Digital Gold: Bitcoin Vs. bitcoin - Webflow

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Digital Gold: Bitcoin Vs. bitcoin

To the memory of Darrin Joss, a well-respected CME pit trader who also went on to master the

art of market making through electronic execution and algorithmic trading strategies.

Darrin was my mentor and taught me the foundation for nearly everything I have learned in

the futures markets.

Written by John Divine Johndivine11@gmail.com

Contents 1. Digital Gold: Bitcoin Vs. bitcoin 2. Institutional Investors are Coming for bitcoin 3. The Importance of Liquidity: Institutional Participation in bitcoin Futures Markets

Chapter 1. Digital Gold: Bitcoin Vs. bitcoin

Bitcoin Vs. bitcoin Bitcoin, with a capital B is the Bitcoin Blockchain network that contains a distributed ledger of all past, present and future transactions across the network. bitcoin, with a lower-case “b” is the cryptocurrency of the Bitcoin Blockchain that can be transacted across the network. We will proceed with a high-level overview of the Bitcoin Blockchain, miners who validate transactions across the network, and how bitcoin, the cryptocurrency, is created or “mined” into existence. The domain for bitcoin.org was registered on the 18th of August 2008. Shortly thereafter, on the 31st of October 2008, a whitepaper surfaced that was written by an author named “Satoshi Nakamoto” titled Bitcoin: A Peer-to-Peer Electronic Cash System. The paper went into detail on the fundamentals of structuring such a system and focused on “trustless” transactions that skipped a middleman for validation, such as a bank; instead, relying upon a decentralized network of computers (miners) for transaction validation and record keeping. Blockchain The goal of a blockchain is to record and distribute unedited packets of digital information across a network to complete a transaction. Individual “blocks” of data transacted across the network are stored in a public (or private) database known as the “chain.” Distributed ledger The term distributed ledger, regarding Bitcoin, is the concept that each computer connected to the Bitcoin Blockchain has a copy of the past transaction history; including every block of data that was ever processed, in chronological order, since inception. As each computer in the network has a copy of the ledger (chain of individual blocks that contain transactional data) the concept is known as a “distributed” ledger. If a malicious actor was to attempt fraud on the blockchain, the hacker would have to alter not just one copy of the Bitcoin Blockchain transaction history (ledger), but every single copy of the distributed ledger that is spread across millions of copies throughout the network. A prominent independent researcher who goes by the name Hasu has elegantly stated that: “Bitcoin’s ledger state should answer the question of ‘who owns what, when?’”

Blocks

If blocks are digital data, what do they represent? What do they contain?

o Blocks store transaction data such as date, time, where, counterparty and quantity. For

example: Party A is sending 30 bitcoin to Party B on August 31st 2019 at 07:59:27 UTC from

wallet address x to wallet address y.

o Blocks contain information on the counterparties in a series of transactions, “from party A to

party B.” Identification of counterparties relies on a “digital signature” of authentication rather

than personal information such as a first and last name for both counterparties.

o Each block in turn self identifies, which distinguishes each block from another by using a unique

code called a “hash.” The unique block identifiers known as a hash are established through

algorithmic processes of “mining” a block.

o Mining blocks is essentially acting as an accountant, or auditor, in validating that the block does

not contain any transactions that are engaging in a “double spending” scenario and that unique

transactions are not being duplicated or reversed.

For the Bitcoin Blockchain, a “block header”, which is part of the digital information stored in each block

on the chain, contains the following information for miners to review and act upon.

o Block version number (unique identifier)

o Timestamp

o Previous block hash

o Nonce

o Target Hash (the hash of the next block)

For a new block to be mined and added to the Bitcoin Blockchain:

1. A transaction must take place. Blocks can store up to 1 MB of data on the Bitcoin Blockchain, so

each block is made up of many different unique transactions.

2. All the transactions in the block must be verified and audited.

3. All the transactions in a block must be securely stored.

4. The next block of data added to the chain must receive the hash of the prior block added to the

blockchain to remain in chronological order, which avoids the “double spend” problem.

5. The final step is a miners ability to generate the “Target Hash” which represents the unique

hash code of the next block to be mined, by decoding the contents of the prior blocks

“block header” which includes the “target hash” for the next block.

Height

One of the data points tracked in each block is known as “height.” Since each block in the Bitcoin

Blockchain is ordered chronologically, “height” is the variable used to distinguish a blocks place in the

blockchain. Each new block that is mined is added to the end of the chain.Mining

Miners are in the business of validating transactions within a block by auditing the 1 MB of data in each

block, generating the target hash of the next block, and then adding that block to the blockchain in

chronological order. The catch with mining is that there are other miners out there seeking to validate

blocks, thus there is a competition to be the first miner to fulfil acceptable “proof of work” in generating

a unique “target hash” for the next block in the chain.

64-digit hexadecimal “Hash” and Proof of Work

As discussed, each block that is added to the blockchain has a unique chronologically valid

“block number.” Each block also has a hash, for bitcoin the hash is a 64-digit hexadecimal beginning with

a string of 0’s and a target hash for the next block.

Miners deploy powerful computers to guess the value of the target hash of the next block of transaction

data to be added to the blockchain. Solving for the target hash demonstrates proof of work.

0000000000000000044fer907ab1049c84e27b5829250eef968ac35d4ef5c97e

The blocks are “hashed”, in other words, “encoded” into a hexadecimal and the degree of difficulty in

solving for the hash is dynamic. For Bitcoin Blockchain, the target hash is a 256-bit number and requires

the miner to solve for a hash that is less than or equal to the target hash to mine the proceeding block.

The difficulty level of decoding a target hash is increased periodically to set the level of mined blocks at

10-minute intervals – every 10 minutes, a new block of transaction data is added to the Bitcoin

Blockchain. As the computing power on the Bitcoin Blockchain increases, the difficulty rate in solving for

the target hash will increase as to keep the block production at a constant rate of 10 minutes.

Miners Reward - bitoin

On January 3rd, 2009, the Bitcoin Blockchain became operational with Satoshi Nakamoto mining the first

block on the chain, known as the Genesis Block (block # 0). At that time, 50 bitcoin were minted and

distributed by the network to miners as compensation for providing the computer power necessary to

validate the transaction and manage the blockchain network.

Miners are rewarded in bitcoin cryptocurrency when they have successfully mined the newest block in

the Bitcoin Blockchain.

This is how new bitcoin are minted into existence – through the process of mining.

