EBULLETIN #2 News and insight from across Sub-Saharan Africa - Mobile Ecosystem Forum

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

eBULLETIN #2

News and insight from across Sub-Saharan Africa

FEATURING

BUILDING MUSIC

REVENUES IN NIGERIA

TRANSFORMING ZIMBABWE

IN TO A CASH-LITE ECONOMY

MARKET SNAPSHOT:

MOBILE MESSAGING USAGE IN

NIGERIA & SOUTH AFRICA

THE NCC CONSULTATION FOR THE PROVISION

OF VALUE ADDED SERVICES IN NIGERIA

PLUS REGIONAL NEWS ROUND-UP & MARKET STATS

3 FOREWORD

RIMMA PERELMUTER, CEO, MEF

5 BUILDING MUSIC REVENUES IN NIGERIA

INTERVIEW WITH EBERE NZEWI, MARKETING MANAGER AT HUAWEI NIGERIA

MAHINDRA

MA

AHINDRA COMVIVA

7 TRANSFORMING ZIMBABWE IN TO A CASH-LITE ECONOMY

HOW MOBILE HAS CREATED AN INCLUSIVE FINANCIAL ECOSYSTEM

SRINIVAS NIDUGONDI, SENIOR VP & HEAD OF MOBILE FINANCE AT MAHINDRA COMVIVA

9 REGIONAL NEWS ROUND UP

LATEST NEWS FROM SUB-SAHARAN AFRICA IN PARTNERSHIP WITH APPSAFRICA ADVISORY

13 MARKET SNAPSHOT: MOBILE MESSAGING

EXCLUSIVE MEF DATA INSIGHTS MESSAGING USAGE IN NIGERIA AND SOUTH AFRICA

16 EVERYTHING YOU NEED TO KNOW ABOUT…

THE NCC CONSULTATION FOR THE PROVISION

OF VALUE ADDED SERVICES IN NIGERIA

18 REGIONAL TRENDS & STATISTICS

MEF AFRICA EDITION #2 2

FOREWORD

RIMMA PERELMUTER

CEO, MEF

elcome to the second edition of MEF’s Africa eBulletin. In it you

W will find interviews and insights in to the ever-changing

pan-African mobile ecosystem.

Whilst Africa’s one billion mobile subscriptions is made up of a mix of

smartphones and feature phones which still account for the majority of handsets,

the roll-out of 3G and 4G mobile networks means that faster mobile internet is

increasingly available to new African consumers.

As such, analyst firm Ovum forecasts that mobile Internet connections in Africa

will reach one billion by 2020. This is a huge increase considering that it

accounted for just 17 per cent of the 884 million total mobile subscriptions in

Africa in 2014. By 2020 it is expected to account for 76 per cent.

As smartphone penetration accelerates and reaches critical mass in the region

and sales concurrently begin to flat-line in the more developed regions,

manufacturers are keen to grasp the price sensitive African opportunity by

providing lower cost smartphone handsets.

The milestone of the sub $100 handset has been surpassed with the likes of

Orange announcing a $40 smartphone handset earlier this year specifically for the

African market. In particular, handsets from Chinese firms such as Huawei, Oppo

and Gionee are all increasing their reach across the African market and it’s Android

that dominates at the OS level.

Taken together faster networks and cheaper smartphones are helping to

accelerate the growth of the mobile ecosystem so that ever more evolved mobile

content and services are becoming routinely available. Alongside the much-hyped

areas of mobile banking, mHealth and education, mobile messaging and

entertainment services such as music and in particular video continue to have a

major impact as key data drivers.

For example Nigeria’s homegrown $5 billion film industry, Nollywood (bigger than

Hollywood by volume and second only to Bollywood in terms of market size) is

using mobile as a key distribution channel for its films. Nigerian online

entertainment platform, iROKOtv, are one of the largest distributors of African

movies in the world. It has attracted $34 million in funding, exemplifying the huge

scaling opportunity for homegrown African content across the continent and to

diaspora globally.

According to iROKOtv, whilst smartphones in Sub-Saharan African will outnumber

TV sets by 5 to 1 and will have achieved an 80-85 per cent share of the market in

video consumption by 2020, the ecosystem must continue to innovate to take

consumers along on the mobile journey.

MEF AFRICA EDITION #2 3

At this year’s Mobile West Africa conference in Lagos, I chaired a panel debate on

‘Empowering, Streamlining and Enriching the Mobile Consumer’s Experience’ with

Bango, Etisalat and Opera. Data transparency, the growth of mobile content

including entertainment, video and music and app store carrier billing were the hot

topics of the panel.

Firstly, consumers need to feel confident about data management in order to have

peace of mind. Opera’s Max for Android shrinks videos and photos to reduce data

usage whilst Huawei MTN’s Music+ service rolls the cost of data into a

subscription and allows its users to stream music for a fixed fee. However, there’s

a genuine fear that services like Facebook Messenger and content that uses

mobile advertising in the background will eat up precious data allowances and this

remains a point of contention.

As in developed markets, in order for the mobile opportunity to truly take off, data

and pricing models need to be affordable, transparent and better understood.

Consumers do not generally understand pricing based on megabytes and given

heightened sensitivity around data pricing, mobile services need to be transparent

in their pricing models with clear guidance on how much data has been spent and

on what services.

Carrier billing such as Bango’s Payment Platform provides a simple way for

consumers to purchase digital content and paves the way for a trusted

experience. Meanwhile Etisalat’s recently introduced data bundles, Smartpaks,

simplifies the pricing around mobile apps and streaming in a way that is

immediately understood by African consumers.

Accelerating the growth of the mobile ecosystem in Nigeria and beyond forms the

core of MEF Africa’s Steering Committee and its ongoing work in the region to

drive sustainability in the ecosystem.

The latest meeting explored the recent changes proposed by the Nigerian regulator

NCC on VAS regulation (see the Everything You Need To Know about...section in

this eBulletin) and gathered member views on how to respond whilst offering

inputs into MEF’s roadmap for the year ahead to drive sustainable business

models and guidance for companies entering new markets on the continent. If you

would like to join MEF Africa Steering Committee and help shape the evolution of

African ecosystem, then please contact the MEF team to learn more.

I hope you enjoy this second edition of the Africa eBulletin covering a broad range

of topics including an in-depth interview with MEF member Huawei looking at

how reducing friction is essential to introducing the next level of mobile services

to consumers in Nigeria, as well as a fascinating look at how Mahindra Comviva

partnered with Econet in Zimbabwe to launch the EcoCash mobile money service

which is driving mass financial inclusion.

