

Global Corporate Venturing April 2013 32

Comment

ing senior management’s cognition, facilitating the iden- become important for the incumbent.” n

tification of emerging business opportunities and related

business models. Importantly, as Maula and colleagues Boris Battistini is a research associate at ETH Zurich and a

observe: “Even when an incumbent does not transfer a project leader of the Corporate Venturing Research Initia-

specific technology that a start-up can commercialise, CV tive with Bain & Co (e-mail: bbattistini@ethz.ch)

investments may provide important insights into the evo-

lution of a technological field. Information received from Martin Haemmig is an adjunct professor at CeTIM at

CV investments may also influence how senior executives UniBW Munich and Leiden University (email: martinhaem-

think about the likelihood that a technological area will mig@cetim.org)

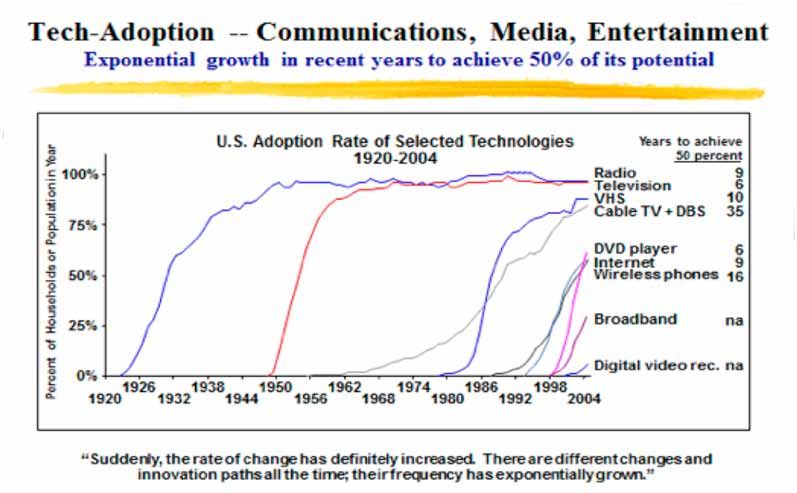

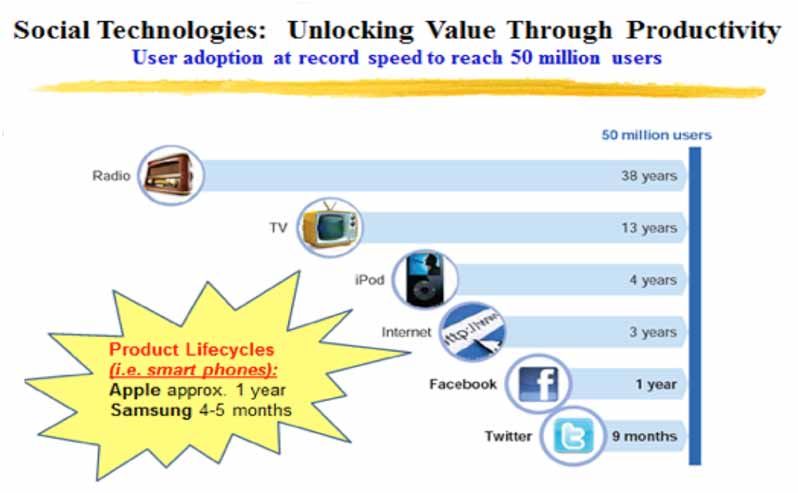

The rate of technology

adoption and diffusion

The rate of technology adoption has

radically increased in recent years

Source: Ernst & Young and

University of California Berkeley

The adoption of social technologies

has occurred at unprecedented pace,

with important implications for product

market strategies and the obsolescence

of products. Also, the product lifecycle

in high technology sectors, notably,

the mobile industry, has significantly

shortened

Source: McKinsey Global Institute

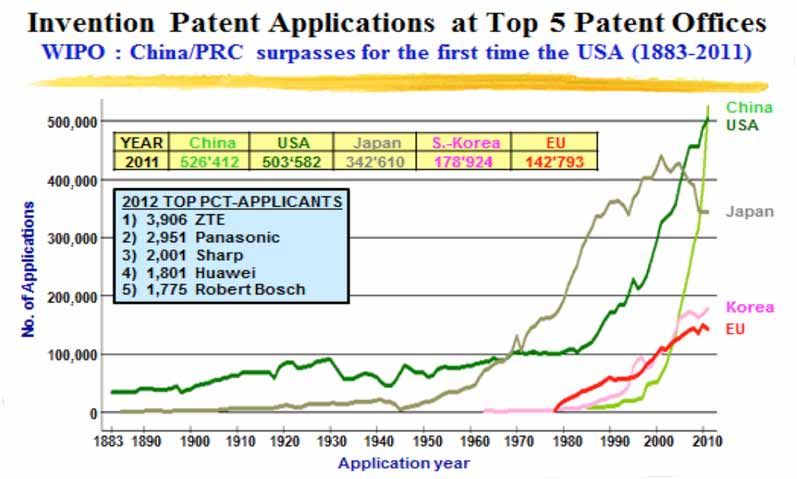

China tops the list of the world’s

leading patent offices with 526,412

applications, compared with 503,582 in

the US, strengthening its position as an

emerging innovation leader

Source: World Intellectual

Property Organization

Global Corporate Venturing April 2013 33

Analysis

Corporate investors add

value to their companies

To what extent can corporate inves-

tors add value to portfolio companies? In our series of articles

This question is particularly important

for a variety of reasons. First, prom- Corporate Venturing on

ising new ventures exert consider- the Test Bench,

able choice regarding their funding

sources and, especially so, in the

Boris Battistini and

case of assessing the pros and cons Martin Haemmig

of corporate backing. Second, promi- review and analyse

nent traditional venture capital funds

(VC) prefer to syndicate with investors the latest trends

that can significantly contribute to the

success of the new ventures, enhancing the likelihood of The results show that CV-backed companies are more

