Econ & Asset Allocation - February 2022 monthly outlook Theodore Roosevelt - ktbst

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Econ & Asset Allocation

February 2022 monthly outlook

Theodore Roosevelt

1

Summary : February monthly outlook

Policy Tightening &

Sector/Style rotation Valuation bargaining

Geopolitical shift Due to the global macroeconomics risk

FOMC tried to tighten their monetary policies to combat From KTBST perspective, We saw a great

the rising in inflation while the market already accept the overwhelming, Investment tends to reduce their discount in DM equities especially the US, EU

view that FED will raise their policy rate but the timing market risk and duration of the portfolio by adding due to the rate hike immunity with 2022

and size still blur while the QT projection has been value and financial sector into their portfolio, impressive growth outlook while the recent

mumbling around the market while in EM like KR still got However, the primary concern for most investors correction gave investors the opportunity to

pressure from macroeconomics like domestic rate hike is not how much the company will grow but the enhance portfolio in short term before FOMC

and political dreadlock which also depress Japan stock downside it is. However, we believed that in March 2022 meeting

market due to increases in the regional correlation short-term valuation pressure in semiconductor

between 2 countries will toned down after KR election

2

Macro factor : Quantitative Tightening conclusion

According to the Fed meeting in December, Some committees decided to implement Quantitative

tightening in this year after the policy rate hike.

The quantitative tightening is highly possible in this year because the most of FOMC

members is hawkish stance, the rotation members in February, supported the unease policy.

If the Fed provide the signal before the QT action like tapering in July 2021, Fed tend

to start the balance sheet runoff in June or July 2022

The risky assets in period of lasted QT is highly volatility; however, the higher volatility does not

mean the risky assets have underperformed or turned to negative return.

3

The cycle of monetary policy and this time will different

The types of monetary policy

The current status of monetary policy tools

10 4 QT +

million

9 QE + Rate cut Tapering Rate hike Rate

3.5

hike

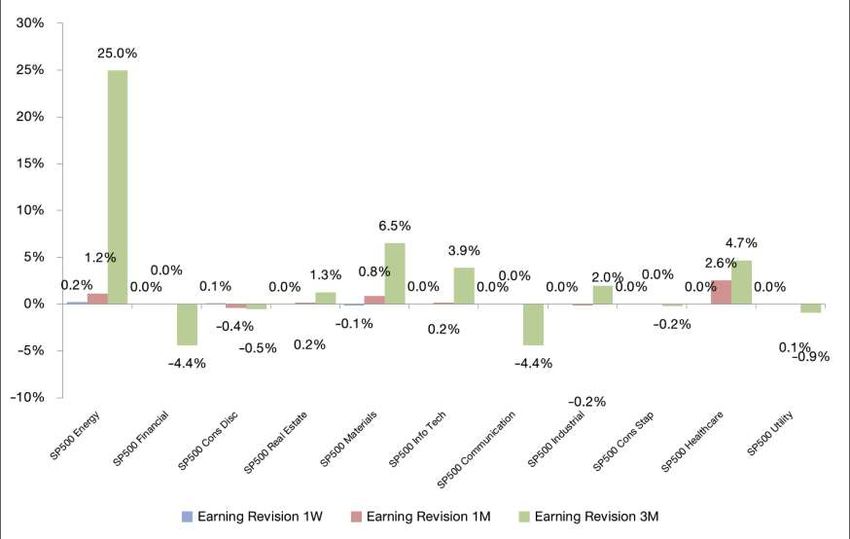

The historical period of time for each policies

8

3

7

6 2.5

5 2

3 years year years year

4 1.5

3

1

2

1 0.5 Easing is around years Tightening is around years

0 0

FED balance sheet mln USD (LHS) Effective FED fund rate (RHS)

to combine the three types in the

4

FOMC Rotation to be more hawkish

2021 Committee Members 2022 Committee Members Hawk vs Dove meter

Jerome H. Powel John C. Williams Jerome H. Powel John C. Williams

Board of Governors New York Board of Governors New York

Michelle W. Bowman Thomas I. Barkin Michelle W. Bowman James Bullard Old

Board of Governors Richmond Board of Governors St. Louis rosters 2 1 1

2021

Lael Brainard Raphael W. Bostic Lael Brainard Esther L. George

Board of Governors Atlanta Board of Governors Kansas City

Richard H. Clarida Mary C. Daly Christopher J. Waller Loretta J. Mester New

Board of Governors San Francisco Board of Governors Cleveland rosters 1 3

2022

Randal K. Quarles Charles L. Evans Kenneth Montgomery

Board of Governors Chicago Boston

0% 50% 100%

Christopher J. Waller

Board of Governors

Dove Neutral Hawk

5

Quantitative Tightening brings volatility to the markets but at what cost?

The financial market is highest volatility in Tapering period and before QT implemented (Annualized)

100%

88.10%

80%

60%

40%

18.64% 15.55% 16.94% 17.02% 15.00% 16.65%

20% 15.47% 13.11% 15.48% 12.96% 14.80%

9.57%

0.82% 0.56% 0.00%

0%

MSCI DM MSCI ACWI MSCI EM NASDAQ S&P500 10Y BTC Index Gold

QE until tapering end period (+-1Y) 1st Hike period (+-1Y) 2nd hike until QT (+-1Y) QT period (+-1Y)

The volatility of risky assets surge when the QE injection move to tapering and balance sheet runoff period, so the central bank is going to use the

tapering and QT in this year, the financial market will be shaken and will be disturbed. The question for the policy makers in this round is..

When the QT is started

What a pace of QT per month?

How do they do the QT Autonomy and discretionary in policies

.What asset types do they choose in this period?

6

Quantitative Tightening expectation

ONE YEAR JUL AUG SEP OCT NOV DEC JAN FEB MAR APR MAY JUN JUL Fed balance sheet unit : million USD

10

million

2021 Tapering Signal

9

2021 2022 8

Tapering Action 7 Start QT

2021 QT Signal 6

First signal for QT

5

2022 1st rate hike

4

3

Signal to halt QT May

2022 QT Action 2 Ends QT

expectation 1 July

0

According to the J. Yellen era, the forward guidance to the

market is around 9 12 months before action. The tapering signal for this

period was announced 3 months before action, so we expected that the Other

proper period for is around June or July this Securities, unamortized premiums and discounts, repurchase agreements, and loans

Coin

year while the size of QT is expected to be around 100 billion USD

Special drawing rights certificate account

capped per month with gradually increasing in the monthly pace Gold certificate account

7

Quantitative Tightening process

Fed has never reached QT ceiling as it announced unit : million USD

60

In practice, Fed has never implemented QT

thousands

equal to the announced target The reasons are..

