Deleveraging Europe 2019: Focus on France - October 2019 - PATRIMOINE24

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Deleveraging Europe 2019: Focus on France October 2019

Deleveraging Europe 2019: Focus on France

Executive summary

The European loan portfolio market marked a record year with more than €200bn traded

in 2018. The contribution of the French market was underwhelming. But why? Healthy

economic indicators, a significant market size, regulatory pressure and a robust legal

environment along with a scaling loan servicing landscape and progress in data quality

make France an attractive market for investing in distressed assets.

Readiness Readiness Readiness

Macroeconomic Market landscape Legal and regulatory

environment With the second largest pool of non- environment

Despite a recent tempering in economic performing loans (NPL) in Europe, The legal and regulatory framework

outlook, the French market has seen and despite an NPL ratio below in France supports effective NPL

sustained growth in recent years the European average, pressure resolution. The implementation of

with confidence returning. While less is mounting on French banks to macro prudential regulation and

impacted than other countries following deleverage. Growing loan activity supervisory guidance across the

the global financial crisis, France still fueled by low interest rates combined banking system, a balanced and

maintains a high public and private debt with restrained loan sales positions efficient legal system and the current

level. The macroeconomic outlook is France to overtake more saturated political stability favour the French NPL

conducive to attracting investors to the markets, justifying the challenges faced market.

distressed assets space. by investors entering a new market.

Readiness Readiness

Quality of information Servicing capacity

Collection and reporting of key NPL Despite historically low NPL sales,

information is a challenging area in the debt servicing infrastructure is

France, but it is gradually improving. relatively developed with the presence

While the banking system provides of six of the top 10 European credit

for consistent loan classification and management players. Until now,

NPL identification, key measures on most NPL trades have gone to local

information quality have not been debt purchasers who service their

systemically implemented. As NPL sales own assets. Still, a few international

increase, the quality and volume of distressed asset funds are venturing

information made available to potential into the market and larger foreign

investors has improved. investors are waiting on the sidelines

for the first signs of market growth.

02

Brochure / report title goes here |

Section title goes here

Contents

Macroeconomic environment 04

Market landscape 08

Legal and regulatory 16

Quality of information 29

Servicing capacity 32

What’s next? 39

Contacts 40

03

Deleveraging Europe 2019: Focus on France

Macroeconomic

environment

Notwithstanding a slump in implemented a countercyclical

the economic forecast, France capital buffer (CCyB) to mitigate

is posting GDP growth aligned the risk of recession, the number

with the European average of individual and corporate

and an unemployment rate bankruptcies decreased.

that declined for the fourth Macroeconomic policies, alongside

consecutive year. Lending to limited NPL resolution, have

households and corporates produced a significant quantity of

continued to increase at a 6% distressed assets to spur market

rate in 2018, and while the French development.

banking supervisory authorities

04

Deleveraging Europe: Focus on France | Non-performing loan market in France

Deleveraging Europe 2019: Focus on France

Deleveraging Europe: Focus on France | Non-performing loan market in France

French economic

French economic indicators

indicators

French economic indicators

Following real GPD growth of 2.3% Nominal GDP growth

Nominal GDP growth

inFollowing

2017, the real GDP growth of 2.3% in

highest level in the six

2017, the years,

previous highest French

level in the six previous

economic 3%

years, French

growth was more economicsubduedgrowthinwas 2018 at

Following real GPD growth of 2.3% Nominal GDP growth

1.7%. Social unrest

more subdued in 2018that at 1.7%.started

Social at

in

the 2017,

endthat

unrest the

of 2018 highest

starteddisrupted level in

at the end economic the

of 2018 six

previous

activities years,protests

French continuing

economic (1%)

disruptedwith economic activities with 3%

growth

into 2019,wasresulting

more subdued in a in 2018 at

decreased

protests continuing into 2019, resulting

1.7%.

GDP Socialforecast

growth unrest that of 1.3%started forofat

in aend

the decreased GDP growth forecast

2019. Anofeconomic

2018 disrupted

slowdown economic

is (5%)

1.3% for 2019.

activities with An economic

protests slowdown is

continuing (1%)

widespread among European 2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

widespread

into

GDP

2019,

growth

the GDP of the

p.5

among European

resulting

countries as the GDP of the Euro

forecast

Euro area

in a countries as

decreased

ofincreased

1.3% forby 1.9%

area increased by 1.9% in 2018, (1)

2019.

in 2018, Ancompared

economic toin slowdown

2.4% in 2017.is France Euro area

compared to 2.4% 2017. (5%)

widespread among European

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Note:

Note: (1) (1 ) Euro area includes 19 countries

Euro area includes 19 countries

countries as the GDP of the Euro Source: Eurostat

Source: Eurostat

area increased by 1.9% in 2018, (1)

France Euro area

compared to 2.4% in 2017.

Note: (1 ) Euro arearate

Unemployment

Unemployment

includes 19 countries rate

A Adecreasing

decreasing trend trend in in

thetheunemployment

Source: Eurostat

unemployment

rate was observed rate

acrosswasmost observed

European

12%

across

countries most withEuropean

unemployment countriesdecreasing 12%

with

fromunemployment

12% in 2013 to 8.2% decreasing

in 2018 in the Unemployment rate

A decreasing

from 12% trend

in 2013 in the

toKingdom

8.2% in 2018

Euro area.

unemployment The United

rate is driving

in the Euro area. Thewas Unitedobserved

the improvement

across most with levels

European significantly

countries

Kingdom is driving the 8%

12%

below

with that of

unemployment other European

decreasing countries. 8%

improvement with levels

from 12% in

The French

significantly 2013 to

unemployment

below that 8.2%ofrate in

other 2018

declined

in the Euro area. The

European countries. The French at

for the fourth consecutive United

year, but,

Kingdom

9.1%, remains

unemployment is driving

above the

ratethe Euro area

declined foraverage

the 4%

8%

2006 2006

2007 2007

2008 2008

2009 2009

2010 2010

2011

2012

2013

2014

2015

2016

2017

2018

improvement

fourth consecutive

and represents with levels

year,highest

the fourth but atrate in

significantly

9.1% remains below

above that theofEurootherarea 4%

Europe behind Greece, Spain and Italy.

