DXB Entertainments PJSC - Investor Presentation May| 2017

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

DXB Entertainments PJSC Investor Presentation May | 2017

Disclaimer

PRESENTATION AND ITS CONTENTS ARE NOT FOR RELEASE, PUBLICATION OR DISTRIBUTION, IN WHOLE OR IN PART, DIRECTLY OR

INDIRECTLY IN OR INTO ANY JURISDICTION WHERE SUCH DISTRIBUTION IS UNLAWFUL.

This presentation has been prepared and issued by DXB Entertainments PJSC (the “Company”). For the purposes of this notice, “presentation” means this

document, its contents or any part of it, any oral presentation, any question or answer session and any written or oral material discussed or distributed during

the presentation meeting.

The information set out in this presentation may be subject to updating, revision, verification and amendment and such information may change materially.

Neither the Company, any of its parent or subsidiary undertakings, the subsidiary undertakings of such parent undertakings, nor any of such person’s

respective directors, officers, employees, agents, affiliates or advisers is under an obligation to update or keep current the information contained in this

presentation to which it relates or to provide the recipient of with access to any additional information that may arise in connection with it and any opinions

expressed in this presentation are subject to change without notice. None of the Company or any of its parent or subsidiary undertakings, or the subsidiary

undertakings of such parent undertakings, and any of such person’s respective directors, officers, employees, agents, affiliates or advisers shall have any

liability whatsoever (in negligence or otherwise) for any loss whatsoever arising from any use of this presentation, or otherwise arising in connection with this

presentation.

This presentation is an advertisement for the purposes of the United Kingdom Prospectus Rules and the information contained herein are not an offer of

securities for sale in the United States nor any other jurisdiction. This presentation does not constitute or form part of, and should not be construed as, any

offer, invitation, solicitation or recommendation to purchase, sell or subscribe for any securities in any jurisdiction nor should it or any part of it form the basis of,

or be relied on in connection with, any contract or commitment whatsoever.

This presentation is for information purposes and convenient reference. It is not definitive advice, nor should it be relied upon as such. This presentation does

not purport to contain all of the information that may be required to evaluate any potential transaction and should not be relied on in connection with any such

potential transaction. Any projection, estimate, forecast or other ‘forward-looking’ statement in this presentation only illustrates hypothetical performance under

specified assumptions of events or conditions, and is not a reliable indicator of future performance.

To the extent available, the industry and market data contained in this presentation may have come from official or third party sources. Such third party

industry publications, studies and surveys generally state that the data contained therein have been obtained from sources believed to be reliable, but that

there is no guarantee of the accuracy or completeness of such data. While the Company believes that each of these publications, studies and surveys has

been prepared by a reputable source, the Company has not independently verified the data contained therein. In addition, certain of the industry and market

data contained in this presentation come from the Company's own internal research and estimates based on the knowledge and experience of the Company's

management in the market in which the Company operates. While the Company generally believes that such research and estimates are reasonable and

reliable, they, and their underlying methodology and assumptions, have not been verified by any independent source for accuracy or completeness and are

subject to change without notice. Accordingly, undue reliance should not be placed on any of the industry or market data contained in this presentation.

You agree to be bound by the foregoing limitations and conditions and, in particular, will be deemed to have represented, warranted and undertaken that you

have read and agree to comply with the contents of this notice.

LEGO ®, the LEGO logo and LEGOLAND ® are trademarks of the LEGO Group. ©2016 The LEGO Group. LEGOLAND IS A PART OF MERLIN

ENTERTAINMENTS plc.

2

Company Overview

3

DXB Entertainments PJSC

DXB Entertainments PJSC is a Dubai headquartered leisure and entertainment company

traded on the Dubai Financial Market under the trading symbol DXBE.

DXB Entertainments PJSC was listed on the DFM in December 2014 originally as Dubai Parks

and Resorts PJSC.

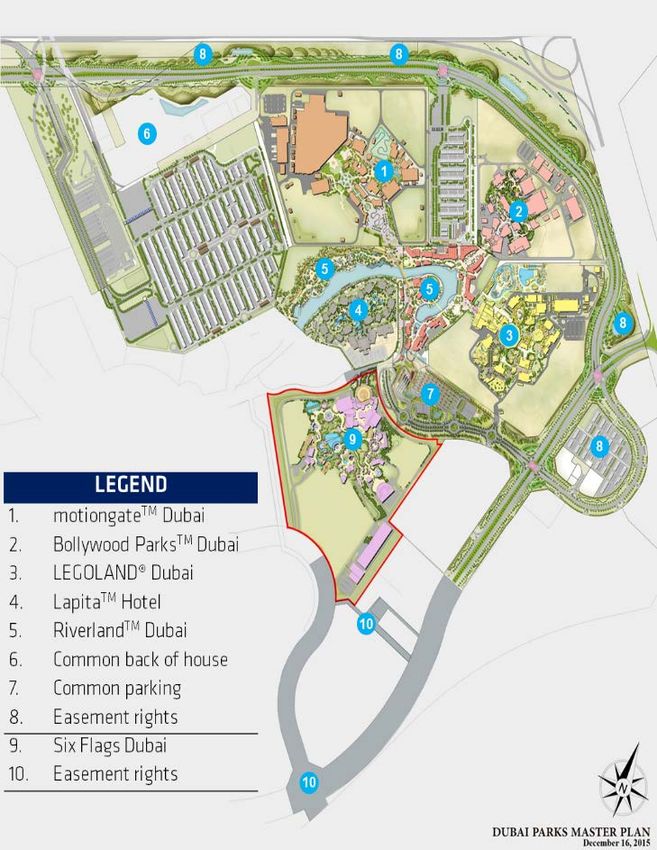

DXB Entertainments PJSC owns the Dubai Parks and Resorts destination which consists of 4

theme parks (Six Flags Dubai coming in 2019) and 1 water park all at the same location.

8.0b 5.2b 8.1b

AED 8 billion equity AED 5.2 billion AED 8.1 billion market

financing cap

DXB Entertainments DXB Entertainments DXB Entertainments

has raised AED 6.3 has raised AED 4.2 PJSC is listed on the

billion in equity billion through a Dubai Financial Market

through an IPO in financing facility for and has a market cap

2014, and an additional Phase I for DPR, and of AED 8.1 billion as at

AED 1.7 billion through an additional AED 1 31 March 2017.

a rights issue in 2016. billion for Phase II.

