Amendment C171 Melton Planning Scheme - Expert witness statement of Chris Abery, Deep End Services Prepared for Ranfurlie Developments Pty Ltd 20 ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Amendment C171 Melton Planning Scheme Expert witness statement of Chris Abery, Deep End Services Prepared for Ranfurlie Developments Pty Ltd 20 March 2017

Deep End Services Deep End Services is an economic research and property consulting firm based in Melbourne. It provides a range of services to local and international retailers, property owners and developers including due diligence and market scoping studies, store benchmarking and network planning, site analysis and sales forecasting, market assessments for a variety of land uses, and highest and best use studies. Contact Deep End Services Pty Ltd Suite 304 9-11 Claremont Street South Yarra VIC 3141 T +61 3 8825 5888 F +61 3 9826 5331 deependservices.com.au Enquiries about this report should be directed to: Chris Abery Principal Chris.abery@deependservices.com.au Document Name Am C171 Chris Abery witness statement (FINAL)- 17 March 2017 20.03.17 Disclaimer This report has been prepared by Deep End Services Pty Ltd solely for use by the party to whom it is addressed. Accordingly, any changes to this report will only be notified to that party. Deep End Services Pty Ltd, its employees and agents accept no responsibility or liability for any loss or damage which may arise from the use or reliance on this report or any information contained therein by any other party and gives no guarantees or warranties as to the accuracy or completeness of the information contained in this report. This report contains forecasts of future events that are based on numerous sources of information as referenced in the text and supporting material. It is not always possible to verify that this information is accurate or complete. It should be noted that information inputs and the factors influencing the findings in this report may change hence Deep End Services Pty Ltd cannot accept responsibility for reliance upon such findings beyond six months from the date of this report. Beyond that date, a review of the findings contained in this report may be necessary. This report should be read in its entirety, as reference to part only may be misleading.