You’ll also find regular eBulletin features including market stats and the quarterly

news round-up from across the region courtesy of AppsAfrica, demonstrating

once again how this exciting mobile economy is shaping up in one of the world’s

fastest growing and dynamic mobile markets.

MEF AFRICA EDITION #2 4

BUILDING MUSIC

REVENUES IN NIGERIA

BY REDUCING FRICTION AROUND

MOBILE DATA COSTS

INTERVIEW WITH EBERE NZEWI

igeria has a flourishing music scene. But, thanks to rampant

N piracy, its musicians don’t make the money they deserve.

Now, MTN’s and Huawei’s Music+ service is giving Nigeria’s

music-mad population a viable alternative to cheap illegal

CDs. MEF’s Feature Editor Tim Green recently interviewed

the service’s marketing manager Ebere Nzewi.

Late in 2015, MTN and Huawei launched the Music+ NextRated

MARKETING MANAGER AT HUAWEI NIGERIA

campaign. The big idea was to encourage unsigned Nigerian artists to

upload their tracks to MTV’s growing music download and streaming

channel. And, in so doing, to the 1.6m active

subscribers using MTN Music+ at the time.

The initiative was not just about

boosting awareness of the MNO’s “PIRACY IS

music channel and giving

unsigned artists unprecedented

STILL A BIG PROBLEM

publicity. It was also yet HERE. WE ARE DOING

another strike against the

piracy that is holding back an OUR BEST TO OFFER A

otherwise flourishing local LEGAL ALTERNATIVE

music scene.

THAT’S EASY FOR

According to Nigeria National PEOPLE TO FIND, AND

Bureau of Statistics data

reported by the FT, the domestic AFFORDABLE

film and music industries contribute TO USE.”

nearly 1.5 per cent to the country’s

GDP. The country’s music scene is central

to the cultural identity of Nigeria. Meanwhile

its movie scene - Nollywood - is the third biggest in the world.

But piracy cuts the potential revenues these sectors could command.

It’s rife. In fact, piracy is embedded into the way the industry works.

Nigeria is home to influential music blogs, which are linked to the

illegal reproduction of CDs that sell in markets for just a few cents.

But local artists are caught in a dilemma. They can make significant

money from corporate sponsorships once they are well-known.

These blogs offer a route to fame. It’s why many artists collude with

them.

Thankfully, legitimate new services like MTN Music+ - which was

built and managed by Huawei - have started a fight back. Ebere

Nzewi, content operation and marketing manager for Music+, says:

“Piracy is still a big problem here. We are doing our best to offer a

legal alternative that’s easy for people to find, and affordable to use.

We also use watermarking to identify when songs are illegally copied.

But some artists are still releasing songs to the blogs. It’s a cultural

thing that will take time to change.”

MEF AFRICA EDITION #2 5

MTN Music+ is a subscription based music streaming and download

platform. Users can access it through web, mobile web and mobile

native app. They can listen to current and trending songs, create

playlists, share music, gift music and enjoy offline streaming.

New users can try the service out free for a month, then there are

three subscriptions options - N100, N300 and N800, all of

which roll in a data allowance so users don’t get bill

shock.

In all facets of the service, MTN and Huawei “INCLUDING DATA

have worked hard to remove friction. Nzewi

says: “Including data in subscriptions was

IN SUBSCRIPTIONS WAS

important. It makes people relax and willing IMPORTANT. IT MAKES

to try out the app. We also charge by

airtime, which ensures that the payment

PEOPLE RELAX AND WILLING

method is easy and available to everyone.” TO TRY OUT THE APP. WE

With 3.3m subs now, MTN Music+ is more

ALSO CHARGE BY AIRTIME,

than playing its part in offering Nigerian WHICH ENSURES THAT THE

musicians a legitimate music option. In fact, it

paid over more than N500m in revenues

PAYMENT METHOD IS EASY

across eight months to local artists. The service AND AVAILABLE

also works hard to source exclusive songs such as

Wyclef’s Divine Sorrow (a chart topper) - all of

TO EVERYONE.”

which brings added attention to the channel.

Now, Huawei is looking to expand the service. It is targeting

more operators across more countries and preparing to add more

payment options including credit card. The company is also preparing

to add more content types, including podcasts.

MEF AFRICA EDITION #2 6

TRANSFORMING ZIMBABWE

IN TO A CASH-LITE ECONOMY

HOW MOBILE HAS CREATED AN INCLUSIVE

FINANCIAL ECOSYSTEM

SRINIVAS NIDUGONDI

SENIOR VP AND HEAD OF

MOBILE FINANCIAL SOLUTIONS AT

S

rinivas Nidugondi talks about how mobile money is driving

true financial inclusion in Zimbabwe sharing a fascinating

case study on EcoCash.

Rewind to 2008 and hyperinflation was wreaking havoc

in Zimbabwe. A bottle of Coke could cost ZIM $50 Billion in the

morning could sell for over ZIM $150 Billion in the evening – a hike of

over 300 per cent. This was what living in Zimbabwe was like in 2008.

By 2009 the Zimbabwean Dollar wasn’t worth the paper it was

printed on and was soon replaced by the US Dollar (I have a worthless

Zimbabwean trillion-dollar note that I’ve kept for posterity).

Although the currency shift managed to control the wildly galloping

inflation it also gave rise to new problems and challenges, EcoCash extended individual savings to group savings by

not least the dollarization of the economy wiped out introducing Savings Club, a mobile-based group

the bank-based savings of millions of savings scheme that can be initiated by any

Zimbabweans. As a result, people lost trust in EcoCash user who can invite participants to join

banking institutions and turned to informal

payment channels. Moreover, with $1

“ECOCASH HAS and make safe and seamless fund transfers

via SMS.

being the minimum currency in use, HAD A REALLY POSITIVE

Zimbabweans experienced an acute

coin shortage leading to a “change

IMPACT ON ZIMBABWEANS. Crucially the service is aimed at smaller

(previously unbanked) groups like the

problem”. THE WAY THAT ALL THE self-employed, informal sector

entrepreneurs, street vendors and

Fast forward to 2015 and the STAKEHOLDERS – women’s groups. A small farmer in

African country’s economy is CONSUMERS, MERCHANTS, need of some capital for buying

rebounding, the change problem seeds or an expectant mother in

has been marginalized and financial ECONET AND STEWARD need of financial support while her

inclusion is a reality for millions of

Zimbabweans. A key driver of

BANK – HAVE COMMITTED TO use-cases.

baby is on the way are typical

transformation is EcoCash, IT IS A GREAT EXAMPLE OF In this way, EcoCash is driving

Zimbabwe's first and most prominent socio-economic benefits and laying a

mobile money service.