a profitable exit. likely to secure a successful exit and, perhaps more sur-

Yet there are pros and cons when corporate investors prisingly, to receive higher valuations and acquisition pre-

engage with innovative and dynamic growth companies miums. However, this is the case only when portfolio com-

and it is therefore important to understand how and under panies have a strategic fit – a strategic alliance or close

which conditions corporate investors actually add value to business relationship – with the parent corporations of

portfolio companies. the corporate venturers. The strategic fit allows portfolio

Recent empirical work, published in Financial Manage- companies to benefit from the assets and operation com-

ment by Vladimir Ivanov of US regulator the Securities and plementarities of corporations – for example, market and

Exchange Commission, and Fei Xie of George Mason Uni- technical knowledge, infrastructure for product develop-

versity, presents evidence suggesting that corporate inves- ment, and access to intra-firm information networks and

tors – compared with traditional VCs – add substantial market channels.

value to the portfolio companies. In particular, they analyse While such results provide a compelling case for the

a sample of VC-backed initial public offerings (IPOs) and potential benefits of partnering strategic corporate inves-

a sample of acquisitions of venture-backed companies to tors, it remains unclear under which particular conditions

see whether corporate venturing (CV) backing affects the corporate backing is beneficial.

valuations at the IPO or the takeover premiums in case of Analysis presented by Haemin Park and Kevin Steensma

acquisitions. in Strategic Management Journal provides some insights

on this, as they specifically exam-

ine the trade-off faced by start-ups

“Corporate investors can provide complementary assets when considering CV funding.

“Corporate investors can pro-

that enhance the commercialisation of new venture vide complementary assets that

enhance the commercialisation of

technologies. However, tight links with a particular new venture technologies. How-

ever, tight links with a particular

corporate investor has drawbacks and may constrain new corporate investor has drawbacks

and may constrain new ventures

ventures from accessing complementary assets from from accessing complementary

assets from diverse sources in an

diverse sources in an open market.” open market.”

Their analysis of 508 venture-

Global Corporate Venturing May 2013 18

Analysis

Median pre-valuation at IPO of VC/CV-backed companies backed start-ups in the computer,

wireless and semiconductor sectors

Global valuations: CV-backed companies show higher valuations

found that CV-backed new ventures

400 were less likely to fail – bankruptcy,

Median pre-money valuation prior to IPO ($m)

Non-corporate participation for example – and significantly more

350

Corporate participation likely to go public under specific condi-

300 Overall (combined) tions, when they required “specialised

complementary assets” and operated

250

in a relative more uncertain environ-

200 ment, where start-ups cannot easily

assess their future resource needs.

150

If corporates do not add significant

100 value to their investee companies,

50

where there is a clear strategic fit with

the parent company, entrepreneurs

0 may opt more frequently for tradi-

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 tional VCs, since they have generally

fewer strings attached and the path

Time to IPO from 1st institutional VC/CV financing to exit – IPO, merger or acquisition

– is significantly shorter than with the

Corporate participation with strategic intent leads to longer holding time

engagement of a corporate investor.

14 As a result, corporates need to com-

pensate for some of their drawbacks

12 Non-corporate participation when being involved with innovative

Corporate participation growth companies and the best way

10 Overall (combined) to overcome this hurdle is to provide

unique and superior value that tradi-

8

Years

tional VCs may not easily match. n

6

4

Sources

2

Ivanov, VI and Xie, F (2010) Do

0 corporate venture capitalists add

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 value to start-up firms? Evidence

from IPOs and acquisitions of

Percentage of failed companies without CV financing VC-backed companies. Finan-

cial Management 39: 129–52. doi:

Majority of company failures (bankruptcy) lack corporate backing

10.1111/j.1755-053X.2009.01068.x

100

Park, HD and Steensma, HK (2012)

90

When does corporate venture capital

80 add value for new ventures? Strategic

70 Management Journal 33: 1–22. doi:

10.1002/smj.937

Percentage

60

50 Boris Battistini is a research asso-

40 ciate at ETH Zurich and a project

30 leader of the Corporate Venturing

Research Initiative with Bain & Co

20

(e-mail: bbattistini@ethz.ch)

10

0 Martin Haemmig is an adjunct

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 professor at CeTIM at UniBW

Munich and Leiden University

Source for all graphs: DowJones VentureSource (email: martinhaemmig@cetim.org)