European countries. The French

2011

2012

2013

2014

2015

2016

2017

2018

average and represents the fourth France Euro area (1)

unemployment rate declined for the 4%

highest rate in Europe, behind

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Note: (1 ) Euro area includes 19 countries

fourth

Greece,consecutive

Spain and Italy. year, but at Source: Eurostat (1 )

9.1% remains above the Euro area France Euro area

average and represents the fourth France Euro area (1)

Note:

Note:

(1)

Euro (1)area includes 19 countries

Euro area includes 19 countries

highest rate in Europe, behind Note:

Source:(1 ) Euro area includes 19 countries

Eurostat

Source: Eurostat

Greece, Spain and Italy. Source: Eurostat Gross public debt level (% GDP)

Gross public debt in France reached

€2.3 trillion at the end of 2018 100%

Gross public debt in France reached €2.3 Gross public debt level (% GDP)

representing 98% of GDP. This

trillion at the end of 2018, representing Gross public debt level (% GDP)

upward trend since the 2008 financial

Gross

98% of public

GDP. This debt in France

upward trend reached

since 80%

crisis results in France having thethe 100%

€2.3

2008trillion

sixth financial

highest atgross

the results

crisis end

public ofin2018

Franceinhaving

debt

representing

the sixthIn

Europe. highest 98% gross

contrast, of levels

GDP. debt

public This in

decreased 60%

upward

inEurope.

the Unitedtrend sincelevels

In contrast,

Kingdom thebetween

2008 financial

decreased in the

2016 80%

crisis

and

United

results

2018 by in

Kingdom 0.6%Franceandhaving

between in the

2016 and

the

rest

2018 of

sixth

the highest gross public debt in 40%

by Euro

0.6% and area by rest

in the 2.3%. of the Euro area by

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Europe. In contrast, levels decreased 60%

2.3%. © 2019 Deloitte SAS. Document Confidentiel Masq

in the United Kingdom between 2016

and 2018 by 0.6% and in the rest of (1)

France Euro area

the Euro area by 2.3%. 40%

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Note: (1 ) Euro area includes 19 countries

Source: Eurostat

(1) 5

France Euro area

Note:

Note: (1)

EuroEuro

(1 )

areaarea includes

includes 19 countries

19 countries

Source: Eurostat

Source: Eurostat 5

05

Deleveraging Europe 2019: Focus on France

Dynamic credit conditions

p.6 and the countercyclical buffer

Lending to households and non-financial Consumer/ Corporate lending and ECB refinancing rate (YoY growth)

companies continued to increase in 2018,

with an annual growth rate of 6% between 16%

Dec-17 and Dec-18, propelled by the low

interest rate environment. 12%

The French supervisory authorities first

8%

employed a countercyclical capital buffer

in Jun-18 when they raised the buffer from

4%

zero to 0.25% of Risk Weighted Assets

(RWA). As a result of the high credit to GDP

-

gap, the CCyB will be increased to 0.5%

from Apr-20. ( 4%)

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Other euro area countries introduced

similar buffers with Germany announcing Consumer financing Corporate financing

a 0.25% buffer, applicable as of Jul-20

p.6(2)

Source: Banque de France and ECB

Source: Banque de France and ECB

in an effort to hedge against recession

uncertainty.

Despite the safeguarding actions,

continued growth in consumer and

corporate lending in France may slow as Evolution of CCyB notified to ESRB (Jul-19)

© 2019 Deloitte SAS. Document Confidentiel Masque Deloitte 4:3 p

an economic downturn could lead to a

renewed credit crunch.

IS

1.75%

CZ

1.5%

SK

1.25%

GB LT IE

1.0% 1.0% 1.0%

FR

0.25%

T3 2018 T4 2018 T1 2019 T2 2019 T3 2019

Date of last update

Note: Upward/stable arrow represents increase/stability of the CCyB at the date of last

update

Source: European Systemic Risk Board (ESRB)

© 2019 Deloitte SAS. Document Confidentiel Masque De

06Deleveraging Europe 2019: Focus on France

p.7 bankruptcies

Consumer and corporate

The number of corporate bankruptcies in Corporate bankruptcies by company size (000)

France remained largely stable between

2017 and 2018 at 54,000. Bankruptcies 70 63 63 62 63

60 60 61

are triggered by micro-enterprises and 56 58

60 54 54

very small enterprises (VSE), representing

50

on average 98% of total corporate

bankruptcies. Small and medium 40

entreprises (SME) and large corporates 30

made up the remainder with 1,149 and 20

39 bankruptcies, respectively, in 2018.

10

Outstanding loans of companies filing for

0

bankruptcy in 2018 represented 0.3% of 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

total outstanding loans in France. VSE SME Large corporate

Despite a downward trend since 2015, the p.7 (2)

number of bankruptcies is expected to Note: Company size is defined according to legal units

marginally increase in 2019 as the global Source: Banque de France

economy is facing difficulties.

© 2019 Deloitte SAS. Document Confidentiel Masque Deloitte 4:3 p

The number of households applying to the Household overindebtedness (000)

Banque de France (BDF) overindebtedness

plan continued to decrease in 2018 to 218

232

221 223 231

240 216 217

163,000, of which 91% were considered 194

200 188 181

eligible for assistance from the household 163

debt commission. This level, which has not 160

been observed since 2003, represents 120

€35 billion of overindebtedness

80

outstanding. The sharp decrease in the

last four years is attributable in part to the 40

low interest rate environment and public -

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

policies that better protect households

Source: Banque de France

against abusive lending practices.

Source: Banque de France

© 2019 Deloitte SAS. Document Confidentiel Masque Deloitte 4:3

07Deleveraging Europe 2019: Focus on France

Market

landscape

With the second largest NPL Coupled with regulatory

pool in Europe and emerging pressure, profitability underpins

deleveraging activity, France is on banks’ reinforced focus on NPL

course to have the highest NPL resolution strategies. Meanwhile,

stock in Europe. While the large run-off banks are continuing

French banking groups that share the wind-down of their assets,

85% of the market are decreasing and smaller players, such as

NPL volumes outside of France, consumer captives and Fintechs

the stock of French distressed with growing distressed assets,

assets has been stagnant over the will bring small and mid-sized

past five years. portfolios to market.

08Deleveraging Europe 2019: Focus on France

p.9

France in the context of European NPLs

France has consistently maintained an €636bn stock of NPLs held by European banks (Jun-19)

NPL ratio below the European average,

140 45%

decreasing further since Mar-15 to 40%

120

reach 2.6% as at Jun-19. In contrast, the 35%

100

corresponding NPL outstanding held by 30%

French banks remains the second largest 80 25%

20%

stock in Europe after Italy. While French 60

15%

banks decreased their NPL exposure to 40

3.0% 10%

€124 billion as at Jun-19 from €140bn as at 20 European

a ve ra ge 5%

Jun-17, this was driven by large NPL sales in 0 0%

other European jurisdictions and, notably,

IT FR ES GR GB NL DE PT BE AT DK IE FI CY PL SE NO HU HR LU

in Italy.

NPLs (€bn) NPL ratio

Note: The graph presents only the top 20 European countries in terms of gross NPL

stock, whereas the European average includes data for all European countries

Source: European Banking Authority Risk Dashboard 2Q 2019

p.9 (2)

Contrary to the €124 billion NPLs held by NPLs and provisioning ratio in France (€bn)

French banks, the stock of non-performing

loans owned in France totaled €70 billion as

at Dec-18, a level that has remained stable 80 60%

over the last five years. Banks’ provisioning

ratio, intended to cover prospective losses © 201960Deloitte SAS. Document Confidentiel 50%

on NPLs, increased to 51% in 2018, a 2%

40 40%

year-over-year (YoY) variance. Recent EU-

wide regulatory guidelines will undoubtedly

20 30%

have an impact on the provisioning ratio as

banks are directed to provision unsecured

- 20%

NPLs at 100% three years after default. 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

With NPL resolution strategies targeting a Gross NPL Provisioning Ratio

rapid clean-up of banks’ balance sheets, Source: Banque de France

Source: Banque de France

an acceleration of NPL disposals is forecast

despite the overall low NPL ratio in France.

