COVER STORY THE CHAIRMAN'S AWARD WINNERS - The newsLINK Group

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

HOMETOWN

PUB. 2 2020 ISSUE 7

hometownbanker.org

BANKER

COVER STORY

THE CHAIRMAN’S

AWARD WINNERS

PAGE 4

PLANNING FOR THE FUTURE:

COMMUNITY BANK LESSONS

FROM THE COVID-19 PANDEMIC

PAGE 20

PACB EDUCATION:

CONNECTING

BANKERS IN

UNCERTAIN TIMES

PAGE 24

THE PUBLICATION CELEBRATING AND EDUCATING PENNSYLVANIA’S COMMUNITY BANKING INDUSTRY. POWERED BY

WE’LL NEVER

BE THE SAME.

As a strategic partner to more than 140 banks,

we never stop working to adapt to change,

quickly and efficiently.

As the world experiences unprecedented changes, history shows that change is more

often the rule than the exception. The same can be said for the world of banking. And when

it comes to changes in banking, you can rely on S.R. Snodgrass. As The Banking Experts,

we’ve worked only in banking, every hour of every day, every week of every month, for

more than 70 years. In fact, no other accounting and consulting firm possesses greater

knowledge of community banks’ needs, challenges, and opportunities than S.R.

www.srsnodgrass.com/banking Snodgrass. Which is why, in a world that continually changes, we’ll never be the same.

(833) 404-0344 If you think our unrivaled banking expertise and personalized service could benefit your

bank, please allow us to introduce ourselves. We’d be delighted to meet you.

HOMETOWN

PUB. 2 2020 ISSUE 7

BANKER

PACB HEADQUARTERS BUSINESS HOURS

3 15 3211 N. Front Street,

Suite 102

8:30 a.m.-5:00 p.m.

Monday through Friday

Harrisburg, PA 17110 Telephone: 717.231.7447

www.pacb.org

STANDING COMMITTEES

2020 EXECUTIVE CHAIRS AND VICE CHAIRS

COMMITTEE

26

Education

Chairman Edward Martel

Jon P. Conklin Jonestown Bank and Trust Co.

Woodlands Bank Wendy Nagle

PennCrest BANK

Chair Elect

Lori A. Cestra Finance and Budget

Enterprise Bank Timothy P. Snyder

Fleetwood Bank

Vice Chairman

Roger A. Zacharia FIRSTPAC

Ambler Savings Bank Chuck Leyh

2 A Word From PACB’s Chairman Enterprise Bank

Secretary/ Treasurer

Legislative

3 From the President/CEO’s Desk Timothy P. Snyder

Chuck Leyh

Fleetwood Bank

Enterprise Bank

4 The Chairman’s Award Winners President/CEO

PACB Foundation

Kevin L. Shivers

Andrew W. Hasley

12 Hometown Champions PACB

Standard Bank, PaSB

Terry L. Foster

Immediate Past Chairman

15 Nextgenu Graduate Jordan Zook Earns Promotion at the Bank of Bird-In-Hand Troy M. Campbell

MCS Bank

Altoona First Savings Bank

16 Insured Cash Sweep® And Cdars ® : A Game Changer for Banks and

PACB STAFF Thomas Ondek

Local Communities Sewickley Savings Bank

President/CEO

18 Now Is a Great Time to Check Flood Compliance Policies and Procedures Kevin L. Shivers

PACB SOCIAL MEDIA

kevin@pacb.org

Twitter: @PaCommBankers

20 Planning for the Future: Community Bank Lessons From the COVID-19 Pandemic SVP Strategy and

Facebook: @PaCommBankers

Operations

Instagram: @PaCommBankers

21 Linkbank President Brent Smith Earns National Recognition as a 40 Under 40 Barbara W. Holbert

barbara@pacb.org

LinkedIn: PACB – Pennsylvania

Association of

Emerging Community Bank Leader Community Bankers

Director of Government

YouTube: PaCommunityBankers

Relations

24 PACB Education: Connecting Bankers in Uncertain Times Allison L. Coccia

Flickr: PaCommunityBankers

allison@pacb.org

25 What Lenders Need to Know About Paycheck Protection Program ADVERTISING SALES

Executive Assistant

Loan Forgiveness to the President To advertise in Hometown Banker,

Jena I. Wolgemuth please contact

Louise Killpack at

26 PACB Joins ICBA and State Banking Groups to Urge Congress to Pass Key jena@pacb.org

The newsLINK Group, Inc.

Reforms in Next COVID-19 Relief Plan Director of Marketing, Public louise@thenewslinkgroup.com

Relations, and Membership or 801.676.9722

28 Turn 2020 Pain Into 2021 Profit With One Simple Strategy Todd F. Willman

Todd@pacb.org

©2020 Pennsylvania Association of Community Bankers (PACB) | The newsLINK Group, LLC. All rights reserved. The Hometown Banker is

published 12 times each year by The newsLINK Group, LLC for the PACB and is the official publication for this association. The information

contained in this publication is intended to provide general information for review, consideration and education. The contents do not

constitute legal advice and should not be relied on as such. If you need legal advice or assistance, it is strongly recommended that you

contact an attorney as to your circumstances. The statements and opinions expressed in this publication are those of the individual authors

and do not necessarily represent the views of the PACB, its board of directors, or the publisher. Likewise, the appearance of advertisements

within this publication does not constitute an endorsement or recommendation of any product or service advertised. The Hometown Banker

is a collective work, and as such, some articles are submitted by authors who are independent of the PACB. While the Hometown Banker

encourages a first-print policy; in cases where this is not possible, every effort has been made to comply with any known reprint guidelines

or restrictions. Content may not be reproduced or reprinted without prior written permission. For further information, please contact the

publisher at 855.747.4003.

Member and Associate Member subscriptions, $60 per year. All other subscriptions, $84 per year. Please send address changes to PACB,

Attention: Hometown Banker, 2405 North Front Street, Harrisburg, PA 17110-5319. HOMETOWN BANKER | HOMETOWNBANKER.ORG | 1

A WORD FROM PACB’S CHAIRMAN

By Jon Conklin

B

efore the onset of the

COVID-19 pandemic, our

industry was preparing to

celebrate National Community

Banking Month during April. Normally,

I would encourage anyone who has not previously been

this is a month dedicated to showcasing involved in these efforts to get involved, and those who

community banking’s history, as well as

its unique role in communities of all sizes have been involved, to stay involved.

across the country. This year, through

utilizing marketing opportunities and

hosting community events, we stepped

up during a crisis. We demonstrated in

environment that is conducive to the ongoing legislative and public relations arenas, the in-

real time the vital role that we play and

vitality of the industry given the ever-evolving dustry risks continuing to be unfairly painted

how we are different from our larger

landscape of banking and customer expecta- by the broad brush of public perception and

competitors in the financial industry.