Global Corporate Venturing May 2013 19

Analysis

What we can learn from

ventures into biotech

The pharmaceutical industry is under-

going considerable changes in face In our series of articles

of R&D diminished productivity, the

patent cliff and increased competi- Corporate Venturing on

tiveness leading to pricing pressure. the Test Bench,

The traditional linear approach to cor-

porate innovation appears unable to

Boris Battistini and

increase pipeline value and corporate Martin Haemmig

revenue. In fact, recent mergers and review and analyse

acquisitions, geographic expansion

and diversification into consumer and the latest trends

animal healthcare have neither com-

pensated for the slowdown in innovation, nor decreased Recent corporate venture capital activities, as docu-

the unsustainable cost of bringing new drugs to the market. mented by Global Corporate Venturing data, show that

Big pharma, as a result, is moving beyond internal dis- corporations have realised the nature of the opportunity,

covery and drug development programmes. In recent becoming a prominent source of capital and resources for

years, industry analysts have documented the increasing the development of early-stage innovation in biotechnology.

number of open innovation initiatives such as academic Interestingly, the current wave of corporate venturing

partnerships, open source platforms, crowdsourcing and exhibits a set of novel characteristics. A recent study pub-

external venture capital units. lished in Nature Biotechnology, conducted by the Swiss

For example, InnoCentive’s pioneering open innova- Federal Institute of Technology (ETH Zurich) and Bain &

tion model was followed by several prominent initiatives Co, reveals the majority of the established corporate ven-

of industry peers, including the public-private partnership ture units reported substantial changes of the corporate

founded by Structural Genomics Consortium and Glaxo- venturing activities of leading pharmaceutical companies,

SmithKline, Lilly’s Phenotypic Drug Discovery initiative primarily with respect to the structure, strategic scope and

and Merck’s Oncology Network for collaborative clinical human capital.

trials. Perhaps more importantly, as observed by Henry “Corporations have developed large and more sophisti-

Chesbrough who coined the term “open innovation” in cated venture units, which take a more active role in syndi-

2003, in the recent years “companies that have used open cates and deliver greater value to co-investors and entre-

innovation not just with technology but also with business preneurs. More importantly, corporations are increasingly

models, there has been a rethinking”. adopting new models, practices and fund structures.”

The shift toward external innovation sourcing is consist- The results of the study revealed a number of ventur-

ent with the increased importance of venture and growth ing practices that distinguish successful venturing activi-

equity capital investments for new biotechnology start-ups. ties and that offer a benchmark against which to compare

As biotech ventures are increasingly regarded as one of current and future corporate venturing practices in other

the most valuable sources for industrial sectors.

future revenue opportunities, So, what are the practices

corporate venturing is grow- that define successful CVC

ing in strategic importance – The current wave of corporate units? First, they develop a

especially at a time when the strong mandate and estab-

market for traditional venture venturing exhibits a set of novel lish direct reporting line. Most

financing is dwindling, affect-

ing the ability to raise new characteristics pharmaceutical firms take

a longer-term view of equity

private VC funds. investments by providing

Global Corporate Venturing June 2013 30

Analysis

a strong mandate to corporate venture units from the Focus venturing and secure strategic alignment:

executive team and board of directors. Percentage of importance and frequency (mean score;

Second, they ensure decision-making autonomy. min=1, max=3.0) of strategic objectives

Successful corporate venturing in the study relied on 70% 3.00

2.90

autonomous governance structures. Three-quarters 60%

2.80 2.80 Highly important (3.0)

2.70

of the corporate venture units enjoyed financial auton- Important (2.0)

Percentage of respondents

Mean score 2.50

omy with either a separate budget – that is, not subject 50%

to internal review – or a closed-fund structure. Moreo- 40%

2.20

ver, the management of the venturing activities and 30%

2.00

1.90 1.90

2.00

1.90

strategic investments showed considerable decision- 1.80 1.80 1.80

1.60

making autonomy. 20%

1.50

Third, they secure external legitimacy and active 10%

involvement. In particular, they build and sustain rela- % 1.00

tionships with traditional VCs, which enables corpo-

n

th

ts

e

gy

re

n

ets

s

s

s

s

t

n

hip

gie

es

itie

tur

nc

tio

rke

row

me

ltu

olo

ss

sin

e

rac

rate units to access high-quality dealflow and identify

l re

bil

ns

olo

cu

ma

llig

lop

ea

hn

eg

pa

bu

tio

att

cia

hn

al

e

tec

ve

rat

-lin

ing

ca

int

ela

uri

re

tec

an

nd

opportunities. Also, the study showed that corporate

de

rpo

gh

co

top

erg

ne

w

et

r

Fin

na

ct/

ic

ne

ce

ark

rou

pre

co

xt

em

teg

du

to

tio

rvi

ne

to

venture units have been moving away from a passive

s/m

kth

ing

tre

pro

on

em

tra

se

to

ss

or

En

ea

rag

uti

gie

ps

ct/

ret

ss

ce

for

hf

trib

Br

investor role with limited involvement to become a

du

ce

olo

ve

elo

Ac

arc

nt

nd

pro

Ac

n

Le

le

hn

v

Se

Co

ma

De

Ta

tec

w

sophisticated investment partner capable of participat-

de

Ne

on

se

ow

rea

ing in larger and more prominent syndication. Often, nd

Corporate venturing unit’s objectives

Inc

Wi

units even lead or co-lead financing rounds and are

involved in the development of their portfolio start- Secure external legitimacy and active involvement.

ups, frequently taking board seats and actively lever- (a) Importance of the relationship with different parties for

aging their corporate resources. the corporate venture unit.