WHAT CAN BE strong economic base by mobilizing small

ACHIEVED.” deposits from the financially excluded. Prior

Launched in 2011, by Econet Wireless, to EcoCash Save and Saving Club that cash

Zimbabwe's leading mobile operator, and based might as well have been (and often was) kept

on Mahindra Comviva’s mobiquity® Money platform, under a mattress.

EcoCash has grown as a viable alternative to cash for

millions of Zimbabweans.

It started out by letting users pay each other with a simple text or

USSD message. But in time, it acted as a springboard to more

‘conventional’ financial services to support people looking to save,

borrow or transfer money.

EcoCash introduced EcoCash Save, a mobile-based savings service

that allows customers to save money and earn interest. Unlike

traditional banks which require multiple prerequisites for opening an

account, EcoCash Save does not require any documentation, opening

balance or maintenance fee. To operate the service, customers need

to transfer money from EcoCash Wallet to EcoCash Save account to

deposit the money and vice versa to withdraw the money.

Everything from account opening to deposits and withdrawals is

done via mobile. EcoCash also offer credit service, EcoCash Loans,

which provides low-value short-term zero collateral loans instantly

via mobile phone.

MEF AFRICA EDITION #2 7

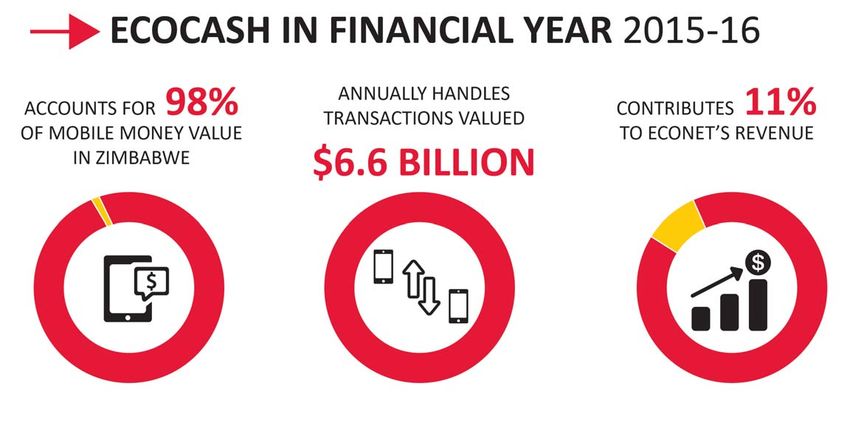

Taking that a step further, in 2015, Mahindra Comviva worked with Econet Wireless and MasterCard to issue debit cards to users of the EcoCash Wallet. It was the largest rollout of secure EMV Chip and PIN payment cards in Zimbabwe, and the first time that MasterCard debit cards were made available to consumers using mobile money services in Africa. The move brought unbanked consumers into the world of traditional payment services delivering multiple benefits. For example, it lets consumers pay conveniently at point-of-sale terminals in-store, withdraw cash at ATMs as well as shop online. Today, EcoCash is used by more than 5.795 million Zimbabweans according to a report from the telecoms regulator POTRAZ. In Econet’s 2015-16 financial report, EcoCash was recorded as having handled $6.6 billion worth of transactions. And now, The Reserve Bank of Zimbabwe has indicated that it wants cashless transactions to account for 80 per cent of all transactions by 2021. Currently, they represent 20 per cent. What’s interesting is how the EcoCash example has effectively expanded the mobile money model in two important directions. Firstly, it doesn’t just depend on the transfer of funds between individuals (or via an agent for cash-out) rather it includes bill and merchant payments as well as savings and borrowing, which extends the financial dynamics of the service and the benefits to its users. Moreover, the value-chain is greater than the sum of its parts, including consumers, agents, merchants, Econet Wireless and Steward Bank. Secondly, EcoCash has broken out of the singular approach of just Mahindra Comviva is now helping many operators to look beyond using a mobile device as the transaction bearer. By providing and payment and launch into insurance, loans, savings and so on. You linking bank-cards to each account holder, EcoCash extends the don’t need interoperability for these products to work and users love opportunity for users to buy goods online, withdraw cash at ATM’s or these services because they drastically reduce paperwork, and are buy goods via point-of-sale machines in stores. In other words the available to millions of people who would otherwise simply not be introduction of the EcoCash service is stimulating new areas of able to save or borrow. commerce in the country. MEF AFRICA EDITION #2 8

REGIONAL NEWS ROUND UP

FROM ACROSS SUB-SAHARAN AFRICA

IN PARTNERSHIP WITH APPSAFRICA ADVISORY

MOBILE MONEY

WHY VODACOM M-PESA FAILED IN SOUTH AFRICA

Despite its renowned success in East Africa, Vodacom is pulling the

plug on M-Pesa in South Africa with the country’s advanced banking

sector and a lack of

demand cited as key

reasons for the lack of

success of Vodacom’s

mobile money product MTN Money Wallet. The

M-Pesa, says a local agreement launches sub-Sa-

analyst. haran Africa’s first operator to

operator cross border remit-

Vodacom has announced tance channel.

that it plans to shut down

the service from June 30 “Our partnership is not only business to business, but also to country

2016. When M-Pesa first launched in South Africa in 2010, Vodacom to country,” Econet Wireless COO Fayaz King told the gathering at

targeted reaching 10 million local users. But only 76,000 users Meikles Hotel, where EcoCash general manager Natalie Jabang-

signed up in 2015 according to the company’s integrated we-Morris and Zambian counterpart Wane Ng’ambi of

report. This contrasts dramatically with Kenya where MTN officially signed the partnership.

mobile network Safaricom has over 11 million

M-Pesa users. “MEANWHILE According to Econet Wireless, someone in Zambia

will send money by registering with MTN

Around 75 per cent of South Africa’s adult

IN KENYA MOBILE Zambia and then initiating a money transfer

population is banked with traditional MONEY SERVICES ARE request via a USSD mobile Money short code,

financial institutions, according to a recent and selecting EcoCash (ZW) mobile number.

survey by the FinMark Trust. Meanwhile in

THE KEY FINANCIAL

Kenya mobile money services are the INCLUSION DRIVER. Econet Wireless CEO Doug Mboweni has

country’s main financial inclusion driver. indicated that the telecom giant plans to

Mobile money account ownership hovers at

MOBILE MONEY extends the service, saying Zimbabweans

around 60 per cent. South Africa also has a ACCOUNT OWNERSHIP from more countries with MTN footprint will

thriving money transfer market via retail soon be able to remit money directly into the

chains such as Checkers.