4

DXB Entertainments group

The Company aims to generate long term growth through developing

relevant companies and assets in target sectors:

Theme Parks Hospitality Retail and Dining

Hotel*

*

In the short-term, DXB Entertainments’ focus is to achieve operational excellence

and delivering additional growth and stable visitor numbers at Dubai Parks and

Resorts.

In the medium to long-term the Company may seek to expand the opportunities

to include media and entertainment.

* Phase II expansion, coming after 2018. LEGO, the LEGO ® logo and LEGOLAND ® are trademarks of the LEGO Group. ©2015 The LEGO Group. 5

LEGOLAND IS A PART OF MERLIN ENTERTAINMENTS plc.

Shareholding structure

Shareholder composition

As at 31 March 2017

A Dubai-based holding company

established in 2007, with operations and

assets in the UAE and overseas

Has access to a huge land bank in prime

locations throughout Dubai

Has launched several projects in the

tourism, retail, hospitality, leisure and

entertainment sectors

Is focused on introducing new and unique Meraas 52%

products to the market

Qatar Holding 11%

Kuwait Investment Authority 5%

Is committed to the success of DXB Institutional 22%

Entertainments Retail 10%

Sources: Meraas, Company information, Other public sources. Shareholder structure as at 31 March 2017.

Due to rounding, numbers presented may not add up precisely to the totals provided and percentages may not precisely reflect the absolute figures 6

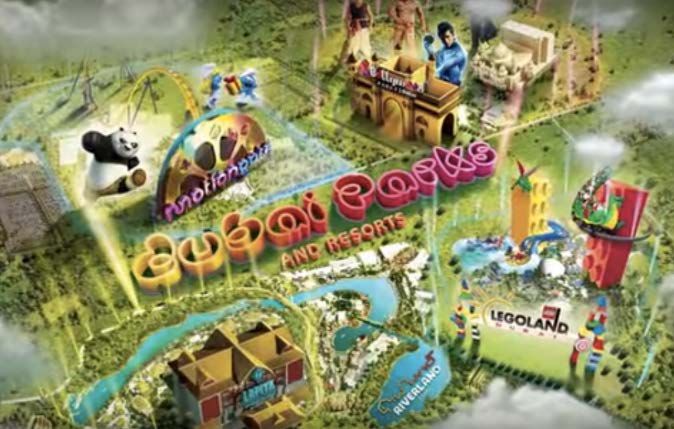

Dubai Parks and Resorts

7

Dubai Parks and Resorts

Premier year-round integrated theme park

destination, opened on 31 October 2016

Total estimated cost is AED 13.2 billion

• AED 10.5 billion for Phase I and

• AED 2.7 billion for Phase II.

World class partners and brands including

LEGOLAND® Parks, DreamWorks Animation

LLC, Colombia Pictures, Lionsgate, Six Flags

and popular Bollywood movies

Set across 30.6 million square feet of land of

which 25.1 million square feet is for Phase I

and 5.5 million square feet for Phase II of DPR

• c. 19.5 million square feet is owned by us,

and

• c. 11.1 million square feet of additional land,

for which we have all necessary easement

rights, will principally be used for access

roads and parking

Due to rounding, numbers presented may not add up precisely to the totals provided and percentages may not precisely reflect the absolute figures 8

DPR location

Strategically located on Sheikh Zayed

Road mid way between Dubai and Abu

Dhabi International Airports

20 km from Al Maktoum International Airport

63 km for Dubai International Airport

68 km from Abu Dhabi International Airport

9

Dubai Parks and Resorts

officially inaugurated on 18

December 2016

10Dubai Parks and Resorts opening

31 October 2016

LEGOLAND® Dubai and

Riverland™ Dubai

17 November 2016 16 December 2016

Bollywood Parks™ Dubai MOTIONGATE™ Dubai

2 January 2017

Lapita™ Hotel

LEGOLAND® Water Park

11Key Investment Highlights

12Key investment highlights

As the owner of the largest theme park destination in the Middle

East and Indian Subcontinent, DXB Entertainments is a unique

opportunity to tap the regional theme park market

01

Untapped theme park market in the MENA/Indian Subcontinent

Despite significant demand for theme park offerings, the Middle East and wider region

currently lacks a world class theme park destination.

02

Favourable UAE tourism growth trends

Dubai’s international visitors reached 14.9 million in 2016 – a 5% increase year on year.

In the first quarter of 2017 it has grown by 11%.

03

Unique offering

Only multi-theme park destination in the region, first Bollywood theme park in the

world, only water park targeting children in the region, first LEGOLAND® Park in the

region, and a unique Hollywood movie themed park.

13Untapped theme park market MENA/Indian subcontinent

3 billion people live DXB arrivals Top 10 global theme Dubai and Abu Dubai and Abu

within a 4 hour Dhabi tourist Dhabi

up 7.2% in 20161 park groups recorded

flight from Dubai arrivals projected population

420.4 million visits in

to grow at 8.6% growth

20152

projected at

CAGR3

4.0% CAGR3

Global Attendance Across Top

Theme Parks (2015, million) 4.6

6.8 4.7

7.7

3.6 8.9

20.5

5.2

2.9

142.7 14.7 50.0

62

UNTAPPED

MARKET

7.7

1.4

4.2

1.0

3.7

1.0

Source: AECOM

1 “Dubai Airports Factsheet. 2 AECOM. 3 Source: Dubai Parks and Resorts 2015 Feasibility Study for the period 2014-2022F. 14

Other sources: TEA and AECOM 2015 Theme park index, AECOM Global Attractions Attendance Report.Tourism growth trends

Visitors from top 10 source markets Q1 2017 Q1 2016 % change

Total visitors Jan-Mar 2017 Jan-Mar 2017 (’000 visitors) India 578 469 23%

Saudi Arabia 440 476 -8%

4.57m UK

China

Oman

350

230

334

140

5%

64%

Up 11.2% YOY Iran

214 322 -33%

181 130 39%

Pakistan 178 152 17%

USA 176 166 6%

Germany 172 171 0%

Kuwait 131 119 10%

Total 2,650 2,479 6.9%

Russia 126 61 106%

7% – Russia, CIS, EE

(Eastern Europe)