© 2019 Deloitte SAS. Document Confidentiel Masque Deloitte 4:3 pour

09Deleveraging Europe 2019: Focus on France

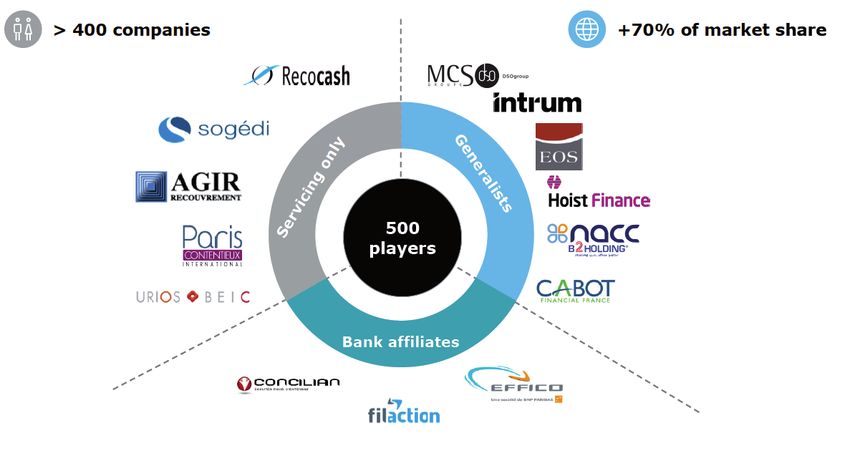

The French banking landscape

The French banking market consists of centralised, banking groups, which account for over 85% of market

mutual and cooperative banking groups, consumer share. The level of centralisation is a key factor in NPL

finance companies, foreign and independent banks, disposal maturity, while regional banks are frequent

Fintech companies and consumer captives. The seemingly sellers of small portfolios via limited auction processes

fragmented market is in fact dominated by the top six or bilateral transactions.

+85% of the French banking market

Centralised Mutual & Consumer Foreign/

New players/ Consumer

Category banking cooperative finance independent

Fintechs captives

groups banking groups companies banks

Examples

Mortgage Mortgage Mortgage Mortgage Mortgage Mortgage

Credit Consumer Consumer Consumer Consumer Consumer Consumer

offering SME SME SME SME SME SME

Corporate Corporate Corporate Corporate Corporate Corporate

- + - + - + - + - + - +

Size

Centralised - + - + - + - + - + - +

NPL sale - + - + - + - + - + - +

activity

Source: Deloitte analysis

10Deleveraging Europe 2019: Focus on France

The six largest French banks dominate the French As retail banking represented 63% of aggregated NBI in

banking market: BNP Paribas (BNPP), Société Générale 2018, NPL monitoring and delinquency resolution are

(SG), BPCE Group (BPCE), Crédit Agricole Group (CAG), key components of profitability. A significant NPL stock

Crédit Mutuel Alliance Fédérale Group (CMG) and La also affects operating performance as both human

Banque Postale (LBP). Despite disparities between capital and financial resources are engaged in credit

banks, the aggregated Net Banking Income (NBI) management procedures, thus curtailing new lending

of the top six increased by 0.9% between 2017 and activities.

2018 to reach €148bn in 2018. Overall, corporate and

investment banking revenue decreased by 6%, while

asset management and insurance and retail banking

activities increased by 6% and 1%, respectively.

p.11

Breakdown of the top six French banks NBI (2018)

• BNP Paribas • Société Générale • BPCE

14% 7%

20%

2018 32% 2018 2018

25%

€43bn

€43bn €25bn

€25bn 13% €24bn

€24bn

61% 61%

67%

• Crédit Agricole SA • Crédit Mutuel • La Banque Postale

16% 7%

20%

2018 6% 2018 2018

17% €33bn

€33bn €18bn

€18bn €6bn

€6bn

67%

74%

93%

Retail banking CIB Other activities

Source: Bank annual reports

© 2019 Deloitte SAS. Document Confidentiel Masque Deloitte 4:3 pour projection 9

11Deleveraging Europe 2019: Focus on France

p.12

p.12

Are French banks less profitable than their EU counterparts?

1.Cost

1. Costof

ofrisk

riskto

tototal

totalassets

assets(2018)

(2018)

Combined cost of risk (CoR) of the top six Cost of risk to total assets (2018)

French banks decreased by 6.4% between

2017 and 2018, as reductions in levels of 0.13%

0.13% 0.12%

0.12%

non-performing loans led to lower NPL ratios. 0.10%

0.10%

0.09%

0.09%

However, three banks still have a CoR to total 0.08%

0.08% 0.09%

0.09%

balance sheet ratio that is above the 2018

0.05%

0.05%

European median of 0.09%.

BNPP

BNPP SG

SG CAG

CAG BPCE

BPCE CMG

CMG LBP

LBP

Costofofrisk

Cost risktotoaverage

averagetotal

totalassets

assets Europeanmedian

European median

Source:

Source:

Source: Autorité

Autorité deContrôle

Contrôle

de contrôle

Autorité de Prudentiel

prudentiel etde

deRésolution

Résolution

et de résolution

Prudentiel et (ACPR) (ACPR)

(ACPR)

2.Cost

2. Costtotoincome

incomeratio

ratio(2018)

(2018)

The cost to income ratio remains a leading Cost to income ratio (2018)

concern as it has continued to increase

79%

79%

since 2015. Operating expenses of French 71%

71% 70%

70%

73%

73%

banks, mainly under pressure from costly 65%

65% 65%

65%

restructuring plans, increased faster than their 64%

64%

net income in 2018. This resulted in a 0.8%

increase in the average cost to income ratio

of French banks to 70.2% in 2018, a level that

is on average 6% higher than the European

median.

BNPP

BNPP SG

SG CAG

CAG BPCE

BPCE CMG

CMG LBP

LBP

Costto

Cost toincome

incomeratio

ratio Europeanmedian

European median

Source:ACPR

Source:

Source: ACPR

ACPR

©©2019

2019Deloitte

DeloitteSAS.

