DECEMBER 2019 STOCK PICKS - BIGFOOT INVESTMENTS

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

December 2019 Stock Picks

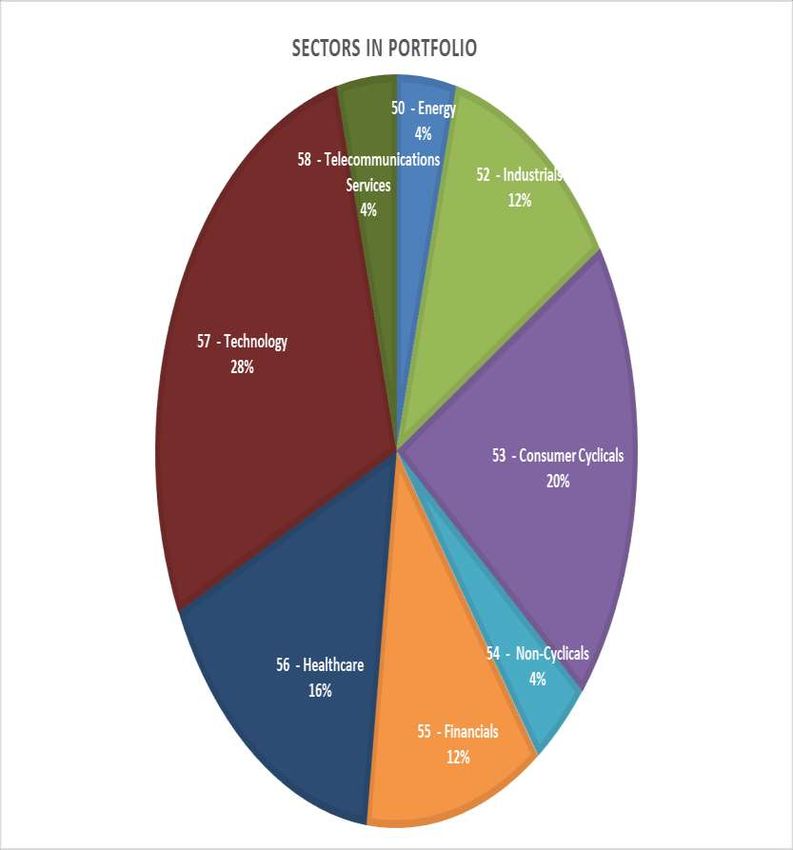

TOP 25 STOCKS December-19

RANK TICKER NAME SECTOR INDUSTRY

1 AAPL Apple Inc. 57 - Technology 57106020 - Phones & Handheld Devices

2 MSFT Microsoft Corporation 57 - Technology 57201020 - Software

3 ADBE Adobe Inc 57 - Technology 57201020 - Software

4 V Visa Inc 57 - Technology 57201030 - Online Services

5 AMZN Amazon.com, Inc. 53 - Consumer Cyclicals 53402010 - Retailers - Department Stores

6 MA Mastercard Inc 57 - Technology 57201030 - Online Services

7 GOOGL Alphabet Inc 57 - Technology 57201030 - Online Services

8 ISRG Intuitive Surgical, Inc. 56 - Healthcare 56101010 - Advanced Medical Equipment & Technology

9 NVDA NVIDIA Corporation 57 - Technology 57101010 - Semiconductors

10 SBUX Starbucks Corporation 53 - Consumer Cyclicals 53301020 - Restaurants & Bars

11 HON Honeywell International Inc. 52 - Industrials 52301010 - Industrial Conglomerates

12 ULTA Ulta Beauty Inc 53 - Consumer Cyclicals 53403090 - Retailers - Other Specialty

13 CAT Caterpillar Inc. 52 - Industrials 52102020 - Heavy Machinery & Vehicles

14 COST Costco Wholesale Corporation 53 - Consumer Cyclicals 53402020 - Retailers - Discount Stores

15 CNC Centene Corp 56 - Healthcare 56102020 - Managed Health care

16 GSK GlaxoSmithKline plc (ADR) 56 - Healthcare 56201040 - Pharmaceuticals

17 DIS Walt Disney Co 53 - Consumer Cyclicals 53302020 - Broadcasting

18 JNJ Johnson & Johnson 56 - Healthcare 56201040 - Pharmaceuticals

19 PANW Palo Alto Networks Inc 57 - Technology 57201030 - Online Services

20 GS Goldman Sachs Group Inc 55 - Financials 55102010 - Investment Banking & Brokerage Services

21 CVS CVS Health Corp 56 - Healthcare 56102010 - Healthcare Facilities & Services

22 BAC Bank of America Corp 55 - Financials 55101010 - Banks

23 C Citigroup Inc 55 - Financials 55101010 - Banks

24 BA Boeing Co 52 - Industrials 52101010 - Aerospace & Defense

25 STZ Constellation Brands, Inc. 54 - Non-Cyclicals 54101020 - Distillers & Wineries

As of November 25th, 2019- Subject to change.December 2019 Growth Stock Picks

As of November 25th, 2019. Subject to change.December 2019 Growth Stock Picks

As of November 25th, 2019. Subject to change.December 2019 Growth Stock Picks

As of November 25th, 2019- Subject to change.December 2019 Growth Stock Picks

As of November 25th, 2019- Subject to change.December 2019 Growth Stock Picks

As of November 25th, 2019- Subject to change.December 2019 Growth Stock Picks

As of November 25th,2019- Subject to change.Apple Inc. (AAPL)

Apple Inc. designs, manufactures, and markets mobile communication and media devices, and

personal computers. It also sells various related software, services, accessories, and third-

party digital content and applications. The company offers iPhone, a line of smartphones;

iPad, a line of multi-purpose tablets; and Mac, a line of desktop and portable personal

computers, as well as iOS, macOS, watchOS, and tvOS operating systems. It also provides

iTunes Store, an app store that allows customers to purchase and download, or stream music

and TV shows; rent or purchase movies; and download free podcasts, as well as iCloud, a

cloud service, which stores music, photos, contacts, calendars, mail, documents, and others.

In addition, the company offers AppleCare support services; Apple Pay, a cashless payment

service; Apple TV that connects to consumers' TVs and enables them to access digital content

directly for streaming video, playing music and games, and viewing photos; and Apple Watch,

a personal electronic device, as well as AirPods, Beats products, HomePod, iPod touch, and

other Apple-branded and third-party accessories. The company serves consumers, and small

and mid-sized businesses; and education, enterprise, and government customers worldwide.