Fourth, they create value-based incentives. It 80% 3.0

emerged from the study that successful coporate ven-

70%

turing units tend to provide greater incentives to the

managers of the fund. As a result, the research docu-

Percentage of respondent

60% 2.5 2.5

mented the increased used of performance-related 50%

incentives as a central component of the overall com-

pensation package. 40% 2.0

Fifth, the study uncovered a systematic use of mul- 30%

1.8

tiple performance metrics. Most firms not only have 1.6 1.6

20% 1.5

a broad range of key performance indicators, includ-

ing metrics for financial and strategic returns, but also 10%

define performance and management-related target 0% 1.0

values. Business idea coming Business idea coming Business idea coming Business idea coming

from VC firms from employees in the from directly from from conferences or

In sum, the study reveals that the corporate ventur- corporation outside external forums

ing practice of pharmaceutical firms has substantially Sources of business ideas

evolved during recent years and that successful CVC (b) Importance of sources for obtaining new business

units have consistently adopted a number of VC-like ideas/business proposals.

practices that allow them to become more profes- 80% 3.0

sional investors. Less important (1.0)

Less important (1.0) Important (2.0) Highly mportant (3.0) Mean score

Important (2.0)

Today’s corporate venturing in biotechnology has a 70%

Highly important (3.0)

new face – and it is more attractive for biotech start- Mean score

2.6

60% 2.5

ups and the VC community. n

Percentage of respondents

2.3

50%

Sources 40%

2.1

2.0 2.0

The changing face of corporate venturing in bio- 30%

technology, Nature Biotechnology 30(10): 911–15,

doi:10.1038/nbt.2383 by Georg von Krogh, Boris Bat- 20% 1.5

tistini, Fotini Pachidou, Pius Baschera (2012)

10%

An audience with Henry Chesbrough, Nature Reviews

Drug Discovery 12(5): 338–9, doi:10.1038/nrd4008 by 0% 1.0

Henry Chesbrough and Asher Mullard (2013) Head Office Corporate business units Venture capital community

Parties of corporate venturing unit

Start-up community

Global Corporate Venturing June 2013 31Analysis

How innovation spreads

from emerging markets

Jeff Immelt, chairman and chief exec-

utive of General Electric (GE), in 2009

prioritised very clearly: “Don’t even

In our series of articles

talk about your growth plans in the Corporate Venturing on

US. You have got to triple the size the Test Bench,

of your Indian business in the next

three years. You have got to put more Boris Battistini and

resources, more people, and more Martin Haemmig

products in there, so you are deep

in that market and not just skimming

review and analyse

the very top. Let’s figure out how to the latest trends

do it … On the one hand, our target

is to win local market shares with

local products which fit to the local needs best; on the bally, thus building up vast economies of scale in manu-

other hand, emerging markets offer effective conditions to facturing and extensive distribution and logistic channels.

develop really new solutions – often solutions that are by During this phase products were created and researched

far simpler and cheaper.” at home and distributed wherever the demand occurred.

For GE, “reverse innovation isn’t optional, it’s oxygen”. In the second stage, MNCs shifted R&D to the local mar-

But what exactly is reverse innovation? Does it matter to kets, in order to become more competitive, tap into local

your innovation strategy? knowledge and decrease the distance to the end customer.

While strategic perception of emerging markets has In so doing, they started winning market shares by adjust-

developed over the past few years and taken an unprec- ing the global offering to the local requirements, a process

edented shape, reverse innovation represents one of the also known as glocalisation.

most unreported – yet potentially impactful – phenomena. Finally the third phase involved refocusing local R&D

Reverse innovation – a concept originally coined by Vijay efforts on developing the products “in country, for coun-

Govindarajan of Tuck School of Business – refers to a case try”, including emerging countries. Hence no longer was

in which an innovation is adopted first in an emerging mar- the global offering simply depleted of its functionality, but,

ket before being successfully adopted in developed markets on the contrary, the local R&D centres performed their own

and added to the global offering. It describes how corpora- assessment of the customer requirements and developed

tions develop innovative products in countries such as China products satisfying such requirements.

and India and then distribute them globally. The number of In today’s marketplace, the biggest competitors for

examples of reverse innovation are becoming increasingly MNCs are larger local companies from emerging markets

frequent, unveiling the extent to which emerging countries that target global markets – for example, Tata, Mahindra,

will become the research and development (R&D) hubs Godrej, Suzlon, and Financial Technologies from India;

and technology accelerators for breakthrough innovations Haier, Lenovo, and Goldwind from China; Cemex from

in a variety of industrial sectors ranging from healthcare to Mexico and Embraer from Brazil.

energy, housing, transportation, financial services and so on. The table below shows a selection of examples of recent

However, to appreciate the current shift in the global disruptive innovations from India by large local players,

innovation strategy and the underlying implications of with some already reaching global markets:

reverse innovation, it should be noted that reverse inno-

vation has been preceded by three stages – three global What does it mean to western corporates?

innovation approaches.

In the first stage – internationalisation – multinational It is often being said that innovation is the mother of com-

corporations (MNCs) began exporting their products glo- petitiveness. That is true, but only to a limited extent.