SAS.Document

DocumentConfidentiel

Confidentiel

f risk to total assets (2018) 3. Return on equity (2018)

The profitability of the top French banks, Return on equity (2018)

measured by their Return on Equity (RoE),

increased to 6.7% in 2018 from 6.3% in 7.6% 7.1% 7.7%

6.8% 6.7% 7.5%

2017; however, French banks on the whole

3% remain less profitable than their European

0.12% 5.3%

counterparts. Similarly, the average Return

0.10%

0.09%

on Assets (RoA) of the same French sample

0.08% 0.09%

reached 0.38% in 2018, below the European

median of 0.51%. 0.05%

PP SG CAG BPCE CMG LBP

BNPP SG CAG BPCE CMG LBP

of risk to average total assets European median

Return on equity European median

e: Autorité de Contrôle Prudentiel et de Résolution (ACPR)

Source:

Source: ACPR

ACPR

o income ratio (2018)

12

79%

70% 73%

65% 65%Deleveraging Europe 2019: Focus on France

Gross NPL exposure held by top French banks

p.13

The cumulative NPLs of the six largest French 1. Gross

Gross NPL NPL

NPLs and and ratio

NPL (1)

ratio

(€bn,(€bn, Dec-18)

Dec-18)

banks totaled €112 billion as at Dec-18 with a

corresponding average NPL ratio of 3%, varying

p.13

among the French groups from 1.5% to 4.3%.

40 4.3% 5%

BNPP was the most exposed to credit risk with 3.6%

3.2% 3.0% 4%

1. Gross NPL and NPL ratio

€34 billion of NPL outstanding in 2018, and La(€bn, 30

Dec-18)

Banque Postale had the lowest level with NPLs

2.6%

3%

of just €1 billion.

40 4.3% 20 5%

The overall level of NPLs decreased further 34 1.5% 2%

for French banks as at Jun-19,3.6%

which should 4%23

30 3.2%10 3.0% 21

be reflected in the individual bank's exposure 18 1%

2.6% 14

once the results of the 2019 EU-wide 3% 1

20 exercise are published.

transparency - 0%

34 BNPP 1.5%

SG CAG

2% BPCE CMG LBP

10 23 21 Gross NPL NPL ratio

18 1%

14

Note: Gross NPLs of French banks held in France and abroad

(1)

1

Source: Company annual reports and financial statements

- 0% Hou

BNPP SG CAG BPCE CMG LBP 2%

5% Hou

Gross NPL NPL ratio 17%

Non-performing exposures are composed NPLs by loan type(1) (Jun-18) SME

26%

of residential mortgages and consumer

Household -Total NPL

Mortgage SME

loans, and SME and corporate loans in equal 2. NPL by loan type (June-18)

2% €86bn 17%

proportions. The only comparable measure 5% Household - Other SME

of this breakdown for the top five French 17%

banks is based on the Internal Rating-Based SME - Corporate Corp

26% 17% 11%

(IRB) reporting published by the EBA annually. 5% Corp

Total NPL SME - Mortgage

2. NPL

Defaulted by loan

exposures type

using (June-18)

this approach

€86bn 17%

totaled €86 billion as at Jun-18 and were SME - Other Publ

distributed evenly between household loans

(34%), SME loans (33%) and corporate loans Corporate - Large

17% 11%

(32%). 5% Corporate - Specialised lending

© 2019 Deloitte SAS. Document Confidentiel

Public sector

Note: (1) NPLs of BNPP, CAG, BPCE, SG and CMG owned in France and

abroad, based on the IRB approach i.e. banks’ own calculation model

© 2019 Deloitte SAS. Document Confidentiel Source: 2018 EU-wide transparency exercises - EBA Masque Deloitte 4:3 pour

13Deleveraging Europe 2019: Focus on France

A closer look at NPL stock beyond the top banking groups

p.14 (1)

A recoller, sans

logos

1.Selected

Selectedconsumer

consumercaptives

captives– Gross outstanding

- Gross outstandinginin

France (€bn, 2018)

France

€19bn €12bn €2bn €2bn €34bn

35 0.1 0.8

0.3 1.5

0.2 1.6

30

Non-performing

25 11.6 Performing

33.6

20

0.2

18.9

p.14 (2) 15

RCI Banque PSA Banque Carrefour Banque Banque Edel Total

A recoller, sans

logos

2. Banks in run-off - Gross outstanding in France

Banks in run-off – Gross outstanding in France (€bn, 2018)

€100bn €105bn(1 ) €13bn €218bn

220 1.3 4.7

11.6

180

104.7

Non-performing

140 212.8 Performing

3.3

100

96.4

60

p.14 (3)

Crédit Foncier Dexia Crédit Immobilier Total

de France

© 2019 Deloitte SAS. Document Confidentiel Masque Deloitte 4:3 pour projection 12

A recoller, sans

logos

Selected Fintechs

3. Selected – Gross

fintechs outstanding

- Gross in France

outstanding (€m, 2018)

in France

€203m €38m €32m €12m €285m

300 0.2

11.8 12.0

2.4

250 0.8 29.7

37.6

200 8.6

Non-performing

150

273.3 Performing

100 194.2

50

-

© 2019 Deloitte SAS. Document Confidentiel Masque Deloitte 4:3 pour projection 13

October LookandFin Credit.fr Bolden Total

Note: (1) The credit risk exposure of Dexia is displayed as gross loans, and NPL data were not available

Source: 2018 annual reports and company websites

14Deleveraging Europe 2019: Focus on France

Private debt in the French market and the breakdown of NPLs

by asset type

Outstanding retail and corporate loans (including Nearly half of this amount belongs to corporates

SME) in France totaled €2.2 trillion as at Dec-18 and (including SME) resulting in an NPL ratio of 3% for

are mainly comprised of retail mortgages (45%), whose this asset class. Consumer loans, which are generally

growth is stimulated by historically low interest rates. unsecured, make up 33% of bad debt and have the

The large corporate segment showed an increase highest NPL ratio at 11% (compared to 1.3% for retail

in corporate loans over the last five years, while mortgages).

consumer loans have remained stable in light of more The share of NPL stock has slightly decreased since

stringent regulation. 2014 and is driven almost entirely by consumer loans,

Retail and corporate NPL outstanding in France, a as the quality of debtors has improved and NPL sales

different measure than the total NPLs held by French have been focused on this asset class.

banks across Europe, totaled €68bn as at Dec-18.