It sells and delivers digital content and applications through the iTunes Store, App Store, Mac

App Store, TV App Store, Book Store, and Apple Music. The company also sells its products

through its retail and online stores, and direct sales force; and third-party cellular network

carriers, wholesalers, retailers, and resellers. Apple Inc. was founded in 1977 and is

headquartered in Cupertino, California.

Source: FinViz.com, October 2019Apple Inc. (AAPL)

POSITIVES: Apple’s non-iPhone businesses, particularly Services and Wearables, are expected to drive top-

line growth in fiscal 2019 and beyond. The Services portfolio has emerged as the company’s new cash cow.

Apple’s endeavors to open up its ecosystem, through partnerships with the likes of Samsung and Amazon,

are positive for the Services segment. The recently announced subscription-based video streaming, news

and gaming services are expected to benefit from Apple’s strong installed base. Robust App Store sales

coupled with solid adoption of Apple Pay and Apple Music are expected to help Apple double its 2016

Services revenues by 2020. Moreover, its Wearables business is expected to be driven by solid demand for

Apple Watch. Apple currently has more than 420 million paid subscribers across its Services portfolio. The

App Store continues to draw the attention of prominent developers from around the world, helping the

company offer appealing new apps that drive App Store traffic. Further, growing number of AI-infused apps

will attract more subscribers on App Store. Apple is encouraging developers to use artificial intelligence (AI)

and machine learning in their apps. The company’s Core ML 2 API helps developers recognize faces or

animals in photos, and parse the meaning of text. Further, the company is offering Create ML for simple and

efficient machine learning training on the Mac, which is built on top of Swift programming language. Apple’s

focus on autonomous vehicles and augmented reality/virtual reality (AR/VR) technologies presents growth

opportunity in the long haul. These are fast emerging as lucrative business opportunities. To ramp up its

efforts, Apple has acquired several smaller firms with expertise in AR hardware, 3D gaming and VR software.

Possible concerns: Lackluster demand for iPhone primarily in China and emerging countries, stiff

competition and increasing regulatory hassles are major headwinds. Apple’s excessive dependence on

iPhone is a risk to overall growth. Although iPhone sales have been benefiting from higher average selling

price (ASP), premium pricing has been blamed for Apple’s declining market share in countries like China and

India.

Source: Zacks Research, October 2019Adobe Inc. (ADBE)

Adobe Inc. operates as a diversified software company worldwide. Its Digital Media segment

provides tools and solutions that enable individuals, small and medium businesses, and enterprises

to create, publish, promote, and monetize their digital content. Its flagship product is Creative Cloud,

a subscription service that allows customer to download and access the latest versions of its creative

products. This segment serves traditional content creators, Web application developers, and digital

media professionals, as well as their management in marketing departments and agencies,

companies, and publishers. The company's Digital Experience segment offers solutions for how

digital advertising and marketing are created, managed, executed, measured, and optimized. This

segment provides analytics, social marketing, targeting, media optimization, digital experience

management, cross-channel campaign management, marketing automation, audience management,

and video delivery and monetization solutions to digital marketers, advertisers, publishers,

merchandisers, Web analysts, chief marketing officers, chief information officers, and chief revenue

officers. Its Publishing segment offers products and services, such as e-learning solutions, technical

document publishing, Web application development, and high-end printing, as well as publishing

needs of technical and business, and original equipment manufacturers (OEMs) printing businesses.

The company offers its products and services directly to enterprise customers through its sales force,

as well as to end-users through app stores and through its Website at adobe.com. It also distributes

products and services through a network of distributors, value-added resellers, systems integrators,

software vendors and developers, retailers, and OEMs. The company was formerly known as Adobe

Systems Incorporated and changed its name to Adobe Inc. in October 2018. The company was

founded in 1982 and is headquartered in San Jose, California..

Source: FinViz.com, October 2019Adobe Inc. (ADBE)

POSITIVES: Adobe continues to be the market leader in the Digital Media space. The company provides one of the

best solutions in most categories of digital media design and publishing, including Internet and video. In fiscal first

quarter, total Digital Media ARR (Annualized recurring revenue), the key cloud performance measure, grew to

$7.07 billion. This indicates strong growth in the Creative Cloud and Document Cloud businesses. As advertising,

entertainment and other content-creation markets are becoming increasingly digitalized, Adobe is well positioned

to benefit from this trend and should enjoy above-average long-term growth. Adobe entered the digital marketing

space with the acquisition of Omniture. This is an area where corporate spending is on the rise. A number of trends

are spurring this trend, including the increased adoption of cloud computing, social media and mobile devices, as

well as the emergence of big data analytics. Acrobat is one of the company’s most successful product lines with a

huge installed base of satisfied customers. Through Acrobat.com, the company offers a set of a cloud-based

document and collaboration subscription services which include PDF creation, centralized online file sharing and

contract signing solutions. There are currently many drivers of the Acrobat business. A portion of the business has

historically been dependent on GDP growth. This business has responded to the improving economic conditions

and stronger IT spending in the U.S. and Europe. Management expects the gradual uptick in enterprise spending to

be an overall positive for the Acrobat business. Using its new cloud-based platform, Adobe is also diversifying into

digital marketing services, offering data mining services, which help businesses to measure page views, purchases

and social media sites. Adobe Marketing Cloud enables marketers to deliver personalized web experiences across

multiple devices, manage multichannel campaigns and optimize media monetization. These services help

businesses streamline marketing and products for targeted consumer groups, including chief marketing officers,

chief revenue officers, advertising agencies, publishing executives and digital marketers. It is expected that Creative

Cloud customers will be wooed to purchase products from the Marketing Cloud, accelerating Adobe’s revenue

growth in both the segments simultaneously.

Possible concerns: Lower end-market demand as a result of weak global economic conditions could impact results.

Also, significant exposure to Europe remains a major concern.

Source: Zacks Research, June 2019Amazon.com Inc. (AMZN)

Amazon.com, Inc. engages in the retail sale of consumer products and subscriptions in North

America and internationally. The company operates through three segments: North America,

International, and Amazon Web Services (AWS) segments. It sells merchandise and content

purchased for resale from third-party sellers through physical stores and online stores. The

company also manufactures and sells electronic devices, including Kindle e-readers, Fire tablets,

Fire TVs, and Echo devices; provides Kindle Direct Publishing, an online service that allows

independent authors and publishers to make their books available in the Kindle Store; and

develops and produces media content. In addition, it offers programs that enable sellers to sell

their products on its Websites, as well as their own branded Websites; and programs that allow

authors, musicians, filmmakers, skill and app developers, and others to publish and sell content.

