RETAIL OPERATIONS INDEX: WHERE IN THE WORLD COULD YOUR RETAIL PORTFOLIO THRIVE?

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

ARCADIS • RETAIL OPERATIONS INDEX

RETAIL OPERATIONS INDEX:

WHERE IN THE WORLD COULD YOUR

RETAIL PORTFOLIO THRIVE?

U

nderstanding how to flex and adapt your

branch portfolio is a critical success factor for

modern retailers. Relying on customer base,

brand strength, and market confidence alone will not

guarantee success. Retailers need to be empowered with

data and insight that not only takes these elements into

consideration but also reviews the varying factors that

impact portfolio success. This will not only ensure risks

are successfully mitigated and managed, but will also

lead to higher returns from retail investment.

The Arcadis Retail Operations Index offers insight into

which locations are most and least difficult to execute,

scale and flex large retail programs based on

an in-depth analysis of the global retail market over

50 countries.

Looking at market demands, economic climate, quality

of infrastructure, and ease of establishment and

operation, we have identified both the key challenges

and the opportunities faced by the world’s largest

retailers when opting to expand or reshape their store

portfolios.

ARCADIS • RETAIL OPERATIONS INDEX ← START I CONTENTS → 2

HEADLINES AT A GLANCE

T he majority of

the Western

European countries

are concentrated in

the top half of the

index, indicating that

the well-established

retail markets

continue to present

sound opportunities

for optimizing store

performance.

T he UAE

ranks highly

overall with both

D espite being the largest

consumer market in the world,

China’s significant barriers to entry,

a strong quality of including strict regulations, economic

H ong Kong tops the ranking as the easiest

market for retailers to enter.

In spite of this, the latest market insight suggests

infrastructure and

a robust economic

environment.

slowdown and a fragmented market

structure, have led to a lower rating

on our attractiveness scale.

that increasing operating overheads such as high

property costs and softening sales will likely have

an impact on local performance in 2015.

B razil has a growing

market demand due

M

to a rapidly growing middle

arket demand

class and increased foreign

in the US interest. However, its low

strengthens position in the index is

with interesting reflective of the challenges

polarisation in certain of an over-regulated labor

retail categories and market, low degree of trade

specific locations. transparency, high inflation

and currency depreciation.

ARCADIS • RETAIL OPERATIONS INDEX ← START I CONTENTS → 3

CONTENTS

4 THE REVOLUTION OF

THE RETAIL STORE

6 12 21 24

THE

OUR MIDDLE

RESEARCH ASIA THE USA EAST

17

EUROPE 22

LATIN

AMERICA

25

WHAT CAN RETAILERS DO TO ENSURE

OPTIMUM RESULTS FROM THEIR STORE

28

PORTFOLIOS ACROSS THE GLOBE?

CONTACT US

ARCADIS • RETAIL OPERATIONS INDEX ← START I CONTENTS → 4

THE REVOLUTION OF THE RETAIL STORE

Evolution is part of the fabric of life within the retail world. However, the retail store environment has seen little change over

the years – that is, until the birth of the digital world and, more importantly, the explosion of mobile technology and social

media that has pushed evolution into revolution.

The net result is that retailers have had to cope with and respond to both the technology enabling change and to the

consumers who are dictating it. The challenge is then compounded by cultural and developmental differences across the

world making it impossible to adopt a single solution.

The key to keeping pace with this revolution is adaptability, flexibility and an absolute focus on really knowing your consumer.

THE IMPACT OF DIGITAL

Online retail revenues are expected to double over the next four need for lower cost, flexible, reusable store formats that can be

years, led by China and the US. Asia has overtaken the USA in relocated to suit a rapidly changing environment. This is already

online sales for the first time and Europe and emerging markets being played out through the explosion of the ‘Pop-Up’ store

are growing exponentially. Retail property portfolios are expected environment.

to shrink by 30% over the next 10 years as retailers are under

Retailers with a heavy focus on services, such as retail banks and

more pressure to maintain performance in their bricks-and-mortar

mobile phone operators, will be equally challenged as their own

assets. So how will this affect portfolios in the future?

services continue to trend towards increasing online transactions.

This depends heavily on the type of retailer you are and the multi- The number of bricks-and-mortar touch points for these types of

channel strategy adopted. But we can certainly expect a heavier retailers are likely to reduce and be focused on premium locations

emphasis on flagships for brand building and showcasing products, and premium customer experiences. They will offer higher levels

supported by a variety of flexible store formats driving core sales of service to their VIP customers to generate the returns required

through localized access for the consumer. There will be a greater from such premium locations.

ARCADIS • RETAIL OPERATIONS INDEX ← START I CONTENTS → 5 OMNI-CHANNEL IS CRITICAL There is a race on to find the optimal omni-channel solution but it would fair to say that there is no single model for success. Determining exactly how to provide customers with the most efficient seamless balance between in-store, online and mobile shopping experiences remains one of the biggest challenges for most retailers. Perhaps one of the best pioneering examples of successful omni-channel retailing could be found with Apple where the consumer experience is absolutely consistent. Even their physical store networks have a blend of high impact city flagships surrounded by an ecosystem of smaller distributor stores and kiosks providing tremendous flexibility to shape their retail real estate portfolio quickly and efficiently. CONVENIENCE IS KING In this rapidly changing environment, the consumer is demanding convenience throughout the experience. Now, more than ever before, convenience is truly a critical success factor for retailers. Retail stores and branches will need to be multi-functional and accessible as the brand experience touch-point for consumers in the real world. The seeds of the revolution were planted many years ago, perhaps as long as three decades ago when catalogue and mail order companies pioneered what has become ‘Click-and-Collect’. In a pre-digital age, this provided catalogue customers with the ability to place orders and then collect in store at their convenience. Most major retailers are adapting their existing store formats to incorporate a form of ‘Click-and-Collect’ allowing their online shoppers to not only collect goods at a convenient time and location, but also to handle returns, resolve customer service issues and make cash payments. Although “Click-and-Collect” is less common in Asia where consumers are not as likely to drive to stores, it is becoming an increasingly popular retail concept in the Americas and Europe where the car still dominates. Many have increased sales by embracing an adapted “Click- and-Collect” concept. The UK department store John Lewis, for example, has leveraged its sister company, supermarket Waitrose, adding almost 320 collection points across the region. Reducing the necessity for customers to make longer journeys into major towns has made the experience more convenient and attractive to consumers. Changes such as this can result in an increase of up to 20% in online sales. Online retailers are also seeing a growing need to adapt. When Amazon opened its first store early in 2014 in the US, its entry into the ‘real world’ bricks-and-mortar environment was an irony not lost on many. Amazon had pioneered the demise of many high street retailers, particularly music, video and bookstores. But the core intention was to provide a physical touch-point with the consumer, a place to experience the brand physically, and to pick up and drop off goods; proof to many that even the digital world requires real world stores in order to satisfy the consumer. THE FLEXIBLE PORTFOLIO Most retailers have developed a toolkit of formats ranging from flagships and brand centers to kiosks and corners. Modifying an existing portfolio of formats requires a ground-up approach incorporating the needs of the chosen multi-channel strategy, demographic and customer research, and detailed local knowledge in each market. The virtual modelling of this data using different formats in various densities and locations will generate scenarios upon which these formats can be fine-tuned, together with real performance metrics from stores. The variety of formats needed will differ significantly between retailers depending on many factors including range and geography. But key to the formats is the ability to rapidly change and flex in response to performance and opportunity. The rapid depreciation of the capital cost of store developments has also become a priority, pressured further by a need to be opportunistic and an ability to respond to higher property costs. These factors all point to an increasing demand for a highly cost efficient and rapidly deployable arsenal of store formats at the disposable of retail executives.

