AFFORDABLE HOUSING READING BOROUGH COUNCIL LOCAL DEVELOPMENT FRAMEWORK - Information to support the Sites and Detailed Policies Document

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

READING BOROUGH COUNCIL

LOCAL DEVELOPMENT FRAMEWORK

AFFORDABLE HOUSING

Information to support the Sites and

Detailed Policies Document

July 2011

1 AFFORDABLE HOUSING BACKGROUND PAPERCONTENTS

1. INTRODUCTION 3

2. POLICY, GUIDANCE AND ADVICE 3

National Policy 3

Regional Policy 5

Local Policy 6

7

3. RESULTS OF PREVIOUS CONSULTATION

4. CURRENT CHARACTERISTICS AND FUTURE TRENDS 8

5. POLICY DISCUSSION 21

6. PREFERRED APPROACH AND REJECTED ALTERNATIVES 25

Preferred Approach 25

Rejected Alternative Approaches 26

7. REFERENCES 27

APPENDICES 28

2 AFFORDABLE HOUSING BACKGROUND PAPER1. INTRODUCTION

1.1 Core Strategy Policy CS16 sets out the strategic affordable housing policy for the

Borough primarily in relation to sites of 15 or more dwellings. However, in the

context of then (drafting of the submission document was finalised at the end of

2006) emerging national policy direction, it provided context for a separate policy

to enable affordable Policy to be sought on sites of less than 15 dwellings. Policy

DM6 deals specifically with the provision of affordable housing on sites of less than

15 dwellings in the context of the guidance in the current version of PPS3

“Housing” and in conformity with the Core Strategy Policy.

1.2 Reading Borough experiences high levels of need for affordable housing. The

evidence submitted as part of the submission of the Core Strategy in 2007 (and

adopted in January 2008) remains valid, certainly in terms of the high levels of

need for affordable housing in the Borough. The development of small sites make

an important contribution to the Borough’s housing land supply. Provision of

affordable housing on such sites will provide a significant contribution to the

provision of affordable housing in the Borough. Such contributions can be made

viably, in reasonable market conditions, on small sites, in accordance with the

thresholds and targets set out in Policy DM6.

2. POLICY, GUIDANCE AND ADVICE

National Policy

2.1 Under government guidance in PPS3 (published at the end of 2006), in their Local

Development Documents, Local Planning Authorities should:

• Set an overall (i.e. plan-wide) target for the amount of affordable housing

to be provided. It should reflect an assessment of the likely economic

viability of land for housing within the area, taking account of risks to

delivery and drawing on informed assessments of the likely levels of finance

available for affordable housing, including public subsidy and the level of

developer contribution that can reasonably be secured;

• Set separate targets for social-rented and intermediate affordable housing

(RBC current seek 70% / 30%);

• Specify the size and type of affordable housing that is likely to be needed

in particular locations and, where appropriate, on specific sites (set out in

SPG);

• Set out the range of circumstances in which affordable housing will be

required. The national indicative minimum site size threshold is 15

dwellings. However, under PPS3, Local Planning Authorities can set lower

minimum thresholds, where viable and practicable. Local Planning

Authorities will need to undertake an informed assessment of the economic

viability of any thresholds and proportions of affordable housing proposed,

including their likely impact upon overall levels of housing delivery and

creating mixed communities.

3 AFFORDABLE HOUSING BACKGROUND PAPER• Set out the approach to seeking developer contributions to facilitate off

site provision, where such provision can be robustly justified, in lieu of on-

site provision (of broadly equivalent value).

2.2 Affordable housing includes social rented and intermediate housing, provided to

specified, eligible households whose needs are not met by the market. Affordable

housing should:

• Meet the needs of eligible households including availability at a lost low

enough for them to afford, determined with regard to local incomes and

local house prices.

• Include provision for the home to remain at an affordable price for future

eligible households or, if these restrictions are lifted, for the subsidy to be

recycled for alternative affordable housing provision’.

Social rented housing is:

‘Rented housing owned and managed by local authorities and registered social

landlords, for which guideline target rents are determined through the national

rent regime. The proposals set out in the Three Year Review of Rent Restructuring

(July 2004) were implemented as policy in April 2006. It may also include rented

housing owned or managed by other persons and provided under equivalent rental

arrangements to the above, as agreed with the local authority or with the Housing

Corporation as a condition of grant.’

Intermediate affordable housing is:

‘Housing at prices and rents above those of social rent, but below market price or

rents, and which meet the criteria set out above. These can include shared equity

products (e.g. HomeBuy), other low cost homes for sale and intermediate rent.’

2.3 Policy DM6 was conceived and drafted to comply with the guidance and definitions

in PPS3. However, following approval of the draft SDPD by Council on 25th January

2011, DCLG published a new technical change to PPS3 (on 14th February 2011) in

order to include the new Affordable Rent product within the definition of

affordable housing 1. A revised version of PPS3 was published on 9th June 2011, to

provide technical amendments to Annex B: Definitions, to reflect the introduction

of Affordable Rent. Affordable Rent is defined in PPS3 as:

“Rented housing let by registered providers of social housing to

households who are eligible for social rented housing. Affordable Rent is

not subject to the national rent regime34 but is subject to other rent

controls that require a rent of no more than 80 per cent of the local

market rent25, 36.

1

The draft definition was as follows:

“Rented housing provided by registered providers of social housing, that has the same characteristics as social rented

housing except that it is outside the national rent regime but is subject to other rent controls that require it to be

offered to eligible households at a rent of up to 80 per cent of local market rents.”

4 AFFORDABLE HOUSING BACKGROUND PAPERThe main wording changes from the draft definition are underlined. PPS3 (2011)

includes the following footnotes:

“34 The national rent regime is the regime under which the social rents of

tenants of social housing are set, with particular reference to the

Guide to Social Rent Reforms (March 2001) and the Rent Influencing

Regime Guidance (October 2001).

35

Including service charges, where applicable.

36

Local market rents are calculated using the Royal Institution for

Chartered Surveyors (RICS) approved valuation methods. The Tenant

Services Authority has issued an explanatory note on these:

www.tenantservicesauthority.org/upload/doc/RICS_rental_valuation_n

ote_20110118140714.doc”

In writing this, it is not apparent how this product differs from Intermediate rent

housing in terms of affordability, although it is clear that this is likely to be the

main product that will be funded by the HCA in the future in terms of grant. There

will be an ongoing review of any policy implications arsing from this change. There

will obviously be some implications for the viability of development involving

affordable housing where grant would have previously been expected.