Further, the company provides compute, storage, database, and other AWS services, as well as

compute, storage, database offerings, fulfillment, publishing, digital content subscriptions,

advertising, and co-branded credit card agreement services. Additionally, it offers Amazon Prime,

a membership program, which provides free shipping of various items; access to streaming of

movies and TV episodes; and other services. It serves consumers, sellers, developers, enterprises,

and content creators. Amazon.com, Inc. has a strategic partnership with Volkswagen AG. The

company was founded in 1994 and is headquartered in Seattle, Washington.

Source: FinViz.com, October 2019Amazon.com Inc. (AMZN)

POSITIVES: Amazon.com is one of the largest e-commerce companies in the world. Amazon keeps its retail business

very hard to beat on price, choice, and convenience with the help of a solid loyalty system in Prime and its FBA

strategy. The company continues to push advantages exclusively to Prime members, thus encouraging them to

spend more on Amazon. The current focus is on building video content, primarily for Prime subscribers because the

growth prospects in the market are considerable. Prime members are much more loyal and spend double the

amount spent by non-Prime members. Amazon’s strategy of gradually merging online and offline retail looks

promising. It will not only reshape the retail landscape but also help it fend off competition, if it could manage a first

mover advantage. Amazon is the leading provider of cloud infrastructure as a service to enterprise customers. The

expanding customer base of Amazon Web Services (AWS) driven by its strengthening cloud offerings will continue to

aid Amazon's dominance in the global cloud space. Amazon is pushing well with its devices strategy. Alexa powered

Echo devices are going great guns and help the company sell products and services. Artificial intelligence (AI) driven

Alexa has already been integrated into a host of everyday devices for the digital home, which has converted the

nascent smart home market into a potential area of growth in a very short time. Amazon is gradually choosing the

buy option over build, which, along with the other positives, ensures that the company generates revenues right

way without wasting any time in building its own infrastructure. In Jul, 2017, the company completed the acquisition

of a Dubai-based e-commerce giant, Souq.com. The deal will help Amazon to establish a presence in countries like

Egypt, Saudi Arabia, and the UAE markets like Egypt, Saudi Arabia, and the UAE.

Possible concerns: There is a downside to a growing international business in the current economic environment.

While expansion opportunities automatically increase, currency also starts playing a bigger role. Prime’s saturation

in the U.S. market is apparent, because Amazon has very high penetration rates in the country. The competition in

online retail is heating up. Traditional retailers have always provided the strongest competition and a number of

them are running e-commerce sites as well. Most retail businesses tend to be seasonal and Amazon’s is no different.

Source: Zacks Research, October 2019The Boeing Company (BA)

The Boeing Company, together with its subsidiaries, designs, develops, manufactures, sales, services, and

supports commercial jetliners, military aircraft, satellites, missile defense, human space flight and launch

systems, and services worldwide. The company operates in four segments: Commercial Airplanes;

Defense, Space & Security; Global Services; and Boeing Capital. The Commercial Airplanes segment

provides commercial jet aircraft for passenger and cargo requirements, as well as fleet support services,

principally. The Defense, Space & Security segment engages in the research, development, production,

and modification of manned and unmanned military aircraft and weapons systems; strategic defense and

intelligence systems, which include strategic missile and defense systems, command, control,

communications, computers, intelligence, surveillance and reconnaissance, cyber and information

solutions, and intelligence systems; and satellite systems, such as government and commercial satellites,

and space exploration. The Global Services segment offers products and services, including supply chain

and logistics management, engineering, maintenance and modifications, upgrades and conversions, spare

parts, pilot and maintenance training systems and services, technical and maintenance documents, and

data analytics and digital services to commercial and defense customers. The Boeing Capital segment

offers financing services and manages financing exposure for a portfolio of equipment under operating

and finance leases, notes and other receivables, assets held for sale or re-lease, and investments. The

Boeing Company was founded in 1916 and is based in Chicago, Illinois.

Source: FinViz.com, October 2019The Boeing Company (BA)

POSITIVES: Boeing is the largest aircraft manufacturer in the world in terms of revenue, orders and deliveries, and is

one of the largest aerospace and defense contractors. Its revenue exposure is spread across more than 90 countries

around the globe. Boeing expects the commercial fleet to be fueled by sustained annual growth in commercial

passenger traffic along with a big wave of retiring, old planes. Of the total units, 44% of the demand will be for the

replacement of old aircraft, while the rest will support future growth. The massive demand for commercial jets

generates a strong and growing demand for aviation services ranging from supply chain support (parts and parts

logistics), to maintenance and engineering services, to aircraft modifications, to airline operations. In this line, Boeing

expects commercial aviation services market to grow 4.1% annually to a value worth $9.1 trillion, over the next 20

years. This should bode well for the company’s growth trajectory. While Boeing’s commercial business has not been

performing well for the past couple of quarters, on account of lower 737 deliveries, the aerospace giant’s defense

business remains buoyant. In the third quarter, the BDS segment registered 2% year-over-year revenue growth driven

by higher volume from satellites, weapons and T-7A Red Hawk programs. Looking ahead, the current U.S.

government’s inclination toward strengthening the nation’s defense system should act as a growth catalyst for

defense players like Boeing. Notably, as part of the fiscal 2020 defense budget, $718.3 billion is allocated as funding

for the Pentagon, reflecting 5% growth over the fiscal 2019 budget.

Possible concerns: Boeing’s commercial business continued to suffer due to lower 737 deliveries as a result of the

worldwide grounding of 737 Max jets in March, following two fatal crashes involving these jets. Consequently, its

commercial deliveries plunged 67% year over year, resulting in a huge 41% decline in the unit’s revenues during the

third quarter. Such dismal performance recorded by Boeing’s largest revenue-generating business segment also hit

the company’s bottom line and cash position. Consequently, Boeing’s adjusted earnings declined 59% year over year

in the third quarter, while its operating cash outflow was $0.26 billion. Canadian, Russian and Chinese manufacturers

will begin delivering airplanes, comparable to Boeing 737 over the next few years. Meanwhile, its arch rival, Airbus

outpaced Boeing in commercial plane deliveries at the end of first half of 2019 for the first time in eight years.