40

The U.S. treasury bills that were expiring below the

20 ceiling of Quantitative tightening

0

The maturity of U.S. treasury bills and Mortgage-

-20

backed securities expired at the same time (Red frame),

the expectation of the Fed is that long-term bonds

-40 maturity is the point of time to scale down the balance

sheet.

-60

The economic situation is one of the main factor to

-80

conduct the QT implementation, e.g. the trade war in

Monthly Actual QT 3 Month rolling QT QT Cap 2018-2019 pressured the central bank to halted the

-100

tightening policy and Fed turned the money back to

economic system again (Green frame)

8

QT 2022 ≠

If Fed is going to implement QT the same portion to , the overall The portion of assets in

volume is twice the previous round (Unit : million USD)

1500 1,366.46

Thousands

US treasury

1000 securities 1 to 5 Y

694.73 MBS10Y

500 US treasury

securities 5 to 10

Y

0 US treasury

securities over 10 Y

QT 2022 QT 2018

The likelihood of double QT per 2022 Fed US treasury US treasury

US treasury securities 1 to 5 Y MBS10Y

month increases due to the size of balance sheet securities 5 to securities over

balance sheet doubled recently US treasury

which expected QT per month will securities 5

2017 Fed US treasury

be capped around 100 bln. USD balance sheet US treasury securities 1 to 5 Y MBS10Y

securities over 10 Y

at least

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

9

Fed turn to hawkish stance as expected

2022 2023

KTBST Economics forecast

KTBST Cons Prev. KTBST Cons Prev.

US 2.9 2.1 2.3 2

Inflation

Base Case

TH 1.1 1.2 1.7 1.3

Policy rate

US 1.00 0.35 0.25 . 0.85 0.5

TH 0.6 0.5 n.m. 0.75

US 2.9 2.1 2.3 2

Inflation

Hawkish Case

TH 1.1 1.2 1.7 1.3

Policy rate

US 1.25 0.35 0.75 2. 0.85 .25

TH 0.6 0.5 n.m. 0.75

US 2.0 2.9 2.1 2.4 2.3 2

Inflation

Pandemic Case

TH 0.8 1.1 1.2 1.3 1.7 1.3

Policy rate

US 0. 5 0.35 0.25 0.75 0.85 0.5

TH 0.5 0.6 0.5 0. n.m. 0.75

10The financial market impact

10Y change (every

Trade war Change in BL (every Change in Rate (every

Easing regime Tapering 100bps from 10 R2

Tweet 1% change) 100bps) The Vector autoregressive model

weeks before)

MSCI DM

MSCI ACWI

about QE or Tapering and the negative impact of

MSCI EM rising in 10 years bond yield is not statistically

NASDAQ significant (Blue table)

S&P 500 The transition period of monetary policy to

10Y n.m. tightening stance (QT in pink table), the financial

BTC index market was more fragile to the QT

Gold announcement at least seven weeks before

QT (7 weeks Change in Rate (every 10Y change (every action, especially in the technology sector,

Trade war Change in BL (every

Tightening regime before 100bps from 1 week 100bps from 7 weeks R2 Crypto currency and gold price.

Tweet 1% change)

implement) before) before)

MSCI DM *: QT lag period for 10Y = 6 weeks , BTC = 16 weeks , Gold 7

MSCI ACWI weeks | ** : 10Y lag period for BTC = 3 weeks , Gold = no lag

MSCI EM

NASDAQ Sig. at the 99% confidence level

S&P 500 Sig. at the 95% confidence level

10Y* n.m. Sig. at the 90% confidence level

BTC*,**

Gold*,**

11QT will pressure market all along?

Mater.

1000.00%

Health

Return

Util. Health Ener.

Mater. IT

Com Ser. Con Sta. Indus. Fin.

tightening, the stock that high net profit

Fin. Indus. Con Dis. IT margin usually outperform the market. So,

Con Dis. the signal of QT period is proper to invest

Util.

1.00%

-10.00% -5.00% 0.00% 5.00% 10.00% 15.00% 20.00% 25.00% 30.00% 35.00% 40.00% in the high net profit margin stock.

EPS Growth MSCI ACWI (Technology sector has 21%) In terms of

1Y Before 1Y After Linear (1Y After) the EPS, the QT period is not statically

different to normal periods.

MSCI ACWI Growth MSCI ACWI Value

24.25% 1Y before implement 51.87% The recommendation for short-term

33.16% 6M before implement 25.49% investment is carefully to the first policy

34.41% 3M before implement 32.12% rate hike, and then we are going to

18.90% 3M after implement 26.84% overweight the technology sector in the

16.14% 6M after implement 20.57% second half of the year.

17.96% 1Y after implement 20.51%

18.13% current (17/01/2022) 17.94%

Source: KTBST

40.00% 30.00% 20.00% 10.00% 0.00% 0.00% 10.00% 20.00% 30.00% 40.00% 50.00% 60.00%

12Focus on the 1st rate hike and yield curve structure for the signal.

UST 10 years prediction for

4%

3.25%

3% 2.64%

2.13%

2% 2.57%

1.16% 2.15%

1.82%

1%

1.25% 1.18%

0%

Policy rate 3M 3Y 5Y 10Y

QT

4 rate hike without QT implemented 4 rate hike with QT implementedQT

we used the data mining to analyze the U.S. treasury bond, we found the steepening curve of UST 10 years in the rate hike cycle. On the other

hand, the UST yield curve tend to flattening, when the Fed is hiking the policy rate and running off the balance sheet together. For 2 assumptions above, we

predicted the U.S. treasury yield rate is reaching 3.25% in near term. Consequently, the growth stocks of emerging country stocks are pressuring in the first

half of this year. In contrast, The Fed is going to raise the policy rate 4 times and implement quantitative tightening that flattening the yield curve and

creating the volatility in bond market. Our base case scenarios, the U.S. treasury yield range is between 2.57% - 3.25% and the central bank will closely

manage the yield curve expectation.

13The stock markets tend to bottom-out after 1st rate hike

MSCI DM (LHS) Effective FED fund rate (RHS) 10Y Effective FED fund rate (RHS)

2400 2 6 2

5

2000 1.5 1.5

4

1600 1 3 1

2

1200 0.5 0.5

1

800 0 0 0

S&P500 (LHS) Effective FED fund rate (RHS) Gold Effective FED fund rate (RHS)

3300 2 2300 2

2800

1.5 1.5

1800

2300

1 1

1800

1300

0.5 0.5

1300

800 0 800 0

14And keep your finger crossed that FED will not do any policies mistakenly.