Global Corporate Venturing July 2013 36Analysis

The fact is that innovation Recent disruptive innovations from India

is only a means and not an

end. So what is the end? Product Firm (year of market Market Entry level price of

Adaptation! Only those introduction) introduction existing, competing

companies, that adapt to a price ($) products ($)

changing environment will Tata Nano (car) Tata Motors (2009) 2,600 6,500

withstand the test of time.

Mac 400 (ECG machine) General Electric (2009) 1,000 10,000

From a western perspec-

tive, the notion of innovation ChotuKool (fridge) Godrej & Boyce (2009) 70 180

as the key source of com- Pureit (water purifier) Hindustan Unilever (2005) 43 150

petitive advantage held true Swach (water purifier) Tata Chemicals (2009) 21 150

for most of the 20th century

as companies in the devel- Sakshat (tablet PC) Indian govt and public institution 35 500

oped markets could rely on www.global-innovation.net/publications/PDF/Working_Paper_61.pdf

global business models and

reap benefits from cost dif-

ferentials and arbitrage opportunities across geographic ducing in large volumes and keeping overhead costs low

regions. However, as globalisation keeps its momentum, enough to survive on razor-thin margins. Once competi-

the traditional paradigm of inventing in the developed mar- tors get access to crucial technology, they penetrate pre-

kets and producing in developing markets is becoming mium markets with lower prices to turn them into volume

increasingly obsolete. markets.

More importantly, there is a different notion of inven- Over the years, multinationals have prospered by turn-

tiveness and innovativeness between mature and ing out premium-priced products for the world’s affluent.

emerging markets. This is a dangerous fallacy, as it pre- Rather than also designing products for poorer people

vents western companies from thinking about innova- elsewhere, many businesses found they could simply

tion in the new and necessary ways that are required to pass yesteryear’s models down, as if they were unload-

succeed in novel markets. Whereas people in the west ing fleets of used cars. Lately, big companies such as

tend to think about innovation as a clearly linear, struc- Microsoft, Nokia and Procter & Gamble are discovering

tured, long-term process with the aim of creating radical they can profit by targeting the world’s masses first. And

or disruptive innovations, innovation in emerging mar- they can score again by selling these low-priced products

kets is often the opposite – unstructured, chaotic and elsewhere.

opportunistic.

This is first driven by a fast-growing economy and a ris- Conclusion

ing middle-class consumer base, which have not yet devel-

oped the level of brand loyalty seen in mature markets. MNCs from mature markets have deep global capabilities

Therefore, agility is essential in order to exploit opportuni- and a solid technological foundation, while local corpo-

ties, which could be perceived as short-term behaviour by rates in the emerging markets have a deep understanding

those from the western world. of local customer problems. Both have different strengths

Second, purchasing power is often orders of magnitude to excel at reverse innovation. Combining these assets

lower in emerging markets whereas the savings rate is through strategic alliances among these key players may

higher. This limits the ability of local consumers to absorb be the answer to success, particularly if they can also

the cost of breakthrough R&D. combine a frugal technical solution with a smart business

Third and finally, consumers in emerging markets often model, which can create a strong sustainable competitive

have special needs and, hence, any product or service advantage.

features that are added are usually idiosyncratic, often As Vijai Govindarajan commented: “If multinationals

low-cost and almost always highly impactful. ignore reverse Innovation, they are likely to get disrupted.

As a result, the western approach to innovation has We have seen this happen in the 1970s and 1980s when

worked well in the business-to-business arena, where the Japanese companies disrupted Detroit [the US auto-

quality and performance requirements are high, and rea- motive industry].”

sonably well with luxury consumer goods and certain prox- The same was true for the Swiss watch industry, which

imity-dependent services. reinvented innovation to gain its leadership in the 21st cen-

For most other industries and direct consumer-facing tury after being almost dismantled by the Japanese elec-

businesses, premium prices are harder to command and tronic watch revolution in the 1970s.

maintain, hence making them vulnerable to emerging Going forward, the statement of GE’s Jeff Immelt, “reverse

market competitors. The reason for this is that emerging innovation isn’t optional, it’s oxygen”, should therefore be

market layers are often adept at reducing complexity, pro- seriously considered by most multinationals that want to

Global Corporate Venturing July 2013 37Analysis

stay ahead of the curve not only in emerging markets but tive with Bain & Co (e-mail: bbattistini@ethz.ch)

also in mature markets. n

Martin Haemmig is an adjunct professor at CeTIM at

Boris Battistini is a research associate at ETH Zurich and a UniBW Munich and Leiden University (email: martinhaem-

project leader of the Corporate Venturing Research Initia- mig@cetim.org)