Source: Zacks Research, October 2019Bank of America Corporation (BAC)

Bank of America Corporation, through its subsidiaries, provides banking and financial products and

services for individual consumers, small- and middle-market businesses, institutional investors, large

corporations, and governments worldwide. It operates in Consumer Banking, Global Wealth & Investment

Management (GWIM), Global Banking, and Global Markets segments. The Consumer Banking segment

offers traditional and money market savings accounts, CDs and IRAs, noninterest- and interest-bearing

checking accounts, and investment accounts and products; and credit and debit cards, residential

mortgages, and home equity loans, as well as direct and indirect loans, such as automotive, recreational

vehicle, and consumer personal loans. As of July 22, 2019, this segment served 66 million consumer and

small business clients with approximately 4,300 retail financial centers; 16,600 ATMs; and digital banking.

The GWIM segment offers investment management, brokerage, banking, and trust and retirement

products; and wealth management solutions targeted to high net worth and ultra high net worth clients,

as well as customized solutions to meet clients' wealth structuring, investment management, and trust

and banking needs, including specialty asset management services. The Global Banking segment provides

lending products and services, including commercial loans, leases, commitment facilities, trade finance,

and real estate and asset-based lending; treasury solutions, such as treasury management, foreign

exchange, and short-term investing options; working capital management solutions; and debt and equity

underwriting and distribution, and merger-related and other advisory services. The Global Markets

segment offers market-making, financing, securities clearing, settlement, and custody services, as well as

risk management, foreign exchange, fixed-income, and mortgage-related products. Bank of America

Corporation was founded in 1874 and is headquartered in Charlotte, North Carolina.

Source: FinViz.com, October 2019Bank of America Corporation (BAC)

POSITIVES: Rising loans and deposits, manageable expenses and expansion into new markets will support Bank

of America’s financials. Technological upgrades are likely to help in cross selling opportunities.Steady loan

growth is expected to continue supporting Bank of America’s interest income. Over the last three years (2016-

2018), net interest income (NII) saw a CAGR of 7.4%. Bank of America continues to align its banking center

network according to the customer needs. By 2021, the bank intends to expand to new cities, open nearly 500

new centers and redesign 2,500 centers with technology upgrades. The company is opening fully automated

branches that will feature ATMs and video conferencing facility, allowing customers to communicate with off-

site bankers. These branches, aiming to sell mortgages, auto loans and credit cards, are smaller in size and

utilize advance technology. Further, the company has announced plans to add 2,200 more ATMs to its network.

Bank of America’s sturdy capital deployment activities look impressive. In June, the company received the Fed's

approval for its 2019 capital plan, which includes a 20% quarterly dividend hike and a share repurchase

authorization worth $30.9 billion. Therefore, in aggregate, the bank intends to return roughly $37 billion to

shareholders. Given the robust capital position and lower dividend payout ratio compared to its peers, the

company will likely be able sustain its capital deployment activities and continue enhancing shareholder value.

Possible concerns: Muted investment banking and trading performance remain major near-term challenges for

Bank of America. This is expected to have an adverse impact on the company’s non-interest income growth.

Source: Zacks Research, October 2019Citigroup Inc. (C)

Citigroup Inc., a diversified financial services holding company, provides various financial

products and services for consumers, corporations, governments, and institutions in North

America, Latin America, Asia, Europe, the Middle East, and Africa. The company operates

through two segments, Global Consumer Banking (GCB) and Institutional Clients Group (ICG).

The GCB segment offers traditional banking services to retail customers through retail banking,

commercial banking, Citi-branded cards, and Citi retail services. It also provides various

banking, credit card lending, and investment services through a network of local branches,

offices, and electronic delivery systems. The ICG segment provides wholesale banking products

and services, including fixed income and equity sales and trading, foreign exchange, prime

brokerage, derivative services, equity and fixed income research, corporate and consumer

loans, investment banking and advisory services, private banking, cash management, trade

finance, and securities services to corporate, institutional, public sector, and high-net-worth

clients. As of December 31, 2018, it operated 2,410 branches in the United States, Mexico, and

Asia. Citigroup Inc. was founded in 1812 and is headquartered in New York, New York.

Source: FinViz.com, October 2019Citigroup Inc. (C)

POSITIVES: A diverse business model, focus on core operations and streamlining of international businesses

will continue to support Citigroup’s growth. Further, steady capital deployment is a tailwind. Over the past

several years, Citigroup’s net interest revenues had been under pressure amid a low interest-rate

environment. However, with improvement in the interest rates scenario following the rate hikes and steady

loan growth, strain on NIR continues to ease. In 2018 and the first nine months of 2019, uptrend in NIR was

recorded, after witnessing a declining trend for years. Notably, management expects net interest income

(NII) to rise in the range of 3-4% for 2019, lower than the prior projection of 4% amid more Fed rate cut

expectations and flattening of the yield curve. Citigroup's long-term strategy to shrink its non-core assets and

increase fee-based business mix would improve valuation over time. The rundown of Citi Holdings – its

legacy problem assets portfolio – is largely complete. Citigroup has been emphasizing on growth in core

businesses through expense management and streamlining operations internationally. Further, the company

continues to optimize its branch network, with focus on core urban markets, improving digital channels and

reducing branches. Driven by a solid capital position, Citigroup remains committed towards enhancing its

shareholders’ value with steady capital deployment activities. Notably, following the approval of 2019 capital

plan, the company increased its quarterly dividend by 13.3% from the prior payout in July 2019.

Possible concerns: Citigroup is burdened with numerous investigations and lawsuits escalating legal costs

and limiting the company’s business growth. Moreover, muted fee income is a concern for the company.