Recession probabilities with yield spread will increasing while the model with economics indicators still low

100%

80%

60%

40%

20%

0%

Recession Period Recession Prob of Yield Curve (RHS)

Recession Prob of Economic indicator (RHS)

15Asset classes perspective provide higher upside due to the recent correction.

2022 CME return changed update with correction from market discount turned DM more attractive

20

15

10

5

0

-5

Global DM EM US EU JP CN KR IN TH

Rf Inflation Growth Valuation Discount from YTD2022 correction

16Asset classes perspective provide higher upside due to the recent correction.

New expected return after YTD2022 correction

30

25

20

15

10

5

0

Global DM EM US EU JP CN KR IN TH

2022 previous CME expected return 2022 CME expected return after correction

17All of the markets crashed at the same time while investors mood covered in fear

Better risk adjusted return after correction to grab opportunity in tactical allocation

24

2022 previous CME expected return

22

20 2022 CME expected return after correction

Annualized Expected volatility

18

16

14

12

10

3 8 13 18 23 28

Annualized expected return

18Tightening playbook

Numbers

Scenario of rate Scale of QT Period of Method Assets

Assets impacted

s hike million USD QT of QT for QT

(times)

before the QT A B C D E

action

A 1H23

years

Maturity

DM Equities

B 694,726 2H22

2 years EM Equities

All assets

Maturity

C 2H22

2 years

sell off

assets

Growth stock

Value stock

D 4 1H22

2 years Bond

Alternative asset

1H22 Maturity

E >

2 years sell off

assets

Positive return Negative return

19Quantitative Tightening TAA roadmap

Hold equity > fixed income

March June Hold equity < fixed income

START

1 2

First rate hike, recommend Second rate hike, start to invest in DM

DM value growth/EM

September July

4 3

Third rate hike, recommend DM First QT action, move to Barbell Growth/Value

Growth/EM > Value portfolio

December Emergency cases

5 6

Fourth rate hike, recommend DM Growth/EM > Value For Yield curve is Flattening, recommend underweight

equity and hold cash at least % of portfolio

20South Korea election and stock market

National level election

Presidential elections : select the president (every five years)

• Directly elected by all citizens over the age of 18

• Plurality voting : candidate who got the most vote

are elected

• Five-year term

• Which will take place on 9 March 2022

Legislative elections : select the National Assembly (every four years) 300 members elected for a four-year term

• 253 constituency seats come from first-past-

the-post method

• 47 proportional representation seats

o 17 members come from parallel voting

method

o 30 members come from additional

• Democratic (172) • Independent (6) • Transition Korea (1)

member system

• People Power (106) • People (3) • Vacant (5)

• Justice (6) • Basic Income (1)

21List of Republic of Korea presidents

40000 5000

4500

35000

4000

30000 Moon Jae-in

Chun Doo-hwan Roh Moo-hyun Lee Myung-bak 3500

Kim Young-sam

25000

3000

Kim Dae-jung Park Geun-hye

20000 2500

2000

15000

1500

10000 election

Roh Tae-woo 1000

NIKKEI

5000

500

KOSPI

0 0

• There are only two major party in South Korea which alternately gain executive power since 1980. However, it does not imply that the president also have the legislative

power in their hand.

• There is an evidence shown the improvement of correlation between Japan stock market and Korea stock market. Besides U.S.-China trade war during 2018 there is a

conflict between Japan and Korea as well. So, we need to pay attention on the foreign policy in Japan-South Korea relations from both candidates since it could affect

the performance of both markets.

22The 20th Republic of Korea presidential election : Candidate

-myung

Yoon Seok-youl

Lee Jae-myung

People Power Party Ticket

Democratic Party Ticket

23The 20th Republic of Korea presidential election : Campaign

Foreign Consumption Industry Capital market

• Try to balance South • Raise housing supply by • Subsidize a new economy • Aim to push forward Korea

Korea-U.S. alliance 2.5 million units business stock to weight in MSCI

(security partner) and

• Deduct pre-sale ceiling • Great Digital DM instead of MSCI EM

South Korea-China

price of housing pre-sale Transformation : build • Reform Korea s equity

alliance (trade partner)

• Universal basic income data infrastructure and market

• Mainly focus on inter- expand digital space (AI,

(UBI) : KRW 1 million per

Korean cooperation than quantum technology,

person per annual / KRW 2

denuclearization of North cybersecurity,

million per person per

Korea blockchain,

Lee Jae-myung annual ( 19 -29 years old)

• Recently, Lee Jae-Myung supercomputing and

Democratic Party Ticket

met Japan ambassador semiconductors)

and ask for meeting with • Focus on a carbon

Kishida emissions tax

24The 20th Republic of Korea presidential election : Campaign

Foreign Consumption Industry Capital market

• Mainly focus on • Reduce property • Support start-ups and • Has not announced

suppress the ownership tax and real ease some restrictions to

nuclearization of North estate sales tax support the growth of

Korea by international small business

cooperation • Build housing supply by

2.5 million units • Offer tax incentives

• Enhance relationship with

United States • Help small business who

suffer from pandemic

• Increase LTV ratio to 80

Yoon Seok-youl

percent for younger age

People Power Party Ticket

groups

25The 20th Republic of Korea presidential election : Opinion polling

Yoon Seok-youl

People Power Party Ticket

Lee Jae-myung

Democratic Party Ticket

26How stock market repones with the election

15 Opinion poll Spread

Lee Jae-myung

10

Democratic Party Ticket

5 LEAD

0

-5

-10 Yoon Seok-youl

-15 People Power Party Ticket

-20

LEAD

10/21 11/21 11/21 11/21 12/21 12/21 12/21 01/22 01/22 01/22 02/22

3050 Capital Market Aspect

3000 • Lee Jae-myung pledge may favor Korean

2950

2900

stock market more

2850 • According to Goldman Sachs Global

2800

2750

2700

equity to MSCI DM index could increase new

2650 capital inflows around $54 billions

2600

2550

KOSPI

27How stock market repones with the election

32.40%

Korean stock performance during election Throughout 8 president elections

30.00% 24.08% 23.80%

22.21%

18.50% 18.84% since 1980, equity rose just 5 out

20.00%

11.03% 10.90%

7.81%

of 8 ahead 1-month period.