Retail and corporate loans outstanding (€bn)

2 244

2 400 2 125

2 018

1 947

2 000 1 838 1 880 2 605

244

2 400 1 752 2 572

125

2 529

018

1 600 456 471 1 500

947

2 000 463 1 838 1 880

1 752 393 415

605

374 383 572

1 200 361 368 500 529

1 600 356 456 471 207 215

463 207 209 207 207

149 393 415

800 374 383

1 200 361 368

356

207

866 207

899 207

954 1 215

010

400 784 815

207 833

209

800 149

- 954 1 010

400 784

2012 815

2013 833

2014 866

2015 899

2016 2017 2018

- Mortgage Consumer SME Large corporate

2012 2013 2014 2015 2016 2017 2018

Note: Consumer

Note: Consumerincludes

includesnon-real

non-real estate loansto

estate loans toindividuals;

individuals; Large

Large corporate

corporate includes

includes

onlyonly

non-financial companies

Mortgage

non-financial companies Consumer SME Large corporate

Source: Banque de France

Note:Source: Banque

Consumer de France

includes non-real estate loans to individuals; Large corporate includes

only non-financial companies

Source: Banque de France72 74 73 72

80 and70

Retail corporate NPL outstanding (€bn) 70 68

80

60 72 74 73 72

70 33 70 68

32 33 34 34 33 32

60

40

32 33 33 34 34 33 32

27 27 28 26 24 22 23

40

20

12

27 11

27 28

13 13

26 14

24 14

22 13

23

20-

2012 2013 2014 2015 2016 2017 2018

12 11 13 13 14 14 13

- Mortgage Consumer Corporate

2012 2013 2014 2015 2016 2017 2018

Note: Consumer includes non-real estate loans to individuals; Corporate includes SME

and large corporate exposure

Mortgage Consumer Corporate

Source: Banque de France

Note: Consumer

Note: includes

Consumer includesnon-real estateloans

non-real estate loans

toto individuals;

individuals; Corporate

Corporate includes

includes SME

SME and

and large

largecorporate

corporate exposure

exposure

Source: Banque de France

Source: Banque de France

e SAS. Document Confidentiel Masque Deloitte 4:3 pour projection 15

15

SAS. Document Confidentiel Masque Deloitte 4:3 pour projection 15Deleveraging Europe 2019: Focus on France

Legal and

regulatory

New guidelines issued by the EBA legal framework enables loan

in June 2019 require EU banks activity as well as debt recovery

to define an NPL strategy to and asset resolution. The

sustainably reduce NPL levels. mortgage financial guarantee

French banks’ adherence to system, insolvency regimes

these guidelines, as well as the (including the overindebtedness

new Pillar 1 and Pillar 2 guidance scheme), collateral enforcement

backing full NPL provisioning, and amicable or judicial

should incentivise deleveraging. procedures facilitate effective,

At the broadest level, the French albeit lengthy, NPL resolution.

16Deleveraging Europe 2019: Focus on France

Impact of the EBA’s new NPL guidance

The EBA's new guidelines on the management of non- Compliance with these new requirements will prompt

performing and forborne loans came into effect on significant additional costs, further reducing banks'

June 30, 2019 and impacted more than 6,000 banks operational and execution capacity. This is expected

in the European Union. The guidance introduces new to lead to an increase in banks’ refinancing costs, a

requirements for banks to define an NPL strategy and reduction of their profitability and will ultimately weigh

to implement operational structures to sustainably on their regulatory capital needs. The potential impacts

reduce NPLs. In line with these guidelines, European of the EBA’s guidelines are outlined below.

banks will have to design new projects to adapt IT

systems, adjust risk models, review business models,

improve credit management practices and adapt NPL

procedures and tools.

Internal

Data and IT System

organisation

device monitoring

and process

• Based on internal and external operating

environment analyses

NPL strategy

• Defines time-bound reduction targets

• Studies all strategic options to reduce NPLs - + - + - +

• Decision making

NPL governance • NPL operating model

and operations • Internal control framework

- + - + - +

• NPL monitoring and early warning processes

• Prevents borrower delinquency due to

Forbearance deterioration of economic situation

• Extends exposure terms and postpones payments - + - + - +

• Updated EBA NPL definition

• Classification according to forbearance status

NPL recognition

• Implementation of mechanism for days past due

determination - + - + - +

• Defines clear internal guidelines for:

NPL impairment - Irrecoverable loans and write-offs

and write-offs - Adequate valuation of loan portfolios impairments

- Robust risk provisioning methods - + - + - +

• Independent, up-to-date and coherent value

Collateral assessments of collateral associated with NPLs

valuation • Regular back-testing

• Sale of foreclosed assets - + - + - +

17Deleveraging Europe 2019: Focus on France

New supervisory directives on NPL provisioning

The EBA’s new definition of default will come into application by

New definition of default

January 2021 with adjusted criteria that should significantly affect

(Jan-17)

the NPL stock and their expected behaviour

The ECB guidance defines supervisory expectations for NPL

ECB NPL guidance

management. It requires banks with large NPL stocks to develop

(Mar-17)

appropriate strategies to reduce their level.

Pillar 2

Addendum to the The addendum clarifies the ECB’s supervisory expectations for

ECB NPL Guidance prudential provisioning of new NPLs (i.e. loans classified as NPL

(Mar-18) on or after April 1, 2018).

This press release established further steps in the supervisory

ECB press release

approach to reducing NPLs and provides coverage expectations for

(Jul-18)

banks’ NPL stock (i.e. loans classified as NPL before April 1, 2018).

The European Parliament and the Council of 17 April 2019

Official Journal of the EU amends the CRR minimum loss coverage for NPLs and sets out

(Apr-19) the prudential treatment under Pillar 1 for NPLs arising from loans

Pillar 1

originated on or after April 26, 2019.

The most recent communication clarifies previous NPL guidance

ECB communication and provides some adjustments to the ECB’s supervisory

(Aug-19) expectations for new NPLs (under the Pillar 2 Addendum) to allow a

consistent and simple approach to reducing NPLs.

Communication from the ECB on coverage • Pillar 2 as per the ECB press release still applies to

expectations, published in Aug-19, attempted to clarify NPL stock, i.e. loans classified as NPL before April 1,

and simplify previously published NPL guidance. 2018; and

The text (i) addresses the overlap in scope between • Pillar 1 and Pillar 2 Addenda have been harmonised

the addenda of Pillars 1 and 2, (ii) specifies the relevant so that coverage expectations are consistent for loans

coverage expectations for NPLs based on the date of classified as NPLs on or after April 1, 2018.

loan origination and the date of the NPL status and (iii)

provides some adjustments to the Pillar 2 Addendum:

Loans classified as NPL Pillar 2 –

before April 1, 2018 ECB press release

Loans originated Pillar 2

before Addendum – Adjusted

Loans classified April 26, 2019 calibration

as NPL after

April 1, 2018 Loans originated

Pillar 1 –

on or after

Backstop

April 26, 2019

18Deleveraging Europe 2019: Focus on France

Pillar 2, as described in the ECB press release of Jul-18, French banks are generally viewed as having low

applies to loans classified as NPL before April 1, 2018 NPL ratios as they are, overall, below 5%. The initial

p.19

(the NPL stock). It provides three different paths to full

coverage –or 100% provisioning rate– based on the

provisioning rate, to be applied in Dec-20 for banks

with net NPL ratios below 5%, is 60% for secured

specific characteristics of each bank: loans classified as NPL for more than seven years and

• banks with net NPL ratios 5% and 12.5%. provisioning rate is expected every year.