Source: Zacks Research, October 2019Caterpillar Inc. (CAT)

Caterpillar Inc. manufactures and sells construction and mining equipment, diesel and natural gas engines,

and industrial gas turbines. Its Construction Industries segment offers asphalt pavers, compactors, cold

planers, feller bunchers, harvesters, motorgraders, pipelayers, road reclaimers, skidders, telehandlers,

and utility vehicles; backhoe, knuckleboom, compact track, multi-terrain, skid steer, and track-type

loaders; forestry and wheel excavators; and site prep and track-type tractors. The company's Resource

Industries segment provides electric rope and hydraulic shovels, draglines, rotary drills, hard rock

vehicles, track-type tractors, mining trucks, longwall miners, wheel loaders, off-highway and articulated

trucks, wheel tractor scrapers, wheel dozers, landfill and soil compactors, machinery components,

electronics and control systems, select work tools, and hard rock continuous mining systems. Its Energy

& Transportation segment offers reciprocating engine powered generator sets; reciprocating engines

and integrated systems for the power generation, marine, oil, and gas industries; turbines, centrifugal

gas compressors, and related services; remanufactured reciprocating engines and components; and

diesel-electric locomotives and components, and other rail-related products. The company's Financial

Products segment provides operating and finance leases, installment sale contracts, working capital

loans, and wholesale financing; and insurance and risk management products. Its All Other operating

segment manufactures filters and fluids, undercarriage, ground engaging tools, fluid transfer products,

precision seals, and rubber sealing and connecting components; parts distribution; integrated logistics

solutions and distribution services; and digital investments services. The company was formerly known

as Caterpillar Tractor Co. and changed its name to Caterpillar Inc. in 1986. The company was founded in

1925 and is headquartered in Deerfield, Illinois.

Source: FinViz.com, October 2019Caterpillar Inc. (CAT)

POSITIVES: Caterpillar will continue to monitor end-user demand, commercial shipments, dealer inventory,

orders and backlog and plans to adjust production levels accordingly. The company has been successful in

reducing the lead times, which allows dealers to maintain lower levels of inventory. Further, shorter lead times

enable both the company and its dealers to adapt quickly to changing market conditions. The company is also

taking steps to reduce production to match dealer demand and will proactively increase production once order

levels improve. For the Construction Industries segment, improvement in residential and non-residential

construction in North America, and infrastructure demand is likely to drive revenues. Increasing commodity

prices are likely to support capital investment in the mining sector. Caterpillar’s cash and liquidity position

remains strong with the company ending third-quarter 2019 with cash and short-term investments of $7.9

billion. In the third quarter of 2019, the company repurchased $1.2 billion of Caterpillar common stock and paid

out dividends of $0.6 billion. So far this fiscal, the company has made share repurchases worth $3.3 billion.

Caterpillar expects around 9% share count reduction by the end of this year. In September 2015, Caterpillar set

out with significant restructuring and cost reduction initiative, which has now been substantially completed. The

plan will likely lower annual operating costs by about $1.5 billion. Caterpillar is focused on developing a more

competitive and flexible cost structure and controlling discretionary spending. Caterpillar continues to focus on

customers and on the future by continuing to invest in digital capabilities, connecting assets and jobsites along

with developing the next generation of more productive and efficient products. The company plans to fund

initiatives that drive long-term profitable growth focused on areas of expanded offerings and services and digital

initiatives like e-commerce.

Possible concerns: Impact of raw material cost inflation on margins, inventory reduction at its dealers and low

end-user demand owing to the global economic uncertainty remain headwinds.

Source: Zacks Research, October 2019Centene Corporation (CNC)

Centene Corporation operates as a diversified and multi-national healthcare enterprise that provides

programs and services to under-insured and uninsured individuals in the United States. The

company's Managed Care segment offers health plan coverage to individuals through government

subsidized programs, including Medicaid, the State children's health insurance program, long-term

services and support, foster care, and medicare-medicaid plans, which covers dually eligible

individuals, as well as aged, blind, or disabled programs. Its health plans include primary and

specialty physician care, inpatient and outpatient hospital care, emergency and urgent care,

prenatal care, laboratory and X-ray, home-based primary care, transportation assistance, vision

care, dental care, telehealth, immunization, specialty pharmacy, therapy, social work, nurse

advisory, and care coordination services, as well as prescriptions, limited over-the-counter drugs,

medical equipment, and behavioral health and abuse services. This segment also offers various

individual, small group, and large group commercial healthcare products to employers and directly

to members in the Managed Care segment. Its Specialty Services segment provides pharmacy

benefits management services; health, triage, wellness, and disease management services; and

vision and dental, and management services, as well as care management software that automate

the clinical, administrative, and technical components of care management programs. This

segment offers its services and products to state programs, correctional facilities, healthcare

organizations, employer groups, and other commercial organizations. The company provides its

services through primary and specialty care physicians, hospitals, and ancillary providers. Centene

Corporation was founded in 1984 and is headquartered in St. Louis, Missouri.

Source: FinViz.com, October 2019Centene Corporation (CNC)

POSITIVES: Growing Top Line: Centene has been witnessing consistent and significant revenue growth since

2002. The witnessed a CAGR of 39.6% from 2012 to 2018. The same was up 28% year over year in the first

nine months of 2019 on the back of the Fidelis Care buyout, growth in the Health Insurance Marketplace

business and expansions plus new programs across many of states in 2018 and 2019. Inorganic Growth:

Centene’s mergers and acquisitions strategy is mainly targeted at expanding the company’s markets and

increasing its Medicaid membership. Certain acquisitions like Community Medical Holdings, MHM Services

and Fidelis Care have contributed to its revenues and helped it expand is capabilities. Centene is on course to

acquire WellCare, which is expected to close by the first half of 2020. The combined entity will have a wider

scale and diversification with more than 12 million Medicaid and around 5 million Medicare members. In

total, it will have around 22 million members across 50 US states. It is presumed that this new company will

have estimated pro forma 2019 revenues in excess of $100 billion and an EBITDA of $5 billion. Medical

membership of the company has been rising over the past several quarters due to contract wins and

expansion across different regions. Following solid third-quarter 2019 results, the company has retained its

2019 guidance. It now expects revenues in the range of $73.6-$74.2 billion, the mid-point point of which is

23.2% above the reported figure of 2018.

Possible concerns: Centene's financial results suffer from rising level of debt and increasing costs. Its

reducing cash flow from operations also remain a concern. Its low return on equity also bothers.

Source: Zacks Research, October 2019Costco Wholesale Corporation (COST)

Costco Wholesale Corporation, together with its subsidiaries, operates membership warehouses in

the United States, Puerto Rico, Canada, the United Kingdom, Mexico, Japan, Korea, Australia,

Spain, France, Iceland, China, and Taiwan. It offers branded and private-label products in a range

of merchandise categories. The company provides dry and packaged foods, and groceries; snack

foods, candies, alcoholic and nonalcoholic beverages, and cleaning supplies; appliances,

electronics, health and beauty aids, hardware, and garden and patio products; meat, bakery, and

deli products, as well as produce; and apparel and small appliances. It also operates gas stations,

pharmacies, optical dispensing centers, food courts, and hearing-aid centers; and offers business

delivery, travel, and various other services online in various countries. As of September 1, 2019,

the company operated 782 warehouses, including 543 in the United States and Puerto Rico, 100

in Canada, 39 in Mexico, 29 in the United Kingdom, 26 in Japan, 16 in South Korea, 13 in Taiwan,

11 in Australia, 2 in Spain, 1 in Iceland, 1 in France, and 1 in China. It also operates e-commerce

Websites in the United States, Canada, the United Kingdom, Mexico, South Korea, and Taiwan.