6.33% 6.55%

10.00% 3.35% 5.63% 6.12% 3.29% 4.14% 2.43% 0.11% 2.13%

4.94% 3.09% 4.62%

0.72% 0.14% 0.29% 2.31% 0.89%

0.88%

0.00%

-3.41% -2.49% -2.54% -1.69% -0.93% -0.86% -0.19% -0.54% -0.26% -0.73%

-10.00% -5.25% -3.42% -5.26% -6.81%

-10.36% -10.54%

-20.00% -15.40% -14.65%

-30.00% -23.61%

-40.00% -39.28%

3M before 1M before 1W before 1W after 1M after 3M after

25-Feb-1981 16-Dec-1987 18-Dec-1992 18-Dec-1997 19-Dec-2002 19-Dec-2007 19-Dec-2012 9-May-2017

Throughout 8 president elections

30.00%

Korean VS MSCI EM performance during election 23.67% since 1980, Korean equity mostly

20.00% 16.58%

18.26%

overperform EM over 1-week period.

10.00% 8.02%

4.14% 4.17% 2.90% 4.11% 3.07% 3.60%

1.37% 2.37% 1.76% 1.30%

0.43% 0.03% 0.00%

0.00%

-0.86% -1.01% -0.58% -0.36%

-5.59% -2.12% -2.93% -2.33%

-5.37% -4.67% -4.58% -4.20% -4.54%

-10.00% -6.03%

-9.67% -11.02%

-14.48%

-20.00% -16.05%

-19.81%

3M before 1M before 1W before 1W after 1M after 3M after

18-Dec-1992 18-Dec-1997 19-Dec-2002 19-Dec-2007 19-Dec-2012 9-May-2017

28Future of Korea government

Lee Jae-myung • Majority of National Assembly of the Republic • It may take time to pass the bills since most Yoon Seok-youl

Democratic Party of Korea come from Democratic Party. If Lee of seats belong to Democratic Party. Korea People Power Party

Jae-myung become the next president, there stock market may not get benefit in the

will be more chance of supporting from the aspect of fiscal policy support.

fiscal side which may benefit the stock • Have to wait until the next election of

market. National Assembly of the Republic of Korea

to unlock political dreadlock.

POLITICAL GROUPS Government (172) Government (172)

POLITICAL GROUPS

• Democratic (172) • Democratic (172)

Opposition (117) Opposition (117)

• People Power (106) • People Power (106)

• Justice (6) • Justice (6)

• People (3) • People (3)

• Basic Income (1) • Basic Income (1)

• Transition Korea (1) • Transition Korea (1)

Independent (6) Independent (6)

• Independent (5) • Independent (5)

Next election : 2024 Next election : 2024

• Speaker (1) • Speaker (1)

Vacant (5) Vacant (5)

• Vacant (5) • Vacant (5)

Best case for stock market Likely case for stock market

29Global market Valuation checking

MSCI ACWI earning yield value to growth

Value style cheaper

0.008

0.004

0

Growth style cheaper

-0.004

-0.008

The MSCI all-country earning yield index reflects the earning yield of value minus the earning yield of growth style, the pathway of index illustrates the growth

style has relatively higher earning in the short-term. The current market is showing the value style outperformed the growth style due to the uncertainty of

central bank tightening policy which directly impacts to discount rate in growth style stock. The earning yield advantages of the growth style and the

attractive valuation are opportunities to invest in this style in medium to long term to be exact is the 2H22.

30MSCI all country index sector breakdown

Current index EPS 2022 PE ratio Implied target index upside/downside Estimated profit margin

Financial *

Material

Consumer Discretionary

Real estate

Information technology

Communication services

Energy

Industrial

Consumer Staple

Healthcare

Utility

* Justify the PE ratio for the financial sector at the average 5 years

sset like a stock

market tend to support the return to the investment portfolio.

31S&P 500 still our the most favorite market for 1H22

S&P 500 target return tend to trade at premium due to higher Strong NPM compare to long term and last cycle of rate hike

NPM and ROE

16.00%

6000 13.51%

10Y avg NPM

5296.33 12.00%

9.36%

5000 8.24%

8.00%

2022 NPM

4000 4336.56 4.00%

0.00% 2015 NPM

3000 10Y avg NPM 2022 NPM 2015 NPM

2000

Strong ROE compare to long term and last cycle of rate hike

25.00% 22.47%

20.00%

10Y avg ROE

1000

14.29%

15.00% 12.26%

10.00% 2022 ROE

SP500 5.00%

Target S&P500 2022 with current P/E ratio 0.00% 2015 ROE

Target S&P500 2022 with avg 5y P/E ratio 10Y avg ROE 2022 ROE 2015 ROE

32&P 500 still our the most favorite market for 1H22

Recommendation

• The overall sectors in the U.S.

market still does not change from 1

month before, the earning growth

reflect the huge upside of the

market index.

• The U.S. market is outperform

against the other developed

countries because the potential

economic and business growth.

• The advantage sector in short-term:

Financial, Energy, and material

sectors

• Market risk: the uncertainty of

hawkish Fed has pressured the

market sentiment. Moreover, the

political budget and spending was

stuck in the parliament.

33STOXX 600 tend to relatively stronger than other markets due to low valuation

STOXX 600 target return tend to trade at premium due to higher Strong NPM compare to long term and last cycle of rate hike

NPM and ROE

12.00%

600 581.20 10.01%

10.00% 10Y avg NPM

550 8.00%

6.04% 5.68%

500 6.00%

2022 NPM

494.40 4.00%

450

2.00%

400 0.00% 2015 NPM

10Y avg NPM 2022 NPM 2015 NPM

350

Strong ROE compare to long term and last cycle of rate hike

300 12.00%

10.51%

10.00% 8.80%

250 8.49% 10Y avg ROE

8.00%

200 6.00%

2022 ROE

4.00%

STOXX600

2.00%

Target STOXX600 2022 with current P/E ratio

0.00% 2015 ROE

Target STOXX600 2022 with avg 5y P/E ratio 10Y avg ROE 2022 ROE 2015 ROE

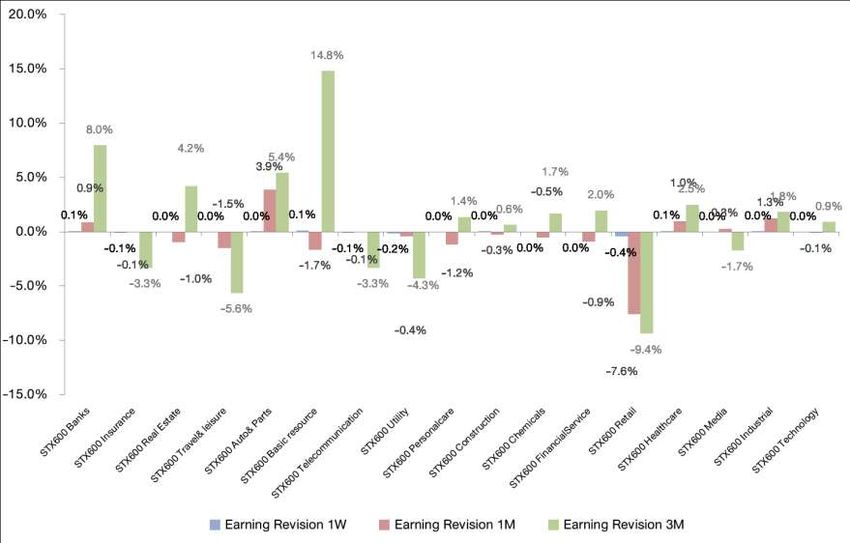

34Earning revision flavor cyclical sector

Recommendation

• The Europe stock market reflect the

cyclical sector upgraded earning

revision, the advantage sector in the

period of tightening monetary policy.