tions. The legislative victories of the past and punished through legislative measures aimed

National Community Banking Month, the battles currently being fought have been at protecting consumers from practices in

while significantly different from years and will continue to be of utmost importance. which we never have nor would engage.

past, still served as a month that shone a Our industry advocates at the state level

spotlight on our industry and our positive (PACB) and at the national level (ICBA) are Our efforts through the pandemic and

impact on economies and communities the only ones on the front lines fighting solely economic crisis have not gone unnoticed by

across the country. for our unique interests as community banks. consumers, the business community and

legislators, and the time is right to continue to

During July, PACB celebrated the communi- While the trade associations do an outstand- fight for a regulatory and legislative environ-

ty-focused efforts of its member banks across ing job of fighting for community banks ev- ment that ensures our industry’s continued

the Commonwealth with its aptly named IM- ery single day, they cannot truly be successful success. I have been beyond impressed by

PACT Awards. As part of the three Regional without our involvement as individual banks the passion, diversity and talent across our

Meetings, which were rescheduled from and bankers. Only through our continued membership and humbled by the opportunity

March and converted to a virtual format, monetary contributions to FIRSTPAC and to serve as your chairman for the 2019-2020

the individual efforts of member banks were ICBPAC, combined with the donation of our term. Let’s all commit to remaining engaged

highlighted, and the impact that these efforts time and our voices to the advocacy effort in our communities and in our industry in or-

had on communities were recognized in in Harrisburg and Washington, D.C., will der to ensure the mutual success of all.

bestowing the IMPACT award. These awards success be ensured. There are plenty of op-

demonstrate how Pennsylvania community portunities for all of us to get involved and to

banks continue to be the foundational pres- have our voices heard by the legislators who

ence and trusted partner for success in every ultimately shape the policy that impacts our

community in which they operate. Also, these prospects for success on a daily basis. I would JON CONKLIN IS

CHAIRMAN OF PACB

individual illustrations of the critical role encourage anyone who has not previously AND PRESIDENT/CEO OF

played by community banks further cement- been involved in these efforts to get involved, WOODLANDS BANK IN

WILLIAMSPORT, PA.

ed for me the importance of the role played and those who have been involved, to stay in-

by PACB in the legislative arena, advocating volved. Without the sustained and resound-

for a level playing field and a regulatory ing presence of our collective voices in the

2 | HOMETOWN BANKER | HOMETOWNBANKER.ORG

FROM THE PRESIDENT/CEO’S DESK

By Kevin L. Shivers, CAE

G

reetings! Banking is an honorable profession and are an important moment in time when

PACB is proud of the powerful role that community bankers can celebrate their

This month’s Hometown our community bankers play year-round accomplishments and learn how others

Banker magazine celebrates the to support homeowners, local businesses, are serving their communities. In the

many ways that community bankers support schools, charitable groups and houses process, we tell the powerful story of the

their local communities, including reflections of worship. community banking difference.

from our IMPACT award winners whom

we celebrated this month during our virtual This month we also celebrate LINK Bank Turning to policy, Congress is currently

region meetings. President and CEO Brent Smith, who debating another relief package coined

recently was recognized among the nation’s CARES Act 2.0. PACB has actively engaged

While the COVID pandemic prevented us 40 emerging bank leaders under 40 by ICBA’s Pennsylvania’s Congressional delegation

from gathering in person last March, during Independent Banker magazine. Brent lives the in support of provisions to create an SBA

Community Banking Month, to celebrate community bank philosophy every day, and forgiveness calculator and simplify PPP

the many achievements by banks and their its rewarding to see Brent recognized for his forgiveness forms and the forgiveness process,

employees who make our communities great contributions to the community. including a presumption of compliance for

places to live, work and raise families, it borrowers whose loans were $150,000 or

was great to celebrate these efforts virtually Finally, Hometown Banker magazine less. Among other provisions currently under

during our region meetings. recognizes Jordan Zook, a recent graduate debate is a liability safe harbor for businesses

of PACB’s NextGen“U” leadership program facing COVID-19-related lawsuits.

SSB earned PACB’s Region 1 Chairman’s who was promoted to credit manager

Award for involving all of its bank employees at the Bank of Bird-in-Hand. Jordan’s Here in Harrisburg, PACB continues its

in unique activities to support business and participation in the online management negotiations with the Wolf administration

economic growth in their communities. training program was made possible by and the Department of Banking and

Riverview Bank earned PACB’s Region 2 a $1,500 scholarship he earned from the Securities for legislation that would protect

Chairman’s Award for three community PACB Foundation. the state’s banking fund from future raids

service projects involving over 300 employers by governors and legislatures.

in 36 offices across 14 counties. Harleysville Embedded inside thousands of annual

Bank earned PACB’s Region 3 Chairman’s financial transactions, community bank Thank you for your many efforts to

Award for its annual giving campaign in which customers know the community bank make your hometown stronger. PACB

120 bank employees helped to raise $42,886, experience is very different. These loyalists stands ready to assist you with education,

which was matched 100% by the bank for a developing professional opportunities

speak of loyalty to people. Customers

total of $85,772 and distributed to 57 local and legislative advocacy to help you

will wait in line for a specific teller.

make a positive impact on the lives of the

nonprofits in the surrounding communities. Daily exchanges involve first names, and

customers that you serve.

the unhurried pace of transaction was

Virtually every Pennsylvania newspaper appreciated. There is stability in each

has covered the extraordinary response bank’s roster of employees. Empathy and

by community banks to the COVID-19 understanding go beyond a call-center

pandemic, especially the work community representative or a customer service manual.

KEVIN SHIVERS IS

bankers did to process the lion’s share of PRESIDENT/CEO

Paycheck Protection Program loans in our While community bank customers know OF PENNSYLVANIA

state. Our community bankers work hard their banks are generous and deeply ASSOCIATION OF

COMMUNITY BANKERS.

every day to help their local entrepreneurs and connected to their communities, sometimes

community leaders build vibrant communities the efforts of their institutions largely go

where families want to live, work and play. unpublicized. The PACB region meetings

HOMETOWN BANKER | HOMETOWNBANKER.ORG | 3

THE CHAIRMAN’S

T

he PACB IMPACT Awards entrepreneurs and community leaders build you invest in us, you are helping us to

are meant to recognize the vibrant communities where families want continue to invest in the community.”

incredible and varied ways that to live, work and play. Employees are serious about supporting

community banks breathe life their community. They do everything

into the neighborhoods they serve. The The Chairman’s Award winners for the they can to take action and get involved

IMPACT acronym stands for the following: three regions are described below. because they know their efforts grow the

Implementing Meaningful Projects and economy, support worthy organizations

Activities to help build stronger Communi- and improve community relationships.

REGION 1: SSB BANK • In 2019, SSB launched its Business

ties for Tomorrow.