ARCADIS • RETAIL OPERATIONS INDEX ← START I CONTENTS → 6

OUR RESEARCH

When determining how to develop and optimize store portfolio CLICK HERE TO VIEW OVERALL RANKINGS ► 3. Market demand - level of disposable income, domestic market

for maximum performance, retailers need to consider a number of size, passenger cars and competitive environment.

1. Infrastructure - quality of transportation, such as ports, roads

factors. Knowing where to locate stores, the size and volume of the CLICK HERE TO VIEW RANKINGS ►

and rail links.

footprint needed, the right channel mix and the local demographics 4. Economic environment - labor costs, inflation and availability

CLICK HERE TO VIEW RANKINGS ►

are all key components to getting the balance right. The use of a of technologies.

number of different store formats which can be applied to different 2. Ease of getting up-and-running - quality and quantity of local

CLICK HERE TO VIEW RANKINGS ►

locations types and demographics can then provide a framework suppliers, rules on Foreign Direct Investment (FDI) and

upon which to move forward. business freedom. 5. Ease of operating - prevalence of foreign ownership, trade

CLICK HERE TO VIEW RANKINGS ► freedom, labor freedom, logistics performance and freedom

The Retail Operations Index offers some insight into how easy or difficult

from corruption.

it is for retailers to scale or flex their portfolios in response to changing

CLICK HERE TO VIEW RANKINGS ►

market conditions by considering the following five key factors:

OVERALL TOTAL RANKINGS

ARCADIS • RETAIL OPERATIONS INDEX ← START I CONTENTS → 7

OUR RESEARCH

When determining how to develop and optimize store portfolio CLICK HERE TO VIEW OVERALL RANKINGS ► 3. Market demand - level of disposable income, domestic market

for maximum performance, retailers need to consider a number of size, passenger cars and competitive environment.

1. Infrastructure - quality of transportation, such as ports, roads

factors. Knowing where to locate stores, the size and volume of the CLICK HERE TO VIEW RANKINGS ►

and rail links.

footprint needed, the right channel mix and the local demographics

CLICK HERE TO VIEW RANKINGS ► 4. Economic environment - labor costs, inflation and availability

are all key components to getting the balance right. The use of a

of technologies.

number of different store formats which can be applied to different 2. Ease of getting up-and-running - quality and quantity of local

CLICK HERE TO VIEW RANKINGS ►

locations types and demographics can then provide a framework suppliers, rules on Foreign Direct Investment (FDI) and

upon which to move forward. business freedom. 5. Ease of operating - prevalence of foreign ownership, trade

CLICK HERE TO VIEW RANKINGS ► freedom, labor freedom, logistics performance and freedom

The Retail Operations Index offers some insight into how easy or difficult

from corruption.

it is for retailers to scale or flex their portfolios in response to changing

CLICK HERE TO VIEW RANKINGS ►

market conditions by considering the following five key factors:

INFRASTRUCTURE RANKINGS VIEW OVERALL TOTAL RANKINGS ►

ARCADIS • RETAIL OPERATIONS INDEX ← START I CONTENTS → 8

OUR RESEARCH

When determining how to develop and optimize store portfolio CLICK HERE TO VIEW OVERALL RANKINGS ► 3. Market demand - level of disposable income, domestic market

for maximum performance, retailers need to consider a number of size, passenger cars and competitive environment.

1. Infrastructure - quality of transportation, such as ports, roads

factors. Knowing where to locate stores, the size and volume of the CLICK HERE TO VIEW RANKINGS ►

and rail links.

footprint needed, the right channel mix and the local demographics

CLICK HERE TO VIEW RANKINGS ► 4. Economic environment - labor costs, inflation and availability

are all key components to getting the balance right. The use of a

of technologies.

number of different store formats which can be applied to different 2. Ease of getting up-and-running - quality and quantity of local

CLICK HERE TO VIEW RANKINGS ►

locations types and demographics can then provide a framework suppliers, rules on Foreign Direct Investment (FDI) and

upon which to move forward. business freedom. 5. Ease of operating - prevalence of foreign ownership, trade

CLICK HERE TO VIEW RANKINGS ► freedom, labor freedom, logistics performance and freedom

The Retail Operations Index offers some insight into how easy or difficult

from corruption.

it is for retailers to scale or flex their portfolios in response to changing

CLICK HERE TO VIEW RANKINGS ►

market conditions by considering the following five key factors:

EASE OF GETTING UP-AND-RUNNING RANKINGS VIEW OVERALL TOTAL RANKINGS ►

ARCADIS • RETAIL OPERATIONS INDEX ← START I CONTENTS → 9

OUR RESEARCH

When determining how to develop and optimize store portfolio CLICK HERE TO VIEW OVERALL RANKINGS ► 3. Market demand - level of disposable income, domestic market

for maximum performance, retailers need to consider a number of size, passenger cars and competitive environment.