Miners have several costs they must cover to maintain operations:

1. Electricity (bitcoin mining is energy intensive – estimates are 61.76 terawatt-hours per year)

2. Payroll & Rent

3. Equipment & Maintenance

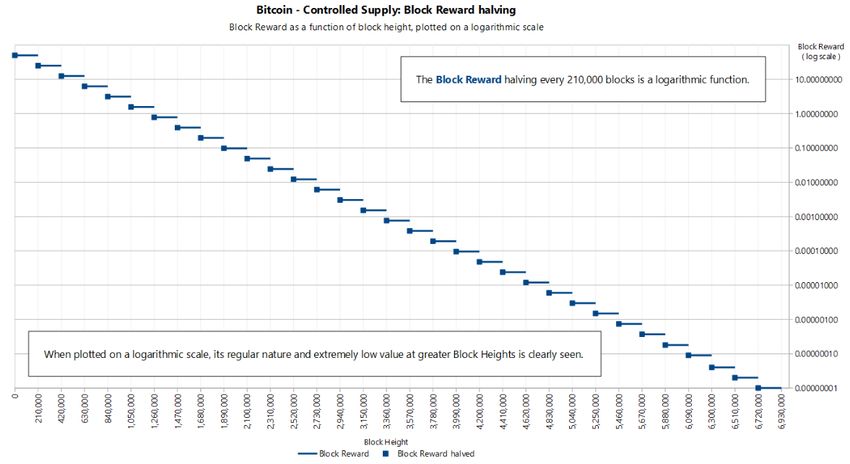

4. Legal / regulatory complianceMiners can sell their bitcoin reward into the spot market either through a designated digital asset exchange, or through a peer to peer transaction in exchange for the fiat currency where they do business (Euros, Dollars, Yuan, Yen…) in order to cover their operating expenses. Thus, bitcoin can be quoted against numerous fiat currencies, given that there is a seller of bitcoin who will accept a designated fiat currency for transfer and there is a buyer of bitcoin willing to pay in fiat currency. For example: BTC/USD BTC/EUR BTC/JPY BTC/GBP BTC/AUD BTC/CAD BTC/ZAR BTC/MEX BTC/CNY Emerging Market Pairs An elegant goal of bitcoin is to provide safe haven for traditional fiat holders (wage earners, pensioners and savers) to exchange traditional fiat into bitcoin to protect from hyperinflation of a currency, that will decay the purchasing power of wages and savings over time. (Think Venezualian Bolivar (BTC/VES) or South African Rand (BTC/ZAR)). Finite Supply Similar to gold, bitcoin has, by design, a finite supply of 21 million bitcoin (outlined in the Bitcoin whitepaper). To accomplish this, the network was deisgned to limit miner rewards of bitcoin per mined block in what is known as a “halving” event that takes place roughly every four years. Halving Back in 2009, when Satoshi Nakomoto mined the first Bitcoin block, the mining reward was set at 50 bitcoin. In 2012, the network experienced a “Halving” event, after 210,000 blocks had been mined since the first “Gensis” block (block # 0). The 2012 halving event lowered the mining reward from 50 to 25 bitcoin per mined block. In 2016 that reward was halved again from 25 bitcoin per mined block to 12.5.

2020 Bitcoin Halving Event On May 11th, 2020 the Bitcoin Blockchain network expeirenced another halving event, as 210,000 blocks had been mined since the prior halving event in 2016. This time, the halving event saw the miner reward cut in half from 12.5 to 6.25 bitcoin per mined block. (Source: bitcoin wiki) The Bitcoin Blockchain network will experience “halving” events roughly every four years until the miner reward reaches zero, at which point the network will be sustained through network fees alone. The last bitcoin reward distribution will not happen until the year 2140.

Understanding Relative Value in Foreign Exchange

Traditional currency markets consist of fiat currency that is distributed to a society of a country through

a central bank (often through debt markets) in exchange for products and services. Each actively traded

fiat currency around the world has a relative value to one another.

For example, in the United States, the Federal Reserve, which is the central bank that controls the

currency in circulation for the United States and that is accepted as legal money by the US Federal

Government is known as the U.S. Dollar (Federal Reserve Note). The U.S. dollar has a relative value to all

other fiat currency in the world such as the European Union’s Euro, the Mexican Peso, The Canadian

Dollar, the British Pound, the Swiss Franc…. etc.

The relative value of a currency is designated as a fiat pair.

EUR/USD

USD/GBP

EUR/GBP

EUR/CAD

GBP/CAD

USD/CAD

As bitcoin is both a store of value and used as a method of payment between willing buyers and sellers,

it too can have a relative value to traditional fiat currencies.

This is how most investors come to know bitcoin – not through mining bitcoin, rather through buying

bitcoin with a local fiat currency such as the U.S. dollar. Thus, there is a relative value, or exchange rate,

between bitcoin and U.S. Dollars.

BTC/USD

“How many US dollars are demanded by the market to buy 1 bitcoin?”

Pricing bitcoin Vs. US Dollars

Lets study the value of EUR/USD (European Union Euros against U.S. Dollars):

o The fiat pair tells a market participant how many U.S. dollars must be exchanged for 1 Euro

o At the time of this writing, 1 Euro = $1.08 USD.

o EUR/USD = $1.08

Now ask yourself the question – how many U.S. dollars must I exchange for one bitcoin?

This question creates the relative value cryptocurrency pair of BTC/USD.Below is a graphical representation of the relative value between bitcoin and the U.S. Dollar since

2015 on the highly liquid Coinbase exchange. The price for 1 bitcoin is currently $9,654.19.

Ounces of gold also have a relative value to the U.S. Dollar, with gold futures contract (physically settled)