SSB earned PACB’s Region 1 Chairman’s Spotlight Series that provided a

Banking is an honorable profession, and Award for its unique activities to support platform for small businesses to

PACB is proud of the powerful role that our business and economic growth in their share their success with the local

community bankers play to support local communities. Further, SSB’s efforts community. The bank profiled five

businesses, schools, charitable groups and involved all of their bank employees local businesses and promoted their

houses of worship. Our community bankers across two branches. The bank’s website success across a variety of platforms,

work hard every day to help their local identifies the bank’s philosophy: “When including publishing articles in the

4 | HOMETOWN BANKER | HOMETOWNBANKER.ORG

AWARD WINNERS

bank’s community newsletter, sharing the stories on the bank’s makes it easier for Caleb to “live life and enjoy it” despite

website, and engaging a broader conversation on social media. his physical limitations and communication difficulties.

• SSB proudly served as the main sponsor for Pittsburgh • SSB staff collected donations from bank employees in support

Community Television’s Greater Pittsburgh Community of a bookbag drive for homeless students living in shelters

Media Awards to celebrate local achievements in community throughout the Pittsburgh region.

television that showcased activities throughout Bethel Park • SSB partners with the Federal Home Loan Bank of Pittsburgh

and Moon Townships in Allegheny County. and its Home4Good grant program.

• SSB underwrote the purchase of communications

• SSB assisted in funding a $100,000 grant to allow the

equipment for children with disabilities, supporting the

Allegheny County Community Health services chapter to

mission of a local charity called Variety — the Children’s

double its outreach to local families and individuals struggling

charity. Employees were given the chance to donate a small

amount of money from each paycheck. In exchange for the with behavioral health disorders.

donation, employees wear jeans each Friday. For 2019, SSB

bought an iPad for a 4-year-old boy named Caleb, and gave If you want to see the impact that SSB’s programs are having,

it to him and his family (including his siblings, parents and consider Caleb, whose story was discussed previously. In

grandparents) at a celebration held July 25, 2019. The iPad CONTINUED ON PAGE 6

HOMETOWN BANKER | HOMETOWNBANKER.ORG | 5

“The grand opening was a real team effort, a great marriage between

two like-minded community banks,” said Tom Bailey, president and CEO at

Brentwood Bank. “Thank you, PACB, for this recognition.”

CONTINUED FROM PAGE 5 helping Caleb. He said, “Every year, we thought we had to wait

particular, Caleb’s parents and the bank’s president all expressed until Christmas to do sponsorships and to sponsor a family.

their appreciation for the iPad Caleb received. Kevin, Caleb’s Fortunately, in 2018 we found Variety, and the bank was able to

father, said, “We appreciate all the sponsors and we feel blessed do something [during the year] … [This] past year, we were able

to be a part of this program. Certainly, it will help Caleb to live to give a voice to a child; it is just a no-brainer. We live for this.

life and enjoy it, so we are really grateful.” We love to give money out of our paychecks to wear jeans so

that we can do things like this. We are proud. We are excited.

Caleb’s mother, Crystal, said, “He has been working a lot with Congratulations.”

the iPad in his speech program both in school and in outpatient

therapy. It will be nice for him to have this [iPad] at home for him Initiatives like this and the others described previously are what

to practice his skills [and increase his vocabulary]. He has come make SSB Bank stand out from the other financial institutions

a long way, but this will continue to help him improve with his out there. SSB Bank is an institution that puts its mission

speech. We are so thankful for the program and all of the sponsors. and values into action for the communities it serves. Each

You make it all happen.” project SSB Bank participates in or leads holds significance,

and bank employees look forward to continuing to serve their

Dan Moon, the president and CEO of SSB, represented the communities in the coming months and years, especially during

bank and its employees when he spoke about the impact of these trying times.

6 | HOMETOWN BANKER | HOMETOWNBANKER.ORG

REGION 2: RIVERVIEW BANK • Riverview Bank’s My Perks Plus Mania Program fostered

engagement opportunities for consumers with local

Riverview Bank and its operating divisions, CBT Bank and business customers of the bank. The program highlighted

Citizens Neighborhood Bank, earned PACB’s Region 2 Chairman’s many valuable merchants and provided Riverview Bank’s

Award for three community service projects involving over 300 communities with opportunities to thrive.

employers in 36 offices across 14 counties. • Lastly, Riverview Bank’s American Heroes Checking

• In December 2019, Riverview delivered more than Account and Community Advocacy Program for veterans,

$57,000 to over 55 giving missions as part of the bank’s active military and first responders provided these customers

Operation: Community Spirit project. Every bank with valuable benefits including identity theft protection,

employee was empowered to donate at least $75 to a local cellphone protection, roadside assistance and prescription

cause they felt passionate about. The bank also allowed benefits. The account being offered has the same benefits

each employee two hours of giving mission volunteer time as the Protect PLUS Checking, which is the bank’s most

to support local nonprofits. Riverview Bank employees prestigious account, but offered at a discounted monthly

contributed over 550 hours in less than 20 days to various fee. As well, the bank also delivered over $15,000 in local

causes, including delivering Christmas to two 3-year- appreciation breakfasts, dinners and other events to honor

old twins, one of whom was awaiting a new heart at local VFWs and fire departments; these events celebrated the

Pittsburgh’s UMPC Hospital. CONTINUED ON PAGE 8

HOMETOWN BANKER | HOMETOWNBANKER.ORG | 7

CONTINUED FROM PAGE 7

lasting impact of courageous American heroes who protect

and support our local communities.

Brett D. Fulk, president and CEO of Riverbank, summarized

the value of the Operation: Community Spirit program when he

spoke about what the bank did in 2019: “Operation Community

Spirit is a community-impact initiative that our entire team looks

forward to annually. It is wonderful to see the genuine interest

and excitement that stems from each of our employee’s giving

missions. I personally have an immense amount of pride for the

efforts our almost 300 employees collectively put forth to support

their local hometown while creating a huge impact together across

our large marketplace.”

REGION 3: HARLEYSVILLE BANK

Harleysville Bank earned PACB’s Region 3 Chairman’s Award

for its annual giving campaign, held each November. In 2019,

120 bank employees in seven offices or branches helped to raise

$42,886 for local nonprofit organizations. Team members

selected the local nonprofits they wanted to help and then they

made a pledge. This amount was matched 100% by the bank for

a final total of $85,772.

Harleysville Bank distributed the money to 57 local

nonprofits in the surrounding communities. For 2019, it was

only possible to present one “big check” in person. That one

check was presented to the North Penn Valley Boys & Girls

Club. (Unfortunately, COVID-19 made it impossible to get

group photos of the other “big check” recipients.)