Regional Policy

2.4 While the Secretary of State has announced his intention to abolish RSS and this

forms part of the Localism Bill, RSS will remain part of the development plan until

that part of the Bill is enacted. Under the regulations, LDF’s have to demonstrate

conformity with the relevant regional strategy.

2.5 Adopted during Summer 2009, the housing policies in the South East Plan are

designed to provide the region with an integrated, strategic approach to housing

provision which supports an urban renaissance, delivers sustainable development

and which provides everyone with the opportunity of a decent home. Amongst

various objectives the housing policies seek to, “Secure a step-change in the

delivery of affordable housing.”

2.6 Policy H4 (Affordable Housing) states that Local Development Documents will

contain policies to deliver a substantial increase in the amount of affordable

housing in the region. Local Development Documents will set targets for the

provision of affordable housing, taking account of the results of housing need and

market assessments and having regard to the overall regional target that 25% of all

new housing should be social rented accommodation and 10% other forms of

affordable housing (Equivalent to a 70/30% split). Where justified by housing need

assessments, Local Development Documents should specify the tenure of housing

being sought. There will be a presumption in favour of on-site affordable housing

provision. To help ensure the delivery of affordable housing, Local Development

Documents will provide comprehensive policy and guidance on financial viability

and the role of public subsidy …….” The full policy wording is attached at

Appendix 1:

5 AFFORDABLE HOUSING BACKGROUND PAPERThe government has announced its intention to abolish Regional Strategies.

Nevertheless, the South East Plan remains part of the development plan and. SEP

policies therefore remain relevant to LDF policy development.

Local Policy

2.7 The Reading Borough LDF Core Strategy contains policy CS16 which states:

All developments of 15 dwellings and above, or of any alternative lower

threshold contained in a future adopted Development Plan Document will

provide 50% of the total number of dwellings in the form of affordable

housing to meet the needs of the area, as defined in a housing needs

assessment.

Affordable Housing is subsidised housing that enables the asking price or

rent to be substantially lower than the prevailing market prices or rents in

the locality 2, and which is subject to mechanisms that will ensure that the

housing remains affordable for those who cannot afford market housing.

2.8 As indicated above, PPS3 provides for affordable housing to be sought on sites of

below 15 dwellings, where viable and practicable. The council has long considered

it desirable for thresholds to be reduced to below 15 dwellings. A considerable

and disproportionate number of applications propose 14 dwellings to avoid

affordable housing provision. In addition there is no good reason why smaller sites

cannot viably make a contribution to the significant need for affordable housing

that exists in the area. Policy DM6 provides a development plan policy to seek

provision on such smaller sites in a way that is viable and practicable.

2.9 The Reading Borough Sustainable Community Strategy (2008) 3 puts forward a

community vision and priorities for Reading.

‘Our vision is to maintain and improve the quality of life in Reading,

embracing the challenges of a dynamic, inclusive urban community of the21st

century. Everyone will have the opportunity to benefit from all that Reading

can offer. Everyone has a part to play in shaping our future’.

2.10 Decent and affordable housing is a priority in achieving that aim. Chapter 7 of the

Strategy sets out a vision for housing in the Borough:

“Reading’s residents will have available to them a range of attractive,

affordable and realistic housing choices. The housing stock itself will be safe,

secure, and environmentally sustainable and this, together with a range of

high-quality housing services, will make a positive contribution to people’s

lives, both at an individual, personal level and also in terms of their wish to

live in thriving, stable neighbourhoods. At the broadest level, ensuring that

2

Planning Policy Statement 3: Housing (PPS3) underpins the delivery of the Government’s strategic housing policy objectives

and the goal is to ensure that everyone has the opportunity to live in a decent home, which they can afford in a community

where they want to live.

3

Reading Borough Sustainable Community Strategy (2008), see:

http://www.reading.gov.uk/councilanddemocracy/General.asp?id=SX9452-A78364E2

6 AFFORDABLE HOUSING BACKGROUND PAPERReading has a well-housed population will make a very significant contribution

to the success of the local economy.”

The Strategy notes that housing is identified as one of the most serious issues

facing Reading today with affordability being the most obvious problem. A key

solution is to increase the overall supply of new housing, including widening the

range of subsidised housing options in all tenures. Priorities for housing in the

strategy are to increase the overall supply of new housing, including affordable

housing in all tenures. The LDF is seen as an important tool in achieving this

increase.

A draft review of the Reading Borough Sustainable Community Strategy (2011) 4

revolves around the themes of People, Place and Prosperity. The need for housing

and affordable housing is crucial to all three themes, and is referred to at various

points in the draft document.

Housing Strategy

2.11 The latest Reading Borough Council Housing Strategy, Firm Foundations, covers the

period 2009-2014 5. The strategy sets out 10 objectives. The planning system is

seen as relevant to the delivery of most of these objectives but particularly the

following:

Strategic Objective 1:

Ensure the sustainable delivery of new build housing to meet identified

needs whilst achieving best use of available land.

Strategic Objective 2:

Increase the availability of appropriate specialist accommodation for those

that need it.

Strategic Objective 3:

Make best use of existing housing stock within the town.

2.12 The Strategy indicates that planning policy will also be reviewed in relation to

decreasing the threshold on which affordable housing provision will be requested.

This will assist the authority in achieving a target of 40% of all new homes in the

town to be affordable housing, with a target of 50% on all sites subject to section

106 agreements and above 14 units.

3. RESULTS OF PREVIOUS CONSULTATION

3.1 The consultation carried out in the early part of 2010 attracted several

representations on SDPD Draft Policy DM6, making the following points:

• The council needs to be clear that the policy is backed up by appropriate

evidence on viability;

4

Draft Reading Borough Sustainable Community Strategy (2011), see http://www.reading2020.org.uk/library/public/file88/

5

Firm Foundations see:

http://ww2.reading.gov.uk/documents/Housing_and_Benefits/Strategies%20and%20Plans/HousingStategy2009.pdf

7 AFFORDABLE HOUSING BACKGROUND PAPER• Objections to the reference to an open book approach to determining

viability in relation to individual applications;

• Objections to the policy requiring for the provision of affordable housing to

be dispersed throughout the development. This is seen as impractical in

terms of management and unreasonable from a market perspective;

• There is some contradiction in the policy that needs to be clarified.