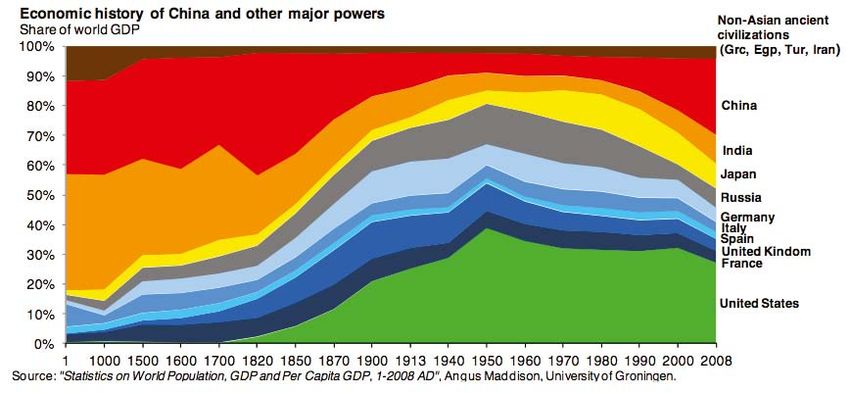

2000 years of economic history of the major powers

Drivers, evidence and cases for GDP pendulum swings back in favour of emerging markets

emerging market innovation for Share of

world GDP

the rest of the world 100%

Non-Asian ancient civilisations (Greece, Egypt, Turkey, Iran)

China

90%

India

80% Japan

In year 1, India and China were home to one- 70%

Russia

third and one-quarter of the world’s population 60%

Germany

respectively and thus also commanded two- 50% Italy

thirds of the world’s economy. The industrial Spain

40% UK

revolution(s) changed all that. Today, the US France

30%

accounts for 5% of the world population and

20% US

21% of its GDP. Asia ex Japan accounts for

10%

60% of the world’s population and 30% of its

GDP. Asia’s growth will now be driven by its 0%

1 1000 1500 1600 1700 1820 1850 1870 1900 1913 1940 1950 1960 1970 1980 1990 2000 2008

huge population and its increasing wealth. www.MartinHaemmig.com / 2013 © Source: Statistics on World Population, (01-2008); Angus Maddison, Univ of Groningen

Global R&D flows between advanced and developing nations

Number of new R&D centres to/from advanced (A) and developing (D) nations

Data available for 2,080 R&D units (by 2010) 180

By 1970 there were 243 established R&D units 243 units established before 1970

160

by MNCs, rising to 2,080 units by 2010, with the

Two-thirds of all units are international, one-third are domestic

number of new R&D centres peaking in 2005 Expand from 31 countries into 78 countries (1970-2010)

140

Number of new R&D centres

at about 160, before the financial crisis brought D D 120

Peak in 2005

it down to 90. Over the past 40 years, about Height of economic boom (#160 new centers)

D A 100

two-thirds of MNC R&D centres are outside A D

Data sources A A 80

their HQ nation, while one-third is domestically 450 of 1000 largest R&D companies (Fortune 1000)

based. In future, developing nations will take a 60

Data sources

bigger share in global R&D, both as hosts and Data sources: UNCTAD and OECD

40

as sources for R&D centres worldwide. 20

0

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

www.MartinHaemmig.com / 2013 © Source: GLORAD-Database www.glorad.org / Max von Zedtwitz

The days where advanced market players Needs in emerging markets require new solutions

leveraged the emerging markets as product Emerging market innovation to both other emerging markets and mature markets

lifecycle extensions with ageing technologies GE-India: Mac 400 ECG machine: for rural India

Designed in India for India’s rural

Tata Motors-India: Nano Nano: emerging market city car

Made and sold in India, the Nano is

and solutions are over. The next phase with market and launched in 2007 for US.

$1,000, this portable cardiac testing

the cheapest car in the world today.

Before it went on sale, a price of

device was developed in only 22 $2,000 was widely touted. Since its

stripped down lower-cost versions – still used months for $500,000 with off-the-

shelf components. Each test cost

2009 debut, the price is now $2,600.

Nevertheless, the Nano remains the

by many international players – is underAnalysis

Are partners worth more

than the sum of their firms?

Most venture capital (VC) firms will

define one of the core competences

as the ability to identify and develop

In our series of articles

high-potential start-ups, so as to cap- Corporate Venturing on

ture value from an exit. However, the Test Bench,

there is a significant difference in fund

performance between the top quartile Boris Battistini and

and other VC funds. Such differences Martin Haemmig

are even more interesting when con-

sidering that about 85% of financial

review and analyse

returns are the result of only 10% of the latest trends

investments.

What determines the ability of VC

firms to generate value from venture investing consist- on delivering below par.

ently? Empirical research in finance and entrepreneurship Several studies on venture capitalists highlight the

seems to point to superior dealflow, industry knowledge or importance of personal traits, often referred to as skillset

networks of high-performing VC firms. or intangible quality. This study confirms that it is not nec-

However, a recent research study published by Carn- essarily the brand name of the VC firm that attracts better

egie Mellon and Harvard academics examines the extent business plans – although this may be the case – but a

to which the variation in performance depends on a VC strong sense and intuition on the part of the individual VC

firm’s organisational capital or the skills of investment pro- who smells the deal, which encompasses market opportu-

fessionals that work for the firm. nity, technology or solution, and the right team to execute

To this end, Michael Ewens and Matthew Rhodes-Kropf it during the early days of the start-up.

examined consistency at the individual partner investment

level using a “unique dataset that tracks the performance of The implications for corporate venturers

individual venture capitalists’ investments across time and

as they move between VC firms”. They covered venture

investments from 1987 to 2012 – 27,079 financing rounds

in 16,897 start-ups financed by 3,777 investing firms.

1 Staffing and processes: Corporate venturers (CVs)

tend to assemble their teams with internal people.