Provision for banks according to NPL ratio

Dec-20 Dec-21 Dec-22 Dec-23 Dec-24 Dec-25 Dec-26

Net NPL ratio 5% and 12.5%

Unsecured NPL 50% 60% 70% 80% 90% 100% 100%

Secured NPL 40% 50% 60% 70% 80% 90% 100%

Source: ECB press release (Jul-18)

© 2019 Deloitte SAS. Document Confidentiel

19Deleveraging Europe 2019: Focus on France

Both the Pillar 1 and Pillar 2 Addenda are applicable to to Pillar 1. Additionally, the coverage expectations

new NPLs: for new NPLs are consistent under both Pillar 1 and

• Pillar 1 applies to NPLs from loans originated on or Pillar 2 Addendum: a 100% provisioning rate for new

after April 26, 2019; and NPLs should be reached by the 3rd, 7th, or 9th years

depending on attached guarantees.

• The Pillar 2 Addendum applies to NPLs from loans

originated on or after April 1, 2018. Simultaneously, the EBA’s new definition of default

p.20

should create “new compartments” of NPLs that

This overlap initially resulted in two different

might enhance both NPL stocks and expectations for

approaches being used for new NPLs classified from

innovative financial solutions.

April 26, 2019 onwards, and has been addressed

in the Aug-19 communication of the ECB. The The impact of these directives could be significant and

communication provides some adjustments so that should create opportunities for NPL disposals.

the Pillar 2 Addendum only applies to NPLs not subject

Provisions on new NPLs by year after default(1)

100% 100% 100% 100% 100% 100% 100%

85%

80% 80%

70%

55%

35% 35…

25%

0%

1+ 2+ 3+ 4+ 5+ 6+ 7+ 8+ 9+

Secured - Real estate collateral Secured - Others Unsecured

Note: (1)On or after April 2018

Source: ECB communication (Aug-19)

© 2019 Deloitte SAS. Document Confidentiel Masque D

20Deleveraging Europe 2019: Focus on France

Potential impact on NPL disposals

Portfolio type Definition Potential impact on NPL transactions

• Unsecured: three years post NPL status • Portfolios are too expensive to maintain

Fully • Secured: nine years post NPL status if on balance sheet despite relatively high

provisioned guaranteed by a real estate collateral, quality of underlying assets (especially

- +

or seven years otherwise for secured loans)

Pillar 1 – Backstop

• Minimum one-year probation period • A default provision rate is applied to

Restructured • Required conditions for reclassification: loans that may no longer be delinquent

(probation - Min. 12 months of regular payments; - + (if sufficient new payments have been

period) - No past due credit obligations; and collected), making them costly to hold

- No signs of unlikeliness to pay

EBA new definition of default

• Default status applies at the customer-level • Borrower level default provision rate

Defaulted (borrower's total exposure) regardless of the applied to loans that may not be

by contagion actual status of each individual loan - + delinquent individually and may still have

good recovery chances

EBA new definition of default

• BDF can require banks to restructure loans • Upon completion of the probation

Overindebted

of overindebted customers period, these loans are reclassified as

customers

• Loans are reclassified as restructured “performing overindebted” and can only

(BDF) - +

and subject to the 12-month probation be acquired by regulated entities

EBA new definition of default

• Minimum 3-month probation period • A default provision rate is applied to

Non-restructured

• Clear assessment of unlikeliness to pay loans that may no longer be delinquent

(probation

triggers must be made before reclassification - + (if new payments have been collected),

period)

to performing making them costly to hold

EBA new definition of default

Recent updates to accounting and regulatory that five years after NPL classification, secured loans

frameworks issued by European regulators have must already be provisioned up to 70%. In France,

created significant opportunities for the French NPL where the judicial process for debt recovery is lengthy,

disposal market. These regulations result in increased applying a high provisioning rate is incompatible with

incentives for NPL holders to deleverage their balance optimistic recovery chances. The increased cost is a

sheets as NPL stocks are becoming more expensive to clear incentive for portfolio disposals.

retain. In particular, the Pillar 1– backstop implies

21Deleveraging Europe 2019: Focus on France

Banque de France overindebtedness plans, a French market

specificity

The Banque de France established a plan for Among the total number of applicants in 2018, there

households that cannot reimburse their loans and were 92,000 were first-time applicants, a 4% decrease

cannot reimburse their loans while paying their current YoY and a level comparable to 1990. Of eligible

expenses. It offers a remediation plan to restructure or applicants, 45% were oriented toward a recovery plan

partially write-off debt. In 2018, 163,000 applications without judicial liquidation, which represents a total

were submitted to BDF under this scheme, of which debt of €1.3 billion. BDF plans can extend expected

91% were considered eligible, either directly by the recovery time significantly as the instruction period

commission or following a district court appeal. The takes up to two years and plans can last up to seven

number of applications submitted decreased by 10% years.

YoY and by 27% compared to 2013.

BDF plan activity by stage (2018)

• Individuals initiate process by submitting a BDF plan

163 000 applications submitted application. Upon application, the individual is registered

to the national payment incident database (FICP)

• BDF examines the application to assess the eligibility of

148 000 eligible applications

a plan

• BDF defines a solution tailored to the applicant's

66 000 standard procedures economic situation (new repayment schedule,

moratorium and/or partial write-off)

• For highly deteriorated financial situations, BDF can

12 000 personal recovery procedures implement a total write-off (FICP registration continues

for five to seven years)

p.22

14 000 procedures terminated • BDF plan is closed (full repayment or total write-off)

Source: Banque de France

The total debt of eligible applicants totaled €6.6 billion Total debt of eligible applicants (Dec-18)

as at Dec-18, of which €3.5 billion relates to eligible

first time applicants. The debt of eligible applicants

Financial debt

is composed mainly of financial debt, of which 42%

is related to mortgage loans with the remainder

divided between personal and revolving loans. Arrears 43%

represented 12% of the total debt and the debt write- 13%

off rate in 2018 was 30%, up 3% from 2017. 75%

23%

12%

25%

9%

Source: Banque de France

22Deleveraging Europe 2019: Focus on France

Simplified BDF plan application cycle

Application submission by debtor

Eligibility assessment of application

by the Commission

Application not eligible Eligible application

Possible recourse to the Assessment by the Commission of the

court of execution most appropriate procedures

Standard procedure No financial solution

(Plan conventionnel ou moratoire) (Procédure de rétablissement personnel “PRP”)

PRP with PRP without

compulsory compulsory

Failure Success

liquidation liquidation

Post-amicable phase Recovery plan

Debtor’s approval Debt write-off

recommended by

Actions imposed: the Commission

• Debt collection

• Debt suspension

• Moratorium

No Yes

Actions recommended:

• Partial write-off Compulsory liquidation Standard

• Balance reduction by court: foreclosure procedure

• Debtor’s obligations and closing of PRP

Source: Banque de France

23Deleveraging Europe 2019: Focus on France

French mortgage market guarantees

Financial guarantees in the mortgage loan market are hypothèques. Most financial guarantee providers,

an alternative to registered mortgages (hypotheque). including Crédit Logement, manage the recovery

In practice, when an individual requests a mortgage process. In the event of default, resolution procedures

loan in France, the lender submits an application for are initiated by the guarantee providers. These could

a financial guarantee from its affiliated subsidiary. If include loan restructuring or loan consolidation. In

the individual is not eligible, the bank will then register case of failure, they proceed to the sale of the assets.

a first ranking mortgage with the Conservateur des

p.24

Of the €203 billion new individual mortgage loans in Mortgage loans by guarantee (2018)

p.24

2018, 51% were secured using financial guarantees.