22% – Western Europe

6% – Americas 11% – North Asia and

South-East Asia

19% – GCC

18% – South Asia

12% – MENA

4% – Africa

1% – Australasia

Source of visitors by region (% in Jan-Mar 2017)

Source: Department of Tourism and Commerce Marketing (DTCM) 15Unique offering

A multi-themed destination unique to region and the world

• Only theme park destination in the world with 4 gates

within walking distance of each other

• Targets a wide audience across age groups and

demographics– families with children 2-12, teenagers,

adults

• Best-in-branded entertainment from three of the largest

picture studios in Hollywood – DreamWorks Animation,

Columbia Pictures and Lionsgate

• First Bollywood theme park in the world

• First LEGOLAND® park in the region

• First water park targeting children 2-12 in the region

LEGO, the LEGO ® logo and LEGOLAND ® are trademarks of the LEGO Group. ©2015 The LEGO Group. LEGOLAND IS A PART OF MERLIN 16

ENTERTAINMENTS plc.Q1 2017 Performance

17Key Q1 2017 performance highlights

1 January 2017 – 31 March 2017

Total Revenue Theme Park Revenue

AED 159.9 million AED 125.4 million

Visits Revenue per cap

586,355 AED 213.9

(theme parks)

Drawn down

Total assets

AED 12.5 billion AED 3.8 billion

From AED 4.2 billion facility

Due to rounding, numbers presented may not add up precisely to the totals provided and percentages may not precisely reflect the absolute figures. 31 March 2017 figures are

unaudited. 18Revenue breakdown

1 January 2017 – 31 March 2017

Totalrevenue Theme parkrevenue Retail revenue Hospitality revenue

AED159.9m AED125.4m AED14.4m AED10.4m

Theme park 78% Admissions 68% Leasing 76% Accommodation 70%

Retail 9% In-park spend 24% Non-leasing 24% Others 30%

Hospitality 7% Others 8%

Others 6%

Visits GLA leased Average occupancy

586,355 84% 21%

Revenue per capita Average daily rate

AED 213.9 AED 795

Theme parks

Due to rounding, numbers presented may not add up precisely to the totals provided and percentages may not precisely reflect the absolute figures. 31 March 2017 figures are

unaudited. The Group currently determines and presents financial information as a single operating segment based on the information that is provided internally to corporate management for 19

decision making.Visits breakdown

Total Visits

586,355 Visits breakdown (bycategory)

Jan-Mar 2017

Walk-in 33%

Online 24%

Tour operator 14%

Others 29%

Note: Others include Schools, Corporates, Annual passes, VIPs and

Complimentary passes

Key visitation factors:

Key School holidays during the period positively impact

attendance

• Saudi school holidays

• Kuwaiti school holidays

• UAE school holidays

Rainy weather during the period negatively impacts

attendance

20Summary financial results

1 January 2017 – 31 March 2017

Financial Performance

AED millions

Q1 2017 Q1 2017 Adjusted*

Revenue 160 160

Cost of Sales (13) (13)

Gross Margin 147 147

Operating Expenses (285) (214)

Depreciation (111) (111)

Interest / Financing Costs (Net) (43) (50)

Loss for the period (292) (228)

CF hedging gain (loss) on FV 4 4

Total Comprehensive loss for the period (288) (224)

* Adjusted Q1 2017 performance excludes pre-operating expenses of AED 71 million from operating expenses and AED 7 million of

interest income from Six Flags Dubai from Interest/Financing Costs

Excluding pre-operating expenses and interest income from Six Flags Dubai

Loss for the period Operating Expenses

AED228m AED214m

Excluding the pre-operating Excluding the pre-operating

expenses and interest income from expenses and interest income from

Six Flags Dubai Six Flags Dubai

Due to rounding, numbers presented may not add up precisely to the totals provided and percentages may not precisely reflect the absolute figures. 31 March 2017 figures are

unaudited. 21Summary financial results

1 January 2017 – 31 March 2017

Total assets

Financing

AED12,541m AED3.8bn

Dec 2016: AED 12,814 million AED 3.8 billion drawn down from

our AED 4.2 billion financingfacility

Property and equipment 75.14% for Phase I of DPR

Investment properties 5.01%

Investment in a Joint Venture 0.14%

Inventories 0.38%

Due from a related party 0.18%

Trade and other receivables 1.15%

Derivative financial instruments 0.33%

Other financialassets 3.34%

Cash and bank balances 14.34%

For the three months ended 31 March 2017

Movement in Cash

AED millions

800

Operating

Investing- other financial assets

600

Investing- property and equipment and

investment properties 400

Investing - others 571

Financing 200 295

-

(10)

(200) (64)

(529)

(400)

(600)

Due to rounding, numbers presented may not add up precisely to the totals provided and percentages may not precisely reflect the absolute figures. 31 March 2017 figures are

unaudited. 22Key challenges ahead

Operating during summer and Ramadan

Q2 and Q3 are expected to be lower performing

quarters due to Ramadan and the summer

months

Effective 21 May 2017 new operating hours,

improved transportation service and attractive

packages will be implemented to continue

attracting visitors during the summer

Increasing attendance numbers from tour and

travel

Key focus for the sales strategy is increasing the

contribution of the tour and travel to the visitation

numbers to ensure targets are met

Ramp-up in contribution from 5% in Q4 2016 to

14% in Q1 2017 shows promising signs of

growth

23DPR Strategy

24Sales strategy

Create active consideration and pre-

booking solutions for tourist planning

to vacation in Dubai

Drive demand and secure conversion

for tourist already in Dubai

Diversify source of business to secure

off-peak attendance

Build consumer insight and revenue

management to better forecast and

optimize our business

Deliver solid booking solution and

engaging customer portal

25Sales strategy

Source market representation and attendance targets

UK Germany / Swiss Russia

- Rep office - Rep office - Rep office

- 2 ticket brokers - 8 Tour - 9 Tour

- 10 Tour operators operators

operators

Russia

Canada

Western Europe

USA China

China

- Rep office

- 9 Tour

operators

Nigeria - 2 OTA’s

India / Pakistan

Australia

Africa

- 8 Tour

operators

UAE India

- 82 DMC’s - Rep office

- 9 Tour

operators

26Ticket prices

In line with regional and international offerings

Dubai Parks and Resorts

Adult ticket price

Park / attraction Adult ticket price ($)