1. Infrastructure - quality of transportation, such as ports, roads

factors. Knowing where to locate stores, the size and volume of the CLICK HERE TO VIEW RANKINGS ►

and rail links.

footprint needed, the right channel mix and the local demographics 4. Economic environment - labor costs, inflation and availability

CLICK HERE TO VIEW RANKINGS ►

are all key components to getting the balance right. The use of a of technologies.

number of different store formats which can be applied to different 2. Ease of getting up-and-running - quality and quantity of local

CLICK HERE TO VIEW RANKINGS ►

locations types and demographics can then provide a framework suppliers, rules on Foreign Direct Investment (FDI) and

upon which to move forward. business freedom. 5. Ease of operating - prevalence of foreign ownership, trade

CLICK HERE TO VIEW RANKINGS ► freedom, labor freedom, logistics performance and freedom

The Retail Operations Index offers some insight into how easy or difficult

from corruption.

it is for retailers to scale or flex their portfolios in response to changing

CLICK HERE TO VIEW RANKINGS ►

market conditions by considering the following five key factors:

MARKET DEMAND RANKINGS VIEW OVERALL TOTAL RANKINGS ►

ARCADIS • RETAIL OPERATIONS INDEX ← START I CONTENTS → 10

OUR RESEARCH

When determining how to develop and optimize store portfolio CLICK HERE TO VIEW OVERALL RANKINGS ► 3. Market demand - level of disposable income, domestic market

for maximum performance, retailers need to consider a number of size, passenger cars and competitive environment.

1. Infrastructure - quality of transportation, such as ports, roads

factors. Knowing where to locate stores, the size and volume of the CLICK HERE TO VIEW RANKINGS ►

and rail links.

footprint needed, the right channel mix and the local demographics 4. Economic environment - labor costs, inflation and availability

CLICK HERE TO VIEW RANKINGS ►

are all key components to getting the balance right. The use of a of technologies.

number of different store formats which can be applied to different 2. Ease of getting up-and-running - quality and quantity of local

CLICK HERE TO VIEW RANKINGS ►

locations types and demographics can then provide a framework suppliers, rules on Foreign Direct Investment (FDI) and

upon which to move forward. business freedom. 5. Ease of operating - prevalence of foreign ownership, trade

CLICK HERE TO VIEW RANKINGS ► freedom, labor freedom, logistics performance and freedom

The Retail Operations Index offers some insight into how easy or difficult

from corruption.

it is for retailers to scale or flex their portfolios in response to changing

CLICK HERE TO VIEW RANKINGS ►

market conditions by considering the following five key factors:

ECONOMIC ENVIRONMENT RANKINGS VIEW OVERALL TOTAL RANKINGS ►ARCADIS • RETAIL OPERATIONS INDEX ← START I CONTENTS → 11

OUR RESEARCH

When determining how to develop and optimize store portfolio CLICK HERE TO VIEW OVERALL RANKINGS ► 3. Market demand - level of disposable income, domestic market

for maximum performance, retailers need to consider a number of size, passenger cars and competitive environment.

1. Infrastructure - quality of transportation, such as ports, roads

factors. Knowing where to locate stores, the size and volume of the CLICK HERE TO VIEW RANKINGS ►

and rail links.

footprint needed, the right channel mix and the local demographics 4. Economic environment - labor costs, inflation and availability

CLICK HERE TO VIEW RANKINGS ►

are all key components to getting the balance right. The use of a of technologies.

number of different store formats which can be applied to different 2. Ease of getting up-and-running - quality and quantity of local

CLICK HERE TO VIEW RANKINGS ►

locations types and demographics can then provide a framework suppliers, rules on Foreign Direct Investment (FDI) and

upon which to move forward. business freedom. 5. Ease of operating - prevalence of foreign ownership, trade

CLICK HERE TO VIEW RANKINGS ► freedom, labor freedom, logistics performance and freedom

The Retail Operations Index offers some insight into how easy or difficult

from corruption.

it is for retailers to scale or flex their portfolios in response to changing

CLICK HERE TO VIEW RANKINGS ►

market conditions by considering the following five key factors:

EASE OF OPERATING RANKINGS VIEW OVERALL TOTAL RANKINGS ►ARCADIS • RETAIL OPERATIONS INDEX ← START I CONTENTS → 12

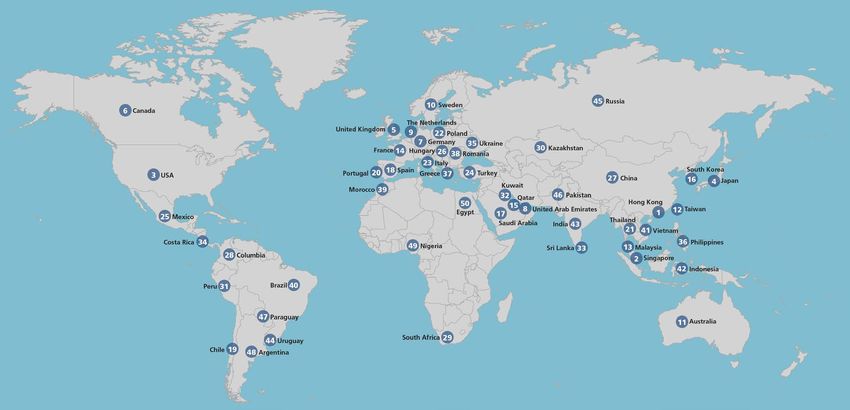

ASIA SPOTLIGHT ON: HONG KONG ► SINGAPORE ► CHINA ► INDIA ► INDONESIA ►

Asian countries feature at all points across the index, illustrating the

differing opportunities and markets, with Hong Kong sitting at the

top of the ranking and Indonesia, India and Pakistan occupying the

bottom.

HONG KONG

South Korea Hong Kong in the top spot means that it offers the best conditions

27 China in the world for retailers to operate within. Hong Kong provides

16 4 Japan some of the most advanced infrastructure in the world through

world-class air and seaports, state of the art telecommunications

Hong Kong and efficient local and regional transportation. It also benefits from

1 12 Taiwan stable and efficient business operating conditions and a strong

Thailand economic climate supported by a high influx of Chinese mainland

43 India

21 41 Vietnam visitors taking advantage of tourism and access to international

36 Philippines and luxury brands at tax free prices. As a result, most international

33 13 Malaysia brands have established multiple high-end flagship stores here.

Sri Lanka 2 Singapore Despite the ranking, retailers should exercise caution in 2015.

42 Indonesia Economists predict slow growth in retail sales due to a reduction

in cross-border tourist numbers and a general slowdown in

China. This is already evident as we saw a steady decline in sales

volume in 2014 compared to the previous year. In addition, rents

have continued to rise to unsustainable levels making portfolio

flexibility more important than ever.

11 Australia

Hong Kong key stats:

GDP: $291bn (IMF Oct 2014)

Real GDP growth: 2.5% (IMF Oct 2014)

Population: 7.24m (IMF Oct 2014)

Unemployment: 3.3% (2013)

Consumer Price Index: 4.4% (2014) worldbank.org

Retail Growth: 7.5% growth y/y (Nov 2014) tradingeconomics.comARCADIS • RETAIL OPERATIONS INDEX ← START I CONTENTS → 13

ASIA SPOTLIGHT ON: HONG KONG ► SINGAPORE ► CHINA ► INDIA ► INDONESIA ►

Asian countries feature at all points across the index, illustrating the

differing opportunities and markets, with Hong Kong sitting at the

top of the ranking and Indonesia, India and Pakistan occupying the

bottom.