Crédit Logement is the leading French specialist

8%

in mortgage loan guarantees with €346 billion of

9%

total loans outstanding guaranteed as at Dec-2018, 8%

more than half of outstanding secured by financial 9% Financial guarantee

€203bn

guarantees. In 2018, it guaranteed more than 575,000 51% Mortgage

Financial guarantee

new loans

loans. €203bn Other guarantees

Mortgage

32% new loans 51%

Banks also have their own mortgage loan guarantee

No guarantee

Other guarantees

subsidiaries such as CEGC, part of the BPCE group, 32%

which has 15% market share, and SOCAMI, also a BPCE No guarantee

entity, distributing through Banque Populaire branches

only. Note:

Note:AsAs

a%a of

%loan production

of loan production

Source:

Source: Crédit

Crédit Logement

Logement Observatoire

Observatoire

Other non-banking players are also present in this Note: As a % of loan production

sector, include CNP Caution, a subsidiary of CNP Source: Crédit Logement Observatoire

Assurances, and MNH and MGEN, which are mutual

insurance companies. Their market share is less than Outstanding by financial guarantee (2018)

20% combined.

3%5% Crédit Logement

4%

3%5% CEGC

Crédit Logement

9%4%

SOCAMI

CEGC

9% €656bn

10% outstanding 54% CAMCA

SOCAMI

€656bn

loans

10% outstanding 54% CMH

CAMCA

loans

15% CNP

CMH

15% Others

CNP

Others

Note: As a % of loan outstanding

Source: Xerfi

Note:

Note: AsAs

a%a of

%loan outstanding

of loan outstanding

Source:

Source: Xerfi

Xerfi

© 2019 Deloitte SAS. Document Confidentiel Masqu

© 2019 Deloitte SAS. Document Confidentiel Masqu

24Deleveraging Europe:

Deleveraging Europe 2019: Focus on France

Legal

p.25

This guarantee system allows a credit Crédit Log

risk pooling between banks and financial

guarantee providers. Crédit Logement is

a joint subsidiary of the main French

This guarantee system allows a credit Crédit Logement – shareholding structure

banking groups. (Dec-18)

To benefit from the

risk pooling between banks and financial guarantee scheme, banks have to be 6%

guarantee providers. Crédit Logement is a 3% shareholders of Crédit

BNP Logement and

Paribas

must be committed to increasing the 9%

joint subsidiary of the main French banking 6% CréditFund,

Agricole Group risk

17%Mutual Guarantee a credit

groups. To benefit from the guarantee 9% sharing mechanism.

Société Shareholders

Générale Sha

7% e

scheme, banks have to be shareholders of contribute to the fund (Fonds Mutuel de

BPCE Group

Crédit Logement and must be committed 7% €1.3bn Garantie), a risk pooling tool used by

shareholder Crédit Logement in case

Crédit of unrecoverable

Foncier 9%

to increasing the Mutual Guarantee equity

9% loans. Crédit Mutuel Group

Fund, a credit risk sharing mechanism.

Crédit

32% Logement has a low NPL ratio over

SF2 - La Banque Postale

Shareholders contribute to the fund total exposure of 0.22% in 2018 related

(Fonds Mutuel de Garantie), a risk pooling 17% to the grantedHSBC France (off balance

guarantees

tool used by Crédit Logement in case of sheet). The NPL outstanding on its

Others Source: Com

unrecoverable loans. balance sheet totals €1.4 billion.

Individuals

Crédit Logement has a low NPL ratio over p.25 (2) annual report

Source: Company

Source: Company annual report

total exposure of 0.22% in 2018 related to

the granted guarantees (off balance sheet).

The NPL outstanding on its balance sheet Créd

totals €1.4 billion.

Crédit Logement exposure (1) (€bn)

1

1 1.0

Commitments

Non-performing

300

1 345

Commitments

© 2019 Deloitte SAS. Document Confidentiel 325 Performing

2016

300

Créd

Créd

2016 2017 2018

OnBalance

On Balance

€1.2bn €1.3bn €1.4bn €1.2b

SheetNPLs

Sheet NPLs

Note: (1) Off balance sheet guarantees related to loans guaranteed by Credit Logement Note: (1) Off ba

Credit Logement

Source: Company annual report

Source: Compan

© 2019 Deloitte SAS. Document Confidentiel

25Deleveraging Europe 2019: Focus on France

Standard recovery process for mortgage NPLs

Standard mortgage recovery procedure

Command of seizure

Forfeiture of term

Collateral auction

Summons to oral

Sales proceeds

Formal notice

hearings

received

process

Days past

due 90 180 210 270 350 720

1 2 3 4 5

A B C

Note: Time estimates outline a standard recovery procedure of a mortgage without a financial guarantee

Source: Deloitte estimates

For mortgages, default is usually declared after 90 The recovery process varies for the lender when

days past due, and the recovery procedure is relatively financial guarantees have been granted for residential

straightforward and lender friendly: loans.

When the debtor is not able to meet the payment Once the debt is forfeited by the bank, the

1 A

due date, the term is forfeited (déchéance du financial guarantee (e.g. Crédit Logement) can be

terme). This enables the bank to ask for the activated to cover the unpaid amounts.

immediate full reimbursement of the loan.

If the request is deemed compliant, the financial

B

Following the forfeiture of the term, through the guarantor repays the lender and receives a

2 command of seizure (assignation des débiteurs), subrogation notice (quittance subrogative) that is

debt holders can put in force the requirement for used to take legal action against the debtor.

debtors to pay the amounts due.

The provider of the financial guarantee exercises

Debtors and guarantors are then summoned to a

C its subrogation action (recours subrogatoire)

3 court hearing (convocations pour audience). against the debtor by command of seizure.

The Court usually decides to sell the collateral

4 through an auction process (ordre de mise en

vente).

Proceeds from the sale of the asset pledged are

5 distributed to debt holders (distribution des fonds).