(AED)

MOTIONGATETM Dubai 80 295*

Bollywood ParksTM Dubai 65 240

LEGOLAND® Dubai 80 295

LEGOLAND® Water Park 65 240

Regional

IMG World of Adventure 66 245

Ferrari World 75 275

Wild Wadi 75 275

Yas Waterworld 68 250

Aquaventure 70 260

Ski Dubai 91 335

At the Top – Burj Khalifa 55 - 136 200 - 500

International

Magic Kingdom 115 422

Disneyland Tokyo 65 238

Disneyland Anaheim 110 404

Epcot 107 392

Disneyland Paris 80 291

Universal Studios

76 199

Singapore

LEGOLAND Malaysia 34 128

* MOTIONGATE Dubai preview price is AED 250, valid until early Q2 2017. Due to rounding, numbers presented may not add up precisely to the totals provided and percentages

may not precisely reflect the absolute figures. Sources: Company information, company websites, Dubai Parks and Resorts 2014 Feasibility Study , CBRE, TEA / AECOM reports 27Revised pricing strategy

Simplifying the diversity of our offering

Single park / multi-park / multi-day ticket options

1 1 day 2 Days 7 days

day 2 parks 4 parks All theme parks

Starting

From* AED 215 AED 335 AED 425 AED 505

Annual Passes

Single VIP all

Single park + All

park parks

water park parks

Starting

From AED 755 AED 985 AED 2,496 AED 6,995

Add On

Q - Fast VIP tours VIP tickets

*the prices as per dated tickets purchased online. 28Driving in-park spend

01 02 03 04

Food and Beverage Merchandising Photography and Services

Games

All F&B concepts IP branded Picsolve Locker rental

within the parks are products International is

operated by Dubai providing in-park Stroller rental

Parks and Resorts Park branded image capture

in partnership with products Wheelchair rental

our central kitchen HB Leisure are

Destination-wide providing skills ECV rental

products games

3rd party Both are revenue

concessionaires share agreements

29Enhancing the visitor experience

Resort App

MAIN FUNCTIONALITIES:

o Discover the park

o Buy tickets

o See all attractions Tickets

o Way finding

o Geo Localization MAIN FUNCTIONALITIES:

o E-Wallet o RFID ticket

o Share E-Wallet o E-Wallet

o Family & Friends o Hotel key

o Meeting Place

o Events

o Share content

o Make reservations

o Couponing

o Push Notification

o Book a table

30Creating and leveraging our own brand IPs

31Mitigating the potential impact of seasonality

• Overall, weather is a key factor that impacts theme park attendance

• Rain, snow and high temperatures impact attendance figures and ability to operate – theme parks

Weather can be located in countries that experience high levels of precipitation (Denmark, France, etc.) or humidity

of concern for (Singapore, etc.) experience a negative impact on attendance

theme

• Temperature is a potential concern for Dubai Parks and Resorts - Dubai is hotter than other theme

park attendance

park destinations during the summer months - however, precipitation levels are by far the lowest when

compared to other international markets with significant theme park offerings

– Dubai has an average monthly precipitation level of 8 mm versus 108 mm, 53 mm and 195 mm for

Florida, Paris and Singapore respectively

The DPR master plan

Mitigating the

has been designed to

DPR heat strategically address

concern heat concerns

78% 43% 69%

% attractions indoor and air conditioned

Integrated Indoor and air Adjustment of

strategy for State-of-the-art conditioned queuing Landscape and operating hours during

dealing with the integrated cooling for rides; any architecture includes summer months to

heat systems additional outdoor significant shading address peak day

queuing has fans temperatures

Addressing the concerns around heat levels in

Dubai during the summer months

Sources: Dubai Meteorological Office, National Environment Agency Singapore, Météo-France, Danish Meteorological Institute, World Weather 32

OnlineSummer Strategy

Operating during summer and Ramadan

Effective 21 May 2017

Attractive summer packages announced

AED 195, one park + unlimited food

AED 295, two parks + unlimited food

Summer operating hours with later start

MOTIONGATE™ Dubai 2pm-10pm

Bollywood Parks™ Dubai 4pm-12am

LEGOLAND® Dubai 12pm- 8pm

LEGOLAND® Water Park 10am–7pm

Tram transportation available between the

parks and through Riverland™ Dubai

33Summer Operational Strategy

R I V E R L A N D - T R A M R OU T E

BOLLYWOOD STOP

RT1 - VIP CAR PARK STOP

MOTIONGATE STOP

RT2 - VIP CAR PARK STOP

RT1 - BOARDWALK STOP LEGOLAND STOP

Air-conditioned trams will

transport guests through

Riverland™ Dubai

RT3 - FREN CH VILLIAGE STOP

Over 150 misting fans will be

placed strategically throughout

Riverland™ Dubai.

FREN CH VILLAGE / BUS-TAXI STOP

34DPR Phase II

35Project funding – DPR Phase II

Project funding (AED m)

993

2,671

Phase II

1,678

Equity Debt Phase II

Funding Financing

Debt facility secured from Abu Dhabi Commercial Bank, Dubai Islamic Bank and Sharjah Islamic Bank.

Source: Company information

Due to rounding, numbers presented may not add up precisely to the totals provided and percentages may not precisely reflect the absolute figures 36Six Flags Dubai

As at 31 March 2017

About Six Flags Dubai

• GCC wide exclusivity (excluding KSA) + Egypt

• Due to open late 2019

• 27 rides and attractions spread across an opening day

footprint of 2 million square feet

• Construction started in July 2016

• Will be operated by Dubai Parks and Resorts (under a

management services agreement with Six Flags)

Construction update

On track to open in late 2019

Procurement:

• 7 ride agreement are signed. Agreement Signing of

10 rides are in final stage, remaining 4 rides are

under negotiation with Ride Vendors.

Design Development:

• 90% DD progressing for multiple packages.

Construction:

• Enabling works and access roads completed

• Nitro splash pond, laydown area & retention basin

substantially completed. BOH Car Park, & BOH

buildings substructure works commenced.