• Compared to the developed market,

the European stock market has

relatively benefit to economic status,

so we recommend the STOXX 600 in

the portfolio to gain a return.

• The advantage sector in short-term:

Financial, Automotive& parts, and

industrial sectors

• Market risk: the economic and

manufacturing situation is sensitively

to outlook of market earning and the

Covid-19 outbreak is closely

monitoring.

35Nikkei 225 still dragged by Korea stock market due to political shifting

Nikkei 225 target return tend to trade at premium due to higher Strong NPM compare to long term and last cycle of rate hike

NPM and ROE

10.00%

34000

7.66% 10Y avg NPM

8.00%

31000

6.00% 5.35% 5.02%

28023.50

28000 2022 NPM

4.00%

25000 2.00%

25581.85

22000 0.00% 2015 NPM

10Y avg NPM 2022 NPM 2015 NPM

19000

Strong ROE compare to long term and last cycle of rate hike

16.00%

16000

12.00% 11.09% 10Y avg ROE

13000 9.57% 9.70%

8.00%

2022 ROE

4.00%

Nikkei225

Target Nikkei225 2022 with current P/E ratio 0.00% 2015 ROE

Target Nikkei225 2022 with avg 5y P/E ratio 10Y avg ROE 2022 ROE 2015 ROE

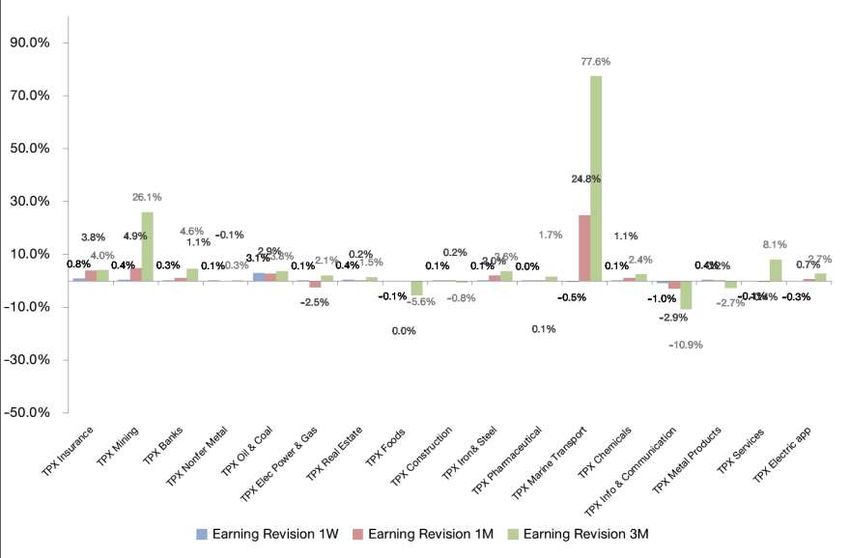

36Earning -term

Recommendation

• The Japanese stock market is

upgraded the earning revision across

the market, but the market does not

perform harmonize with their outlook.

• Compared to the developed market,

the Nikkei market has relatively

underperformed to other countries,

the currency volatility and the capital

flow ignored the risky assets.

• The advantage sector in short-term:

Financial, Electronic& semiconductors

, and industrial sectors

• Market risk: the Covid-19 outbreak is

getting worse due to the highest daily

cases and the policy support form the

new government still disappear.

37CSI 300 : The key for China is to raise more debt rather than a rate cut

CSI300 target return Strong NPM compare to long term and last cycle of rate hike

10.80

5,579.55 10.60

5,500.00 10Y avg NPM

10.40

5,177.97 10.20

5,000.00 10.00

9.80 2022 NPM

9.60

4,500.00

9.40

9.20

2015 NPM

4,000.00 9.00

8.80

10Y avg NPM 2022 NPM 2015 NPM

3,500.00

Lower ROE compare to long term and last cycle of rate hike

14.00

3,000.00 13.50

13.00 10Y avg ROE

2,500.00 12.50

12.00

11.50 2022 ROE

CSI 300 11.00

10.50

Target CSI300 2022 with current P/E ratio 10.00

2015 ROE

9.50

9.00

Target CSI300 with avg 5y P/E ratio

10Y avg ROE 2022 ROE 2015 ROE

As of 28 Jan 2022

38Earning revision : Series of earning downgrade slowdown

15.0%

China earning revision by sector

11.4%

Recommendation

10.0% • Since Chinese government has ramped

up regulations in various sectors such as

information technology, consumer

5.0% 3.1% 3.1% discretionary and finance (property)

3.0% 3.0% 3.6% 3.0%

2.4% sector, the earning of those sector has

1.2% 1.2%

0.9%

0.4% 0.6% not been upgraded yet.

0.0% 0.1%

0.0%

-0.1%

• Despite an intense policy from

-0.2% -0.4% -0.2% -0.4% -0.2%

government, China has step up

-1.8%

-2.3% monetary stimulus. If private sectors in

-3.9%

-5.0%

-5.2% -4.7% China owe more debt, it may be a better

-6.2% -5.8% sign due to low interest rate and D/E

-7.9%

-10.0%

• Market risk: A tightening monetary policy

still pressure china stock market.