currently priced at $1,757.50 per ounce.Inflationary Hedge With both gold and bitcoin sharing the quality of finite supply, both viewed as a store of value, and both having a market consisting of participants willing to exchange gold or bitcoin for goods and services as a medium of exchange, it is now thought that bitcoin, like gold, will maintain its value or rise in value, relative to fiat currencies that experience inflation. In the current global economy (circa 2020) central banks around the world are printing fiat currency to prop up government and corporate debt markets, add liquidity to financial assets, and provide access to dollars for lenders to disperse throughout the economy as new debt either through mortgage, credit card, auto sales, land purchases, equipment purchase… etc. With new fiat currency being minted, and no new real goods or services being produced, the amount of dollars in circulation outpaces production, or GDP, and the value of hard assets are likely to rise relative to fiat currency – as more fiat currency is now available to purchase the same amount of hard assets (there is a finite amount of gold and bitcoin in the world). Bitcoin is now being considered a form of digital gold, where its value, relative to the dollar, may increase in times of central bank stimulus (“quantitative easing”) in the same manner that ounces of gold are expected to rise in value relative to U.S. dollars or other fiat currencies. This idea will be explored in Chapter 2, which focuses on traditional financial markets and traditional money managers newfound appetite for investing in bitcoin. Many prominent financial market professionals are now subscribing to the idea of bitcoin being an inflationary hedge, while blockchain as a network concept may be thought of as the future of processing transactions, even in traditional fiat currency. Paul Tudor Jones, a vocal and widely popular hedge fund manager that famously called the gold price spike in the 1970s era of stagflation and the 1987 stock market crash said publicly in May 2020 of bitcoin, “If you take cash, on the other hand, and you think about it from a purchasing power standpoint, if you own cash in the world today, you know your central bank has an avowed goal of depreciating its value 2% per year,” Jones said. “So you have, in essence, a wasting asset in your hands (U.S. Dollars).” Many people, especially of older generations, listen to PTJ and take his advice seriously. Aside from the general public, hedge fund managers respect and often seek to imitate the strategies of PTJ. The public proclamation of bitcoin from Mr. Jones will one day be marked in the history books of digital assets as a notable catalyst for broader adoption from traditional financial managers.

Chapter 2. Institutional Investors are Coming for bitcoin

Portfolio Diversification with Gold & bitcoin Gold has long been a staple in the investment portfolio diversification pitch from traditional financial managers as a hedge against fiat currency inflation. As bitcoin emerges into mainstream portfolio diversification literature and institutional fund managers begin to allocate serious capital toward the asset, the looming question of risk management hangs in the balance – how will these institutional investors manage risk around bitcoin investments as they do with other traditional asset classes? Gold is a staple in many professionally managed funds where the fund managers can rely on the deeply liquid gold markets to move in and out of large positions as needed, while also having the ability to hedge those large positions through highly liquid futures and options markets, protecting investors during times of extreme price volatility or uncertainty. For bitcoin as a financial asset, the next logical step forward will be mass adoption from institutional investors, followed by broad retail adoption to the point where financial advisors begin suggesting to mom and pop that diversification into digital assets such as bitcoin is a positive financial decision. Financial assets naturally inherit price risk for investors and practical users alike. For institutional investors and sophisticated traders, managing risk is of top priority. Price volatility presents opportunity when the proper tools for risk management are available to market participants. It is significant to note that the peak speculation levels of bitcoin and other digital assets that were observed in late 2017 aligned with the CME bitcoin futures contract launch on December 17, 2017, and the ability for professional capital to either hedge bitcoin long positions or sell the market by taking a short position through the world’s largest derivatives marketplace. As federally regulated bitcoin futures markets continue to mature and develop, institutional capital will be much more comfortable establishing large positions in the bitcoin spot market when risk management procedures through derivatives like futures and options can be well defined through an execution protocol. December 17th, 2017

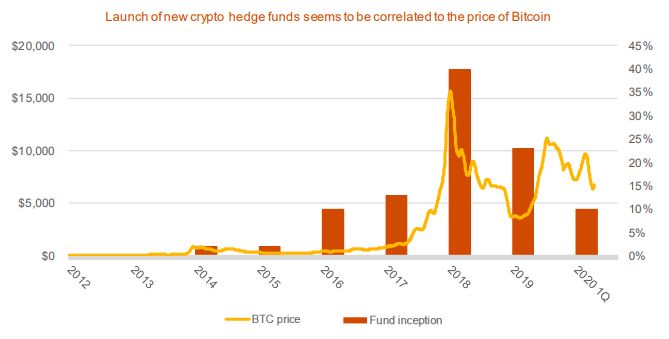

The Emergence Crypto Hedge Funds In May of 2020 Price Waterhouse Cooper (PWC) and Elwood Asset Management put out a report covering the emerging crypto hedge fund industry that has been developing alongside the expansion of user adoption, and price, of the cryptocurrency markets. https://www.pwc.com/gx/en/financial-services/pdf/pwc-elwood-annual-crypto-hedge-fund-report-may-2020.pdf Below we can examine the number of funds that have come into existence since 2012 relative to the price of BTC/USD. total assets under management for crypto focused hedge funds are also rising, with total AUM at $2 billion toward the end of 2019, up from roughly $1 billion at the end of 2018. The average size of a crypto focused hedge fund rose to $44 million at the end of 2019 from $21.9 million a year prior. As crypto hedge funds emerge and become my sophisticated in their approach to asset management, the market has also seen an increase in the use of derivative products such as options and futures, to either leverage portfolio holdings or incorporate traditional risk management strategies.

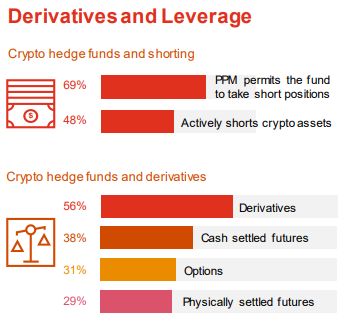

PWC and Elwood Asset Management break down their findings on derivatives use by stating: “Derivatives can either be used as hedging or alpha generating instruments…This means that crypto funds are more easily able to offer complex investment strategies such as market-neutral, as they have a more advanced toolkit at their disposal. It also means that we are seeing a closer correlation between investment strategies at crypto hedge funds and traditional hedge funds. Our 2019 data supports this view, as almost half of the funds short crypto (48%) and over fifty percent (56%) actively use derivatives. Looking into the options and futures markets, about one third of funds use futures (either cash or physically settled) and options. The presence of regulated futures offerings should contribute to an increase of usage of such instruments over the coming years.” Endowments University endowments ranging from Stanford, the University of Michigan and Ivy League stalwarts Harvard and Yale have been reported to have invested in bitcoin. Another report from 2018 mentions that 94% of all Universities surveyed had the ability to allocate a percentage of endowment funds into cryptocurrency markets. Jonathan Watkins, managing editor of Global Custodian and The TRADE who ran the report on 2018 endowments said: “It’s fascinating to see that despite the widely-publicized concerns around regulation, custody and liquidity, endowments have been factoring crypto-related investments into their allocations, and very few are showing intentions of stepping away…All the talk over the past 18 months has been around when institutional investors will begin participating in cryptocurrency investments, but it turns out they had already arrived, in the form of endowment funds.” Traditional Hedge Fund Participation On May 7th, 2020, the traditional financial world was rocked by the admission of famed hedge fund manager Paul Tudor Jones PTJ, that he holds close to 2% of his assets in CME bitcoin futures contracts. It is estimated that PTJ has roughly $38 billion AUM with around 22 billion in the Tudor-BVI fund. Paul Tudor Jones (Tudor Investments – Tudor BVI-Global Fund) Paul Tudor Jones became a household name throughout the 70’s with his accurate calls on the price of gold rising relative to the U.S. dollar, and also in the 80’s by nailing short positions into the S&P 500 futures market prior to the crash of 1987. In a letter to investors during May 2020, PTJ titled a piece The Great Monetary Inflation which discusses in detail his views on central bank quantitative easing in the coming decade, as was witnessed in the prior, that will lead to a period of inflation, where the price of hard assets rises relative to the U.S. dollar. Jones went on to mention that his Tudor BVI Fund is allocating a low single-digit percentage of its assets toward CME bitcoin Futures contracts. The fund is not holding physical bitcoin but is actively trading the CME bitcoin cash settled futures markets.