HOVERS AT receiver’s EcoCash wallet.

AROUND 60%.”

“Vodacom is fully committed to mitigating any

inconvenience to customers impacted by the decision

and assures all M-Pesa South Africa customers that their FINTECH START-UP ZOONA PROCESSES

funds remain safe and readily accessible,” said Vodacom CEO $1BN IN TRANSACTIONS

Shameel Joosub.

South African Fintech start-up Zoona has announced it has

processed over US$1 billion in money transfers, bill payments and

MTN & ECOCASH PARTNERSHIP ENABLES other financial services through its

WALLET-TO-WALLET TRANSFERS ACROSS network of entrepreneur agents.

BORDERS

The Zoona platform enables entrepre-

neurs to provide mobile money

EcoCash and MTN Zambia have officially unveiled a remittance services to unbanked or underbanked consumers, with its agents

partnership that will enable MTN customers in Zimbabwe’s northern serving more than one million customers every day across close to

neighbour to send money into the country via the mobile platform 1,500 locations in Zambia and Malawi.

MEF AFRICA EDITION #2 9

The start-up said its network of agents fulfils an important purpose FACEBOOK WAKES UP TO NIGERIA BUT IS FREE

in emerging markets where financial inclusion rates are low and there BASICS ENOUGH?

are few ways to safely

send and receive money.

In a partnership with Airtel, subscribers in Nigeria will be able to

“As an African business access all the services that are available through Free Basics without

that came up with an paying extra for data charges or rental. The service will launch in

African solution to an Nigeria with more than 85 free services dedicated to health,

African problem, we’re

thrilled to reach this

milestone. It’s a

vindication and vote of

confidence from our

consumers – who have chosen to trust us when sending and

receiving money. We are immeasurably grateful for this trust,” said

Lelemba Phiri, Zoona’s chief communication officer.

Phiri said the strength of the Zoona model rests in its over-the-coun-

ter approach, which means customers do not need to open an

account, complete any paperwork, or even have a mobile phone in

order to benefit from mobile money.

education, jobs, and finance. To date, Facebook estimates that its

connectivity efforts, which include Free Basics, have brought more

GHANA: MOBILE MONEY IN TRANSACTIONS HIT than 25 million people online who wouldn’t be otherwise.

GHC35.4BN (USD9BN)

With the cost of mobile data still an issue for subscribers Airtel Africa

will also be offering Facebook Flex in Nigeria, which allows people to

The penetration of mobile money in Ghana has seen an astronomical access a version of Facebook without data charges. According to

rise for the fourth year running with last year’s value of transaction Facebook, this initiative is part of their commitment to bringing

reaching GHC35.4billion, an increment of more than 216 percent over people online and reducing affordability barriers.

the previous year according to the Business & Financial Times.

Zuckerberg references Olalekan Elude, Ayodeji Adewunmi and

In 2014, the three telecom operators (Airtel, Tigo and MTN) engaged Opeyemi Awoyemi from Jobberman, a successful online recruitment

in mobile money processed transactions worth about GHC11.2billion platform. “Free Basics offers Nigerians, including 90 million people

across the country. Last year’s transactional value was recorded on who are currently offline, the opportunity to access services like

the back of more than 260 million transactions in a market that has Jobberman.”

since seen a new entrant in the form of Vodafone Cash, powered by

the mobile operator.

VODACOM BETS ON INTERNET OF THINGS.

CONTENT & SERVICES REVENUE FROM IOT GROWS 20.7 PER CENT TO

R556 MILLION

SOUTH AFRICA SET FOR MOBILE DATA BOOM Vodacom has over 2.2

million SIM cards in

"machines or things",

South Africa is set for a mobile data explosion, with mobile data

which are not mobile

traffic growing nine-fold at a compound annual growth rate of 55 per

phones, and the company

cent by 2020 according to the 10th Annual Cisco Visual Networking

sees big revenue potential

Index. The report relies upon independent analyst forecasts and

in this market as the

real-world mobile data usage studies. According to the report, in

Internet of things (IOT)

South Africa, 63 per cent of mobile connections will be ‘smart'

grows in South Africa.

connections by 2020, up from 22 per cent in 2015.

"I think we are going to be

Cisco notes mobile video will have the highest growth rate of any

surprised at the level of innovation that will come into play in the IOT

mobile application predicting video will be 73 per cent of mobile data

space," CEO Shameel Joosub told ITWeb in an interview after the

traffic by 2020, compared to 52 per cent at the end of 2015.

telecom operator's financial year-end results presentation in

Consumer and business users' demand for higher video resolution,

Johannesburg yesterday. Joosub says IOT is one of three new growth

more bandwidth and processing speed will increase the use of 4G

pillars Vodacom is focusing on to capture new revenue streams.

connected devices, it notes, adding 4G connectivity share is projected

to surpass 2G by 2018 and 3G by 2020.

"If you look at it today, you have 2.2 million SIMs in machines in

South Africa. That's just Vodacom's SIMs. If you take the entire

The report also anticipates machine-to-machine (M2M) traffic in SA

industry, it's probably around four million or five million SIMs and that

will grow 24-fold from 2015 to 2020 to account for 8% of total mobile

is growing at around 25 per cent a year, so it's a very rapidly

data traffic by 2020, compared to 3 per cent at the end of 2015.

expanding market," explains Joosub.

MEF AFRICA EDITION #2 10GHANA INITIATES REVIEW OF OTT SERVICES SHOWMAX LAUNCHES IN 36 AFRICAN

COUNTRIES

Ghana's National Communications Authority says it is reviewing the

country's OTT market with a plan to make decisions Internet video streaming service ShowMax has switched on its

for an enabling regulatory environment - not only service in 36 African countries since it launched in South Africa in

because of the impact on the revenue streams August 2015, months before rival US streaming service Netflix

of telecom operators that fulfil their tax switched on its global service in January this year.

obligations, but for national security concerns.

The Authority is concerned with the fact that ShowMax spokesperson Richard Boorman confirmed to Fin24 that

most of these OTT players are generally not the service is now live in 36 African countries ranging from Botswana

bound by regulations in many countries which in the south to Ethiopia and Djibouti in the north although is notably

orients market dynamics in their favour. not available in two of Africa’s biggest economies: Nigeria and Egypt.