Brendan McGill, president and CEO, stated, “This was truly

a team effort; through our team members generosity they have

created value for our community. I’m proud of our team and the

commitment they have to helping others, providing support and

strengthening the communities we serve and live in.”

How does Harleysville Bank select organizations and events to

receive donations? The bank uses the following criteria:

• The organization or event has to be local (that is, within

the service area for Harleysville Bank). It also has to benefit

residents.

• The organization, and the number of people being served,

both have to be credible.

• Whether the organization has received help previously.

• The relationship between bank employees and those

involved in the organization or event.

• Whether the organization is nonprofit and tax-exempt, or

whether it is a public service organization or institution.

• Organizations that provide community development,

education, housing and youth services.

Bank leaders are careful about which organizations they choose.

They make its selections impartially, and not because of individual

personal requests. They avoid political organizations, especially

if they are involved in elections or lobbying. They do not

support discriminatory organizations. Finally, they only support

organizations that have legal, ethical and safe activities.

8 | HOMETOWN BANKER | HOMETOWNBANKER.ORG“This is an organization that we really believe in, and adds

value to small businesses in the area.”

— Andy Hasley, president of Standard Bank.

HOMETOWN BANKER | HOMETOWNBANKER.ORG | 9“We hold these individuals very near and dear to our heart, and

showcase that by giving to them,” said LeeAnn Gephart, chief

marketing officer at Riverview Bank. “Operation Community

Spirit is very special to us because it not only creates an

impact in the 20 counties near us, it shows the integral part our

employees play in the lives of our communities.”

10 | HOMETOWN BANKER | HOMETOWNBANKER.ORG“Our team at Woodlands Bank packed over 500 boxes of

food for the Central Pennsylvania Food Bank.”

— Sara Kropp, marketing officer, Woodlands Bank.

HOMETOWN BANKER | HOMETOWNBANKER.ORG | 11HOMETOWN CHAMPIONS:

here. Our hearts and dreams are BIG when

it comes to the goals of the bank, as well as

our employees and customers.

PACB: TELL US SOMETHING ABOUT

YOURSELF THAT MOST PEOPLE

DON’T KNOW.

C

ommunities across Pennsylva- RACHELLE: On a personal level, one thing

nia are growing and thriving most people don't know about me is I love

because their community banks going to the dirt track races. I've gone ever

care. The service and commit-

ment demonstrated by community bank Rachelle Williamson since I was a little girl, because a lot of my

family races and now my fiancé races too.

employees keeps customers faithful, and On a work level, I've made a lot of friend-

their sincerity keeps others hopeful. It is be- ships throughout my career at CSB.

cause of these employees that communities

across the Commonwealth are thriving and

RACHELLE WILLIAMSON PACB: WHAT IS THE FIFTH PICTURE

becoming better places to live and work. TELLER IN YOUR CAMERA ROLL ON YOUR

PHONE, AND CAN YOU PLEASE

PACB: HOW DID YOU GET INTO

When it comes to community banking in SHARE THE STORY BEHIND IT?

Pennsylvania, the uniqueness, talent and at- COMMUNITY BANKING?

tributes of the 14,000 individual community RACHELLE: The fifth picture in my

RACHELLE: I started working in com- camera roll is my sweet fur baby on her

bank employees combine to make the entire

munity banking right out of high school. I first birthday. I made her pup cakes for her

industry greater than the sum of its parts.

enrolled in two accounting classes my senior big day. Her name is Zoey and she is a full

As we travel across Pennsylvania, we meet year and that's when I knew I wanted to Siberian husky. Her coat is rare, its called

community bank employees from many work in the banking field. When I got a call agouti. She has one brown eye and one blue

different backgrounds. Some are new to the for an interview, I already knew how CSB eye. She is the sweetest, craziest and most

industry, others have worked their entire operated because my family and I always beautiful puppy.

careers in it. No matter how long these banked there. I knew CSB was the career

employees have been involved in banking, for me because I enjoy working for a family

they all share a common thread – a love for based business and I knew I would do well

their community. They truly are the ones with all of the accounting aspects of the job.

responsible for bettering their hometowns. I am currently a part-time teller and I've

been with the bank for a little over three

As part of an ongoing series, each month years now.

we will be featuring interviews with

these community bank employees, these PACB: WHAT IS THE MOST

“Hometown Champions.” Through these REWARDING ASPECT OF WORKING IN

interviews, we hope to gain some insight COMMUNITY BANKING?

into what makes the community banking

industry great in Pennsylvania. RACHELLE: Every relationship with our

customers is personal; they're not just a

This month, we chat with the hometown number. Our employer values us as em-

champions from Community State Bank ployees, as well as the customers. There is a

of Orbisonia. For 69 years, Community lot of room for growth with CSB, which is

State Bank has put their customers first by great for my long-term goals here.

creating financial opportunities for their

customers and supporting the communities PACB: PEOPLE ALWAYS WANT A

in which they serve. As Huntingdon Coun- DEFINITION OF “COMMUNITY BANK,”

ty's only locally owned bank headquartered WHAT’S YOURS?

in Huntingdon County, Community State

Bank remains committed to enhancing RACHELLE: Most people think small

long term value to their shareholders while when they think of community banking.

providing exceptional service to their cus- We may be small, but we have the oppor-

tomers and reinvesting in their community. tunity to know each employee who works

12 | HOMETOWN BANKER | HOMETOWNBANKER.ORGAMBER GERHOLT DENISE DOYLE

DEPOSIT OPERATIONS MANAGER LOAN OFFICER II

PACB: HOW DID YOU GET INTO PACB: HOW DID YOU

COMMUNITY BANKING? GET INTO COMMUNITY

BANKING?

AMBER: I became a customer at Commu-

nity State Bank when I was a young adult. DENISE: I began working

From the very first time I stepped foot in my at Community State Bank

local branch, I fell in love; at home, almost. my senior year of high

I was made to feel like I was among friends, school through a co-op

Amber Gerholt as though they truly cared about me as a

person, not just a customer. Fast forward to a

Denise Doyle program.

few years later when I was at a point in my life that I needed a job. I heard the PACB: WHAT IS THE

bank was hiring a part-time teller and decided I would give it a go. I thought MOST REWARDING ASPECT OF WORKING IN

my employment with the bank was just temporary. It was intended to buy me COMMUNITY BANKING?

some time to search for my true calling. Boy was I wrong! Here I am 11 years

DENISE: The most rewarding aspect in my job as a lender

and counting with a career that continues to bless me beyond belief.

in a community bank is financing someone’s first car or

PACB: WHAT IS THE MOST REWARDING ASPECT OF WORKING IN home and experiencing the excitement of the purchase with

COMMUNITY BANKING? my customers.