o “The best profit-maximizing strategy is to own the fastest horse… If I am forced to forecast, my

bet is it will be bitcoin. We are witnessing an unprecedented expansion of every form of money

unlike anything the developed world has ever seen.”

o “When I think of bitcoin, I look at it as one tiny part of a portfolio. It may end up being the best

performer of all of them, I kind of think it might be, but I am very conservative. I am going to keep

a tiny percent of my assets in it and that is it. It has not stood the test of time, for instance, the

way gold has.”

o “If you take cash, on the other hand, and you think about it from a purchasing power standpoint,

if you own cash in the world today, you know your central bank has an avowed goal of

depreciating its value 2% per year…So you have, in essence, a wasting asset in your hands.”

This has led PTJ to make a reference to gold during the 1970’s stagflation period of the US economy.

(Adjusted for inflation)James Simmons (Renaissance Capital) All through not as much of a household name as Paul Tudor Jones, James Simmons is thought by many to have started the concept of a Quantitative Hedge Fund and the idea of making investment decisions based solely on the output of a computer algorithm. Thus, for traditional investors and crypto investors alike, it is important to note that James Simmons is now able to trade CME Bitcoin Futures Contracts. In a brochure that was originally dated March 30, 2020 --- the United States regulator -- the Securities and Exchange Commission (SEC) confirmed that Renaissance Technologies’ Medallion Funds now has access to CME Bitcoin futures markets. As noted from the SEC submission: “Bitcoin Futures – The Medallion Funds are permitted to enter into bitcoin futures transactions, which Renaissance will limit to cash-settled futures contracts traded on the CME (Chicago Mercantile Exchange). The underlying commodity for these futures transactions, bitcoin, is a relatively new and highly speculative asset. Bitcoin and futures based on bitcoin are extremely volatile, and investment results may vary substantially over time. These instruments involve substantially more risk and potential for loss relative to more conventional financial instruments. Investments of this type should be considered substantially more speculative and significantly more likely to result in a total loss of capital than many other investments.” “Some of the risks associated with bitcoin are: 1. its limited history 2. the absence of any recognition of bitcoin as legal tender by any government 3. the lack of any central authority to issue or control bitcoin 4. its susceptibility to manipulation by malicious actors or botnets 5. its susceptibility to forking 6. its substantial price volatility 7. its possible correlation to the price volatility of other distributed ledger assets 8. the susceptibility of bitcoin spot exchanges to the risk of fraud, manipulation, and other malfeasance 9. the undeveloped and evolving nature of bitcoin regulation 10. the enhanced basis risk in bitcoin futures compared to other types of investment vehicles 11. the possibility of exchanges or FCMs’ imposing other requirements or limitations on bitcoin futures trading 12. increased regulatory scrutiny of participants in the crypto space. Any of these factors could materially and adversely affect the value of the Fund’s investments.”

Aside from his hedge fund notoriety, James Simmons is a famous mathematician and codebreaker that has posted incredible returns for investors. Bloomberg has published estimates of his return on investment for investors at an average return of 40% from 1988 to 2018. Renaissance provides some clarity to investors on how they can make these types of returns through SEC submissions: “Renaissance uses quantitative analysis, specifically, mathematical and statistical methods, to uncover technical indicators that drive its automated trading systems. These systems, or models, are the product of an extensive research effort by Renaissance's technical staff who hold advanced degrees in mathematics and the sciences. The Firm's quantitative analysis and trading activities are applied to mature, highly liquid, publicly traded instruments in the following asset classes: U.S. and non-U.S. equities, debt instruments, futures, forwards, and foreign exchange, as well as derivatives thereon. A computer is merely an aid in compiling and organizing information and in executing algorithms developed by human beings.” As stated above, Renaissance uses quantitative analysis, specifically, mathematical and statistical methods, to uncover technical indicators with predictive value. This analysis is used to construct proprietary computer models that use publicly available financial data to identify and implement trading decisions. The Firm uses these computational trading models to seek appreciation of assets through speculative trading in securities-related and futures-related financial instruments. Within the Medallion Funds, the Firm seeks to achieve appreciation of its assets through speculative investment and trading in a variety of both securities-related and futures-related instruments. “The prices of securities and of futures, forwards, and other derivatives are subject to unpredictable changes, which can be rapid and substantial. Such changes may result from, among other things, changing supply and demand relationships; changes in interest rates and stock-loan availability; currency fluctuations; government trade, fiscal, and economic policies; and other world events, including without limitation the outbreak of epidemics or pandemics, natural disasters, terrorist attacks, or military conflicts.”

Mike Novagratz (Galaxy Digital, former Goldman Sachs & Fortress Investment Group) Another traditional money manager that crossed the bridge into crypto markets – Mike Novograts, who also now runs a full-service digital asset bank that focuses on asset management and principal investment called Galaxy Digital. From a recent conference call to investors in May 2020, Mr. Novagratz spoke about a surge in interest from more traditional hedge funds looking at digital asset markets: “Bitcoin came out of a financial crisis, out of the 2008 financial crisis, really, because of a breakdown in trust, a trust in the financial system, and it is now coming of age in this second crisis (Covid-19), which is both a humanitarian crisis and a financial crisis.” “I’m seeing so many positive signs, from hedge fund managers that have never bought it, that were skeptical, calling me up and asking me how to buy it, and then actually buying it. The high net worth individuals, you know, putting money in funds, are starting to buy it. The coin-based and the other exchanges are seeing a big uptick in people signing up for their services again. So, it feels to me like we are going into a very, very good era for crypto; bitcoin specifically, but all the crypto.” On the same conference call, Christopher Ferraro – President of Galaxy Digital said: “In Asset Management, as we discussed previously, the fourth quarter of 2019 saw us launch our family of bitcoin Funds, an institutional solution with a blue-chip service provider roster, including custodians ICE, Bakkt and Fidelity. We anticipate a strong market demand for bitcoin. So, one more time echoing Mike’s commentary, we believe the case for bitcoin has never been stronger, with over $6 trillion stimulus alone, and likely more coming, and we believe will ultimately result in the large-scale monetization of Fed funded indebtedness. Gold has clearly responded to initial long-run inflation concerns and we believe that bitcoin, with its fixed and known supply, will be the digital gold for future generations. So, we cannot be more fundamentally aligned with the strategy and with our bitcoin fund offering, a simple, secure, low- cost way to gain direct bitcoin exposure.” Mr. Ferraro’s statements further back up the assertion that traditional financiers are beginning to look at bitcoin, and the digital asset markets more broadly, to hedge fiscal stimulus through central banks and the potential for fiat currency inflation.