Contents

Introduction 1

1.1 Name & address of expert 1

1.2 Experts qualifications & experience 1

1.3 Expert’s area of expertise 2

1.4 Expertise to make report 2

1.5 Documents, materials, and literature used in preparing this report 2

2 Melton Retail and Activity Centres Strategy 3

2.1 Amendment C171 Melton Planning Scheme 3

2.2 Economic and Policy context 4

2.3 MRACS Methodology 5

Population and spending 5

Floorspace demand 5

Scope for New Centres 6

Catchment analysis 7

2.4 Activity Centre expectations 8

2.5 Caroline Springs findings 9

2.6 Burnside findings 9

3 Burnside Activity Centre 12

3.1 Location 12

Regional setting 12

Regional population growth 13

Regional roads connections & traffic volumes 16

Surrounding employment growth 18

3.2 Burnside activity centre 19

3.3 Burnside Hub 21

3.4 Extended centre 21

3.5 Extended MRACS Catchment area 22

3.6 The case for a DDS at Burnside 24

3.7 Burnside meeting the expectations for Activity Centres 26

4 Activity centres hierarchy 28

4.1 Melton East Structure Plan Activity Centre Framework (1997) 28

4.2 Activity Centre Network 30

4.3 Comparable spaced centres 32

4.4 Impacts 33

4.5 Benefits 35

5 Conclusions 36

Appendices

Appendix A Curriculum Vitae – Chris Abery

Amendment C171 Melton Planning Scheme—20 March 2017 Deep End Services

Tables + Figures

Table 1—Population growth 15

Table 2—Burnside Hub existing floorspace 21

Table 3— Core catchment area populations 22

Table 4—Activity Centre floorspace 32

Figure 1—Sub regional catchments from MRACS 8

Figure 2—MRACS Final Proposed Activity Centre Network 11

Figure 3—Regional location 13

Figure 4—Population areas 15

Figure 5—Regional road connections 16

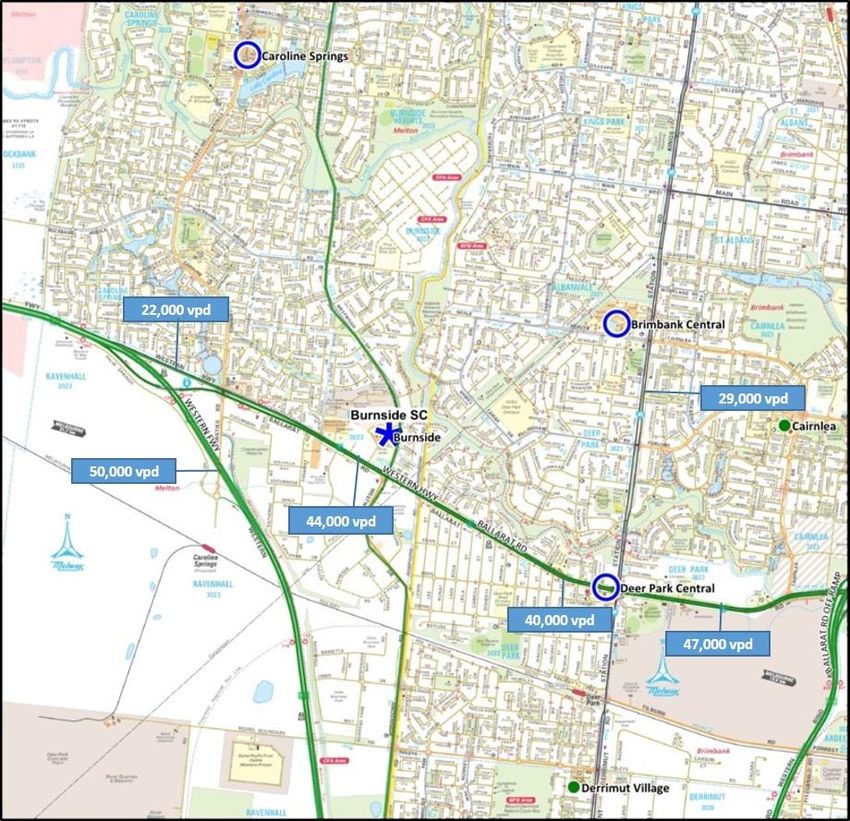

Figure 6—Traffic volumes 2015 (vehicles per day) 18

Figure 7— Commercial and Industrial land available - 2016 19

Figure 8—Burnside Activity Centre – February 2017 20

Figure 9—Adjusted MRACS catchments 23

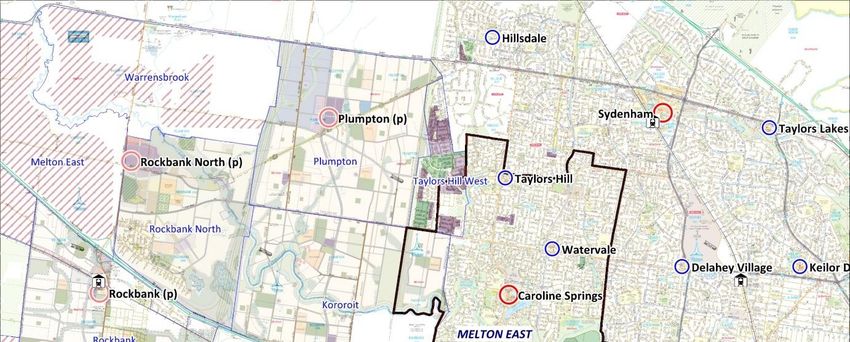

Figure 10—DDS provision outer west 26

Figure 11—Melton East Strategy Plan (1997) Activity Centre Framework 29

Figure 12—Activity Centre Network 31

Figure 13—Relative locations of Activity Centres and other DDS-based

centres 33

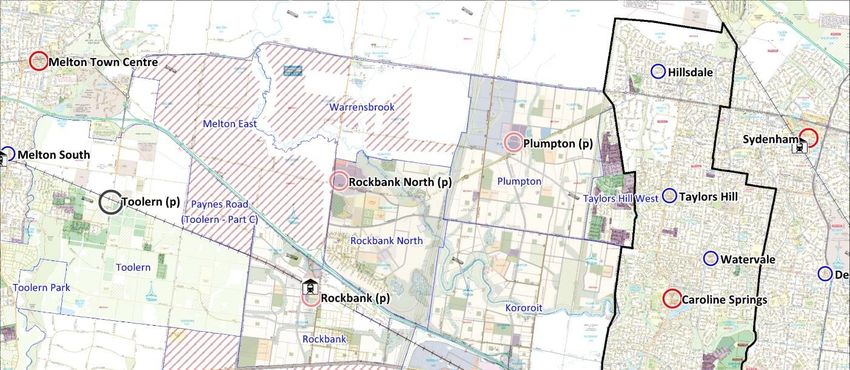

Amendment C171 Melton Planning Scheme—20 March 2017 Deep End Services

1

Introduction 01 My name is Chris Abery. I am a Principal of Deep End Services, a consulting firm

which practices in retail analysis and property economics. My statement has been

prepared to assist the review by Planning Panels Victoria of Amendment C171 (the

Amendment) to the Melton Planning Scheme.

02 My instructions from Minter Ellison on behalf of Ranfurlie Developments Pty Ltd

(owners of Burnside Hub Shopping Centre and surrounding land) are to review the

Amendment and provide expert retail and economic evidence in relation to

Burnside’s proposed designation as an Activity Centre under the Melton Retail and

Activity Centres Strategy (MRACS) and Clause 21.05 of the Melton Planning

Scheme.

03 In preparing this report I have inspected the site, surrounding areas and shopping

centres. I have reviewed the Melton Planning Scheme and the Melton Retail and

Activity Centres Strategy.

04 In arriving at my conclusions, I have made all the inquiries that I believe are desirable

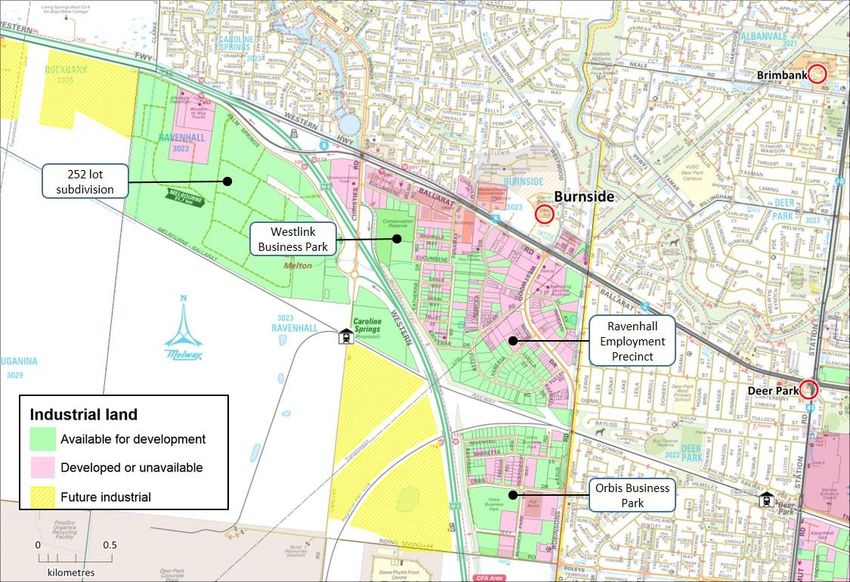

and appropriate and no matters of significance that I regard as relevant have, to my

knowledge, been withheld from the Panel.

1.1 Name & 05 Mr Chris Abery

address of expert Principal

Deep End Services Pty Ltd

Suite 304 / 9-11 Claremont Street

South Yarra Victoria 3141

1.2 Experts

qualifications & 06 Bachelor of Town and Regional Planning, University of Melbourne

experience

07 Graduate Diploma Social Statistics, Swinburne Institute

08 I have 32 years’ experience in spatial modelling, retail and market analysis and

property economic evaluation.

09 I have been a Principal of Deep End Services, a property and retail economics

consultancy since June 2009, where I have worked with national retail clients,

shopping centre owners and developers on need and demand assessments, network

planning and economic impact evaluations.

10 I was a Director in the Property Economics unit of Urbis between March 2007 and

April 2009.

11 I have held senior roles in the Property Team at Coles Myer Ltd between 1992 and

2007 including as National Manager Strategy and Property Analysis. In that role, I

lead a team responsible for the network planning of Coles Myer retail businesses

across Australia, forecasting turnover of all new store proposals, due diligence of

property and business acquisitions, urban planning advice and general market

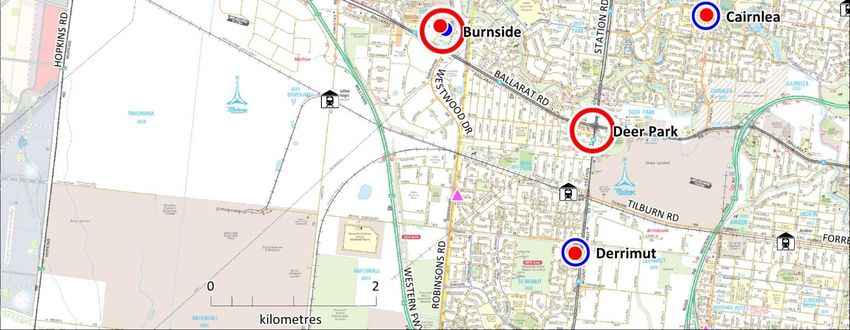

advice to senior management and the Coles property team.

12 Between 1986 and 1992 I was employed as a consultant with Ratio Consultants, an

economics and urban planning consultancy.

13 A full CV is included at Appendix 1.

Amendment C171 Melton Planning Scheme—20 March 2017 Deep End Services

2

1.3 Expert’s area 14 Development and execution of turnover forecasting models for new retail stores

of expertise including supermarkets, discount department stores, department stores, liquor

stores and fast food outlets for retailers and shopping centre owners.