-10.5%

Moreover, China regulator still strict with

-15.0%

CSI300 Finan CSI300 Indus CSI300 Cons CSI300 Info CSI300 Health CSI300 Cons Dis CSI300 CSI300 Utilit CSI300 Telecom CSI300 Energy

the zero-covid policy

Sta Tech Materials

Earning Revision 1W Earning Revision 1M Earning Revision 3M

As of 30 Dec 2021

39Review : China

11 6000

Recommendation

10 5000

• Lower Financial leverage

9 4000

minimize current China's ROE

8 3000 • Lower policy rate but business

7

Lower rate Rise in total debt Stock market perform more

2000

still aware of taking a loan

• Private sector did not take

6 1000

advantage from a lower

5 0 financing cost that much

• Easing monetary policy with

China 1 Y Lending rate cut Net profit margin Financial Leverage Total debt (RHS) last price(RHS) tightening policy from China

As of 28 Jan 2022

government is continuing,

Goldman Sachs China Regulation Barometer : Antitrust, Financial Markets, Data Security and Social Sector according to the China

Regulation Barometer from

Goldman Sachs still high

• Key Trigger : Less tightening

policy from regulator may

increase a business sentiment.

Source: Goldman Sachs

40KOSPI : good valuation but political risk headwinds

KOSPI target return tend to trade at premium due to higher NPM and ROE

Strong NPM compare to long term and last cycle of rate hike

4,237.15 8.00

7.00

10Y avg NPM

4,000.00

6.00

5.00

3,500.00 4.00 2022 NPM

3,132.87 3.00

2.00

3,000.00

2015 NPM

1.00

0.00

2,500.00 10Y avg NPM 2022 NPM 2015 NPM

Strong ROE compare to long term and last cycle of rate hike

9.00

2,000.00

8.50

10Y avg ROE

8.00

1,500.00 7.50

7.00 2022 ROE

KOSPI 6.50

6.00

Target KOSPI 2022 with current P/E ratio 5.50 2015 ROE

5.00

Target KOSPI with avg 5y P/E ratio 10Y avg ROE 2022 ROE 2015 ROE

As of 28 Jan 2022

41Earning revision : New economy upgrade

60.0% 57.2% Recommendation

50.0%

• Only some sectors in Korea has been

revised up due to a disappointed earning in

40.0% Q4 and a high EPS growth.

• Despite a remarkable valuation, Korea

30.0%

stock market still under pressure from a

19.9%

20.0% large size IPO which force institution

7.5%

8.9% investor to rebalance their portfolio.

10.0% 5.1% 7.8% 1.6%

0.7% 0.5% 0.1% 1.8% 2.0% 0.3% 0.5% Moreover, newly listed stock in Korea stock

1.0% 1.3% 0.9% 1.4% 0.0% -0.1% 0.1% 1.5% 0.1% -0.1% 0.1% 0.3%

0.0%

0.6% 0.3% 0.0% market tend to make Korea stock exchange

0.2% 0.1% 0.7% 0.0% -0.3% -0.1% -1.5% -0.2% -1.9% -0.6% -0.3% 0.3%

-4.5% -0.8% -3.0% -1.1% -4.0% has the highest implied equity duration

-10.0% -7.0% -3.9%

-3.4% compared to other countries in MXAPJ

-20.0% index.

• The advantage sector in short-term:

-30.0%

-29.5% Financial

-40.0%

-34.3% • Market risk: Korea stock market heavily

weight on information technology sector

which sensitive with the tightening

monetary policy. Fiscal policy is still no sign

As of 30 Dec 2021 Earning Revision 1W Earning Revision 1M Earning Revision 3M of support even the election is coming up.

42SENSEX does not price-in new fiscal policy yet

SENSEX target return Strong NPM compare to long term and last cycle of rate hike

16.00

65,000.00

14.00 10Y avg

59,468.70 12.00 NPM

60,000.00

10.00

57,742.65 2022 NPM

55,000.00 8.00

6.00

50,000.00

4.00

2015 NPM

2.00

45,000.00

0.00

10Y avg NPM 2022 NPM 2015 NPM

40,000.00

Lower ROE compare to long term and last cycle of rate hike

35,000.00

16.00

10Y avg

30,000.00 15.00

ROE

14.00

25,000.00

13.00 2022 ROE

SENSEX 12.00

11.00 2015 ROE

Target SENSEX 2022 with current P/E ratio

10.00

10Y avg ROE 2022 ROE 2015 ROE

Target SENSEX with avg 5y P/E ratio

As of 28 Jan 2022

43SENSEX does not price-in new fiscal policy yet

47.00

India's major expenditure at 22/23 Rajya Sabha (Upper house)

Unit: Billion USD

National Democratic Alliance (120)

31.20 United Progressive Alliance (55)

28.60 27.60 29.00 Others (62)

26.00

Vacant (8)

20.50

18.00 19.90

13.90

11.3012.50 10.70 11.60 10.20 Lok Sabha (Lower house)

10.00

6.50 6.90 6.20 7.30

5.00

National Democratic Alliance (327)

United Progressive Alliance (110)

Agriculture Education Health Rural Development Social Welfare Transport Urban Developmet

Others (111)

Vacant (1)

Source: Aljazeera, Government of India

LT ROE • There is a political stability since a ruling party dominate in both upper house and lower house.

Public investment •

government • Increment of an infrastructure spending may lead economist to revise up GDP growth in 2022 to

spending ST two-digits growth rate from an estimate of 8 to 8.5% GDP growth rate in 2022.

Public consumption

44Earning revision : More to be upgraded on new fiscal policies

2.5% Recommendation

• Earning of India stock exchange

2.0% 1.9% mostly revise up between April to

May.

1.5% • Compared to other emerging market,

India stock market become more

1.0% attractive in the aspect of fiscal policy

support and growth of India

0.5%

economy. Moreover, India has a high

chance to pass fiscal budget since

majority of India parliament consist of

0.0%

0.0% ruling party members.

• The advantage sector in short-term:

-0.5%

Materials, banking

-0.4%

• Market risk: A tightening monetary

-1.0%

policy from both internal central bank

SENSEX

and external central bank.

Earning Revision 1W Earning Revision 1M Earning Revision 3M

45SET index may need to focus on new election?