SINGAPORE

South Korea Singapore occupies second place in the rankings as a country

27 China with outstanding ease of operations, business and economic

16 4 Japan environment. Grocery stores, primarily NTUC FairPrice,

and Dairy Farm, dominate the retail market together with

Hong Kong major department store operators such as Takashimaya and

1 12 Taiwan Robinsons. The highly successful urban malls have attracted

Thailand international brands and created a strong platform for retailers

43 India

21 41 Vietnam to operate successfully in Singapore.

36 Philippines However, Singapore is constrained by being a small island nation

33 13 Malaysia

and the significant volume of international brands has largely

Sri Lanka 2 Singapore saturated the market. This success has driven up rents and made

42 Indonesia consumers more value focused.

To feed growth ambitions, international brands are being forced

to explore the out of town suburban retail landscape with mixed

results. It has also forced an explosion in e-commerce activity.

A number of foreign retailers with a rigid approach to retail and

11 Australia unwillingness to adapt to local conditions are struggling to move

to profitability and several have exited.

Whilst recent retail sales have been under pressure and

reducing, the overall local economic conditions are still strong.

Singapore key stats:

GDP: $308m (2014)

Real GDP growth: 2.92% (2014)

Population: 5.47m (2014)

Unemployment: 2.8% (2013)

Consumer Price Index: 1% (2014) worldbank.org

Retail Growth: 6.5% y/y (Nov 2014) tradingeconomics.comARCADIS • RETAIL OPERATIONS INDEX ← START I CONTENTS → 14

ASIA SPOTLIGHT ON: HONG KONG ► SINGAPORE ► CHINA ► INDIA ► INDONESIA ►

Asian countries feature at all points across the index, illustrating the

differing opportunities and markets, with Hong Kong sitting at the

top of the ranking and Indonesia, India and Pakistan occupying the

bottom.

CHINA

South Korea At no 27, China’s ranking is much lower than its regional

27 China counterparts. This is primarily due to the difficulties retailers face

16 4 Japan in getting up and running in a challenging business environment.

Tightening of regulations and the imposition of heavy fines

Hong Kong over the past few years has forced some of the luxury retailers, China key stats:

1 12 Taiwan and grocery stores such as Walmart, to deliver optimisation or

Thailand consolidation strategies in China. Other retailers are pulling out of GDP: $10,360bn (2014)

43 India

21 41 Vietnam the market altogether.

Real GDP growth: 7.35% (2014)

36 Philippines Attracted by the size and scale of the consumer base, many

33 13 Malaysia

retailers in the past had rapidly expanded in China but in many Population: 1.364bn (2014)

Sri Lanka 2 Singapore cases had not carried out sufficient research on reliable customer

42 Indonesia demand to be successful. Potential for growth and domestic Unemployment: 4.6% (2013)

competition had been overestimated. For many, incorrect

Consumer Price Index: 2% (2014) worldbank.org

predictions have led to portfolio underperformance and, as a

result, investors in stores in China are increasingly cautious. Retail Growth: 11.9% y/y (2014) tradingeconomics.com

That said, for many retailers China is viewed as ‘long-play’ where

11 Australia it is important to be there and build brand awareness and loyalty.

Although it is fiercely competitive, it also holds massive potential for A balanced portfolio with flexible formats that can be easily scaled

those who are well prepared and knowledgeable about the market. is the most successful retailer platform.

Having the right local partner to help navigate the unique pitfalls

and prizes of local markets can ensure a more successful entry. In spite of these restrictions, there is no denying that China is set to

be one of the fastest growing e-commerce markets in the world -

A principal issue facing retailers in China is its fragmented market but not at the rate of growth that we have previously experienced.

structure: the combination of small and medium-sized retailers Overall, China anticipates a moderate retail sales growth of 8%

and a large disparity of regional consumer purchasing power over the next five years and a positive growth in middle-income

means consumer demand can differ greatly from one end of the earnings. Such growth forecasts point to China surpassing the US

country to the other. in retail sale volumes over the next few years and, therefore, is still

Due to the much higher income levels, the major urban areas of very much a country in the spotlight for retailers.

Beijing, Shanghai and Guangzhou make up the majority of China’s Casual and fast fashion retailers such as H&M and GAP, sports

retail sales. Although international chain stores are growing, apparel retailers and many international automotive retailers are

expanding from the major centers has proved very challenging all underway with large-scale expansions and a focus on the lower

due to provincial barriers to market and the difficulty in getting tier cities. To operate successfully, retailers will need to plan their

business cases to ‘stack up’. Confidence is easily bruised. portfolios carefully, understand the market conditions for the sector

Although as much as 80% of demand comes from the Tier 1 cities, in which they operate and undertake thorough due diligence studies

high rental rates faced in cities such as Shanghai and Beijing are around customer sales demand. Above all, China is a long-term

driving some retailers away from the market altogether. investment and expectations should be tempered accordingly.ARCADIS • RETAIL OPERATIONS INDEX ← START I CONTENTS → 15

ASIA SPOTLIGHT ON: HONG KONG ► SINGAPORE ► CHINA ► INDIA ► INDONESIA ►

Asian countries feature at all points across the index, illustrating the

differing opportunities and markets, with Hong Kong sitting at the

top of the ranking and Indonesia, India and Pakistan occupying the

bottom.

INDIA

South Korea A poor economic environment score leaves India at a very low

27 China 43 in the rankings. This may appear a surprising result when

16 4 Japan comparing the position of other Asian countries, especially with

India’s burgeoning middle class and a consumer culture. However,

Hong Kong challenges regarding the operating environment together with

1 12 Taiwan high inflation have created a difficult environment for retailers to

Thailand expand.

43 India

21 41 Vietnam

In the past, India has been restricted by a lack of quality mall

36 Philippines space outside of the major cities as well as on-going regulatory

33 13 Malaysia

challenges for foreign retailers. In spite of this, retailing records

Sri Lanka 2 Singapore healthy growth due to rising income levels in the middle classes

42 Indonesia and an improvement in the presence of consumer marketing,

which has boosted the awareness of brands and products and

supported growth during over the past year.

The Indian government through Prime Minister Modi

is recognizing the regulatory issues FDI companies are

11 Australia experiencing and is starting to relax these, introducing free trade

and beneficial tax initiatives to promote retail growth.