JP Morgan Chase

The outspoken CEO of JP Morgan Chase, Jamie Diamon, has a long list of colorful quotes that hint at his

disdain for cryptocurrency and digital assets, as these assets directly impact the role banks play in global

markets and money management in a negative way. Afterall, digital assets represent the ability for one

to become their own bank in essence, and exchange value freely throughout the world without a third

party intermediary, such as a bank; while also being able to choose a unique store of value for savings

accounts.

Despite the open criticism toward many of the popular digital assets in existence today, including

bitcoin, JP Morgan has gone on to create their own blockchain (Quorum – built on Ethereum network,

designed to power its blockchain-based Interbank Information Network) and digital asset product (JPM

Coin – which it plans to distribute through Quorum as a form of currency used to settle interbank

transfers).

The “INN” was launched in 2017 with the intention to reduce friction between cross boarder payments,

which is one of the main characteristics of bitcoin*. The bank has publicly stated that 397 other banks

currently use JP Morgan’s Quorum network.

The JPM coin is a stable coin, which means its value is held at 1:1 relative to a fiat currency, such as the

US dollar, and is directly redeemable for fiat currency. Stable coins are the beginning of digital fiat;

the most common stable coins in the digital asset markets are:

1. USDT (US Dollar Tether)

2. USDC (U.S. Dollar Coin)

JPM Coin (from jpmorgan.com – February 14, 2019)

o 1:1 redeemable in fiat currency held by J.P. Morgan (e.g., US$)

o JPM Coin is a digital coin designed to make instantaneous payments using blockchain

technology. Exchanging value, such as money, between different parties over a blockchain

requires a digital currency, so we created the JPM Coin.

o Over time, JPM Coin will be extended to other major currencies (besides the US dollar). The

product and technology capabilities are currency agnostic.

o The JPM Coin will be issued on Quorum Blockchain and subsequently extended to other

platforms. JPM Coin will be operable on all standard Blockchain networks.

o We have always believed in the potential of blockchain technology and we are supportive of

cryptocurrencies as long as they are properly controlled and regulated. As a globally regulated

bank, we believe we have a unique opportunity to develop the capability in a responsible way

with the oversight of our regulators. Ultimately, we believe that JPM Coin can yield significant

benefits for blockchain applications by reducing clients’ counterparty and settlement risk,

decreasing capital requirements and enabling instant value transfer.JP Morgan Begins Banking Digital Asset Exchanges

2020 has shown to be an active year for the news wire regarding digital assets, JP Morgan continued to

expand involvement by extending banking services to two of the most prominent digital asset exchanges

in the industry in April 2020 – Coinbase and Gemini (Winklevoss Twins). This is a big deal, as traditional

banks have widely shunned digital asset exchanges until this point.

The bank will not process digital asset transactions but will provide dollar-based transaction and cash –

management services to the digital asset exchanges that provide an onramp for many fiat holders to

enter digital asset markets. JP Morgan will also be processing wire transfers, deposits and withdrawals

through the ACH (automated Clearing House) that is connected to the Federal Reserve.

Coinbase is registered as a money services business with the Financial Crimes Enforcement Network

(FCEN), and Gemini obtained a trust charter from New York’s Department of Financial Services back in

2015. Both exchanges are licensed money transmitters in multiple states.

Coinbase Exchange Former Chief Legal Officer Join U.S. Treasury Department

In truly stunning news that underpins the acceleration of digital asset adoption by traditional financial

institutions in 2020, Brian Brooks, the former CLO of Coinbase, was asked to join the US Treasury

Department as the Chief Operating Officer of the “Office of the Comptroller of the Currency” beginning

in April 2020. Brian was specifically tapped for the role by the current US Treasury secretary, Steven

Mnuchin.

The OCC, for short, handles many important matters relating to the flow of US dollars throughout the

economy and banking institutions.

o to ensure the safety and soundness of the national banking system

o to foster competition by allowing banks to offer new products and services

o to ensure fair and equal access to financial services to all Americans

o to enforce anti-money laundering and anti-terrorism finance laws that apply to national banks

and federally licensed branches and agencies of international banks

o to investigate misconduct committed by institution-affiliated parties of national banksChapter 3. The Importance of Liquidity: Institutional Participation in bitcoin Futures Markets

Wide Ranging Sources of Demand To this point we have focused on why demand for bitcoin is increasing, from university endowments, hedge funds and regulated exchange adoption, all the way to traditional financial institutions such as JP Morgan Chase and Fidelity Investments. With this institutional demand, there is also a surge in retail adoption, as we will look at below. Crypto Wallets Below is a chart of unique crypto wallets since 2011. Crypto wallets are used to store digital assets just like your bank account stores fiat currency. From a crypto wallet, an individual or business can send digital assets to other wallet holders around the world nearly instantaneously without a third-party intermediary. With surging interest from multiple demand points, there is a need for increased participation from statistical arbitrage market makers – traders who provide a service to the marketplace of an exchange through market liquidity (placing orders to buy and sell) that market participants can interact with. We are currently at such a unique point in time for the progression of the bitcoin market complex; the opportunity to learn about market making and discovering the trading opportunities presented from being a service provider to an exchange for a new product such a bitcoin will never be greater. Market makers are compensated through the bid-ask spread, volume and fee rebates for assuming risk in the marketplace. **** Pitch Market Making Book*****