37LEGOLAND® Dubai Hotel

As at 31 March 2017

LEGO® themed hotel to open at Dubai Parks and

Resorts

• First LEGOLAND® Hotel in the Middle East

• Adjacent to LEGOLAND® Dubai

• Set across 300,000 square feet

• 250 rooms

• 60:40 joint venture between DXB Entertainments

and Merlin Entertainments

• Will be operated by Merlin Entertainments once

open

Construction update

Project Management

• Contracts for lead consultants finalized.

Design & Site Progress

• Detailed Design stage for Facility works completed

and currently VE exercise in progress.

• Detailed Design stage for Infrastructure works

completed and for Area Development being

developed.

• Grading works completed and Erection of Hoarding

in progress.

38Projected theme park visits and market penetration

UAE theme park addressable market Theme park visits and market penetration1

(millions of potential visitors) (2013-2022F visits in millions)

UAE Resident Population Income and Drive Qualified

45.4 43.8 Orlando Denmark Japan Hong Kong Singapore

UAE International Tourists (VFR) 40.2

9.2 Penetration rate

UAE International Tourists (Hotel Guests) 35.2 9.4 90% 42% 37% 24% 18%

32.5 8.9

30.1 4.5 No of parks 7 2 5 2 1

28.4 8.7 4.3

26.6 3.9

23.4 25.0 8.4

7.8 8.1 3.3

7.5 3.0

7.0 7.2 2.8

2.4 2.6

2.3 2.2 31.7 30.1

27.3 Total market penetration potential 44%

21.0 23.1 37%

16.8 18.0 19.2

14.1 15.5 Actual penetration (assumed 38%

28%

in business plan)

19.8

2013 2014 E 2016F 2017F 2018F 2019F 2020F 2021F 2022F

2015F

Theme Park Visits 16.9

• Total UAE theme park addressable market consists of

Potential 17.4

14.2

– Hotel tourists 15.7

12.6

– UAE residents

11.2

– Visiting friends and relatives (“VFR”) 10.1 12.1

9.1

• UAE theme park demand estimated based on penetration rates of

8.1

comparable markets 7.6 9.8 12.8

8.4 11.2

• Large variation in penetration rates based on maturity of theme park 7.8

offering

6.6

• Dubai Parks and Resorts will serve the majority of the pent up theme 3.7 6.1

park demand (number of visits does not include visits to the

0.8 1.0 1.5

Bollywood Parks’ Rajmahal theatre and to the LEGOLAND® Water 0.9 4.3 4.5 4.7

2.2 2.3 3.2

Park) 0.8 0.9 1.0

• DPR offering appeals to multiple customer segments 2013 2014 E

2015F 2016F 2017F 2018F 2019F 2020F 2021F

• World class IPs and differentiated offering Other UAE theme park visits DPR theme park visits

Source: Dubai Parks and Resorts 2014 Feasibility Study. Other UAE theme parks is based on announced and existing theme parks and assuming a steady annual growth rate in visitation numbers.

Due to rounding, numbers presented may not add up precisely to the totals provided and percentages may not precisely reflect the absolute figures

Notes: 1 - Market penetration is calculated as total theme park visits / addressable market. The addressable market for the UAE is adjusted for certain factors such as income, location etc. as per the Dubai Parks and

Resorts 2014 Feasibility Study .2 - 2016F DPR visits only include visits from expected commencement of operations as per analysis in the Dubai Parks and Resorts 2014 Feasibility Study . DPR theme park visits 39

includes Six Flags Dubai starting 2019.Financial projections summary – DPR Phase II

Total visits per year for Six Flags Dubai (million) Six Flags Dubai revenue by category (million)

1,043 1,048

893

229 230

197

78% of

theme

3.3 3.2 park

2.9 revenue

187 814 818 generate

696

d from

tickets

42

0.6 145

2019F 2020F 2021F 2022F 2019F 2020F 2021F 2022F

AED 312 AED 308 AED 316 AED 327 Revenue per capita

Tickets In-park spend

Uses of funds (AED 2,671 million) Financial performance (AED million)

Financing, corporate and others

cost Business 2020F 2021F 2022F CAGR

286 development and

issue expenses 1 Visits 2.9 3.3 3.2 5.1%

Land cost 65 Growth 13.4% -2.6%

390

Revenue 893 1,043 1,048 8.3%

Growth 16.8% 0.5%

Infrastructure EBITDA 296 371 365

cost Margin 33.2% 35.6% 34.8%

473

Net Income 134 209 204

Construction cost

1,457

1

Business Development budget to be utilized for master-planning of future phases, hospitality offering expansion, development of strategic partnerships / JV, evaluation of new concepts / ideas, etc.

In-park spend includes park sponsorship revenue. Due to rounding, numbers presented may not add up precisely to the totals provided and percentages may not precisely reflect the absolute figures. 40Contact Us

Investor Relations Contacts DXB Entertainments PJSC

Marwa Gouda Emaar Square, Building 1, Level 2

Head of Investor Relations PO Box 123311, Dubai

United Arab Emirates

Abdulrahman Al-Suwaidi

Investor Relations Officer Tel: +971 4 8200 820

Fax: +971 4 8200 819

IR@dxbentertainments.com contact@dxbentertainments.com

www.dxbentertainments.com/investor-relations www.dxbentertainments.com

41DXB Entertainments IR App

Our new Investor Relations App is available for download on the

iTunes App store and the Google Play store!