26Deleveraging Europe 2019: Focus on France

Real and non-real estate guarantees that back SME loans

Type of Financial guarantee Company’s

Real estate pledge Personal guarantee

guarantee (BPI, SIAGI etc.) undertaking pledge

What it is? • Real property pledged • Unsecured written • Counter-guarantee • Pledge of the business

to loan by debtor promise from an provided by French (and its assets) to the

• Considered as a real individual, owner Public Investment benefit of the creditor

security (linked directly or management Bank, which offers to protect it against the

to loan) guaranteeing payment funding and guarantees risk of payment default

of loan in the event of to SMEs, Micro- by the debtor

payment default enterprises and self-

• Not tied to a specific employed individuals

asset • Guarantees range from

40% to 70% of loan

amount

How can it be • Property must be • Guarantor must sign • Intended as guarantee • Contract should be

triggered? registered (for a given a written document, for financial institutions signed between debtor

value and duration) for which lender holds as to cover part of the and lender

benefit of the lender security debt in the event of • Eight days after a

• Once default has been • Can be revoked in borrower default unsolved order to pay,

declared, the lender several cases (physical • Will only settle the lender can request

launches property loss of the guarantee, lender’s final loss after to the commercial

foreclosure procedures mandatory information all other securities have court to order the

missing, disproportion been activated public auction of the

between the guarantor company’s assets. This

patrimony and his gives priority to pledge

commitment, etc.) holder in proceeds

disbursement

Requisite • Mortgage registration • Signed promise with • BPI’s signed approval • Registered deed

document complete information deposited at the clerk

(greffe)

Valuation - + - + - + - +

strength and

transparency

• One of the most solid • Value assessment • After collections from • Difficult to assess

types of guarantees more complex as other securities, BPI will recoverability amount

• Property can be valued value impacted by reimburse a portion as value of assets

according to market solvency and holding (40% to 70%) of lender will depend on the

index of guarantor (property, final loss liquidation of company

liquid assets, etc.) holdings

Source: Deloitte analysis

27Deleveraging Europe 2019: Focus on France

Overview of restructuring and insolvency proceedings

for French companies

Simplified restructuring and judicial procedures

In case of financial difficulties, a French company can use amicable out-of-court proceedings or judicial proceedings.

A company can enter into amicable negotiations with creditors prior to insolvency(1):

Ad hoc proceedings (Mandat ad hoc): An out-of-court and confidential proceeding,

1 a solvent debtor facing financial difficulties can request the appointment of an ad hoc

agent, whose role is to facilitate negotiations with creditors.

Amicable

Conciliation: An out-of-court and generally confidential proceeding, available to

proceedings 2 all private entities and individuals acting as merchants, artisans or independent

professionals in commercial or artisanal activities (except farming) facing legal or

financial difficulties and insolvent for less than 45 days. The court appoints a conciliator

to facilitate negotiations with creditors and reach a workout agreement.

Failure of out-of-court proceedings or direct recourse to judicial proceedings

Available to solvent companies, safeguard proceedings can only be petitioned by the debtor

and allow a restructuring under court supervision.

1 Safeguard proceedings (sauvegarde)

• Safeguard

Safeguard plan

• Accelerated financial safeguard

• Accelerated safeguard

Judicial In the case of insolvency (cessation de paiements), two judicial proceedings exist to rehabilitate

proceedings the company or liquidate its assets.

2 Receivership (redressement judiciaire) Receivership plan

• Aim to protect a company’s activity

Disposal of assets

and employment

3 Compulsory liquidation (liquidation judiciaire)

• Liquidation of a company when rehabilitation Liquidation of company assets

is not possible

Note: (1) A French company is insolvent if it is not able to meet its payment obligations with its available assets when payments are due

Source: Deloitte analysis

Average length of legal procedures

Years 2 4 6 8 10 12 14

Safeguard and

Observation period Plans up to 10 years (and up 15 years for farmers)

receivership

Compulsory When business and assets are sold. On average, 4 years

liquidation without assets or 8 years with assets

28Brochure / report title goes here |

Section title goes here

Quality of

information

As the French NPL market These guidelines support an

develops, a key driver for investor effective NPL secondary market

confidence is the quality of through the introduction of

information of NPLs and their enriched reporting, standardised

underlying assets. data templates and centralised

The European Commission's credit registers. The French

(EC) 2017 Action Plan to tackle market has been lagging in

high levels of NPLs provides implementing these measures

a framework for information as notably demonstrated by the

obligations aimed at lenders, debt opacity of NPL transactions.

purchasers and public authorities.

29Deleveraging Europe 2019: Focus on France

An Action Plan aimed at improving information quality across

Europe

The European Commission introduced an Action The most impactful action for enhancing data quality

Plan to tackle NPLs in Europe in Jul-17. It addressed would be the use of a loan reporting template that

various aspects of the NPL market and presented would improve the consistency and comparability of

a comprehensive set of measures to improve the NPL portfolios, increasing potential investors’ trust in

quality of information. Key actions and progress the provided information. The lack of transparency of

on implementation are outlined in the EC’s fourth traded portfolios also puts France at a disadvantage

progress report on the reduction of NPLs in the as it underestimates the depth of the market and

Banking Union. While positive on average, tangible decelerates NPL resolution.

progress in France is not readily apparent.

Key measures from the Action Plan related to information quality

Measures Progress

Create an NPL reporting template to improve loan information provided by banks and facilitate

NPL disposals

Enhance disclosure requirements on asset quality and NPLs

Strengthen NPL data infrastructure, including implementation of potential transaction

platforms and the development of credit registers

Develop an NPL secondary market to support NPL reduction efforts

Issue new guidelines on bank loan origination, monitoring and internal governance

Completed In progress

Note: Progress includes the implementation of the Action Plan in Europe

Source: European Commission (Jun-19)

30Deleveraging Europe 2019: Focus on France

Availability and quality of information on value drivers

Compared to more mature NPL markets, France is it is possible to estimate recoverability potential

still considered a new market. This is noticeable in and forecast possible scenarios. The preparation

terms of availability and homogeneity of information, of NPL reporting using EBA templates would help

whether obtained from lending institutions, public reduce information asymmetries between sellers

or private sources creating high barriers to entry. and acquirers and increase access and quality of

Still, the French market is rich with information on loan information. Improvements in key areas of data

macroeconomic indicators, accurate financial and legal management could further enhance NPL information

information on debtors and credit scoring. Combined quality in France.

with comprehensive data provided by NPL sellers,

Real estate valuation

Credit bureaus

Limited public information on properties and

The absence of credit

valuations. Availability of cadastral information via

bureaus makes it difficult

restricted sources and a multitude of traditional and

to access consumer credit

Fintech firms offering property valuations, including

information. Specialised

automated, desktop and drive-by assessments.

companies provide credit

scoring for individuals

and companies. Extensive

Regulatory action

customer information is

available via private sources,

Supervisory guidance

including solvency reports

providing for comparable

and legal proceedings.

and standardised NPL

Civil investigation

information to meet

companies can find missing NPL investor needs increases

debtors and data on the information awareness of data quality

solvency of a company or quality limitations and and drives

individual.

a remediation exercise

to improve quantity and

quality of information

available.

Benchmarks

Debt servicers have valuable

collections and pricing Digitalisation

information. Limited public

benchmarks, but prior data French banks are investing in digitalisation,

can also be sourced through but availability of electronic credit files varies

business information greatly between lenders. Debt servicers are

companies and consulting also investing in innovation, notably IT and

firms. digital tools, to improve servicing capacity.

31You can also read