The company was formerly known as Costco Companies, Inc. and changed its name to Costco

Wholesale Corporation in August 1999. Costco Wholesale Corporation was founded in 1976 and

is based in Issaquah, Washington.

Source: FinViz.com, October 2019Costco Wholesale Corporation (COST)

POSITIVES: In the evolving retail ecosystem, Costco has been able to create a niche for itself on the back of

growth strategies, better price management, strong membership trends and increasing penetration of e-

commerce business. Certainly, these helped the company to continue with its decent comparable sales run.

Definitely, improving job prospects and rising disposable income have also aided the performance. We believe

that Costco continues to be one of the dominant retail wholesalers based on the breadth and quality of

merchandise offered. The company’s strategy to sell products at heavily discounted prices has helped it to

remain on a growth track as cash-strapped customers continue to reckon Costco as a viable option for low-cost

necessities. The company is also gradually expanding its e-commerce capabilities in the U.S., Canada, U.K.,

Mexico, Korea and Taiwan. To drive its online sales further, Costco launched new delivery services for its

customers, one CostcoGrocery option to deliver non-perishable items to buyer’s home within two days of

ordering and another same day grocery delivery service in collaboration with Instacart. Costco continues to

make prudent use of its cash flow through share repurchases and dividend payments. During the fourth

quarter, the company bought back shares worth of $52 million bringing the total to $247 million in fiscal 2019.

We are also encouraged by the company’s expansion strategy. Costco has one of the highest square footage

growth in the industry, and remains committed to opening new clubs in the domestic and international

markets. In our view, the company’s diversification strategy is a natural hedge against risks that may arise in

specific markets.

Possible concerns: Costco faces stiff competition from BJ’s Wholesale Club and Sam’s Club, a division of Wal-

Mart Stores. These two rivals follow similar business models as they market high volumes of merchandise at

low prices in a membership-only warehouse clubs. The company’s customers are very sensitive to

macroeconomic factors including interest rate hikes, increase in fuel and energy costs, sluggishness in the

housing market, unemployment levels, and high household debt levels, which may affect their spending levels.

Source: Zacks Research, October 2019CVS Health Corporation (CVS)

CVS Health Corporation provides health services and plans in the United States. Its Pharmacy Services

segment offers pharmacy benefit management solutions, such as plan design and administration,

formulary management, retail pharmacy network management, mail order pharmacy, specialty

pharmacy and infusion, Medicare Part D, clinical, disease management, and medical spend

management services. The company's Retail/LTC segment sells prescription drugs and general

merchandise, such as over-the-counter drugs, beauty products, cosmetics, and personal care

products, as well as provides health care services through its MinuteClinic walk-in medical clinics.

Its Health Care Benefits segment offers traditional, voluntary, and consumer-directed health

insurance products and related services, including medical, pharmacy, dental, behavioral health,

medical management, Medicare plans, PDPs, Medicaid health care management services, workers'

compensation administrative services, and health information technology products and services.

The company's customers include employers, insurance companies, unions, government employee

groups, health plans, Medicare Part D prescription drug plans, Medicaid managed care plans, plans

offered on public health insurance exchanges and private health insurance exchanges, other

sponsors of health benefit plans, individuals, college students, workers, labor groups, and

expatriates. As of December 31, 2018, it had approximately 40 leased on-site pharmacies, 25

leased retail specialty pharmacy stores, 20 specialty mail order pharmacies, and 90 branches for

infusion and enteral services; and 9,900 retail locations and 1,100 MinuteClinic locations, as well as

operated an online retail pharmacy Websites, LTC pharmacies, and onsite pharmacies. The

company was formerly known as CVS Caremark Corporation and changed its name to CVS Health

Corporation in September 2014. CVS Health Corporation was founded in 1963 and is

headquartered in Woonsocket, Rhode Island.

Source: FinViz.com, October 2019CVS Health Corporation (CVS)

POSITIVES: Over the past three months, CVS Health outperformed its industry. The stock gained 15.7%, in

comparison to the 8.9% growth of the industry. Following the colossal 70-billion acquisition of health insurance giant

Aetna for a colossal sum of $70 billion, CVS Health has introduced a new business arm called Health Care Benefits.

This segment has already started to show strong momentum, particularly in government business. With regard to its

2020 PBM selling season, CVS Health has noted that, as of June, its gross new businesses increased by $600 million

with net new business improving by about $1.4 billion. : The soaring demand for specialty pharmacy, especially in

the on-going decade, is likely to accelerate growth for the company. This time the company encouragingly noted that

despite a slowdown in revenue growth compared to prior years on lower levels of inflation on specialty drugs and

increase in generic dispensing, the company registered strong performance overall. We are optimistic about

domestic demographic trends, which are expected to drive utilization rates for years to come as the population ages.

CVS Health exited the second quarter of 2019 with cash and cash equivalents of $6.06 billion compared with $5.89

billion at the end of the first quarter. Year-to-date, net cash provided by operating activities was $7.29 billion, as

compared to $5.29 billion a year ago. This remains perfectly on track with the company's free cash expectations for

the year.

Possible concerns: Rising pressure to reduce reimbursement rates for generic drugs, disappointing retail

performance, highly competitive market and pressure on margins provide stiff challenges to CVS Health. CVS Health

expects 2019 to be a transition year as it integrates the Aetna and expects that the following challenges may have

certain adverse impact on the operating income of its Pharmacy Services and Retail/LTC segments in 2019 compared

to 2018. Despite significant new client wins in the course of a strong selling season, intense competition and tough

industry conditions act as major impediments. Major competitors such as Walgreens, Target and Wal-Mart are

expanding their pharmacy businesses.