3.2 The point about the wording of the policy being unclear is accepted and some

wording changes have been made to, hopefully, add clarity to the policy. The

Council’s responses to the remaining points generally note the comments but do

not accept that they warrant any change in the policy.

3.3 The Second Pre Submission consultation undertaken during February, March and

April 2011, produced very similar comments to the 2010 consultation from the

same parties.

4. CURRENT CHARACTERISTICS AND FUTURE TRENDS

Population Forecasts including household growth and types

4.1 The 2008 Mid Year Population Estimates indicated a population of 149,100 for the

Borough at 2008. It forecasts a population of 161,400 at 2016 and one of 173,000

at 2026 6. Based on these projections, ONS produced projections for total

households which were published in November 2010. For Reading households are

forecast to grow from 58,000 in 2006 to 66,000 in 2018 and to 71,000 in 2026 7.

Average household size is forecast to fall from 2.48 to 2.34 between 2006 and

2016.

4.2 2011 population projections for Reading prepared by the Greater London Authority

Intelligence Unit 8 are based on ONS assumptions but also relate population growth

to forecast housing supply. They use the Council’s own housing trajectory/forecast

of housing completions as the basis for the forecast housing supply. The table In

Appendix 2 provides the resulting projections for Reading. These projections

indicate that there will be a population of 166,570 in 2016 (compared to 151,324 in

2006) and 181,417 in 2026. They forecast 69,200 households in the Borough in

2016 (compared to 61,900 in 2006) and 75,900 in 2026. The GLA projections

therefore indicate a faster rate of population and household growth for Reading

compared to the ONS forecasts.

Housing Data and Information

Housing in Reading

4.3 Reading’s continued economic success means that there is high demand for

housing, resulting in higher than national and regional average house prices that

have fallen relatively little even in the current economic recession. Because of

6

Table 2c at: http://www.statistics.gov.uk/downloads/theme_population/snpp-2008/InteractivePDF_2008-basedSNPP.pdf

7

See Table 406 at:

www.communities.gov.uk/housing/housingresearch/housingstatistics/housingstatisticsby/householdestimates/livetables-

households/

8

Berkshire Demographic Projections: 2010, GLA Intelligence Unit, February 2010

8 AFFORDABLE HOUSING BACKGROUND PAPERthis, the property market has become increasingly inaccessible to those on low to

middle incomes, due to the shortage of affordable housing 9.

4.4 A profile of housing in Reading:

• Number of dwellings: 64,388 10

• Tenure

o Homes owner occupied: 35,639(55.3%)

o Rented from a private landlord: 17,806 (27.4%)

o Houses of Multiple Occupation (HMO) – 5.5% (1.4% Licensable)

o Student accommodation: 1.9% (1254)

o Rented from a RSL: 3,762 (5.8%)

o Rented from Reading Borough Council (Including those in the PFI Area):

7,178 11.1%

o Miscellaneous: 0.4%

• 74% of Reading households live in detached, semi-detached, or terraced

houses, while a relatively high proportion (18%) live in flats or apartments.

• Reading ranks 3rd in the South East 11 for the percentage of homes without

sole use of bath/shower and/or toilet, and 4th in terms of ‘overcrowding’ 12.

Almost 8% of Reading households lack central heating.

• Nearly all new homes built in recent years have been built on land that had

been previously developed (“brownfield” sites). 13

• Households on the Council’s Housing Register: 7852 (April 2011), compared to

5993 (April 2010). Up from 4834 (April 2009). As can be seen Housing

registrations are growing rapidly in the current climate.

Reading Housing Stock

4.5 The Housing Stock in Reading was estimated at 64,759 at 31/03/2010.

Approximately 17.5% of the stock is owned by the local authority or Registered

Social Landlords (now known as Registered Providers).

House Prices

4.6 Information from the Land Registry plots the changes in house prices in Reading

Borough since 2000.

9

Housing that is available below market rent and will include shared ownership and sub-market rent properties (such as key

worker accommodation) as well as those available at social rent (Housing Associations, council housing).

10

Berkshire Demographic Projections: 2010, GLA Intelligence Unit, February 2010.

11

out of the 67 local authorities in the South East (excluding London)

12

assumes that every household requires a minimum of two common rooms

13

Berkshire Joint Strategic Planning Unit, Planning Commitments for Housing, annual publication.

9 AFFORDABLE HOUSING BACKGROUND PAPERReading Average Residential Property Prices

Semi- Flat

Year Detached Terraced Overall

detached /Maisonette

June £248,365 £139,585 £113,103 £102,689 £132,129

2000

June £256,300 £144,044 £116,717 £105,970 £136,350

2001

June £300,183 £168,707 £136,701 £124,114 £159,695

2002

June £324,315 £182,270 £147,690 £134,092 £172,534

2003

June £338,798 £190,410 £154,286 £140,080 £180,239

2004

June £352,472 £198,095 £160,513 £145,734 £187,513

2005

June £363,524 £204,306 £165,546 £150,303 £189,241

2006

June £400,837 £225,277 £182,538 £165,731 £208,666

2007

June £411,252 £231,130 £187,280 £170,037 £214,087

2008

June £347,898 £195,524 £158,430 £143,842 £180,963

2009

June £377,804 £212,332 £172,049 £156,208 £196,675

2010

£373,931 £210,155 £170,285 £154,606 £194,589

April

2011

% 50.56% 50.56% 50.56% 50.56% 50.56%

change

2000-

2011

4.7 The more detailed changes in average house prices along with changes in sales

volumes are illustrated in the graph below. They show that despite a halving of

sales volumes from their height, house prices remain relatively close to values not

long before the recession, perhaps reflecting a low supply of housing for sale.

Since April 2009, property prices have continued to increase steadily, albeit

relatively flatly over the recent 12 months, despite the current economic situation.