15 Market assessments and turnover forecasts for new or expanding retail centres.

16 Preparation of demand and supply studies on supportable levels of retail and

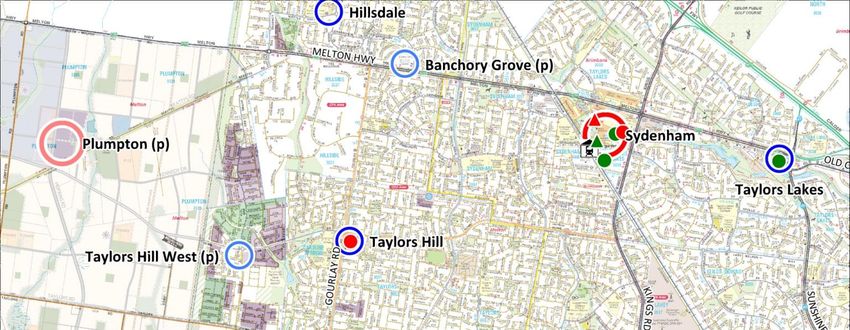

commercial floorspace in growth areas and established markets.

17 Analysis of consumer data and research relating to retailing and shopping centre

developments.

18 Spatial analysis of customer data to model retail catchments and market shares for

the purpose of sales forecasting.

19 Market research and commercial advice in relation to the recommended land use,

layout, size, facility mix, turnover and rents of mixed use developments.

20 Preparation of economic impact assessments for proposed retail developments and

expert witness evidence.

1.4 Expertise to 21 Detailed knowledge of Australian retail and shopping centre operations and impacts

make report resulting from development of new supermarkets and other retail facilities.

22 Long term involvement with retailers and owners and developers of shopping

centres.

23 Preparation of evidence for and appearances at Planning Panels, Appeal Tribunals,

Licensing Boards and courts in Victoria, Tasmania and New South Wales.

1.5 Documents, 24 Amendment C71 Melton Planning Scheme

materials, and 25 City of Melton Retail & Activity Centres Strategy

literature used in

preparing this 26 Australian Bureau of Statistics Census and other published data

report

Amendment C171 Melton Planning Scheme—20 March 2017 Deep End Services

3

Melton Retail and Activity Centres Strategy

27 This section reviews the economic and policy context for the MRACS and the

assumptions and analysis which lead to the findings in relation to the Burnside

Activity Centre.

2.1 Amendment 28 Amendment C171 implements the recommendation of the City of Melton Retail and

C171 Melton Activity Centres Strategy, March 2014 by amending the Municipal Strategic

Planning Scheme Statement and Local Planning Policy.

29 The Amendment inserts a new Clause 21.05 (Activity Centres and Retail Provision)

and updates the existing Clause 22.06 (Retail Policy). Clause 21.05 introduces a new

hierarchy of activity centres in the municipality with new Objectives and Strategies.

30 Clause 21.05-4 (Activity Centre Network) contains Map 1: City of Melton Activity

Centre Hierarchy: Supportable Network of activity centres at full development

which identifies Burnside as one of four existing ‘Activity Centres’ along with four

new Activity Centres. Under this clause, Burnside its upgraded from its current

designation as a neighbourhood centre.

31 Clause 21.05-4 also contains Table 1 (City of Melton Activity Centre Hierarchy)

which sets out the ‘Land Use Strategies’ for each level in the hierarchy. Activity

Centres sit below Metropolitan Activity Centres and are to be encouraged to

develop the following land uses:

• A broad mix of integrated sub regional land uses such as retail (discount

department store as well as supermarkets and specialty stores), office,

business, community, education and residential.

• Residential development (usually above ground level) and medium and

higher density housing in close proximity.

Amendment C171 Melton Planning Scheme—20 March 2017 Deep End Services

4

• Accessibility via public transport including a public transport interchange

and pedestrian and cycling networks.

• Extensive public open space.

• Approximately 35,000 square metres of conventional retail floorspace

and up to 20,000 square metres of restricted retail floor space based on a

catchment of approximately 50,000 people.

2.2 Economic and 32 The need for a new Activity Centres Strategy stems from a range of economic and

Policy context policy themes set out in the MRACS including:

• The City of Melton’s population is projected to grow from 132,000 people in 2015

to 400,000 at full development over the next 30-40 years. This unprecedented

rate of growth requires both the redevelopment and expansion of existing

centres and a network of new centres to service the growth areas.

• Surveys by Council showing residents want a higher level of service from their

activity centres, reducing the need to travel elsewhere.

• Generating new job opportunities. Melton’s activity centres are vitally important

to generate a high proportion (up to 60%) of the 140,000 new jobs needed when

the municipality reaches full development.

• A need to merge the activity centre planning undertaken by the former Growth

Areas Authority in Melton’s new areas (where the focus was on centre

hierarchies based on retail functions) with the latest metropolitan plan (‘Plan

Melbourne’) where the hierarchy of centres has been broadened with a focus on

jobs and services.

• The new hierarchy of centres under ‘Plan Melbourne’ is:

• National Employment Clusters

• Metropolitan Activity Centres

• Activity Centres

• Neighbourhood Centres

• The introduction of reformed commercial zones in Victoria in 2012. These were

designed to respond to changing market forces and provide greater flexibility

and growth opportunities by (amongst other things) broadening the range of

activities not requiring a permit, removing floorspace restrictions and allowing

limited retail uses in industrial zones. With the removal of floorspace caps, the

MRACS notes that “... the area of land to be zoned will be the principle control

on the size of the centre” 1.

• ‘Plan Melbourne’ setting higher minimum densities within growth areas of 18

dwellings per hectare. This could have implications for the size and number of

activity centres to serve the growth areas.

33 The strategic planning studies for Melton East pre-date most of the area’s

development. There has been no review of activity centres since the Melton East

Structure Plan (MESP) was released in 1997. A review of the Indicative Activity

Centre Framework Plan within the MESP reveals several proposed centres failed to

materialise as the locations were poorly placed and the low floorspace caps only

1

MRACS Background Report p.40.

Amendment C171 Melton Planning Scheme—20 March 2017 Deep End Services

5

allowed small supermarkets which could no longer be secured by developers. While

Caroline Springs is now at the size contemplated by the MESP Activity Centres

Framework, the balance of the area has a much lower floorspace provision than

proposed in the MESP.

2.3 MRACS 34 The MRACS analysis is undertaken through various stages including:

Methodology

• An analysis of existing centres including trade areas, floorspace, retail sales and

the results of a web-based survey of residents’ views about their centres.

• Trends in activity centre planning and the retail and office sectors.

• Policy developments.

• Projected population at the municipal and small-area level and retail spending

levels at the municipal level.

• Supportable retail floorspace at the municipal level at full development.

• Organising floorspace needs into centres.

• Resolving network issues.

35 The major assumptions and conclusions are reviewed below.

Population and spending

36 The MRACS takes population forecasts for the City of Melton from small area

projections prepared by .id consulting. By 2031, the municipal projections by .id

(242,000) are about higher 7% than the State Government’s forecasts (226,000)2.

The difference can be explained by different assumptions and normal variability in

forecasting over long time periods however both estimates represents an increase of

either 95,000 people or 109,000 people over the 2015 levels (133,000) – a range

which still shows significant growth and potential demand for new activity centre

floorspace.

37 In examining the detailed .id estimates, I note the East Melton area covering

Caroline Springs, Taylors Hill, Burnside Heights and Burnside will increase from

48,713 people in 2016 and peak at 52,200 people in 2021. Across this sub-region, the

largest area of growth in the next 10 years is projected by .id at Burnside, based on

the large infill estate (Modeina) now developing off Westwood Drive, beginning 1.6

km north of the Burnside centre.