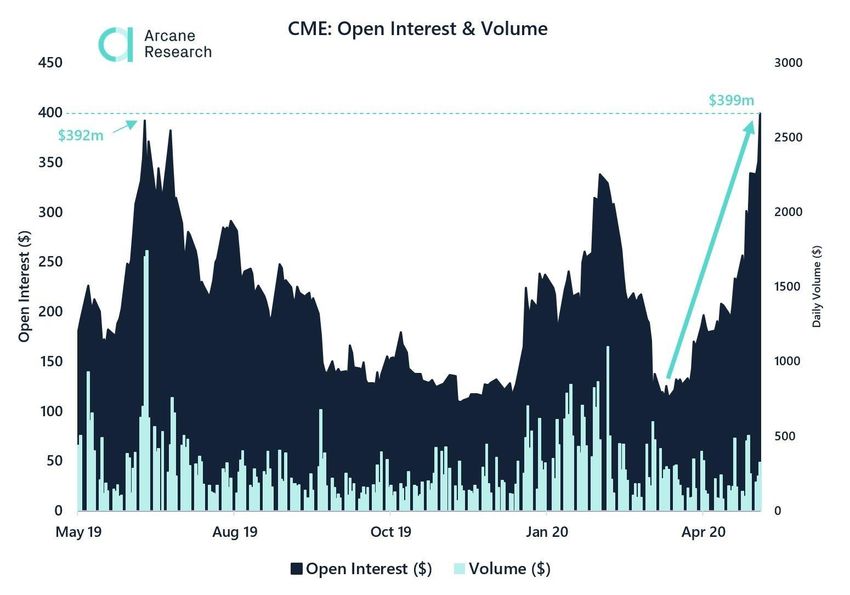

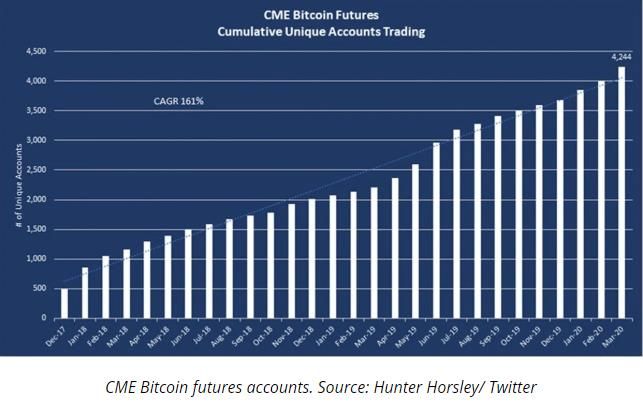

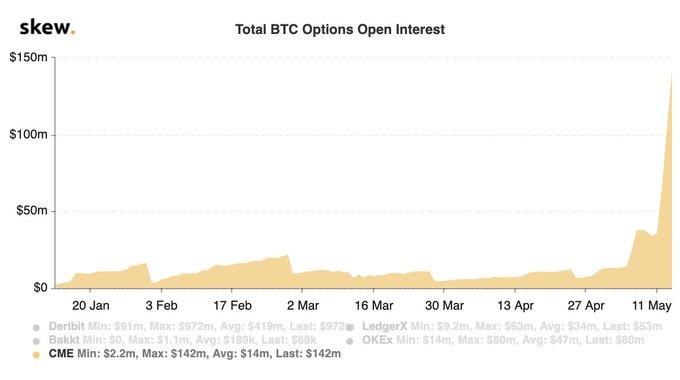

As we discovered back in Chapter 1, institutional investors are flocking to bitcoin futures markets at the Chicago Mercantile Exchange, below we can see the # of trading accounts accessing those markets. 6 Consecutive Contracts & 2 Decembers + Options Market 2020 is the year for traditional investors to enter the digital asset market through bitcoin futures contracts – The Chicago Mercantile Exchange is the largest futures market in the world and the largest money managers already have accounts open and cleared by compliance at the exchange. In January of 2020, the CME broadened the CME bitcoin futures product suite from just 2 consecutive futures contracts to 6 consecutive futures contracts + 2 December contracts (current and next year). Aside from expanding the listed futures contracts for bitcoin, the CME introduced options contracts, that notably settle against the futures contracts. For professional money managers seeking to manage risk around bitcoin or to speculate on bitcoins price, the expansion of the product suite is huge news. With new markets there is new opportunity and we will dive into statistical arbitrage trading strategies that are now available to market makers with the broadening of the listed contract months. Liquidity is the service being provided by market makers, but there must be rising volumes and new open interest in the contract for market makers to make any money; so first we will examine the drastic impact this move by the CME has had on trading activity in bitcoin futures and options markets. According to the CME, on May 14, 2020 a record number of open interest in bitcoin futures occurred, with market participants holding 10,792 contracts into daily settlement. 10 days prior, the CME set another record for the number of “Large Open Interest Holders” (LOIH) in the complex, with 66 participants meeting the qualification, implying the entrance of professionally managed capital.

The CME launched bitcoin futures markets back in December 2017, now with options markets going live

in January of 2020, it did not take long for volumes to begin an accelerated pace higher. CME bitcoin

options contracts settle against prices set in the CME bitcoin futures market.

(source: skew.com)As the open interest in CME bitcoin options rises exponentially, we also notice a steady rise in the CME

bitcoin futures contracts (each CME bitcoin futures contract is specified at 5 bitcoin per contract).

CME Bitcoin Futures Average Daily Volume (ADV)

12,000 10,710

10,000 9,427

8,000

6,000 5,534

5,053 4,820

4,109 4,369

3,577

4,000

1,854

2,000

0

Q1 2018 Q2 2018 Q3 2018 Q4 2018 Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020

A fundamental reason for lagging institutional investment in bitcoin toward the latter end of the 2010’s

was a lack of highly liquid futures and options contracts on federally regulated exchanges to properly

hedge the massive price risk exposure found within professionally managed funds. As of this writing, there

are many exchanges that have or are planning to list bitcoin futures and options contracts for traders and

investors alike, the big question will be liquidity.

Liquidity in futures markets is a measure of how many contracts are available to be bought or sold at

different prices throughout the trading session. If you can buy 5 bitcoins at $9,000 and sell 5 bitcoins at

$8,995 that is great, the real question for market maturation is what price you can buy or sell 100 bitcoins,

1,000 or 20,000? In deeply liquid markets you can transact large volumes near the best bid and best ask.

The best bid is the highest price that buyers are willing to accept in the market, while the best offer is the

lowest price sellers are willing to accept.