As can be seen from the figures, Reading remains a high house price area. It

follows that affordability remains a major issue for the borough. It is noticeable

10 AFFORDABLE HOUSING BACKGROUND PAPERthat prices have started to fall again since November 2010, albeit very slowly,

reflecting continuing uncertainty in the market.

Detached Semi- Terraced Maisonette/Flat All

(£) Detached (£) (£) (£) (£)

Apr-09 344,467 193,596 156,867 142,424 179,130

May-09 344,725 193,741 156,985 142,531 179,264

Jun-09 347,992 195,577 158,472 143,881 180,963

Jul-09 355,641 199,876 161,956 147,044 184,941

Aug-09 358,970 201,747 163,472 148,420 186,672

Sep-09 359,294 201,929 163,619 148,555 186,841

Oct-09 359,229 201,892 163,590 148,527 186,807

Nov-09 357,127 200,711 162,633 147,659 185,714

Dec-09 364,325 204,756 165,910 150,634 189,457

Jan-10 367,932 206,783 167,553 152,126 191,332

Feb-10 373,371 209,840 170,030 154,375 194,161

Mar-10 378,528 212,738 172,378 156,507 196,843

Apr-10 373,194 209,740 169,949 154,301 194,275

May-10 377,571 212,201 171,942 156,111 196,554

Jun-10 377,804 212,332 172,049 156,208 196,675

Jul-10 378,340 212,633 172,293 156,429 196,954

Aug-10 380,089 213,616 173,089 157,152 197,865

Sep-10 378,759 212,868 172,483 156,602 197,172

Oct-10 379,237 213,137 172,701 156,800 197,421

Nov-10 379,120 213,071 172,648 156,752 197,360

Dec-10 375,116 210,821 170,825 155,096 195,276

11 AFFORDABLE HOUSING BACKGROUND PAPERJan-11 370,479 208,215 168,713 153,179 193,035

Feb- 11 365,929 205,657 166,641 151,298 190,708

Mar-11 369,190 207,490 168,126 152,646 192,122

Apr- 11 373,931 210,155 170,285 154,606 194,589

Source: Land Registry 2011

House Price Change April 2009-Apr 2011

Average All Dwellings

200,000

195,000

190,000

185,000

All (£)

180,000

175,000

170,000

165,000

Jun-09

Apr-09 Aug-09 Dec-09

Oct-09 Feb-10 Jun-10

Apr-10 Dec-10

Oct-10

Aug-10 Feb-11

Private Rent Information

4.8 There is no authoritative data on average market rents in Reading. A number of

the letting agents in the town provide data on the average rent that they are

letting particular properties. An exercise to average a number of these provides

the following information:

Average monthly cost of a privately rented property in Reading (July 2011,

Home.co.uk 14):

1 bed properties: £633

2 bed properties: £1,021

3 bed properties: £1,056

4 bed properties: £1,101

5+ bed properties: £1,218

This compares with similar data for April 2009:

14

www.home.co.uk

12 AFFORDABLE HOUSING BACKGROUND PAPER 1 bed properties: £654

2 bed properties: £787

3 bed properties: £884

4 bed properties: £1203

5+ bed properties: £1976

As can be seen the cost of 2 and 3 bedroom properties have increased dramatically

in 2 years whereas for the larger sizes of property, rental levels have fallen fairly

dramatically

Affordable Housing Completions

4.10 Information on affordable housing provision since 1990 is contained in Appendix 3.

Provision since 2001 is set out below in Table 4.

No of affordable unit HSSA Affordable Housing

completions via planning Completions including

Year permissions (on fully Homebuy and non

completed sites). planning provision.

2001/2 173

2002/3 51 +£188,000 149

2003/4 30 302

2004/5 195 +£100,000 360

2005/6 309 +£372,000 311

2006/7 91 +£80,000 180

2007/8 210 302

2008/9 229 294

2009/10 121 184

2010/11

Total 1236 2255

Divide by 155 dwellings per annum. 251 dwellings per annum.

number of

Years

4.11 The figures above in column 2 are taken from planning records and trace

applications subject to Section 106 agreements for the provision of affordable

housing. Numbers in relation to each individual scheme have then been cross

checked against Housing Section records for provision on a scheme by scheme

basis. The figures do not include any housing bought for the purpose of renting or

reselling as affordable housing or affordable housing resulting from schemes such

as the Homebuy or deposit guarantee schemes. They therefore solely reflect

affordable housing provision resulting directly from the operation of planning

policy and agreements under Section 106.

4.12 For comparison, the total numbers of affordable housing provided in the Borough

each year, as recorded on HSSA (Housing Strategy Statistical Appendix) returns to

DCLG and its predecessors provides the estimate in column 3 for total affordable

housing provision in the Borough. The Council’s Housing Section produce their own

annual provision figures derived from their liaison work with partner organisations

13 AFFORDABLE HOUSING BACKGROUND PAPERincluding partner registered providers. This includes details of provision arising

from non planning provision such as instances where registered providers purchase

new or second hand properties on their own account. It also includes houses

purchased as a result of the Homebuy initiative, the Deposit Guarantee Scheme

and other non planning additions to the affordable housing stock.

4.13 As can be seen from the results in the table of affordable housing completions

existing local plan policies and their interpretation through the SPG on Planning

Obligations, and the adopted LDF Core Strategy, along with the separate efforts of

the Council’s Housing and Planning Sections, have been very effective in producing

new affordable housing in the Borough over many years.

Right to Buy

Number of dwellings

sold under Right to

Buy

Outturn Outturn Outturn Outturn Outturn Outturn

2005 2006 2007 2008 2009 2010

17. Number of 45 13 17 13 4 10

dwellings sold under

RTB

An average of 17 dwellings per year are lost from the Affordable Housing Stock as a result

of the Right to Buy Scheme.

Housing Needs

The assessment of need for affordable housing in Reading

4.14 Government policy, including national and regional planning guidance, requires

Local Authorities to have an up-to-date assessment of housing need on which to

base affordable housing policy. In 2000, Reading Borough Council commissioned

ORS (Opinion Research Services, a spin-out company of the University of Wales at

Swansea) to undertake a Housing Needs & Aspirations Survey (HN&AS).

4.15 It was the Council’s intention to match or exceed good practice recommended by

Government at that time as it wished to examine and understand the dynamics of

demand and need within the whole of Reading’s housing market, rather than just

the need for affordable housing.