Floorspace demand

38 Tables 8 and 9 of the MRACS Background Report calculate the projected retail

floorspace needs of the Melton City Council area at full development. The

assumptions are that:

• Supportable retail floorspace per capita in Melton will increase from 2.0 sqm per

person in 2012 to 2.37 sqm at full development or sometime around the year

2050.

• The total supportable retail floorspace by Melton residents is 946,800 sqm at full

development. Assuming 82% of this could, or should, be provided in Melton

2

MRACS Background Report p.31.

Amendment C171 Melton Planning Scheme—20 March 2017 Deep End Services

6

(allowing 18% escape spending) then the total to be accommodated is 774,100

sqm.

• This is an increase of +628,400 sqm of retail floorspace over and above Melton’s

existing supply of 145,700 sqm.

39 In my view, the assumptions are plausible and set a reasonable expectation on what

the city should be seeking to accommodate. These are significant requirements

resulting in approximately 15,000-18,000 sqm of new retail floorspace in the city

each year, for the next 35 years.

40 Even under the lower forecasts by the State Government which would see Melton’s

average annual growth rising to 10,000 people per annum, a net increase of 15,000-

18,000 sqm (or at least 1.5 sqm per capita) would be a minimum average annual retail

floorspace requirement for the region.

41 It is often the case in outer growth areas where new housing areas are occurring on

different growth fronts – as it is in Melton – that new retail supply often lags

demand. With a dispersed growth pattern, established centres with further capacity

to expand often take up the demands where they can efficiently service the new

areas, until such a time as the new areas have critical population thresholds to

support new centres.

Scope for New Centres

42 Table 10 of the MRACS (Background Report) seeks to allocate the 774,100 sqm of

additional retail floorspace to regional, sub-regional, neighbourhood and other

centres in the hierarchy. It allocates a proportion of floorspace to each level in the

hierarchy and calculates the number of centres needed based on an average

floorspace per centre.

43 At the sub-regional level (which generally correlates with ‘Activity Centres’ under the

‘Plan Melbourne’ centres hierarchy), the table makes the following assumptions:

• 43% of the 774,100 sqm is allocated to sub-regional centres or 332,900 sqm.

• With a sub-regional centre having a typical retail floorspace of 55,000 sqm,

Melton at full development can support a total of 6 sub-regional centres.

• With three existing sub-regional centres this creates the notional scope for 3

additional sub-regional centres.

44 A similar analysis is undertaken for regional centres (2 new) and neighbourhood

centres (25 new).

45 While I understand the calculation on new sub-regional centre requirements is a

hypothetical estimate, the assumption of an average of 55,000 sqm per sub-regional

centre (comprising 35,000 sqm of conventional retail space and 20,000 sqm of

restricted retail premises) could be an over estimate as some locations will not

deliver either or both these floorspace assumptions. In these instances, the

floorspace could be allocated to other locations that can deliver the floorspace from

stronger locations or a smaller average size should be assumed in the analysis which,

in turn, would substantiate more sub-regional centres. For example:

Amendment C171 Melton Planning Scheme—20 March 2017 Deep End Services7

• There are approximately 300 sub-regional or discount department store (DDS)-

based centres in Australia and approximately 85% of these are single-DDS

centres with an average retail floorspace of approximately 20,000 sqm. Centres

of this size will be more commonly found in new growth areas as the DDS market

has weakened and the industry is shifting away from the larger but smaller

number of, double-DDS centres which average about 47,000 sqm of retail

space.

• The assumption of 35,000 sqm of retail floorspace is higher than the average for

all sub-regional centres in Australia (28,000 sqm) but, more importantly, is not a

realistic planning tool for individual locations as DDS or sub-regional centres

tend to group around the 15,000-22,000 sqm range (for single-DDS centres) or

are 40,000+ for most double-DDS centres. An average of 35,000 sqm implies a

small double DDS-based centre however these are becoming increasingly

difficult to develop in new locations given the state of the DDS market. The

market is, in fact, now moving towards a higher number of smaller single DDS

centres.

• The Caroline Springs Town Centre (currently 22,000 sqm retail space) is typical

of a single DDS-based centre but may not generate strong enough commercial

interest from major retailers to achieve 35,000 sqm of shopping centre space

and almost certainly will not develop 20,000 sqm of restricted retail premises.

• Other ‘Activity Centre’ locations in the growth areas may also find that without a

second DDS or strong main road exposure to attract national large-format

retailers, that the 55,000 sqm floorspace allocations will not be achieved.

46 While Table 10 may be a useful tool to generate a high-level estimate of activity

centre needs, there should still be some flexibility to allow centres to move within

the hierarchy and to grow as the market considers the relative strengths and

weaknesses of emerging or established locations and the changing viability of

multiple major stores in one location.

Catchment analysis

47 The MRACS determines sub-regional or ‘Activity Centre’ locations by aggregating

small areas (at full development) to catchments of about 50,000 people and

confirming either an existing centre or assigning a new ‘Activity Centre’ to the area.

The MRACS Final Report (p.12) notes that while 50,000 people was adopted for

planning purposes this could vary between 35,000 and 70,000 people.

48 The map in Figure 1 is taken from the MRACS showing six residential catchments for

sub-regional centres. In Melton East, a single catchment area extending from

Taylors Hill to Burnside is shown with the Caroline Springs Town Centre as the only

sub-regional centre.

49 Five other catchments across Melton are shown for sub-regional centres (bringing

the total to 6) which corresponds with Table 10 which calculated a similar long-term

need in Melton.

Amendment C171 Melton Planning Scheme—20 March 2017 Deep End Services8

Figure 1—Sub

regional

catchments from

MRACS

Source: MRACS p.13

2.4 Activity 50 The expectations for ‘Activity Centres’ are set out in Sections 6.2 and 6.4 of the Final

Centre Report. It notes that each Activity Centre will be different in its offering and

expectations emphasis however each will generally contain:

• A sub-regional retail function with multiple supermarkets, a DDS and specialty

shops

• Community services

• Entertainment and recreation activities

• Commercial accommodation

• Office activities

• Extensive public open space

• Public transport interchange

51 I note that the criteria include a DDS in each centre. There is no requirement or

expectation that any centre should have multiple DDS. Clearly, this is a matter for

the market to determine.

Amendment C171 Melton Planning Scheme—20 March 2017 Deep End Services9

2.5 Caroline 52 In the case of Caroline Springs, the MRACS Background Report and Final Report

Springs findings make the following points:

• Caroline Springs is presently the nominated Activity Centre for East Melton and

has developed to provide a small sub-regional offering and a substantial non-

retail service.

• The Town Centre has about 22,000 sqm of retail floorspace and over 50,000

sqm of other commercial and community uses.

• Its share of retail spending (23%) is towards the lower end of the typical share for

sub-regional centres.

• Caroline Springs is central to its catchment which the Final report indicates will

be 50,000 people at full development (MRACS p.15) although I note the

Background Report (Appendix 6) indicates it will reach 63,000 people by 2031.

• Assuming future development at Burnside and Plumpton, the natural catchment

area is likely to contract to about 30,00-40,000 people.

• These developments are likely to limit the retail potential of the centre to the

provision which currently exists.