Hence there is a high likelihood that a number of the

The study found evidence of individual VCs have repeat- required skills are missing when dealing with start-ups.

able investment skill, even after controlling for observable This is particularly critical for corporations that set up a CV

characteristics such as time, industry, dollars invested, team with no experienced VC or CV member.

VC experience, investment round number, firm founding

date and other factors. In particular, the study found “evi-

dence of skill and exit style differences even among ven-

2 VCs converting to CV: With a currently shrinking VC

industry in mature markets, some successful VCs are

hired to CV teams. Historically, many CVs have become

ture partners investing at the same VC firm at the same VCs, creating a brain drain, but this is now reversing, lead-

time”. Furthermore, their estimates suggest the partner’s ing to brain circulation. This is particularly true in emerg-

human capital is two to five times more important than the ing markets, where there is a need to assemble new CV

VC firm’s organisational capital in explaining performance. teams and processes from scratch. The following global

The authors also noticed a persistent pattern related sample includes:

to the performance of individual VCs, irrespective of the l US: George Hoyem moved from Blueprint Ventures to

firm in which they were involved. Top performers with sig- In-Q-Tel, Central Intelligence Agency-backed venture firm.

nificant initial public offerings (IPOs) continued to deliver l US: Sue Siegel moved from MDV to GE Ventures

again and again, while their underperforming peers kept (Healthymagination).

Global Corporate Venturing August 2013 17Analysis

l Europe: Jonathan Tudor moved from CodyGate to BP Companies receiving added value from VCs

Ventures.

l India: Akhil Awasthi moved from Baring Private Equity

India to Tata Capital’s growth fund.

l China: Shaohui Chen, moved from WI Harper in Beijing

to Tencent in Shenzhen.

l Korea: Young Sohn, moved from Silver Lake to Sam-

sung Electronics in California’s Silicon Valley.

3 Long-term venturing: Building a personal network

takes a VC two to three years, not only to source deals

but to establish a solid deal generation pipeline combined

with a co-investment network and an exit platform. Several

Asian CVs tend to rotate people globally every three to

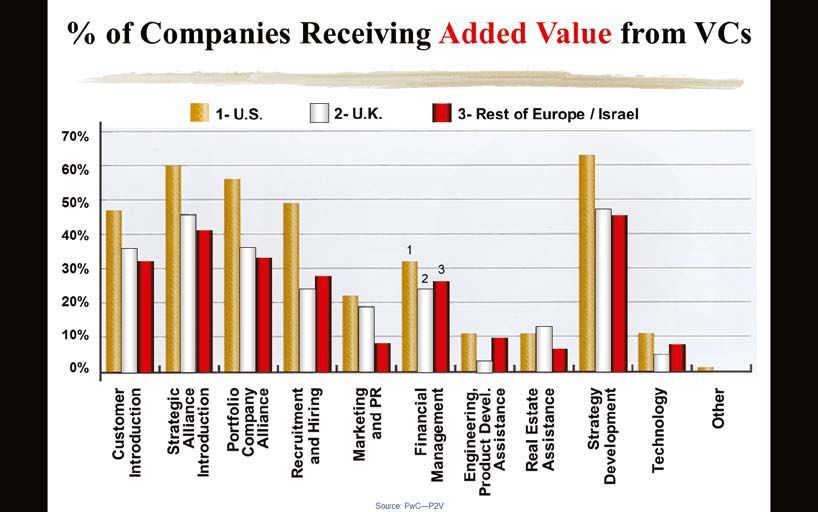

four years. Hence it is difficult for them to have significant Source: PwC – Paths to Value (on 350 early-stage companies) 2002

impact and results. Since a lot of deals are financed from

Consultant PricewaterhouseCoopers surveyed senior managers at 350 VC-backed

the corporate parent’s balance sheet, there are no hurdles companies in the US, Europe and Israel from 1999 to 2001. Of more than 10 vari-

to a CV investment professional changing positions or firm ables, the top five require lots of experience and a vast network, often beyond the

reach of an early-stage start-up. This is the value VCs and CVs can provide.

at any time. In contrast, typical VC fund structures include

such hurdles – key-man clauses, for instance – which

makes it difficult to leave the VC firm. Most important human capital for a VC profile

4 Compensation for CVs: This has been a long-term

issue, so many CV funds are restructuring to enable

third-party investors to contribute the majority of the fund

volume while the corporate parent remains a minority

anchor investor. This forces these funds to deliver solid

returns and VC-like compensation. Some global examples

include:

l US: Microsoft Ventures

l Spain: Amérigo (Telefónica)

l Switzerland: Zuehlke Ventures

l UK: Inventages (Nestlé, Switzerland) % %

l Japan: Itochu Ventures Source: Dr Martin Haemmig (compiled) / Data: Journal of Private Equity – Fall 2000 (pp7-29)

l China: Hony Capital (Legend Holdings/Lenovo)

l India: Tata Capital There are 17 important skills required by VC investment professionals. Of the top

10, eight are soft skills. Hence it is all about people and people skills. Finance and

As highlighted by the Ewens/Rhodes-Kropf study, the accounting knowledge are necessities but are least critical.