4.16 The Council therefore invited a cross-sector group of stakeholders to contribute

their expertise to enabling ORS to evolve its survey-methodology to best capture

and analyse the characteristics of Reading’s complex and highly pressured housing

market. This cross-sector group subsequently steered the study. The group

comprised:

• Reading Borough Council

• The Housebuilders Federation

14 AFFORDABLE HOUSING BACKGROUND PAPER• The DTLR Research Division

• The Berkshire Joint Strategic Planning Unit

• Thames Valley Housing Association (on behalf of Reading BC’s five housing

association partners)

• Haslams’ New Homes Consultant

4.17 Relevant key findings of the Housing Needs & Aspirations Survey were:

• Over each of the 5 years 2003-2008, Reading will require some 6660 annual

housing “transactions” (i.e., sales/purchases and lettings/re-lettings) across

its entire housing market, to meet both the demand for open-market housing

and the need for affordable housing;

• The existing housing stock and the anticipated net additions to it will provide

some 5604 of these transactions annually;

• The shortfall in Reading’s housing supply is therefore some 1056 units in each

of the 5 years. (This does include an element to clear within 5 years the

backlog-need of newly-forming households which are currently living within

other, existing, households)

• Of the 1056 households each year for whom there is a shortfall of housing

supply, 390 (37%) households would be able to buy or rent at open market

values, i.e. without some degree of subsidy.

• The remaining 666 households (63%) would require some form of affordable

housing.

• The needs identified are split between the tenures in terms of household

incomes and house prices in the following way:

o social rented, 37%

o intermediate sale (e.g. shared ownership), 27%; and

o sub market rented accommodation, 36%

It is anticipated that the provision of a range of tenures in the proportions

described will appropriately provide for the range of needs identified including the

needs of key workers who are currently unable to afford housing at open market

prices.

Berkshire Strategic Housing Market Assessment

4.18 This Study was jointly commissioned by the six Berkshire Unitary Authorities and

was prepared by DTZ during 2006 and the early part of 2007. The final report of

the study was submitted to commissioning local authorities at the beginning of May

2007. It covers some 230 pages. The Study was prepared and conducted in

accordance with the CLG draft Housing Market Assessment guidance. The DCLG

published the final guidance on 30th March 2007. The study is wide-ranging and

15 AFFORDABLE HOUSING BACKGROUND PAPERvery detailed. The analysis below is based on the details contained in the

summary document.

4.19 The first step of the study was to analyse housing market areas. The study found

that Berkshire is made up of 2 separate functional housing market areas, albeit

facing different influences, with East Berkshire strongly influenced by London, and

West Central Berkshire, within which Reading is the main attraction, showing a

higher level of economic self-containment.

4.20 Reading is the main hub of the West Central Berkshire Area being the main centre

of employment. The study found that Reading formed part of a market that

includes West Berkshire, Wokingham and Bracknell, stretching also into parts of

South Oxfordshire.

Demographic Drivers

4.21 The current (2004) population of the West Central Berkshire area is 584,000.

Overall growth in population over the period 1981-2004 was 19% in West Central

Berkshire (a population increase of 92,400), compared to 12% growth in the South

East over the period. The Berkshire housing markets experience net in-migration

from London and internationally but net out-migration to all other parts of the UK.

At present the population of both market areas has a slightly younger bias when

compared to the South East and England as a whole. Average household size in the

West Central Berkshire is 2.46 people per household space. This is above the

average for the South East (2.39) and England (2.37). The total number of

households in the West Central Berkshire area increased by 13% between 1991 and

2001 (an additional 26,600 households). The East Berkshire market area

experienced more limited household growth over the period of around 8%, less

than the rate of growth observed in the South East (11%) and England (9%).

Although there is likely to be significant growth in single person households

(including elderly households) in the future, couple households (with and without

children) will remain the largest group in all authorities in 2026.

4.22 Ethnic composition of the population shows higher levels of ethnic communities

than in SE or England. In common with other centres in Berkshire, Reading has

experienced a substantial influx of migrants from Eastern Europe, particularly

Polish migrants. This is undoubtedly affecting the private rented housing market.

4.23 Economic Growth. For the period 1995-2004, growth in the number of jobs in

each of the market areas has surpassed comparative growth in England; West

Central Berkshire area experienced 24% employment growth, Berkshire County 22%

employment growth, and both East Berkshire and the South East 19% employment

growth. The economies of West Central and East Berkshire have undergone

considerable change over the past 10 years. Change has been driven by growth

within the service sectors such as Banking, Finance and Insurance activities and

Other Services. Demand for market housing within both market areas will therefore

have been driven by those employed in high paid and high value sectors who will

tend to have higher incomes and who are able to exercise greater choice within

the market. Up until 2007, both the East Berkshire and West Central Berkshire

economies were operating at the levels associated with full employment.

16 AFFORDABLE HOUSING BACKGROUND PAPER4.24 Tenure, Housing Stock and Recent Completions. Owner-occupation in West

Central Berkshire (75%), is marginally higher than the level for the South East

(74%). Levels of social renting are relatively low but the distribution of social

renting tends to be concentrated in particular locations. West Central Berkshire

area has a lower proportion of social rented housing (13%) than in East Berkshire

(16%). West Central Berkshire has a relatively low proportion of flats, maisonettes

and apartments (15%) and a high proportion of detached housing (32%) compared

to East Berkshire and the South East. 60% of the stock in the West Central

Berkshire is detached or semi-detached, slightly higher than the average for the

South East. The Buy to Let market has emerged as a phenomenon since 2001 and

recent development (in the towns at least) has been dominated by flats and

apartments. Since 2001 within Berkshire, over 50% of new private development in

has been delivered as flats. 15

4.25 House Prices: Overall, the average house price in Berkshire (£247,000) is higher

than the average for the South East (£229,000) or England (£195,000) (2006 prices).

Furthermore, house prices within Berkshire have doubled in the last 10 years, with

the fastest rises in East Berkshire. In all areas, semi-detached house prices have

increased at a higher rate than overall average house prices over the period 1995

to 2006, which can indicate pressure on the larger stock of dwellings.