Highly Liquid Lightly Liquid

BTC SEP-20 BTC DEC-20

Bid Price Offer Bid Price Offer

9415 355 9550 19

9410 305 9545 2

9405 200 9540

9400 44 9535

9395 188 9530

9390 9525

103 9385 9520

52 9380 9515

227 9375 9510

288 9370 1 9505

382 9365 14 9500Liquidity can be a chicken before the egg type of question – which comes first? Do natural hedgers enter the market first or is it market makers, sophisticated traders and arbitrageurs, or simply pure speculators? All exchanges that attempt to establish options and futures markets for bitcoin and other digital assets will face not only the hardships of obtaining regulatory approval, but also the difficulty of attracting liquidity to their markets. From many exchanges, only a few will survive. The Role of Exchanges Financial and commodity market exchanges serve institutional clients, retail clients and corporate accounts that participate in transactions of corporate stock and bonds, government bonds, and commodities. The products offered by exchanges are access to corporate stock, standardized futures and options contracts, listed spreads and strips markets and exotic derivatives. The Chicago Mercantile Exchange is the largest commodities futures market in the world and meets the stringent compliance standards of the most influential hedge funds, pension funds and banks across the globe. If bitcoin is to become an investable asset for these firms, having access to CME futures markets for initiating and hedging positions is a logical progression for the wide-spread adoption of bitcoin into professionally managed investment and speculative portfolios. Chicken Before the Egg To properly serve institutional and sophisticated retail clients, exchanges need to develop market liquidity, they often tap large natural hedgers first, those who actually need to hedge price risk based on their business structure (gold producers can sell forward in the futures market, bitcoin miners can lock in forward sale prices based on expected mining reward generation…etc). The second group of market participants an exchange will seek to attract are statistical arbitrage traders at large proprietary trading firms throughout the world that understand the principles of market making. The need for liquidity from an exchange is an enormous task, and in the case of commodity futures markets (bitcoin and gold) it is very important for the exchange to structure the contract in a way that is both acceptable by the regulators (Commodities Futures Trading Commission CFTC) and that is also acceptable to natural hedgers & proprietary traders. Take the CBOE (Chicago Board of Options Exchange) for example. The CBOE, which is in competition with the CME, was the first exchange cleared by regulators to host a BTC futures contract and launched a week prior to the CME. No one talks about CBOE bitcoin futures markets as they do not exist anymore – the CBOE had to close the contract due to lack of…*liquidity*. There was not enough trading volume to justify the costs of supporting the contract.

One key difference between the CME and CBOE contract is the settlement process. The CBOE chose to settle their bitcoin contract against the price at 1 exchange, Gemini (Winklevoss). The CME on the other hand decided to settle their bitcoin futures contract against a basket of exchanges based on bitcoin volumes. The latter decision proved to be the correct strategy, as market makers and natural hedgers were concerned about potential price manipulation in the former structure, where the price of the futures contract was to settle against a single other exchange. Exchange Rebate / Incentive Programs The exchange and market makers on the exchange often share a love hate relationship. The market makers always want lower trading fees (commission paid to execute on the exchange), while the exchange always wants more fee’s (core business model). Exchanges, however, need to have a strong foundation of market makers to build out liquidity on their markets, which in turn attracts more market participants, and leads to more transactions that the exchange can take commission on. Exchanges create rebate programs for market makers – typically a contract that states “if you trade x amount of volume per month your fees will be lowered by y”. If you trade z amount of volume per month, your fees will be v.” This type of structure incentivizes market makers to participate as much as possible, with the tightest bid-ask spread as possible, as to encourage ever greater volumes from other participants. Rebates on commission provide another form of edge to statistical arbitrage market makers as they are now transacting in a marketplace for less of a cost as all the other market participants. The Service of Market Making When someone asks a retail trader – what do you do? A common reply is I apply fundamental or technical analysis to a financial asset and use a rule set to either buy or sell that asset, with stop losses for risk management and profit targets for risk/reward calculations. When someone asks a professional proprietary trader – what do you do? A common reply is: I apply statistical arbitrage strategies to financial markets to seek out opportunities of arbitrage or near arbitrage. Arbitrage is a risk-free investment or a risk-free speculative position. Proprietary traders are often market makers, seeking to profit from the bid-ask spread by being the first bid and offer in a marketplace for others to trade with. There are other variations of statistical arbitrage aside from the bid-ask spread, such as basis trading or calendar spread trading. Calendar spread markets are common derivatives of futures markets as they represent the price differential between two contract months. It is within this price differential that there are also opportunities for arbitrage, and those opportunities, to the benefit of both the trader and the exchange, provide liquidity to not only the front month futures contract (often most heavily traded) but also to deferred month contracts (that may be of more use to natural hedgers).

Market Makers: Providing Liquidity as a Service Cont. Big news for institutional investors, professional traders and algorithmic trading strategy developers hit the news wire in late 2019 when the CME confirmed the number of listed contracts for bitcoin futures would increase from 2 deferred months + 2 quarterly listings to 6 consecutive monthly contracts inclusive of the nearest two December contracts... This is huge! Opportunity is knocking for market makers and liquidity providers to serve institutional investors and large money managers who are seeking to transact “down the futures curve” for risk management or position management purposes. Deep liquidity in bitcoin futures contracts can provide a tailwind for institutional investor adoption. The above data set shows the first listings on the CME that included 6 consecutive futures contracts that became available to trade in January 2020. We can see contracts listed for Jan20, Feb20, Mar20, Apr 20, May 20, Jun 20. The addition of 4 consecutive contracts available to trade expands the practical use of bitcoin futures for hedging and speculative trading which drives demand for market makers to provide bid and offer quotes throughout the complex. We also notice December 2020 and December 2021 futures contracts, although there is no volume nor any open interest. Are the spreads too wide? Is there a way to narrow those spreads and generate some trading activity? Those are the types of questions market makers ask.

A general definition of market liquidity is the number of units or contracts that are available to be

bought or sold at different price levels for any particular asset. The price of any asset has the potential

to increase or decrease over the course of time through changes in supply – willingness and ability to

sell; and changes in demand – willingness and ability to buy. As prices for a stock, bond, commodity,

futures contract, or options contract increase or decrease, the quantity of units or contracts available to

be bought or sold at different price levels will change as well. The market is always searching for an

equilibrium between supply and demand and prices will adjust accordingly to find a level where there

are an equal number of buyers and sellers.

If demand for an asset begins to diminish at price x, while supply remains constant, the price of that

asset will fall as less and less buyers are willing to transact at x. If demand for an asset rises at price x,

while supply remains constant, price will rise, as more and more participants are willing to buy at price x,

or even higher. Conversely, if supply for an asset at price x increases, while demand at price x decreases,

the price will fall, as there are more participants willing to sell at price x, or even lower, than there are

participants willing to buy at price x. If supply at price x diminishes relative to demand, prices will move

higher, as there are more buyers than sellers at price x.