SET target return tend to trade at discount due to soft ROE Strong NPM compare to long term and last cycle of rate hike

7.60

1,900.00 7.40

1,854.27 10Y avg

7.20 NPM

1,800.00

7.00

6.80

1,700.00 2022 NPM

6.60

1,600.00

6.40

6.20

1,500.00 6.00 2015 NPM

5.80

1,400.00 5.60

1,387.40 10Y avg NPM 2022 NPM 2015 NPM

1,300.00

Lower ROE compare to long term and last cycle of rate hike

1,200.00 12.00

10.00 10Y avg

1,100.00

ROE

1,000.00

8.00

6.00 2022 ROE

SET 4.00

2.00 2015 ROE

Target SET 2022 with current P/E ratio

0.00

Target SET with avg 5y P/E ratio 10Y avg ROE 2022 ROE 2015 ROE

As of 28 Jan 2022

46Earning revision :

15.0%

Thai earning revision by sector

9.3%

Recommendation

10.0%

6.8% • Only some sectors in Thai stock

5.6% 5.0% 3.6% 4.3%

5.0% 3.6%

4.5%

2.4%

3.9% exchange has been revised up due to

1.2% 2.1%

0.3% -0.4% 1.4% 1.0%

0.5% -0.4%-1.1% 0.5% 0.0% 0.7% 0.1% 0.1% 0.0%

0.4% 0.6%

-0.1%

0.6% 0.0% a strong demand from foreign such

0.0% 0.1% 0.0%

-0.1% -0.5% 0.1% -0.1% -0.5% -1.1% -0.3% 0.0% 0.1% -0.1% -0.3%

-1.8% -0.4% as an electronic component sectors.

-1.6% 1.7%-3.0% -1.6% -1.5% -1.7% -1.6% -2.3%

-5.0% -3.5% -2.4% -3.7% • Compared to other emerging market,

-10.0% -7.6% -7.1% Thai stock market is less attractive in

the aspect of the EPS growth. While

-15.0% -13.7%

-14.0% the other emerging countries has two

-20.0% digits of EPS growth, Thai EPS

growth is negative.

-25.0% -23.9% • Market risk: A tightening monetary

-26.9%

-30.0% policy still pressure Thai stock

-35.0%

exchange whereas Thai economy is

-33.9%

not already for the domestic

-40.0% tightening policy. Moreover, Thailand

has a political instability.

As of 30 Dec 2021 Earning Revision 1W Earning Revision 1M Earning Revision 3M

47Stick to the plan : DM and value 1st then EM and growth later

Factors and KTBST

2021 YTD

Policies

Safehaven Safehaven

Asset Rotation

seeker seeker

Value for 1H

Style Rotation Growth Growth Blend Growth Growth Value Growth Blend Growth Growth Value

Growth for 2H

Country G-7 for 1H

Non-G7 Non-G7 G7 Non-G7 G7 Non-G7 Non-G7 Global G7+1 G7+1 G7

Rotation Non-G7 for 2H

DM EM DM EM DM EM EM EM DM EM DM DM for 1H

Regional play

Outperform outperform Outperform outperform Outperform outperform outperform outperform Outperform outperform Outperform EM for 2H

Most Asset Country Country Country Regional Country Regional Asset Style Style Style

Style Rotation

outperform Rotation Rotation Rotation Rotation play Rotation play Rotation Rotation Rotation Rotation

Aid

Fiscal policy Tax cut Trade war Trade war Aid package Infra plan

package

Tapering/Rate

Monetary policy QE QE Late QE Tapering Rate hike Rate hike Rate hike Rate hike Rate cut QE Late QE

hike

Source : KTBST

Tightening policy

Expansionary policy2022 Tactical Asset allocation summary

Current Asset preferrences Current Regional preferences Next 3 - 6 mths Regional preferences Thematic and Sector preferences

Slightly Overweight UW N OW UW N OW

Adv. Economies

Adv. Economies

Adv. Economies

DM DM Omicron uncertainties

US US Clean energy

DM

Equities

EU EU Growth disparities

JP JP Policy tightening

EM EM Valuation Laggard

Dev. Economies

Dev. Economies

Dev. Economies

CN CN Pre-reopening

KR KR EM Commodities exporter play

IN IN Omicron uncertainties

TH TH

Current Asset preferrences Current Regional preferences Next 3 - 6 mth Regional preferences Thematic and Sector preferences

Slightly Underweight UW N OW UW N OW

IG FI Govt. FI

IG FI Govt. FI

IG FI Govt. FI

DM DM DM FED's asset underweight

Incomes

EM EM EM FED's asset underweight

Fixed

DM DM DM n.m.

EM EM EM n.m.

DM DM DM Yield seeking

HY FI

HY FI

HY FI

EM EM EM Yield seeking

Current Asset preferrences Current Regional preferences Next 3 - 6 mth Regional preferences Thematic and Sector preferences

Underweight UW N OW UW N OW

Alternative Asset

Alternative Asset

Alternative Asset

Gold Gold Gold FED's asset underweight

Alternative

REIT REIT REIT Leisure and hospitality play

Assets

Global Global Global Leisure and hospitality play

US US US Open boarder reopening

TH TH TH Laggard play

MBS MBS MBS FED's asset underweight/Yield seeking

Current Asset preferrences Current Regional preferences Next 3 - 6 mth Regional preferences Thematic and Sector preferences