• Office development is likely to be one of the key areas for expansion at Caroline

Springs Town Centre.

2.6 Burnside 53 In relation to Burnside and its elevation from a Neighbourhood Centre to an Activity

findings

Centre, the MRACS says the following:

• The centre has 4.5 hectares of vacant land zoned Commercial 1 and 7 hectares

zoned Mixed Use adjoining the existing centre. (I note this reference is incorrect

since the recent rezoning of the two land parcels – swapping the Mixed Use and

Commercial 1 zones – now results in 7.8 hectares of vacant Commercial 1 zoned

land adjoining the centre and 4.1 hectares of Mixed Use zoned land).

• While presently designated a neighbourhood centre it has surrounding uses that

provide sub-regional services including (then) two hardware stores and a

growing large format retail precinct.

• The area of vacant Commercial 1 zoned land is large enough to accommodate a

DDS, supermarket and specialty shops.

• The new Commercial zones have done away with floorspace caps and the

owners do not need a permit for retail or office uses.

• Given the above, it is prudent to nominate Burnside as an Activity Centre and for

Council to influence the design to produce the best outcome for residents and

centre users.

54 Further strategic support in the MRACS is given to Burnside’s Activity Centre status

by the following comments:

• At full development, Burnside and Caroline Springs would share a catchment of

60,000-70,000 people which would be sufficient to support small sub-regional

facilities at each centre (that is, a single DDS, two full line supermarkets and

specialty stores) (MRACS p.16).

• A sub-regional retail facility at Burnside would also attract shoppers from the

nearer parts of Brimbank. It could also serve some people in the newly

Amendment C171 Melton Planning Scheme—20 March 2017 Deep End Services10

developing growth areas east of the Outer Metropolitan Ring Road, at least until

the Activity Centre at Plumpton was developed (Background Report p.57).

• Burnside could also host a more extensive bulky goods offering because of its

location on the Western Highway and accommodate specialist services for the

adjoining industrial areas (MRACS p.16).

55 The proposed Activity Centre Network is shown in Figure 2.

Amendment C171 Melton Planning Scheme—20 March 2017 Deep End Services11

Figure 2—MRACS

Final Proposed

Activity Centre

Network

Source: MRACS

56 Section 3 of my report expands on some of the strategic location and catchment

area arguments put forward in the MRACS relating to Burnside’s new Activity

Centre status.

Amendment C171 Melton Planning Scheme—20 March 2017 Deep End Services12

Burnside Activity Centre

3.1 Location

Regional setting

57 Burnside has unique location advantages that favourably position it for new retail

and other investment in the next ten years. Some are discussed in more detail in the

following sections but broadly, its regional setting is characterised by:

• Access to a large, established population base through the Melton East corridor

and the outer suburbs of Brimbank.

• Western Highway access to the West Growth Corridor Precinct Structure Plan

(PSP) areas which are in final stages of planning or formative stages of

development in the case of Rockbank and Rockbank North. The four PSPs west

of Caroline Springs and adjacent to the highway, have a long-term capacity of

87,500 people – a population much larger than the East Melton corridor today.

• An emerging large format retail, showroom and commercial area along Ballarat

Road which has seen significant growth in the last five years.

• Proximity to the vast West Industrial Node which already extends north along

Robinsons Road to Burnside with a growing employment base in the industrial

and business parks through Ravenhall.

• Exposure to a major highway with 44,000 vehicles per day, close connections to

the Western Ring Road and Western By-pass and the future development of

Westwood Drive creating a second arterial past the site.

• Its position as the closest activity centre to the new Caroline Springs railway

station.

• Limited growth and development of other major activity centres which are

constrained by location, site features or demographic changes.

Amendment C171 Melton Planning Scheme—20 March 2017 Deep End Services13

Figure 3—Regional location

Regional population growth

58 The City of Melton (2015 population 132,752) is the fourth fastest growing outer

municipality of Melbourne. Melton’s average annual population growth of 5,200

people in the last five years ranks it below Wyndham (10,920 per annum), Whittlesea

(8,537) and Casey (7,550).

59 Population projections by the State Government (Victoria in Future 2016) however

indicate that Melton will gradually increase its annual growth rate to almost 8,000

new residents per annum by 2021 and to 10,000 per annum by 2031. In 2031,

Melton’s population would reach 266,000 – approximately double the 2015

population level.

60 According to the State Government’s forecasts, Melton will surpass Whittlesea’s

average annual population increase in 2021 and exceed Casey and Wyndham’s

annual growth after 2026.

Amendment C171 Melton Planning Scheme—20 March 2017 Deep End Services14

61 Burnside is well-positioned to the existing population and future growth. The

original Melton East Strategy Plan area, (refer Figure 3) broadly defined as the

corridor between Burnside and Caroline Springs in the south up to Hillside in the

north, has developed since the mid 1990’s. Originally planned for between 60,000

and 82,000 people, the area had an estimated 2016 population of almost 70,000

people and should peak at just over 75,000 people.

62 The narrow Taylors Hill West PSP area which was annexed to East Melton and

commenced in 2012 is about 80% developed towards its expected capacity of 2,400

lots or 7,000 – 7,500 people.

63 Within the broad East Melton corridor, the MRACS defined a smaller sub-regional

centre catchment area (refer Figure 4) from Taylors Hill down to Burnside where the

population has grown from 22,528 to 48,379 in the last 10 years (refer Table 1). The

main area of infill housing is the Modeina estate at Burnside off Westwood Drive

where approximately 200 homes have been built or are under construction of the

850 lot capacity.

64 The Modeina Estate, other infill housing and higher density development around

Caroline Springs Town Centre is likely to increase the population of the East Melton

sub-regional catchment to 52,700 in 2021 and about 56,260 at full capacity (refer

Table 1).

65 South east of Burnside, the new suburb of Derrimut and areas of Deer Park south of

Ballarat Rd – both in the City of Brimbank - have more than doubled in the last 10

years to about 22,000 people in 2016 (refer Table 1). Derrimut is now almost fully

developed although its population will continue to grow as young families increase

in size.

66 The vast West Growth Corridor Plan area has two approved PSPs and two in

progress close to Melton East. There are four PSPs (Mt Atkinson, Kororoit,

Rockbank North and Rockbank) abutting the Western Highway, generally within 5-

10 km of Burnside with a capacity of 87,500 people. Mirvac is developing its largest

housing estate in Australia at Rockbank North where several hundred homes are

either built or under construction. The Mirvac estate has a capacity of 7,000 lots (or

20,000 people) which is most of the North Rockbank PSP capacity.

67 In the Rockbank PSP south of Western Highway, major estates known as Thornhill

Park and Bridgefield are now selling lots with the first houses yet to be built.

68 As the Melton East area approaches full development, the West Corridor PSPs will

escalate their land release and population growth. It will be at least five years before

the first supermarket is developed in these areas and many more before major

discount department stores or similar retailers can be supported. Until then, centres

such as Burnside which is a short drive along the highway can serve a valuable role in

providing higher level retailing to the new areas.

69 The current and future population levels of the three established urban areas defined

around Burnside and the nearest PSPs to the west are shown in Table 1.