It’s unclear if ShowMax has plans to launch in Nigeria, but Boorman

“OTT players are currently not under the purview of the telecom told Fin24 that the company is undergoing a “phased roll-out”.

regulations in the country as they are not registered or recognised

operating agencies under International Telecommunications Regula-

tions," the statement continues. "The lack of national regulations also

poses a threat to security and safety because of the very nature of

the communications sector.”

SOCIAL MEDIA SERVICES CUT IN ETHIOPIA

Applications including WhatsApp and Twitter have not worked in

parts of Ethiopia for more than a month due to a “blackout targeted

at mobile data connections”, according to local users speaking to

Bloomberg. The services, also including Facebook Messenger, have

been unavailable on the country’s sole mobile network Ethio Telecom,

claimed the publication’s sources.

Among the regions affected include Oromia, which recently suffered

fatal protests, leading to the death of 266 demonstrators according

to reports.

A Government spokesperson has reportedly said restricting access TERRAGON GROUP PARTNERS WITH BLIPPAR

isn’t a policy, and put the issue down to possible connection TO BRING AUGMENTED REALITY TO AFRICA

problems. However, Andualem Admassie, chief executive of

state-owned Ethio Telecom, reportedly told Ethiopia’s daily newspa-

per Capital that the government has the technology “to control” Under the terms of the deal Terragon will now offer a range of

messaging applications, earlier this month. Augmented Reality solutions to its customer base of pan-African

brands and businesses. Moreover, the AR technology enables

campaigns where consumers can view additional engaging branded

content on any object or surface by using the Blippar app in conjunc-

tion with a smartphone camera (Blipping) and visual tags on things

like magazine or outdoor advertising.

UBER LAUNCHES IN TWO NEW AFRICAN CITIES

To announce its AR capabilities, Terragon has launched a social media

campaign (#BlippNaija) urging consumers to download the app and

On-demand transportation service Uber has launched in two new Blipp a N1000 note (amongst other every-day objects) to access

locations, Abuja, Nigeria, and Mombasa, Kenya. This brings the amazing additional content and to share their experiences using the

company’s global #BlippNaija hashtag.

network to 400 cities

in 70 countries. The Temitope Esan, Product manager, AR, Terragon Group, said: “The

service launched in opportunities for AR are endless to any organization as it seeks to

Lagos in 2015, but is enhance our real world experience. By superimposing digital informa-

only now coming to tion on real life objects, individual customers are given a personalised

Nigeria’s capital city. and rich user experience that enables them to easily connect to a

brand’s offerings. With the use of AR, brands have an in-depth

“We’re really excited understanding of their

to be launching Uber customer behaviour that

in these two great will increase affinity, user

African cities, providing locals and visitors with a safe, affordable and engagement and interac-

flexible choice to move around their city.” said General Manager of tion with their various

Uber SSA, Alon Lits. product/service offering."

MEF AFRICA EDITION #2 11ESKIMI PROGRAMMATIC DSP PLATFORM VODACOM OVERTAKES MTN AS THE HIGHEST

LAUNCHES NEW DATA MANAGEMENT VALUED AFRICAN TELCO

CAPABILITY

According to Bloomberg data MTN's market cap was ZAR236 billion

Mobile media company, (USD15 billion), straggling behind Vodacom's ZAR248 billion worth. It's

Eskimi (which includes been a tough six months for MTN, which is still facing a $3.9 billion

the mobile social (ZAR59 billion) fine in Nigeria for missing a deadline to disconnect 5.1

network, Eskimi) has million unregistered SIM cards. MTN's share price has slumped almost

raised the bar for 33 per cent from ZAR190 a share to ZAR128.05. MTN's market cap

marketing quality in has lost ZAR114 billion since the fine was made public. Vodacom

Nigeria by introducing a however, seems to be going from strength to strength. The telco's

new local DMP - data stock has grown by 9.5 per cent year-to-date and almost 20 per cent

management platform - in the last 12 months.

which will allow

advertisers to target specific audiences instead of just sites and apps. In terms of subscriber numbers, MTN is still by far the biggest telco,

with 229 million subscribers across 22 operations in Africa and the

Currently the Eskimi DSP platform reaches more than 37 million active Middle East. As of 31 December, Vodacom had 65.2 million across its

users on Nigeria through more than 5 billion page impressions across five African operations.

19,000 mobile websites and apps. The addition of the new data

management capability allows advertisers to target much more

specifically so that a beer brand can target only alcohol consuming

audience or a mobile operator striving to reach high-value users, can

target only users who belong to the TOP 10 per cent of data

consumers for example.

Vytas Paukstys, CEO of Eskimi, commented: "We are launching a piece

of technology that was missing in the Nigerian market - local data

platform. This will allow advertisers to target very specific audience

instead of relying on their perception of certain sites or apps. An

advertiser can target by age, location and gender in sites and apps

where it was not possible before."

MOBILE OPERATOR NEWS

ORANGE INVESTS €75 MILLION IN AFRICA

INTERNET GROUP

Africa Internet Group, the largest e-commerce platform in Africa and

parent company of Jumia, has announced a partnership with Orange to

accelerate the growth of the

company and seize

development opportunities on

the continent.

In line with the partnership,

Orange – one of the leading

telecommunication operators

in Africa – will make a EUR75

million equity investment in Africa Internet Group. This follows hot the

heels of AXA’s 75 million euros investment for an 8 percent stake in

Africa Internet Group (AIG). Orange will become a shareholder of Africa

Internet Group alongside existing shareholders MTN, Rocket Internet,

Millicom, AXA and

Goldman Sachs.

Jumia has built a strong

presence in several key

African markets where

it will now be able to further improve its offering and customer

experience thanks to this partnership, in particular in key countries

such as Morocco and Egypt.

MEF AFRICA EDITION #2 12MARKET SNAPSHOT: MOBILE MESSAGING

USAGE IN NIGERIA AND SOUTH AFRICA

Just like the rest of the world, chat apps are rapidly evolving in parts of Africa to become the preferred platform for person-to-per-

son messaging. However, unlike the rest of the world, much of the continent has a majority legacy of feature phone users and

mobile infrastructure that is gradually upgrading to 3G and 4G speeds (a requirement for the use of chat apps).

MEF’s Mobile Messaging Report supported by Mblox launches later this month. The report is part of MEF’s Mobile Messaging

Programme: Future of Messaging which looks at combatting fraud and market development in A2P Messaging. Below we’ve

exclusively previewed some of the findings on the African countries included in the nine market study which looks at the consumer

attitudes and behaviours when in comes to mobile messaging.