The Indian retail market reached US$490 billion in 2013, 69% of

which came from food. In recognition of this, India is identified as

a hot spot for expansion, specifically in grocery, with Metro and

Spar experiencing significant growth and Walmart and Tesco

planning ambitious rollout programmes. Alongside this, Internet

retailing of non-grocery products is seeing strong growth and is India key stats:

now posing huge competition to store-based retailing. Retailers

remain undeterred with Ikea, Uniqlo, Burger King and other food GDP: $2,067bn (2014)

and beverage retailers planning expansion into India during

2015. Therefore, given the positive outlook of this country, we Real GDP growth: 7.42% (2014)

expect India’s position in the ranking to climb during 2015.

Population: 1.267bn (2014)

Unemployment: 3.6% (2013)

Consumer Price Index: 6.4% (2014) worldbank.org

Retail Growth: 13% forecast to 2018 ibef.org.ARCADIS • RETAIL OPERATIONS INDEX ← START I CONTENTS → 16

ASIA SPOTLIGHT ON: HONG KONG ► SINGAPORE ► CHINA ► INDIA ► INDONESIA ►

Asian countries feature at all points across the index, illustrating the

differing opportunities and markets, with Hong Kong sitting at the

top of the ranking and Indonesia, India and Pakistan occupying the

bottom.

INDONESIA

South Korea Slower economic growth and diminishing purchasing power,

27 China 16 especially for the lower income class, has dampened any potential

4 Japan

retail growth in Indonesia. Nevertheless, throughout 2014, major

retailers continued to expand into developing cities to capture the

Hong Kong growing middle class. One example is Ikea who established their

1 12 Taiwan first store in Indonesia last year and are moving ahead with further

Thailand stores.

43 India

21 41 Vietnam

As the economic recovery gains some pace, retailers should

36 Philippines expect to see sales growth of at least 10% this year and this

33 13 Malaysia

is being recognized by new international retailers who have

Sri Lanka 2 Singapore entered the market, including H&M and Uniqlo,who recently

42 Indonesia opened their first stores in Jakarta.

For many, barriers to entry make the only route of entry into

Indonesia through a joint venture or franchise model, which can

be a lower risk but often less successful model. It is our opinion

that caution should be taken when considering entering the

11 Australia market, however, due to challenges with importing materials and

products where regulations and transparency issues continue to

impact time and cost.

Looking ahead, we expect slower yet positive sales growth across

Indonesia, and although there are uncertainties around the

economic environment we should expect it to remain positive due

to increasing consumption and the expanding presence of leading

brands. Indonesia key stats:

GDP: $889bn (2014)

Real GDP growth: 5.02% (2014)

Population: 253m (2014)

Unemployment: 6.3% (2013)

Consumer Price Index: 6.4% worldbank.org

Retail Growth: 18.6% y/y (July 2014) euromonitor.comARCADIS • RETAIL OPERATIONS INDEX ← START I CONTENTS → 17

EUROPE SPOTLIGHT ON: UNITED KINGDOM ► GERMANY ► POLAND ► THE NETHERLANDS ►

The well-established retail markets of Europe present sound

opportunities for optimizing store performance. Many countries

benefit from strong supply chains and our results demonstrate that

overall the ease of doing business and becoming operational is far

easier across Europe than in other regions.

That said, the recent economic crisis within the Eurozone has left its

mark on the retail sector; on-going uncertainty over interest rates,

UNITED KINGDOM

employment levels and overall economic stability are still weighing The United Kingdom ranks fifth overall, reflecting a retail market

heavily on the continent with, perhaps unsurprisingly, Greece and in growth mode once again, driven primarily by the gradual

Italy performing comparatively poorly. Only time will tell how long economic recovery.

it takes the individual European economies, and consequentially the

There is major structural change underway with most large

retail sector, to achieve something by10 Sweden

way of recovery.

scale retailers reducing or halting their network expansion

programmes for larger formats. Demand for innovative retail

experiences will continue to grow in popularity, perhaps driven

harder by the recent issues faced by major UK supermarkets

United Kindom The Netherlands who are challenged by over-sized and inefficient store footprints.

Investment capital is being spent on improving and remodelling

5 9 Despite its high ranking, the UK is let down by its infrastructure,

22 Poland existing stores to protect market share (against tougher

7 scoring 18 in that category. This is primarily based on negative

competition from the hard discounters Aldi and Lidl), and growing

Germany public perception of issues such as road congestion that is

the convenience store-base. But some commentators argue that

affecting traditional out of town malls, and limited public transport

France 14 26 Hungary there is overcapacity amongst the major grocers and it remains

investment. This is then impacting more recent town center

to be seen whether further consolidation activity occurs. This will

schemes, resulting in the construction of fewer new shopping

test the flexibility and adaptability of their formats.

23 Italy centers.

Even though e-commerce is rising in popularity in the UK, 90%

20 18 Spain The rise of “super regions” shopping centers such as Bluewater,

37 Greece of sales revenue is still generated in the physical store with food

Kent, the Trafford Center, Manchester, and the two London

Portugal retailers continuing to dominate the market in 2015. Tesco

Westfield centers is attracting trade away from regional or

maintains that their ‘in store picking’ approach for online shopping

neighbourhood shopping centers. As a result, local retailers

remains the only way to operate profitability.

and owners need to reassess their retail proposition and target

customer demographics to re-align these assets to the available

market.

UK key stats:

GDP: $2,941bn (2014)

GDP growth: 2.55% (2014)

Population: 65m (2014)

Unemployment: 6% (Aug 2014) (lowest since 2008 and

largest annual fall)

Consumer Price Index: 1.5% (2014) imf.org databank.worldbank.org

Retail Growth: 2.7% y/y (2014) reuters.comARCADIS • RETAIL OPERATIONS INDEX ← START I CONTENTS → 18

EUROPE SPOTLIGHT ON: UNITED KINGDOM ► GERMANY ► POLAND ► THE NETHERLANDS ►

The well-established retail markets of Europe present sound

opportunities for optimizing store performance. Many countries

benefit from strong supply chains and our results demonstrate that

overall the ease of doing business and becoming operational is far

easier across Europe than in other regions.

GERMANY

That said, the recent economic crisis within the Eurozone has left its

Germany ranks seventh overall. Annual sales in goods and

mark on the retail sector; on-going uncertainty over interest rates,

services topped €2 trillion in 2014 making it the world’s

employment levels and overall economic stability are still weighing

fourth largest economy. An area holding back Germany,

heavily on the continent with, perhaps unsurprisingly, Greece and

however, is its business environment and, in particular, its labor

Italy performing comparatively poorly. Only time will tell how long

restrictions with strict regulatory control and high unionisation.

it takes the individual European economies, and consequentially the

Furthermore, Germany also controls credit card/store card

retail sector, to achieve something by10 Sweden

way of recovery.

uptake at source so access to easy credit is restricted.