On any given day there may be high levels of liquidity in a market or low levels of liquidity in a market -

just as the market price may be rising, falling, or remaining flat. In highly liquid markets there are many

units or contracts available to be bought or sold, allowing buyers and sellers to transact large quantities

of the underlying asset at acceptable price levels, if they so choose. In lightly liquid markets there are

very few units or contracts available to be bought or sold at different prices. Lightly liquid markets are

susceptible to large price swings as participants must buy or sell at multiple price points to fill their

desired order size.

Highly Liquid Lightly Liquid

BTC SEP-20 BTC DEC-20

Bid Price Offer Bid Price Offer

9415 355 9550 19

9410 305 9545 2

9405 200 9540

9400 44 9535

9395 188 9530

9390 9525

103 9385 9520

52 9380 9515

227 9375 9510

288 9370 1 9505

382 9365 14 9500Using stocks as an example, if a trader wants to buy 1,000 shares of AAPL, one of the most liquid stocks on the market, that trader is likely able to do so quite easily, as there are often 1,000 contracts available to be purchased at a single price level (buy 1,000 shares of AAPL at $950/share). Now if a trader wants to buy 10,000 shares of stock in a less liquid market, stock XYZ for example, there may not be 10,000 shares available to be bought for stock XYZ near the current market price. If XYZ stock is currently trading at $5.00/share, to buy 10,000 shares the trader may have to buy all of the offers at $5.00/share and then buy all of the offers at $5.01/share, and $5.02/share….possibly up to $5.10/share – or even $5.50/share, to fill the entire order of buying 10,000 shares. This also demonstrates how increased demand can increase price (if the trader were trying to sell 10,000 shares in an illiquid market, the inverse would be true - what is the price for XYZ stock where there are 10,000 units available to be bought that I can sell into --- $4.90…4.75?). If a market participant wants to buy 10,000 shares of XYZ stock currently trading at $5.00/share…what price do I have to pay if I want to buy 10,000 shares? What price does a trader have to pay to buy 50,000 shares? If there are not 10,000 shares available at $5.00/share, the participant must pay a higher price, they must find the price that another market participant is willing to sell 10,000 shares, or 50,000 shares of XYZ stock at. Note: One critical value add that traders bring to the marketplace is a deepening of liquidity. With traders in the market, there are more units and contracts available to be bought or sold near the best bid and offer, or more generally, throughout the entire orderbook. To understand the value that traders can bring to the marketplace, let us turn our attention away from directional trading, where a trader is taking a position either long (buying) or short (selling) based on the traders bias in opinion on direction; and instead focus on traders that are known as relative value traders or market makers. Relative value strategies provide both buy and sell orders within a marketplace for traditional participants (actual producers and consumers of the underlying asset, portfolio managers, endowment managers, pension funds, original stake holders, etc.) to transact with. Speculative traders with an opinion on direction can also supplement this liquidity from relative value trading strategies while also benefiting from it with their own trading execution. For practical use, suppose a bitcoin miner wanted to sell bitcoin futures to protect gains from downward price movement in the bitcoin spot market. A sophisticated miner could call his broker and ask what price is available to sell bitcoin futures. With good liquidity, the broker should be able to find a good price for the miner to sell. In less liquid markets, the broker may have trouble finding a good price for the miner to sell at.

The bid/ask Spread:

Another value that traders and market makers add to a marketplace has to do with the difference

between the best bid and the best ask, otherwise known as the bid/ask spread. The best bid is the

highest price a market participant can sell at and the best offer is the lowest price a market participant

can buy from.

In tight markets, the difference between the bid and the ask is quite minimal. For bitcoin it may be that

the best offer is at $9,000 while the best bid is at $8,990 – a $10 bid/ask spread on 100 bitcoin order.

For smaller orders, such as 0.01 bitcoin, the bid/ask spread might only be 50 cents wide. Tight bid/ask

spreads are typically found in highly liquid markets that have many contracts or units available to be

bought or sold.

In wide bid/ask spread markets, the difference between the best bid and the best offer can be

significant. For a 100-lot bitcoin order, it may be that the best offer is at $9,100 while the best bid is at

$8,980 – a $120 bid/ask spread! Wide bid/ask spreads are typically found is lightly liquid markets that

have very few contracts available to be bought or sold. With this in mind, we can begin to understand

why institutional capital is more likely to transact in highly liquid markets with tight spreads.

Tight Bid/Ask Spread Wide Bid/Ask Spread

BTC SEP-20 BTC DEC-20

Bid Price Offer Bid Price Offer

9415 355 9550 19

9410 305 9545 2

9405 200 9540

9400 44 9535

9395 188 9530

9390 9525

103 9385 9520

52 9380 9515

227 9375 9510

288 9370 1 9505

382 9365 14 9500Liquidity & Volatility Exaggerated price swings (when markets go up or down by a significant rate) in highly volatile markets can also be a sign of lightly liquid markets and present greater risk to both buyers and sellers as the exaggerated price swings can be unpredictable given that there is no identifiable support or resistance from large buy and sell order quantities in throughout the orderbook. For bitcoin, think about the year 2017 when the price rose from $800/bitcoin to nearly $20,000/bitcoin! If you happened to be an early investor or buyer of bitcoin, this was great news for you. However, from a fundamental market perspective, it is important to note that liquidity on the offer (willing sellers) was minimal relative to the liquidity on the bid (willing buyers). There was significantly more demand than supply, which pushed the price to unimaginable levels at the time and created unprecedented risk and volatility for potential investors that were attempting to join the market late, and at the same time causing headaches for natural sellers such as miners or early adopters who were missing out on upside revenue each time they sold into the spot market on the way up.

Conversely, let us look at bitcoin throughout 2018, where the price went from nearly $20,000/bitcoin to just above $3,000/bitcoin. In 2018, liquidity on the bid (willing buyers) was minimal relative to the liquidity on the offer (willing sellers). There was significantly more supply than demand, which pushed the price down like a rock thrown out the window. The disparity in liquidity causes these massive price swings, which although good for directional speculation, hinder a critical goal of bitcoin – acting as a medium of exchange. Imagine if the US dollar had price swings of 10-20%/day over the course of two years – how do you know what the price of gas or bread is going to be tomorrow if your medium of exchange (US dollars) experiences exaggerated price swings.

Bitcoin Volitility Vs. Gold & Silver (Charts by TradingView) For a more acceptable comparison, look at the historical prices for gold and silver – physical mediums of exchange that are backed by traditional acceptance as currency throughout human history. The exaggerated price swings of gold and silver are insignificant compared to those experienced by bitcoin – largely due to highly liquid markets for gold and silver – the physical coins (spot market) and the futures and options contracts used to manage risk for investors of these financial assets.

You can also read