factors driving superior deal performance are primarily the

result of the personal skills, capabilities and strong sense Typical profile of successful US venture capitalists

for the right deals by individual VC partners, and less (145 VCs in 98 VC firms, 42% West, 38% East, 20% others)

with the brand name of the VC firm. To be in a position to

Education / schools

attract and maintain such exceptional talents, corporates 83% BA/BS, 17% MA/MS, 67% MBA, 14% PhD/MD (84% => 1 technical degree)

with CVC programs/teams are well advised to consider the 36% Harvard, 20% Stanford, 7% Wharton, 4% Chicago & Columbia, 29% others

above mentioned structures and compensation, in order to Career background (not mutually exclusive)

34% corporate manager, 32% banking/finance, 30% entrepreneurs, 24% consulting,

create stellar teams for the long-term. n 18% marketing, 16% technologists, 10% sales, 6% manufacturing

Business experience

Reference: Ewens, M and Rhodes-Kropf, M (2013) ‘Is a 26% > 15yrs, 16% 11-15yrs, 36% 4-10yrs, 15% 1-3yrs, 4%Analysis

On the role and value

of business models

The role of business models has

recently received considerable atten-

tion both in practice and academia. In

In our series of articles

this article we briefly review the cur- Corporate Venturing on

rent debate and highlight a number the Test Bench,

of interesting insights regarding the

value of business models and the pur- Boris Battistini and

pose they serve. Martin Haemmig

What is a business model? While

there is, surprisingly, no consensus

review and analyse

on how to define a business model, the latest trends

most studies appear to agree that it is

the construct that conceptualises how

firms generate, deliver and capture value – the model that In today’s world, where product lifecycles may often

explains how financial value can be extracted from a tech- have only a few months of shelf-space – particularly in the

nology, product or service. consumer, mobile and internet products, service and solu-

In particular, the business model depicts how a firm tions sector – business models are often at the core of it.

makes money by specifying where it is positioned in the Large corporations and corporate venturers are well

value chain and determines the design of the content, advised to learn from young start-ups, since they often

structure and governance of economic transactions so tend to follow and understand the needs of their friends

as to generate value through the exploitation of business in the same age bracket. This is particularly true in the

opportunities. In so doing, it specifies the value proposi- emerging markets, where western internet companies

tion, the partners and channels through which value is have often failed, particularly in China.

generated and delivered, and the revenue model. Chinese companies typically look at some existing tech-

An interesting set of research studies by Doganova of nologies, re-engineer it and add local features and include

Mines ParisTech and colleagues suggest that the design local services, and add a completely new business model

of models is particularly important for the development on top, which has little to do with western revenue models.

of entrepreneurial ventures. In fact, “the business model This is particularly true in the area of e-commerce – Ali-

works as both a calculative and a narrative device. It baba vs eBay – and in mobile gaming – Tencent, Shanda

allows entrepreneurs to explore a market and to bring their and others. By investing as a corporate venturer in innova-

innovation – a new product, a new venture and the net- tive local start-ups, large foreign and local corporates can

work that supports it – into existence”. It is suggested that prevent very, very costly mistakes, while such investments

business models can be therefore be fruitfully analysed as may lead even to potential acquisitions or a new distribu-

“market devices” that play an important role in the interac- tion channel, in order to get rapid access and traction in

tions with business partners and investors. the market.

Management scholars “found that the stock market con- When considering an investment in a young and inno-

sistently values certain types of business models more vative company, financial backers, mentors and coaches

highly than others. Specifically, [the study] found that in should assist the entrepreneurs in the following three

recent years, investors have favoured business models questions – why, when and how?

focusing on licensing intellectual property – such as Goog- Why an analysis of the business model? On the one

le’s business model – and a certain kind of highly innova- hand it provides a guide for the entrepreneurs in the defi-

tive manufacturing – such as Arduino’s rapid prototyping or nition of all the parameters related to the future business

the largest 3D-pinting companies: 3D Systems, Stratasys and its activities right from the beginning of the business

and Exone”. creation project. On the other hand it provides a useful

Global Corporate Venturing September 2013 21Analysis

tool for investors to help entrepreneurs prepare the crea- model must evolve constantly over the various stages of

tion of their businesses, notably in the communication with the company’s development, and structure relations with

the project’s stakeholders. business stakeholders and decision-makers.

When should the business model analysis start? As How can entrepreneurs be helped in the development

soon as the business idea has been identified, entrepre- of their business models? Financial backers and men-

neurs should start building their business model. The tors and advisers should assist in building and testing the

results of the work on the business model will end up being business models. It is in their own interest to understand

formalised in the company business plan. The business the foundation of the company, which they are trying to

help and end up investing in. The

THE BUSINESS MODEL FRAMEWORK business model is becoming a cen-

Our business model framework defines the types of assets a company sells and the rights tral element in optimising the way

it grants customers to use those assets. We classified all the companies listed on US entrepreneurs and their projects

exchanges into the framework by identifying the percentage of their revenues generated progress in tight collaboration with

through one or more of the business models. their investors, in order to improve

Share of total the chances of business success.

Asset type revenue of

US-listed firms In today’s increasingly global,

Financial Physical Intangible Human complex and competitive world,

Manufacturer companies looking for profitable

Creator N/A* sustainable growth need constantly

0% 57% 0% 57%

to invent new competitive advan-

Financial Wholesale/ tages. Innovation brings differentia-

Distributor trader retail N/A*

AssetYou can also read