Source: Zacks Research, October 2019The Walt Disney Company (DIS)

The Walt Disney Company, together with its subsidiaries, operates as an entertainment company

worldwide. The company's Media Networks segment operates cable programming businesses under

the ESPN, Disney, and Freeform brands; broadcast businesses, including ABC TV Network and eight

owned television stations; and radio businesses. It also produces original live-action and animated

television programming to first-run syndication and television markets; and subscription video-on-

demand services and in home entertainment formats, as well as operates ESPN+, a direct-to-

consumer streaming service providing multi-sports content. Its Parks and Resorts segment owns and

operates the Walt Disney World Resort in Florida and the Disneyland Resort in California. This

segment also operates Disney Resort & Spa in Hawaii, Disney Vacation Club, Disneyland Paris, Disney

Cruise Line, and Adventures by Disney; and manages Hong Kong Disneyland Resort and Shanghai

Disney Resort, as well as licenses its intellectual property to a third party for the operations of the

Tokyo Disney Resort in Japan. The company's Studio Entertainment segment produces and acquires

live-action and animated motion pictures for distribution in the theatrical, home entertainment, and

television markets primarily under the Walt Disney Pictures, Pixar, Marvel, Lucasfilm, and Touchstone

banners. This segment also produces stage plays and musical recordings; licenses and produces live

entertainment events; and provides visual and audio effects, and other post-production services. Its

Consumer Products & Interactive Media segment licenses its trade names, characters, and visual and

literary properties; develops and publishes mobile games, books, magazines, and comic books;

distributes branded merchandise directly through retail, online, and wholesale businesses; offers

Website management and design; and develops and distributes online video content. The company

was founded in 1923 and is based in Burbank, California.

Source: FinViz.com, October 2019The Walt Disney Company (DIS)

POSITIVES: Disney completed the acquisition of Twenty-First Century Fox. The majority of Fox’s assets

acquired contribute to Disney’s content portfolio. Fox’s television business is expected to help the company

strengthen its TV slate globally, which has been facing some issues in terms of distribution or subscribers.

Disney’s international footprint will increase substantially post the acquisition. Notably, Fox Networks

International operates above 350 channels in 170 countries, while Star India has 69 channels serving 720

viewers per month. Disney’s Studio Entertainment segment has an impressive line-up of big budget movies

slated to be released over the next 18 months. Additionally, following Fox’s acquisition, the company’s slate of

movies releases have increased. The movies scheduled to release till Christmas include Maleficent: Mistress of

Evil, from Disney; Frozen 2 from Disney Animation; and Star Wars: The Rise of Skywalker as well as Stuber, The

Art of Racing in the Rain, Ready or Not, Ad Astra, Woman in the Window, Ford V. Ferrari, and Spies in Disguise

from the Fox Studios. Disney plans to launch its own direct-to-consumer service by November this year in the

United States. The service called Disney+ is expected to be launched in European markets in the near future.

Notably, Disney+ will feature exclusive content from Disney, Pixar, Marvel, Star Wars, National Geographic

content and Lucasfilm. Additionally, users will have access to the company’s film and television library content,

including all the theatrical releases starting with the 2019 slate. Further, to support its direct-to-consumer

(DTC) business, Disney is looking to boost FX network’s production capacity. The company is also working with

National Geographic to bring its content to its DTC platforms.

Possible concerns: Higher programming costs at ESPN, heavy investments in ESPN+ and Disney+ and softness

experienced in tourism and consumer confidence in China are factors that may hamper growth in the near

term.

Source: Zacks Research, October 2019Alphabet Inc. (GOOGL)

Alphabet Inc. provides online advertising services in the United States, Europe, the Middle East,

Africa, the Asia-Pacific, Canada, and Latin America. It offers performance and brand advertising

services. The company operates through Google and Other Bets segments. The Google segment

offers products, such as Ads, Android, Chrome, Google Cloud, Google Maps, Google Play,

Hardware, Search, and YouTube, as well as technical infrastructure. This segment also offers

digital content, cloud services, hardware devices, and other miscellaneous products and services.

The Other Bets segment includes businesses, including Access, Calico, CapitalG, GV, Verily,

Waymo, and X, as well as Internet and television services. Alphabet Inc. was founded in 1998 and

is headquartered in Mountain View, California.

Source: FinViz.com, October 2019The Alphabet Inc. (GOOGL)

POSITIVES: Alphabet is showing increased appetite in the Home Assistant space. The company made its foray

into this market in 2016 with the launch of Google Home. Google Home performs an array of tasks such as

playing music, reading books, managing calendars, answering queries, searching places, calling over cabs,

controlling smart home devices and so on. It runs on Google’s new voice assistant. Alphabet focuses on

innovation, launching products and services for multiple industries. The development and enhancements of its

search technology over time has created win-win situations wherein buyers, sellers and the public at large were

benefited. The success of this strategy led to very strong growth since inception. Google has been growing

rapidly in this fast-growing highly-competitive cloud market. The company has signed many partnerships and

has been opening data centers to extend its cloud footprint worldwide. Alphabet and Cisco announced a

partnership per which the duo will deliver an open hybrid cloud solution. The solution will enable usage and

management of applications and services across on-premises setups and the Google Cloud Platform. Google has

also partnered with Nutanix for hybrid cloud computing. The Google search engine is advanced, simple and

adaptable, all at once. This is the main reason for its leading search market share. A Jul 2016 global desktop

search market share report from netmarketshare.com says that Google had 72.5% of market share, followed by

Bing’s 10.4%, Yahoo’s 7.8% and Baidu’s 7.2%. In mobile, Google was even more dominant with a 94.9% share of

the search market globally, compared to Yahoo’s 3.0% and Bing’s 1.1%. Although the desktop was the most

popular computing device in the past, mobile search is now equally if not more popular. Alphabet has a number

of mobile initiatives. First, it is leveraging its Android OS not just to build search market share but also to drive

sales of apps and digital products through Google Play. The company continues to bring improvements with

each version of the OS, at the same time spurring app development. Online and mobile video consumption is

soaring and Alphabet remains strongly positioned here with the YouTube platform.

Possible concerns: Alphabet’s diversification strategy involves significant investment in mobile, cloud, devices

and digital goods. Growing competition and legal hassles are other headwinds.