AMBER: I would have to say that the most rewarding aspect of working in PACB: PEOPLE ALWAYS WANT A DEFINITION OF

community banking is togetherness. When you work in a community bank, “COMMUNITY BANK,” WHAT’S YOURS?

you have the opportunity to build meaningful relationships with both cus-

DENISE: My definition of a “community bank” is one that

tomers and colleagues. It’s not just a job, it’s a passion to make a difference in

is involved and supports the community in various ways and

the lives of others, whether it’s balancing a checkbook, offering a solution to

provides policies that enable their employees to help their

a financial need or simply offering a warm smile to a passerby.

entire customer base, including the ones that are forgotten by

PACB: PEOPLE ALWAYS WANT A DEFINITION OF “COMMUNITY the larger banks.

BANK,” WHAT’S YOURS?

PACB: TELL US SOMETHING ABOUT YOURSELF

AMBER: Simply stated, a community bank is a financial institution that is THAT MOST PEOPLE DON’T KNOW.

locally owned and operated. On a deeper level, it’s an organization that knows

DENISE: Most people do not know that my desire initially

where its roots are and is dedicated to making decisions for its individual com-

was to attend school and become an X-ray technician. I’m

munities. Their priority truly is taking care of the people and areas they serve.

glad now that the cards fell the way they did.

They never have to explain what sets them apart because it already shows.

PACB: WHAT IS THE FIFTH PICTURE IN YOUR

PACB: TELL US SOMETHING ABOUT YOURSELF THAT MOST

CAMERA ROLL ON YOUR PHONE, AND CAN YOU

PEOPLE DON’T KNOW.

PLEASE SHARE THE STORY BEHIND IT?

AMBER: Hmmm … this is a hard one. I’m usually an open book, so there’s

DENISE: My three precious grandsons, ages 4, 6 and 8.

not much that goes unknown. When I first meet people, I’ve been known to

They fill my life with love and play.

use memory tactics to remember their name. These tactics have included, but

are not limited to, word associations, mental pictures and rhyming. Being

able to refer to someone by name is something I take very seriously.

PACB: WHAT IS THE FIFTH

PICTURE IN YOUR CAMERA ROLL

ON YOUR PHONE, AND CAN

YOU PLEASE SHARE THE STORY

BEHIND IT?

AMBER: My family and I enjoy

spending time in nature. We found

this cross on one of our recent hikes.

It was on the side of a ridge in the

middle of the woods. Envelopes had

been nailed to it. The envelopes ap-

peared to have handwritten messages

inside. It was a beautiful discovery

that evoked profound emotion. CONTINUED ON PAGE 14

HOMETOWN BANKER | HOMETOWNBANKER.ORG | 13CONTINUED FROM PAGE 13 corporate banking and I am so glad to laughing so hard and also challenged

be back with a banking family whose with life lessons. What an amazing

values, missions and visions come first speaker she was; if you haven’t seen her

before the numbers. you need to!

PACB: TELL US SOMETHING ABOUT

YOURSELF THAT MOST PEOPLE

DON’T KNOW.

KARLA: Well, if you haven’t known me

for long, you will quickly find out I love to

talk. There isn’t too much that people don’t

know about me.

Karla Shadle

PACB: WHAT IS THE FIFTH PICTURE

IN YOUR CAMERA ROLL ON YOUR

KARLA SHADLE PHONE, AND CAN YOU PLEASE

TRAINER/MARKETING SPECIALIST SHARE THE STORY BEHIND IT?

PACB: HOW DID YOU GET INTO KARLA: I was recently at a Women’s

COMMUNITY BANKING? conference where I saw Candace Payne

(Chewbacca Mom). I am telling you I

KARLA: I was fresh out of high school left there with my sides hurting from

working at my uncle’s little country store

and loving life. One day my grandfa-

ther took me in to meet the CEO of our

community bank at the time. I loved what

he had to share with me about banking

and decided to fill out an application.

About a week or so later I was called in for

an interview. Two weeks later, I started

as a part-time teller. My intentions were

to work in that profession until I got my

degree; however, when I graduated from

college, banking was already in my blood

and I never left.

PACB: WHAT IS THE MOST

REWARDING ASPECT OF WORKING IN

COMMUNITY BANKING?

KARLA: The most rewarding aspect is

knowing you are working for the customers,

the community, and at the end of the day

you have made a difference for them. So

many banks get caught up in profit mar-

gins, goals and deadlines that they lose sight

of the real reason banking exists in the first

place. Their main focus should be serving

the customers and having a part in serving

the local communities.

PACB: PEOPLE ALWAYS WANT A

DEFINITION OF “COMMUNITY BANK,”

WHAT’S YOURS?

KARLA: Community Banking is the

soul of banking. It’s the type of banking

that still values what is important for our

customers and communities. When you

don’t focus on those two valuable pieces

you wouldn’t succeed. I have worked in

14 | HOMETOWN BANKER | HOMETOWNBANKER.ORGNEXTGENU GRADUATE

JORDAN ZOOK

EARNS PROMOTION

AT THE BANK OF

BIRD-IN-HAND

their current position,” said Barbara Holbert, PACB’s senior vice

president for Strategy and Operations.

Jordan started as a credit analyst three years ago. With the help of

the PACB scholarship, Jordan believes he is prepared to take on the

added responsibility in his new role as a credit manager.

“NextGen‘U’ helped me to develop the important skills required to

be successful in a leadership role, and will enable me to excel in the

next phase of my career,” said Jordan.

Established in 1994, the PACB Foundation provides funds

for charitable and educational initiatives throughout the

Commonwealth. The scholarship program is the foundation’s

most visible activity, having awarded more than $300,000 in

scholarships since its inception.

Recently, the foundation updated its strategic mission to align itself

more closely with the PACB and has started investing in the future

of community bankers directly. The scholarship benefits community

J

bankers by providing professional development and leadership

ordan Zook, a recent graduate of PACB’s NextGenU skill advancement opportunities to those who have demonstrated

leadership program, has been promoted to credit manager excellence and the propensity for promotion in their field.

at the Bank of Bird-in-Hand. Jordan’s participation in the

online management training program was made possible by “Local community banks are the backbone of many communities

a $1,500 scholarship he earned from the PACB Foundation. and serve as a model for a commitment to excellence. They place

a high value on civic responsibility, and, in turn, are quick to

“You are investing in a young man with a bright future and recognize those who do the same,” said Kevin L. Shivers, president/

providing valuable training that our young Bank does not have CEO, PACB. “Through the scholarship program, community

the internal structure to provide,” wrote Tim Bender, chief credit banks in the Commonwealth can play an important role in helping

officer and chief operations officer/SVP at the Bank of Bird-in- to develop the leaders of tomorrow,” Shivers added.