42Appendix I

Management and Board

43Senior management

Raed Kajoor Al Nuaimi Sandesh Pandhare, CFA Paul La France

Chief Executive Officer Chief Financial and Investment Officer Chief Projects Officer

• Has held senior management roles over a 15- • Over 23 years of experience in the global • Over 37 years of experience in worldwide

year period with companies such as Tatweer, private equity and investment industry entertainment and hospitality

Dubailand and Dubai Properties Group • Previously held senior positions at Istithmar developments

• Previously, he was the Chief Leisure and World and JAFZA, among others • Previously Vice President of Program

Entertainment Officer at Meraas Holding • CFA charter holder and holds a Master’s in Management at Samsung C&T

where he helped develop new strategies and Management Studies from Mumbai University, Corporation

identify opportunities for the company in the India • Selected projects include Disneyland Paris,

leisure and entertainment field Walt Disney Studios Paris, Animal

Kingdom (Florida), Hong Kong Disneyland

Resort, Universal Studios’ Hollywood and

CityWalk Expansion (California), Universal

Studios Japan, Royal Island Resort

(Bahamas)

Vinit Shah Stanford Pinto Matthew Priddy

Chief Strategy and Business Chief Parks Operating Officer Chief Technical Officer

Development Officer • Over 20 years of professional experience with • Over 35 years of experience in prototype,

expertise in the areas of risk management, project development and real estate with

• Over 15 years of experience in the leisure and

corporate governance, internal auditing, as expertise in the creative development of

hospitality industry

well as process control and design entertainment destination projects

• Has previously held senior management

management • 20 years of experience at the Walt Disney

positions at Dubai Properties Group and a

• Has previously held senior executive positions Company, with responsibility for design,

number of Fortune 500 companies

within the business consulting and risk engineering, manufacturing and overall

• Holds an MBA from the Asian Institute of

management divisions of leading accounting project management for a number of

Management in the Philippines, a Strategic

firms including Arthur Andersen and Ernst & Disney theme parks, resorts and technical

Finance certificate from the Vienna University

Young developments

of Economics and Business, and a Master’s in

• Holds an MBA from Pune University and a • Holds a bachelor’s degree in Theatrical

Commerce and Business Management from

bachelor’s degree in Commerce from the Technology from the University of

the University of Mumbai, India

University of Mumbai California, Los Angeles

Aida Hamza Klaus Assman David Loiseau

Chief Business Support Officer SVP- Retail and Hospitality SVP-Sales and Marketing

• Over 27 years of experience in management, • Over 3 decades of experience as a sales

• More than 27 years of experience in the

corporate affairs, marketing and communications and marketing professional, vastly in the

hospitality industry across the UAE, Thailand

• Has previously held the position of Director of hotel industry, working with global brands

and the United States leading the

Supply Chain Management, Human Resources, like Marriott International, Mandarin

opening/renovation of more than seven hotel

Corporate Affairs and Marketing at Ejadah Asset Oriental Hotel Groups and the Jumeirah

properties.

Management Group as well as Executive Director Group.

• Previously held the position of General

of Corporate Services at Istithmar World • Has previously held the position of Vice

Manager of Sofitel Dubai Downtown as well as

• Worked with leading companies in the UAE such President Sales with Kerzner International,

completing tenures at Jumeirah Group in the

as Dubai World, Standard Chartered Bank, ENOC, Atlantis the Palm.

UAE, Thailand and the United States, Shangri-

Citibank and Emirates Broadcasting Corporation • He is a Science Graduate with various

La Hotels and Resorts in the Philippines, Park

• Holds a bachelor’s degree in Management and leadership certifications from the industry.

Hyatt in Germany and the United States, as

Marketing from the Davis and Elkins College, West well as Nikko Hotel in the United States and

Virginia, United States the United Kingdom and Holiday Inn in

Germany

• Holds a bachelor’s degree in Hotel

Management from the Hotel School, Aachen,

Germany

44Senior management

Julien Munoz Brian Machamer Muhammad Suleman

VP – Sales VP – Theme Park Operations VP of Governance, Risk and Compliance

• More than 20 years’ experience in leisure and • Over 25 years of experience in the theme park

hospitality, including 12 in the theme park industry, including various roles in park • Over 13 years of experience in governance, risk

industry, having previously been Director, opening and operations advisory, corporate compliance, policies

Marketing & sales at Disneyland Paris. • Joined Universal Studios’ international team in development, business process review.

• He also worked with Group Accor in France, and 2008 to help design the Universal Studios • Previously he served as Senior Manager

Hilton International in the UK. theme park planned for Dubai Governance for the Engineer’s Office of His

• He now leads Dubai Parks and Resorts'’ sales • Worked with Resorts World Sentosa as Highness Sheikh Mohammed Bin Rashid Al

and distribution strategies internationally and Assistant Vice President of Attraction Maktoum and responsible for the development

domestically, and is also responsible for ticket Operations for more than 4 years, where he of its governance and control framework.

pricing and revenue management. was closely engaged in the pre-opening and • He has also previously worked with KPMG

• Mr. Munoz is an MBA graduate from Essec ongoing operations of Universal Studios (Dubai Office) as part of the Assurance &

Business School in Paris and Cornell university Singapore Business Advisory services division.

New York. • Also worked at Universal Studios Florida and • He is an Associate Member of the Institute of

Walt Disney World’s Magic Kingdom in Chartered Accountants of Pakistan. He holds

Orlando, Florida an Advanced Diploma in Management

Accountancy from CIMA—UK and a bachelor’s

degree in Commerce from the University of

Karachi, Pakistan.

Marwa Gouda, CAIA, CIRO

Head of Investor Relations

• Over 15 years experience in investor relations and

financial marketing. She previously held the

position of Head of Investor Relations at I2BF

Global Ventures, a boutique investment

management firm.

• In 2003 she joined Man Group in Switzerland and

during her six year tenure held different positions

in investment marketing and client services in

London, Zurich and Dubai. Her last position was as

Marketing and Client Service Manager at Man

Environmental Capital Opportunities, Man’s

private equity environmental finance arm.

• She is a Certified Alternative Investment Analyst

and holds a BA in Political Science and a BA in

Economics from the American University in Cairo

45Board of Directors and board committees

Nomination and Board of Directors by type

Remuneration

Name Nationality Independent Audit Committee Committee

Abdulla Al Habbai UAE Non-Executive - 5

Raed Kajoor Al Nuaimi UAE Executive -1

-3

Abdul Wahab Al-Halabi UAE Independent

Edris Alrafi UAE

Board of Directors by nationality

Fayez Mohamed Al-Boainin Qatari

Cristian Viorel Gheorghe Romanian

UAE National 5

Fahad Kazim UAE

Other Nationalities - 4

Dennis C. Gilbert USA (Chairman)

Steven D. Shaiken USA (Chairman)

Abdulla Al Habbai Abdul Wahab Al-Halabi Raed Kajoor Al Nuaimi

Chairman, Non-executive Director Non-executive Director Executive Director and Chief Executive Officer

• Group Chairman of Meraas Holding and Chairman of Dubai • Abdul Wahab Al-Halabi is the Group Chief Investment • Raed Kajoor Al Nuaimi is the Chief Executive Officer of DXB