4.26 Affordability: Affordability is poor and has worsened since 2002. The relationship

between house prices and incomes within Berkshire is such that a proportion of

households are unable currently to buy or rent housing within the market areas.

There are over 21,000 households registered as seeking housing with the local

authorities in Berkshire. In March 2006, over 600 homeless households were living

in temporary accommodation, an unequivocal indicator of housing need.

4.27 The assessment of housing need in five of the Berkshire authorities was undertaken

in line with the DCLG draft guidance.

15

NHBC completions data by type and size obtained by DTZ

17 AFFORDABLE HOUSING BACKGROUND PAPER4.28 The assessment estimates that there is a need for between 3,000 and 4,200

additional affordable homes across Berkshire per annum. Given the scale of

housing need identified, there is therefore a need to prioritise in terms of future

affordable housing provision. The level of need in Berkshire exceeds the total

annual housing allocations (market and affordable) for Berkshire as proposed in the

Regional Spatial Strategy. Thus, with the current levels of funding and at current

levels of housing development, it is unlikely that there will be sufficient provision

of affordable housing to both meet current and newly arising need. There is a

need for all types of affordable housing but the analysis shows that between 15-

20% of newly forming households will not be able to afford any of the intermediate

tenures such as shared ownership of intermediate rent. The core requirement to

address the housing need within Berkshire is for social rented accommodation and

it is likely that the authorities will need to prioritise the provision of this type of

housing.

4.29 Within Reading the analysis of affordable housing needs also found that there was

a substantial unmet need for large family houses. This is backed up by the severe

pressures being experienced by Housing colleagues in providing such

accommodation.

4.30 Housing Mix. Under consideration of Housing Mix the study noted that there are

relatively severe levels of overcrowding evident across Berkshire but in Reading

and Slough in particular in the private and social rented sectors. There is evidence

of pressure on large affordable dwellings in some authority areas with larger

households in need having to wait longer to be re-housed and this may point to the

need secure a higher number of larger affordable homes in some authorities than

has been delivered in recent years

4.31 The summary and recommendations put forward a number of salient points. While

housing markets within Berkshire work well for the majority, there are a number of

challenges for the Berkshire authorities and their delivery partners:

18 AFFORDABLE HOUSING BACKGROUND PAPER• The Challenge of Addressing Housing Need within Berkshire. The scale of

housing need outstrips what can realistically be met;

• The Challenge of Delivering Mixed Communities. – The housing market

within Berkshire is polarised;

• The Challenge of Delivering New Housing in the Future. New affordable

housing and the opportunity to create mixed income communities is highly

dependent on the delivery of new market housing within Berkshire.

4.32 Seven recommendations were put forward.

• Recommendation 1 deals with the range of factors that need to be

considered in providing for the high level of need for affordable housing;

• Recommendation 2 is concerned with prioritising in terms of the type of

affordable housing secured with the core requirement being for social

rented accommodation;

• Recommendation 3 is that authorities could improve the data held on

housing registers so that authorities can assess the extent to which

households are able and willing to access intermediate housing products.

This recommendation also indicates that an overall target of 35% is an

achievable target for affordable housing provision in line with the figure in

the emerging RSS. It indicates that authorities will need to consider higher

targets for larger sites and their thresholds if such a target is to be

achieved;

• Recommendation 4 There is a relatively strong case for supporting the

development of a greater proportion of certain types and sizes of homes in

different authority areas, including a higher proportion of larger new homes

in Slough and Reading.

• Recommendation 5 Authorities should allocate a variety of different types

and sizes of housing land to assist in encouraging a range of tenures and

housing types.

• Recommendation 6 is concerned with how authorities such as Reading

might facilitate the provision of more houses to meet the priority need for

such accommodation in the affordable housing sector;

• Recommendation 7 is that all authorities need to plan for an aging

population and that Slough and Reading need to plan for the needs faced by

ethnic minorities in their areas. It goes on to make comments on the

delivery of housing to meet the requirements set out in the emerging South

East Plan.

4.33 The Berkshire Housing Market Assessment provides a wealth of evidence on the

housing markets in Berkshire. It emphasises the need for a high level of provision

overall to meet economic objectives. It notes that recent trends are providing

considerable numbers of flats that may be unbalancing the market and failing to

19 AFFORDABLE HOUSING BACKGROUND PAPERmeet needs. It reinforces existing evidence of the high level of need for

affordable housing that exists, emphasising the importance of determining

priorities within the wide range of needs that are evident. The assessment does

not appear to have made findings or reached conclusions that suggest that any part

of the Core Strategy needs to be changed. It does, however, provide evidence and

recommendations that will be picked up in future housing strategies and that will

inform future DPD’s and the preparation of SPD‘s particularly on affordable housing

and planning obligations.

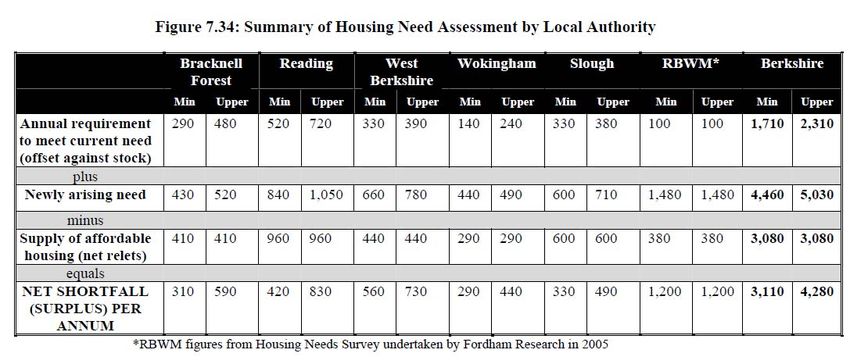

4.34 The Berkshire Strategic Housing Market Assessment is also backed up by “A

Technical Report for Reading Borough Council, Housing Need Assessment, April

2007. 16 This report provides a more detailed analysis of need in Reading Borough

arising from the methodology used by the study. The Figure below copies Figure

3.12 from the study which provides the Estimated of Total Requirement for

Affordable Housing in reading and for West Central Berkshire and Berkshire as a

whole.