It show how SMS compares against messaging apps with WhatsApp topping the usage charts in both countries with 82% in South

Africa and 73% in Nigeria. Facebook Messenger and SMS are also in the top three with Blackerry’s BBM remaining strong for now

at least in Nigeria (44%).

SMS dominates Application 2 Person messaging (A2P) – where businesses communicate with consumers. Mobile messaging is

widely adopted by enterprises in both markets for mission critical use cases like dialogue with banks, authenticating passwords

and so forth as well as a marketing channel for brands. In South Africa for example 38% have used SMS to confirm a password and

34% have used SMS to check their bank balance whilst in Nigeria its 49% and 42% respectively.

73%

NIGERIA – FAVOURITE MESSAGING SERVICES

62% 61%

47%

44%

22% 22%

17%

11% 10%

8% 7% 7% 8%

5%

2% 1% 1% 1% 0 1% 1% 2%

0 0 0

WHICH SERVICES & APPS DO YOU USE REGULARLY TO SEND OR RECEIVE DIRECT MESSAGES

WHICH ONE SERVICE OR APP DO YOU USE THE MOST

82%

SOUTH AFRICA – FAVOURITE MESSAGING SERVICES 69%

62%

54%

23%

20%

15%

10% 9% 11% 9%

7% 5%

3% 2% 3% 1% 1% 0 1% 0 1% 1%

0 0 0

WHICH SERVICES & APPS DO YOU USE REGULARLY TO SEND OR RECEIVE DIRECT MESSAGES

WHICH ONE SERVICE OR APP DO YOU USE THE MOST

MEF AFRICA EDITION #2 13YO YO

UR UR

YO EM YO EM

UR PL UR PL

SC O SC O

YE YE

H R H R

YO O O

O O

22%

26%

20%

24%

UR L YO L

O O

D R UR R

O D

MEF AFRICA EDITION #2

CT UN O UN

H O IV IV

YO E AL R/ ER YO H

CT

ER

SI EA OR SI

UR TH HO TY UR LT /H TY

BA CA SP BA H O

24%

26%

30%

20%

NK RE IT NK CA SP

AL RE IT

O PR O A

R R PR L

O AC OR O AC OR

TH TI OT TH

TI H TI OT

ER O E ER TI H

fiN NE R fiN O E

A R A

NE R

17%

R

10%

10%

14%

AN NC AN NC

IA I

A AI

R L A AI

RL

AL

CO LI IN CO IN IN

NE

M ,T

ST

IT M E, ST

IT

PA UT PA TA UT

NY AX NY

IO IO XI IO

N O N

A

YO R A

YO R

65%

50%

54%

U

32%

TR U TR

CO H CO H

M AV AI

N M AV AI

N

PA E CO PA E CO

NY O M NY O M

RD PA RD PA

CO ER CO ER

Nfi ED NY Nfi ED NY

7%

9%

8%

9%

RM SO RM SO

IN M IN M

G ET G ET

AN AN

H H

AP IN AP IN

A PO G A PO G

CO FR CO FR

SMS

M IN O M IN O

M M

SMS

PA TM PA TM

15%

21%

25%

20%

NY EN NY EN

T T

G

PR O G

PR O

O O R O O R

APP

M BO M BO

APP

VE O O

VE O O

RN TI KI RN TI KI

M NG NG M NG NG

EN G EN G

O O

11%

T T

12%

18%

12%

D O D O

D D

EP S EP S

O O

NIGERIA – ENTERPRISES USING A2P MESSAGING

AR AR

TM R TM R

SE SE

EN RV EN RV

T IC T IC

O O

R ES R ES

37%

LO LO

24%

29%

49%

CA CA

L L

SOUTH AFRICA - ENTERPRISES USING A2P MESSAGING

AU AU

A TH A TH

SP O SP O

O RI O RI

A RT TY A RT TY

7%

9%

W W

14%

S S

10%

EB O EB O

SI R SI R

TE SO TE SO

O CI O CI

R AL R AL

EM CL EM CL

AI UB AI UB

L L

14%

14%

15%

19%

SE SE

RV RV

IC IC

OR INSTITUTIONS - OR SENT OR RECEIVED A MESSAGE VIA ONE OF YOUR MESSAGING APPS?

E E

OR INSTITUTIONS - OR SENT OR RECEIVED A MESSAGE VIA ONE OF YOUR MESSAGING APPS?

PR PR

O O

VI VI

D D

ER ER

31%

41%

35%

25%

5%

8%

9%

IN THE LAST 12 MONTHS, HAVE YOU RECEIVED A TEXT MESSAGE (SMS) TO ONE THE FOLLOWING COMPANIES

14%

IN THE LAST 12 MONTHS, HAVE YOU RECEIVED A TEXT MESSAGE (SMS) TO ONE THE FOLLOWING COMPANIES

NO NO

NE NE

O O

F F

TH TH

ES ES

E E

8%

12%

18%

26%

14NIGERIA – A2P MESSAGING USE CASES

IN THE LAST 12 MONTHS HAVE YOU SENT AN SMS OR MESSAGE FROM WITHIN AN APP TO DO THE FOLLOWING?

SMS APP

45%

34%

33%

22% 22%

19%

17%

14%

7% 11%

7%

6% 6% 6%

MAKE A MAKE A MAKE A SET UP AN CONFIRM A CONFIRM OR CONFIRM A CHECK YOUR CHECK THE ORDER PROVIDING DONATE OTHER NONE OF

CHARITY PAYMENT TO PAYMENT TO ACCOUNT PASSWORD CANCEL A CREDIT CARD BANK STATUS OF A GOODS AND INFORMATION INTERNET TIME THESE

DONATION FRIENDS & A COMPANY BOOKING TRANSACTION BALANCE OR BUS, TAXI, SERVICES TO A TO FRIENDS

FAMILY CREDIT LIMIT AIRLINE COMPANY OR FAMILY

SOUTH AFRICA – A2P MESSAGING USE CASES

IN THE LAST 12 MONTHS HAVE YOU SENT AN SMS OR MESSAGE FROM WITHIN AN APP TO DO THE FOLLOWING?