Amendment C171 Melton Planning Scheme—20 March 2017 Deep End Services15

Table 1—Population Population

growth 2006 2011 2016 2021 Capacity

Established areas

Melton East* 22,528 40,651 48,379 52,696 56,260

Derrimut-Deer Park 9,232 18,187 22,037 24,537 25,000

Brimbank Central 23,883 27,391 29,472 31,222 31,500

Total Established areas 55,643 86,229 99,888 108,455 112,760

PSP areas

Rockbank - 1,081 1,032 2,370 22,200

Rockbank North - 36 239 5,725 20,400

Mt Atkinson - - - - 19,000

Kororoit - part - 100 100 342 22,430

Taylors Hill West - part - 0 4,850 5,880 5,880

Total PSP areas 0 1,217 6,221 14,317 89,910

Total 55,643 87,446 106,109 122,772 202,670

* MR&ACS-defined area which includes part Taylors Hill West and part Kororoit

Source: ABS, PSPs, id., UDP

Figure 4—Population areas

Amendment C171 Melton Planning Scheme—20 March 2017 Deep End Services16

Regional roads connections & traffic volumes

70 Burnside has excellent access and exposure to an evolving road and rail network in

the outer west.

71 The vacant Commercial 1 zoned land has a 400 metre frontage to Ballarat Road and

200 metres to Westwood Drive. The centre is close to the Western Freeway (1.5 km)

and Western Ring Road (3.8 km) interchanges. These are important linkages which

bring significant volumes of through and passing traffic to the area and are

important factors for retailers considering the potential of the site.

Figure 5—Regional road connections

72 The high visibility and main road attributes are like some of the early and most

successful discount department store-based centres in Melbourne and Geelong -

such as the Coles and Kmart centres at East Burwood, Campbellfield and Belmont.

These have proven to be resilient centres over almost 50 years despite substantial

changes in competition, technology and population shifts.

Amendment C171 Melton Planning Scheme—20 March 2017 Deep End Services17

73 Data from Vic Roads (refer Figure 6) shows average 24-hour two-way traffic volumes

on Ballarat Road (Western Highway) passing the Burnside site was 44,000 vehicles

per day (vpd) in 2015.

74 These volumes contrast with about 30,000 vpd on Station Road passing Brimbank

Central and a similar volume (30,000 vpd) on Melton Highway near Watergardens

Town Centre.

75 Westwood Drive is planned as a future north-south arterial road through Melton

East, ultimately extending between the Calder Highway in the north and Princes

Freeway at Williams Landing in the south (refer Figure 5). When complete, it will

form a continuous 18 km 4-lane arterial and act as an alternative north-south link to

the narrow and congested Caroline Springs Boulevard where it passes through the

Caroline Springs Town Centre. To facilitate the extension, Westwood Drive will

bridge Kororoit Creek, 2 km north of Burnside.

76 Through GTA, I understand that VicRoads have modelled the future daily traffic

flows along Western Highway and Westwood Drive at 50,00 vpd each (100,000 vpd

in total).

77 The high exposure to passing and through-traffic is a key driver in the demand

analysis and commercial interest for an expanded Burnside Centre.

78 Burnside’s location at the intersection of two major arterial roads is a unique

characteristic shared by only one other centre in the western suburbs, namely

Watergardens.

79 The future extension of Rockbank Middle Rd into the West Corridor Growth area

enhances Burnside’s east-west connections into new areas.

80 The Regional Rail Link passes 1.3 km south of Burnside with its nearest station at

Deer Park. The new Caroline Springs Station on the Melton line is just 2.3 km by

road from Burnside and 4.1 km from the Caroline Springs Town Centre. Burnside is

the closest activity centre to this station.

81 Burnside will be well served by local and regional bus routes with connections to

Caroline Springs and Deer Park stations.

Amendment C171 Melton Planning Scheme—20 March 2017 Deep End Services18

Figure 6—Traffic

volumes 2015

(vehicles per day)

Source: Vic Roads

Surrounding employment growth

82 The area south of Ballarat Road, extending west to the current urban boundary of

Caroline Springs and south between the Western Freeway and Robinson Road, is

known as the Ravenhall Employment Precinct (REP) (refer Figure 7).

83 The existing 328 hectares of Commercial 2 and Industrial 3 zoned land through the

REP forms the northern end of the much larger West Industrial Node. The area

south of Burnside is characterised by retail and commercial display uses, small

office-warehouse and industrial premises and Business Parks with conventional

office buildings. Figure 7 shows land within the REP either developed or vacant,

according to the State Government’s Broadhectare Data Base in 2016.

84 In 2016, approximately 106 hectares in the REP was developed and 222 hectares (or

67%) was vacant and available for development. Since 2010, the developed land

area has increased from 61 to 106 hectares suggesting the take-up of land and

employment growth has been very strong.

85 The current employment base is difficult to estimate however at the last Census

(2011) there were 1,347 people working in the REP. Based on the growth in the area

and more intensive retail and office developments at Orbis Business Park and along

Amendment C171 Melton Planning Scheme—20 March 2017 Deep End Services19

the highway, I estimate the current employment levels in the REP to be at least

2,300 people.

86 With approximately one-third of the zoned area developed, the employment level at

full capacity in 10-15 years (at current rates of land take-up) would be close to 7,300

people. The yellow shaded areas in Figure 7 are future industrial areas of some 100

hectares that will also increase the area’s employment base.

87 For Burnside, the growing number of businesses in the REP, particularly the

associated office components, will have demands for office and business supplies

and retail and professional services which could be provided in an expanded

Burnside Activity Centre. The large and growing workforce is within walking

distance or a short drive of Burnside where a range of dine-in and take-away food,

groceries and personal services can be made available in an expanded centre.

Figure 7—

Commercial and

Industrial land

available - 2016

Source: DELW&P

3.2 Burnside 88 The Burnside Activity Centre is broadly defined by the MRACS3 to include:

activity centre

• The Burnside Hub neighbourhood shopping centre on Westwood Drive.

• McDonalds and KFC on Ballarat Road and a commercial development to the rear

off Westwood Drive.

• 7.8 hectares of vacant Commercial 1 zoned land south and west of Burnside Hub

through to Ballarat Road and 4.1 hectares of vacant Mixed Use zoned land north

of Burnside Hub.

• Large-format retail developments west of the vacant land including Bunnings,

the former Masters store and a new showroom and office development west of

Masters known as West Springs Centre.

3

MRACS Background & Analysis Discussion report, Appendix p.20

Amendment C171 Melton Planning Scheme—20 March 2017 Deep End Services20

89 These uses and areas are shown in Figure 8. I would argue that the land use and

employment functions of an ‘Activity Centre’, as they are defined under the centres

hierarchy in Plan Melbourne, are also evident in other adjoining areas of Burnside

including:

• Medium density housing to the north comprising the Burnside Retirement Village

and Westwood Aged Care Service.

• Commercial uses on the south side of Ballarat Road, generally east of Bunnings

through to Westwood Drive. This area is part of the REP and has a mix of retail,

large format retail, trade supplies, fuel and light industrial uses.

• A large format retail development on Ballarat Road, west of Bunnings. Built in

2013, the 14,387 sqm complex with 8 occupied tenancies includes national

retailers Officeworks, Petbarn, Autobarn, Furniture Galore and Fantastic

Furniture. Two leisure tenancies include a children’s play centre and café and

trampoline park.