Properties Officer of Equitativa, a diversified financial services group Entertainments PJSC

• Mr. Al Habbai is also Chief Executive Officer of the specialising in the development of REITs in emerging • Previously, he was the Chief Leisure and Entertainment Officer at

Engineering Office since 2005 and the Chairman of Dubai markets. Meraas Holding

Hills, Dubai Valiant Healthcare and Deputy Chairman of Rove • He was previously the Group Chief Investment Officer of • Has held senior management roles over a 15-year period with

Hospitality. Meraas Holding group. Mr. Al-Halabi has more than 18 companies such as Tatweer, Dubailand and Dubai Properties

• Serves on the Boards of Dubai Real Estate Corporation and years’ experience in the real estate sector, with expertise in Group

Museum of the Future amongst others. financial restructuring, crisis and debt management, credit • Holds a bachelor’s degree in Business Administration from

• Holds a Master’s Degree in Cadastral & Land Information enhancements and joint ventures. Ashford University, UK, and is a member of the Chartered Institute

Management from the University of East London • Previously held positions include partner at KPMG, Chief of Personnel and Development

Executive Officer of Dubai Properties Group

• Holds a bachelor’s degree in Economics from the London

School of Economics and an Executive MBA from Ecole

Nationale des Ponts et Chaussées

46Board of Directors contined

Edris Alrafi Cristian Viorel Gheorghe Fayez Mohamed Al-Boainin

Non-executive Director Non-executive Director Non-executive Director

• Mr Alrafi is the Chief Commercial Officer at Meraas Holding. • Mr Gheorghe is Chief Financial and Investment Officer at • Mr Al-Boainin is a talented and value-driven professional

He brings more than 13 years of experience in investment Meraas LLC. Bringing with him over 18 years of banking offering 29 years’ experience in the Information Technology

banking, finance and private equity. experience working globally across several industries. (IT) field, with 19 years in management roles.

• Prior to Meraas, he served as Head of Middle East Business • Prior to joining Meraas, Cristian served as Investment • He is currently the IT Director at Qatar Investment Authority

at the private equity firm Developing Markets Capital (DMC) Strategist at Citi Private Bank in Geneva where he led the buy managing 3 departments relating to corporate IT needs

Partners side advisory to a high profile, multibillion-dollar franchise including IT planning and strategies, business systems,

• Mr Alrafi also served as Head of UAE client coverage at relationship of the bank in Saudi Arabia. He is a board infrastructure and services.

Goldman Sachs for the UAE. Prior to Goldman Sachs, he member at Yvolve LLC, MD Health and Wellness LLC and • He is a member of the Board of the Qatar Stock Exchange

served as General Manager at First Gulf Bank in the Marsa Al Seef LLC and others. and a member of its Audit and Risk Committee. Mr Al-

Securities Division and worked closely with the CEO and • Along with a CFA designation, Cristian holds an MBA degree Boainin received his BA in Computer Science and Math from

Managing Director of the Bank. from Rotman School of Management, University of Toronto the Pacific Lutheran University in the USA.

• He is currently Vice Chairman at Noor Bank and Nshma and a Bachelor’s degree in Economics from the Academy of

Properties and the Chief Executive Officer at Dubai Holding. Economic Studies in Bucharest.

He holds a finance degree from the Higher College of

Technology in the UAE.

Fahad Kazim Denis C. Gilbert Steven D. Shaiken

Independent Non-executive Director Independent Non-executive Director

Independent Non-executive Director

• He is an Independent Advisor to the to the Group • More than 45 years of experience in the theme park and • Provides consulting services to major companies in the

attraction business travel and leisure industry including Disney, Universal,

Chairman at Meraas

• Aramark etc.

• Previously the Chief Commercial Officer at Meraas Holding Has held various senior management positions at Sea

• More than 40 years of experience in the destination

where he was responsible for the business development World of Ohio, Resorts World Sentosa (Singapore), Stone

Mountain Park (Atlanta), Ocean Embassy and three branded entertainment arena

and asset management functions including its retail

interests together with its recently launched Food & Anheuser Busch Adventure Parks • Previously, Executive Managing Director at Adventure

• Chairman of the Board and majority stockholder for World (Warsaw)

Beverage division

• Has previously worked at PwC in the audit and transaction Gilberts of Atlanta, a restaurant company operating as a • Has previously worked with industry majors such as the

‘‘Wendy’s’’ franchisee Royal Caribbean International, Seaworld Parks &

services divisions

Entertainment, Disney Cruise Lines, Starwood and Hilton

• Serves on several boards, the Oversight Board at Emirates

hotel chains, among others

REIT and Arthrogen BV.

• Holds a bachelor’s degree in Accounting from Concordia

University, Canada, and is a qualified Certified Public

Accountant

47Appendix II

Summary Financials for the three month period

ended 31 March 2017

48Condensed consolidated statement of financial position

As at 31 March 2017

Assets Equity and Liabilities

31 Mar 17 31 Dec 16 14,000 14,000

Reviewed Audited

(AED m) (AED m)

12,000 12,000

ASSETS

Property and equipment 9,423 9,465

10,000 10,000

AED Millions

Investment properties 628 634

Investment in a Joint Venture 18 -

Inventories 48 42 8,000 8,000

Due from a related parties 22 21

Trade and other receivable 144 90 6,000 6,000

Derivative financial instruments 41 37

Other financial assets 419 990

4,000 4,000

Cash and bank balances 1,798 1,535

Total assets 12,541 12,814

2,000 2,000

EQUITY AND LIABILITIES

EQUITY - -

31-Mar-17 31-Dec-16 31 Mar 17 31 Dec 16

Share capital 8,000 8,000

Cash flow hedge reserve 41 37 Property and equipment

Total Equity

Accumulated losses (930) (639) Investment properties

Bank facilities

Total equity 7,111 7,398 Investment in a Joint Venture

Trade and other payables

LIABILITIES Inventories

Bank facilities 3,560 3,204 Due from a related parties

Trade and other payables 1,870 2,212 Trade and other receivable

Total liabilities 5,430 5,416 Derivative financial instruments

Total equity and liabilities 12,541 12,814 Other financial assets

Cash and bank balances

Due to rounding, numbers presented may not add up precisely to the totals provided and percentages may not precisely reflect the absolute figures. 31 March 2017 figures

are unaudited. 49Condensed consolidated statement of comprehensive income

For the three months ended 31 March 2017

Loss for the period

31 Mar 17 31 Mar 16

Reviewed Reviewed

31-Mar-17 31-Mar-16

AED Millions

(AED m) (AED m) -

Revenue 160 - (38)