Figure 3.12: Estimated of Total Requirement for Affordable Housing

Total

4.35 The study goes on to look at tenure. It points to the fact that although products

such as shared ownership and intermediate rent will help provide affordable

housing for sections of those households that cannot afford open market housing, it

still leaves many still unable to afford housing. Paragraph 3.65 states,

“The key conclusion here is that even with the cheapest intermediate product

(and the highest level of subsidy) at least 19% of new households within Reading

are unlikely to be able to meet their needs in the market and, by implication,

are likely to require social rented accommodation.”

4.36 Housing Waiting Lists and Registers currently point to the following finer grained

needs:

• disabled persons units +other specialist properties such as properties with a

bedroom and bathroom downstairs for those families coping with a disabled

adult in the house;

16

http://ww2.reading.gov.uk/documents/Housing_and_Benefits/housing%20development/040407%20-

%20Reading%20HNA%20v1.0.pdf

20 AFFORDABLE HOUSING BACKGROUND PAPER• Big 4 bed & above houses;

• Disabled adapted housing especially to meet needs of disabled children;

• 1 bed flats in blocks of not more than 6 for vulnerable singles.

• Pepper potted small flats on s 106 sites

• Accommodation for Learning Disability clients and physically disabled people.

• Bungalows with flexible use e.g. flat for carers;

• Extra Care Provision for more vulnerable elderly.

4.37 Other needs and priorities will from time to time be detailed and changed through

the Council’s Housing Strategy.

4.38 Current Housing waiting lists show a total of 5993 on the list at 1st April 2010. Of

these, 3030 were considered to be in a reasonable preference category.

4.39 The above evidence demonstrates a very high level of need for affordable housing

in the Borough. Planning has a crucial role in assisting in meeting those needs

through the provision of a proportion of affordable housing as part of all new

developments.

5. POLICY DISCUSSION

5.1 The need for affordable housing is one of the most important issues facing

Reading. The success of the sub region as an economic driver has added to

demand for housing overall. House prices are well above the national average.

Average house prices make it increasingly difficult for those on low incomes to find

accommodation they can afford. The concept of “affordability” is essential when

looking at housing needs. That is what households can afford to pay for their

housing, and whether this is sufficient to meet their needs. Access to reasonably

priced homes is essential for the local economy, so that there is a ready supply of

locally based workers to meet job vacancies. Key workers, who are essential to

support the local economy and society, such as teachers and nurses, must have

affordable housing in order to live locally. Having a workforce living locally also

reduces the environmental and economic costs incurred in travelling to and from

work.

Affordable Housing Targets

5.2 The Council’s Housing Strategy, 2009 -2014, discusses a target of 40% of all housing

being in the form of affordable housing. It points to the target in the Adopted

Core Strategy (paragraphs 6.26 and 6.27) that 50% of housing on sites of over 15

dwellings will be affordable.

21 AFFORDABLE HOUSING BACKGROUND PAPERAffordable Housing Thresholds

5.3 Over a number of years, Reading Borough Council has operated a threshold of 15

dwellings above which affordable housing has been expected as part of residential

development schemes. In preparing its SPG on Planning Obligations during 2003/4,

the Council considered and resolved to make allowance for the reduction of this

threshold figure in line with draft Changes to PPG3 that were published by the

government during 2003. However, the draft changes enabling lower thresholds

to be used did not materialise in the final changes to PPG3. That proposal was

then carried over into the new PPS3 published, at the end of 2006, just as the

draft Core Strategy was being submitted.

5.3 Statistics for small site completions, defined as sites of less than 1ha with less than

10 net dwellings is monitored annually. For the Core Strategy, the Inspector

accepted that an average of 141 dwellings are completed on windfall sites of less

than 10 dwellings per year (although the figures below suggest a higher level of

completions on such sites). Analysis has been undertaken on completions on sites

of 10-14 dwellings and the table below sets out evidence of housing provided on

sites of less than 15 dwellings in the bands referred to in the draft policy.

Dwellings Dwellings Dwellings

Net Dwelling completed in completed in completed in

Year

Completions developments of developments developments

10-14 units of 5 - 9 units of 1 - 4 units

00/01 371 27

01/02 747 91

02/03 574 24

03/04 761 130

04/05 1177 116

05/06 656 98 40 118

06/07 637 74 51 75

07/08 837 54 31 137

08/09 782 91 79 137

09/10 693 140 58 124

10/11

Totals 7235 845 259 591

Yearly Average 723 84 52 118

% of Total 11.6 7.2% 16.3

Affordable

Housing

Potential with 25 (30%) 10 (20%) 12 (10%)

30%, 20% and

10%

Note: Staged applications and adjoining sites have been counted as separate

developments where they have been assigned a separate application number.

Source: Planning Commitments for Housing, Reading, Berkshire Joint Strategic

Planning Unit, 2000-2010

22 AFFORDABLE HOUSING BACKGROUND PAPER5.4 As indicated, this produces an average of 84 dwellings per year on sites of 10-14

dwellings and an average of 254 dwellings on sites of less than 15 dwellings. It is

clear that a sizeable proportion (35.1%) of the Borough’s housing land supply

derives from sites of below the threshold of 15 dwellings and that appropriate

contributions from sites of this size of site could, potentially, make a significant

contribution towards affordable housing completions in the Borough.

5.5 As indicated by the analysis in the final row, this policy has the potential to

produce an average of up to 47 affordable dwellings per annum which will provide

more than an additional 30% to the average provision of affordable housing

achieved through planning on sites of 15 or more dwellings. The pursuit of such a

level of affordable housing will be very worthwhile.

5.6 As indicated, small sites of 1-4 dwellings have scope to make a contribution

towards affordable housing provision either on site or more likely, offsite as the

market improves. Offsite contribution will provide valuable income that can be

put to the construction of affordable housing, perhaps much needed larger family

homes, elsewhere in the Borough. A very rough estimate of completions over last 5

years shows an average of 110 completions in the 1- 4 category, approximately half

of which are new build developments. On 50 new build houses, if the charge was

£7,000 a unit as the 10% contribution to providing a unit, it would provide around

£350,000 a year? Appropriate contributions from conversions and COU in the 1-4

dwelling category will add to this figure.