Hand. “I am grateful for the training for Jordan and the generosity

of PACB to support him and the bank. I have no doubt he will do The Bank of Bird-in-Hand was incorporated under the laws of

you proud!” the State of Pennsylvania on May 31, 2013, and opened its doors

for business on Dec. 2, 2013. The first denovo bank in the United

PACB’s NextGen“U” career pathing modules were developed to

States in almost three years at the time, and in Pennsylvania in

provide the skills training required to enable a bank’s team to

over five years, Bank of Bird-in-Hand is an independent bank

become poised and professional representatives.

headquartered in Lancaster County.

“This program can be the keystone that will assist them in TO LEARN MORE ABOUT THE PROFESSIONAL DEVELOPMENT SCHOLARSHIPS OR THE PACB’S

moving into a management or leadership role, or be stronger in NEXTGEN“U” MANAGEMENT TRAINING PROGRAM, PLEASE VISIT PACB.ORG

HOMETOWN BANKER | HOMETOWNBANKER.ORG | 15INSURED CASH SWEEP® AND CDARS®:

A GAME CHANGER FOR BANKS

AND LOCAL COMMUNITIES

By Patrick Kealey

INSURED CASH SWEEP® AND way to build a stable balance sheet, HOW INSURED CASH SWEEP AND

acquire more funds to lend and help the

CDARS®: A GAME CHANGER FOR local community.

CDARS WORK

BANKS AND LOCAL COMMUNITIES Nationwide, thousands of banks use ICS

In the past, many large-dollar depositors, Reciprocal deposits are those that a bank and CDARS to provide safety-conscious

such as public entities, institutional receives through a deposit placement customers with access to FDIC insurance

investors and nonprofits, were reluctant to network in return for placing an equal beyond the traditional $250,000 per

deposit their cash at small banks because amount of deposits at other network insured bank, per depositor (for each

their deposits could only be insured up to banks. This means that a bank that account ownership category). By splitting

$250,000. They feared losing money if their participates in a deposit placement a customer’s original deposit into smaller

bank failed. In effect, small banks were network can attract and retain a greater increments — each below the standard

penalized for their size on the mistaken amount of deposits from local customers. FDIC insurance maximum — and placing

belief that small automatically equaled risky. Promontory Interfinancial Network, the it into deposit accounts at other banks,

This changed in 2002 when Promontory inventor of reciprocal deposits, offers Insured Cash Sweep and CDARS enable

Interfinancial Network began offering the the nation’s leading reciprocal deposit safety-conscious customers to access multi-

first “reciprocal deposit” placement service placement services, Insured Cash Sweep million-dollar FDIC insurance through a

— CDARS® and, later, another called and CDARS. single bank relationship.

Insured Cash Sweep, or ICS®.

Now, many institutional and individual

investors are embarking on a flight to

safety, moving funds out of the stock

market and into cash to manage volatility

during these challenging economic

times brought on by the COVID-19

pandemic. For banks that are part of

Promontory Interfinancial Network’s

network of banks, this shift represents an

opportunity to offer customers access to

multimillion dollar FDIC insurance while

using reciprocal deposits as a cost-effective

16 | HOMETOWN BANKER | HOMETOWNBANKER.ORGThe Insured Cash Sweep service provides most reciprocal deposits are considered core With CDARS and Insured Cash Sweep,

access to FDIC insurance on funds placed into deposits. The non-brokered status of most banks can help more customers — including

demand deposit accounts and money market reciprocal deposits presents an opportunity businesses, nonprofits, municipalities,

deposit accounts, whereas the CDARS service for banks to grow core deposits, attract financial advisors and even individuals —

provides that access to funds placed into CDs. high-value relationships and make cost- safeguard their funds, potentially at even

Reciprocal deposits are “sticky.” (CDARS effective funding available. higher levels, while at the same time attracting

reinvestment rates are approximately 80%,1 locally priced, large-dollar deposits, the full

and banks typically see less than 5% of ICS Reciprocal deposits held by an FDIC- amount of which can be used to make loans

Reciprocal accounts liquidated in any given insured depository institution are locally. These are loans that can launch new

month even as total accounts and balances considered core as long as: businesses or help existing ones to expand,

steadily increase.2) And, the institution 1. The bank is well capitalized and has creating jobs and providing much-needed

accepting the deposit maintains a relationship received an “outstanding” or “good” services for a community, or that can help

with the depositor — typically a locally based on its most recent examination; and individuals to finance a new home, college

depositor. The safety-conscious customer is 2. The total amount of reciprocal expenses and more.

often a government organization (such as a city deposits held does not exceed the

or county treasurer or a public school district), lesser of $5 billion or 20% of the Built on relationships and serving as pillars

an institutional investor, a nonprofit, or another bank’s total liabilities. of the community, Main Street banks are

depositor that would otherwise the engines behind small business growth

• Make a large deposit in a large money- A bank that drops below well-capitalized and a key source of stability, helping

center bank, rather than a community can continue to accept reciprocal deposits many individuals not just to weather,

bank (foregoing access to FDIC without a waiver from the FDIC so long but to shine through key events in life,

insurance for most of the deposit and as the bank does not receive an amount including challenges like those presented by

relying on large rating agencies, like of reciprocal deposits that cause its total COVID-19. Armed with reciprocal deposits,

Standard & Poor’s and Fitch, and then reciprocal deposits to exceed a previous representing another arrow in their quiver,

tracking the ratings over time); four-quarter average.3 banks can do more — billions of dollars

• Require that a bank collateralize or more — both to help customers meet their

otherwise secure the deposit with BANK-TO-BANK CONNECTIONS – desire for safety and to fund additional

Treasuries or other ultra-safe, highly

liquid government securities (an added

HELPING COMMUNITY BANKS HELP lending that otherwise might not take

place. This helps communities throughout

cost for the bank that could lead to the EACH OTHER Pennsylvania and across the United States.

customer receiving a lower interest rate Why would a bank agree to take Insured Cash

if the bank adjusts its rate to compensate Sweep or CDARS deposits from another bank, If you are a banker who wants to learn

for the added cost it incurs); or essentially helping that other bank? Because more about reciprocal deposits and how

• Manually split its large deposit among in a reciprocal deposit allocation service, each they compare to other funding or deposit-

multiple banks (which requires bank is sending an equal amount of customer gathering alternatives, please visit https://

negotiating different interest rates, deposits to other banks. Exchanges occur on a www.promnetwork.com/solutions/banks/

signing multiple agreements, receiving dollar-for-dollar basis so that each participating grow-franchise-value-with-reciprocal-

multiple statements, etc.). bank comes out whole. deposits. And if you’re a depositor/investor

who would like to learn more, please visit

Bank customers enjoy peace of mind and This benefits banks and local communities https://www.icsandcdars.com/.

the convenience of working through one across the United States in several ways,

institution. Participating banks can grow helping Main Street banks to attract and retain

relationships and deposits from a local the amount of deposits from local customers by THROUGH 3/31/20. PROMONTORY INTERFINANCIAL