• Further west of the large format retail strip extending to Christies Road is a

cluster of new automotive dealerships including Chrysler/Jeep/Dodge, Hyundai,

Kia, Nissan, Honda and Mazda.

Figure 8—Burnside Activity Centre – February 2017

Source: Nearmap, MRACS, Deep End Services

Amendment C171 Melton Planning Scheme—20 March 2017 Deep End Services21

90 The Ballarat Road retail and commercial strip through Burnside (on the north side)

and Ravenhall (south side) has developed rapidly since 2011. In particular:

• Bunnings and Masters hardware stores were developed in 2012. The now vacant

Masters store is likely to revert to a range of large format retail tenancies further

consolidating the area as a growing destination for national retailers.

• The large format retail centre and car dealerships on the south side and the West

Springs Centre on the north side have all developed from 2013 through to mid-

2015.

3.3 Burnside Hub 91 Burnside Hub Shopping Centre was developed in 2003 as the first supermarket-

based centre in the Melton East corridor. Other than some tenancy changes (Bi-Lo

rebadging to Coles) and a recent minor extension to ALDI, the centre itself has

remained largely unchanged since opening.

92 The centre has a mid-sized Coles supermarket (2,522 sqm), free-standing ALDI store

(1,506 sqm), 17 shops and a medical centre. The total gross leasable area is

approximately 6,284 sqm (refer Table 2).

Table 2—Burnside No. of tenants Floorspace (sqm)

Hub existing

floorspace Coles 1 2,522

ALDI 1 1,506

Specialty shops 16 1,935

Total retail 18 5,963

Medical 2 318

ATMs/Kiosks 3 3

Total centre 23 6,284

93 The centre is oriented towards Westwood Drive which currently functions as a

collector road for the Burnside housing estates. Westwood Drive terminates at the

future bridge crossing on Kororoit Creek, 2.2 km north of Burnside. The centre has

low visibility and exposure to Ballarat Road and while the specialty shop component

has been fully let and stable over many years, the centre has been constrained by its

current layout and small Coles supermarket.

3.4 Extended 94 The opportunity at Burnside, created by the favourable site attributes, regional

centre growth characteristics and the available Commercial 1 zoned land, is to develop a

large single DDS-based centre, consistent with the MRACS with the following

features:

• A centre with high convenience which is attractive to the existing catchment and

new housing areas in the West Growth Corridor.

• To re-orientate the centre away from its current perspective to Westwood Drive

towards the Western Highway with strong links to the large format retail areas

west of the vacant land.

• To secure a major DDS tenant such as Kmart whose nearest stores are at Keilor

Downs, Melton and Footscray.

• To increase the size and number of supermarkets.

Amendment C171 Melton Planning Scheme—20 March 2017 Deep End Services22

• To create a strong north-south link through to the Mixed Use zoned land and

retirement village to the north.

• To attract a range of non-retail, commercial and leisure / entertainment tenants

and uses which complement the retail function and increase the mixed-use

elements of the centre.

• Provide a relevant centre for the businesses and large and growing employment

base through Ravenhall.

3.5 Extended 95 Figure 9 shows the Caroline Springs (East Melton) sub regional catchment

MRACS reproduced from the MRACS, limited, as it was, to the residential areas within the

Catchment area City of Melton. This area is outlined in red. I also show two shaded areas being a

reduced core Caroline Springs catchment (red) and Burnside’s core local catchment

(shaded blue) which occupies part of the Melton East area and penetrates other

adjacent areas labelled Derrimut – Deer Park in Brimbank (outlined in blue). The

connections to the employment land and PSP areas are also shown.

96 These areas are not the entire catchments of each centre as major road connections

will extend Burnside’s catchment into other areas of East Melton (north of Kororoit

Creek) and further east into Brimbank (Cairnlea).

97 Table 3 shows the relative current and future population of both shaded areas

around each centre. Caroline Springs has a slightly larger population of 37,890 in

2016 compared to 32,530 people around Burnside.

98 By 2021, Burnside’s population is projected to reach 37,240 which meets the 35,000

threshold for a sub-regional centre set out in the MRACS.

99 Both centres will experience growth in their catchments – Caroline Springs from

parts of Taylors Hill West, the eastern part of the Kororoit Creek PSP and higher

density housing around the Town Centre. Burnside will grow with the Dennis Family

housing estate at Modeina (Burnside) and new and larger families growing into the

new areas of Derrimut.

Table 3— Core Adjusted catchments 2016 2021 Capacity

catchment area

populations Caroline Springs 37,890 39,990 43,460

Burnside 32,530 37,240 37,800

Total 70,420 77,230 81,260

100 Figure 9 also shows an almost straight road distance of 7.5 km from Burnside to a

point on the Western Highway where the new estates are being sold either side at

Rockbank and Rockbank North. The same relative distances from this point are

9.4km to Caroline Springs Town Centre (including via the slower Caroline Springs

Boulevard route) or 9.6 km back to Woodgrove Shopping Centre at Melton.

Amendment C171 Melton Planning Scheme—20 March 2017 Deep End Services23

Figure 9—Adjusted MRACS catchments

Amendment C171 Melton Planning Scheme—20 March 2017 Deep End Services24

3.6 The case for a 101 A DDS such as Kmart, Target or Big W is the major retail tenancy commitment that

DDS at Burnside will facilitate Burnside’s elevation to a sub-regional shopping centre.

102 Over the last five years there has been a considerable shift in the DDS market which

has had general implications for shopping centre sites looking to secure DDS

commitments. The market participants are shaping the Brimbank and East Melton

activity centres in the following ways:

• Kmart, who has been the leading DDS operator for the last 7 years with

remodelled stores, reduced merchandise lines, a new pricing model and better

marketing, closed an underperforming store at Brimbank Central in 2012.

Brimbank was a case of an established centre whose catchment, while relatively

large, was insufficient to support both the Wesfarmers’ owned Kmart and Target

brands.

• Target and Big W now have significantly reduced new store programs

considering their lower trading levels.

• Caroline Springs Square added Target to its centre in a Stage2 expansion in

2009 raising the centre to about 22,000 sqm (retail GLA). I understand Lend

Lease has plans to increase the centre to 36,000 sqm with a second DDS. In the

almost five years which have elapsed since the previous Amendment C112 Panel

Report into Burnside’s then proposed expansion, it has become evident to me

that Target is an underperforming store at Caroline Springs and Kmart and Big W

have little or no interest in pursuing a new store at the centre.

103 While the DDS operators have formed their own view about Caroline Springs, in my

opinion it has some inherent location and design weaknesses that constrain it from

achieving its desired status as a double DDS-based centre in the short-medium term.

These include:

• Its central location to Caroline Springs is desirable for a neighbourhood or large

community-sized centre however it does not command a large enough regional

catchment to support multiple large retail stores.

• The internal location 3km inboard of Ballarat Road is too far to draw people into

the site off the external main road network.

• Caroline Springs Boulevard is designed and functions as a 4-lane collector road,

not a major arterial carrying through traffic which many of the large sub-regional

centres require to access wider catchments.