SMS APP

36%

29%

27%

28%

15%

11% 13%

11% 8% 9%

9% 9%

6%

5%

MAKE A MAKE A MAKE A SET UP AN CONFIRM A CONFIRM OR CONFIRM A CHECK YOUR CHECK THE ORDER PROVIDING DONATE OTHER NONE OF

CHARITY PAYMENT TO PAYMENT TO ACCOUNT PASSWORD CANCEL A CREDIT CARD BANK STATUS OF A GOODS AND INFORMATION INTERNET TIME THESE

DONATION FRIENDS & A COMPANY BOOKING TRANSACTION BALANCE OR BUS, TAXI, SERVICES TO A TO FRIENDS

FAMILY CREDIT LIMIT AIRLINE COMPANY OR FAMILY

NETWORK MARKET ENTERPRISE CONSUMER

A2P MESSAGING THE FUTURE OF MOBILE MESSAGING:

FRAUD FRAMEWORK

VERSION 1.0 A CROSS-ECOSYSTEM APPROACH

MEF AFRICA EDITION #2 15EVERYTHING YOU NEED TO KNOW ABOUT…

THE NCC CONSULTATION FOR THE PROVISION

OF VALUE ADDED SERVICES IN NIGERIA

I

n March 2016 the Nigerian Communications Commission (NCC)

published a consultation paper on the Procedures and Guidelines

for the future provision of Value Added Services in Nigeria. Its

goal is to make sure that consumers are properly protected.

The proposals were broad, impacting all stakeholders directly and

included the introduction of a new structure for the VAS value chain,

new revenue models, proposals related specifically to the activities of

the mobile operators as well as attempts to address the issue of

unauthorised billing and delivery of unsolicited SMS, which is

currently a big problem in Nigeria.

MEF has been supporting its members with a response to the

consultation, highlighting best practice and experiences from other

markets. It recommends that positive engagement and full industry

collaboration is the best way to proceed with any new regulation in

order to create an effective regulatory regime that will protect

consumers from harm, but one that will also enable the market to

continue to develop and grow, to the benefit of the wider Nigerian

economy.

Here, we take a deeper look at the proposal which could have a

significant impact on future mobile ecosystem in this key African

market.

BACKGROUND TO THE CONSULTATION

The NCC was established by the Nigerian Federal Government as an

independent regulatory authority for the telecommunications

industry in Nigeria. The Nigerian Communications Act (NCA) also

confers on the NCC the responsibility to control and regulate other

related services offered in addition to the basic voice

communications; these include data services, Internet and other

value added services.

The NCC has up to this time allowed the value added services

industry to develop without any encumbrance or significant

regulatory interference. The VAS industry in Nigeria has grown into a

multi-billion Naira industry and become an enabling tool for

facilitating efficient operations in other sectors of the economy.

The Commission cites having received several complaints from the

public in respect of service providers who use short codes assigned

for value added services to perpetuate fraud, the menace of

unsolicited text messages that flood customers’ phones, fake bank

credit alerts and anti-competitive activities.

As such the Commission is now of the opinion that it is time to

regulate the industry in order to protect, balance and reconcile

stakeholders’ interests and has developed a set of regulatory

guidelines and opened a public consultation.

MOBILE EDITION

MEF AFRICA MONEY eBULLETIN

#2 #3 16PROPOSED GUIDELINES

The consultation includes three key areas and covers a wide range of proposals that have a direct impact

on the providers of VAS services as well as mobile messaging.

1. Regulatory Guidelines

2. Technical Guidelines

3. Draft VAS Hosting Service license

The consultation includes proposals on:

• A new market structure consisting of three parties within the VAS value chain namely:

1) VAS and content developers [owners of franchise and copyright on applications and content]

2) VAS hosting service providers [providers of software and hardware platforms for hosting VAS

and providing transmission links to network operators]

3) Network operators [providers of connections to end users for VAS connection]

• Specific functions and responsibilities assigned to each party as well as restrictions on the

provision of certain types of services by some parties [e.g. only operators are allowed to provide

ringtones, callback ringtones, Cell-ID dependant locations based services.

• Separation of mobile subscribers’ voice, data and VAS accounts. For pre-pay customers which is

most of the Nigerian subscriber base, this means that consumers have to decide at the point of

topping up how much of their top up is allocated to voice, data and VAS

• The requirement that both the sender and provider (aggregator) must be identified within bulk SMS

• Unbundling of the product selling price and weighted segmentation of different components that

make up a total selling price, e.g., development costs = 40%, distribution costs = 10%, branding &

advertising = 15% etc

• New VAS franchise/distribution models and revenue collection models

• Development of a code of practice for consumers which would cover service information,

complaints handling, T&Cs etc.

CONSULTATION PAPER PUBLISHED 15/16 MARCH 2016

MEF RESPONDED ON BEHALF OF MEMBERS 6 APRIL 2016

NCC HELD AN INDUSTRY STAKEHOLDER MEETING ON 27 APRIL 2016

FURTHER UPDATES ON THE CONSULTATION ARE NOW AWAITED

MOBILE EDITION

MEF AFRICA MONEY eBULLETIN

#2 #3 17STATS THAT OUTLINE

THE MARKET DRIVERS

IN THE REGION

HERE WE LOOK AT THE STATS BEHIND THE HEADLINES THAT INDICATE

SOME OF THE KEY MARKET DRIVERS ACROSS AFRICA.

1 MOBILE DATA REVENUE IN AFRICA IS EXPECTED TO

DOUBLE BY 2019, FROM ABOUT $11 BILLION 2014

TO $22 BILLION ACCORDING TO REPORT LINKER.

2 CISCO’S TENTH ANNUAL VISUAL NETWORKING

INDEX SUGGESTS THAT SOUTH AFRICA IS SET FOR

A MOBILE DATA EXPLOSION,

WITH TRAFFIC GROWING 7 THE AVERAGE SELLING PRICE OF SMARTPHONES

NINE-FOLD AT A COMPOUND HAS FALLEN SIGNIFICANTLY ACROSS AFRICA

ANNUAL GROWTH RATE OF WITH MORE DEVICES NOW AVAILABLE IN THE

55% BY 2020. SUB-$100 PRICE RANGE. YET, ACCORDING TO THE

GSMA DESPITE THIS SHIFT, NEARLY 450 MILLION

3 THE SAME REPORT INDICATES THAT 63% OF CONNECTIONS WILL STILL BE BASED ON FEATURE

MOBILE CONNECTIONS WILL BE ‘SMART' CONNEC- PHONES BY 2020.

TIONS BY 2020, UP FROM 22% IN 2015.