Like the UK, Germany is experiencing a polarisation effect in

the retail sector. Mid-range retailers are being driven out of

United Kindom the market due to the growth of the personalised experience

The Netherlands

high-end retailers are creating in store. Retailers are optimising

5 9 omni-channel strategies as a result of a 0.5% decline in in-store

22 Poland

7 sales since 2007. With general living costs predicted to rise,

Germany consumer spending may show signs of slowing in several sectors,

although as the economy is in a strong position, the government

France 14 26 Hungary

may resolve this through easing of taxes over the next few

years. Despite a robust economy, Germany, like all EU countries,

23 Italy is at risk from a decrease in market demand due to EU-Russia

sanctions and the Eurozone fragility, which leave it vulnerable.

20 18 Spain

37 Greece Nonetheless, over the past year the grocery retailers such as

Portugal

Lidl, Edeka and Aldi have reported strong sales in Germany, as

have pharmaceutical retailers. GDP is forecast to rise 1.6% in

2015, indicating a boost in consumer confidence and a potential

increase in retail sales.

Looking forward, high-end retail is expected to be a driver of Germany key stats:

growth in Germany over the next 5 years.

GDP: $3,852bn (2014)

GDP growth: 1.6% (2014)

Population: 80.6m (2014)

Unemployment: 5.3% (2013)

Consumer Price Index: 1.5% (2014) worldbank.org

Retail Growth: 2.6% on previous month (Aug 2014) reuters.comARCADIS • RETAIL OPERATIONS INDEX ← START I CONTENTS → 19

EUROPE SPOTLIGHT ON: UNITED KINGDOM ► GERMANY ► POLAND ► THE NETHERLANDS ►

The well-established retail markets of Europe present sound

opportunities for optimizing store performance. Many countries

benefit from strong supply chains and our results demonstrate that

overall the ease of doing business and becoming operational is far

easier across Europe than in other regions.

POLAND

That said, the recent economic crisis within the Eurozone has left its

Whilst Poland sits in the top half of the index rankings, the

mark on the retail sector; on-going uncertainty over interest rates,

country’s downfall is its infrastructure, ranking below even the

employment levels and overall economic stability are still weighing

developing economies of Thailand and Morocco. Technological

heavily on the continent with, perhaps unsurprisingly, Greece and

improvements in Poland’s transport systems and more efficient

Italy performing comparatively poorly. Only time will tell how long

power infrastructure are desperately required, but funding new

it takes the individual European economies, and consequentially the

projects is constrained due to high public debt. Alongside this,

retail sector, to achieve something by10 Sweden

way of recovery.

Poland’s government remains prone to bouts of instability,

making this country a little risky for major retail investment.

Irrespective of that, Poland demonstrates strong market

United Kindom demand and the encouraging result in our ‘business

The Netherlands

environment’ category shows the potential in this market.

5 9 22 Poland Poland is fast becoming an inspirational target for retailers,

7

in particular retail banks, who are planning small expansion

Germany

strategies underpinned by a strengthening labor market.

France 14 26 Hungary Growth has been apparent amongst the discount retailer chains,

particularly in the grocery and apparel sectors due to stronger

consumer confidence. Such discount retail chain expansions

23 Italy

are, however, pushing out many of the independents causing

20 18 Spain a corresponding reduction in their store portfolios. There have

37 Greece been fewer new overseas entrants into the market over the past

Portugal

few months, primarily due to instability in neighbouring Ukraine.

E-commerce is also becoming increasingly popular in the Polish

market with a steady growth in online revenues. But it is the

closing price gap between bricks and mortar and digital sales,

Poland key stats: alongside a predicted uplift in market conditions which could

mean a rapid growth in store outlets for the major market

GDP: $548bn (2014) players.

Looking ahead, retailing in Poland is expected to continue

GDP growth: 3.37% (2014)

developing in constant value terms. It is our opinion that retail

chains looking for expansion opportunities will need to look more

Population: 38m (2014)

towards the small and medium sized cities as well as retail parks,

currently dominated by larger homeware stores such as Ikea.

Unemployment: 10.4% (2013)

Consumer Price Index: 0.1% (2014) worldbank.org

Retail Growth: 1.7% y/y (Aug 2014) tradingeconomics.comARCADIS • RETAIL OPERATIONS INDEX ← START I CONTENTS → 20

EUROPE SPOTLIGHT ON: UNITED KINGDOM ► GERMANY ► POLAND ► THE NETHERLANDS ►

The well-established retail markets of Europe present sound

opportunities for optimizing store performance. Many countries

benefit from strong supply chains and our results demonstrate that

overall the ease of doing business and becoming operational is far

easier across Europe than in other regions.

That said, the recent economic crisis within the Eurozone has left its

mark on the retail sector; on-going uncertainty over interest rates,

employment levels and overall economic stability are still weighing

THE NETHERLANDS

heavily on the continent with, perhaps unsurprisingly, Greece and The Netherlands high ranking in our index is primarily due to

Italy performing comparatively poorly. Only time will tell how long slower market demand and economic environment following the

it takes the individual European economies, and consequentially the prevailing influence of Europe’s recession. After a few years of

retail sector, to achieve something by 10 Sweden

way of recovery. economic turmoil and cuts in government spending, many Dutch

households have faced financial difficulties that have impacted

consumer spending. Although real GDP has started to show

some signs of recovery, the economic environment for retailers

has remained relatively low as consumer confidence and there-

United Kindom The Netherlands fore spending remains modest.

5 9 22 Poland Internet retailing continues to have an impact as major chains

7

dominate at the expense of independents, and in recent years

Germany

this grip has strengthened.