Cost of Sales (13) - (50)

General, administration and operating expenses (334) (40)

Marketing and selling expenses (41) (15) (100)

Other expenses (21) -

Interest (expenses) / income (37) 19 (150)

Amortization of borrowing cost (6) (2)

Share of loss from Joint Venture - - (200)

Loss for the period (292) (38)

Cash flow hedge gain / (loss) on fair value 4 (37) (250)

Total comprehensive loss for the period (288) (75) (292)

(300)

(350)

Due to rounding, numbers presented may not add up precisely to the totals provided and percentages may not precisely reflect the absolute figures. 31 March 2017 50

figures are unaudited.Condensed consolidated statement of cash flows

For the three months ended 31 March 2017

Movement in Cash

31 Mar 17 31 Mar 16

Reviewed Reviewed

(for three months ended 31 Mar 2017)

(AED m) (AED m)

Operating Activities

Loss for the period (292) (38)

Adjustments for:

Depreciation Expense 111 2

Interest expenses / (income) 37 (19) 800

Provision for employees' end of service indemnity 1 1

Amortization of borrowing cost 6 2 600

Share of loss from Joint Venture - -

(Increase) / Decrease in advances to contractors and other

400

receivables (43) 44

Increase in inventories (6) -

(Increase) / Decrease in trade and other payables (342) 218 200 571

Movement in related party balance (1) (13)

295

Net cash (used in) /generated by operating activities (529) 197 -

(529) (10)

Investing activities (200) (64)

Decrease in other financial assets 571 (178)

Additions to property and equipment (64) (844) (400)

Additions to investment properties - (40)

Interest received 8 3

(600)

Investment in Joint Venture (18) -

Net cash (used in) / generated by investing activities 497 (1,059) Operating

Investing-Other Financial Assets

Financing Activities

Proceeds from bank facilities 353 887 Investing-Property and equipment and Investment properties

Borrowing cost paid (6) (5) Investing-Other

Finance cost paid (52) (22)

Financing

Movement in restricted cash - (14)

Net cash (used in) / generated by financing activities 295 846

Net cash movement during the period 263 (16)

Cash and cash equivalent at the beginning of the period 1,344 364

Cash and cash equivalent at the end of the period 1,607 348

Due to rounding, numbers presented may not add up precisely to the totals provided and percentages may not precisely reflect the absolute figures. 31 March 2017

51

figures are unaudited.Appendix III

DPR Phase I projections based on 2014 IPO prospectus

52Projections DPR Phase I

Project funding (AED m)

4,214

10,536

Phase I

6,322

Equity Funding Debt Financing Phase I

2014 IPO Projections

The projections covered in this section are based on the 2014 IPO prospectus and have not been

revised since.

Management has indicated that revised guidance for 2017 will be given post Q1 2017 results and that

it is seeking a 20% operational cost reduction in 2017.

53Financial projections summary – DPR Phase I

Total visits per year (million) Theme park revenue by category (million)

2,573

2,289

2,038 616

550

492

76% of

theme park

9.1 10.3 revenue

7.9 1740 1957 generated

6.7 7.2 1546 from tickets

2017F 2018F 2019F 2020F 2021F 2017F 2018F 2019F

AED 304 AED 318 AED 324 Revenue per capita

Tickets In-park spend

Revenue by entity (AED million) Financial performance (AED million)

3,086

2,755 172 63 2017 2018 2019 CAGR

2,447 153 62 278

135 251 Visits 6.7 7.2 7.9 11.3%

220 54

Growth 7.5% 9.7%

Theme Revenue 2,447 2,755 3,086 12.3%

2573 park

2038 2289 Growth 12.6% 12.0%

revenue

is 83.4%

EBITDA 605 726 845

Margin 24.7% 26.3% 27.4%

2017F 2018F 2019F Net Income (36) 108 249

Theme parks Lapita Hotel Riverland Dubai Other

Source: Dubai Parks and Resorts 2014 Feasibility Study. Note: All the above charts capture full-year performance commencing 2017F. In-park spend includes park sponsorship revenue.

Due to rounding, numbers presented may not add up precisely to the totals provided and percentages may not precisely reflect the absolute figures. 54Summary projected financials – DPR Phase I

AED million

Forecasts as of the offering memorandum issued in November 2014

2015F 2016F 2017F 2018F 2019F

Income statement

Revenue - 563 2,447 2,755 3,086

Gross profit - 188 868 1,014 1,160

EBITDA (360) (402) 605 726 845

Operating profit before taxes and interest (360) (495) 234 351 465

Net income (326) (559) (36) 108 249

Balance sheet

Assets

Total non-current assets 4,921 9,223 8,881 8,584 8,300

Total current assets 4,138 575 719 728 865

o/w Cash 3,786 487 622 620 742

Total assets 9,059 9,798 9,600 9,312 9,165

Liabilities

Total current liabilities 687 466 91 104 119

Total non-current liabilities 2,496 4,016 4,229 3,819 3,408

o/w Loans 2,496 4,013 4,215 3,793 3,372

Total liabilities 3,183 4,482 4,320 3,923 3,527

Total equity 5,875 5,316 5,280 5,389 5,638

Total equity and liabilities 9,059 9,798 9,600 9,312 9,165

Cash flow statement

Cash flow from operating activities (152) (424) 221 726 843

Cash flow from investing activities (2,793) (4,169) (18) (65) (83)

Cash flow from financing activities 2,199 1,294 (73) (671) (645)

Sources: Company information, Dubai Parks and Resorts 2014 Feasibility Study.

Due to rounding, numbers presented may not add up precisely to the totals provided and percentages may not precisely reflect the absolute figures

Notes: 1- Income statement and cash flow statement shown above are for the periods indicated. Balance sheet relates to the financial position at the end of the corresponding

periods. 2- The financial year ending for the Company is December. 55You can also read