8 THE TOP FIVE AFRICAN COUNTRIES BY INTERNET

4 THERE IS AN ESTIMATED 800 MILLION INHABIT- USE (IN MILLIONS) ARE:

ANTS IN SUB-SAHARAN AFRICAN AND 386 MILLION NIGERIA - 97.21 (POPULATION 173.6M)

MOBILE SUBSCRIPTIONS TRANSLATING TO A POPULA- EGYPT – 48.3 (POPULATION 82.6M)

TION PENETRATION RATE OF 41% AND AN ANNUAL KENYA – 31.99 (POPULATION 44.35M)

SUBSCRIBER GROWTH RATE OF 14% ACCORDING TO SOUTH AFRICA – 26.84 (POPULATION 52.98M)

DETECON CONSULTING. MOROCCO – 20.21 (POPULATION 33.01M)

5 IN TERMS OF HANDSET SHIPMENTS TO THE END OF 9 DATA FROM THE CENTRAL BANK OF KENYA

2015, AFRICA AND THE MIDDLE EAST ACCOUNTED SHOWS THAT MOBILE MONEY TRANSFER SERVICE

FOR AN 11% SHARE OF THE GLOBAL HANDSET PROVIDERS MOVED CLOSE TO

MARKET - THE SECOND BIGGEST REGION GLOBALLY 2 TRILLION KENYAN

BEHIND ASIA PACIFIC AND A TRAJECTORY THAT SHILLINGS ($23 BILLION)

STRATEGY ANALYTICS PREDICTS WILL CONTINUE VIA 733 MILLION

THROUGHOUT 2016. TRANSACTIONS LAST

YEAR. THAT WAS UP

6 ANALYSYS MASON FORECASTS THAT SMART- FROM 579 MILLION

PHONES WILL ACCOUNT FOR 63% OF ALL HAND- TRANSACTIONS WORTH 1.5

SET SALES IN SUB-SAHARAN AFRICA BY 2020. TRILLION SHILLINGS IN 2012.

MOBILE EDITION

MEF AFRICA MONEY eBULLETIN

#2 #3 1810 THIS IMF REPORT ON KENYA, INDICATES THAT

MOBILE MONEY PROVIDER

M-PESA HAS A PENETRATION

RATE OF 985 REGISTERED

MOBILE MONEY ACCOUNTS PER

1,000 PEOPLE CREATING

EMPLOYMENT FOR SOME 80,000 AGENTS.

11 ERICSSON’S STUDY ‘FINANCIAL SERVICES FOR

EVERYONE’ FOUND THAT MORE

THAN HALF OF

CONSUMERS IN SUB-SAHARAN

AFRICA ARE USING MOBILE MONEY

SERVICES THROUGH AN AGENT.

12 ACCORDING TO CISCO VIDEO WILL HAVE THE

HIGHEST GROWTH RATE OF ANY MOBILE SERVICES.

IN SOUTH AFRICA FOR EXAMPLE, VIDEO WILL BE 73%

OF MOBILE DATA TRAFFIC BY 2020, COMPARED TO

52% AT THE END OF 2015.

13 NIGERIANS ARE CONSUMING MORE OF THEIR TV

AND VIDEO CONTENT ON MOBILE DEVICES THAN

EVER BEFORE ACCORDING TO ERICSSON CONSUMER-

LAB’S TV AND MEDIA REPORT FOR NIGERIA. THE

SHARE OF TIME SPENT WATCHING VIDEO

BREAKS DOWN AS: TV (36%) PC (25%)

SMARTPHONE (26%) TABLET (13%). TAKEN

TOGETHER SMARTPHONE AND TABLET

OUTWEIGH ANY OTHER CATEGORY.

14 IN 2014, 100 MILLION PEOPLE

WERE USING FACEBOOK EACH

MONTH ACROSS AFRICA, WITH OVER

80% DOING IT VIA MOBILE. BY THE END OF

2015 THAT FIGURE HAD JUMPED TO OVER

120 MILLION. 4.5 MILLION OF THOSE

FACEBOOK USERS ARE BASED IN KENYA, 15 MILLION IN

NIGERIA AND 12 MILLION IN SOUTH AFRICA, IN STATIS-

TICS REPORTED BY REUTERS.

15 SOUTH AFRICAN INTERNET USERS SPEND 24.7% OF

THEIR INCOME ON MOBILE SERVICES (DATA AND

VOICE). ELSEWHERE, THE THREE MOST EXPENSIVE

COUNTRIES IN TERMS OF MOBILE SERVICES SPEND

VERSUS AVERAGE MONTHLY INCOME ARE:

MALAWI – 56.29%

MADAGASCAR – 52.55%

CENTRAL AFRICAN REPUBLIC – 51.63%

MOBILE EDITION

MEF AFRICA MONEY eBULLETIN

#2 #3 19ABOUT HUAWEI

Huawei is a leading global information and communications technology (ICT) solutions provider. Our aim is to enrich life and improve

efficiency through a better connected world, acting as a responsible corporate citizen, innovative enabler for the information society,

and collaborative contributor to the industry. Driven by customer-centric innovation and open partnerships, Huawei has established

an end-to-end ICT solutions portfolio that gives customers competitive advantages in telecom and enterprise networks, devices and

cloud computing. Huawei’s 170,000 employees worldwide are committed to creating maximum value for telecom operators,

enterprises and consumers. Our innovative ICT solutions, products and services are used in more than 170 countries and regions,

serving over one-third of the world’s population. Founded in 1987, Huawei is a private company fully owned by its employees.

For more information, please visit www.huawei.com

ABOUT MAHINDRA COMVIVA

Mahindra Comviva is the global leader in providing mobility solutions. It is a subsidiary of Tech Mahindra and a part of the USD

16.5 billion Mahindra Group. With an extensive portfolio spanning mobile finance, content, infotainment, messaging and mobile

data solutions, Mahindra Comviva enables service providers to enhance customer experience, rationalize costs and accelerate

revenue growth. Its mobility solutions are deployed by over 130 mobile service providers and financial institutions in over 90

countries, transforming the lives of over a billion people across the world.

For more information, please visit www.mahindracomviva.com

ABOUT APPSAFRICA ADVISORY

Appsafrica Advisory develops strategies and drives expansion for companies

entering or expanding in Sub-Saharan Africa. We are a private advisory service

providing expert insight, business development and implementation assistance

for mobile web and technology ventures.

For more information, please visit www.appsafrica.com

MOBILE EDITION

MEF AFRICA MONEY eBULLETIN

#2 #3 20MOBILEECOSYSTEMFORUM.COM MEF MOBILE MONEY eBULLETIN #3 16

You can also read