France 14 26 Hungary Real GDP is projected to see some growth in 2015, and inflation

and unemployment will likely fall. In light of this, retail conditions

23 Italy are predicted to improve in the Netherlands. Whilst growth is

predicted to be modest and slow, growth will return as confidence

20 18 Spain

37 Greece returns.

Portugal

The Netherlands key stats:

GDP: $870m (2014)

GDP growth: 0.87% (2014)

Population: 17m (2014)

Unemployment: 6.7% (2013)

Consumer Price Index: 1% (2014) worldbank.org

Retail Growth: 0.7% y/y (July 2014) tradingeconomics.comARCADIS • RETAIL OPERATIONS INDEX ← START I CONTENTS → 21

THE USA SPOTLIGHT ON: USA ►

The USA, the global leader of the retail industry by revenue and third Many of the larger chains (JC Penny, Macys, Walmart, and Sears) USA key stats:

in our rankings, boasts strong market demand and a good business and teen-focused stores (Aeropostale, Abercrombie, Wet Seal

environment for retailers to operate successfully. That said, it does and American Eagle) announced significant closures across their GDP: $17,419bn (2014)

rank lower in the quality of its infrastructure, which is a barrier to portfolios in Q1 as post-holiday underperformers are outed.

operations. Although recently the price of petroleum has fallen, GDP growth: 2.39% (2014)

In contrast retailers such as Walmart, Home Depot and Lowes are

easing the cost of logistics and shipping, there has been a reduced

providing a strong online experience. Mobile apps that navigate Population: 319m (2014)

investment in freight rail, roads, bridges and ports relative to other

stores, find products and direct orders to fulfilment centers are

regions over the past few decades, and journey times in comparison

common-place and growing. Unemployment: 7.4% (2013)

are long and uncompetitive. As a result, the US has a growing

need to invest in infrastructure, as shown in Arcadis’ report Global The US retailing environment was irrevocably changed by the

Consumer Price Index: 1.6% (2014) worldbank.org

Infrastructure Investment Index 2014, placing the USA tenth out recession and, while parts of the economy look ready to surge

of 41 countries for the greatest potential for growth and investment ahead, the picture as a whole is a mixed one.

Retail Growth: 5% y/y (Sep 2014) tradingeconomics.com

in their economic infrastructure. There is a growing need to renovate -0.3% m/m (Sep 2014) reuters.com

Retailers should be aware that recent regulatory enforcement

and upgrade existing assets, with costs estimated by the American

initiatives focused on the retail market at the national and state

Society of Civil Engineers at $3.6 trillion by 2020.

levels (US Environmental Protection Agency, Occupational Safety

The highly fragmented nature of the US retail market has meant and Health Administration and equivalent) have also presented

that its gradual revival is not homogeneous and has generally been challenges and have the potential to increase operational costs in

focused in major cities, with many suburban areas still experiencing the year ahead. However we believe that consumer spending will

downsizing and closure of stores. grow steadily over the coming months, supported by stronger job

creation, low interest rates and lessening levels of household debt.

Despite a tepid economic recovery in many parts of the US, certain

locations and sectors remain strong. Overall vacancy rates are at To operate successfully in the USA, the retailer should understand

their lowest levels in three years resulting in a corresponding rise in the fragmented nature of its market; much of the consumer

rental rates particularly seen in the major cities such as Houston, spending will be in food and high-end retail due to increasing

Chicago, Boston, New York City and San Francisco. Some of this can disparities in household earnings. The polarisation affect is driving

be attributed to longer opening hours which are generating higher out mid-range retail players and this is particularly impacting

revenues, as evidenced in Trader Joes for example, where substantial the saturated department store retailers in a similar way as the

customer numbers are frequenting the stores until their 10pm trends we are seeing in the UK and Western Europe. This should be

closing time. Furthermore, we are seeing markets strengthening in considered carefully in expansion or optimization strategies.

New England, the West Coast, the Gulf Coast, and to some degree,

the South East.

There is real consolidation in US grocery wholesalers that could

change the availability and pricing structures for retailers in

subsequent years. In this market there is shift towards ‘high end’ and

specialty foods that are more profitable, especially in those more

affluent regions. 3 USA

Many of the food retailers have been traditionally very regional

and we are starting to see expansion beyond their small cluster of

states, such as is evident with Meijer, Marianos and Heinens in the

Mid-West. Contrary to some other retail sectors, many food retailers

are experiencing a shift from destination big box single tenant stores

to convenience locations. Focus is on attracting increased footfall

through creating bespoke customer experiences in an effort to lift

revenues and reduce footprint.ARCADIS • RETAIL OPERATIONS INDEX ← START I CONTENTS → 22

LATIN AMERICA SPOTLIGHT ON: BRAZIL ► MEXICO ►

In spite of fractured markets and continuing economic uncertainty

in Latin America, a growing consumer class has proven resilient

against entrenched corruption, roller-coaster inflation and eroding BRAZIL

currencies. Throughout the majority of the region’s commercial With poor infrastructure and economic and business

markets, falling commodity prices and a strong US dollar have environments, Brazil nears the bottom of our index at 40.

slowed growth in larger cities, notably Sao Paulo, while oversupply

and slow demand continue to push vacancies up and rents down. A principal reason for its low ranking is high tax levels,

Nonetheless, there are positive signs and many retailers are taking particularly import and distribution tax. These taxes combined

advantage of changing franchise regulations and the lack of make imported goods almost a third more expensive than

modern formats to push ahead with expansion plans. equivalent local goods and this understandably is discouraging

consumers and retailers alike. Brazil’s highly regulated labor

market and consumer debt have resulted in low investment

in infrastructure leaving much of the networks in need of

6 Canada

intensive upgrade. Only 1.5% of GDP is invested in infrastructure

development.

However, Brazil’s growing middle class and reasonably

unsaturated retail market is providing some incentive for

retailers. Retailing continued to show healthy sales growth in

consumer goods and midrange fashion as well as electronic

3 USA appliances and pharmaceutical retail.

The competitive landscape is growing and we are experiencing

greater competition between retailers in Brazil. Multi-channel

strategies are growing in popularity, GDP has increased in recent

25 Mexico years, and despite an uncertain economic outlook, it is predicted

that the retail sector will experience steady growth in 2015.

Although local players dominate much of the market, many

Costa Rica 34 international retailers see this as an opportunity and several of

the grocery retailers, including Carrefour and Walmart, have

28 Columbia

experienced successes to date.

The main caution for international players considering entry is

the deficiencies in the country’s infrastructure and a failure to

Peru 31 Brazil 40 Brazil key stats:

address complications in regulatory issues for FDI.

GDP: $2,346bn (2014)

47 Paraguay GDP growth: 0.14% (2014)

Population: 202m (2014)

44 Uruguay

Chile 19 48 Argentina Unemployment: 5.9% (2013)

Consumer Price Index: 6.3% (2014) worldbank.org

Retail Growth: -0.9% y/y (July 2014) www.arcadis.comARCADIS • RETAIL OPERATIONS INDEX ← START I CONTENTS → 23

LATIN AMERICA SPOTLIGHT ON: BRAZIL ► MEXICO ►

In spite of fractured markets and continuing economic uncertainty

in Latin America, a growing consumer class has proven resilient

against entrenched corruption, roller-coaster inflation and eroding

currencies. Throughout the majority of the region’s commercial

markets, falling commodity prices and a strong US dollar have

slowed growth in larger cities, notably Sao Paulo, while oversupply

MEXICO

and slow demand continue to push vacancies up and rents down. Ranked at number 25 in the index, Mexico is proving an

Nonetheless, there are positive signs and many retailers are taking interesting country to watch. A weak economic climate has

advantage of changing franchise regulations and the lack of typically led to caution in this market historically, but with

modern formats to push ahead with expansion plans. a growing middle class, reduction in petroleum prices and

administrative reforms attempting to create a more stable

business environment, we are seeing a trend of foreign retailers

6 Canada entering the market. Luxury retail, pharmaceutical retail, apparel

and several retail banks are all in competition for prime space.