• The Boulevard’s low traffic function and the lack of a strong east-west connector

road reinforce its localised catchment.

• The schools and community facilities are desirable close to the centre but create

traffic congestion in peak periods limiting the Boulevard’s carrying capacity.

104 Figure 10 shows a large functional region around Caroline Springs and Brimbank

Central with over 100,000 people and just 2 DDS - both Target. Outside this area,

the nearest DDS are a third Target store and Big W at Watergardens Town Centre

and Big W at Sunshine.

Amendment C171 Melton Planning Scheme—20 March 2017 Deep End Services25

105 Kmart has just one store in the outer west at Keilor Downs. Its next nearest stores

are well beyond the Burnside – Caroline Springs catchment at Melton, North Altona

and Footscray.

106 DDS rates of provision (population per store) vary widely across Melbourne. While

metropolitan-wide rates pf provision are in the order of one store per 45,000-50,000

people, rates in outer areas are much higher (that is, lower populations per store)

where there are more opportunities for large-format stores and where household

characteristics and spending patterns are more inclined to DDS shopping. Figure 10

shows notional DDS catchments around groups of centres in the outer west.

107 Although boundaries between or around groups of centres are subject to

interpretation, it is evident to me that:

• The discrete outer areas of Melton and Point Cook have one DDS per 30,000

people on current population levels. Point Cook has all three DDS brands in

close proximity.

• The balance of Wyndham has three DDS and one under construction (Kmart)

which is one per 38,500 people. A potential DDS commitment at Wyndham

Vale could drop the rate of provision to one per 34,000 by 2018.

• Sydenham – Keilor has three DDS (all brands) with one per 32,830 people.

• An area covering Caroline Springs Square, Brimbank Central and Burnside with

107,000 people has just two Target stores – or one DDS per 53,500 people.

• Even if the Sydenham - East Keilor and Caroline Springs – Brimbank catchments

were combined, the effective rate of provision is still lower than the other areas

at one per 41,100 people.

• In the Sydenham-Keilor-Brimbank-Melton East area, not only is the rate of

provision low but three of the five DDS are Target stores which is arguably the

worst performing DDS brand in the market.

• Importantly, across all the centres in the outer west, the only locations with 2 or

more DDS are the strong-performing centrally located activity centres on major

arterials roads including Watergardens, Pacific Werribee and Woodgrove.

108 Caroline Springs Square which has sought to attract a second DDS would be one of

only four centres in the outer west with 2 DDS. Its embedded location and local

road connections make it a poor comparison against the much stronger and larger

double DDS centres in the region that it seeks to emulate.

Amendment C171 Melton Planning Scheme—20 March 2017 Deep End Services26

Figure 10—DDS provision outer west

Source: Deep End Services

3.7 Burnside 109 On the available information and my inspection of the area, Burnside can meet the

meeting the role and expectations of an Activity Centre, as set out in the MRACS (p.12). It can

expectations for provide a broad range of jobs and services to a substantial catchment comprising a

Activity Centres suburb or several suburbs and can generate a large number of trips for retail,

entertainment, community and business purposes.

110 As the NRACS indicates, not all Activity Centres are alike. Some, like Caroline

Springs, have an embedded residential setting and a high quality, master-planned

built environment with well-arranged retail, community, office and other uses.

Other planned Activity Centres at Plumpton, Rockbank and North Rockbank will

probably develop in a similar way.

Amendment C171 Melton Planning Scheme—20 March 2017 Deep End Services27

111 Burnside on the other hand, is emerging from a disparate group of uses including a

small neighbourhood centre, a retirement village, restricted retail premises and

other commercial and light industrial uses along a major arterial road. These uses

can now be integrated and linked via the large areas of Commercial 1 and Mixed Use

zoned land. Burnside will have a harder physical appearance but will nonetheless be

a strong contributor to jobs and services on the Melton – Brimbank boundary. This

role could be similar to the future Hopkins Road Activity Centre at Mt Atkinson

which has a smaller planned population base relative to other centres but is intended

to service a significant industrial and commercial area.

112 On the specific expectations of Activity Centres, Burnside has or should contain:

• A sub-regional retail function including a DDS, multiple supermarkets and an

important cluster of restricted retail premises.

• A range of community services such as allied health and medical services.

• Entertainment and recreation activities including cafes and restaurants. The

surrounding commercial and industrial areas already have a range of leisure-

based businesses including a swimming school, indoor play centres and

trampoline park.

• Commercial offices in and around the retail centre and along Ballarat Road.

• Linkages to the Kororoit Creek walking trail and linear open space system.

• Bus services to the surrounding area and the nearest stations at Deer Park and

Caroline Springs.

113 On the important employment criteria, Burnside is now at the centre of a growing

commercial and industrial area through Ravenhall with about 2,300 jobs. This area is

just one-third developed with a strong take-up of industrial and business land. These

areas will have growing need for office support and business services, food and

restaurants, medical services and other retail businesses that can be frequented by

employees to or from work.

114 The core catchment population of Burnside will be at least 35,000 people meeting

the minimum threshold set out in the MRACS. The catchment will be effectively

much larger based on the surrounding workforce, the Ballarat Road and future

Westwood Drive arterial road intersection and the potential to reach the growing

areas on the West Growth Corridor.

115 Burnside’s retail floorspace could well start as a large single-DDS sub regional centre

of up to 25,000 sqm growing with subsequent stages to the 35,000 sqm indicative

floor area.

116 Outside the Commercial 1 zoned land, the Ballarat Road strip will become

increasingly popular for restricted retail uses as the Masters store converts to

smaller premises and other national retailers become aware of the area’s favourable

access and regional catchment.

Amendment C171 Melton Planning Scheme—20 March 2017 Deep End Services28

Activity centres hierarchy

4.1 Melton East 117 Until the release of the MRACS, activity centre planning has progressed based on

Structure Plan the 1997 Melton East Structure Plan (MESP) – now 20 years old.

Activity Centre 118 The plan recommended an activity centre network with 63,000 sqm of retail

Framework (1997)

floorspace for the (then estimated) 62,000 people - a very low provision of less than

1 sqm per capita which retained just 52% of floorspace demands in the area. This is a

very low rate as current-day expectations of floorspace provision have changed.

119 The low floorspace provision is now incompatible with Council’s community

feedback on the need for a wider range of services at centres and Council’s

expectations that activity centres make higher contributions to employment

generation.

120 Other factors which render the activity centre recommendations of the MESP

redundant are that:

• Actual population levels in the MESP area are likely to be at the top end of the

60,000 - 80,000 population range which was estimated for planning purposes.

• The West Corridor Growth Plan and the PSP areas now planned and developing

west of Burnside and Caroline Springs, were not contemplated in 1997.

• Two of the five ‘neighbourhood centres’ have not developed due to proximity to

larger centres while a third was relocated and reduced in size.

• Two of the three ‘Community Centres’ (Burnside & Taylors Hill) have been

developed while the Banchory Grove site, acquired by QIC (owners of

Watergardens), has been held for over 15 years undeveloped.

121 The Indicative Activity Centre Framework from the 1997 MESP is shown in Figure 11

with commentary on the various locations.

Amendment C171 Melton Planning Scheme—20 March 2017 Deep End ServicesYou can also read