Overweight Cash Cash Cash Liquidity BufferTAA Market recommendation

Asset Class Selection Prev. New Comment

Q21

U.S. OW OW

Omicron

slightly overweight

Europe OW OW

KTBST

FOMC

Japan NT NT

regulatory risk Evergrande

Foreign Equity China NT NT

Omicron lockdown

Opinion poll

Korea NT NT

Omicron

India UW NT

% GDP

Other EMs UW UW BM Omicron

Thai Equity Thailand UW UW Omicron

TH Money

1 year Deposit OW OW Omicron Delta

Market

Government

UW UW DM EM QT

Bond

Fixed Income

High yield DM EM Tapering

Corporate Bond OW OW

Property/REIT NT NT Neutral FOMC REIT

FED

Alternative asset Gold UW UW

QT

THBUSD Hedge hedged .50 $ % Portfolio

50TAA playbooks

+1 +3 - 6 Key factors turning recommendation to

Asset Class Selection

Months Months

Strategy

Positive Negative

U.S. OW OW Value/blend Vaccine gen 2 - 3 Lockdown

Europe OW OW Value/blend Vaccine gen 2 - 3 Lockdown

Value,semiconductor , exporter

Japan NT OW Vaccine gen 2 - 3 Geopolitical

China NT OW EM mRNA vaccine/Antiviral medication Tradewar

Foreign

Equity

Opinion poll

Korea NT NT Earning upgrade No revision in EPS

Omicron

India NT OW Policy easing Omicron control

% GDP

Other EMs UW UW EM H22 mRNA vaccine/Antiviral medication Trade war

Thai Equity Thailand UW UW Selective buy" FDI EV Lockdown

TH Money 1 year

OW UW Omicron Delta

Market Deposit

Governmen

UW UW DM EM Gradually QT Hawkish policy

Fixed t Bond

Income Corporate High yield DM EM Tapering

OW NT Reopening NPL rising

Bond

Property/RE

NT NT Tapering policy FED Occ. Rate improvement Hawkish policy

IT

Alternative

asset FED

Gold UW UW US and russia tension Hawkish policy

THBUSD Hedge hedged Portfolio

51TAA Recommendation

Conservative Moderate Aggressive

Asset Class Selection Prev. New SAA TAA Change SAA TAA Change SAA TAA Change

Overall DM portion OW OW Conservative

U.S. OW OW ER = 5.38 %

Europe OW OW S.D = 3.45 %

Japan NT NT Var95 = -0.31%

Foreign Equity Overall EM portion UW UW Sharpe = 1.1253

China NT NT

Korea NT NT

India UW NT

Balance

Thailand UW UW

ER = 6.37 %

Liquidity 1 year Deposit OW OW S.D = 4.81 %

Government Bond UW UW Var95 = -1.58 %

DM UW UW Sharpe = 1.011

EM UW UW

Fixed Income

Corporate Bond OW OW

DM OW OW Growth

EM OW OW

ER = 8.27 %

Global REIT NT NT

Alternative asset S.D = 8.24 %

Gold UW UW

Var95 = -5.33 %

Sharpe = 0.8209

522020 : Tactical Asset Allocation Performance

Total Return (D) Total Return (P) Total Return (B)

50 TAA 2020 Performance as of 1 February 2022 3

40 2.5

30 2

20 1.5

10 1

0 0.5

-10 0

-20 -0.5

-30 -1

WTD Active return as of 1 February 2022 TAA Aggressive portfolio Performance as of 1 February 2022

35

Comments: Port BM 31.96 31.97

30

Our portfolio weekly

25

outperforms around 7 bps

20

from recovery in DM 15 12.57 13.44

equity asset after 10

correction for a whole 5

1.16 1.10

month of January. 0

Source: KTBST, Bloomberg as of 1 -5

-3.71 -3.14

-1.19 -0.84

-3.68 -2.86

Feb -10

WTD 3M 6M YTD 1Y SI

532020 TAA aggressive portfolio

0.0500 Selec Curr MTD Active return attribution as of 1 February 2022

0.0400

0.0300

0.0200

0.0100

-

(0.0100)

(0.0200)

(0.0300)

(0.0400)

(0.0500)

(0.0600)

TAA AGG 2020 CSI 300 TR EM USD Aggregate Global Aggregate Gold KOSPI INDEX MSCI EM GR MSCI WORLD GR Nikkei Total Return Idx S&P 500 Total Return S&P Global REIT USD TR STXE6 $GR

MTD return composition as of 1 February 2022 MTD Active return attribution as of 1 February 2022

54Appendix : Equity Market : U.S. Market

Source: Bloomberg as of 01/02/2022

55Appendix : Equity Market : Euro Market

Source: Bloomberg as of 01/02/2022

56Appendix : Equity Market : Japan Market

Source: Bloomberg as of 01/02/2022

57Appendix : Equity Market : China Market

Source: Bloomberg as of 01/02/2022

58Appendix : Equity Market : South Korea Market

Source: Bloomberg as of 01/02/2022

59Appendix : Equity Market : India Market

Source: Bloomberg as of 01/02/2022

60Appendix : Equity Market : Emerging Market

Source: Bloomberg as of 01/02/2022

61Appendix : Equity Market : Thailand Market

Source: Bloomberg as of 01/02/2022

62Appendix : Equity Market : Property fund and REITs

Thai REIT Singapore REIT

Japan REIT Global REIT

Source: Bloomberg as of /0 /2020

63Appendix : Volatility in Market

Source: Bloomberg as of /0 /2022

64Appendix : Volatility in Market

Source: Bloomberg as of /0 /2022

65Appendix : Global Price/Earnings Ratio Current

Growth

Bloomberg ticker fwd P/E 2021 EPS 2021 2022 2023

DJIA INDU 19.73 1855.92 3.52% 4.52% 10.00%

S&P500 SPX 24.75 209.98 15.14% 7.40% 9.49%

STOXX 600 SXXP 20.06 29.42 25.35% 5.83% 4.50%

Nikkei 225 NKY 15.83 1650.18 -5.93% 7.32% 6.41%

CSI300 SHSZ300 16.58 310.58 6.09% 16.61% 14.65%

Hang Seng HSI 9.56 2007.99 -19.05% 10.39% 13.64%

Nifty 50 NIFTY 25.12 743.41 8.28% 17.82% 14.79%

BSE SENSEX SENSEX 27.05 2341.37 9.33% 17.80% 15.84%

KOSPI KOSPI 13.65 214.98 28.53% -2.21% 11.18%

SET SET 19.08 85.76 3.05% 11.46% 12.10%

MSCI AC MXWD 20.79 39.28 12.68% 6.32% 8.46%

MSCI DM MXWO 22.18 158.61 13.93% 6.47% 8.10%

MSCI EM MXEF 14.04 93.38 6.90% 5.48% 10.40%

Source : Bloomberg, Fiscal year, as of 03/01/2022, Green = Increase in P/E , Red = Decrease in P/E

66Appendix : Global Manufacturing PMI Monitor

70

Global Manufacturing PMI

60

50

40

30

20

ISM US PMI Caixin China PMI Markit Euro PMI Nikkei Japan PMI

Markit Germany PMI JPMorgan Glabal PMI Nikkei India PMI Nikkei SK PMI

Markit UK PMI Markit Thai PMI Markit EM PMI

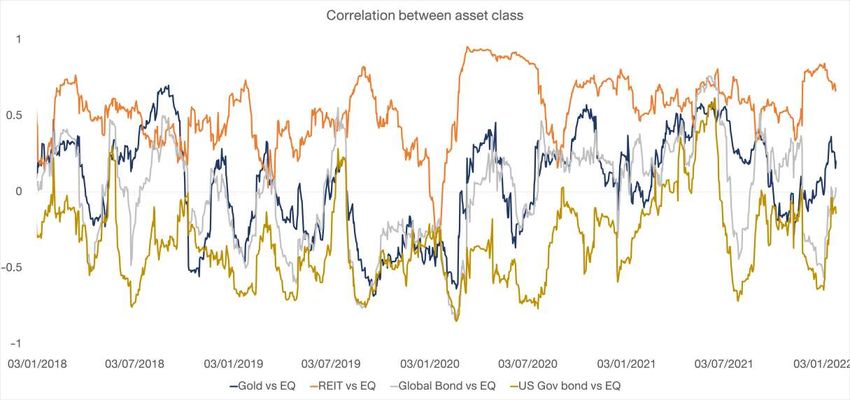

67Appendix : Correlation across asset

68•

•

•

•

•

•

•

•

69You can also read