1

customer base without losing either to larger • Expanding the availability of deposit NETWORK CALCULATES THE REINVESTMENT RATE BY

DETERMINING WHETHER A PARTICULAR CUSTOMER’S FUNDS

institutions, without the added costs or funding for such banks; WERE REINVESTED WITHIN 28 DAYS OF MATURITY.

tracking burdens associated with ongoing • Providing banks with more funding to

collateralization requirements, and with the make loans within their communities;

2

CALCULATED FOR THE REACH OF THE 12 MONTHS

PRECEDING MARCH 2020. THE ICS RECIPROCAL ACCOUNT

ability to lend the amount of these relatively • Potentially lowering the cost of CLOSURE RATE FOR A GIVEN MONTH IS THE NUMBER OF

low-cost funds locally. At the end of the day, funding for banks over time; and RECIPROCAL ACCOUNTS CLOSED DURING THE MONTH AS

it’s a win-win for banks and their customers. • Enabling banks to compete more A PERCENTAGE OF THE TOTAL NUMBER OF RECIPROCAL

ACCOUNTS AT THE BEGINNING OF THE MONTH. THE NUMBER

effectively with larger, too-big-to-fail OF RECIPROCAL ACCOUNTS CLOSED DURING THE MONTH

MOST RECIPROCAL DEPOSITS ARE banks for stable funding. IS THE NUMBER OF NON-ZERO-BALANCE RECIPROCAL

ACCOUNTS WITHDRAWN TO ZERO DOLLARS DURING THE

CONSIDERED CORE DEPOSITS As a result, banks have a larger source of stable MONTH AND NOT RETURNED TO A NON-ZERO-BALANCE

DURING THE MONTH OR THE SUBSEQUENT TWO MONTHS.

In recent years, community banks have deposits. And banks can replace more expensive

received relief from certain rules and deposits, like brokered deposits, routinely AS UNDER CURRENT LAW, INTEREST RATE RESTRICTIONS

3

regulations through the Economic Growth, collateralized deposits and those from listing WILL APPLY.

Regulatory Relief and Consumer Protection services, with reciprocal deposits received by FOR MORE INFORMATION, CONTACT PATRICK KEALEY AT

Act. Among the law’s many provisions, using CDARS and Insured Cash Sweep. PKEALEY@PROMNETWORK.COM OR (866) 776-6426, EXT. 3468.

HOMETOWN BANKER | HOMETOWNBANKER.ORG | 17NOW IS A GREAT TIME TO

CHECK FLOOD COMPLIANCE

POLICIES AND PROCEDURES

By Western Technologies Group, LLC,

W

e’ve all recently experi- staff or working remotely. As these recent It’s at these times that other crucial

enced what it’s like to times have demonstrated, the way we do measures, like maintaining adequate flood

have a sudden shift in business can change abruptly at any time compliance policies and procedures, can

focus to more immediate and cause a variety of challenges and inadvertently go unchecked. Sudden changes

challenges, such as working with limited distractions. that affect our daily operations and the speed

18 | HOMETOWN BANKER | HOMETOWNBANKER.ORGand quality of otherwise sound practices, can, unfortunately, lead to

mistakes, violations, liabilities and unfortunate penalties.

If your team, department or organization hasn’t already done so,

now is the time to revisit your flood compliance procedures and Review all specific steps in your

policies in order to avoid confusion, frustration and even future current procedures, conducted as a

civil money penalties incurred by common flood compliance

violations. Flood compliance violations can result in heavy fines. department team.

It’s important to stay aware of and avoid common violations:

• No insurance coverage

• Inadequate insurance coverage amount

• Lapsed flood insurance coverage

• No notice of flood coverage needed provided to buyer/owner

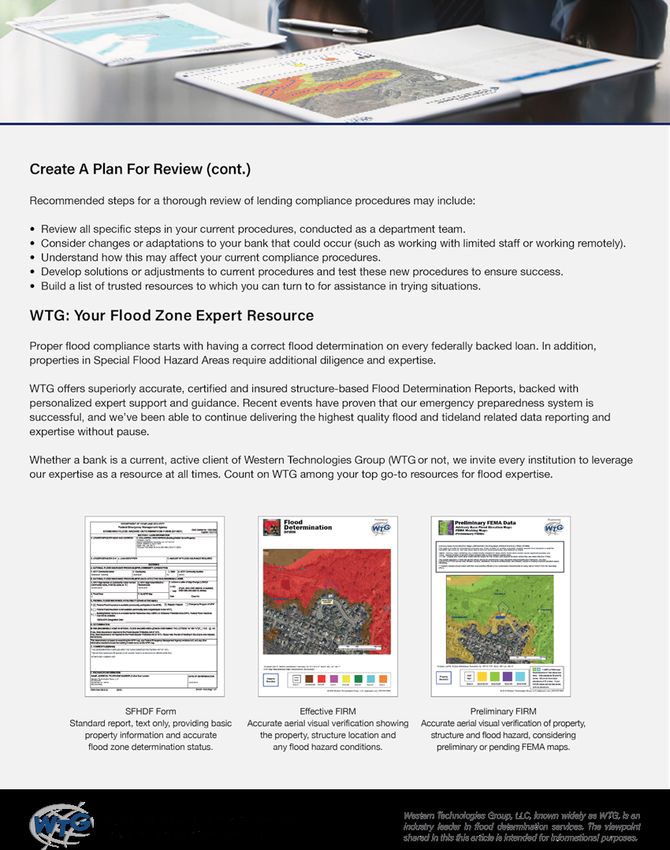

WTG: YOUR FLOOD ZONE EXPERT RESOURCE

• Failing to comply with force-placement of flood insurance

Proper flood compliance starts with having a correct flood

determination on every federally backed loan. In addition,

CREATE A PLAN FOR REVIEW properties in Special Flood Hazard Areas require additional

As we look forward to some resurgence of business, it’s an ideal diligence and expertise.

time to plan a review of all procedures and policies.

A plan can be simply structured as follows: WTG offers superiorly accurate, certified and insured structure-

1. Review procedures and policies. based Flood Determination Reports, backed with personalized

2. Identify areas of potential. expert support and guidance. Recent events have proven that

compliance failure. our emergency preparedness system is successful, and we’ve been

3. Develop resources for guidance in any situation. able to continue delivering the highest quality flood and tideland

related data reporting and expertise without pause.

Recommended steps for a thorough review of lending compliance

procedures may include: Whether a bank is a current, active client of Western Technologies

Group (WTG) or not, we invite every institution to leverage our

• Review all specific steps in your current procedures, conducted

expertise as a resource at all times. Count on WTG among your

as a department team.

top go-to resources for flood expertise.