Viability

5.7 Work was undertaken in house during 2009 by the Council’s Valuation Section to

consider the viability of various levels of target provision for a range of sites of less

than 15 dwellings. Viability was tested in market conditions prevailing at the time

during 2009, when the market was quite near the bottom of the downswing in the

economy, and for the market conditions that existed at September 2007 when the

market was approaching, but not at, its highest. The market peaked in the early

part of 2008, at about the time that the Northern Rock Building Society was

brought into national ownership. The assumption was that the market would

return to conditions similar to those that existed at September 2007 during the

plan period. That work determined that the target provision set out in the draft

policy would be viable, certainly with modest levels of grant, at September 2007

conditions, although it was accepted that they were challenging in the 2009

market conditions.

5.7 Various changes in planning policy, law and the housing market since the original

Draft SDPD was published in February 2010 has required a review of existing Draft

Policy DM 6 on Affordable housing. In particular there was a need to reassess

whether the justification for the target provision set out in the policy remains

viable.

5.8 The High Court (Blyth Valley Borough Council vs. Persimmon Homes (North East)

Limited) has ruled that policies seeking the provision of affordable housing must be

accompanied by evidence that demonstrates that the targets contained within the

23 AFFORDABLE HOUSING BACKGROUND PAPERpolicy are viable (i.e. have a reasonable prospect of being delivered by

development in the Borough and not likely to deter such development). Having

undertaken the analysis and review discussed below, the conclusion is that the

policy and its targets can continue to be justified in terms of viability on the basis

that the housing market is improving and will improve, although there may be

some bumps along the way, that grant may be available for small sites in the

future, within the plan period, and the wording is very clear that the policy allows

applicants to submit viability information to demonstrate why targets can not be

achieved.

5.9 The target proportions for provision were tested at the end of 2009/beginning

2010, before the first Pre-Submission Draft SDPD was published, in terms of

viability based on Autumn 2009 prices when the market was probably at its lowest

and compared with September 2007 prices. Historically we know that markets are

cyclical, the housing market rises, then falls but usually returns to rising prices. At

the time of publishing the SDPD in February 2010, it was considered that the

housing market was likely to return to September 2007 house prices in a relatively

short space of time. There were clear signs that the economy was starting a

recovery. A series of viability assessments on hypothetical sites were undertaken

to test different sizes and types of developments. Viability was tested for

situations where affordable housing grant was available and where grant was not

available.

5.10 The conclusion of the viability assessments was that most developments, especially

the larger schemes, would be of marginal viability in providing the target provision

in the 2009 house price scenario, both when grant is available but more so where

no grant is available. However, in nearly all cases the proposals would be viable at

2007 prices with or without grant. It was therefore considered that the policy was

broadly in line with current practise and likely to be found sound based on the

assumption that the property market would recover to prices comparable with

2007 price levels within the plan period.

Current Situation (June 2011)

5.11 The current economic situation and the new public sector settlement have

changed the outlook in several ways. House price growth, levels of mortgage

offers and new build outputs are all rather flat and demonstrating only limited

signs of recovery. In fact, as can be seen above, the evidence on house prices

shows a gradual fall and then a gradual rise so far during 2011. This reflects

continuing uncertainty in the market as a result of uncertainty in the economy,

public sector cutbacks, fears of interest rate rises, international financial

uncertainty, continuing restraints in mortgage lending, etc. This suggests that low

viability will remain a concern for most schemes of less than 15 dwellings. House

prices are now not seen as likely to return to 2007 levels for some time. Prices

since the end of 2010 have reflected this uncertainty but remain relatively higher

than 2009 levels as can be seen above. Borrowing and other funding costs are

expected to remain much higher than in 2007. Expected profit levels/rates of

return are likely to remain at higher levels reflecting higher perceived risks and

consequently more onerous lending criteria. These factors mean that viability is

likely to remain lower than September 2007 levels on sites of less than 15 dwellings

24 AFFORDABLE HOUSING BACKGROUND PAPERfor some time yet. The recovery may be slower than was anticipated during the

early part of 2010. Nevertheless, the medium to longer term outlook is for the

economy to recover and for house prices to rise and viability to improve.

5.11 Further work has been undertaken to test viability, including independent

verification of the work undertaken in house. This has included consideration of

the emerging regime arising from government policy on affordable housing and

changes in HCA grant allocations. It is clear from the public sector settlement

outlined in October 2010, that there will be less public subsidy of affordable

housing and thus more emphasis on developer provision to meet identified needs.

The government has introduced the affordable rent product and added this to its

typology of affordable housing to which PPS3 applies. The council and various

housing associations have been assessing the new product/model against identified

need, current priorities, costs and viability. Under this model, DCLG through the

HCA are promoting a form of rental affordable housing at levels of up to 80%

market rents. This will allow providers to achieve high levels of provision without

public subsidy and is intended to produce more affordable housing at lower costs.

While, where provided on site, such housing will provide for an element of housing

need for those on moderate incomes which do not allow them to buy on the open

market, it is not going to produce housing for those most in need or the priority

need identified in the Strategic Housing Market Assessment.

5.13 Officers have given some further thought to how the policy will be operated and

how any provision/contributions are determined in the current circumstances.

5.14 One issue is that the preparation and assessment of viability studies is relatively

expensive, certainly in relation to the amounts of provision and contributions we

are talking about for the smaller sites. In addition, a part of the housing provision

from smaller sites is in the form of conversions and changes of use, where viability

is likely to be much less certain than for new build situations. We need to find

ways of determining an acceptable level of provision/contributions without every

application having to be subject to an individual viability assessment. That might

take the form of an SPD that is updated annually or just an informal position

statement that sets out what officers will accept at particular points in time in

view of market conditions and the availability/ non availability of grant. A

reference to some such mechanism has been added to the text.

6 PREFERRED APPROACH AND REJECTED ALTERNATIVES

Preferred Approach

6.1 Various alternative approaches to implementing the provisions in PPS3 and Policy

CS16 of the Core Strategy were considered as follows:

No SDPD Policy for AH provision on sites below 15 dwellings;

A policy providing complementary guidance to Policy CS 16 but retaining

the threshold of above 15 dwellings;

Having a lower threshold of 1-14 units;

Having a lower threshold of 10-14 units or 5-14 units

25 AFFORDABLE HOUSING BACKGROUND PAPERYou can also read