Source: Zacks Research, September 2019Goldman Sachs Group Inc. (GS)

The Goldman Sachs Group, Inc. operates as an investment banking, securities, and investment

management company worldwide. It operates in four segments: Investment Banking, Institutional Client

Services, Investing & Lending, and Investment Management. The Investment Banking segment provides

financial advisory services, including strategic advisory assignments related to mergers and acquisitions,

divestitures, corporate defense activities, restructurings, spin-offs, and risk management; and

underwriting services, such as debt and equity underwriting of public offerings and private placements

of various securities and other financial instruments, as well as derivative transactions with public and

private sector clients. The Institutional Client Services segment is involved in client execution activities

related to making markets in cash and derivative instruments for interest rate products, credit products,

mortgages, currencies, commodities, and equities; and provision of securities services comprising

financing, securities lending, and other brokerage services, as well as the marketing and clearing of

client transactions on various stock, options, and futures exchanges. The Investing & Lending segment

invests in and originates longer-term loans; and makes investments in debt securities and loans, public

and private equity securities, and infrastructure and real estate entities, as well as provides unsecured

and secured loans through its digital platforms. The Investment Management segment offers

investment management services; and wealth advisory services consisting of portfolio management,

financial planning and counseling, and brokerage and other transaction services. The company serves

corporations, financial institutions, governments, and individuals. The Goldman Sachs Group, Inc. was

founded in 1869 and is headquartered in New York, New York.

Source: FinViz.com, October 2019Goldman Sachs Group Inc. (GS)

POSITIVES: The key source of Goldman’s earnings stability is its business diversification. Within

traditional banking, a diversified product portfolio has better chances of sustaining growth than many

other banks, which have exited some of these areas. Notably, Goldman has been undertaking initiatives

to boost the GS Bank’s business with its acquisition of the online deposit platform of GE Capital Bank in

April 2016. Though Goldman recorded 8% decrease in investment banking revenues in the first nine

months of 2019, affected by weak underwriting business, revenues recorded a three-year (2016-2018)

CAGR of 12% providing a decent support to Goldman’s top-line growth despite lower industry-wide

transactions in 2016. Nevertheless, M&A activities were strong in 2018, with the execution of many

large transactions. Steady economic growth and low interest rates in the emerging economies, along

with growth in corporate earnings on tax reforms, are likely to keep the momentum alive in the quarters

ahead. Moreover, Goldman’s solid position in worldwide announced and completed M&As will likely

give it further edge over its peers. Goldman has benefited for the past few years from its successful

expense-reduction initiatives. Backed by a solid capital position, Goldman has consistently enhanced

shareholders’ value with steady capital-deployment activities. The company’s approved 2019 capital

plan includes up to $7 billion in repurchases and $1.8 billion in total common stock dividends beginning

third-quarter 2019 through second-quarter 2020.

Possible concerns: Muted trading activities aided by low client activity may hinder top-line growth of

Goldman. Further, legal hassles and higher dependence on overseas revenues remain other headwinds

for the company.

Source: Zacks Research, October 2019GlaxoSmithKline plc, (GSK)

GlaxoSmithKline plc engages in the creation, discovery, development, manufacture, and

marketing of pharmaceutical products, vaccines, over-the-counter medicines, and health-

related consumer products in the United Kingdom, the United States, and internationally. It

operates through four segments: Pharmaceuticals, Pharmaceuticals R&D, Vaccines, and

Consumer Healthcare. The company offers pharmaceutical products comprising medicines

in the therapeutic areas, such as respiratory, HIV, immuno-inflammation, anti-virals, central

nervous system, cardiovascular and urogenital, metabolic, anti-bacterials, and

dermatology. It also provides consumer healthcare products in wellness, oral health,

nutrition, and skin health categories primarily under the Sensodyne, parodontax, Poligrip,

Voltaren, Panadol, Otrivin, and Theraflu brand names. The company offers its consumer

healthcare products in the form of nasal sprays, tablets, syrups, pods, lozenges, gum and

trans-dermal patches, caplets, infant syrup drops, gels, effervescents, toothpastes,

toothbrushes, mouthwashes, denture adhesives and cleansers, topical creams and non-

medicated patches, and malted drinks and foods. It has collaboration agreements with

23andMe; Liquidia Technologies, Inc.; SpringWorks Therapeutics, Inc.; Merck KGaA.; and

Lyell Immunopharma. GlaxoSmithKline plc was founded in 1715 and is headquartered in

Brentford, the United Kingdom.

Source: FinViz.com, October 2019GlaxoSmithKline plc, (GSK)

POSITIVES: Glaxo's three newest products — Trelegy Ellipta, Shingrix and Juluca — are doing well. They coupled

with buyout of Novartis’ stake in the Consumer Healthcare JV have strengthened its competitive position. The

company’s diversified base and presence in different geographical areas should help support revenues.

Expansion into markets like Japan and emerging markets should provide new opportunities for growth. The

company has made significant progress in expanding its presence in emerging markets by acquiring product

portfolios from companies like Bristol-Myers and UCB. Glaxo is focused on oncology, immuno-inflammation, HIV

and respiratory therapeutic areas. The company has terminated or divested around 80 pipeline programs since

2017 as those showed less potential to succeed, allowing the company to focus more on the most promising

assets. Glaxo has had major positive data read-outs on multiple new medicines in HIV, oncology, immuno-

inflammation and respiratory in 2019 so far with many other scheduled for the second half. The successful

development and commercialization of the pipeline candidates should boost the company’s top line. Glaxo has

made a significant progress in its oncology pipeline recently and now has 16 assets in development, double from

8 as of July 2018. Glaxo has delivered annual cost savings of more than £3 billion following the Novartis

transaction. These cost savings have helped the company overcome pricing pressure and decline in sales of key

brands like Seretide/Advair/Avodart despite significant promotional investment behind new products

Possible concerns: A generic version of its top-selling drug Advair has been launched, which is significantly

eroding Advair’s sales. Glaxo’s top line is under significant pressure due to generic competition faced by key

products. Products like Lovaza and Avodart are facing declining sales due to intense generic competition. In

addition to facing generic competition, most of Glaxo’s products are up against significant competition from

small as well as large pharmaceutical companies. Advair is facing stiff competition in the COPD and asthma

market from AstraZeneca’s and Merck’s respiratory disease drugs. Glaxo’s Consumer Healthcare segment faces

competition from big companies like Colgate-Palmolive, Johnson & Johnson, Procter & Gamble and Pfizer.

Glaxo’s Consumer Healthcare business has been affected by certain supply interruptions. In addition, there are

many small companies that compete with Glaxo in certain markets. Loss of market share due to intense

competition will severely impact Glaxo’s top line.

Source: Zacks Research, October 2019You can also read