• Consider changes or adaptations to your bank that could

occur (such as working with limited staff or working

remotely). WESTERN TECHNOLOGIES GROUP, LLC, KNOWN WIDELY AS WTG, IS AN INDUSTRY LEADER

• Understand how this may affect your current compliance IN FLOOD DETERMINATION SERVICES. THE VIEWPOINT SHARED IN THIS THIS ARTICLE IS

INTENDED FOR INFORMATIONAL PURPOSES.

procedures.

• Develop solutions or adjustments to current procedures and

test these new procedures to ensure success.

• Build a list of trusted resources to which you can turn to for

assistance in trying situations.

HOMETOWN BANKER | HOMETOWNBANKER.ORG | 19PLANNING FOR THE FUTURE:

COMMUNITY BANK LESSONS

FROM THE COVID-19 PANDEMIC

By Martin B. Ellis, Shumaker Williams, P.C.

I. INTRODUCTION and internal capability within the bank’s virtual demise of in-person banking. That

workforce. Consider rethinking how you might be true during this pandemic for

As challenging as the Covid-19 pandemic is train and cross-train your employees. During regional and national bank conglomerates,

for community bank customers, it has been a pandemic, as well as after, the bank will which have completely closed any

especially difficult for the banks themselves. need its employees to back one another. number of their branch offices in major

Moreover, while experts may disagree on metropolitan areas, thereby forcing a

the timing and parameters of COVID-19 Also, consider hiring people who will work large segment of their customers to bank

for the rest of this year and beyond, to expand their skills, thus becoming part of digitally. However, it is decidedly not true

economic and political turmoil will almost the “readiness” factor both during and after for community banks.

certainly continue. The key for community this pandemic. Encourage your employees

banks is to develop “readiness” strategies to to build deeper and stronger social networks What COVID-19 has proven so far is

address these concerns and best serve their inside and outside the bank. For a bank’s that when businesses are forced to close,

customers in a post-pandemic world. executives, learn before you need to know and people are encouraged or mandated

something. The bank’s community has an by local governments to stay home except

Such “readiness” strategies going forward abundance of information and intelligence for essential trips to address medical

require accepting that world events do that can help the bank through an needs or groceries, people lose their

not necessarily align with an industry’s emergency such as COVID-19. inherent need to foster quality human

well-thought strategic planning. However, experiences and relationships, often face-

this does not mean discarding the

present plan. Rather, an examination of a

B. DIGITAL VERSUS IN-PERSON to-face. Community banks have thrived

over the years because they are uniquely

bank’s strategies employed to address the BANKING positioned to support those experiences and

pandemic, coupled with a reexamination COVID-19 has brought several relationships, especially through in-person

of the banks’ core strengths and financial architectural changes to community meetings with their customers.

needs of their customer base, should lead to banks as well as their much larger banking

future sustainability. competitors. This has also greatly reduced During this pandemic, most community

in-person banking. Many community banks have seen their customers understand

II. COVID-19 LESSONS banks had adopted significant digital the safety, convenience, and value of the

banking capacity pre-pandemic to remain bank’s digital banking tools. Community

A. FLEXIBLE WORKFORCE competitive with their regional and banks must also commit to improving

Pre-pandemic, many community banks national bank competition. Two schools of them by inquiring as to what digital tools

may have provided job flexibility to those thought have addressed the future of digital the bank may be lacking, and which digital

employees who needed it. These banks versus in-person banking. Some experts services proved to be substandard. For

invested in technology to enable remote- predict that electronic banking is no longer example, the bank’s call center may need

working and supplied the equipment the “wave of the future”; rather, it is both to add bilingual staff, anticipating that a

employees would need to work remotely the present and the future, with in-person growing and diverse clientele may need

at home. Because such banks deployed banking being a relic of the past. Others, more services provided by phone. Also,

this strategy pre-pandemic, they were able however, see a continuing need for in- community banks must recognize that

to have much of their workforce working person banking, especially for community a “digital divide” exists between under-

safely from home when COVID-19 began. banks. Oddly, each side cites the resourced communities, both urban and

COVID-19 pandemic as fully supportive of rural that lack high-quality digital access,

Whether your bank fits this category their position. compared with residents of large urban

pre-pandemic or has adopted it in whole centers that take digital access for granted.

or in part as a result of the pandemic, the The digital proponents cite the pandemic-

issue is how to build on that successful driven need for “masking” and “social With these lessons in mind, community

experience. Simply put, community banks distancing,” with concomitant architectural banks will continue to thrive once this

need to address how to create more resilience changes to bank offices, as presaging the pandemic has run its course.

20 | HOMETOWN BANKER | HOMETOWNBANKER.ORGLINKBANK PRESIDENT BRENT SMITH

EARNS NATIONAL RECOGNITION AS A 40 UNDER

40 EMERGING COMMUNITY BANK LEADER

B

rent Smith, president of LINKBANK in Camp Hill, PA, LINKBANK has three locations in the state of Pennsylvania and

recently was recognized nationally as a “40 Under 40: total assets of approximately $247 million. Its footprint includes

Emerging Community Bank Leaders” by Independent Chester, Cumberland and Lancaster counties. The bank offers

Banker magazine. “Brent Smith lives the community a comprehensive portfolio of products and services to meet the

bank philosophy every day and Pennsylvania community bankers banking needs of the communities it serves, including a state-of-the-

are proud that Brent was recognized for his contributions to the art internet banking website. To learn more about LINKBANK, visit

community,” said Kevin L. Shivers, PACB president and CEO. www.linkbank.com.

“Brent has worked hard not only to learn his profession but also

to make a positive impact on the lives of those who live in the This is the second year that Independent Banker has recognized

community. Brent’s meaningful involvement with so many local

rising community bank innovators and influencers who represent the

charities personifies a true community banker.” Brent Smith’s

future of the industry. It also is the second year that a Pennsylvania

vision for community banking began with his instrumental role in

community banker was selected for national recognition.

founding LINKBANK, a new community-driven, locally focused

community bank in South Central PA, with a vision to foster

personal relationships, inspire trust, and empower digital innova- “Community banking is not just a profession, it is an opportunity

tion. In addition to starting the bank, Smith established the LINK for bankers to help support the financial well-being of the businesses,

Foundation, which proudly allocates LINKBANK’s resources back homeowners and communities they serve,” Shivers continued. “It’s

into the communities they serve. He also serves on the board for gratifying to see Pennsylvania’s community bank professionals

Rider Musser Corp., Brethren Housing Assoc. and The Meeting earn national recognition for their leadership in the industry and

House Church. contributions to their communities. This recognition showcases

the great work of our community bankers and the results of their

LINKBANK, headquartered in Camp Hill, Pennsylvania, has charitable, economic-development and impressive volunteer

been a local, independent bank serving the community since 1999. contributions. That is something we all can be proud of.”

HOMETOWN BANKER | HOMETOWNBANKER.ORG | 21You can also read