Where existing retailers, particularly in food, are reaching

saturation in Tier 1 cities such as Mexico City and Monterrey,

plans to expand into Tier 2 cities are underway and here lies the

biggest opportunity for retailers entering the market.

Retailers are up against significant challenges which are

3 USA

highlighted by the lower scores of infrastructure and economic

environment in our index. These include Mexico’s high

unemployment, income level inequality and elevated inflation.

Retailers considering Mexico in their portfolio should also be

25 Mexico

aware of, and learn from, mistakes made in China where a lack of

data around sales and consumer statistics led to the closure of

underperforming stores. Plans should most definitely consider

Mexico key stats:

Costa Rica 34

the Tier 2 growing cities but also factor in the challenges around

GDP: $1,282bn (2014)

28 Columbia availability of sales data and infrastructure quality for logistical

purposes as well as closely monitoring the economic recovery. GDP growth: 2.12% (2014)

Peru 31 Brazil 40 Population: 124m (2014)

Unemployment: 4.9% (2013)

47 Paraguay Consumer Price Index: 4% (2014) worldbank.org

Retail Growth: 1.2% y/y (Nov 2014) tradingeconomics.com

44 Uruguay

Chile 19 48 ArgentinaARCADIS • RETAIL OPERATIONS INDEX ← START I CONTENTS → 24

THE MIDDLE EAST SPOTLIGHT ON: UAE ►

Overall, the retail market is booming across the Gulf Cooperation 45

Council (GCC). High levels of wealth and disposable income for the

majority of GCC nationals and sections of the expat communities

are driving a high level of spending. Whilst the majority of major

brands are already located in the region, many more are looking

to enter the market and or to further increase their presence. A

UAE

growing population, and one that is increasingly fashion conscious, is The UAE ranks eighth overall, with a strong economic

attracting all the major fashion brands. environment and infrastructure ranking. Much of the UAE retail

is driven by the tourist industry that further boomed in 2014

Automotive retail is enjoying a boost with Infiniti reporting Q2 sales due to government efforts to maintain a wide number of tourist

increase of 31% compared to the same period last year. A surge of attractions, and a high calibre infrastructure in the country. A

high-end retail malls has also attracted the retailer and this makes healthy performance is forecasted and consumer confidence

the UAE one of the most lucrative markets for foreign investors. will be boosted as a result of economic stability, which will in

turn lead to more spending, higher employment and increased

numbers of expats and tourists.

Key stats:

Retailers entering or optimising portfolios in the UAE need to

be aware of these demographics and market demands and GDP: $402bn (2014)

tailor their portfolios accordingly. Most retail categories are

expected to thrive, with the exception of grocery retail which GDP growth: 3.61% (2014)

has been constrained by government price controls that protect

consumers from inflation of imported foods. This in turn has Population: 9.45m (2014)

affected revenues for the grocery retailers.

Unemployment: 3.8% (2013)

Consumer Price Index: 2.3% (2014) worldbank.org

Retail Growth: 5% (2014) gulfnews.com emirates247.com

Kuwait

32

Qatar

15

8 United Arab Emirates

17 Saudi ArabiaARCADIS • RETAIL OPERATIONS INDEX ← START I CONTENTS → 25

WHAT CAN RETAILERS DO TO ENSURE OPTIMUM RESULTS

FROM THEIR STORE PORTFOLIOS ACROSS THE GLOBE?

The success of a retailer’s portfolio lies in integrating 100 ASSESS ASSESS

demographic and market information into a robust

omni-channel strategy based around consumer

preferences.

Retailers will have detailed information on sales per store and

on various fixed and variable operating costs, but the key to a

PROPERTY FLEXIBILITY SCORE

successful portfolio is in understanding the variables that affect

these figures and the relationships between them.

These variables include:

■ Location

■ Footprint

■ Functionality

■ Flexibility

■ Fiscal Impact

■ Design Impact.

■ Socio-economic market dynamics.

Knowing how to optimise these variables, and comparing them

for each store across an entire portfolio, can lead to faster

and more accurate decision-making, and consequentially to

achieving greater and more sustainable financial returns.

The graph below illustrates areas for portfolio optimization by

highlighting the highest and lowest performing stores against the

highest and lowest flexibility scores to potentially improve sales.

The flexibility score measures the retailers ability has to change

property attributes of a location e.g. ability to relocate, terminate

or sub-let).

CLOSE RENEW LEASE/ ACQUIRE

0.0 SALES PER STORE 100

BEFORE TRANSFORMATION AFTER TRANSFORMATIONARCADIS • RETAIL OPERATIONS INDEX ← START I CONTENTS → 26

CASE STUDY

`The Challenge BEFORE CLICK HERE TO VIEW THE PORTFOLIO AFTER OPTIMIZATION ►

A retailer with a large store portfolio across Asia had

expanded at pace and scale over the past five years

resulting in an inconsistent customer experience and

subsequently, poorly performing stores. The retailer

was looking for ways to achieve higher returns from

their store portfolio.

The Approach

The first step to solving the problem was to understand

why some stores were achieving higher returns than

others in the portfolio, and to consider which lessons

they could apply to the poorer performing stores to

reduce unnecessary operating costs and help improve

sales.

The next step involved collating a large amount of

detailed information, such as performance figures,

location demographics, space efficiency, condition of

the store property etc. in order to get a clear picture

of the current situation.

In order to fully understand this information, the data

was entered into a model which generated simulated

results that could test the impact of various strategic

decisions on the retailer’s portfolio and help make

the right investments or divestments to improve BEFORE

portfolio returns. TOTAL STORE NO. 12

A Positive Outcome FLAGSHIP 4

STANDARD 3

The results were significant, providing the retailer MINI 5

with a reduction in operating expenditure and square SQFT 38,000

footage and improving the customer experience in

SALES HEADCOUNT 200

selected stores through added innovative design. This

led to a portfolio that generated greater returns, as REVENUE 45M

can be evidenced in the graphic on the right. EXPENSE 20M

ROI 2.3You can also read